Gummy Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

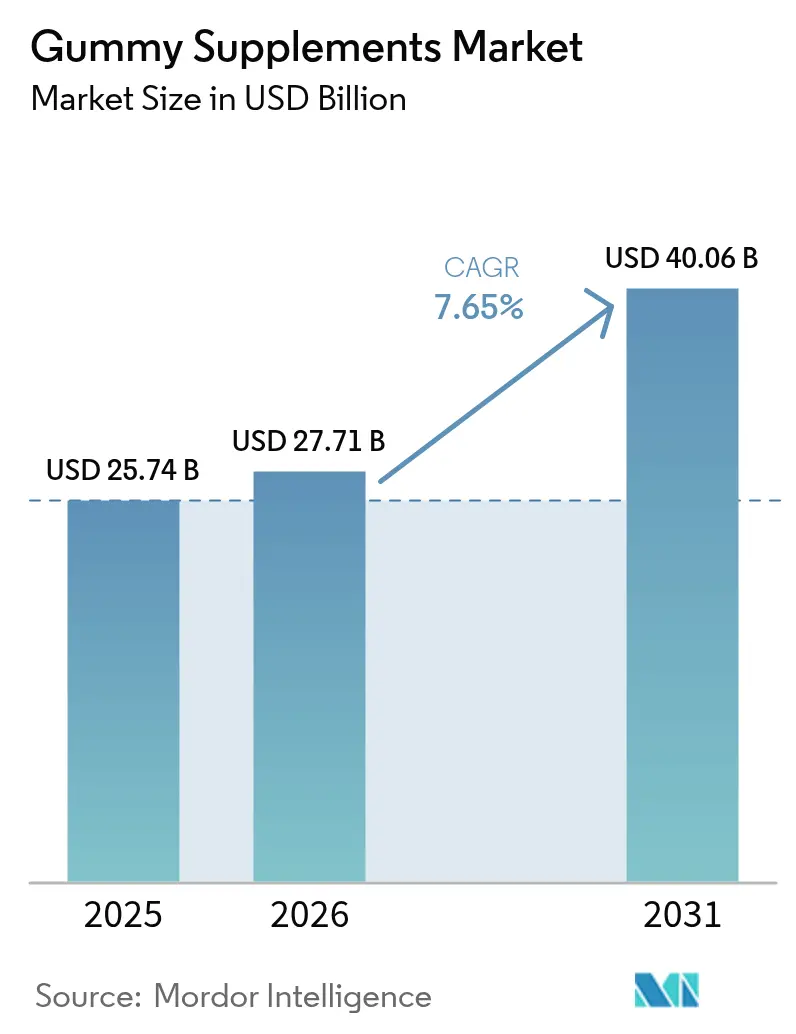

| Market Size (2026) | USD 27.71 Billion |

| Market Size (2031) | USD 40.06 Billion |

| Growth Rate (2026 - 2031) | 7.65% CAGR |

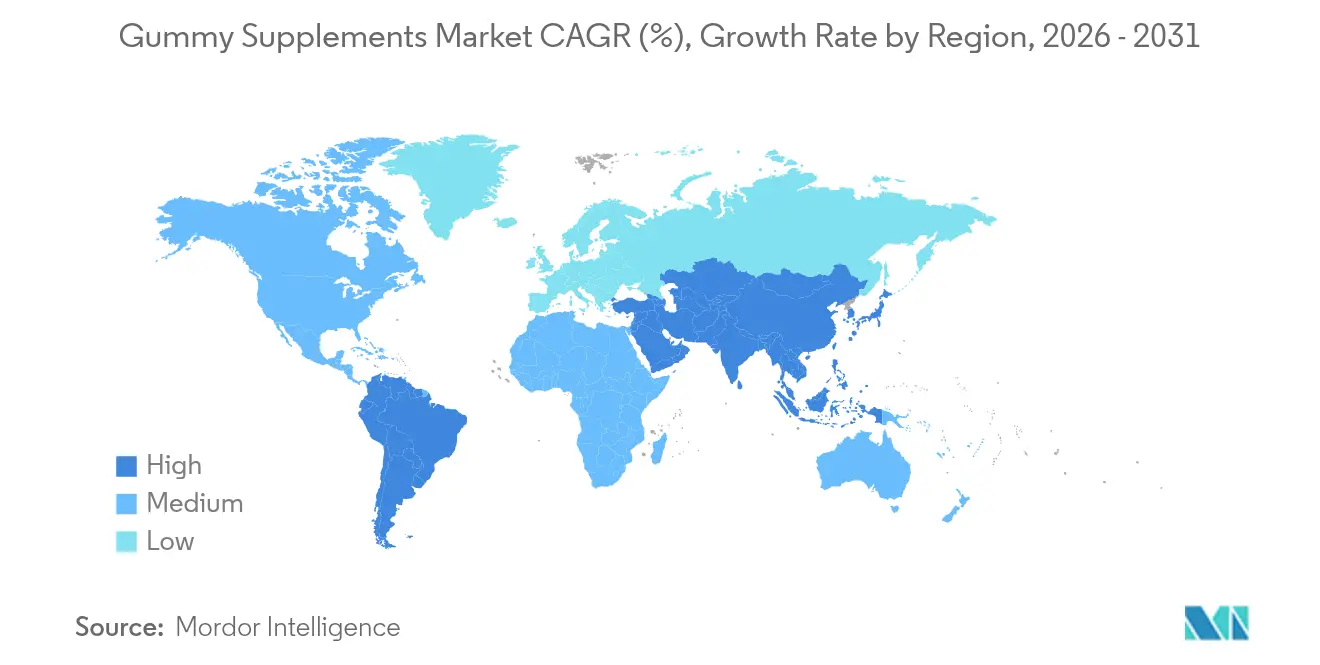

| Fastest Growing Market | South America |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gummy Supplements Market Analysis by Mordor Intelligence

The gummy supplements market size is expected to grow from USD 25.74 billion in 2025 to USD 27.71 billion in 2026 and is forecast to reach USD 40.06 billion by 2031 at 7.65% CAGR over 2026-2031. Consumers increasingly favor convenient and tasty delivery formats, streamlining their daily nutrient routines and aligning with a preventive health mindset. Multivitamin gummies dominate the market, with adults fueling the majority of demand. While pharmacies continue to lead in-store sales, e-commerce is rapidly gaining ground, especially as younger shoppers pivot to online health purchases. North America, bolstered by established regulatory frameworks, takes the lead regionally. However, South America is witnessing the fastest growth, driven by Brazil's burgeoning middle class and its robust food-processing sector. Ingredient innovations, particularly with pectin and plant-based gelling agents, are enhancing clean-label positioning, addressing challenges in texture and shelf stability. Meanwhile, a proposed inspection delegation in the U.S. could lead to inconsistent enforcement, favoring compliant firms while intensifying scrutiny on those lagging behind.

Key Report Takeaways

- By product type, multivitamin gummies held 41.78% of the gummy supplements market share in 2025, whereas probiotic gummies are projected to register an 8.11% CAGR through 2031.

- By end user, adults captured 65.10% of the gummy supplements market share in 2025; the children’s segment is on track for a 7.95% CAGR to 2031.

- By source type, animal-based held 62.88% of the gummy supplements market share in 2025, whereas plant-based is projected to register a 10.05% CAGR through 2031.

- By distribution channel, pharmacies controlled 40.62% share of the gummy supplements market size in 2025, while online retailers are set for a 8.96% CAGR through 2031.

- By packaging, bottles and jars captured 80.65% of the gummy supplements market share in 2025; the stand-up pouches are on track for a 8.88% CAGR to 2031.

- By Geography, North America led with 43.70% share of the gummy supplements market size in 2025, whereas South America is expected to expand at a 9.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gummy Supplements Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Convenience, taste, and palatability increase demand across all consumer segments | +2.1% | Global, with stronger adoption in North America and Europe | Medium term (2-4 years) |

| Rising adoption of women's health and prenatal gummy supplements | +1.8% | North America and Europe primary, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Market growth driven by CBD and cannabinoid-infused gummy supplements | +1.4% | North America dominant, selective European markets | Short term (≤ 2 years) |

| Diversification of supplement flavor profiles to meet consumer preferences | +1.2% | Global, with regional flavor preferences | Medium term (2-4 years) |

| Rising demand for plant-based and alternative gummy formulations | +1.7% | Europe and North America leading, Asia-Pacific emerging | Long term (≥ 4 years) |

| Functional gummies targeting specific health benefits are gaining traction among consumers. | +1.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Convenience, taste, and palatability increase demand across all consumer segments

Shifting consumer preferences toward enjoyable supplementation experiences are driving significant changes in market dynamics. This trend spans across age groups, with gummy formats addressing medication adherence issues among seniors who face challenges with traditional tablets, while also appealing to younger consumers seeking enhanced sensory experiences. The Seattle Gummy Company's approval of the first FDA Investigational New Drug Application for gummy medications signals potential market expansion from supplements to pharmaceuticals. Advancements in manufacturing, such as starch-free production methods, are improving operational efficiency and hygiene standards while enabling faster production cycles. These innovations support scalable operations to meet increasing demand. Companies that excel in balancing taste optimization with the delivery of functional ingredients are gaining sustainable competitive advantages. Reflecting confidence in the market's growth potential, firms like Pharmavite are making substantial investments in new gummy production facilities, highlighting the anticipated longevity of demand.

Rising adoption of women's health and prenatal gummy supplements

Targeted research into hormonal health, bone density, and prenatal nutrition is significantly driving innovation and expansion within the women’s formulations market. Supplements specifically designed for menopause management are demonstrating growth rates that exceed those of the broader category, highlighting a strong demand in this niche. Younger female consumers are increasingly emphasizing the importance of transparent product labeling and active community engagement, compelling brands to validate their claims through robust data and recognized certifications. The emergence of women-owned companies is further enriching the diversity of brand choices available in the market, while the incorporation of adaptogen blends is enhancing the functional positioning of products. Retailers are observing that strategies centered on education-driven merchandising and engaging digital storytelling are instrumental in fostering customer loyalty and driving repeat purchases. Additionally, certifications such as kosher, halal, and vegan are expanding market reach by appealing to previously underserved consumer groups, while simultaneously enhancing brand credibility and supporting premium pricing strategies.

Market growth driven by CBD and cannabinoid-infused gummy supplements

Regulatory frameworks continue to play a pivotal role in shaping the cannabinoid market. The FDA's issuance of warning letters concerning delta-8 THC gummies highlights a growing focus on safeguarding child safety and ensuring transparency in marketing practices. Concurrently, toxicology assessments conducted in Germany have determined that the evidence supporting the health benefits of CBD, even at safe consumption levels, remains inconclusive. This limitation restricts the scope of claims that can be legally approved, thereby influencing market dynamics. As regulatory authorities across jurisdictions establish clearer boundaries, compliant manufacturers have the opportunity to cater to a substantial and underserved market segment. Conversely, brands failing to meet compliance standards face significant risks, including product removal from the market. Moreover, adherence to Good Manufacturing Practices is expected to become a critical differentiator, enabling credible and reliable players to gain a competitive edge over opportunistic entrants in the industry.

Rising demand for plant-based and alternative gummy formulations

Millennials and Gen Z are increasingly adopting vegan, vegetarian, or flexitarian diets, driving demand for plant-based alternatives to traditional gelatin-based gummies. Consumers are also avoiding artificial colors, flavors, and preservatives, aligning with the clean-label movement. Plant-based gummies meet these demands and justify premium pricing by fostering trust. The market is seeing rising interest in gummies with botanical extracts, adaptogens, and superfoods like ashwagandha, elderberry, turmeric, and apple cider vinegar, targeting health areas such as immunity, sleep, mood, skin, and gut health. In North America, the growing demand for plant protein gummies reflects health-conscious dietary preferences. A 2023 National Institute of Health report notes animal protein consumption is below 60% in Peru, Chile, and Costa Rica [1]Source: National Institute of Health, "Contribution of Proteins to the Latin American Diet", www.pmc.ncbi.nlm.nih. As consumers prioritize health, ethics, and transparency, brands innovating with plant-based formulations gain advantages in market share, loyalty, and pricing power.

Restraints Impact Analysis*

| RESTRINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Added-sugar concerns driving negative media and regulatory scrutiny | -1.3% | Global, with stricter European regulations | Medium term (2-4 years) |

| Regulatory framework and growing consumer ingredient consciousness | -0.9% | North America and Europe primary, expanding globally | Long term (≥ 4 years) |

| Rising pectin and vegan-gelling input costs compressing margins | -1.1% | Global supply chain impact | Short term (≤ 2 years) |

| Counterfeits and mislabeling hinders growth | -0.8% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Added-sugar concerns driving negative media & regulatory scrutiny

Health concerns and stricter regulations on sugar consumption are driving the need for advanced ingredient technologies to reduce sugar while maintaining taste. The German Federal Institute for Risk Assessment has updated guidelines, capping allowable levels of vitamins and minerals in food supplements to curb excessive nutrient intake and address sugar-related issues. Rising demand for sugar-free gummy formulations reflects consumer acceptance of alternative sweeteners that preserve taste. This trend is supported by increasing diabetes prevalence; in 2024, the International Diabetes Federation reported 589 million adults aged 20-79 living with diabetes, often linked to high sugar intake [2]Source: International Diabetes Federation, "Facts and figures", www.idf.org. Regulatory frameworks now emphasize front-of-pack labeling, highlighting nutritional content, and impacting high-sugar products. Manufacturers face the challenge of creating tasty, health-focused gummy supplements that justify premium pricing while meeting regulatory standards.

Regulatory framework and growing consumer ingredient consciousness

Established manufacturers with strong quality systems benefit from shifting regulatory frameworks, while smaller players face innovation challenges due to limited regulatory expertise. The FDA's proposed dietary supplement product listing aims to enhance transparency by requiring manufacturers to register products and ingredients, boosting consumer confidence despite challenges for non-compliant operators. In the EU, Directive 2002/46/EC seeks regulatory harmonization, though botanical ingredient rules remain inconsistent across member states. Rising consumer demand for transparency and clean-label formulations drives manufacturers to balance efficacy, simplicity, and cost efficiency. Third-party certifications and testing, while increasing compliance costs, are vital for building trust and differentiating premium brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Multivitamins Lead, Probiotics Accelerate

In 2025, multivitamin gummies led the gummy supplements market with a 41.78% share, driven by convenient daily dosages and diverse nutrients. Major pharmacy chains boosted sales, while private-label products on e-commerce platforms intensified price competition. Probiotic gummies, growing at a CAGR of 8.11% (2026-2031), are gaining popularity among consumers focused on gut health, immunity, and mood. As clinical research highlights the microbiome's importance, the probiotic gummy market is set to grow further. Single-nutrient products, like vitamin D gummies, address deficiency concerns and enable targeted upselling. Omega-3 gummies, using fruit flavors to mask the fish-oil taste, attract health-conscious consumers focused on heart health.

Investments in advanced formats, such as liquid-fill and layered gummies, are driving sensory differentiation and enabling premium pricing strategies. However, manufacturers face challenges in ensuring the stability of active ingredients while maintaining consistent product texture. Successfully addressing these challenges can enhance brand equity and improve profit margins. As the gummy supplements market evolves, products that combine robust scientific validation with appealing flavors are well-positioned to maintain shelf presence amid increasing competition.

By Source Type: Plant-Based Gains Ground

Animal-derived gelatin, valued for its cost-effectiveness and texture, dominates gummy bases with a 62.88% share. However, plant-based alternatives are rising, with a 10.05% CAGR (2026-2031), as ethical and sustainability concerns shape consumer choices. The growth of plant-based gummy supplements is supported by mainstream retailers introducing vegan sections. Since 2023, pectin adoption in new launches has doubled, driven by stable citrus peel supply agreements. Gellan and carrageenan enhance texture flexibility, enabling heat-stable SKUs for warmer regions. Companies excelling in plant-based gelling technologies are addressing potential declines in gelatin demand due to religious or vegan preferences. Vertical sourcing agreements protect businesses from raw material price volatility, which pressures smaller players during pectin price hikes. Cruelty-free and eco-friendly brands are gaining a competitive edge in the gummy supplements market.

Simultaneously, hybrid systems that combine minimal gelatin with plant polysaccharides are addressing processing challenges while advancing toward fully animal-free formulations. This strategy enables product line extensions without requiring significant capital investment in retooling. Consumer education initiatives highlighting pectin's fruit-based origin are alleviating concerns about unfamiliar ingredient names, facilitating smoother adoption. Ultimately, transparent sourcing practices and clearly communicated functional benefits are driving the most sustainable growth opportunities in the market.

By Packaging: Bottles Dominate, Pouches Gain Traction

Rigid bottles, accounting for 80.65% of unit sales, maintain shape integrity during extended shipments. Their wide mouths facilitate portion control, though they result in increased plastic usage. Stand-up pouches, boasting a 8.88% CAGR, minimize material consumption and shipping weight, aiding brands in achieving sustainability targets. The market for flexible packs in gummy supplements is poised for growth as resin suppliers roll out recyclable mono-material films. Zip closures allow resealing to preserve texture, while matte finishes provide a premium appearance on shelves. Designs for child-resistant pouches now align with bottle compliance standards, catering to cannabinoid and high-potency SKUs.

Brands are investigating paper-based laminates that promise reduced carbon footprints, but they face challenges with moisture ingress. In emerging markets, where gray imports are prevalent, tamper-evidence indicators and QR codes serve as authenticity markers to counteract counterfeiting. These packaging enhancements not only emphasize environmental responsibility but also bolster supply chain security, resonating with broader ESG reporting goals.

By End User: Adults Dominate, Children’s Uptake Climbs

In 2025, adults accounted for 65.10% of global consumption, primarily driven by the preference for self-managed preventive health routines and the convenience of gummies over pills. Millennials represent a key demographic, influenced by their fast-paced lifestyles and the effectiveness of digital marketing strategies. The children's segment, expanding at an 7.95% CAGR (2026-2031), benefits from strong parental demand for easy-to-administer nutrition solutions and child-friendly flavors. In the women's health category, prenatal gummies have gained prominence due to their folic acid and iron formulations, which address nausea commonly associated with tablets. Senior-specific formulations featuring vitamin K2 and calcium support bone health and cater to individuals with swallowing challenges.

Cross-generational marketing strategies, underpinned by age-specific research and development, enable precise customer targeting. Safety-focused product designs, such as child-resistant packaging and clear dosing instructions, enhance consumer trust. Subscription-based replenishment models drive consistent product usage while ensuring recurring revenue streams. These factors collectively reinforce the dominance of the adult segment while accelerating growth in the children's gummy supplements market.

By Distribution Channel: Online Retail Accelerates

In 2025, pharmacies and drug stores represented 40.62% of total sales, driven by pharmacist endorsements and strong consumer trust in product authenticity. Loyalty programs at these outlets further reinforce customer retention. Conversely, online retail is experiencing robust growth, with a 8.96% CAGR, supported by increasing mobile adoption and the convenience of home delivery. Direct-to-consumer platforms are enhancing customer engagement through compelling brand narratives and customized product bundles, driving higher customer lifetime value. As delivery times improve and cross-border shipment regulations advance, e-commerce is expected to capture a larger share of the gummy supplements market. Supermarkets continue to serve as key discovery channels for value-seeking consumers, while specialty health stores attract ingredient-conscious buyers with curated product offerings.

Regulatory directives to marketplace operators emphasize the accountability of e-tailers in ensuring compliance, prompting platforms to implement stricter vendor screening processes. Enhanced hygiene protocols in fulfillment centers are safeguarding product quality, particularly for heat-sensitive botanicals. Brands that effectively execute omnichannel merchandising strategies, aligning pack sizes, pricing models, and digital content, are achieving stronger sales performance across all distribution channels. Health stores are also aggressively partnering with branded gummy supplements to capture the growing demand in the market. For instance, in 2023, Power Gummies Junior was introduced through an exclusive partnership with Apollo 24/7, Online Pharmacy, aiming to provide parents with a convenient platform for top-notch health supplements for their children.

Geography Analysis

In 2025, North America accounted for 43.70% of the global market value, driven by stringent DSHEA regulations and a well-established culture of supplement consumption. Canada's market growth is supported by its aging population's increasing demand for joint and immune health products. In Mexico, the expanding middle class with greater purchasing power is fueling market expansion. Gummy supplements have achieved significant penetration in pharmacy channels across the region, supported by endorsements from healthcare professionals. Companies adhering to the updated FDA inspection protocols are positioned to gain a competitive edge in the evolving regulatory environment.

Europe represents a large but complex market. Germany, operating under Directive 2002/46/EC, is the second-largest supplement market in the region. Consumer preferences for sugar-reduced formulations are driving ongoing research and development efforts into alternative sweeteners. The gummy supplements segment faces fragmented regulations for botanicals, prompting multinational companies to adapt product labels for individual countries to expedite market entry. In Spain, the sizable aging population increasingly turns to gummy supplements as a convenient alternative for vitamin intake. The chewable format is particularly appealing to individuals with swallowing difficulties or dental issues. According to 2024 data from INE Spain, 9.93 million people in the country are aged 65 and above, contributing to the growth of the gummy supplements market .

South America is experiencing robust growth, with a projected CAGR of 9.02% through 2031. Retailers report strong consumer interest in beauty and energy gummies, reflecting the success of aspirational lifestyle marketing strategies. Argentina and Chile are key contributors, driven by rising health awareness and improving macroeconomic conditions. While local registration processes can be time-consuming, the growing demand presents lucrative opportunities for long-term investors. In the region's dynamic retail environment, packaging that emphasizes flavor and natural colors resonates strongly with consumers. The Asia-Pacific region offers diverse growth prospects. Japan's streamlined functional food regulations under the Foods with Function framework facilitate faster market entry for science-backed products. In China, stringent dual filing registration requirements pose challenges, but the vast wellness economy attracts global players willing to collaborate with local partners. In 2024, India's Food Safety and Standards Authority introduced updated labeling regulations that incentivize brands for transparent sourcing practices.

Regulatory Landscape

In the United States, gummy supplements are regulated as dietary supplements under DSHEA and the Federal Food, Drug, and Cosmetic Act, with manufacturing controls governed by dietary supplement CGMPs (21 CFR Part 111) and labeling requirements such as the Supplement Facts panel (21 CFR 101.36). In 2026, regulatory activity focused on tightening oversight and documentation. The Dietary Supplement Listing Act of 2026 (S.3677) was introduced to require manufacturers to list dietary supplements with the FDA, and the FDA also advanced a proposed information collection for CGMP recordkeeping requirements under Part 111 (with a July 20, 2026 public comment deadline) alongside a March 2026 public meeting on dietary supplement innovation and the adequacy of current pathways such as New Dietary Ingredient notifications.

In Europe, the framework includes Directive 2002/46/EC for food supplements, and formulation and claim strategies continue to depend on country-level interpretation for certain ingredient classes. In June 2026, the European Commission initiated a call for evidence to set Maximum Permitted Levels for vitamins and minerals in food supplements, which increases the need for formulation discipline in high-dose multivitamin gummies and tighter alignment between product development, substantiation, and local-market compliance. Across major markets, heightened attention to high-moisture, high-sugar formats has reinforced the need for documented allergen segregation, moisture control, and sanitation controls in gummy production, particularly for starch-molding operations.

Competitive Landscape

The gummy supplement market is fragmented, with multinational consumer health firms competing against focused supplement specialists. Due to several players and the dominance of local players in the market, the rivalry among the competitors is also moderate. The major players operating in the market include Unilever Plc, Nestle S.A., and Haleon Plc. The major players in the market are indulging in strategies, like product launches, mergers and acquisitions, expansions, and partnerships, to establish a strong consumer base and esteemed position in the market.

With expertise in the supplements segment, leading companies drive innovation and launch new products. Economies of scale and strong brand loyalty give them a competitive edge. Expanding product portfolios across categories strengthens their market position. Increased Research and Developments investments enhance taste, bioavailability, and functional benefits, meeting consumer demand for clean-label, plant-based, and sugar-free products. Many localize flavors and packaging to suit regional preferences, boosting penetration in emerging markets. Securing long-term supplier contracts and streamlining logistics helps manage input costs and ensure consistent product availability.

Start-ups are leveraging direct-to-consumer (DTC) channels and influencer collaborations to establish niches, particularly in the sleep and mood segments. Technology investments are directed toward starch-free mogul lines to reduce allergen cross-contact and improve production efficiency. Personalized nutrition is emerging as a key growth area, with algorithm-driven vitamin packs and DNA-based recommendations creating significant customer retention barriers. Increased FDA scrutiny on e-commerce listings favors brands that emphasize robust stability data and third-party audits. Supply chain resilience, especially for pectin and specialty flavors, is expected to play a critical role in managing gross-margin performance amid ongoing raw-material price volatility.

Gummy Supplements Industry Leaders

-

Unilever Plc

-

Nestle S.A

-

Hero Nutritionals LLC

-

Santa Cruz Nutritionals

-

Haleon Plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Manufacturing localization and scale-up are creating opportunities for contract manufacturers and vertically integrated brands that can meet tighter quality expectations for high-moisture gummy formats. The investment cycle points to growing capacity for starch-based production and related controls: Pharmavite opened a 225,000-square-foot gummy facility in New Albany, Ohio, with stated capacity of 3 billion gummies annually and infrastructure for additional lines, while ILS Gummies secured institutional backing in February 2026 to scale its 130,000-square-foot facility in McKinney, Texas. TopGum also expanded its industrial base by completing the acquisition of a New York gummy manufacturing site (up to USD 35 million) in May 2026, adding a U.S. platform for domestic customers.

Product and process opportunities are increasingly tied to compliance and technical performance, not only flavor innovation. FDA emphasis on CGMP controls and documented safety systems for gummies supports demand for automation, real-time monitoring, and environmental controls to manage mold, allergen, and foreign-material risks commonly associated with starch-molding. On the demand side, premiumization continues to show up in targeted functional positioning, including gut-health formats such as probiotic gummies and plant-based formulations using pectin and alternative gelling systems, where stability, sugar reduction, and clean-label constraints rely on specialized formulation know-how and validated manufacturing controls.

Recent Industry Developments

- April 2026: Unilever announced an agreement to acquire Gruns, a US-based greens supplement company with a strong position in gummy supplements. The acquisition strengthens Unilever's participation in the premium, daily-wellness gummy segment and adds a brand platform aligned to functional nutrition positioning. It also signals ongoing M&A interest in differentiated gummy formats rather than traditional pill-based supplements.

- October 2025: Haleon expanded its Bone Up campaign in China, reaching over 1,000 counties and cities to engage healthcare practitioners around bone health nutraceutical initiatives. The scale of practitioner-focused outreach supports demand creation for targeted condition-specific supplements and helps formalize education-driven selling in a market where trust and channel influence are important. It also highlights the role of China in branded nutraceutical portfolio building.

- December 2024: Santa Cruz Nutritionals completed an expansion in Sumter County, South Carolina following an USD 84 million investment, adding a 24,000-square-foot packaging and employee facility and a 120,000-square-foot warehouse and distribution center. The expansion increases packaging and logistics throughput for gummy products, improving lead times and supporting higher-volume retail programs. It also reinforces the US as a manufacturing and fulfillment hub for gummy supplements amid rising scrutiny on quality and traceability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue from gummy format dietary supplements sold for health and wellness use, counted at the point of sale across retail and online channels, and tracked in USD across major regions.

Scope exclusions: We exclude gummy confectionery without supplement positioning and products sold only as prescription medicines.

Segmentation Overview

-

By Product Type

- Single-Vitamin

- Multivitamin

- Probiotic

- Omega-3

- Collagen

- Other Product Types

-

By Source Type

- Animal-based

- Plant-based

-

By Packaging

- Bottles and Jars

- Stand-up Pouches

- Others

-

By End User

- Children

- Adults

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Pharmacies/Drug Stores

- Online Retailers

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- New Zealand

- Malaysia

- Singapore

- Philippines

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with aligning definitions and guardrails for what qualifies as a supplement gummy versus adjacent candy-like nutrition items. For this, we used public references such as the NIH Office of Dietary Supplements, the US FDA (dietary supplement labeling and GMP guidance), the European Food Safety Authority for ingredient opinions, and the World Customs Organization HS framework to interpret trade flows where relevant.

We then reviewed supporting signals that help explain demand and pricing, including national statistics releases, customs and import-export summaries, peer-reviewed nutrition journals for ingredient and dosage trends, and association publications on vitamins and nutraceuticals. Company annual reports, investor decks, and credible news were also used to track product launches, format shifts (gelatin versus pectin), and channel expansion, and selective paid subscriptions were used only for company financials, patent lookups, and shipment-level trade checks. The sources mentioned are illustrative rather than exhaustive, and many other references were consulted to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary inputs came from interviews and short surveys with category managers, contract manufacturers, ingredient suppliers, and distributors, who helped us validate what is selling, where it is selling, and how prices are moving. Since this is a global market, we ensured coverage across APAC, EMEA, and the Americas so regional differences in regulations, channel mix, and consumer usage could be reflected in the final assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 15% | APAC: 44% |

| Mid tier: 56% | Functional/Unit leaders: 41% | EMEA: 32% |

| Smaller Players: 18% | Managers: 44% | Americas: 24% |

Market-Sizing & Forecasting

We built the size using a top-down and bottom-up approach, where global supplement spending and region-level consumption patterns were first converted into a gummy-format demand pool, and then the output was checked with selective supplier and channel math. In practice, the top-down side relied on reconstructing the addressable pool by region using indicators like supplement penetration, online share for vitamins and wellness products, and gummy format adoption (especially in children and adult wellness use).

To keep the model realistic, we leaned on a small set of inputs that can be tracked consistently, such as average selling price bands by channel, mix shifts between multivitamin, single vitamin, and functional claims, the split between gelatin and plant-based gelling systems, and packaging choices that often change unit economics. Where direct bottom-up data was thin, we used sampled volume and ASP checks by region and then filled gaps using peer group logic that was reviewed with interviewees. For the forecast, scenario analysis was used to reflect how regulation tightness, clean-label reformulation pace, and e-commerce growth can change unit demand and price realization over time.

Data Validation & Update Cycle

Outputs were validated through cross-checks that link back to independent signals, such as region-wise supplement market direction, trade movements for key inputs, and documented channel growth trends, and then we looked for outliers that did not match real-world pricing or usage. When a variance appeared, assumptions were reviewed, and follow-up calls were triggered to confirm whether it was a true shift (for example, a sudden ASP change driven by reformulation) or just a data artifact.

Before sign-off, the model goes through multi-step internal reviews, where calculations, currency handling, and year-to-year movements are checked for consistency. Reports are refreshed annually, and interim updates are made when material events change demand or pricing, followed by a final pre-delivery pass so clients receive the latest view.

Mordor Intelligence's Global Gummy Supplements Market Size Versus Other Published Estimates

Published numbers for gummy supplements often do not match because groups define the product boundary differently and then apply different price and channel assumptions. The year selected as the anchor point, currency conversion timing, and how fast new formats are assumed to penetrate also push totals apart.

The table highlights a common split, which is whether the count includes only supplement-positioned gummies or also pulls in gummy vitamins sold as part of broader functional confectionery, and this changes the revenue base materially. It also matters if online prices are treated as net realized values or as listed prices, and if the forecast assumes steady premiumization or a more conservative normalization after recent demand spikes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 27.71 B (2026) | |

| Global Consultancy A | USD 25.10 B (2026) | Uses a narrower channel view that underweights e-commerce and specialty retail, and applies a slower price progression without separating plant-based and clean-label premium items. |

| Industry Association B | USD 30.40 B (2026) | Includes a wider set of gummy-format wellness products, including functional confectionery overlaps, and leans on listed prices that can overstate realized revenue in promotion-heavy markets. |

The table shows a tight but meaningful spread, and in Mordor Intelligence's model, revenue is counted only for products positioned and sold as dietary supplements, with channel-level ASP checks used to reduce inflation from list prices. With those scope and pricing steps stated clearly, the number remains traceable to repeatable inputs and practical checks.

Key Questions Answered in the Report

What is the current value of the gummy supplements market?

The gummy supplements market generated USD 27.71 billion in 2026 and is projected to grow to USD 40.06 billion by 2031 at a 7.65% CAGR.

Which product type leads sales?

Multivitamin gummies hold 41.78% share, making them the leading product segment in 2025.

Which region shows the fastest growth?

South America is forecast to post a 9.02% CAGR through 2031, the highest of any region.

Why are plant-based gummies gaining popularity?

Consumers seek sustainable, vegan options, and pectin now appears in majority of new launches, supporting cruelty-free positioning and clean labels.

Page last updated on: