Broaching Machine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.42 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Broaching Machine Market Analysis by Mordor Intelligence

The Broaching Machine market size is expected to grow from USD 1.08 billion in 2025 to USD 1.13 billion in 2026 and is forecast to reach USD 1.42 billion by 2031 at 4.62% CAGR over 2026-2031. Rising demand for sub-micron tolerances in electric-vehicle gearboxes, the rebound of commercial aviation production schedules, and defense localization mandates lift capital spending on advanced broach lines. Orders for horizontal and surface machines expand as factories pair legacy CNC cells with high-speed broaching units to compress takt times. Equipment-as-a-service subscriptions, remote diagnostics, and predictive-maintenance modules widen access for small and mid-sized suppliers that lack upfront capital. Labor scarcity and tungsten-carbide price swings weigh on profit margins, yet regional incentives for smart-factory retrofits maintain a supportive investment climate. Collectively, these elements sustain a steady, mid-single-digit growth path for the broaching machines market through 2030.

Key Report Takeaways

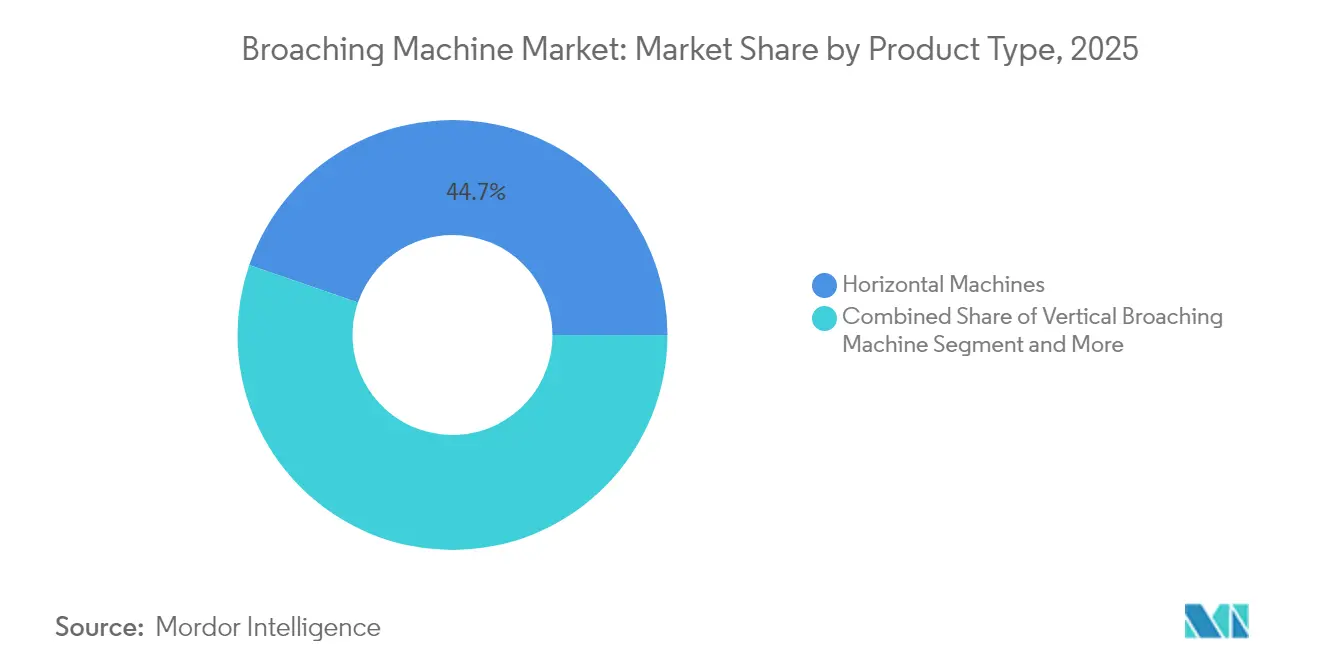

- By product type, horizontal machines held 44.72% revenue share in 2025; surface broaching is projected to expand at a 6.46% CAGR through 2031.

- By operation mode, the semi-automatic segment accounted for 52.98% of the broaching machines market share in 2025, while fully automatic systems are forecast to grow at a 7.12% CAGR to 2031.

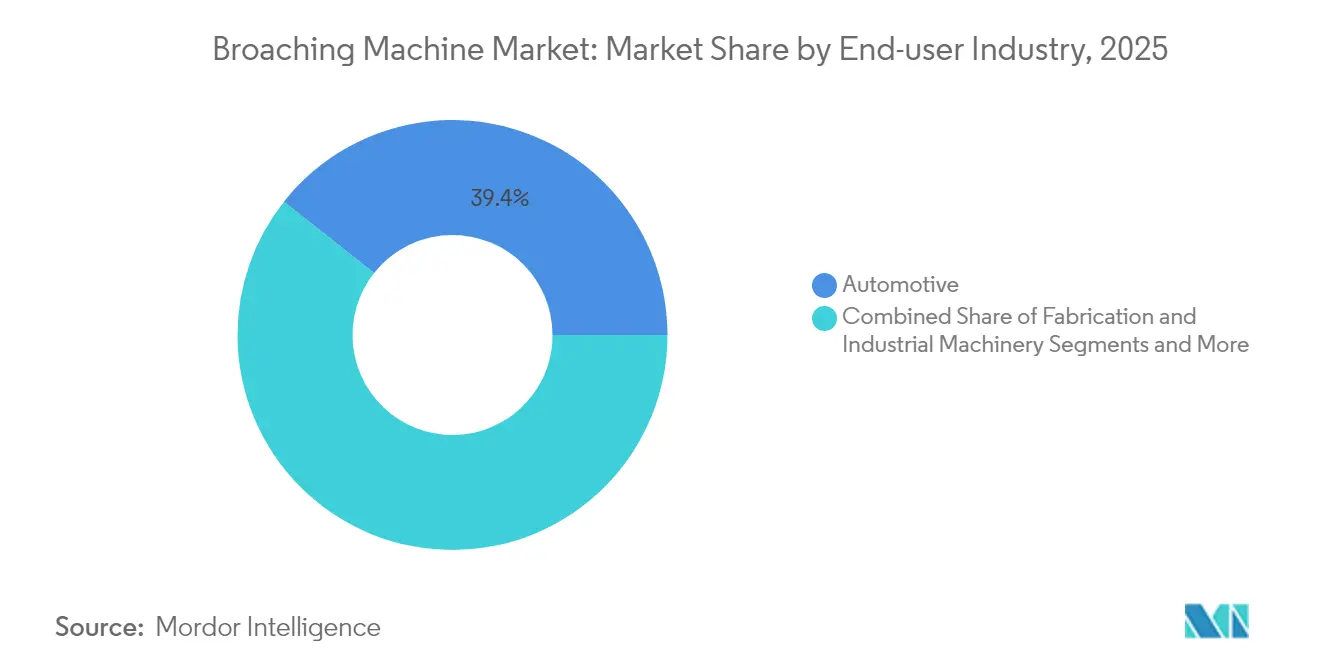

- By end-user industry, automotive contributed 39.35% of the broaching machines market size in 2025; medical devices are slated to register a 6.85% CAGR from 2026-2031.

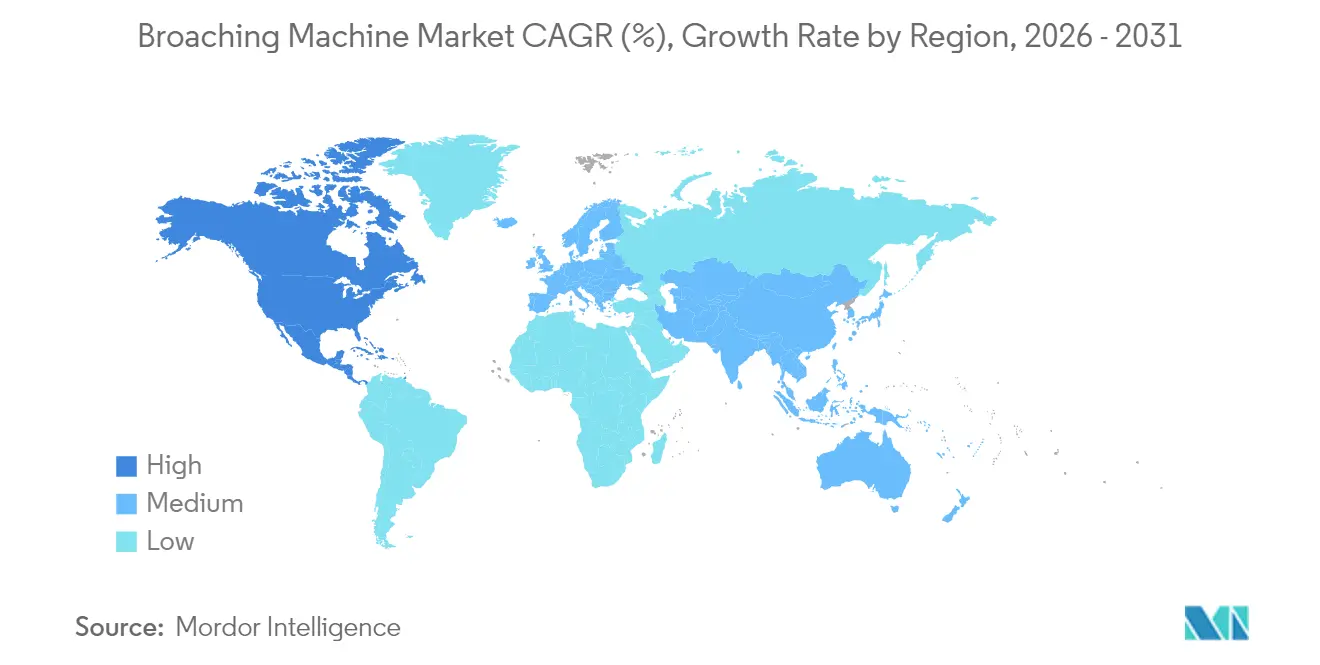

- By geography, Asia-Pacific captured 55.22% of global revenue in 2025, whereas North America is expected to post the fastest 6.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Broaching Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Precision-Machined EV Power-train Components (Asia) | +1.2% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Aggressive Automation Retrofits in Chinese Tier-2 Job-Shops | +0.9% | China, with technology transfer to ASEAN | Medium term (2-4 years) |

| Revival of Commercial Aerospace Build-Rates (North America & Europe) | +0.8% | North America & Europe | Short term (≤ 2 years) |

| OEM Shift from Hobbing to Rotary-Table Broaching for High-Mix Gearboxes | +0.7% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Defence Offset Mandates Fueling Local Gear-Hob & Broach Demand (Middle East) | +0.6% | Middle East, with expansion to emerging markets | Long term (≥ 4 years) |

| Rapid Tooling-as-a-Service Models for Short-Run Prototyping | +0.5% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Precision-Machined EV Power-train Components (Asia)

Electric-vehicle gearboxes now require tooth accuracy of ±0.0005 inches, a tolerance level impractical for milling at scale. Chinese manufacturers leverage policy loans and tax credits to install horizontal broach cells with fully enclosed servo drives that hold dimensional drift below 2 microns for 20-hour runs. Integrated e-axle designs fold multiple gears, splines, and keyways into a single housing, pushing demand toward flexible broaching lines able to complete internal and surface cuts sequentially. Export contracts for Asia-manufactured e-power-trains into North American assembly plants reinforce capacity additions, amplifying the broaching machines market across both regions. As product life cycles compress, suppliers favor modular broach heads with quick-change guides that cut setup times by 40%, further entrenching technology adoption.

Aggressive Automation Retrofits in Chinese Tier-2 Job Shops

Beijing’s equipment-upgrade initiative seeks 25% real growth in machine-tool investment by 2027 and targets 75% numerical-control penetration across key processes. Provincial grant programs reimburse up to 30% of CNC broach-line spend for small and mid-sized firms[1]Ministry of Industry and Information Technology, “Notice on Promoting High-End Equipment Upgrading,” Government of China, gov.cn. Automation retrofits integrate robot loaders, vision-based datum checking, and closed-loop tool-wear sensors, enabling lights-out operation in high-mix environments. Pilot plants report 18% unit-cost savings and 32% scrap reduction, reinforcing repeat orders. Technology diffusion to ASEAN vendors follows, as Chinese tier-ones transfer production packages to regional partners, expanding the broaching machines market footprint across Southeast Asia.

Revival of Commercial Aerospace Build-Rates (North America & Europe)

Aircraft order backlogs exceeded 14,700 units in late-2024, prompting air-framers to raise monthly output targets. Landing-gear trunnions, engine-mount sockets, and titanium pylon-flange bosses all feature deep internal slots best produced on broaching equipment. Tier-one structures groups therefore add surface broach stations rated at 120 MPa cutting pressure, reducing cycle times by 30% versus ram-type machining. European subcontractors diversify into broaching to satisfy dual-sourcing mandates from air-framers, distributing new-machine demand across the Atlantic. Process-capability audits by aerospace primes increasingly require in-house broach capability, embedding the technology as a core fixture of supply-chain resilience.

Defence Offset Mandates Fueling Local Gear-Hob & Broach Demand (Middle East)

Kuwait enforces a 35% industrial-participation clause on defense imports, and Saudi Arabia targets 50% defense-spend localization by 2030 under Vision 2030. Program offices direct a share of offset funds to joint ventures that build gearboxes for armored vehicles and helicopter power-trains. These plants specify horizontal broach systems capable of processing 17-4 PH stainless, while regional tool-grind centers ensure sovereign sustainment. Because funding is tied to multi-year platform life cycles, broaching capacity additions in the Gulf are largely insulated from near-term commodity swings, granting the broaching machines market a long-dated revenue stream.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Broach-Skilled Toolmakers in EU & U.S. | -0.7% | Europe & North America | Long term (≥ 4 years) |

| Volatile Tungsten-Carbide Pricing Disrupting Broach Tool Supply | -0.4% | Global | Short term (≤ 2 years) |

| Cap-Ex Freeze at Oil-field Service Firms (2024-25) | -0.3% | Global, concentrated in North America & Middle East | Short term (≤ 2 years) |

| Import Tariffs on Japanese CNC Systems in India | -0.2% | India, with spillover effects in South Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Broach-Skilled Toolmakers in EU & U.S.

The manufacturing sector forecasts 2.1 million unfilled roles by 2030 as senior machinists retire[2]European Labour Authority, “Annual Report on Labour Shortages 2024,” ELA, ela.europa.eu. Broach-tool design demands expertise in rake-angle sequencing and shear-zone heat management, skills rarely covered in standard CNC curricula. Finland’s Tampere region reports machinist graduation rates at half replacement demand, mirroring shortages across Germany and the United States. Factories hesitate to install new broaching lines until apprenticeship pipelines improve. Vendors respond with mixed-reality simulators and cloud-based application support, yet the talent gap persists as a structural cap on throughput, limiting upside for the broaching machines market.

Volatile Tungsten-Carbide Pricing Disrupting Broach Tool Supply

China supplies more than 80% of global tungsten concentrate, exposing toolmakers to quarterly price swings above 20%. High-grade carbide billets account for up to 45% of broach tool cost, so a 15% price spike can neutralize maintenance budgets at mid-sized plants[3]U.S. Geological Survey, “Mineral Commodity Summary: Tungsten 2025,” USGS, usgs.gov. Geopolitical uncertainty and export quota adjustments complicate long-term procurement, while alternative cermet solutions lack wear resistance in high-load broach operations. Some aerospace primes now manage vendor-held stock to buffer shocks, but uneven surcharge pass-through still compresses margins, dampening capital expansion in the broaching machines market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Horizontal Machines Retain Scale Leadership

Horizontal models generated 44.72% of 2025 revenue, reflecting their dominance in drive-shaft and heavy-equipment lines where components exceed 1 m length. Built on cast-iron bases, modern units integrate dual-servo hydraulic drives that boost push forces to 300 kN without chatter. Surface broach systems, though smaller in unit shipments, post the fastest 6.46% CAGR as aerospace and orthopedic applications require fir-tree and bone-plate contours unachievable with grinding. The broaching machines market size for surface platforms is projected to climb from USD 223.7 million in 2026 to USD 306.1 million by 2031.Rotary-table attachments expand reach into high-mix gearbox shops. Mounted on standard CNC centers, they cut 10 times faster than milling while holding ±0.0005 inches. Quick-change guide packs enable programed switch-over in under 3 minutes, attractive for batch sizes below 200 pieces. The broaching machines industry continues to evolve toward hybrid vertical-horizontal frames that swap out heads for shaping or slotting, delivering a flexible cell capable of three distinct cutting processes without repositioning, thereby deepening equipment utilization.

By Operation Mode: Semi-Automatic Dominance Meets Rapid Automation

Semi-automatic systems accounted for 52.98% revenue in 2025, combining manual fixture loading with automated stroke cycles that suit moderate volumes. Plants appreciate the operator’s ability to intervene on first-article setup and unusual alloys, yet chronic absenteeism pushes management toward lights-out solutions. Fully automatic lines, forecast to grow at 7.12% CAGR, integrate robot loaders, barcode traceability, and adaptive tool-wear compensation, raising overall equipment effectiveness by 28% on medical-device pilot runs. The broaching machines market size for full-automation platforms is expected to rise from USD 428.6 million in 2026 to USD 604.8 million in 2031.Digital-twin models simulate force loads across the stroke, flagging thermal drift beyond 1 micron in real time. Predictive-maintenance modules schedule tool changes using vibration signatures, extending stick life by 15%. Though upfront investment is 35% higher than semi-automatic counterparts, labor savings and higher first-pass yield shorten payback to 2.8 years, accelerating adoption. The broaching machines industry now offers subscription models bundling equipment, software, and tool re-conditioning, transforming capex hurdles into opex commitments.

By End-user Industry: Automotive Volume Meets Medical Velocity

The automotive sector contributed 39.35% of 2025 revenue as multi-speed transmissions, differential gears, and electric-drive splines rely on broach finishes for spiroid and involute profiles. Hybrid-power-train adoption requires tighter stack-up tolerances, locking in baseline demand. At 6.85% CAGR, medical devices form the fastest-growing end-use, stimulated by FDA quality-system regulations that enforce full process validation and traceability. Orthopedic implants and surgical instruments demand burr-free internal slots and chamfers that broaching can deliver in a single pass.Aerospace and defense segments register steady growth as landing-gear trunnions, engine-mount brackets, and missile fins all feature complex internal pockets unsuitable for end-milling. Oil and gas stays subdued amid capital-discipline policies, yet valve manufacturers still specify broach lines for non-circular seat geometry. Electronics and precision components gain traction as 5G infrastructure and semiconductor-tooling parts move toward sub-100-micron features, broadening the broaching machines market across high-tech verticals.

Geography Analysis

Asia-Pacific retained 55.22% global share in 2025, buoyed by China’s 25% equipment-investment growth target through 2027. Chinese OEMs integrate broach lines into intelligent-manufacturing cells under the “Made in China 2025” strategy, while Japan upgrades long-stroke machines for precision machinery exports. South Korea and ASEAN nations invest in semiconductor and automotive supply chains, spurring incremental demand. India contributes fresh orders via defense-offset gear-train plants, though import tariffs on Japanese CNC systems raise cost hurdles.

North America is projected to post the fastest 6.94% CAGR to 2031 as US air-frame build-rates rebound and defense programs expand. Reshoring policies funnel grants toward small machine shops that add broaching to shorten component lead times. Canada benefits from Pratt & Whitney turbofan offsets and mining-truck component demand, while Mexico’s Bajío corridor hosts new propulsion and aerospace machining centers. The broaching machines market size for North America is estimated to climb from USD 185.7 million in 2026 to USD 259.8 million in 2031.

Europe maintains stable growth as Germany’s automotive supply chain refreshes horizontal broach capacity, and the United Kingdom accelerates aerospace tooling upgrades. France and Italy renew equipment under energy-efficiency tax credits, and Nordic plants leverage automation to offset labor scarcity. Skilled-worker shortages remain a limiting factor, with 367 occupations flagged as in deficit across the EU in 2024. Nonetheless, vendor managed-services and virtual training mitigate bottlenecks, sustaining a modest yet predictable expansion of the broaching machines market.

Regulatory Landscape

Broaching machines sold into the EU fall under the Machinery Regulation (EU) 2023/1230, which tightens requirements for documentation and safety measures tied to risk assessment for industrial machinery. For performance and verification, ISO measurement standards used in broaching-machine acceptance and accuracy checks, including ISO 6779:2023 for vertical internal broaching, ISO 19744:2020 for NC vertical surface broaching, and ISO 6480:2019 for horizontal internal broaching, set technical baselines that show up in buyer specifications and factory-acceptance testing.

Trade policy also affects delivered equipment costs in key importing markets. In the United States, USTR tariff-exclusion procedures for machinery used in domestic manufacturing, referenced in late-2024 Federal Register actions and subsequent USTR process guidance, can reduce tariff exposure for eligible industrial equipment. Separately, June 2026 U.S. action adjusting Section 232 tariff regimes for aluminum, steel, and copper derivative products introduced modified duty treatment through December 31, 2027, which acts as an input-cost and pricing variable for machine builders and buyers budgeting for broach lines and other metal-intensive assemblies.

Value Chain Analysis

The value chain begins with upstream inputs such as specialty steels and precision castings for machine frames, CNC and servo control components, and wear materials, with tungsten carbide acting as a key cost driver for broach tooling. These tooling economics and availability flow into machine utilization, where carbide price volatility and supply concentration, including China’s dominance in tungsten concentrate supply, can squeeze maintenance budgets. Where bespoke broach tools carry 8 to 12 week lead times, new-part industrialization cycles extend and commissioning timelines can slip in high-mix programs.

Midstream, broaching-machine OEMs and integrators build complete systems around hydraulic and increasingly servo-driven or electromechanical drive platforms, then layer in automation such as robot loading, closed-loop sensing, and remote diagnostics. Downstream, distribution and value capture increasingly sit with application engineering, commissioning, and recurring services, including tool reconditioning, coatings, and uptime contracts, which also help address the broach-skilled toolmaker shortage highlighted for Europe and North America. End users in automotive, aerospace and defense, electronics and precision components, and medical devices pull demand based on tolerance, traceability, and cycle-time requirements, while local service hubs near manufacturing clusters support faster turnaround for regrind and repair.

Competitive Landscape

The market shows moderate concentration. Mitsubishi Heavy Industries reported FY 2024 revenue of JPY 5,027.1 billion, a 7.9% year-on-year increase, with 35.6% business-profit growth attributed to precision-manufacturing and smart-factory projects. Top players differentiate through servo-hydraulic drives that cut cycle times by 15%, integrated tool-life analytics, and cloud dashboards that visualize real-time overall equipment effectiveness.

Strategic playbooks emphasize vertical integration and recurring-revenue models. Several OEMs now market equipment-as-a-service contracts bundling machines, software, and scheduled tool re-sharpening. Patent filings highlight adaptive clamping, edge-force monitoring, and machine-learning driven parameter optimization. Rotary broach attachments for CNC centers represent a white-space that disruptors exploit, offering lower entry cost for job shops that cannot justify standalone machines.

Service networks form a critical moat. Established providers operate tool-re-conditioning hubs within 48 hours’ reach of major aerospace and automotive clusters. Remote diagnostics cut on-site callouts by 60%, boosting uptime and reinforcing vendor loyalty. Market consolidation is probable as global suppliers acquire regional tool-sharpening firms to secure consumables flow. Together, these moves sustain a balanced yet competitive environment within the broaching machines market.

Broaching Machine Industry Leaders

American Broach & Machine Co

Axisco Precision Machinery Co., Ltd

Forst Technologie GmbH & Co. KG

Nachi-Fujikoshi Corp

Mitsubishi Heavy Industries, Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One opportunity area is the retrofit and replacement cycle toward servo-driven, CNC-controlled broaching platforms that support programmable stroke control, variable cutting speeds, and Industry 4.0 modules such as remote diagnostics and predictive maintenance. This aligns with the operational constraints emphasized in the market context, including labor scarcity and a shift toward lights-out operation, and it is reinforced by government-backed modernization efforts such as China’s equipment-upgrade initiative, which targets higher numerical-control penetration and includes provincial reimbursements for CNC broach-line spend. For suppliers, bundling machines with digital service layers and application support broadens reach beyond large OEMs to job shops that want lower upfront burden and faster ramp capability.

A second whitespace area involves supply-chain resilience around tooling and installed-base support. Volatile tungsten-carbide pricing and longer lead times for custom broach tools lift the value of vendor-managed tooling logistics, faster reconditioning cycles, and modular tool concepts that reduce delivery-time sensitivity. Forst Technologie’s MSE-Broach modular tool initiative and patent activity is one visible signal of this direction. On the demand side, broaching’s role in high-precision EV power-train components, including sub-micron gearbox features, and in aerospace structures with deep internal slots in high-strength alloys supports turnkey cell opportunities that combine broaching, metrology or traceability, and automation, particularly in Asia-Pacific where equipment-upgrade programs are explicit and in North America where reshoring-driven investments favor shorter lead times and more in-house capability.

Recent Industry Developments

- July 2026: Nachi-Fujikoshi Corp. revised its consolidated earnings guidance for the fiscal year ending November 30, 2026. The update reflected ongoing demand conditions across its industrial portfolio, and it reinforces the importance of automation and machine-tool related businesses that influence capital spending on precision metalworking equipment such as broaching systems.

- January 2026: Axisco Precision Machinery Co., Ltd. reported finalizing a repeat equipment order from an existing customer. Repeat orders point to follow-on capacity additions at end-user sites and can shorten sales cycles for broaching OEMs by leveraging proven applications and established service support.

- October 2025: Forst Technologie GmbH & Co. KG announced development work and a patent application for its MSE-Broach modular broaching tool concept. Standardized, reusable tool components target shorter delivery times and more flexible tooling logistics, which directly addresses bottlenecks created by custom tool lead times in high-mix production.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from new broaching machines sold to industrial users, where material is removed using a broach to create accurate internal or external profiles.

Scope exclusions: The sizing excludes used equipment resales, maintenance contracts, and standalone broaches or tooling accessories.

Segmentation Overview

- By Product Type

- Vertical Broaching Machines

- Horizontal Broaching Machines

- Surface Broaching Machines

- Others (Rotary, CNC Broaching, Hydraulic Broaching Machines)

- By Operation Mode

- Manual

- Semi-Automatic

- Fully Automatic

- By End-user Industry

- Automotive

- Fabrication & Industrial Machinery

- Aerospace & Defense

- Oil & Gas / Energy

- Construction Equipment

- Electronics & Precision Components

- Medical Devices

- Others (Agricultural Equipment, Firearms & Defense, etc.)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Peru

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Turkey

- Egypt

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

For the first cut of the model, we used public statistics and technical references that explain where broaching demand usually comes from and how machine-tool investment moves over time. Typical inputs include sources such as US Census Bureau manufacturing data, Eurostat industrial production series, UN Comtrade trade flows for machine tools, national customs tariff schedules, and technical papers in machining journals that clarify process adoption and productivity trends.

We also reviewed company annual reports, investor presentations, and press releases to understand product positioning and the order environment, and then to sanity check assumptions on pricing and replacement cycles. Where it supported consistency, we referenced paid subscriptions for company financials and intelligence, patent databases, and an import-export shipment-level database to verify trade directionality and timing. These desk sources are not exhaustive, and we used additional public references for cross-checks and clarification during the research process.

Primary Interviews and Surveys

Primary work focused on validating what is actually being purchased, how buyers compare vertical and horizontal systems, and what price bands are common by capacity and automation level. We spoke with machine-tool manufacturers, component suppliers, distributors, and end users across major manufacturing regions so gaps from public data could be filled and assumptions could be aligned to how orders are placed and spec'd.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 13% | APAC: 42% |

| Mid tier: 51% | Functional/Unit leaders: 35% | EMEA: 33% |

| Smaller Players: 15% | Managers: 52% | Americas: 25% |

Market-Sizing & Forecasting

Our sizing starts with a top-down build that reconstructs demand from machine-tool spending patterns and industrial production signals, and then narrows it down to broaching based on where tight-tolerance profile cutting is used in volume manufacturing. To keep the totals realistic, we corroborate with selective bottom-up approximations, such as sampled average selling price by machine class multiplied by estimated unit shipments, followed by channel checks with distributors and system integrators.

Key inputs used in the model include machine-tool output and investment cycles, automotive and industrial machinery production trends, trade flows of metalworking machinery, capacity additions in manufacturing hubs, and observed shifts toward automation-ready broaching systems. Forecasts were built using scenario analysis, where the base case was adjusted using expert views on order pipelines, utilization, and expected lead-time normalization. When bottom-up detail was not available for a country, we used proxy indicators like production intensity and import reliance, and then re-tested the assumptions in interviews before carrying them into the final totals.

Data Validation & Update Cycle

Outputs are checked against independent signals like machine-tool trade balances, manufacturing PMI direction, and reported capital expenditure trends, and then any outsized jumps are investigated before sign-off. If variance is high versus these external markers, we revisit key drivers such as pricing, unit mix, and regional demand allocation, and we re-contact selected experts to confirm whether a real market shift has occurred.

The work goes through multi-step analyst review so arithmetic, unit conversions, and time-series logic stay consistent across regions. Reports are refreshed annually, and interim updates are triggered when material events occur, such as sharp currency moves or sudden demand changes in major end-use industries. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Broaching Machines Market Size Compared With Other Published Estimates

Published market values for broaching machines can look far apart even when they refer to the same equipment, because the counted revenue line and the year used for pricing can differ. Differences also show up when one study expands into adjacent items like tooling or services, or when the regional mix is simplified.

The table points to a split mainly driven by what gets counted as machine revenue and how the time window is set. In Mordor Intelligence's model, only newly manufactured broaching machines are included at the point of original sale, with used resales and maintenance contracts excluded, which can widen the gap versus estimates that capture a different revenue pool.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.08 B (2025) | |

| Industry Research Publisher A | USD 0.47 B (2024) | Uses an earlier base year and appears to emphasize a narrower revenue pool tied closely to machine shipments, which can understate value when higher-spec automated systems are more common in the mix. |

| Industry Research Publisher B | USD 0.50 B (2025) | The scope description is less explicit on exclusions, and the time horizon and pricing basis can differ, which can shift results when currency timing and price progression are treated differently. |

Looking at the spread, the most practical takeaway is that scope and counting rules matter as much as the math. When machine-only revenue, pricing year, and regional allocation are clearly stated and then cross-checked with trade and production signals, the estimate becomes easier to reproduce and easier to use in planning discussions.

Key Questions Answered in the Report

What is the current size of the broaching machines market?

The broaching machines market was valued at USD 1.13 billion in 2026 and is forecast to grow to USD 1.42 billion by 2031.

Which region leads the broaching machines market?

Asia-Pacific holds the largest regional share at 55.22% of 2025 revenue, driven by substantial equipment-upgrade programs across China, Japan, and emerging ASEAN manufacturing hubs.

What factors are driving demand for broaching machines in electric-vehicle manufacturing?

EV gearboxes require sub-micron accuracy, internal splines, and keyways that broaching delivers more efficiently than milling, spurring investments in advanced broach cells.

How does the labor shortage affect the broaching machines market?

A shortage of skilled toolmakers, especially in Europe and North America, slows new-equipment adoption and pushes manufacturers toward higher automation and remote-support solutions.

Page last updated on: