Lathe Machines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.35 Billion |

| Market Size (2031) | USD 14.21 Billion |

| Growth Rate (2026 - 2031) | 2.86% CAGR |

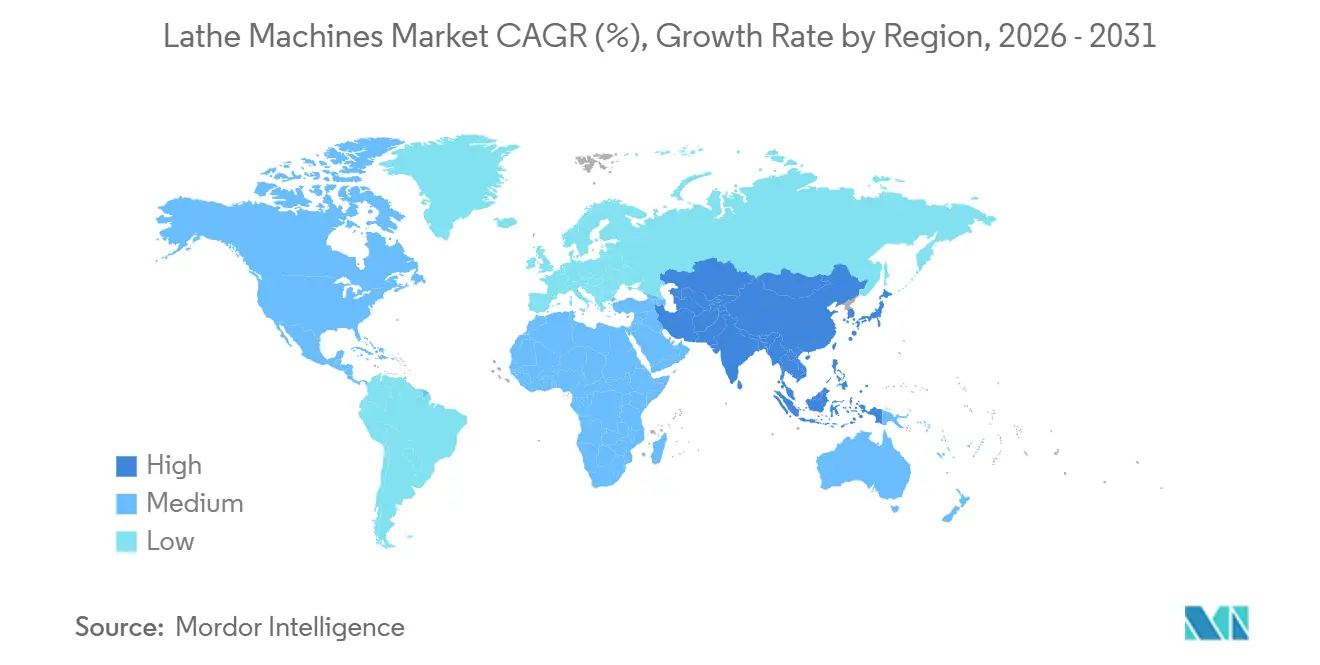

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lathe Machines Market Analysis by Mordor Intelligence

The Lathe Machines Market size is expected to grow from USD 11.76 billion in 2025 to USD 12.35 billion in 2026 and is forecast to reach USD 14.21 billion by 2031 at 2.86% CAGR over 2026-2031.

Demand is anchored by aerospace components, automotive powertrains, and precision medical hardware, where high repeatability and tight tolerances favor advanced turning platforms. Buyer priorities in 2026 center on uptime guarantees, remote diagnostics, and process integration that removes secondary operations across milling, grinding, and in-process measurement. Capital intensity and workforce scarcity remain the primary constraints, with the U.S. reporting 433,000 unfilled machining-related roles by early 2026, which limits throughput even when capacity is available. To counter these pressures, manufacturers are adopting AI-guided programming, modular automation cells, and digital twins, which shorten ramp times and improve first pass yield at a stable total cost of ownership. The lathe machines market is thus shaped less by uniform growth and more by selective investments in high-value applications, regulatory compliance, and localized service ecosystems.

Key Report Takeaways

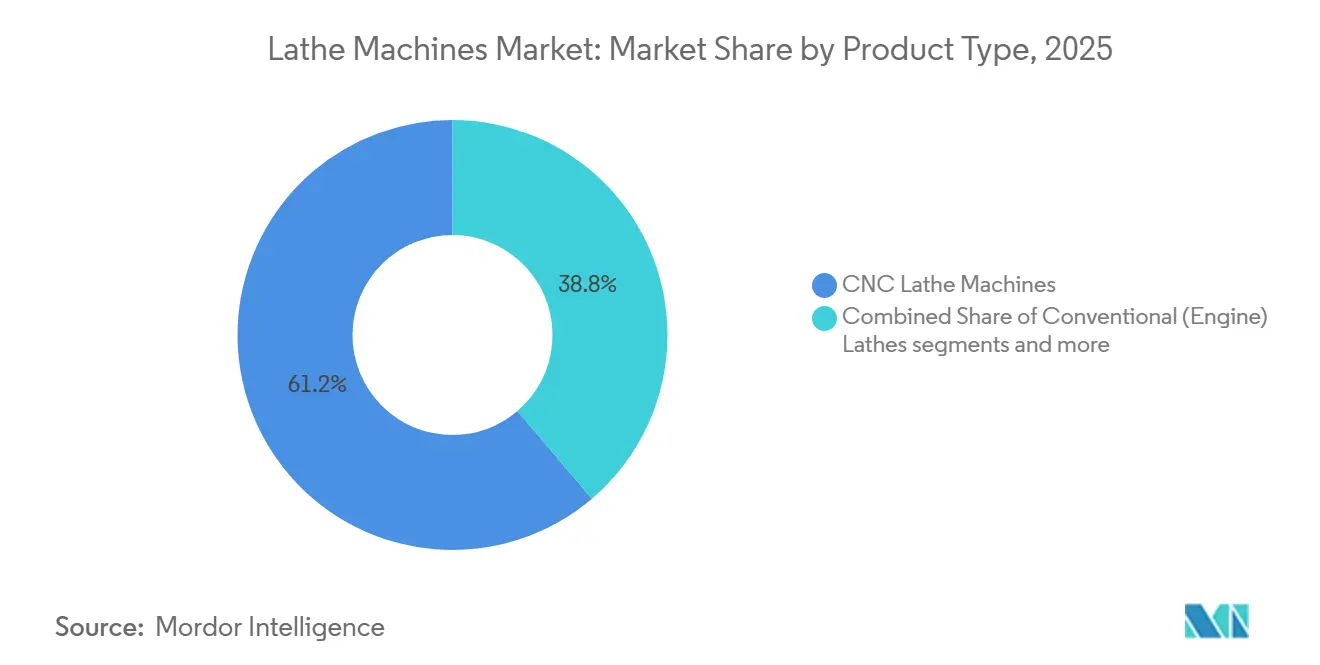

- By product type, CNC lathes led with 61.23% revenue share in 2025, while multi-spindle lathes are forecast to expand at a 6.23% CAGR through 2031.

- By machine configuration, horizontal lathes held 52.87% share in 2025, and multi-axis turning centers are projected to post a 5.41% CAGR through 2031.

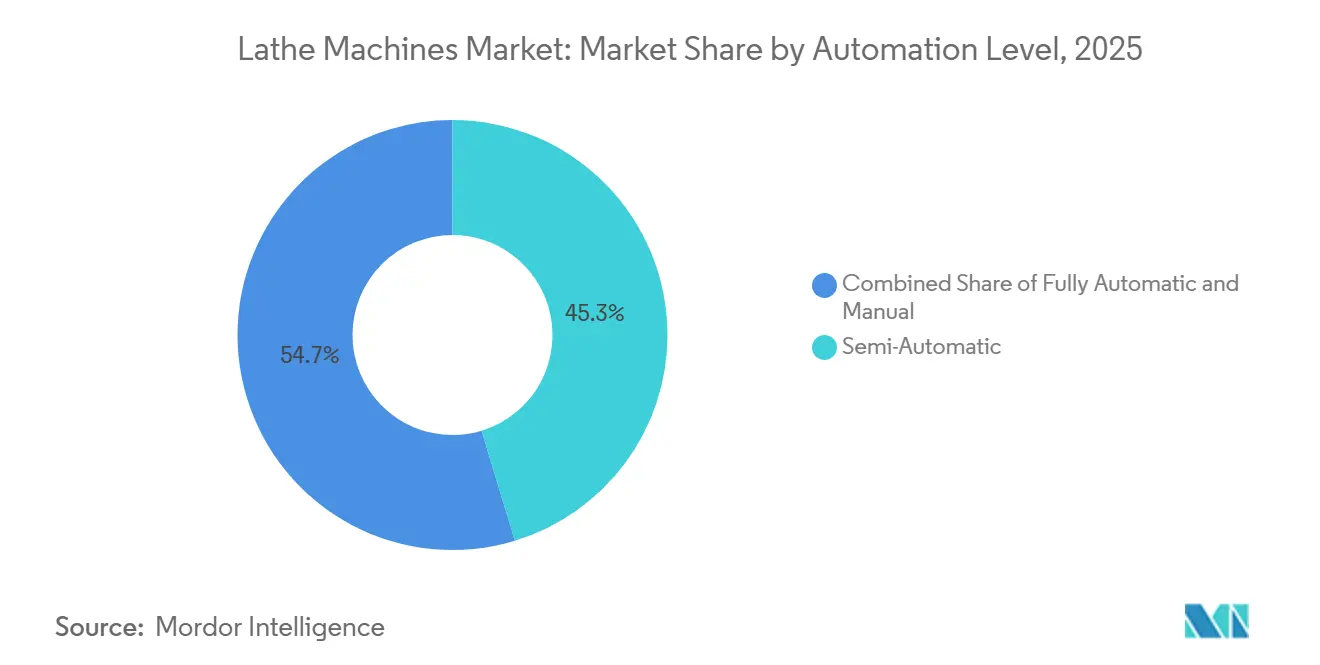

- By automation level, semi-automatic configurations accounted for 45.31% of the lathe machines market size in 2025, while fully automatic cells are expected to advance at a 5.87% CAGR through 2031.

- By end user industry, automotive applications represented 43.78% of deployments in 2025, while medical devices are projected to grow at a 6.67% CAGR through 2031.

- By geography, the Asia Pacific commanded 48.12% of the lathe machines market share in 2025 and is projected to grow at 6.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lathe Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing aerospace component manufacturing demand | +1.2% | Global, with concentration in North America, Europe, and emerging Asia‑Pacific hubs | Medium term (2-4 years) |

| Automotive industry demand for engine and transmission components | +0.9% | Global, led by Germany, the U.S., Japan, India, and China | Medium term (2-4 years) |

| Expansion of general engineering and job shop operations | +0.6% | Global, with regional intensity in North America and Europe | Long term (≥ 4 years) |

| Medical device manufacturing growth | +0.7% | North America and EU regulatory hubs, with rapid expansion in India and Costa Rica | Long term (≥ 4 years) |

| Oil and gas equipment manufacturing requirements | +0.4% | North America offshore, the Middle East, and select Asia‑Pacific markets | Long term (≥ 4 years) |

| Rising adoption of multi‑axis and turn‑mill centers | +0.8% | APAC cores of China, Japan, and South Korea, with spillover to North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Aerospace Component Manufacturing Demand

Aerospace demand is a structural tailwind for advanced turning platforms, supported by rising commercial aviation output, defense program modernization, and a growing space economy. Recent industry analysis highlights substantial growth potential through 2035, with commercial aviation taking the larger share and defense initiatives adding resilience across cycles. In the United Kingdom, long-horizon defense initiatives such as the Global Combat Air Program are expected to stimulate precision manufacturing and dual-use R&D that spills into civilian aerospace supply chains. Additive to subtractive hybrid workflows have become standard for many flight-critical parts, with EASA guidance underscoring machining as a required post-process to achieve certified interfaces and finishes.[1]European Union Aviation Safety Agency, “Supplemental Document to Certification Memorandum, Additive Manufacturing, CM-S-008 Issue 04,” EASA, easa.europa.eu These quality and certification norms reinforce demand for multi-axis lathes, turn mill centers, and integrated metrology that support zero defect execution at small batch sizes. Fiscal policies that improve capital allowances further catalyze upgrades to automation-ready, digitally enabled turning centers among aerospace suppliers in key markets.

Automotive Industry Demand for Engine and Transmission Components

Automotive powertrain machining remains a key use case for CNC and multi-spindle lathes, even as electrification reshapes component mixes. Germany produced 4.15 million passenger cars in 2025, which was a 2% year over year increase, though still below 2019 volumes, and early 2026 readings point to a near flat trajectory that keeps suppliers focused on productivity and complexity rather than volume alone. In the United States, motor vehicle assemblies averaged 10.18 million units in 2025, with light trucks comprising the bulk, which sustains heavy-duty turning for axles, crankshafts, and drivetrain housings.[2]Board of Governors of the Federal Reserve System, “Industrial Production and Capacity Utilization, G.17, Table 3,” Federal Reserve Board, federalreserve.gov EV architectures change the lathe workload by reducing multi-speed gear counts while adding new turning needs such as rotor shafts, single-speed gearbox housings, and thermal management components. These shifts favor flexible turn mill centers and 5-axis capable platforms with digital cycles that integrate gear cutting, measuring, and grinding in the same setup. As model cycles shorten and part variety rises, the lathe machines market benefits from capital that moves toward platforms able to absorb design churn without extending lead times.

Expansion of General Engineering and Job Shop Operations

Contract manufacturers and general engineering shops are expanding capabilities to meet reshoring, higher mix, and faster new product introductions. Manufacturers report persistent hiring gaps that push firms toward automation-ready equipment and digital workflows that reduce setup time and operator dependence over a sustained period. Policy signals and public-private initiatives prioritize workforce development and integrated factory technologies, which lift adoption of connected lathes that tie into robotics, process measurement, and scheduling systems.[3]M. Molnar et al., “Manufacturing USA Program Strategic Plan,” National Institute of Standards and Technology, nist.gov Federal initiatives that modernize skilled trade programs add a pipeline response that reinforces capital investment decisions across small and mid-sized shops. As OEMs push overflow work and rapid prototyping needs to their supplier base, job shops gravitate to multi-axis lathes and turn mill hybrids that eliminate secondary operations and consolidate quality checks in process. This favors premium equipment with robust application support and leaves the lathe machines market skewed toward platforms that convert labor bottlenecks into cycle time and yield gains.

Medical Device Manufacturing Growth

Medical device makers are increasing investments in advanced turning for implants, surgical instruments, and precision components that require biocompatible materials and sub-micron accuracy. Regulatory harmonization with ISO 13485 quality systems heightens expectations for process validation, traceability, and in-process inspection, which favors multi-axis and Swiss-type lathes that can complete parts in one setup. The move toward minimally invasive and robotic procedures drives smaller form factors and tighter tolerances, which further expands addressable demand for precision turning. Hybrid workflows that combine additive builds with CNC finishing are now common in orthopedic and dental applications, where accurate interfaces and threads are essential. These demands keep the lathe machines market aligned with micro machining, thermal stability, and in-cut measurement capabilities that enable reliable throughput at small batch sizes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extremely high capital investment for advanced CNC lathes | -0.6% | Global, with acute pressure in emerging markets and SMEs | Medium term (2-4 years) |

| Critical shortage of skilled lathe operators and CNC programmers | -0.9% | Most acute in North America and Europe, emerging in the Asia‑Pacific | Medium term (2-4 years) |

| Long lead times for custom machine configurations | -0.3% | Global OEM backlogs with emphasis on North America and Europe | Short term (≤ 2 years) |

| High tooling and maintenance cost structure | -0.4% | Global, concentrated in asset‑intensive sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extremely High Capital Investment for Advanced CNC Lathes

Capital intensity impedes adoption, especially for small and mid sized firms that face uneven order books and short payback thresholds. Entry level CNC turning can meet basic needs, yet regulated markets and high value parts push buyers toward premium multi axis platforms with linear drives, higher rigidity, and integrated measurement that raise acquisition costs. Tooling, workholding, integration, and validation add to the total cost of ownership, which complicates the business case when labor constraints reduce attainable utilization in the early ramp period. Supplier ecosystems that include application engineering and phased automation are now central to justify spend as shops scale from semi automatic to lights out cells. Published pricing ranges for advanced machining platforms illustrate the investment profile and reinforce the need for lifecycle ROI analysis that captures yield, uptime, and energy savings in addition to headline cycle time.

Critical Shortage of Skilled Lathe Operators and CNC Programmers

Persistent operator and programmer shortages cap throughput and delay equipment purchases. As of early 2026, U.S. manufacturing had 433,000 open roles, with machining and maintenance among the hardest to fill, which left capacity underutilized across many sites. Long training curves for multi axis programming and setup intensify the gap, while retirements add structural pressure on the skilled base through the decade. AI assisted toolpathing and digital work instructions are helping shorten learning cycles, but adoption is uneven across smaller firms that face budget and change management hurdles. As a result, some buyers postpone capital outlays until staffing stabilizes, which pushes a portion of latent demand into future periods. This bottleneck keeps the lathe machines market correlated with workforce policy progress and the scaling of training partnerships with OEMs and technical programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: CNC Dominance Amid Multi-Spindle Acceleration

CNC lathes held 61.23% of 2025, reflecting their versatility for prototypes, high mix batches, and regulated parts where process control is critical to qualified supply, and multi spindle platforms are projected to record a 6.23% CAGR as buyers chase cycle time reduction on complex rotational parts through parallel operations. Integration is the differentiator as advanced machines combine turning, milling, gear cutting, in cut measurement, and energy saving modes within a single setup to compress lead times for aerospace and medical components. Conventional engine lathes persist in repair and maintenance, while vertical turret lathes serve large diameter, short length work in energy and heavy equipment. Special purpose lathes address outlier geometries and regulated niches that can sustain customization premiums. The lathe machines market favors platforms that can remove secondary steps because workforce scarcity elevates the value of process elimination in addition to raw metal removal rate.

The category lines are also blurring as turn mill hybrids present a single workholding path to final geometry and reduce handling risks tied to multiple fixtures. This shift aligns with validated manufacturing in regulated sectors, where traceability and in process confirmation are now table stakes. Buyers prioritize lifecycle support and application expertise rather than peak spindle ratings alone. These demands help the lathe machine industry segment its offerings by capability clusters, which more closely mirror end user evaluations than traditional product labels. The result is continued share for CNC platforms and faster growth for multi spindle and hybrid systems that align with complex part families and shorter design cycles.

By Machine Configuration: Horizontal Lathes Lead, Multi-Axis Gains Momentum

Horizontal lathes accounted for 52.87% in 2025 on the strength of bar-fed production and compatibility with robotic loading, and multi-axis turning centers are forecast to grow at 5.41% CAGR as buyers consolidate operations for tighter tolerances and shorter queues. Vertical configurations remain essential for large diameter workpieces such as flanges, rotors, and turbine disks, where gravity-assisted stability and rigid workholding are critical. Swiss-type lathes are expanding beyond legacy niches to serve medical devices and precision fasteners where sub-thousandth tolerances and small form factors dominate. Digital cycles and thermal control additions are now standard expectations in the upper tier. As a result, the lathe machines market rewards platforms that can reliably hold tolerance bands through long unattended runs.

The configuration mix is shifting toward flexible and integrated systems because supplier roles have broadened to cover overflow capacity and rapid new product introduction support for OEMs. As part designs iterate faster, buyers require simulation, closed-loop measurement, and pre-built machining cycles that preserve quality while pushing throughput at stable energy draw. The lathe machine industry continues to move toward multi-axis solutions that accept volatility in part mix without giving up accuracy or spindle uptime. This tilt helps multi-axis solutions lift their share of the lathe machines market over the forecast period as digital adoption lowers historical programming barriers.

By Automation Level: Semi-Automatic Pragmatism Meets Fully Automatic Ambition

Semi-automatic lathes represented 45.31% in 2025, providing a balance of capital cost and flexibility for small batches and diverse part families, while fully automatic cells are projected to post a 5.87% CAGR as lights-out economics improve at moderate volumes. Semi-automatic platforms remain effective in MRO and custom jobs, where operator insight offsets lower repeatability. The scale advantage of fully automatic turning grows where quality systems require documented process control, in cut measurement, and stable thermal behavior, which improves yield and reduces rework. Automation-ready interfaces, digital twin simulation, and integrated inspection functions are becoming baseline in premium tiers. These features help the lathe machines market reach target cycle times with consistent outcomes even when staffing remains tight.

Adoption patterns vary by end use and local labor conditions, yet the trajectory favors higher autonomy as shop leaders focus on throughput stability. Total cost of ownership now includes downtime avoidance and faster changeovers in addition to headline cycle times, which shifts ROI calculations in favor of platforms with integrated metrology and reliable tool life monitoring. Lifecycle partnerships, including application engineering and training, are shaping purchase decisions alongside price and specs. The lathe machines industry is therefore bifurcating, with price-sensitive buyers relying on semi-automatic assets and precision-demanding segments scaling fully automatic cells with robust data capture.

By End-User Industry: Automotive Anchor, Medical Device Accelerator

Automotive applications held 43.78% of deployments in 2025, anchored by crankshafts, transmission shafts, axles, and steering components across internal combustion, hybrid, and electric programs, while medical devices are projected to expand at a 6.67% CAGR through 2031. Aerospace and defense, though smaller in unit counts, maintain high equipment value per cell because of traceability, qualification, and long-term agreements. General machinery and hydraulics provide a diversified baseline that is less cyclical but slower to adopt high-end automation features. Electronics and energy applications add smaller but rising demand streams as fasteners, connectors, and thermal management parts grow in volume. These mixes support the lathe machines market case for multi-axis capability and in-process verification.

The fastest growth path rests with regulated medical programs that value single setup completion, surface finish stability, and validated measurement over raw speed. Orthopedic and dental parts, along with surgical instruments, continue to move toward Swiss-type and micro-machining workflows where consistency at scale is critical. Aerospace parts maintain a premium tier that requires hybrid machining options and digital compliance artifacts tied to every workpiece. Oil and gas, rail, and heavy equipment add steady needs for heavy-duty capacity and robust spindle torque. Together, these patterns shape a lathe machines market in which end-use requirements determine not only the machines purchase but also the structure of the lifecycle service relationship.

Geography Analysis

Asia Pacific accounted for 48.12% in 2025 and is projected to grow at 6.91% through 2031, making it the regional engine of the lathe machines market, while diversified manufacturing and policy support reinforce capacity expansion across automotive, electronics, and aerospace suppliers. Japan and South Korea continue to export advanced multi-axis and hybrid solutions that set performance benchmarks, and domestic champions in India expand their portfolios to address reshoring and vendor diversification. Precision clusters in Southeast Asia add demand for bar-fed turning and small-form precision parts. The region’s balance of installed base and capability upgrades positions it to continue leading new equipment placements. As capital allocation follows electronics and mobility supply chains, the lathe machines market gains from the broader adoption of automation and digital workflows across APAC.

North America’s outlook is stable as automotive, aerospace, and medical supply chains prioritize higher value parts and lifecycle service depth. U.S. motor vehicle assemblies remained elevated in 2025, with a light truck skew that supports heavy-duty turning for drivetrain and chassis components. Public-private programs and policy modernization emphasize integrated factory technologies and workforce development, which raise the appeal of connected turning platforms and modular automation among small and mid-sized firms. Federal workforce initiatives aim to expand the skilled trade pipeline, which can unlock latent equipment demand as staffing constraints ease. These drivers keep the lathe machines market tied to capability upgrades that enhance utilization and compliance.

Europe retains a significant base anchored by automotive leaders, aerospace primes, and medical clusters. Germany produced 4.15 million passenger cars in 2025, which sustained core demand for powertrain machining even as electrification changes part requirements. The United Kingdom’s long-run defense program investment supports precision manufacturing ecosystems that ripple across civil aerospace suppliers and their machining partners. Italy and Spain maintain production strengths in heavy-duty and vertical turning, while the Nordics contribute niche capabilities in marine and energy parts. Across the rest of the world, industrialization agendas in the Middle East and selective expansions in South America provide incremental growth opportunities. Together, these trends support a lathe machines market where Europe emphasizes high-value segments and lifecycle support, while other regions drive volume placements.

Mordor Intelligence provides coverage of the lathe machines market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

The market is moderately concentrated around global OEMs with deep service networks, broad application libraries, and strong installed base loyalty. Differentiation is shifting from peak hardware specifications to digital capability, predictive maintenance, and integration that delivers quality and uptime at scale. OEM product lines now embed digital twin simulation, process-specific technology cycles, and energy-efficient modes that enable repeatable results in lights-out environments. Tier 1 aerospace and automotive suppliers continue to favor premium multi-axis and hybrid platforms for complex parts, while tier 2 and job shops balance capability and capital by adopting modular automation. This mix sets the stage for a lathe machines market where lifecycle partnerships and application engineering are decisive.

Strategic moves increasingly rely on partnerships and co-development with customers and universities. DMG MORI and the University of Tokyo formed the Machining Transformation Research Center to advance digital twins, process integration, and sustainability, linking academic research to industrial programs. Modig and Orizon established a major production cell that advances aerospace structural machining through co-investment and toolpath innovation, showing how OEM customer collaboration can lock in long term value. Nidec Machine Tool America partnered with Blaser Swisslube to integrate fluid and machine optimization, highlighting how ecosystems now target total cost and yield, not just machine cycle time. These examples reinforce a lathe machines market that prizes solution stacks over standalone assets.

Education partnerships and supplier expansions address the workforce bottleneck that constrains utilization. Matsuura’s collaboration with TITANS of CNC and YCM Alliance’s multi-year partnership with the same program expand hands on exposure to advanced platforms, which supports future adoption and brand familiarity. Z MaT’s university collaboration on fault diagnosis and prediction shows how software-first capabilities are diffusing across mid-market suppliers in Asia. Customer side upgrades, such as LASIT’s machining investments and ITA Nordic’s robotic cell expansion, also expand the installed base that consumes precision turning capacity. These moves orient the lathe machines market toward integrated ecosystems that reduce ramp times and spread best practices.

Lathe Machines Industry Leaders

DMG Mori Co., Ltd.

Yamazaki Mazak Corporation

Haas Automation, Inc.

Doosan Machine Tools Co., Ltd.

Dalian Machine Tool Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DMG MORI and The University of Tokyo established the Machining Transformation Research Center to advance machining science, digital twins, and sustainable production, funded through The University of Tokyo Fund.

- December 2025: Nidec Machine Tool America and Blaser Swisslube announced a strategic partnership to provide integrated, application driven solutions that optimize machine, tool, and fluid interactions for improved cycle times, tool life, and surface quality.

- November 2025: Modig Machine Tool and Orizon Aerostructures announced a strategic partnership implementing a large RigiMill cell with moving gantry and moving table machines for advanced aerospace structures, improving accuracy and reducing secondary operations.

- September 2025: DMG MORI launched its NHX 4th Generation horizontal machining centers and NLX 2500|1250 2nd Generation universal turning machines with shorter cycle times, energy reductions, and CELOS X integration aimed at aerospace, EV, semiconductor, and construction machinery applications.

Global Lathe Machines Market Report Scope

The Lathe Machines Market Report is Segmented by Product Type (CNC, Conventional, Multi-Spindle, Vertical Turret, Special-Purpose, Others), Machine Configuration (Horizontal, Vertical, Multi-Axis, Swiss-Type), Automation Level (Manual, Semi-Automatic, Fully Automatic), End-User Industry (Automotive, Aerospace, General Machinery, Electronics, Medical Devices, Oil & Gas, Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts in Value (USD Billion).

| CNC Lathe Machines |

| Conventional (Engine) Lathes |

| Multi-Spindle Lathes |

| Vertical Turret / Turning Lathes (VTLs) |

| Special-Purpose Lathes |

| Others - Capstan & Turret Lathes, Bench & Speed Lathes |

| Horizontal Lathes |

| Vertical Lathes |

| Multi-Axis Turning Centres |

| Swiss-Type / Sliding-Head Lathes |

| Manual |

| Semi-Automatic |

| Fully Automatic |

| Automotive |

| Aerospace & Defence |

| General Machinery Manufacturing |

| Electronics & Electrical |

| Medical Devices |

| Oil & Gas |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | CNC Lathe Machines | |

| Conventional (Engine) Lathes | ||

| Multi-Spindle Lathes | ||

| Vertical Turret / Turning Lathes (VTLs) | ||

| Special-Purpose Lathes | ||

| Others - Capstan & Turret Lathes, Bench & Speed Lathes | ||

| By Machine Configuration | Horizontal Lathes | |

| Vertical Lathes | ||

| Multi-Axis Turning Centres | ||

| Swiss-Type / Sliding-Head Lathes | ||

| By Automation Level | Manual | |

| Semi-Automatic | ||

| Fully Automatic | ||

| By End-User Industry | Automotive | |

| Aerospace & Defence | ||

| General Machinery Manufacturing | ||

| Electronics & Electrical | ||

| Medical Devices | ||

| Oil & Gas | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value and long term growth outlook for the lathe machines market?

The lathe machines market size is USD 12.35 billion in 2026 and is projected to reach USD 14.21 billion by 2031 at a 2.86% CAGR, supported by aerospace, automotive, and medical demand.

Which region leads global demand, and how fast is it growing?

Asia Pacific led with 48.12% in 2025 and is projected to grow at 6.91% through 2031, driven by diversified manufacturing and capability upgrades across key supply chains,

Which product and configuration segments are most influential in the next cycle?

CNC lathes hold the largest share at 61.23%, while multi spindle lathes post the fastest growth, and horizontal lathes lead configurations with multi axis centers growing fastest due to process integration needs.

How is the talent shortage affecting investment decisions in turning equipment?

Staffing gaps delay purchases and push buyers toward automation ready, digitally enabled lathes that raise utilization with fewer operators, a trend reinforced by public private workforce programs.

Which end uses are expanding fastest for precision turning?

Medical devices show the fastest trajectory on stricter quality requirements and smaller part geometries, while aerospace maintains a premium tier that values hybrid additive subtractive workflows and in process verification.

What differentiators matter most when selecting new lathes in 2026?

Buyers prioritize integrated processes, digital twin simulation, in cut measurement, and lifecycle service that deliver predictable uptime and quality in lights out environments.

Page last updated on: