Out-of-Home Coffee Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 43.31 Billion |

| Market Size (2031) | USD 52.98 Billion |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

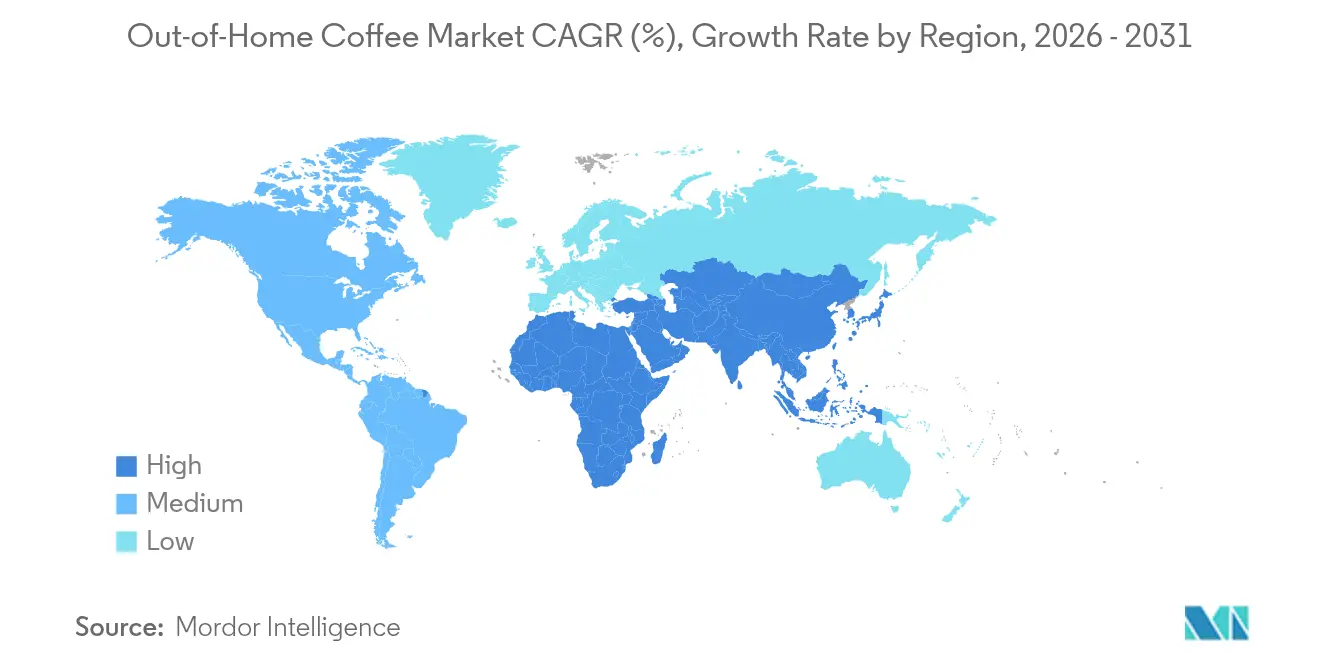

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

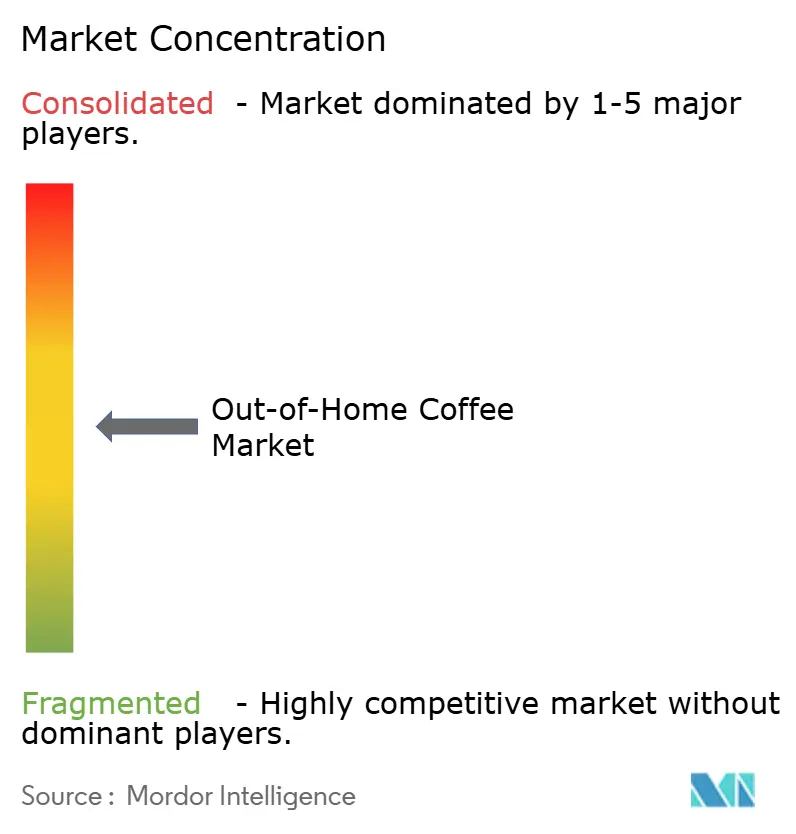

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Out-of-Home Coffee Market Analysis by Mordor Intelligence

The out-of-home coffee market reached USD 41.53 billion in 2025, stood at USD 43.31 billion in 2026, and is forecast to reach USD 52.98 billion by 2031, expanding at a CAGR of 4.11% during 2026-2031. Younger consumers are increasingly driving demand for specialty coffees, as they seek unique flavors and high-quality offerings. The market continues to experience premiumization, fueled by the rising popularity of single-origin beans, which appeal to consumers looking for authenticity and traceability in their coffee choices. Additionally, there is a growing preference for functional ready-to-drink (RTD) coffee options, which cater to the demand for convenience and health-focused beverages. Operators are actively expanding their presence by establishing suburban drive-thru locations to cater to on-the-go consumers. Europe maintains profitability by combining its deeply ingrained café culture with the implementation of strict sustainability regulations, which align with evolving consumer expectations for environmentally responsible practices. In contrast, the Middle East and Africa are experiencing the fastest outlet growth, driven by the resurgence of large-format mall openings, which attract significant foot traffic, and a revival in tourism activities that boost demand for out-of-home coffee experiences.

Key Report Takeaways

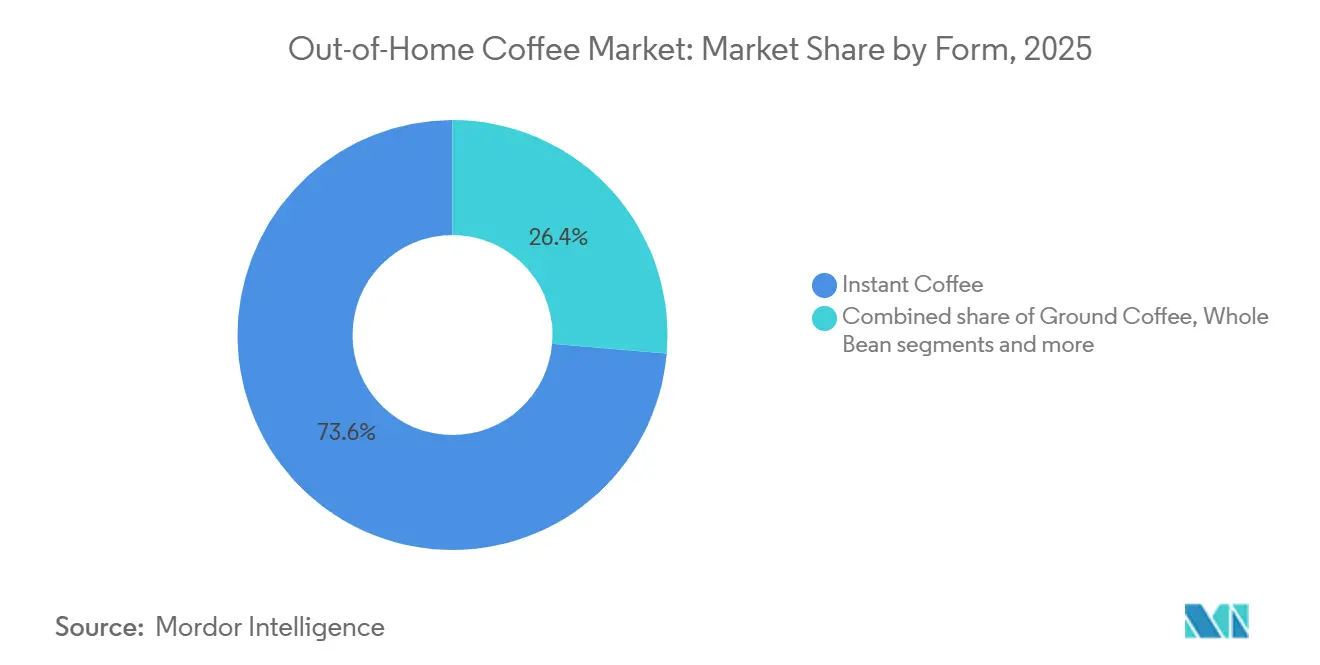

- By form, instant coffee held 73.62% of the out-of-home coffee market share in 2025, while coffee pods and capsules variants are projected to expand at a 4.80% CAGR through 2031.

- By bean type, arabica accounted for 54.74% in 2025; robusta is forecast to grow at a 5.11% CAGR through 2031.

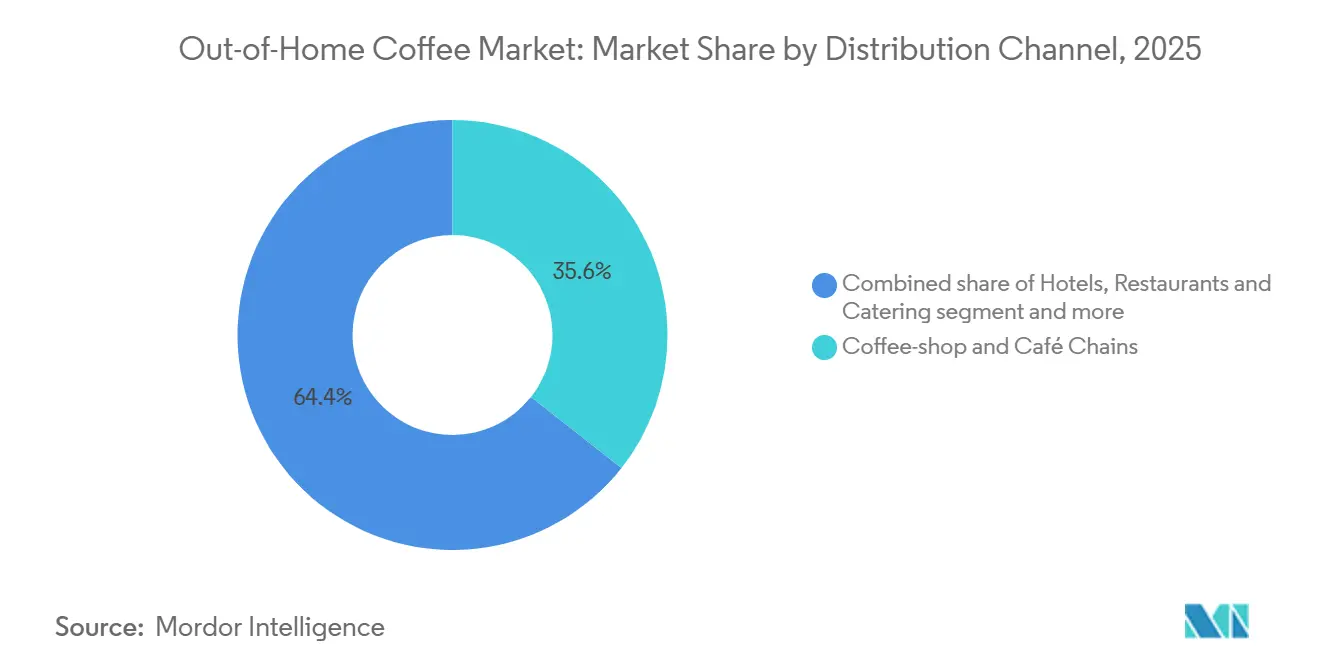

- By distribution channel, coffee-shop and café chains captured 35.62% of revenue in 2025, whereas quick-service and fast-casual restaurants will advance at a 4.92% CAGR over the forecast period.

- By geography, Europe accounted for 35.43% of the out-of-home coffee market in 2025, while the Middle East and Africa will register the highest CAGR of 5.52% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Out-of-Home Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising specialty-coffee demand among Millennials and Gen Z | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Convenience-led uptake of RTD and cold-brew formats | +0.8% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Expansion of café chains and social café culture | +0.9% | Middle East and North America, Asia-Pacific core with spillover to Europe | Long term (≥ 4 years) |

| AI-driven beverage personalisation lifting average ticket size | +0.6% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Premiumization with specialty blends and artisanal methods | +0.7% | Europe, North America, urban Asia-Pacific markets | Medium term (2-4 years) |

| Drive-thru micro-formats boosting suburban throughput | +0.5% | North America, expanding to Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising specialty-coffee demand among Millennials and Gen Z

Millennials and Gen Z drive the surging demand for specialty coffee, significantly influencing the Out-of-Home Coffee Market. These demographics prioritize premium coffee experiences, often seeking unique flavors, high-quality beans, and sustainable sourcing. Their preference for artisanal and specialty coffee options has led to increased visits to coffee shops, cafes, and other out-of-home coffee establishments. This trend is further fueled by their willingness to spend on premium beverages, making them a key consumer group driving growth in this market. According to Convenience Org, Gen Z coffee drinkers are just as likely to start with iced coffee as hot coffee, and about 85% of them add creamer, compared to 70% of coffee drinkers overall [1]Source: Convenience Org, "Here's How Gen Z Takes Their Coffee", convenience.org. This highlights their distinct preferences, which are shaping product offerings and marketing strategies in the out-of-home coffee segment. Additionally, according to the National Coffee Association of the USA, 46% of American adults consumed specialty coffee in 2024 [2]Source: National Coffee Association of USA, "NCDT Specialty Coffee Report", ncausa.org. This statistic underscores the growing popularity of specialty coffee among a broader consumer base, further driving the expansion of the Out-of-Home Coffee Market.

Convenience-led uptake of RTD and cold-brew formats

Health-conscious consumers, especially younger demographics, are increasingly opting for functional ready-to-drink (RTD) products that offer wellness benefits. These consumers prioritize on-the-go convenience without sacrificing quality. Cold-brewed options are emerging as premium alternatives to traditional iced coffee. In response, brands are innovating with sugar-free and organic variants to appeal to health-focused segments. An expanded distribution network, spanning supermarkets, convenience stores, and online platforms, is enhancing product accessibility. Notably, Asia-Pacific markets are witnessing significant growth, driven by evolving dietary preferences and increasing disposable incomes. This shift towards premium RTD products underscores a broader consumer trend: a willingness to pay a premium for convenience and perceived health benefits. This trend presents operators with opportunities to broaden their brand presence beyond just physical locations.

Expansion of café chains and social café culture

The expansion of café chains and the growing social café culture are significant drivers of the Out-of-Home Coffee Market. The increasing number of café outlets, coupled with the rising trend of socializing in coffee shops, has contributed to the market's growth. World Coffee Portal reports that Starbucks aims to launch 500 stores in the Middle East by 2030 [3]Source: World Coffee Portal, "Starbucks seeking to open 500 stores in Middle East by 2030", worldcoffeeportal.com, reflecting the rapid expansion of café chains. Social café culture is further strengthened through digital ordering integration and community-focused store designs, although traditional coffeehouse experiences face pressure from mobile-first convenience models. This café expansion aligns with urbanization trends and the rising disposable income of the middle class, particularly in emerging markets. In these regions, the adoption of coffee culture creates substantial growth opportunities. Consumers, particularly millennials and young professionals, are increasingly seeking spaces that offer both quality coffee and a conducive environment for social interactions or remote work. This trend has encouraged café chains to innovate and expand their offerings, further boosting the market.

Premiumization with specialty blends and artisanal methods

Artisanal methods and specialty blends drive premiumization in the Out-of-Home Coffee Market. Consumers increasingly seek high-quality coffee experiences, leading to a growing demand for premium products. Specialty blends, often crafted with unique flavor profiles and sourced from specific regions, cater to this demand. These blends are typically made using high-grade coffee beans, which are carefully selected and processed to ensure superior taste and aroma. Additionally, artisanal methods, such as hand-brewing techniques, small-batch roasting, and precision grinding, enhance the overall coffee experience, attracting a more discerning customer base. These methods emphasize craftsmanship and attention to detail, which resonate with consumers who value authenticity and exclusivity in their coffee choices. This trend is reshaping the market, as businesses focus on offering differentiated products to meet evolving consumer preferences. Furthermore, the rise of third-wave coffee culture has amplified the emphasis on quality, sustainability, and transparency, further driving the premiumization trend in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased preference for at-home coffee due to cost | -0.9% | Global, strongest impact in price-sensitive markets | Short term (≤ 2 years) |

| Price sensitivity and coffee price inflation | -1.1% | Global, particularly emerging markets | Medium term (2-4 years) |

| Supply chain disruptions affecting quality and availability | -0.7% | Global, concentrated in import-dependent regions | Medium term (2-4 years) |

| Rising operational and labor costs for cafés | -0.8% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased preference for at-home coffee due to cost

Rising costs drive a growing preference for at-home coffee, which acts as a significant restraint on the Out-of-Home Coffee Market. Consumers are increasingly opting to brew coffee at home to save money, especially as economic pressures and inflation impact disposable incomes. This shift in consumer behavior reduces the frequency of visits to coffee shops and other out-of-home coffee establishments, directly affecting market growth. Additionally, advancements in home coffee-making equipment and the availability of premium coffee products for home use further encourage this trend, intensifying the challenge for the Out-of-Home Coffee Market. The affordability and convenience of at-home coffee preparation have become key factors influencing this shift. Many consumers perceive at-home coffee as a cost-effective alternative to the often higher-priced beverages offered by coffee shops. Furthermore, the growing availability of subscription services for coffee beans and pods, along with the increasing popularity of do-it-yourself coffee recipes shared through social media platforms, has made at-home coffee preparation more appealing.

Price sensitivity and coffee price inflation

Price sensitivity and coffee price inflation act as significant restraints in the Out-of-Home Coffee Market. The rising cost of coffee, driven by factors such as fluctuating raw material prices, adverse weather conditions affecting coffee bean production, and increasing transportation costs, has led to higher prices for consumers. This inflation directly impacts consumer purchasing behavior, especially in price-sensitive markets, where individuals may reduce their frequency of coffee purchases or opt for lower-priced alternatives. Additionally, businesses in the out-of-home coffee sector face challenges in maintaining profit margins while trying to absorb or pass on these increased costs to customers. The combination of these factors creates a complex scenario, limiting the market's growth potential during the forecast period. Furthermore, global supply chain disruptions and geopolitical tensions have exacerbated the situation, leading to inconsistent coffee supply and further price volatility. For instance, coffee-producing regions like Brazil and Vietnam have experienced irregular weather patterns, including droughts and frosts, which have significantly impacted coffee yields.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Whole Bean Premiumization Accelerates Despite Price Pressures

Instant coffee remains the dominant segment in the out-of-home coffee market, projected to account for 73.62% of the market by 2025. Its leading position is attributed to its ease of preparation, cost-effectiveness, and suitability for high-volume consumption settings such as offices, vending machines, and quick-service outlets. The format ensures consistent taste with minimal equipment requirements, making it an ideal choice for operators prioritizing speed and scalability. Furthermore, its widespread availability and affordability solidify its role as a preferred option across various out-of-home environments.

On the other hand, coffee pods and capsules represent a steadily expanding segment, anticipated to grow at a CAGR of 4.80%. This growth is fueled by the rising demand for convenience combined with premium-quality coffee experiences in workplaces, hotels, and small-format cafés. Pods and capsules provide benefits such as portion control, reduced wastage, and consistent flavor, making them particularly appealing for controlled-service environments. As consumers increasingly seek café-like experiences outside traditional café settings, this segment is expected to gradually strengthen its presence within the out-of-home coffee market.

By Form: Arabica Innovation Drives Form Evolution

Arabica remains the leading bean type in the out-of-home coffee market, projected to account for 54.74% of the total market share in 2025. Its popularity stems from its smooth flavor profile, lower bitterness, and reputation for superior quality, making it the preferred choice for premium outlets, cafés, and hospitality establishments. Arabica beans are a staple in specialty coffee offerings, which are increasingly favored in urban areas and high-end consumption spaces. This enduring consumer preference for high-quality coffee continues to solidify Arabica's dominant position in the market.

Conversely, robusta is anticipated to grow steadily, with a projected CAGR of 5.11% through 2031. This growth is fueled by its higher caffeine content, bold flavor, and cost-effectiveness, which make it ideal for high-volume and mass-market out-of-home consumption. Robusta is widely used in instant coffee and vending machine solutions, where affordability and functional benefits are critical. As demand increases in emerging markets and price-sensitive segments, robusta is expected to gain further traction within the out-of-home coffee market.

By Distribution Channel: QSR Growth Challenges Traditional Café Dominance

Coffee-shop and café chains hold the largest share of the distribution channel in the Out-of-Home Coffee Market, commanding 35.62% in 2025. Their dominant position is supported by strong brand recognition that attracts a loyal customer base across multiple regions. These chains focus on creating immersive and experiential environments where consumers can enjoy their coffee in a social and comfortable setting. Customer loyalty programs further enhance retention by rewarding frequent visits and encouraging repeat business. The combination of well-established brands, inviting ambiance, and consistent product quality allows these chains to maintain a competitive edge. Their extensive network of outlets ensures wide accessibility, reinforcing their market leadership. This segment’s sustained success reflects its ability to evolve while preserving core elements that resonate with coffee consumers.

In contrast, quick-service and fast-casual restaurants are the fastest-growing distribution segment, projected to achieve a CAGR of 4.2% between 2026 and 2031. This growth is driven by their ability to capitalize on convenience factors such as drive-thru services and shorter wait times, which appeal to busy consumers and commuters. These restaurants also benefit from integrated food and beverage offerings, providing a one-stop solution that attracts customers looking for quick, efficient dining and coffee options. Operational efficiencies and streamlined service models further enable these establishments to expand rapidly. The shift towards convenience-driven consumption habits supports their growth trajectory. As consumer preferences continue to evolve, quick-service and fast-casual restaurants are positioned to gain an increasing share of the out-of-home coffee market, challenging traditional café chains.

Geography Analysis

Europe continues to maintain its position as the market leader in the market, commanding a substantial 35.43% share in 2025. The region's leadership is deeply rooted in its sophisticated and well-established coffee culture, which has been cultivated over centuries and is integral to daily life across many European countries. European markets benefit from stringent regulatory frameworks that emphasize sustainability and high-quality standards, fostering consumer trust and promoting ethical sourcing practices. These regulations encourage coffee operators to innovate responsibly, focusing on environmentally friendly practices and premium product offerings. Furthermore, the dense network of coffee shops and café chains in Europe reinforces consumer loyalty and consistently drives demand in the out-of-home segment.

In contrast, the Middle East and Africa represent the fastest-growing region in the Out-of-Home Coffee Market, with a projected CAGR of 5.52% from 2026 to 2031. This dynamic growth is propelled by rising urban populations, changing lifestyle preferences, and increasing disposable incomes that fuel demand for fashionable and premium coffee experiences. Investments in coffee retail infrastructure and the introduction of international coffee chains are significantly expanding access and awareness in these regions. Moreover, cultural openness toward new lifestyle trends and a youthful demographic are supporting the shift toward coffee consumption outside the home. The growth in this region also reflects a broader economic diversification strategy and increased tourism, further expanding the consumer base for out-of-home coffee products.

Meanwhile, the Asia-Pacific region exhibits the most dynamic and complex growth patterns in the out-of-home coffee space. Countries such as China, Japan, and South Korea are witnessing burgeoning coffee scenes, characterized by a mix of modern café formats and traditional beverage variations. North America also remains a significant player, with a strong coffee culture that continues to evolve through innovation in ready-to-drink (RTD) beverages and specialty coffee formats. The competitive but mature North American market is driven by both established chains and artisanal coffee shops innovating to cater to increasingly sophisticated consumer palates.

Competitive Landscape

The Out-of-Home Coffee Market demonstrates a moderate level of market concentration, indicating a fragmented competitive landscape. This market is characterized by the presence of a diverse range of players, including global coffeehouse chains, regional specialists, technology-driven entrants, and local operators. The growing consumer demand for convenient and premium coffee experiences outside the home has intensified competition, compelling market participants to innovate and adapt to evolving consumer preferences. The interplay of these diverse players creates a dynamic and competitive environment that continues to shape the market's trajectory.

Global coffeehouse chains maintain a significant presence in the market, leveraging their established brand equity, extensive distribution networks, and standardized offerings. However, these players are increasingly facing challenges from regional specialists who cater to localized tastes and preferences. Regional players often capitalize on their deep understanding of cultural nuances and consumer behavior, enabling them to create unique and tailored offerings that resonate with their target audience. This localized approach allows regional competitors to carve out a niche in the market, posing a growing threat to the dominance of global chains.

In addition to regional specialists, local operators and technology-driven entrants are further intensifying the competitive landscape. Local players emphasize authenticity, community engagement, and personalized customer experiences, which appeal to consumers seeking unique and meaningful coffee experiences. Meanwhile, technology-driven entrants are disrupting traditional business models by introducing innovative solutions such as app-based ordering, subscription services, and data-driven personalization. These advancements not only enhance customer convenience but also enable players to streamline operations and build stronger customer relationships. As a result, the Out-of-Home Coffee Market is witnessing heightened competition, with all players striving to differentiate themselves and secure consumer loyalty in an increasingly dynamic environment.

Out-of-Home Coffee Industry Leaders

-

Nestlé S.A.

-

Starbucks Corporation

-

JAB Holding Company Sàrl

-

The Coca-Cola Company (Costa Coffee)

-

Luigi Lavazza S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Coffeeshop Company, the Austrian coffeehouse brand, entered the Indian café landscape with the launch of its first flagship store in Delhi. Bringing over 25 years of legacy from Vienna to the heart of India, the brand harmonizes the rich, UNESCO-recognized tradition of Viennese café culture with modern, high-speed coffee-to-go sensibilities. Unlike other coffee chains, Coffeeshop Company operates locations that function as both a cafe and a bar, serving coffee, cocktails, and other alcoholic beverages.

- April 2025: Starbucks has introduced two new ready-to-drink (RTD) beverage lines, targeting health-conscious consumers who seek convenient and healthier caffeine options. The newly launched RTD Starbucks Iced Energy and RTD Frappuccino Lite are designed to meet the growing demand for functional beverages, offering reduced sugar content while delivering a quick and accessible energy boost.

- January 2025: Starbucks announced a USD 3 billion investment to open 1,500 new stores across China by 2027, targeting tier-2 and tier-3 cities where café penetration remains below national averages. The expansion includes 300 drive-thru locations, a format previously underutilized in the market, and aims to recapture share lost to Luckin Coffee's aggressive discounting.

Global Out-of-Home Coffee Market Report Scope

The out-of-home coffee market refers to sales of coffee through the HRI (hotels, restaurants, and institutions) industry worldwide. The out-of-home coffee market studied is segmented by product category, beverage format, distribution channel, and geography. By product category, the market is segmented into regular coffee and gourmet/specialty coffee. By beverage format, the market is segmented into hot brewed, iced/cold brew, and ready-to-drink (RTD). By distribution channel, the market is segmented into coffee-shop and café chains, quick-service and fast-casual restaurants, hotels, restaurants and catering, and other distribution channels. The study also covers the global analysis of the major regions, such as North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD billion) and volume (in tons).

| Whole Bean |

| Ground Bean |

| Instant Coffee |

| Coffee Pods and Capsules |

| Arabica |

| Robusta |

| Blends |

| Coffee-shop and Café Chains |

| Quick-Service and Fast-Casual Restaurants |

| Hotels, Restaurants and Catering |

| Corporation and Education Institutions |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Form | Whole Bean | |

| Ground Bean | ||

| Instant Coffee | ||

| Coffee Pods and Capsules | ||

| By Bean Type | Arabica | |

| Robusta | ||

| Blends | ||

| By Distribution Channel | Coffee-shop and Café Chains | |

| Quick-Service and Fast-Casual Restaurants | ||

| Hotels, Restaurants and Catering | ||

| Corporation and Education Institutions | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the out-of-home coffee market by 2031?

The market is forecast to reach USD 52.98 billion by 2031, expanding at a 4.11% CAGR from 2026 to 2031, driven by premiumization, RTD format adoption, and geographic expansion in the Middle East and Africa.

Which region is growing fastest in the out-of-home coffee space?

Middle East and Africa will expand at a 5.52% CAGR through 2031, the highest globally, fueled by rising disposable incomes, urbanization, and café-chain expansion in Saudi Arabia and the UAE.

How are quick-service restaurants competing with specialty café chains?

QSR operators integrate espresso platforms into existing drive-thru infrastructure, offering coffee at 30-40% lower prices than specialty chains while leveraging mobile-order-ahead technology to reduce wait times; McDonald's global coffee sales exceeded USD 8 billion in 2025.

What role does artificial intelligence play in coffee sales?

AI-driven personalization engines analyze purchase history, weather, and time of day to recommend high-margin beverages; Starbucks' Deep Brew platform increased order frequency by 12% among active app users in 2025.

Page last updated on: