Coffee Concentrate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

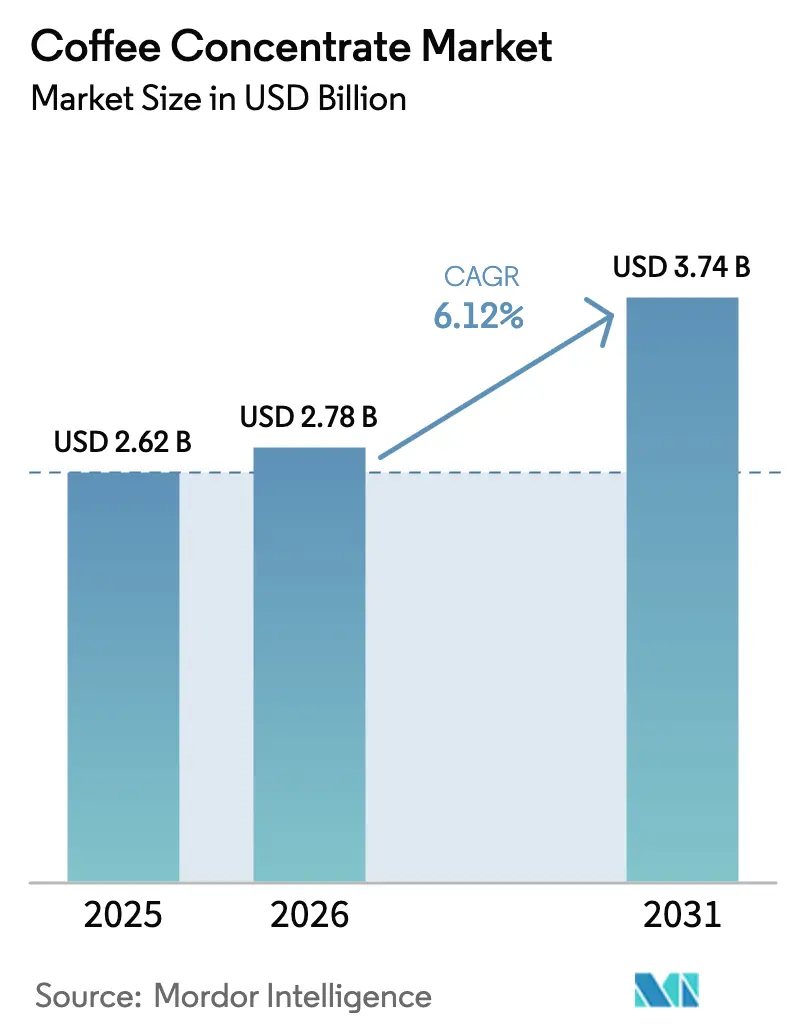

| Market Size (2026) | USD 2.78 Billion |

| Market Size (2031) | USD 3.74 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

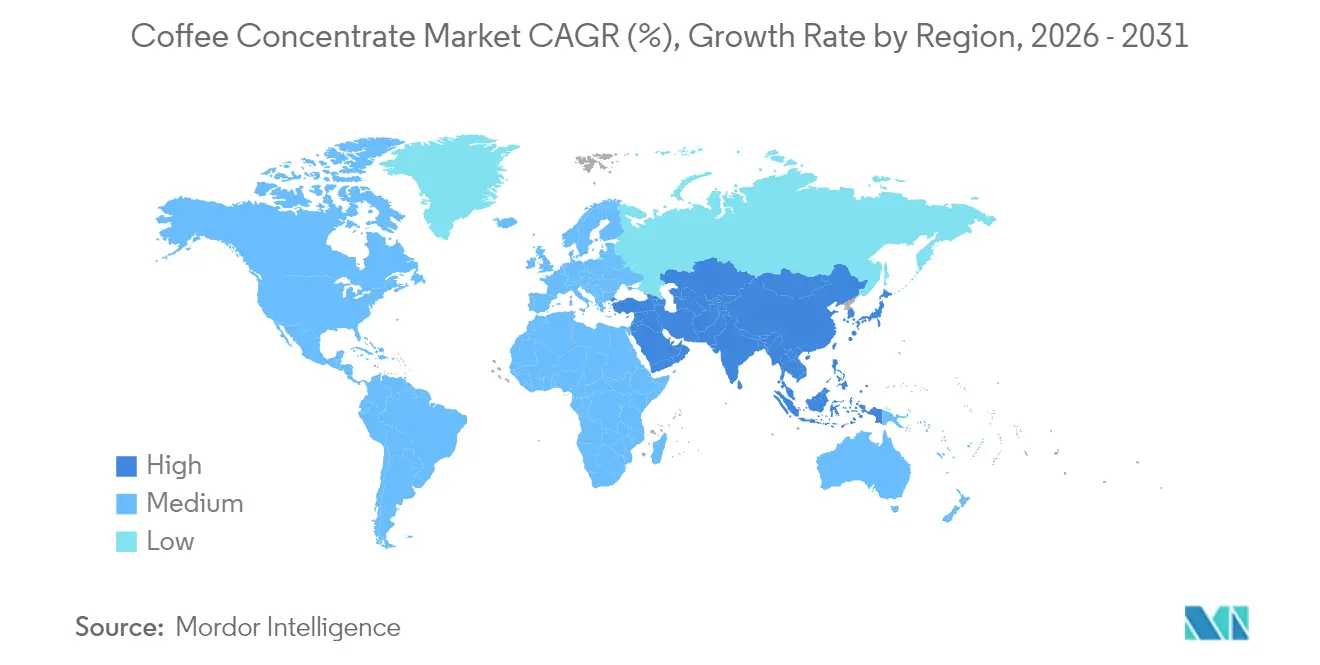

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

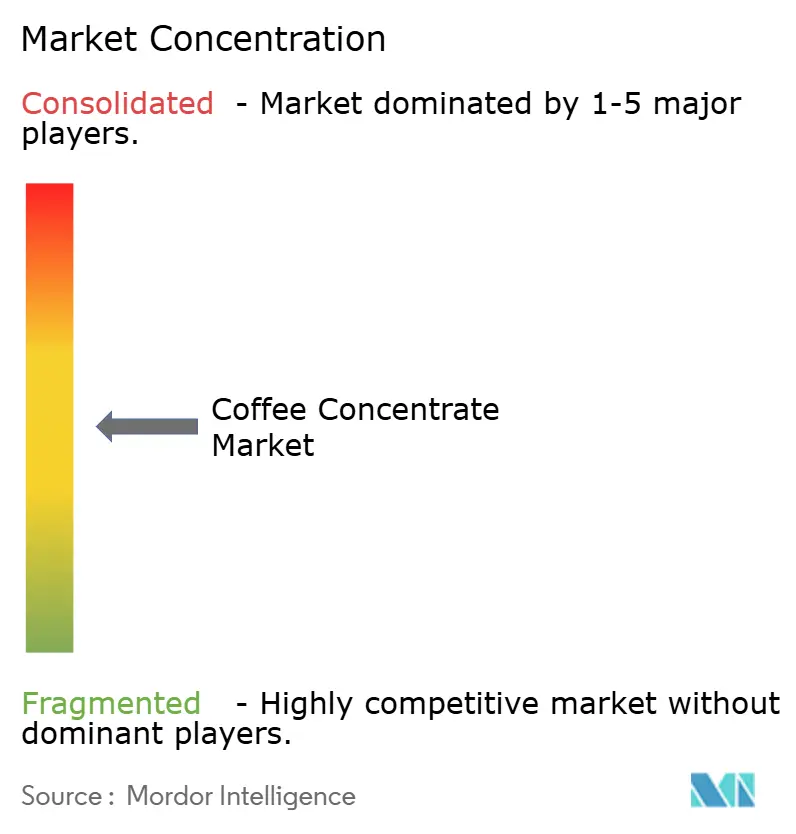

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coffee Concentrate Market Analysis by Mordor Intelligence

The coffee concentrate market size was valued at USD 2.62 billion in 2025 and estimated to grow from USD 2.78 billion in 2026 to reach USD 3.74 billion by 2031, at a CAGR of 6.12% during the forecast period (2026-2031). This growth trajectory is driven by an increasing preference for convenient premium beverages, a surge in the adoption of cold-brew formats, and enhanced operational efficiencies in foodservice channels. North America maintains its dominant position, bolstered by a deep-rooted coffee culture and advanced distribution systems. In contrast, the Asia-Pacific region witnesses the swiftest growth, as urban consumers increasingly favor café-style beverages in their homes. Innovations in product development emphasize smoother taste profiles and unique functional ingredients, offering concentrate suppliers a distinct competitive advantage over traditional brewing methods. However, sourcing strategies and packaging decisions remain under pressure due to supply-chain challenges tied to fluctuating arabica prices and pressing sustainability mandates.

Key Report Takeaways

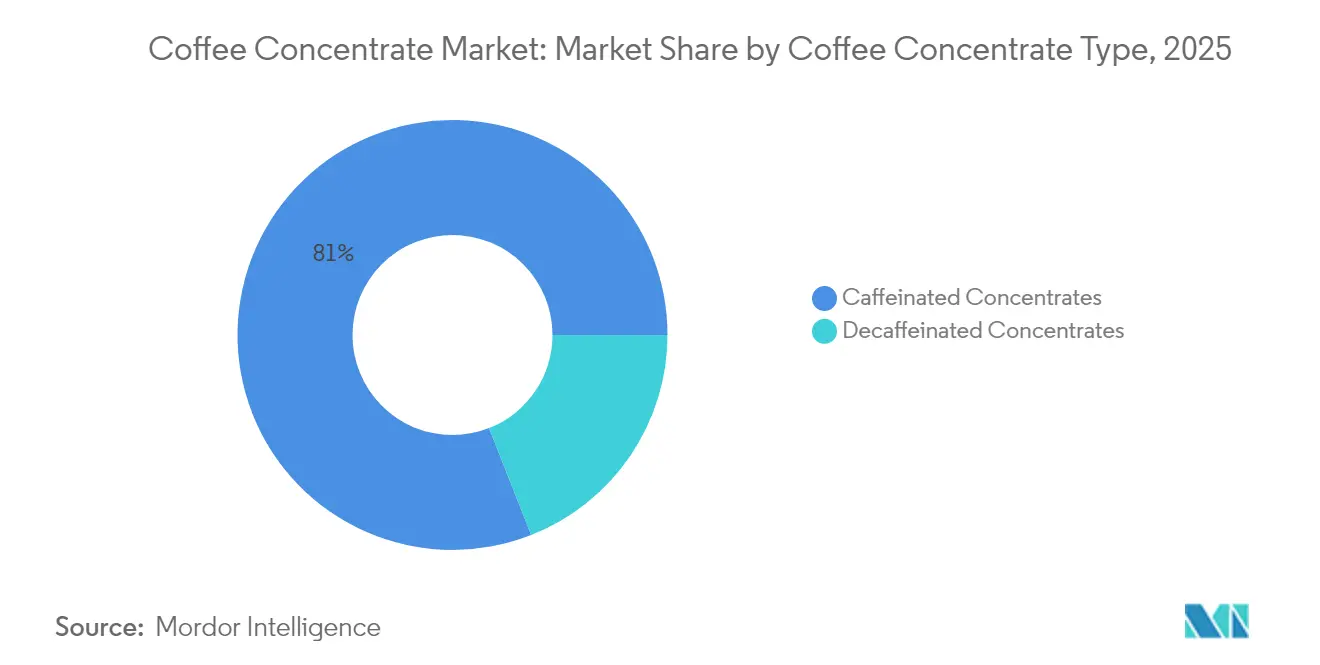

- By concentrate type, caffeinated variants represented 80.96% share in 2025, whereas decaffeinated products will grow at an 8.34% CAGR through 2031.

- By product type, cold-brew coffee concentrate held 46.21% of the coffee concentrate market share in 2025, whereas espresso concentrate is forecast to expand at a 8.82% CAGR through 2031.

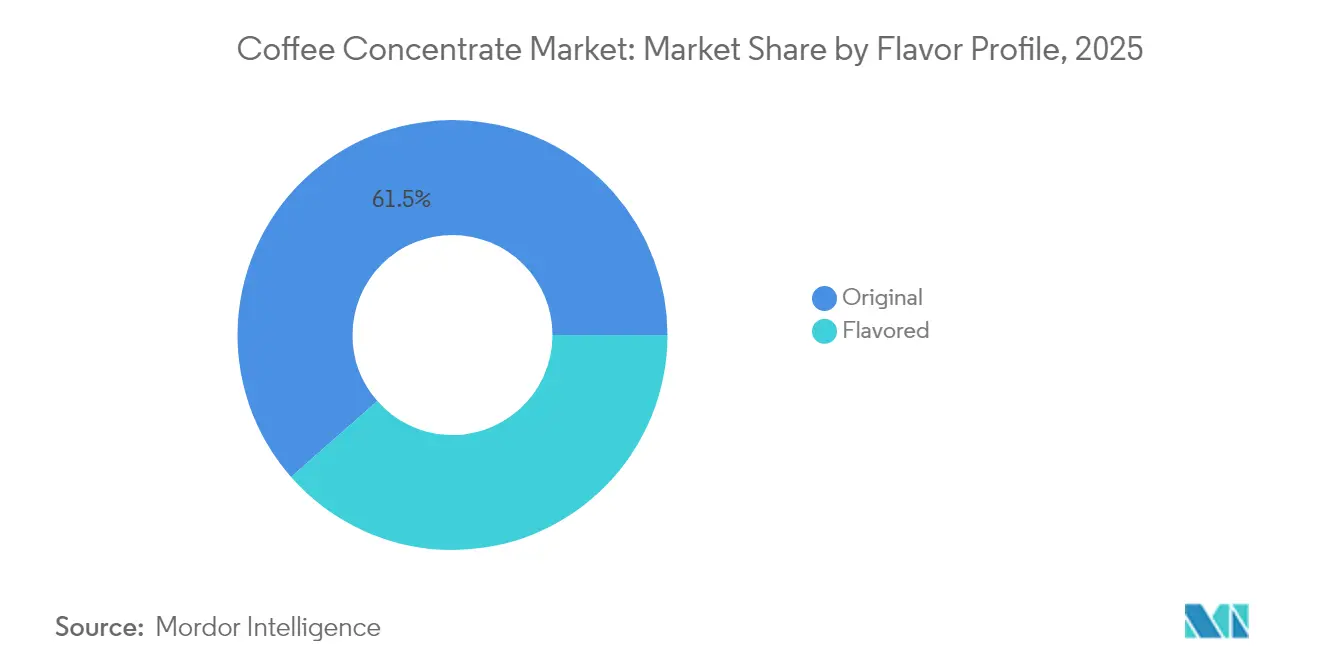

- By flavor profile, original flavor held 61.48% of the coffee concentrate market share in 2025, whereas flavored coffee concentrates are forecast to expand at a 7.71% CAGR through 2031.

- By end-user, foodservice captured 40.73% of the coffee concentrate market in 2025, while food and beverage manufacturers are projected to grow the fastest at 7.96% CAGR to 2031.

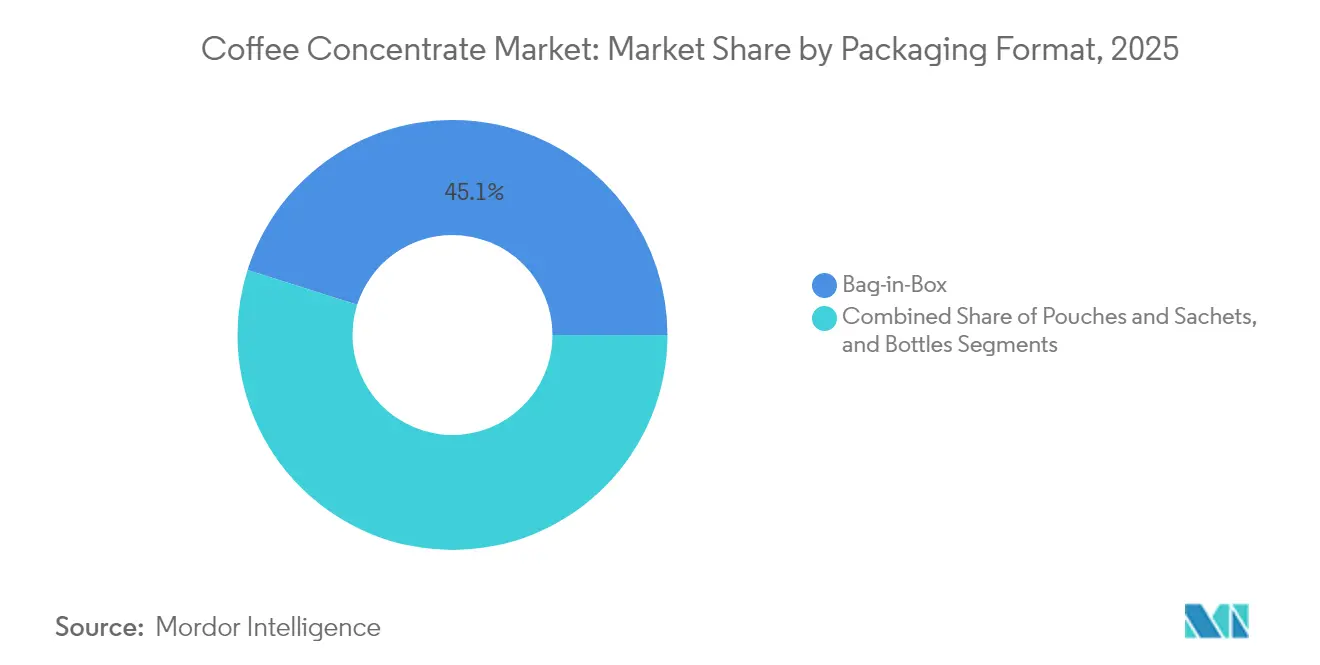

- By packaging format, bag-in-box commanded 45.12% share in 2025, and bottles are advancing at a 7.24% CAGR over the forecast period.

- By geography, North America held a 52.05% share in 2025, and the Asia-Pacific leads growth at a 7.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Coffee Concentrate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for RTD coffee and convenience beverages | +1.8% | Global, with strongest impact in North America and Asia-Pacific | Medium term (2-4 years) |

| Consumers opting for at-home Gourmet/Barista experience | +1.2% | North America and Europe, expanding to urban Asia-Pacific | Long term (≥ 4 years) |

| Product launches by global brands in cold-brew concentrates | +0.9% | Global, led by North America with spillover to Europe | Short term (≤ 2 years) |

| Growing café culture in emerging countries markets driving at-home premiumization | +0.7% | Asia-Pacific core, spillover to South America and MEA | Long term (≥ 4 years) |

| Adoption of bag-in-box formats by QSRs to cut storage and CO₂ footprint | +0.6% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Versatility in culinary applications | +0.4% | Global, with premium segment focus in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for RTD Coffee and Convenience Beverages

The explosive growth of the ready-to-drink (RTD) coffee segment is reshaping demand patterns for coffee concentrates, mirroring trends in the broader RTD beverage market. As beverage manufacturers increasingly seek cost-effective and shelf-stable inputs that ensure consistent flavor across production scales, this surge places added pressure on concentrate suppliers. Moreover, the rising trend of functional RTD coffee infused with electrolytes and adaptogens demands specialized concentrate formulations, a feat that traditional brewing methods struggle to achieve efficiently. In recent years, a shift towards at-home coffee consumption has emerged, leading to a dual demand: both for retail RTD products and concentrates meant for home preparation. This convenience is especially pronounced in emerging markets, where traditional coffee infrastructure is still in development. Here, concentrates are not just tools for efficiency; they serve as pivotal enablers for deeper market penetration.

Consumers Opting for At-Home Gourmet/Barista Experience

As consumers invest in home brewing equipment, they're moving beyond traditional foodservice uses, seeking professional-grade flavor profiles. Younger demographics, viewing coffee preparation as a lifestyle expression, are driving a surge in specialty coffee consumption. This shift fuels demand for single-origin and estate-specific concentrates, prized for their terroir characteristics and preparation convenience. With the rise of functional coffee trends, like mushroom-infused and adaptogen-enhanced varieties, concentrate manufacturers are pivoting, honing specialized processing capabilities to preserve bioactive compounds. In response, equipment manufacturers are rolling out home systems tailored for concentrate dilution and customization, broadening the market reach beyond conventional commercial channels. This trend is gaining momentum in affluent markets with a rich coffee culture, where consumers are eager to pay a premium for authentic experiences in convenient formats.

Product Launches by Global Brands in Cold-Brew Concentrates

According to Beverage Daily, Nestlé has introduced Nescafe Espresso Concentrate in Australia, marking the beginning of a global rollout. This move underscores the industry's recognition of cold brew's advantages: its concentrates boast better extraction efficiency and longer shelf life than their hot-brewed counterparts. By investing in cold-brew concentrate technology, brands are not only gaining a competitive edge through unique extraction techniques but are also differentiating their flavor profiles. These new products are especially appealing to millennial and Gen Z consumers, who favor the smoother, less acidic taste of cold brew and view it as a premium offering. This trend is fueling both volume growth and increased margins for producers of these concentrates.

Growing Café Culture in Emerging Countries Markets Driving At-Home Premiumization

Despite facing economic challenges, China's coffee consumption surged by 57% from 2019 to 2023, highlighting the rapid evolution of café culture in emerging markets, according to the World Coffee Portal. As consumers cultivate more refined tastes, there's a growing demand for authentic coffee experiences at home. This shift has led to a rising adoption of coffee concentrates, serving as a convenient bridge between café-quality brews and home preparation. This trend isn't confined to China; markets in India, Southeast Asia, and South America are witnessing similar transformations. Here, urbanization and increasing disposable incomes are reshaping lifestyle choices. In response, café chains across these regions are introducing retail concentrate products, capitalizing on their established customer bases to promote at-home coffee consumption. This burgeoning trend presents a golden opportunity for concentrate manufacturers. By collaborating with local café chains, they can craft flavor profiles that resonate with regional tastes, all while upholding global quality benchmarks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in arabica bean prices squeezing concentrate margins | -1.1% | Global, with highest impact in cost-sensitive emerging markets | Short term (≤ 2 years) |

| Competition from canned RTD cold brew reducing DIY concentrate usage | -0.8% | North America & Europe, expanding to urban Asia-Pacific | Medium term (2-4 years) |

| Environmental Risks to Coffee Production | -0.6% | Coffee-producing regions globally, supply chain spillover effects | Long term (≥ 4 years) |

| Limited consumer awareness in emerging markets | -0.5% | Asia-Pacific, Latin America, MEA emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Arabica Bean Prices Squeezing Concentrate Margins

In 2024, Arabica coffee prices surged to a historic high of USD 4 per pound, marking a 47-year peak that fundamentally shifts the economics of concentrate production, as reported by De La Gente. This price volatility is attributed to production hurdles in major growing regions like Colombia, Brazil, and Vietnam. These challenges are further exacerbated by speculative investments, which have reached unprecedented levels, surpassing USD 7 billion in net positions, according to Sucafina. Concentrate manufacturers are grappling with margin compression, unable to swiftly transfer rising costs to their price-sensitive foodservice clients, who operate on tight margins. This predicament compels manufacturers to make strategic choices: either absorb the costs to retain market share or raise prices, risking a shift of customers to competitors or alternative products. Moreover, the volatility in coffee futures complicates long-term contract negotiations, with both buyers and sellers finding it challenging to set stable pricing mechanisms amidst rapid commodity cost fluctuations.

Competition from Canned RTD Cold Brew Reducing DIY Concentrate Usage

Climate change is disrupting coffee-growing regions, jeopardizing the stability and cost predictability of concentrate production. In Colombia, the 2024 harvest saw a 10% increase, reaching 12.2 million bags. However, as reported by Sucafina, this boost came at the cost of quality, with issues stemming from dryness and the Coffee Berry Borer pest[1]Source: Sucafina, “Colombian 2024 Harvest Update,” sucafina.com. This underscores the profound impact of environmental factors on both the quantity and quality of raw materials. Meanwhile, Central America and Mexico grapple with delayed harvests, a consequence of drought and heavy rains from tropical storms. Adding to the woes, the Chiapas region in Mexico faces labor shortages, exacerbated by violence, as highlighted by Sustainable Harvest[2]Source: Sustainable Harvest, “Central America and Mexico Harvest Update,” sustainableharvest.com. Such environmental challenges cast a long shadow of uncertainty for concentrate manufacturers, who depend on consistent raw material quality and availability to uphold their product standards. In response, there's a heightened emphasis on diversifying supply chains and adopting sustainable sourcing practices. However, these measures come with the trade-off of increased procurement costs and complexities for concentrate producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coffee Concentrate Type: Caffeinated Dominance Drives Market

In 2025, caffeinated concentrates dominate the market with an 80.96% share, underscoring a widespread consumer inclination towards energizing coffee experiences at all times of the day. This segment's lead is largely due to its strong foothold in foodservice and retail channels, where caffeine content is a key purchase motivator, especially for morning boosts and afternoon pick-me-ups. Meanwhile, decaffeinated concentrates, though a smaller player, are on an impressive growth trajectory, boasting an 8.34% CAGR through 2031. This surge is driven by health-conscious consumers opting for evening coffee without the worry of sleep disturbances. Furthermore, the FDA's caffeine regulations, specifically 21 CFR 182.1180, set a 0.02% tolerance for cola-type beverages, offering clear directives for concentrate manufacturers targeting diverse beverage applications.

The rapid expansion of the decaffeinated segment highlights the industry's adept consumer segmentation strategies. Manufacturers are honing specialized processing techniques that retain flavor depth while eliminating caffeine. Techniques like methylene chloride and ethyl acetate decaffeination, under the watchful eye of 21 CFR Part 173 FDA regulations, empower producers to craft premium decaffeinated offerings that rival their caffeinated counterparts in taste. This segment finds particular favor during evening hours, especially among health-conscious consumers who value coffee's flavor over its stimulating properties, paving the way for niche market opportunities in specialized concentrate formulations.

By Product Type: Cold Brew Leadership Meets Espresso Innovation

In 2025, cold brew coffee concentrate commands a 46.21% share of the market, capitalizing on its efficient extraction methods and a growing consumer preference for smoother, less acidic flavors. This segment's dominance underscores cold brew's natural fit for concentrate applications; its prolonged extraction yields a coffee that's already concentrated, needing only minimal processing. Meanwhile, espresso concentrate is the rising star, projected to grow at a robust 8.82% CAGR through 2031. This surge is fueled by a trend towards premiumization and a consumer appetite for genuine Italian coffee experiences, especially in convenient formats.

On the other hand, black coffee concentrate caters to traditionalists, while specialty flavor concentrates resonate with younger audiences and seasonal trends. Nestlé's introduction of Nescafe Espresso Concentrate in Australia, with a global launch set for 2024, underscores the brand's dedication to espresso concentrate innovation. This strategic move highlights the potential of espresso concentrate to meld premium appeal with widespread market reach, paving the way for new consumption moments beyond the conventional espresso. While cold brew continues to thrive, thanks to its natural concentrate traits and alignment with health trends, the espresso concentrate's ascent signals a lucrative premiumization avenue for manufacturers ready to invest in specialized processing and authentic flavor crafting.

By Flavor Profile: Original Preference Balances Flavored Innovation

In 2025, original flavor concentrates command a 61.48% market share, underscoring a consumer preference for genuine coffee experiences. These concentrates deliver authentic tastes without resorting to artificial additives. This segment's dominance highlights that consumers prioritize convenience and consistency over flavor alterations, resonating with coffee purists who cherish traditional profiles. Meanwhile, flavored concentrates are on a growth trajectory, expanding at a 7.71% CAGR through 2031. This surge is largely fueled by younger consumers and seasonal trends that lean towards variety and experimentation. Notably, the flavored segment finds its strength in culinary uses and specialty drinks, where coffee acts as a foundational ingredient rather than the main flavor.

The interplay between original and flavored segments signals a maturing market. Here, the age-old appreciation for authentic coffee experiences meets a modern appetite for innovation, variety, and personalization. Trends like herbal coffee, which infuse ingredients such as rosemary, lemongrass, and ashwagandha, as highlighted by Symrise, pave the way for flavored concentrates. These can uphold coffee's authenticity while introducing functional benefits. With projections indicating the flavored coffee segment will swell from USD 7 billion to USD 9 billion by 2029, there's a clear and lucrative avenue for concentrate manufacturers. Those who can craft innovative flavor blends stand to capture the attention of both health-conscious and adventurous consumers.

By End-User: Foodservice Leadership Meets B2B Manufacturing Growth

In 2025, the foodservice segment commands a dominant 40.73% market share, underscoring the widespread adoption of concentrates in restaurants, cafes, and quick-service outlets. These establishments are drawn to the operational efficiencies and consistent quality that concentrates offer. The advantages of concentrates in foodservice are clear: they enable precise portion control, boast an extended shelf life, and streamline preparation processes. This not only curtails labor costs but also significantly reduces waste. Meanwhile, food and beverage manufacturers are emerging as the fastest-growing segment, projected to expand at a robust 7.96% CAGR through 2031. This surge is largely fueled by the development of ready-to-drink (RTD) products and industrial applications that demand a consistent coffee flavor.

On the retail front, the household segment caters to consumers desiring a premium coffee experience at home. This segment is particularly thriving amidst the rising trend of home barista equipment and the do-it-yourself (DIY) beverage preparation movement. The foodservice segment's dominance is a testament to the operational benefits concentrates bring to commercial venues. Here, the emphasis on consistency, efficiency, and cost control heavily influences purchasing choices. Quick-service restaurants (QSRs) are increasingly turning to bag-in-box formats, highlighting how packaging innovations not only bolster foodservice growth but also address pressing sustainability concerns. The rapid expansion of food and beverage manufacturers can be attributed to the burgeoning ready-to-drink (RTD) market and the demand for shelf-stable coffee ingredients. These ingredients are crucial for preserving flavor integrity throughout extended supply chains and diverse storage conditions.

By Packaging Format: Bag-in-Box Efficiency Meets Bottle Convenience

In 2025, bag-in-box packaging commands a leading 45.12% market share, propelled by its sustainability benefits, operational efficiency, and cost-effectiveness. These attributes resonate with commercial clients pursuing eco-friendly solutions. According to Amcor, this format can slash carbon footprints by up to 68% compared to traditional packaging, all while boasting enhanced storage efficiency and a longer shelf life. Bottles, on the other hand, are witnessing a 7.24% CAGR growth projected through 2031, drawing in retail consumers who value convenience, portion control, and a premium look.

Meanwhile, pouches and sachets cater to niche markets, especially in emerging regions where single-serve formats align with local purchasing habits and consumption trends. The shifting dynamics in packaging mirror wider trends in sustainability and the push for operational efficiency across various market segments. Highlighting this industry shift, Mother Parkers, in collaboration with Graphic Packaging, unveiled paperboard canisters that cut plastic use by 50%. This move underscores the industry's pivot towards eco-friendly packaging solutions that prioritize both product integrity and environmental responsibility. While the bag-in-box format thrives commercially, the rising popularity of bottles in retail underscores the diverse packaging needs across different end-user applications and global markets.

Geography Analysis

In 2025, North America commanded a dominant 52.05% share of the coffee concentrate market, fueled by its entrenched café culture and a distribution network that spans multiple channels. Consumers in the region are increasingly willing to invest in premium convenience. Thanks to robust cold chain logistics, coffee concentrates are making their way into grocery stores, clubs, and foodservice outlets, all while maintaining their quality. Highlighting the significance of concentrated coffee products, Starbucks reported a Channel Development revenue of USD 436.3 million in Q1 FY2025, underscoring the strength of its retail partnerships. While Canada’s specialty retail chains are adopting on-tap concentrate systems, Mexico is turning to imports to bridge supply gaps from unpredictable harvests. Furthermore, with the FDA's regulatory clarity, including GRAS notices for coffee fruit extract, product approvals have become more streamlined, fostering innovation in the sector.

Asia-Pacific is set to witness a robust growth rate of 7.45% CAGR through 2031, spurred by urbanization, increasing disposable incomes, and a swift rise in café establishments. According to the World Coffee Portal, China stands out with nearly 50,000 branded coffee outlets. E-commerce platforms are enhancing household adoption by bundling concentrates with grinder-free capsule machines. In India, café chains are collaborating with concentrate suppliers to bottle their signature drinks, making premium flavors accessible in grocery stores and appealing to younger consumers. Japan is focusing on specialty single-origin concentrates for its discerning clientele, while craft roasters in Australia are innovating with nitrogen-infused concentrate kegs tailored for the foodservice sector.

Europe, with its established espresso traditions and mature consumption habits, is witnessing stable but slower growth. Germany and the Netherlands are at the forefront, leveraging advanced retail merchandising and private-label strategies to boost concentrate adoption. Meanwhile, Southern Europe remains hesitant, with consumers leaning towards freshly ground preparations. However, sustainability regulations are nudging these operators to consider waste-saving concentrate solutions. In Latin America, the lines between production and consumption blur, with Brazil taking the lead in export-driven concentrate manufacturing, strategically located near coffee bean origins. The Middle East and Africa present budding opportunities. Here, rapid urbanization and a surge in tourism are fueling a demand for convenient café experiences. Yet, challenges like infrastructure limitations and price sensitivity are moderating immediate growth prospects.

Competitive Landscape

In the coffee concentrate market, competition remains moderately concentrated. Leveraging global brand equity and integrated supply chains, giants like Starbucks, Nestlé, and JDE Peet’s dominate mainstream channels. Through the Global Coffee Alliance, Starbucks collaborates with Nestlé, distributing RTD and concentrate products in supermarkets, broadening its reach without incurring direct retail costs. Meanwhile, mid-sized specialists such as Califia Farms, Wandering Bear, and Jot Coffee carve out niches by prioritizing clean-label ingredients, adopting direct-to-consumer subscription models, and offering high-caffeine products.

Players differentiate themselves through technology investments; proprietary cold-brew extraction and flash pasteurization methods not only safeguard sensory profiles but also prolong shelf life. Sustainability pledges become competitive advantages, exemplified by Amcor’s AmPrima Plus pouch, which boasts a 68% smaller carbon footprint and has clinched a global packaging award, leading to early-access contracts with eco-conscious brands. Vertical integration, encompassing farm ownership and long-term supply agreements, acts as a buffer for large firms against commodity price swings. In contrast, smaller entrants, by sourcing from microlots and sharing transparent origin narratives, connect deeply with ethically conscious consumers.

Strategic maneuvers in 2024 and 2025 hint at escalating R&D investments in functional concentrates, particularly those infused with probiotics or adaptogens, targeting the wellness market. Newcomers, facing capital expenditure challenges, find relief in collaborative manufacturing agreements, paving the way for a vibrant array of limited-edition flavors. E-commerce platforms not only facilitate direct brand-consumer interactions but also empower brands to gather taste-preference insights, refining future product formulations. As regional players in Asia-Pacific and Latin America expand their footprint, multinationals counter with minority investments or licensing agreements, intensifying the competitive landscape of the coffee concentrate market.

Coffee Concentrate Industry Leaders

Starbucks Corp.

Nestlé S.A.

JDE Peet’s N.V.

Califia Farms LLC

Wandering Bear Coffee Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Lavazza introduced Tablì, a packaging-free single-serve coffee solution developed through 5 years of R&D and over 15 patents, representing a significant innovation in sustainable coffee preparation that could influence concentrate packaging approaches and consumer convenience expectations.

- January 2025: Mother Parkers Tea & Coffee partnered with Graphic Packaging International to launch sustainable paperboard canisters using 80% FSC-certified paperboard and 50% less plastic, indicating industry-wide shifts toward sustainable packaging that create opportunities for concentrate producers to differentiate through environmental benefits.

- June 2024: Nestlé launched Nescafé Espresso Concentrate in Australia with plans for global rollout, representing a major brand investment in concentrate innovation and market development that validates the segment's growth potential and competitive importance.

Global Coffee Concentrate Market Report Scope

| Caffeinated Concentrates |

| Decaffeinated Concentrates |

| Black Coffee Concentrate |

| Cold Brew Coffee Concentrate |

| Espresso Concentrate |

| Specialty Flavor Concentrates |

| Original |

| Flavored |

| Foodservice | Resturants |

| Cafes | |

| Others | |

| Food and Beverage Manufacturers | |

| Retail/Household |

| Bottles (Glass and PET) |

| Bag-in-Box |

| Pouches and Sachets |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Coffee Concentrate Type | Caffeinated Concentrates | |

| Decaffeinated Concentrates | ||

| By Product Type | Black Coffee Concentrate | |

| Cold Brew Coffee Concentrate | ||

| Espresso Concentrate | ||

| Specialty Flavor Concentrates | ||

| By Flavor Profile | Original | |

| Flavored | ||

| By End-User | Foodservice | Resturants |

| Cafes | ||

| Others | ||

| Food and Beverage Manufacturers | ||

| Retail/Household | ||

| By Packaging Format | Bottles (Glass and PET) | |

| Bag-in-Box | ||

| Pouches and Sachets | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the global coffee concentrate market by 2031?

The coffee concentrate market size is forecast to reach USD 3.74 billion by 2031, supported by a 6.12% CAGR.

Which product type leads overall sales today?

Cold-brew coffee concentrate currently holds the largest share at 46.21% thanks to its smooth flavor and high extraction strength.

Why are bag-in-box packages popular with restaurants?

Bag-in-box formats lower storage space needs, cut carbon emissions by up to 68%, and protect product quality through oxygen-barrier liners.

Which region is expected to grow the fastest through 2031?

Asia Pacific is set to expand at a 7.45% CAGR as urban consumers in China, India, and Southeast Asia adopt café-style drinks at home.

Page last updated on: