Graphene Battery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

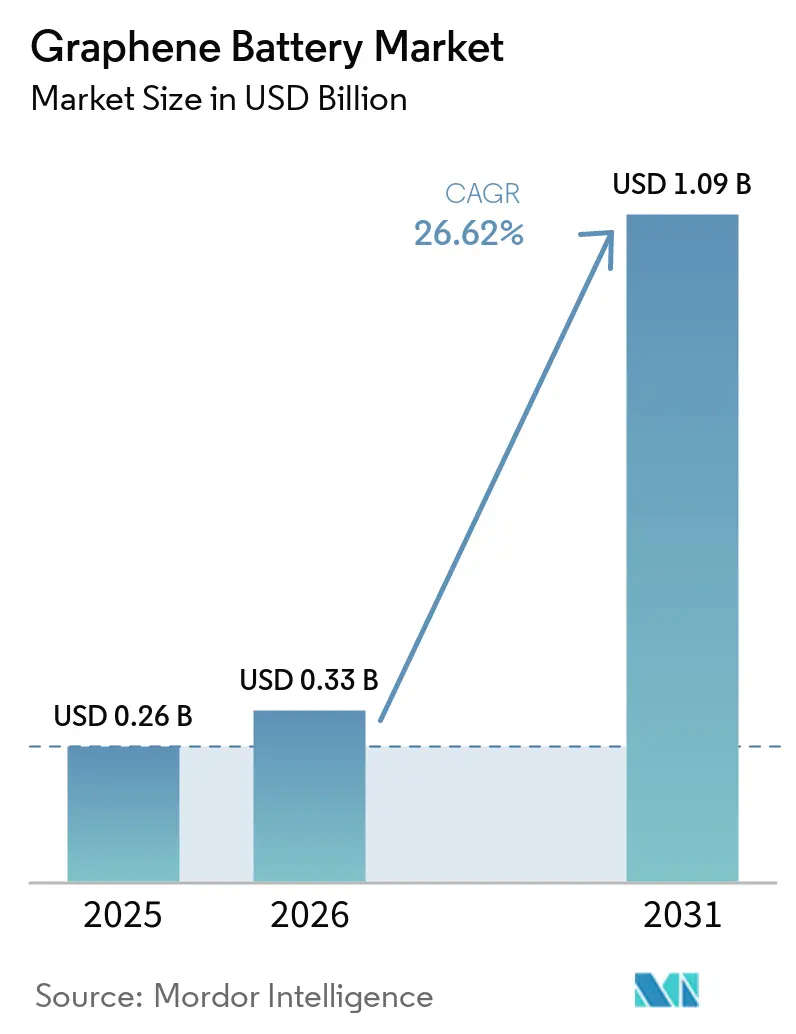

| Market Size (2026) | USD 0.33 Billion |

| Market Size (2031) | USD 1.09 Billion |

| Growth Rate (2026 - 2031) | 26.62% CAGR |

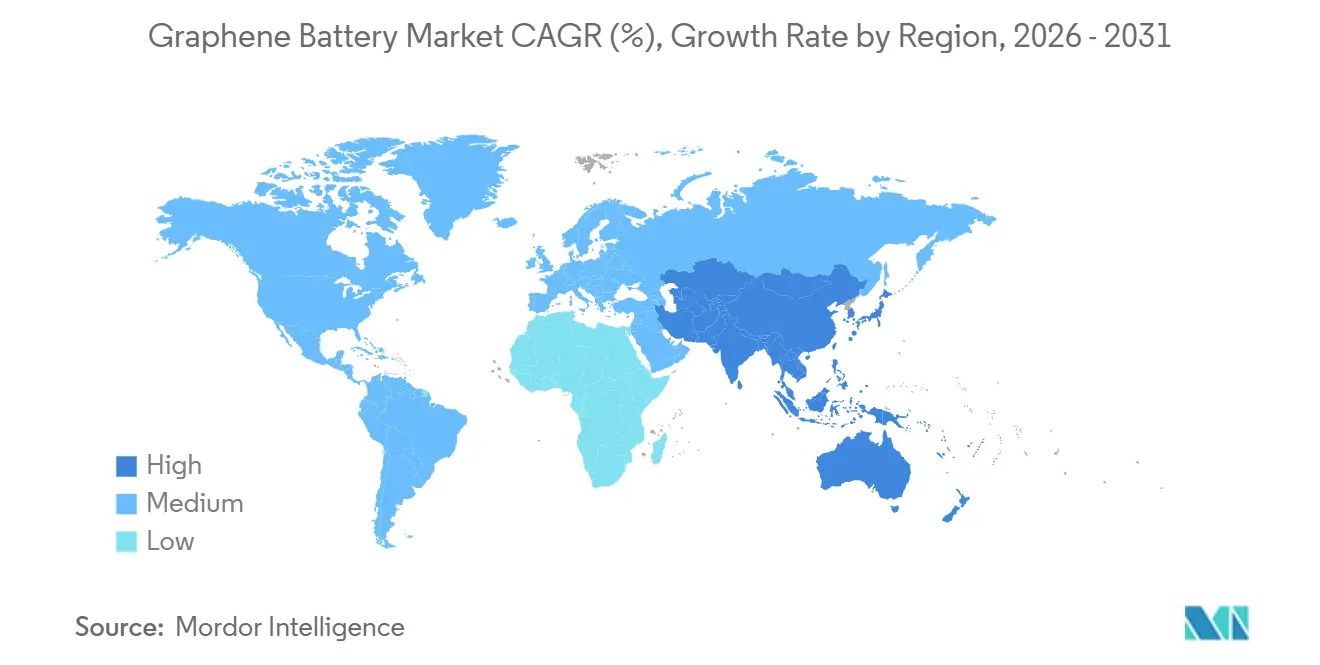

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Graphene Battery Market Analysis by Mordor Intelligence

The Graphene Battery Market size is projected to be USD 0.26 billion in 2025, USD 0.33 billion in 2026, and reach USD 1.09 billion by 2031, growing at a CAGR of 26.62% from 2026 to 2031. Rapid policy-driven electrification in China, the EU, and California is compressing acceptable EV charging windows, which in turn accelerates the adoption of graphene-enhanced electrodes that combine high energy density with supercapacitor-level charge acceptance. Defense and aerospace programs, such as the U.S. Navy’s SBIR Phase II contract for holey-graphene anodes, are validating the technology in weight-sensitive, high-power platforms. Public funding from the U.S. Department of Energy’s USD 4 million grant to Lyten to the EU’s EUR 4.5 million GRAPHERGIA project is lowering pilot-scale risk while helping localize supply chains. Meanwhile, falling production costs from electrochemical exfoliation and methane-decomposition routes are bringing graphene additives within cost parity of carbon black, removing a key barrier for tier-one cell makers.

Key Report Takeaways

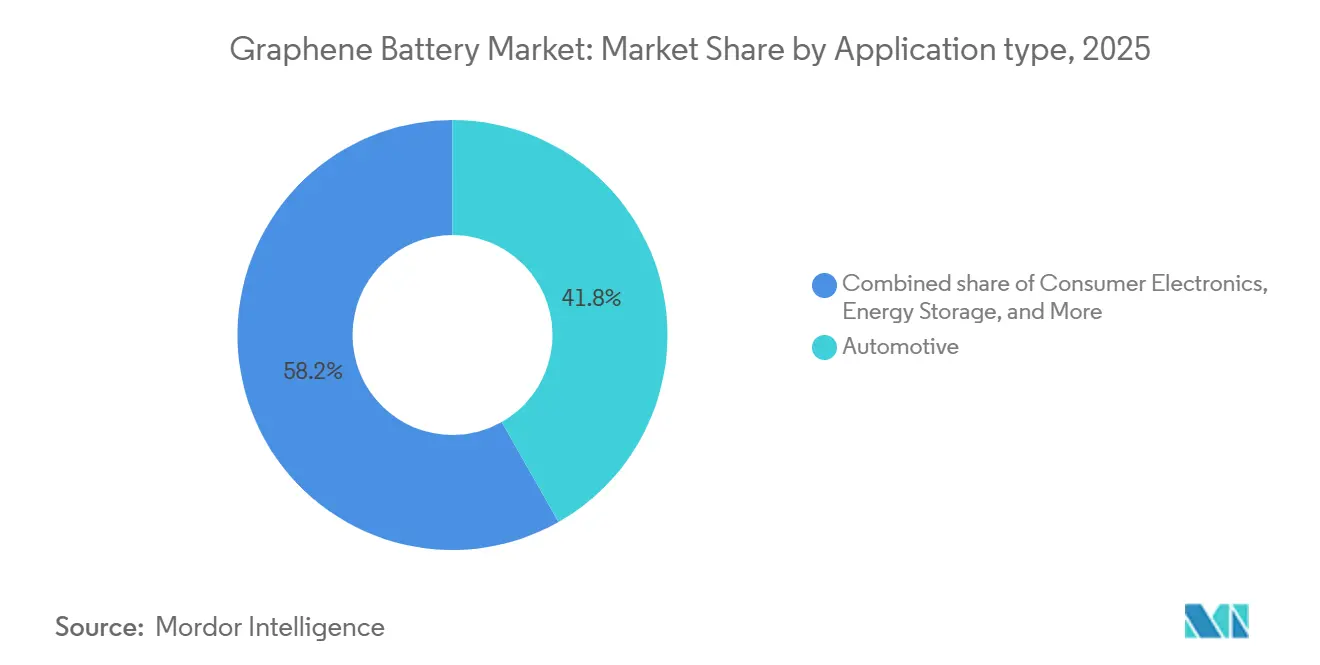

- By application, automotive led with 41.8% revenue share in 2025, while energy storage is projected to expand at a 31.5% CAGR through 2031.

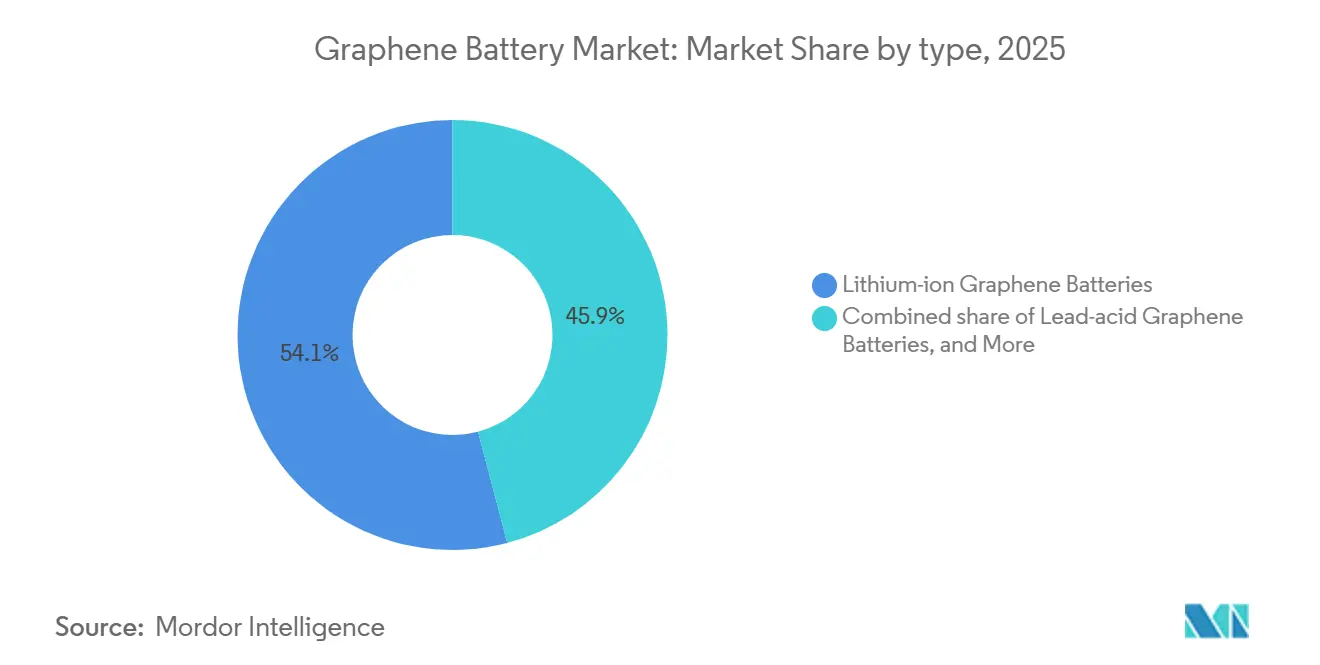

- By battery chemistry, lithium-ion graphene variants held 54.1% of the graphene battery market share in 2025, whereas solid-state graphene batteries are poised for a 37.0% CAGR to 2031.

- By region, Asia-Pacific accounted for 44.9% share of the graphene battery market size in 2025 and is forecast to grow at a 27.8% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Graphene Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-led demand acceleration | +6.8% | Global, with concentration in China, EU, and California | Medium term (2-4 years) |

| Superior energy density & ultra-fast charging | +5.2% | Global, early adoption in Asia-Pacific and North America defense | Short term (≤ 2 years) |

| Government R&D funding incentives | +3.9% | North America, EU, select Asia-Pacific (Australia, South Korea) | Medium term (2-4 years) |

| Declining graphene production costs | +4.1% | Global, led by China and emerging India capacity | Long term (≥ 4 years) |

| Integration with solid-state battery architectures | +3.5% | Asia-Pacific (China, South Korea, Japan), North America | Long term (≥ 4 years) |

| High-power UAV & aerospace adoption | +2.0% | North America, Europe (defense procurement), emerging Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV-led Demand Acceleration

Zero-emission mandates such as China’s dual-credit policy, the EU’s 2035 engine phase-out, and California’s Advanced Clean Cars II rule are forcing automakers to meet 80% state-of-charge targets in under 20 minutes [1]Electrive, “CATL Solid-State Patent Filing,” electrive.com. Graphene lowers charge-transfer resistance, enabling 3C-plus currents without runaway heat. A March 2026 simulation of a Tata Nexon EV showed 22-27% faster charging and up to 15 °C lower cell temperatures when graphene was added. Samsung’s graphene-ball-coated NCM cathode retained 97.3% capacity after 100 cycles at 4.5 V, confirming durability under high power [2]HackerNoon, “Samsung Graphene-Ball Cathode Study,” hackernoon.com. Fleet operators benefit because smaller packs or opportunity charging cut payload weight and idle time. Together, these factors position the graphene battery market as a near-term enabler for regulatory compliance and total-cost-of-ownership goals.

Superior Energy Density & Ultra-Fast Charging

Graphene’s 2,630 m²/g surface area and carrier mobility above 10,000 cm²/V·s simultaneously raise active-material loading and electron transport. Monash University’s multiscale reduced graphene oxide supercapacitor delivered 99.5 Wh/L and 69.2 kW/L, rivaling lead-acid while keeping supercapacitor power. A January 2026 laser-prelithiated silicon-graphene anode surpassed 1,700 mAh/g at 5 A/g with <2% fade over 2,000 cycles. GMG’s aluminum-ion pouch cell hit 62% charge in 3.2 minutes and targets a full 6-minute charge, demonstrating how graphene opens non-lithium chemistries at lower cost. These milestones prove that graphene not only upgrades lithium-ion but also unlocks alternative chemistries.

Government R&D Funding Incentives

The U.S. DOE’s USD 4 million award to Lyten aims to commercialize 3D-graphene lithium-sulfur cells and reduce nickel/cobalt dependence. Canada’s Energy Innovation Program granted NanoXplore up to USD 1.97 million for ultra-high-power cylindrical cells. Australia’s Queensland government co-funded GMG’s aluminum-ion pilot plant with USD 1.41 million. EU’s GRAPHERGIA allocates USD 5.18 million to flexible supercapacitor pilot lines. These subsidies de-risk pilot infrastructure and attract private capital, accelerating the graphene battery market trajectory.

Declining Graphene Production Costs

Electrochemical exfoliation now yields few-layer graphene at up to 60% with controllable oxygen content, cutting costs below USD 40/kg. The U.S. Air Force funds Skynano to convert captured CO₂ into battery-grade graphite, pairing sustainability with cost reduction. GMG’s methane-decomposition process co-produces hydrogen, enhancing economics. As volumes rise, adding 1-5 wt% graphene converges toward the cost of carbon black, incentivizing incumbent cell makers to test graphene at the gigawatt-hour scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of graphene materials | -4.5% | Global, most acute in price-sensitive consumer electronics and entry-level EVs | Short term (≤ 2 years) |

| Limited commercial-scale manufacturing capacity | -3.2% | Global, particularly North America and Europe lacking integrated graphene-to-cell lines | Medium term (2-4 years) |

| Inconsistent quality in CVD graphene flakes | -2.8% | Global, affecting all chemistries relying on CVD-sourced material | Short term (≤ 2 years) |

| Environmental & safety concerns over nano-emissions | -1.9% | EU and North America (stringent occupational health regulations), emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Graphene Materials

High-purity graphene still doubles electrode additive cost, squeezing margins in entry-level EVs and consumer electronics. CATL noted in 2025 that sulfide solid-state cells with advanced materials run 3-5 times the cost of conventional lithium-ion. Until reduced graphene oxide reaches parity with carbon nanotubes, likely by 2028, adoption will cluster in premium niches and curb the graphene battery market expansion by roughly 4.5 percentage points.

Limited Commercial-Scale Manufacturing Capacity

GMG is still optimizing 1,000 mAh pouch prototypes before publishing repeatable metrics. Lyten operates a semi-automated pilot line but will not ship automotive cells until later in the decade. Asia has integrated supply chains that can trial graphene quickly, but Western gigawatt-hour capacity lags, creating a chicken-and-egg standoff that slows graphene battery market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Solid-State Chemistries Outpace Conventional Hybrids

Lithium-ion graphene batteries held 54.1% revenue share in 2025, underlining the preference for incremental 1-5 wt% graphene additives in established NCM and LFP lines. Solid-state variants, though nascent, are forecast to expand at a 37.0% CAGR because graphene coatings stabilize sulfide electrolytes and suppress dendrites, raising cell energy toward 500 Wh/kg targets.

Graphene supercapacitors occupy a small yet strategically important corner of the graphene battery market. Monash University’s 99.5 Wh/L pouch cell proves volumetric energy can rival lead-acid while delivering 69.2 kW/L power. Emerging aluminum-ion and lithium-sulfur chemistries form the “Others” bucket; GMG’s aluminum-ion pouch cell charges in six minutes, and Lyten’s 3D-graphene lithium-sulfur cathodes shipped for automotive tests in 2024. As integration techniques mature, the graphene battery market size for these alternative chemistries is expected to widen, offering diversified revenue streams beyond conventional lithium-ion.

By Application: Energy Storage Cycles Drive Supercapacitor Adoption

Automotive dominated 41.8% of 2025 revenue, yet utility-scale energy storage is the quickest climber, advancing at a 31.5% CAGR on the back of supercapacitors that cycle multiple times daily without significant capacity fade. Grid-level installations leverage graphene’s tolerance for −10 °C to 80 °C swings, ideal for frequency regulation in high-renewable mixes.

Industrial robotics, power tools, and regenerative braking systems in commercial vehicles exploit graphene’s high power density and low ESR to capture transient energy. Aerospace and defense volumes remain small but validate safety and cycle-life claims under extreme conditions, helping de-risk subsequent mass-market launches. Wearable electronics and e-textiles, demonstrated by the EU GRAPHERGIA self-charging fabric, provide new outlets where flexible, thin-film storage trumps raw capacity. Cumulatively, these dynamics reinforce the graphene battery market’s shift from a single dominant application toward a balanced demand portfolio.

Geography Analysis

Asia-Pacific generated 44.9% of global demand in 2025 and is projected to grow at 27.8% through 2031, thanks to integrated graphite mines, graphene synthesis, and cell assembly hubs in China and South Korea. CATL’s roadmap toward 500 Wh/kg solid-state prototypes by 2027 exemplifies how local champions use graphene to leapfrog performance ceilings.

North America trails in volume but leads in public funding. The U.S. DOE’s backing for Lyten’s lithium-sulfur pilot and the Air Force’s CO₂-to-graphite project indicate security-driven interest in supply diversification. Canada’s NanoXplore grant for ultra-high-power cylindrical cells further cements the region’s role in niche, high-value applications.

Europe positions itself through consortium funding like GRAPHERGIA, aiming to lift technology readiness from 3-4 to 5 via flexible supercapacitors and dry-electrode lithium-ion cells [3]Cordis, “GRAPHERGIA Consortium Details,” cordis.europa.eu. Australia’s Queensland program links critical mineral reserves to value-added aluminum-ion pilot plants, while India’s Production-Linked Incentive schemes draw domestic graphene suppliers into battery lines. Overall, the graphene battery market benefits from Asia’s scale, North America’s defense capital, and Europe’s regulatory and R&D pull.

Competitive Landscape

The Graphene Battery Market is moderately fragmented. Incumbents Samsung SDI, LG Energy Solution, CATL, Panasonic add small graphene percentages to existing lines, leveraging established gigawatt-hour capacities and customer bases [4]Korea IT Times, “Samsung SDI Gel Polymer Electrolyte Study,” koreaittimes.com. Venture-backed specialists Nanotech Energy, Skeleton Technologies, Lyten, and Graphene Manufacturing Group focus on ultra-fast charging, non-flammable electrolytes, or lithium-sulfur chemistries to capture premium niches.

Strategic moves feature vertical integration of graphene powder (NanoXplore), government-funded pilots (GMG in Queensland), and academic partnerships (Samsung SDI with Columbia University). Patent activity clusters around CVD quality control, anti-restacking coatings, and solvent-free dry electrodes; LG Energy holds 450+ dry-electrode patents adaptable to graphene composites.

Defense contracts, such as the U.S. Navy’s holey-graphene anode program and the Air Force’s CO₂-derived graphite initiative, fund early-stage scale-up that later migrates into commercial aerospace and high-performance automobiles. Competitive intensity will escalate as graphene prices align with carbon black and solid-state timelines compress toward the decade’s end, pushing the graphene battery market toward consolidation around process IP and supply agreements.

Graphene Battery Industry Leaders

Samsung SDI Co. Ltd.

LG Energy Solution Ltd.

Nanotech Energy Inc.

Skeleton Technologies OÜ

Contemporary Amperex Technology Co Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Graphene Manufacturing Group (GMG) unveiled a significant advancement in graphene battery technology. GMG announced it had successfully doubled the energy density of its Graphene Aluminium-Ion Battery (G+A Cells), all while keeping its ultra-fast charging target of approximately 6 minutes. This groundbreaking technology is being co-developed with the University of Queensland and has garnered backing from industry giant Rio Tinto.

- January 2025: The U.S. Department of Energy allocated USD 88 million for FY 2025 vehicle-technology research, earmarking funds for ultra-long-cycle batteries that leverage graphene materials.

- November 2024: Caltech researchers unveiled a scalable graphene-coating method for lithium-ion cathodes that doubles cycle life and enhances charge-rate capacity.

- March 2024: The Queensland government awarded USD 1.32 million to Graphene Manufacturing Group to advance a pilot plant for graphene battery production.

Global Graphene Battery Market Report Scope

A graphene battery is an energy storage device that integrates graphene, a highly conductive and ultra-thin carbon material, into traditional battery designs, typically lithium-ion. This integration enhances performance by enabling faster charging, higher energy capacity, longer lifespan, and better heat management.

The graphene battery market is segmented by type, application, and geography. By type, the market is segmented into lithium-ion graphene batteries, graphene supercapacitors, lead-acid graphene batteries, solid-state graphene batteries, and others. By application, the market is segmented into automotive, consumer electronics, energy storage, industrial robotics and machinery, aerospace and defense, and others. The report also covers the market sizes and forecasts for the global graphene battery market across major countries within key regions. For each segment, the market sizing and forecasts have been provided on the basis of value (USD).

| Lithium-ion Graphene Batteries |

| Graphene Supercapacitors |

| Lead-acid Graphene Batteries |

| Solid-state Graphene Batteries |

| Others |

| Automotive |

| Consumer Electronics |

| Energy Storage |

| Industrial Robotics and Machinery |

| Aerospace and Defense |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Lithium-ion Graphene Batteries | |

| Graphene Supercapacitors | ||

| Lead-acid Graphene Batteries | ||

| Solid-state Graphene Batteries | ||

| Others | ||

| By Application | Automotive | |

| Consumer Electronics | ||

| Energy Storage | ||

| Industrial Robotics and Machinery | ||

| Aerospace and Defense | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the graphene battery market?

The graphene battery market stands at USD 0.33 billion in 2026 and is set to reach USD 1.09 billion by 2031, reflecting a 26.62% CAGR from 2026-2031

Which application is expected to grow fastest?

Utility-scale energy storage leads with a projected 31.5% CAGR.

Which region dominates current demand?

Asia-Pacific held 44.9% of 2025 demand and remains the volume leader.

How do graphene batteries shorten EV charging times?

Graphene lowers internal resistance, enabling safe 3C-plus charging that cuts 80% SOC times to under 20 minutes.

What is the biggest cost barrier today?

High-purity graphene additives still cost 2-3 times more than carbon black, limiting mass adoption.

Page last updated on: