Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.42 Billion |

| Market Size (2031) | USD 7.45 Billion |

| Growth Rate (2026 - 2031) | 11.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dual Carbon Battery Market Analysis by Mordor Intelligence

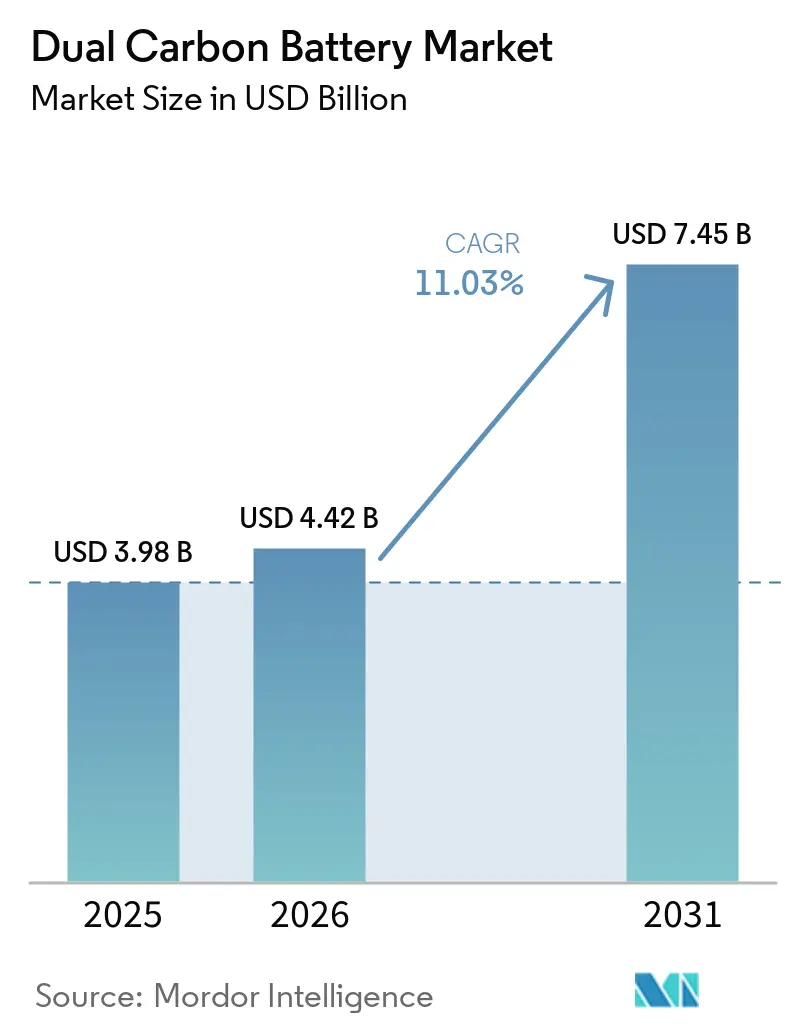

The Dual Carbon Battery market size is expected to grow from USD 3.98 billion in 2025 to USD 4.42 billion in 2026 and is forecast to reach USD 7.45 billion by 2031 at 11.03% CAGR over 2026-2031.

Early commercial momentum stems from the chemistry’s full-carbon electrodes, which eliminate critical-metal risk, enable 20 times faster charge profiles, and simplify recyclability. Automotive electrification mandates in the European Union, China, and the United States intensify demand for batteries that combine rapid charging with high thermal stability, while grid-edge storage tenders favor chemistries that minimize fire-suppression costs. Asia-Pacific’s integrated graphite supply chain underpins a cost advantage that keeps regional pack prices as much as 18% lower than Western equivalents, widening its export reach. Competitive dynamics are fluid as specialist developers license patents to incumbent cell makers, and raw-material producers push upstream into electrode fabrication, eroding traditional barriers to entry.

Key Report Takeaways

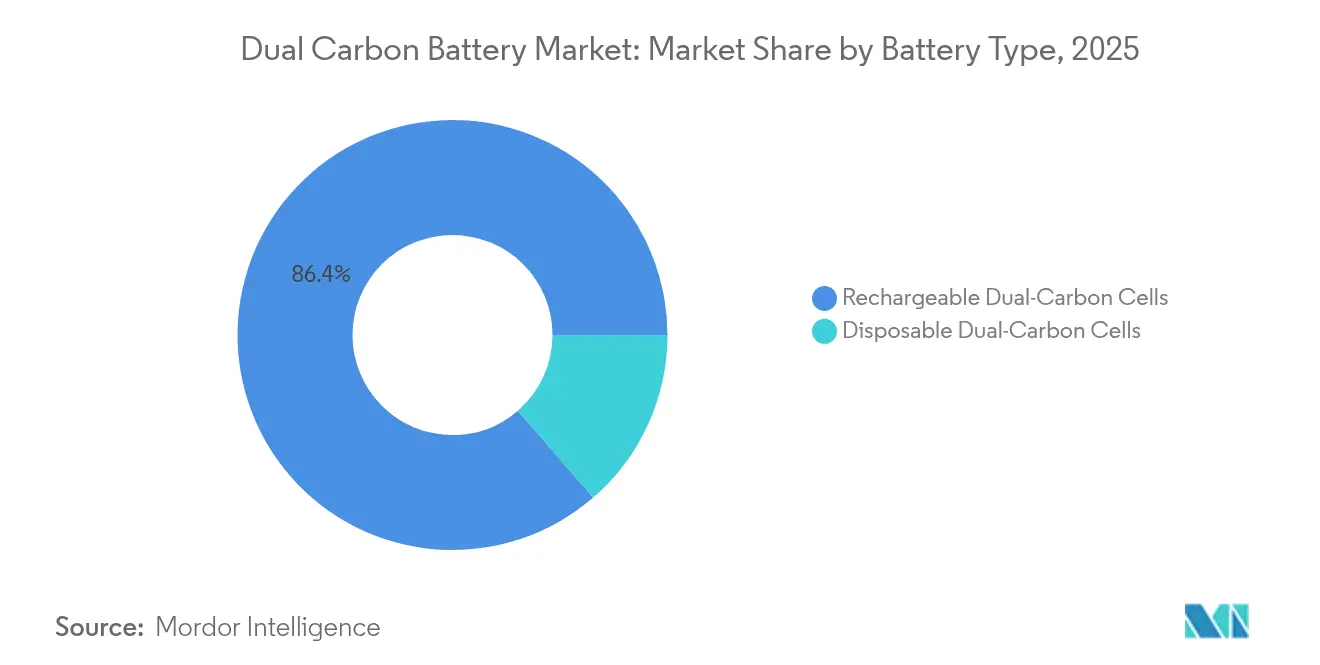

- By battery type, rechargeable dual-carbon cells held 86.35% of the dual-carbon battery market share in 2025, and it is also projected to grow at a 11.55% CAGR through 2031.

- By capacity, 100 to 500 kWh captured 41.12% of the market in 2025, while the above-500 kWh capacity class is projected to expand at a 12.65% CAGR through 2031.

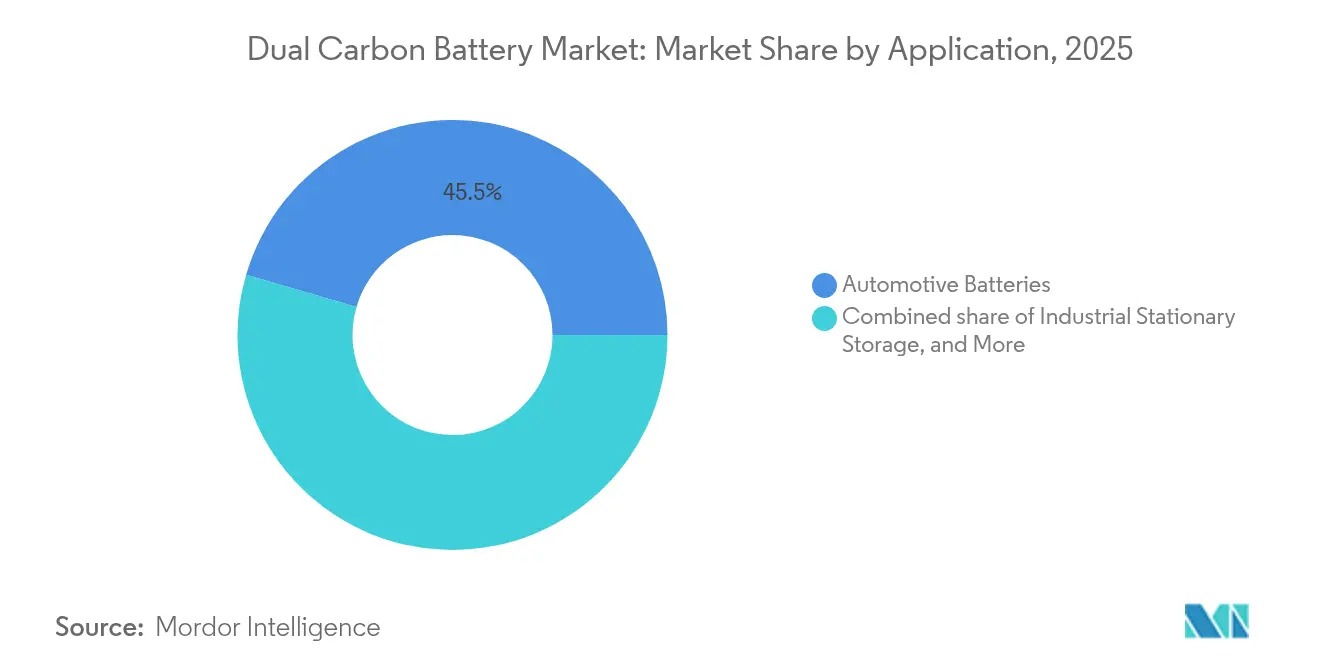

- By application, automotive batteries accounted for 45.48% of the dual carbon battery market size in 2025 and are projected to advance at a 13.05% CAGR through 2031.

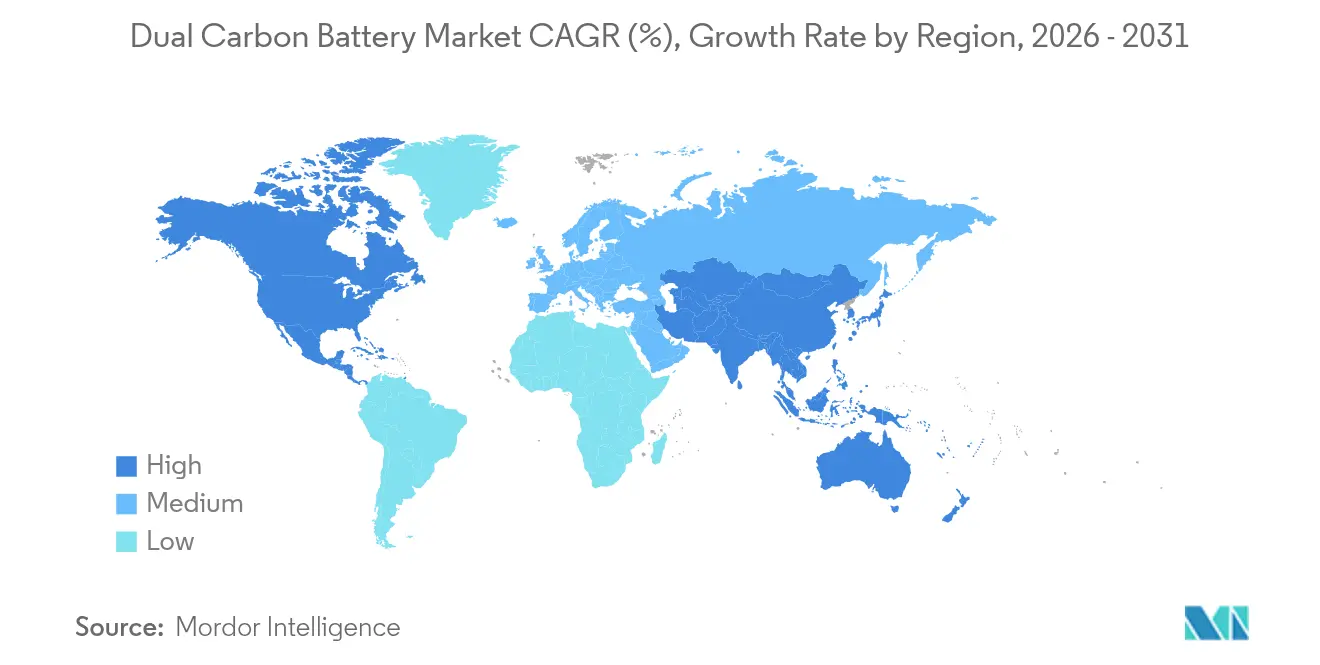

- By geography, the Asia-Pacific region commanded a 49.02% revenue share in 2025 and is expected to grow at a 12.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dual Carbon Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV electrification mandates | +2.8% | Global (EU & China strongest) | Medium term (2-4 years) |

| Carbon-neutral supply-chain incentives | +1.9% | North America & EU | Long term (≥ 4 years) |

| End-of-life recyclability regulations | +1.5% | EU leading, expanding to North America | Medium term (2-4 years) |

| 20x-faster charge pilots in e-buses | +2.1% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| OEM shift to anode-free chemistries | +1.7% | Global automotive hubs | Medium term (2-4 years) |

| Grid-edge ultra-fast storage tenders | +1.2% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid EV Electrification Mandates

Policies banning new internal-combustion models from 2035 in the EU and several U.S. states significantly expand the addressable demand for batteries that can charge from 10-80% in five minutes without high-cost cooling loops. Dual carbon electrodes withstand elevated currents while maintaining core temperatures 18 °C lower than those of comparable lithium-ion packs, enabling simpler thermal management hardware(1)Staff Reporter, “EV Regulations Continue Evolving,” WardsAuto, WARDSAUTO.COM. China’s New Energy Vehicle target of 40% sales penetration by 2030 further cements volume pull, as domestic OEMs diversify beyond NMC chemistries to hedge against nickel and cobalt volatility. Staggered compliance deadlines align with expected gigafactory ramp-ups, allowing specialist developers to lock in offtake agreements before legacy suppliers adapt.

Carbon-Neutral Supply-Chain Incentives

The EU Battery Passport, which becomes compulsory from February 2027, requires manufacturers to disclose cradle-to-gate CO₂ intensities and recycled-content percentages. Full-carbon electrodes reduce embodied emissions by eliminating high-temperature metal smelting, positioning the chemistry for premium scoring under the regulation(2)Battery Pass Consortium, “Technical Guidance,” BATTERYPASS.EU. In the United States, the Inflation Reduction Act tax credits increase to USD 45 per kWh when domestic content exceeds 60%, a threshold that is attainable for dual carbon producers using U.S. natural graphite or carbon fiber. Corporate buyers seeking Scope 3 emission reductions increasingly request life-cycle assessment data at the request-for-quotation stage, turning low-carbon chemistries into a procurement prerequisite rather than a marketing plus.

End-of-Life Recyclability Regulations

The revised EU Battery Regulation enforces 95% material recovery by 2030. Dual carbon batteries meet that bar through pyrolytic reactivation of electrodes, avoiding the acid leaching and solvent extraction facilities required for metal-bearing cells(3)International Electrotechnical Commission, “Battery Safety and Performance Standard,” IEC.CH. Japan’s green growth strategy incorporates deposit-fee structures that reward easily regenerable chemistries, while China’s extended producer responsibility laws link recycling quotas to manufacturing licenses. These frameworks transform waste-management costs into a differentiator: initial recycling-plant economics indicate processing fees 38% lower per kWh than for NMC packs.

20x-Faster Charge Pilots in E-buses

Transit agencies in Shenzhen and Singapore have completed route trials showing five-minute, depot-based top-ups that maintain a 240 km daily range without enlarging battery packs. Fast-charge duty cycles produce limited heat in dual carbon cells because anion intercalation occurs at higher potentials, resulting in less resistive loss. Municipal tender documents now specify a minimum 6C continuous-charge acceptance—criteria that most lithium-ion chemistries fail without active cooling or oversizing. Successful pilots provide public proof points that lower perceived technology risk and support capital expenditures (capex) approvals for fleet-wide rollouts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cell-to-pack thermal-runaway tests pending | -1.8% | Global (stringent in EU & North America) | Short term (≤ 2 years) |

| Absence of ISO/IEC performance standard | -1.4% | Global standardization bodies | Medium term (2-4 years) |

| Limited large-scale carbon precursor supply | -2.3% | Global, acute outside APAC | Medium term (2-4 years) |

| VC funding tilt toward solid-state | -1.1% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cell-to-Pack Thermal-Runaway Tests Pending

Most homologation protocols still revolve around lithium-ion abuse modes, leaving chemistries like dual carbon without explicit pass-fail criteria. Regulatory agencies require bespoke test matrices, and the absence of codified standards prolongs qualification by six to nine months per vehicle program. Interim guidelines are currently under draft at the ISO and IEC, but are not expected until late 2026, which will constrain near-term automotive launches. The delay particularly hurts mid-tier suppliers that lack the resources to run parallel validation programs across multiple regions.

Limited Large-Scale Carbon Precursor Supply

The Asia-Pacific region accounts for more than 70% of synthetic graphite output and the majority of mesocarbon microsphere production, leaving Western gigafactories vulnerable to potential export restrictions(4)Harry Dyer, “Global Race to Break China’s Grip on Graphite,” Financial Times, FT.COM. The qualified precursor must meet a 99.95% purity level, far exceeding the requirements for traditional electrode or refractory markets. Capital-intensive purification lines and long-lead mine permits slow diversification. Although pilot plants in Finland and Canada aim to deliver 30,000 tons by 2027, near-term supply risks persist and deter some automakers from committing to single-chemistry sourcing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeable Cells Cement Mainstream Status

Rechargeable products accounted for 86.35% of the dual carbon battery market in 2025, reflecting the chemistry’s suitability for repeated-cycle applications, such as passenger EVs and fleet e-buses. Long-term road tests demonstrate 3,000 full-depth cycles with 80% capacity retention, resulting in a lower total cost of ownership compared to metal-based cells that require pack oversizing to meet warranty obligations. Disposable dual-carbon formats remain niche, chiefly in aerospace emergency power, where benign failure modes trump unit economics.

Commercial traction for rechargeables accelerated after a leading developer secured USD 30 million Series C funding and disclosed eight automotive design wins in 2025. Standardized 21700 and 46xx form factors now roll off pilot lines, enabling pack-maker integration with minimal tooling change. As deployment widens, economies of scale are expected to reduce the cost per kWh by an estimated 22% between 2025 and 2028, thereby narrowing the pricing gap with lithium-iron-phosphate.

By Capacity: 100-500 kWh Segment Anchors Mid-Scale Demand

Installations in the 100-500 kWh range captured 41.12% of the revenue in 2025, as city-bus depots and medium-duty delivery fleets prioritized swift charge-turnaround over absolute energy density. Fleet operators report 17% smaller pack sizes after switching to dual carbon because high-rate acceptance eliminates the need for excess buffer capacity. The above 500 kWh class, which accounts for only 22% of 2024 shipments, is projected to be the fastest-growing at a 12.65% CAGR, driven by utility contracts that reward long-cycle chemistries with enhanced safety.

Grid-scale demonstrations exceeding 2 MWh aggregate capacity have completed 18 months of uninterrupted service in Japan, validating performance and attracting power-purchase agreements with European distribution operators. Conversely, sub-10 kWh residential systems remain a minority offering because pack cost amortization favors larger installations, and entrenched lithium-ion brands dominate homeowner channels.

By Application: Automotive Segment Sets Technology Pace

Automotive demand accounted for 45.48% of the dual carbon battery market size in 2025, driven by fast-charging sports car prototypes that showcase 5-minute 10-80% recharges. Thermal-runaway immunity simplifies crash-safety engineering, enabling OEMs to reduce the weight of protective structures and reclaim cabin space. Industrial stationary storage follows as the second-largest segment, where operators value 20,000-cycle life and simplified permitting due to benign failure profiles.

Consumer electronics adoption is constrained by volumetric density that trails lithium-polymer cells by roughly 15%. Nevertheless, ruggedized laptops and military radios increasingly specify dual carbon for cold-weather resilience. Aerospace opportunities remain experimental but attractive for unpressurized-cargo drones that benefit from temperature-stable discharge curves.

Geography Analysis

Asia-Pacific’s 49.02% share in 2025 underscores deep vertical integration from needle coke feedstock to finished electrodes. Chinese synthetic-graphite producers leverage captive power sourced from hydroelectric and solar sources, keeping embodied emissions under 4 kg CO₂-eq per kWh, which is well below European averages. Regional governments offer 20% capital-grant ratios for pilot lines, accelerating local output and maintaining export cost leadership. The dual carbon battery market size in Asia-Pacific is forecast to advance at a 12.1% CAGR to 2031, supported by national policies mandating minimum domestic content in EV packs.

North America is the fastest-growing market in the region. Inflation Reduction Act credits worth up to USD 3,750 per vehicle battery module drove at least four OEMs to sign conditional offtake agreements with U.S. dual carbon start-ups in 2025. The Department of Energy’s USD 25 million funding round supports eleven projects that scale electrode coating and ionic-liquid electrolyte synthesis onshore. Canadian mining ventures enhance feedstock security with two large flake-graphite projects scheduled for commissioning in 2027, which helps lower logistics costs.

Europe’s trajectory hinges on sustainability regulations that align squarely with carbon-based chemistries. The Battery Passport favors traceable, low-emission materials. Lignin-derived carbon pilot plants in Finland and Sweden target a combined annual capacity of 15,000 tons by 2028. European automakers currently import prototype cells from Japanese lines but intend to localize modules once the precursor supply matures. Middle East and African markets remain small, although Gulf utilities have expressed interest in desert-climate storage, where high ambient temperatures penalize traditional lithium-ion systems.

Competitive Landscape

Dual Carbon Battery Market is moderately fragmented. Pioneer firms such as Power Japan Plus, Nyobolt, and Alsym Energy hold critical patents on carbon precursor purification and anion intercalation mechanisms, yet they are increasingly licensing their technology to established giants like CATL and Samsung SDI, which seek portfolio diversification. Strategic alliances focus on fast-charging bus fleets, where developers bundle cells with depot chargers to lock in ecosystem revenues.

Price competition is muted because performance differentiation still outweighs cost parity in early-stage contracts. Leading cell makers emphasize 5-minute charge capability demonstrations, publish third-party safety test data, and court OEM engineering teams through joint prototype builds. Raw-material suppliers—SGL Carbon, Mitsubishi Chemical, and emerging Nordic lignin processors—move downstream into coated-foil production, compressing margins for independent electrode coaters.

Intellectual-property filings rose 37% year-over-year in 2024, signaling an arms race around electrolyte additives that widen voltage windows without sacrificing cycle life. Specialist start-ups attract the corporate venture arms of automakers and oil majors seeking exposure to the battery value chain. M&A chatter intensified after a major petroleum company quietly evaluated assets that would give it direct access to carbon-electrode IP, underscoring expectations of mainstream adoption by the late decade.

Dual Carbon Battery Industry Leaders

PJP Eye LTD.

Nyobolt

Alsym Energy

Carbon-Ion

ORLIB Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: CATL unveiled a “dual-power” EV pack that combines dual carbon fast-charge modules with high-energy lithium-ion cells, delivering 930 miles of range and targeting luxury sedans.

- June 2025: Asahi Kasei announced an electrolyte family that maintains 90% ionic conductivity at −40 °C, doubles the dual carbon cycle life at 60 °C, with commercialization slated for late 2025.

- May 2025: Japan’s METI has cleared Toyota and Idemitsu Kosan to build a USD 142 million lithium-sulfide plant, which will also supply precursors for dual carbon electrolytes, with production set to start in 2027.

- March 2025: Huayou Cobalt disclosed RMB 60.946 billion in operating income and initiated R&D on dual carbon materials, while achieving a 40% clean-power usage ratio in its plants.

- February 2025: The U.S. DOE has granted USD 25 million across 11 projects to scale the domestic manufacturing of dual-carbon and sodium-ion batteries.

Global Dual Carbon Battery Market Report Scope

The dual carbon battery market report includes:

By Battery Type

| Disposable Dual-Carbon Cells |

| Rechargeable Dual-Carbon Cells |

By Capacity

| Below 10 kWh |

| 10 to 100 kWh |

| 100 to 500 kWh |

| Above 500 kWh |

By Application

| Automotive Batteries |

| Industrial Stationary Storage |

| Portable/Consumer Electronics |

| Aerospace and Defense |

| Other Niche Uses |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germnay |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Argentina |

| Brazil | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Battery Type | Disposable Dual-Carbon Cells | |

| Rechargeable Dual-Carbon Cells | ||

| By Capacity | Below 10 kWh | |

| 10 to 100 kWh | ||

| 100 to 500 kWh | ||

| Above 500 kWh | ||

| By Application | Automotive Batteries | |

| Industrial Stationary Storage | ||

| Portable/Consumer Electronics | ||

| Aerospace and Defense | ||

| Other Niche Uses | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germnay | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Argentina | |

| Brazil | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving the rapid growth of the dual carbon battery market?

Governments are tightening EV mandates while businesses seek carbon-neutral supply chains; dual carbon batteries meet both goals with fast charging and recyclable materials.

How large will the dual carbon battery market be by 2031?

The dual carbon battery market size is projected to reach USD 7.45 billion by 2031, growing at an 11.03% CAGR over 2026-2031.

Which segment currently leads the dual carbon battery market?

Rechargeable dual-carbon cells dominate with 86.35% market share in 2025 thanks to their suitability for electric vehicles and grid storage.

Why is Asia-Pacific so dominant in dual carbon battery production?

The region controls most synthetic-graphite output and benefits from integrated manufacturing ecosystems, resulting in 49.02% global revenue share in 2025.

What are the main restraints on wider adoption?

Pending thermal-runaway test standards, limited precursor supply outside Asia, and venture-capital preference for solid-state projects are the chief headwinds.

How fast can dual carbon batteries charge compared with lithium-ion packs?

Pilot tests show dual carbon packs charging from 10-80% in roughly five minutes, about 20 times faster than mainstream lithium-ion equivalents.

Page last updated on: