Thin Film Battery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 315.68 Million |

| Market Size (2031) | USD 774.45 Million |

| Growth Rate (2026 - 2031) | 19.66% CAGR |

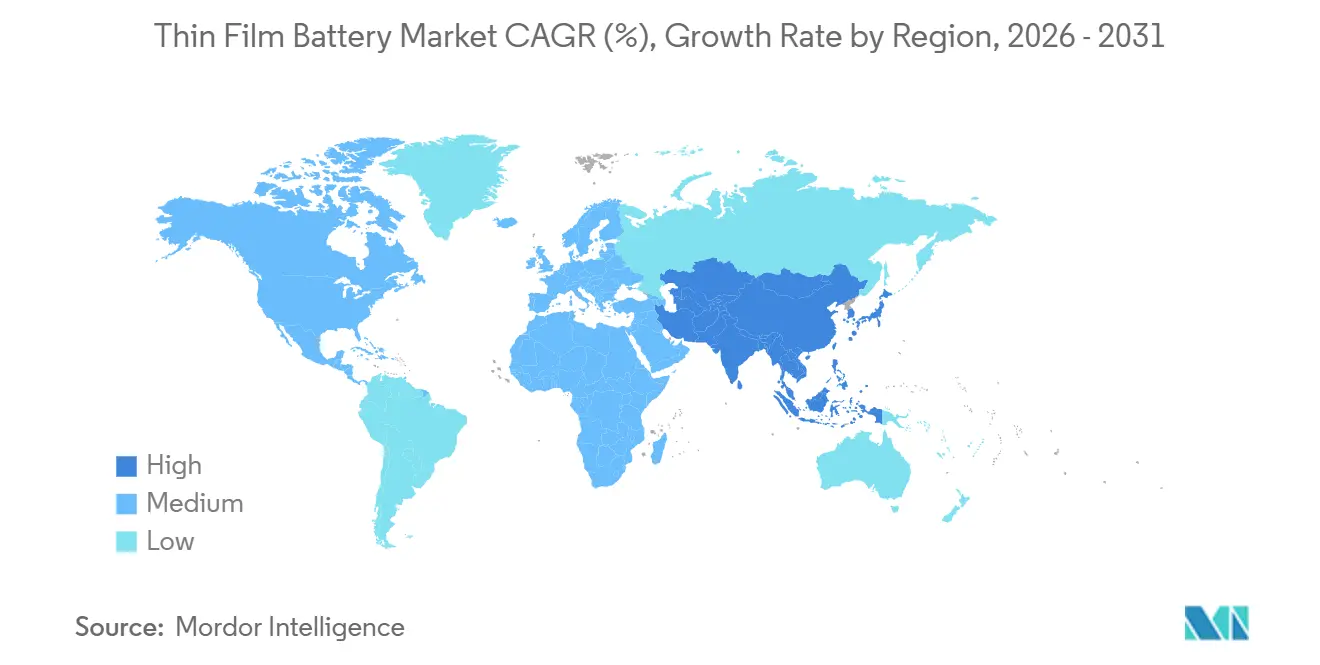

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

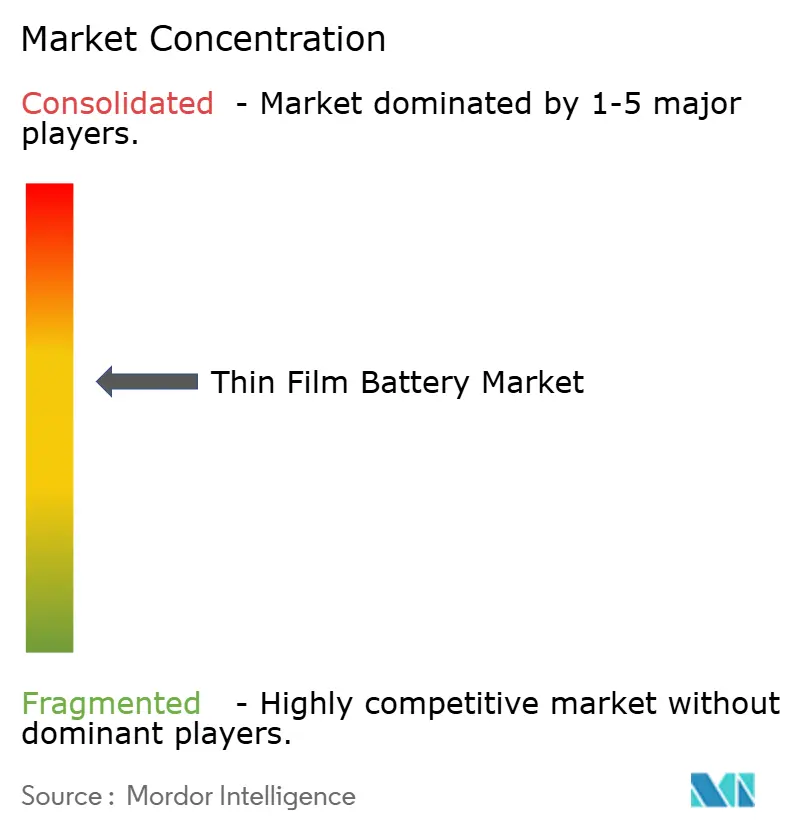

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thin Film Battery Market Analysis by Mordor Intelligence

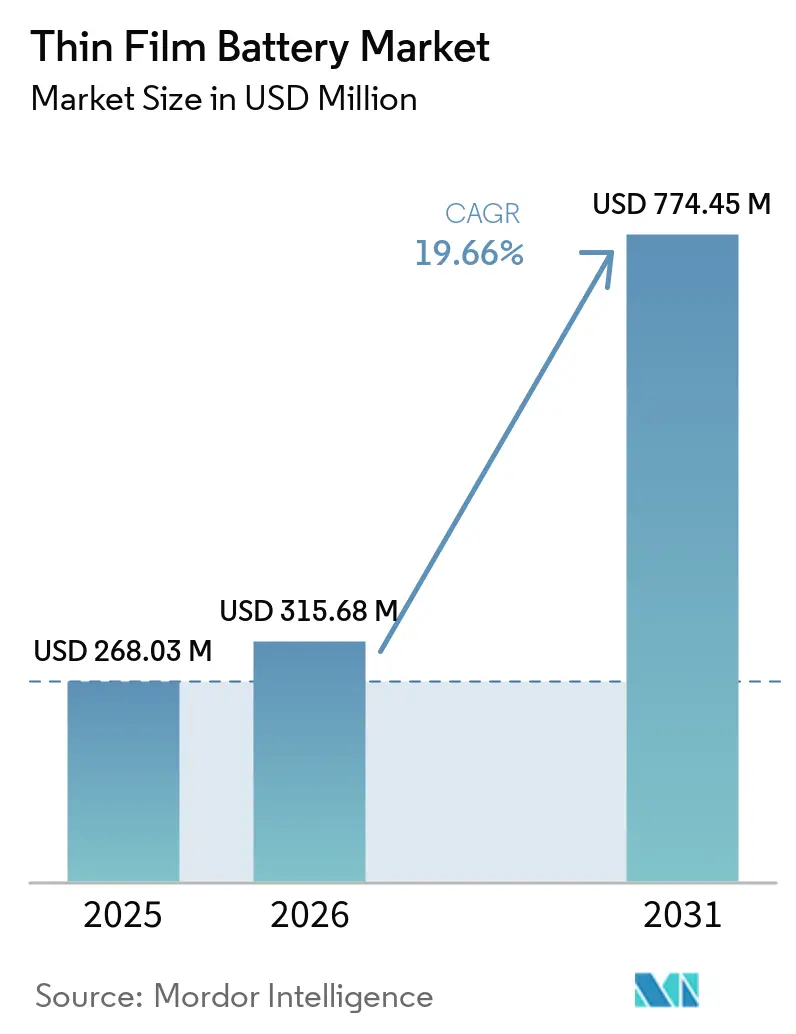

The Thin Film Battery Market size is projected to expand from USD 268.03 million in 2025 and USD 315.68 million in 2026 to USD 774.45 million by 2031, registering a CAGR of 19.66% between 2026 and 2031. Defense agencies, medical-device innovators, and consumer-electronics brands are converging on thin-film architectures because they allow sub-millimeter form factors, intrinsic solid-state safety, and high-speed charging. Soldier-worn power programs under DARPA, implantable stimulators qualified with solid-state micro-batteries, and smartwatch makers targeting <5 mm device thickness are the immediate demand catalysts. Roll-to-roll vacuum-deposition upgrades are driving down unit costs, making printed formats cost-competitive with legacy coin cells. Intellectual-property concentration around LiPON electrolytes and all-solid-state laminate stacks raises entry barriers yet signals technology maturity that attracts institutional capital. As traceability rules under the EU Batteries Regulation tighten after 2027, suppliers able to embed digital passports directly onto flexible cells are positioned for contractual preference.

Key Report Takeaways

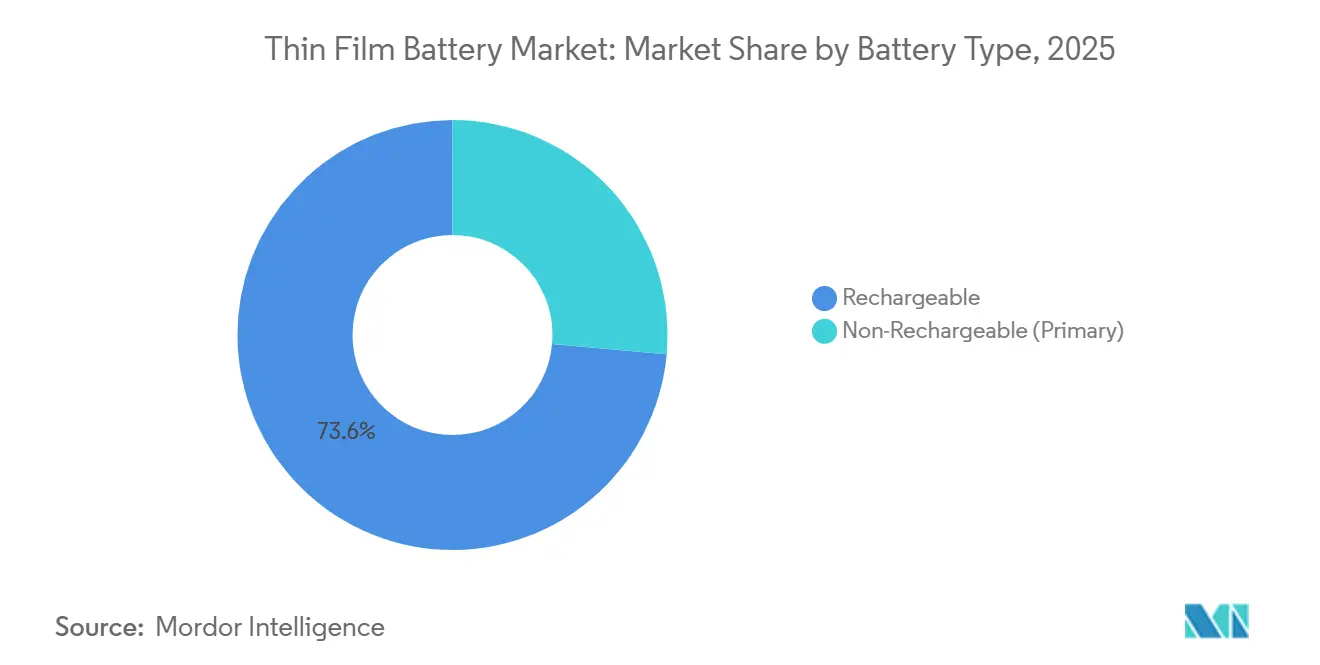

- By battery type, rechargeable cells held 73.57% of thin film battery market share in 2025 and are projected to expand at a 20.69% CAGR through 2031.

- By technology, printed batteries commanded 81.64% revenue share of the thin film battery market in 2025, while the segment is forecast to grow at 21.47% CAGR to 2031.

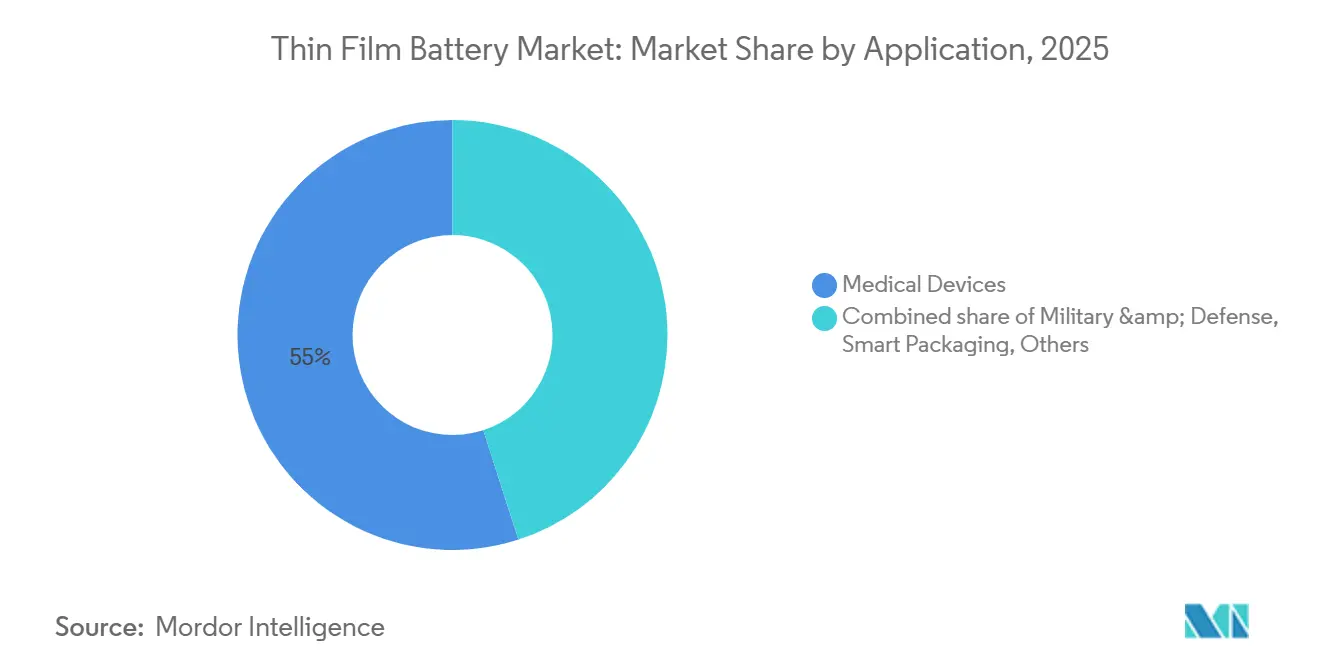

- By application, medical devices accounted for a 54.97% share of the thin film battery market size in 2025, and wearable technology is advancing at a 25.36% CAGR through 2031.

- By region, Europe led with 52.11% of 2025 revenues, while Asia-Pacific is registering the fastest growth at 22.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thin Film Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in wearable & IoT device production | +4.2% | Global, with APAC core and spill-over to North America | Medium term (2-4 years) |

| Miniaturization trend in consumer electronics | +3.8% | Global, led by North America & APAC | Short term (≤ 2 years) |

| Rising demand for solid-state micro-batteries in medical implants | +3.5% | North America & Europe | Medium term (2-4 years) |

| Roll-to-roll PVD scale-ups reducing per-unit costs | +2.9% | Europe & APAC manufacturing hubs | Long term (≥ 4 years) |

| Integration with energy-harvesting IIoT sensors | +2.1% | Global, early adoption in Europe & North America | Long term (≥ 4 years) |

| Defense funding for soldier-worn power sources & smart munitions | +1.8% | North America, selective adoption in Europe & Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Wearable & IoT Device Production

Global shipments of smartwatches, earbuds, service robots, and industrial sensors are creating sustained pull for sub-1 Ah planar cells. TDK’s thin-film inductors introduced for true-wireless-stereo earbuds make mechanical coin cells obsolete in devices where every cubic millimeter counts.[1]TDK Corporation, “Thin-Film Inductor Release,” evertiq.com Ensure batteries reach 90% charge in under 25 minutes, supporting daily-wear gadgets without bulky housings. Samsung SDI forecasts robot demand rising from 500,000 units in 2025 to 2.04 million by 2030, and it unveiled a solid-state pouch cell to serve that wave.[2]Samsung SDI, “All-Solid-State Prototype for Robots,” yonhapnews.co.kr Energy-harvesting modules such as Dracula Technologies’ LayerVault OPV sheets buffer intermittent power for logistics sensors, lifting thin film battery market volumes across consumer and industrial use cases. The synergy between ambient-light harvesters and flexible micro-cells underpins the replacement of CR2032 batteries in temperature loggers and asset tags.

Miniaturization Trend in Consumer Electronics

Device makers are setting chassis thickness targets below 5 mm for smart cards, AR glasses, and biometric tags, forcing a pivot to flat battery geometries. BTRY’s 1S4P cell, barely 0.1 mm thick yet delivering 50 mAh in one-minute charges, exemplifies innovation that unlocks active security authentication inside ID cards.[3]BTRY AG, “Seed Funding Announcement,” btry.ch Planar cells laminate directly onto flex circuits, skip wire-bond fixtures, and cut assembly time, giving OEMs a compelling cost-of-ownership story even when volumetric energy is lower than 18650 standards. The design freedom enables curved smartwatch backs and bezel-less displays while maintaining device rigidity. Because the operating profile is intermittent rather than continuous, consumers accept daily re-charging in exchange for lighter wearables, driving repeat orders across the thin film battery market.

Rising Demand for Solid-State Micro-Batteries in Medical Implants

Regulatory open-door policies for solid-state chemistries remove concerns over electrolyte leakage in Class II implantables. Ilika’s Stereax M300, qualified in 2025, powers peripheral nerve stimulators and continuous glucose monitors with predictable discharge curves over ten-year implant lives.[4]Ilika PLC, “Goliath Pilot Line Commissioning,” ilika.com The FDA has shaved roughly six months off 510(k) clearances for devices employing solid-state cells, encouraging OEM pipeline expansion. Bioresorbable zinc-based thin-film batteries position startups for transient wound-care sensors that safely dissolve after therapy completion. Predictable voltage output simplifies firmware design, cutting validation cycles and giving incumbents a head-start against emerging sodium-ion microsystems. Together, these factors enlarge the thin film battery market among medical OEMs seeking miniaturized, safe, and maintenance-free power sources.

Roll-to-Roll PVD Scale-Ups Reducing Per-Unit Costs

Equipment vendors are adapting semiconductor deposition tools for continuous web processing, achieving 2 µm/h spatial ALD and 1 µm/s e-beam titanium sputtering that slashes tack times. BTRY’s solvent-free roll-to-roll lines eliminate drying ovens, cutting energy use 30% and pushing consumable yield above 90%. Ilika’s pilot facility reached 93% first-pass yield on 10 Ah prototypes, confirming scalability metrics attractive to automotive Tier-1 suppliers. High European labor costs become less punitive as automation density rises, narrowing Asia’s wage advantage and spurring regional diversification of thin film battery market capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of alternative battery chemistries | -2.3% | Global, with stronger substitution in APAC cost-sensitive segments | Medium term (2-4 years) |

| Limited energy density versus bulk Li-ion batteries | -2.0% | Global | Short term (≤ 2 years) |

| High CAPEX for vacuum deposition tooling | -1.7% | Europe & North America manufacturing hubs | Long term (≥ 4 years) |

| LiPON electrolyte patent bottlenecks | -1.2% | Global, concentrated in North America & Europe IP jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Energy Density Versus Bulk Li-ion Batteries

Thin-film cells provide 100-200 Wh/L, about one-third of advanced 21700 cylindrical formats now touching 320 Wh/kg. Ionic conductivity in LiPON remains at the 10⁻⁶ S/cm level, capping discharge rates and precluding use in power tools. As EV-grade packs adopt silicon-graphite anodes, the performance contrast widens, making it harder for the thin film battery market to win long-duration or high-drain slots. Smartwatch makers chasing multiday runtimes sometimes revert to coin cells, and AR headset OEMs blend small lithium-polymer pouches for auxiliary loads. Composite electrolyte R&D could double conductivity, yet commercialization after 2027 offers no relief during the current forecast window.

High CAPEX for Vacuum Deposition Tooling

Laser pulsed-deposition units alone cost USD 100,000-750,000, with a modest 1.5 MWh pilot line totaling USD 8-12 million in capital before clean-room fit-out. Mid-tier entrants struggle to secure such funding, slowing ecosystem expansion and leaving production clustered around conglomerates capable of amortizing semiconductor fabs. Ceramic sputter targets run into the tens of thousands of dollars, and utilization often falls below 40%, inflating material cost curves. Roll-to-roll automation promises relief but demands process retooling that defers payback well beyond five years. In regions lacking subsidy frameworks, particularly North America and parts of Europe, these hurdles temper the otherwise robust thin film battery market growth outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeable Cells Extend Lead in Long-Cycle Use

Rechargeable thin-film cells accounted for 73.57% of 2025 revenue and are forecast to grow at 20.69% CAGR, reinforcing their dominance in the thin film battery market. This cohort benefits from smartwatch, humanoid-robot, and medical-implant workloads that demand thousands of charge cycles. Samsung SDI’s SolidStack prototypes deliver eight-hour duty cycles in service robots and promise fast top-ups during shift changes. Non-rechargeable primary cells still power disposable smart packaging where unit economics dictate pennies per label, yet their share in the thin film battery market is shrinking as IoT device operators calculate life-cycle cost advantages of rechargeability.

ISO/IEC 7810 durability tests and UN 38.3 transport certification shape R&D roadmaps, pushing vendors to validate thermal stability above 1,000 cycles and shelf life beyond five years. Defense logistics add momentum as the STUB standard adopts rechargeable formats to slash field battery shipments. Consequently, the thin film battery industry is funneling R&D budgets toward cycle-life extension through LiPON refinement and anode-free stack designs, reinforcing the share supremacy of secondary chemistries.

By Technology: Printed Formats Scale Fast on Cost and Flexibility

Printed batteries captured 81.64% of thin film battery market share in 2025 and will rise at 21.47% CAGR through 2031. Screen and inkjet techniques allow direct deposition onto paperboard and polymer films, fulfilling the EU digital battery-passport mandate from 2027 with serialized QR tags laminated into cartons. The thin film battery market size tied to printed lines is projected to jump as food-packaging schemes funded by NIFA move toward volume trials.

Ceramic thin-film batteries, prized for ≥150 °C tolerance, occupy niche industrial sensor applications. Lithium-polymer cells bridge flexibility and moderate capacity, feeding wearable-health patches that must bend with human skin. Solid-state chip batteries fabricated at wafer scale serve real-time clocks in micro-controllers but encounter wafer-cost ceilings that limit output. As scale economics overwhelmingly favor printability, roll-to-roll web widths wider than 600 mm are coming online, sharply trimming overhead and fortifying printed technology’s leadership in the thin film battery market.

By Application: Medical Devices Dominate While Wearables Accelerate

Medical devices brought in 54.97% of 2025 revenue, reflecting strict biocompatibility needs that only solid-state architectures satisfy. Implantable stimulators, drug pumps, and continuous glucose monitors hinge on predictable voltage curves over decadal lifetimes. Parallel momentum comes from bioresorbable sensors using zinc or magnesium anodes that dissolve harmlessly in vivo.

Wearable technology is registering the quickest climb at 25.36% CAGR, birthing a sizable slice of the upcoming thin film battery market size. TDK component miniaturization allows earbud cases to shrink 20% yet retain six-hour playback. Smart cards and RFID tags enjoy steady gains as fintech rolls out biometric verification, whereas military demand remains smaller in volume but lucrative in per-unit terms under DARPA’s Promethean Clay program. Smart packaging rockets from a low base as the FDA’s DSCSA mandates serialized pharma tracking, propelling printed cells embedded in NFC labels.

Geography Analysis

Europe generated 52.11% of thin film battery market revenue in 2025, underpinned by the EU Batteries Regulation (2023/1542) that enforces carbon-footprint disclosure and battery passports from 2027. Switzerland’s BTRY raised USD 5.7 million to industrialize solvent-free roll-to-roll solid-state cells, showing deep-tech vigor in the region. France’s ITEN and the UK’s Battery Industrialisation Centre pushed Ilika’s Goliath prototypes toward 93% pilot-line yield, anchoring supply resilience. Nordic producers tout hydropower-sourced electricity for low-carbon credentials, but mining permits for lithium and cobalt remain a bottleneck.

Asia-Pacific is the momentum engine, expanding at 22.35% CAGR and reshaping the thin film battery market landscape. Samsung SDI presented a pouch-type all-solid-state prototype for humanoid robots at InterBattery 2026 and owns about 1,100 patents, fortifying its moat. China scales printed-battery output for connected packaging under Made in China 2025 subsidies, while Japan’s TDK commercializes ceramic variants for industrial electronics. Vietnam and Thailand lure assembly capacity as diversification away from China accelerates, although upstream materials remain concentrated in Northeast Asia.

North America captures defense and med-tech niches within the thin film battery market. DARPA funding and Silicon Valley start-ups provide steady demand, while Amprius’ silicon-anode facility under NDAA alignment hints at onshoring synergies should thin-film versions mature. South America’s pilot projects in Brazilian smart agriculture and the Middle East’s oil-field IoT deployments use ceramic thin-film batteries for high-temperature resilience. Africa remains embryonic, though renewable-energy micro-grids may later seed sensor demand that benefits flexible micro-batteries.

Competitive Landscape

Competition in the thin film battery market sits at a moderate level as semiconductor giants, battery specialists, and materials innovators vie for a share. Samsung SDI leverages existing PVD lines, unveiling the SolidStack brand and amassing 1,100 all-solid-state patents to fence key architectures. STMicroelectronics and Panasonic exploit lithography heritage to co-integrate energy and IC packages, trimming BOM for IoT modules.

Start-ups fill white-space opportunities. BTRY’s ultra-thin, one-minute-charge cells address biometric smart cards; Ilika’s Goliath program scales 10 Ah to 50 Ah solid-state pouches for automotive telemetry; Ensurge targets hearables with sub-30-minute high-cycle offerings. Materials disruptors develop polymer-ceramic composite electrolytes aimed at boosting ionic conductivity beyond LiPON limits, while equipment firms license roll-to-roll blueprints to shorten plant ramps.

Regulatory traceability and ISO/IEC standards favor vertically integrated suppliers able to fuse QR-coded substrates, cloud tracking, and battery passport data. As printed cells commoditize, competitive intensity will pivot to differentiation in charging speed, high-temperature tolerance, and integration with energy harvesters. M&A activity is expected as conglomerates acquire start-ups for know-how and niche customer bases, gradually pushing the thin film battery industry toward higher concentration.

Thin Film Battery Industry Leaders

Kurt J. Lesker Company

Panasonic Corporation

Samsung SDI

Ilika plc

Cymbet Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Samsung SDI unveiled a pouch-type all-solid-state battery prototype for humanoid robots at InterBattery 2026, scheduling mass production for H2 2027.

- February 2026: Lyten acquired Northvolt Ett and Northvolt Labs, gaining 16 GWh capacity and Europe’s largest battery R&D center.

- February 2026: Amprius partnered with Nanotech Energy to scale domestic silicon-anode cell production, refining the 320 Wh/kg SA128 cell.

- November 2025: BTRY closed a USD 5.7 million seed round to industrialize solvent-free roll-to-roll solid-state batteries.

Global Thin Film Battery Market Report Scope

Thin film batteries are a type of energy storage device that is characterized by their light and flexible nature. They are made using thin layers of various materials deposited on a substrate, usually through a process called physical vapor deposition or chemical vapor deposition. These batteries typically use solid-state technology and offer advantages such as flexibility, small form factors, and the ability to be integrated into various devices and applications.

The Thin Film Battery Market is segmented into battery type, technology, application, and geography. By battery type, the market is segmented into rechargeable and non-rechargeable batteries. By technology, the market is segmented into printed battery, ceramic battery, lithium-polymer battery, solid-state chip battery, and other technologies. By application, the market is segmented into consumer electronics, medical devices, wearable technology, smart cards, RFID, IoT sensors, military and defense, smart packaging, and other applications. The report also covers the market size and forecasts for the thin film battery market across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Rechargeable |

| Non-Rechargeable (Primary) |

| Printed Battery |

| Ceramic Battery |

| Lithium-Polymer Battery |

| Solid-State Chip Battery |

| Other Technologies |

| Consumer Electronics |

| Medical Devices |

| Wearable Technology |

| Smart Cards |

| RFID |

| IoT Sensors |

| Military & Defense |

| Smart Packaging |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Battery Type | Rechargeable | |

| Non-Rechargeable (Primary) | ||

| By Technology | Printed Battery | |

| Ceramic Battery | ||

| Lithium-Polymer Battery | ||

| Solid-State Chip Battery | ||

| Other Technologies | ||

| By Application | Consumer Electronics | |

| Medical Devices | ||

| Wearable Technology | ||

| Smart Cards | ||

| RFID | ||

| IoT Sensors | ||

| Military & Defense | ||

| Smart Packaging | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the thin film battery market expected to grow through 2031?

Revenues are forecast to rise from USD 315.68 million in 2026 to USD 774.45 million by 2031, translating into a 19.66% CAGR.

Which segment currently holds the largest thin-film revenue share?

Medical devices led with 54.97% of 2025 sales thanks to implantable sensors and drug-delivery pumps that mandate solid-state safety.

What technology scales most rapidly within thin-film batteries?

Printed batteries, already at 81.64% 2025 share, are advancing at 21.47% CAGR because roll-to-roll web printing slashes unit costs.

Which region offers the highest growth potential?

Asia-Pacific is expanding at 22.35% CAGR on the back of Samsung SDI's robot-battery ramp, China's printed-cell subsidies, and Japans sensor demand.

Why are rechargeable thin-film cells overtaking primary cells?

Wearables, service robots, and soldier systems demand thousands of charge cycles, making rechargeable formats more cost-efficient over product lifetimes.

What limits the wider adoption of thin-film batteries in high-drain tools?

Current LiPON electrolytes exhibit lower ionic conductivity, capping discharge rates and leaving power tools to stick with high-capacity cylindrical lithium-ion cells.

Page last updated on: