Fortified Edible Oils Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

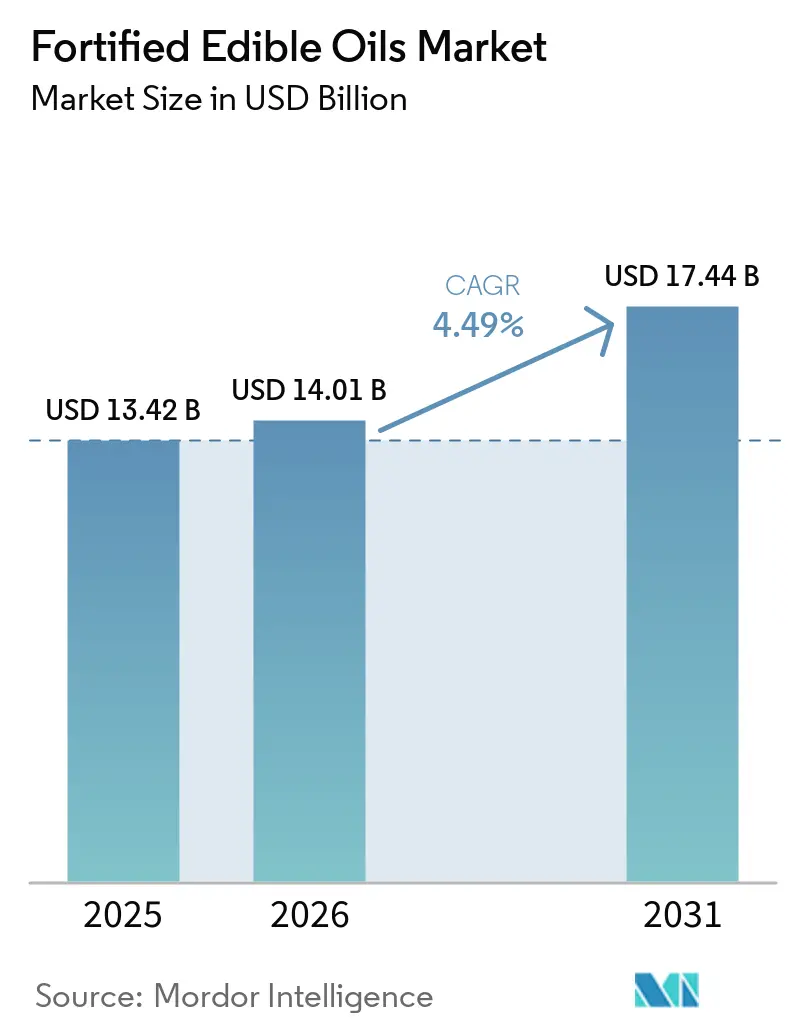

| Market Size (2026) | USD 14.01 Billion |

| Market Size (2031) | USD 17.44 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

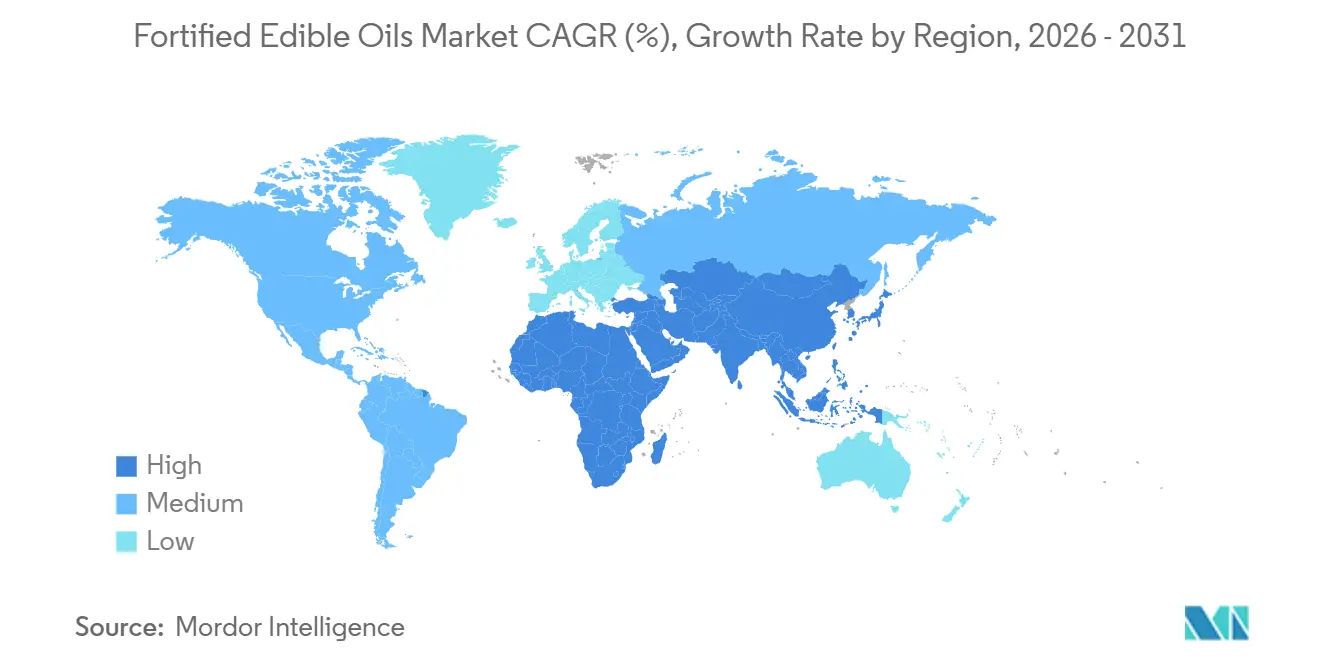

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fortified Edible Oils Market Analysis by Mordor Intelligence

The fortified edible oil market size was valued at USD 13.42 billion in 2025 and estimated to grow from USD 14.01 billion in 2026 to reach USD 17.44 billion by 2031, at a CAGR of 4.49% during the forecast period (2026-2031). Momentum stems from a policy shift that treats edible oils as reliable, wide-reaching carriers of vitamins A and D, following the World Health Organization’s 2025 guideline that ranked oil fortification ahead of supplementation in terms of cost-effectiveness. Governments have translated this guidance into mandates: India’s Food Safety and Standards Authority, Indonesia’s SNI 7709:2019, and Bolivia’s Supreme Decree 28094 collectively pull more than half of global retail volume into compulsory compliance. At the same time, nutrition-conscious consumers in North America and Europe reward voluntary fortifiers, especially where labels combine lower trans-fat claims with vitamin enrichment. Yet raw-material price swings, palm oil, sunflower oil, and recycled PET, continue to squeeze margins, prompting processors to hedge feedstock contracts and lighten packaging to hold shelf prices steady.

Key Report Takeaways

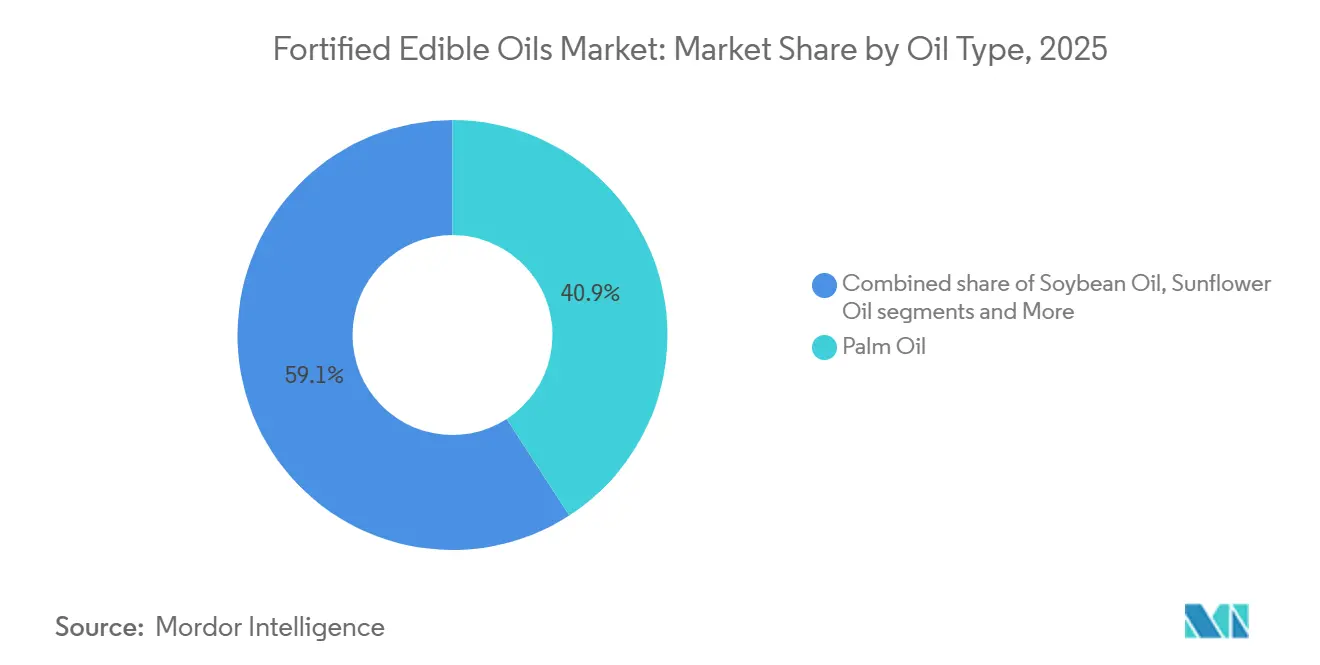

- By oil type, palm oil accounted for 40.87% of the fortified edible oil market share in 2025, while sunflower oil is expected to expand at a CAGR of 6.28% through 2031.

- By packaging type, PET and HDPE bottles represented 52.33% of total revenue in 2025, whereas flexible pouches and sachets are projected to grow at a CAGR of 5.94% through 2031.

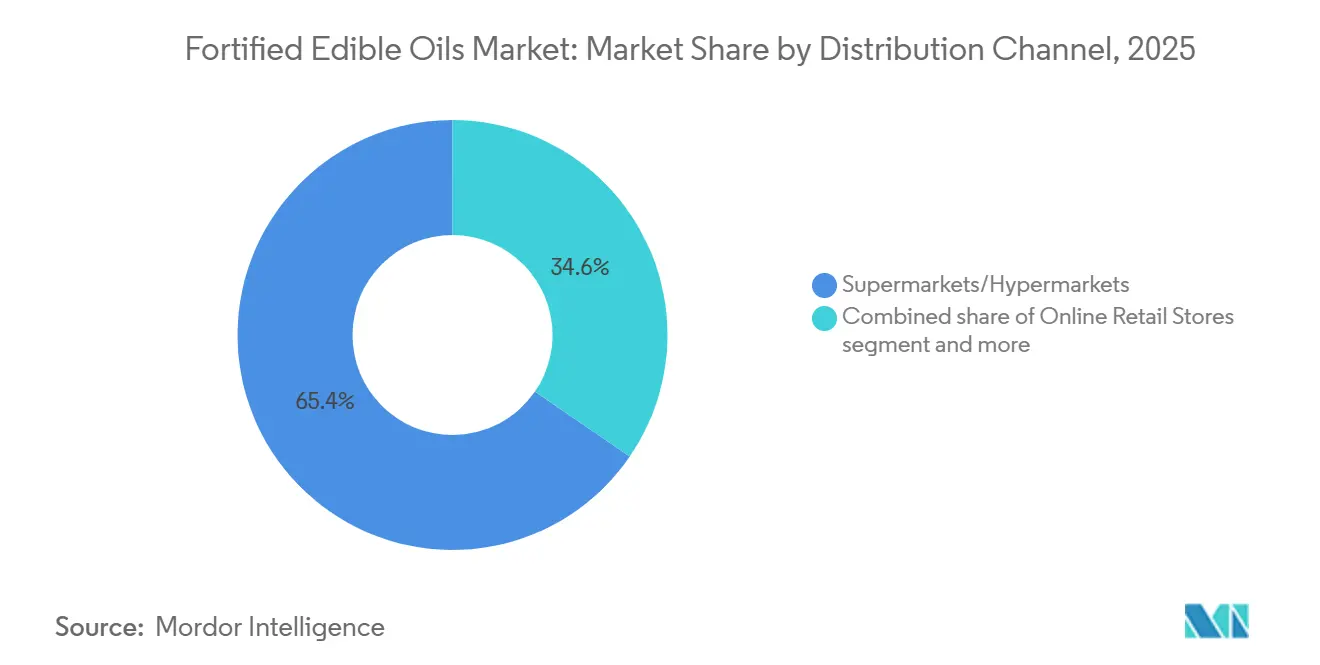

- By distribution channel, supermarkets and hypermarkets accounted for 65.44% of 2025 sales. Online retail is projected to grow at 5.84% CAGR through 2031.

- By geography, Asia-Pacific held a dominant 54.78% share in 2025, while the Middle East and Africa region is expected to record the fastest growth, with a projected CAGR of 5.75% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fortified Edible Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing health consciousness and demand for nutrient-rich diets | +0.9% | Global, strongest in Asian and North American metros | Medium term (2-4 years) |

| Stronger adoption of vitamin A, D, E, and K enrichment | +1.1% | India, Indonesia, Philippines, spill-over in Middle East and Africa | Long term (≥ 4 years) |

| Shift towards plant-based and sustainable oils | +0.7% | Europe and North America, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Improved fortification technologies that protect nutrient stability | +0.6% | Europe, North America, urban Asia | Long term (≥ 4 years) |

| Product reformulation in response to preventive-health and family-nutrition positioning | +0.5% | Europe and North America | Short term (≤ 2 years) |

| Mandatory fortification regulations and subsidies | +1.2% | Asia-Pacific, Middle East and Africa, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing health consciousness and demand for nutrient-rich diets

Preventive nutrition is reshaping household purchasing decisions as consumers link micronutrient intake to immunity, cognitive development, and reduced chronic-disease risk. Ethiopia's April 2025 mandatory fortification guidelines for edible oils and flour emerged from evidence that 66% of women of reproductive age in the country are deficient in one or more micronutrients, a statistic that galvanized policymakers to mandate industrial fortification rather than rely on supplementation campaigns with low adherence, according to the Federal Democratic Republic of Ethiopia Ministry of Health[1]Source: Federal Democratic Republic of Ethiopia Ministry of Health, “Mandatory Fortification Guidelines for Edible Oils and Flour,” fmoh.gov.et. India's Tata Trusts fortification program demonstrated that adding vitamins A and D to edible oil costs approximately USD 0.0018 per kilogram, a negligible increment that processors can absorb without triggering consumer resistance, yet delivers measurable reductions in night blindness and rickets prevalence in intervention districts. This cost-effectiveness is prompting governments to view fortification as a high-return public-health investment, particularly where staple oil consumption is universal, and brand loyalty is low enough that mandates do not distort competition. ADM's January 15, 2026, USD 26 million investment in its Erlanger, Kentucky, facility to expand reformulation capabilities reflects corporate recognition that 80% of US consumers favor product reformulation over supplementation, and 45% specifically seek reduced saturated fats, creating a dual opportunity to fortify while improving lipid profiles.

Stronger adoption of Vitamin A, D, E, and K enrichment

Fat-soluble vitamin fortification is accelerating because edible oils provide an ideal lipid matrix for absorption, bypassing the bioavailability challenges that plague water-soluble fortificants in flour or rice. China's GB/T 21123-2025 national standard for vitamin A fortified edible oils, which replaced the 2007 version and applies to soybean, rapeseed, peanut, and corn oils, mandates opaque packaging in containers up to 100 liters and prescribes high-performance liquid chromatography testing per GB 5009.82, signaling a shift from voluntary guidelines to enforceable quality benchmarks, according to the Standardization Administration of China. A draft regulation issued in September 2025 further proposes vitamin A levels of 4,000 to 8,000 micrograms per kilogram and vitamin D levels of 50 to 100 micrograms per kilogram for vegetable oils, aligning China's fortification intensity with WHO recommendations and potentially unlocking a market where per-capita oil consumption exceeds 20 kilograms annually, according to the China National Center for Food Safety Risk Assessment.

Shift towards plant-based and sustainable oils

Consumer migration toward plant-based diets is creating a halo effect for oils perceived as minimally processed and sustainably sourced, yet this trend also introduces competition for fortified variants. Wilmar International's FY2024 annual report highlighted that its Food Products segment generated USD 28.83 billion in revenue and sold 33.0 million metric tonnes, with leadership positions in China, Indonesia, India, Vietnam, Sri Lanka, and Africa, and noted that its Goodman Fielder subsidiary operates under a Nutrition Policy that prioritizes healthier reformulations, including fortification with omega-3 fatty acids and vitamins. However, the rise of cold-pressed, organic, and extra-virgin oils marketed on naturalness claims creates a perception gap: some consumers view fortification as adulteration rather than enhancement, a framing that processors must counter through transparent labeling and third-party certifications such as ISO 22000 for food safety management. The European Union's Regulation 1925/2006 permits vitamin and mineral addition to edible oils but requires Annex I and II compliance, specifying permitted vitamins, A, D, E, K, among others, and their chemical forms, which standardizes fortification practices but also imposes compliance costs that favor larger processors with in-house regulatory expertise.

Mandatory fortification regulations and subsidies

Legislative mandates are the single most potent driver, converting fortification from a voluntary corporate social responsibility initiative into a baseline compliance requirement that levels the competitive playing field. Bolivia's Supreme Decree 28094, enacted in 2005, mandates vitamin A fortification of all edible vegetable oil sold in hermetically sealed containers, grants a 90-day compliance timeline, and assigns enforcement to municipal health authorities, a decentralized model that has sustained high compliance rates despite limited central oversight, according to the Government of Bolivia. Indonesia's SNI 7709:2019 standard, which requires 45 IU/g of vitamin A and achieved 68.42% compliance among industrial millers between 2021 and 2023, is undermined by the fact that only 14.99% of Indonesian households consume packaged oil, with 85% purchasing loose or unpackaged oil from wet markets where fortification is absent and quality is unverifiable, a structural gap that the Millers for Nutrition coalition is addressing through packaging subsidies and consumer education. Egypt's National Operational Plan 2025-2030, launched in July 2025, prioritizes flour fortification but leaves edible oil fortification voluntary, a policy asymmetry that reflects political-economy constraints in which oil imports are dominated by state-owned enterprises resistant to premix procurement mandates, according to the Government of Egypt. The Organisation for Economic Co-operation and Development's 2024 regulatory governance framework for large-scale food fortification identifies six pillars, data and evidence, policies and regulations, authorization, supervision and enforcement, capacity building, and incentives, and notes that country pilots in Burkina Faso, India, Indonesia, Nigeria, and Vietnam face common challenges: inadequate laboratory capacity for quality testing, insufficient budget allocations for enforcement, weak import controls that allow unfortified products to undercut compliant processors, premix import taxes that inflate input costs, and bulk oil traceability gaps that enable adulteration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher shelf price versus conventional unfortified edible oil | -0.8% | Low-income markets in South Asia and Sub-Saharan Africa | Short term (≤ 2 years) |

| Complex labeling and regulatory variation across markets | -0.5% | Global, especially import-dependent MENA and SSA | Medium term (2-4 years) |

| Competition from naturally positioned oils | -0.6% | Europe and North America, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Raw-material price volatility in base oils | -0.9% | Middle East, North Africa, and Sub-Saharan Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex labeling and regulatory variation across markets

Divergent fortification standards and labeling requirements across jurisdictions impose compliance costs that disproportionately burden mid-sized exporters and regional players. Argentina's Joint Resolution 38/2025 modified fortified food requirements to mandate that fat-soluble vitamins provide 20% to 50% of the daily reference value per portion, while water-soluble vitamins must deliver 20% to 100%, a specificity that requires reformulation for products previously compliant under older thresholds. The European Union's Regulation 1925/2006 harmonizes permitted vitamins and their chemical forms across member states, yet individual countries retain discretion over maximum fortification levels: Germany's Federal Institute for Risk Assessment proposed a vitamin D ceiling of 7.5 micrograms per 100 grams for edible oils in 2024, while Sweden and Belgium mandate margarine and fat-spread fortification but leave liquid oils voluntary, creating a patchwork that complicates pan-European distribution. China's September 2025 draft regulation proposing vitamin A levels of 4,000 to 8,000 micrograms per kilogram and vitamin D levels of 50 to 100 micrograms per kilogram for vegetable oils introduces a new compliance hurdle for multinational processors that must reconcile Chinese thresholds with WHO recommendations and domestic standards in their home markets, according to the China National Center for Food Safety Risk Assessment.

Raw-material price volatility in base oils

Feedstock price swings compress processor margins and destabilize retail pricing, undermining the predictability that governments and institutional buyers require for long-term fortification commitments. The FAO Vegetable Oil Price Index rose 5.1% month-on-month in March 2026 and stood 13.2% higher year-on-year, with palm oil reaching its highest level since mid-2022, soybean oil remaining stable, and sunflower oil climbing due to Black Sea supply tightness exacerbated by geopolitical disruptions. US Environmental Protection Agency projections that biofuel demand for soy and palm oil will rise from 11.0 million metric tonnes in 2025 to 17.9 million metric tonnes in 2026 are tightening feedstock availability and pushing crude oil prices to USD 110 per barrel as of May 2026, creating a feedback loop where energy costs inflate vegetable oil prices, which in turn raise fortified oil retail prices and dampen demand in price-sensitive markets[2]Source: U.S. Environmental Protection Agency, “Biofuel Demand Projections 2025-2026,” epa.gov. Indonesia's reliance on imported premixes and packaging materials, both denominated in US dollars, means that rupiah depreciation amplifies input-cost inflation, a dynamic that the Millers for Nutrition coalition is attempting to mitigate through bulk premix procurement and local blending partnerships, yet currency risk remains an unhedged exposure for most small and medium processors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Oil Type: Palm Dominance Meets Sunflower Momentum

Palm oil commanded 40.87% market share in 2025, a position rooted in its cultivation scale across Indonesia and Malaysia, its stable lipid matrix for fat-soluble vitamin retention, and its cost advantage over alternatives in South and Southeast Asian markets where per-capita consumption exceeds 15 kilograms annually. Canola and rapeseed oil, popular in Canada and Northern Europe for their favorable omega-3 to omega-6 ratios, are gaining traction as processors reformulate for heart-health claims, with Cargill's April 21, 2026 opening of a 1 million metric tonne canola facility in Regina, Saskatchewan signaling confidence in long-term demand for premium, health-positioned oils. Mustard oil, concentrated in North India and Bangladesh, occupies a niche where cold-pressed formats and pungent flavor profiles command brand loyalty, yet fortification adoption lags due to small-scale, artisanal production that lacks the blending infrastructure for consistent premix incorporation. Adani Wilmar's May 2024 launch of Fortune Pehli Dhaar fortified mustard oil targets this segment, leveraging the company's 121 million household reach in India and its Haryana integrated plant capacity exceeding 627,000 metric tonnes to scale fortification in a traditionally unfortified category.

Sunflower oil is forecast to grow at 6.28% CAGR from 2026 to 2031, driven by consumer preference for lighter taste profiles in Eastern Europe and South America, and by cultivation expansion in Ukraine, Russia, and Argentina, despite Black Sea supply disruptions that pushed prices upward in early 2026. Soybean oil, the second-largest segment, benefits from integrated crushing and refining infrastructure in the United States, Brazil, and Argentina, yet faces headwinds from biofuel mandates that divert feedstock away from food applications, tightening supply and raising input costs for fortification programs. Other oils, coconut, groundnut, sesame, collectively account for the residual share, serving regional cuisines and specialty applications where fortification is either technically challenging due to high saturated fat content or economically unviable due to low volumes. China's GB/T 21123-2025 standard, which applies to soybean, rapeseed, peanut, and corn oils but excludes palm and coconut, reflects regulatory prioritization of oils with broad consumption bases and established refining infrastructure, a pattern likely to repeat as other governments draft fortification mandates, according to the Standardization Administration of China.

By Packaging Type: Bottles Lead, Pouches Gain

PET and HDPE bottles accounted for 52.33% of the volume of fortified edible oil packaging in 2025, favored for their transparency (which signals purity), resealability, and compatibility with modern retail shelf sets. Sidel's May 2026 launch of a laser-blown PET bottle for edible oils, weighing 16.5 grams versus the conventional 20.5 grams and incorporating 100% recycled PET, illustrates how packaging innovation addresses both cost and sustainability pressures[3]Source: Sidel, “Ultra-Light PET Bottle Launch,” sidel.com . The 20% weight reduction lowers transportation emissions and per-unit material cost, enabling brands to either improve margins or pass savings to consumers, a critical consideration in price-sensitive markets. Brands targeting e-commerce channels are experimenting with tamper-evident seals, QR codes for traceability, and compact packaging that reduces shipping costs and breakage risk, recognizing that online retail's 5.84% CAGR requires packaging optimized for last-mile logistics rather than shelf appeal.

Flexible pouches and sachets are growing at 5.94% CAGR through 2031, the fastest among packaging types, driven by their lower unit cost, reduced logistics weight, and appeal to low-income and rural consumers who purchase in small quantities to manage cash flow. Tinplate and metal containers retain a niche in bulk purchase channels, where bulk packaging and extended shelf life justify the higher per-unit cost. Other packaging formats, including glass bottles for premium segments and bag-in-box for food service, remain marginal, constrained by cost and handling complexity. Flexible pouches, while growing rapidly, face consumer perception challenges in premium segments, where rigid bottles signal quality and shelf presence; brands like Emami Healthy & Tasty offer fortified oils in both 1-liter pouches (Rs 140, USD 1.70) and bottles to straddle price tiers and distribution channels. Sachets (50-200 ml) are proliferating in rural India, Sub-Saharan Africa, and Southeast Asia, where they enable trial at minimal upfront cost and fit the daily-purchase behavior of households with limited storage and refrigeration. However, sachet proliferation raises environmental concerns, single-use plastic waste, and some governments are considering bans or taxes on small-format packaging, a regulatory risk that could curtail the fastest-growing segment.

By Distribution Channel: Modern Retail Dominates, Online Surges

Supermarkets and hypermarkets retained 65.44% of the distribution of fortified edible oil in 2025, reflecting their dominance in organized retail, their ability to carry multiple SKUs and pack sizes, and their role as trusted venues for health-oriented purchases. Supermarkets and hypermarkets respond by expanding private-label fortified oils, which offer 15-20% lower prices than branded equivalents by eliminating marketing overhead and leveraging retailer buyer power; private-label penetration in fortified oils reached an estimated 12-15% in European modern retail by 2025, up from 8-10% in 2020. Convenience stores capture impulse purchases and top-up buying in urban areas, but their limited shelf space constrains SKU proliferation and favors established brands with high turnover. Other channels, including traditional kirana stores in India, wet markets in Southeast Asia, and door-to-door sales, remain significant in volume terms but are underserved by fortified oils due to a lack of cold-chain infrastructure, consumer education, and retailer incentives to stock premium-priced SKUs. Convenience stores, constrained by 200-500 SKU limits, prioritize high-velocity items and often stock only one or two fortified-oil brands, making shelf-space negotiation and distributor incentives critical for smaller players. Traditional trade channels, kiranas, wet markets, dominate volume in India and Indonesia, but fortified-oil penetration remains low due to price sensitivity, lack of refrigeration (which accelerates vitamin degradation in non-encapsulated oils), and retailer unfamiliarity with fortification benefits.

Online retail stores are accelerating at a 5.84% CAGR through 2031, propelled by subscription models, direct-to-consumer brands that bypass traditional trade margins, and pandemic-induced shifts in grocery shopping behavior that have proven durable. E-grocery platforms in India (BigBasket, Amazon Fresh) and Southeast Asia (Lazada, Shopee) now offer subscription discounts of 10-15% for fortified oils, locking in repeat purchases and reducing per-order acquisition costs, a model that incumbent CPG brands find difficult to replicate without cannibalizing existing retail relationships. Direct-to-consumer fortified-oil brands invest subscription savings into consumer education (recipe videos, nutrition webinars, influencer partnerships), creating a virtuous cycle where higher engagement drives retention and word-of-mouth. Online retail's growth is not uniform: it is concentrated in tier-1 and tier-2 cities with reliable last-mile delivery, while rural areas, where micronutrient deficiencies are often most acute, remain underserved by e-commerce, perpetuating a geographic mismatch between need and access. Government programs like India's FSSAI +F logo and Indonesia's Minyakita subsidized distribution are attempting to bridge this gap by providing point-of-sale materials, retailer training, and price support, but scale-up remains slow.

Geography Analysis

Asia-Pacific accounted for 54.78% of global fortified edible oil revenue in 2025, supported by large-scale government initiatives and rising health awareness. Key programs include India’s FSSAI +F logo scheme, Indonesia’s SNI 7709 palm oil fortification mandate, and increasing demand from China’s expanding middle class for preventive health products. In India, per capita edible oil consumption of approximately 19 kg annually, combined with a population exceeding 1.4 billion, creates substantial market scale, where even incremental penetration of fortified oils translates into tens of millions of households, supporting investments in dedicated refining capacity and regional distribution infrastructure, according to the USDA FAS. Indonesia’s Minyakita program distributed more than 2 million liters of subsidized fortified palm oil per month in 2025, achieving significant reach among lower-income consumers, while the reduction in bulk packaging from 42% to 6.5% between 2020 and 2025 reflects rapid market formalization, as reported by BPOM Indonesia. In China, although per capita consumption of fortified oils remains relatively limited, demand is increasing alongside urbanization and income growth; however, regulatory approval timelines of 12-18 months continue to constrain market entry for new products. In developed markets such as Japan and South Korea, high consumer awareness of micronutrient benefits is balanced by a preference for minimally processed oils, creating niche opportunities for fortified variants positioned around bioavailability and stability. Meanwhile, Thailand’s King Rice Oil Group invested 1.5 billion baht (USD 43 million) in November 2024 to expand production capacity, targeting revenue of 10 billion baht (USD 286 million) by 2030, reflecting expectations of growing demand for functional oils such as oryzanol-enriched rice bran oil. Australia and New Zealand remain relatively small markets with voluntary fortification frameworks, although their stringent food safety standards provide an environment for validating premium fortified oil products prior to broader regional expansion.

The Middle East and Africa region is expected to record the fastest growth, with a projected CAGR of 5.75% through 2031, driven by the expansion of mandatory fortification programs and national nutrition strategies. Countries including Saudi Arabia, the UAE, Egypt, and Ethiopia are integrating fortified edible oils into public health initiatives such as school feeding and maternal nutrition programs. Saudi Arabia’s February 2026 draft standards for vitamin A and D fortification, if implemented, will require reformulation across the edible oil market, effectively making fortification a baseline requirement rather than a point of differentiation, according to the Saudi Food and Drug Authority. Ethiopia’s April 2025 mandatory fortification guidelines, aligned with WHO standards and supported by compliance monitoring through random sampling, signal a broader regional shift toward compulsory frameworks, as noted by the Ethiopian Public Health Institute. Large-population markets such as Nigeria and Egypt present significant volume opportunities; however, fragmented retail structures, informal distribution channels, and foreign exchange limitations pose challenges to pricing and supply chain efficiency. In contrast, South Africa’s more developed retail sector, led by major chains such as Shoprite, Pick n Pay, and Woolworths, provides a relatively structured entry point, although competition remains intense and price sensitivity high. The Gulf Cooperation Council countries benefit from high per capita income levels and government-led health initiatives but remain dependent on imports, increasing exposure to global price volatility. Markets such as Morocco and Turkey, influenced by both European and regional regulatory frameworks, present opportunities for companies capable of navigating dual compliance requirements.

North America and Europe together represented a significant share of global fortified edible oil revenue in 2025, characterized by voluntary fortification regimes, strict labeling standards, and clear segmentation between mass-market and premium products. In Canada, regulatory updates in 2025 increased vitamin D fortification levels in margarine to 26 µg per 100 g and introduced mandatory front-of-pack labeling effective January 1, 2026, supporting demand for products positioned on transparency and health benefits, according to Health Canada. In the United States, while awareness of vitamin D deficiency remains high, particularly in northern regions, the market faces strong competition from dietary supplements, which offer higher dosages and targeted delivery formats. Europe operates under Regulation (EC) No 1925/2006, which permits fortification but allows individual member states to impose additional restrictions, resulting in a fragmented regulatory environment. For example, Finland and Sweden mandate fortification in certain categories, whereas Germany, France, and the United Kingdom maintain voluntary approaches. The Netherlands enforces stricter controls through its Commodities Act Decree, limiting vitamin additions and setting intake thresholds, complicating cross-border distribution strategies. In both North America and Europe, premium segments such as cold-pressed and organic oils command price premiums of 20–30%, appealing to consumers who prioritize natural product attributes over fortification, thereby requiring fortified oil producers to emphasize measurable health benefits and nutrient bioavailability. In South America, markets led by Brazil, Argentina, and Chile are gradually shifting toward more structured fortification policies; Argentina’s July 2025 regulatory amendment streamlined approval processes for fortified foods without mandating adoption, while Brazil’s large population and public nutrition programs create opportunities for fortified oil distribution, albeit within a context of economic volatility and currency fluctuations.

Competitive Landscape

The fortified edible oil market exhibits moderate concentration, with five leading players, Cargill, Archer-Daniels-Midland, Bunge, Adani Wilmar, and Ruchi Soya, commanding an estimated 35-40% combined share, leaving substantial white space for regional specialists, private-label entrants, and ingredient suppliers forward-integrating into branded products. Competitive intensity is rising as ingredient suppliers like BASF and AAK leverage their formulation IP to co-pack or launch proprietary fortified blends, compressing margins for pure refiners who lack consumer-facing distribution or technical differentiation. BASF's stabilized vitamin A and D premixes, designed for high-temperature refining, enable oil producers to fortify at the refinery stage, simplifying logistics and reducing contamination risk, a capability that smaller players struggle to replicate without dedicated R&D and quality-control infrastructure.

AAK's October 2025 joint venture with KLK to build a specialty oils and fats refinery in Pasir Gudang, Malaysia, with ramp-up targeted for 2028 and full utilization by 2029, signals a long-term commitment to fortified and functional oils in Southeast Asia, a region where palm oil dominance and government mandates create favorable conditions for scale. Strategy patterns cluster around three archetypes: (1) volume leaders pursuing cost leadership through refining scale and distribution breadth (Cargill, ADM, Bunge); (2) regional champions leveraging local brand equity and government relationships (Adani Wilmar in India, Sime Darby in Malaysia); and (3) premium specialists targeting health-conscious urban consumers with multi-functional fortified blends (Emami Healthy & Tasty, KRBL India Gate Uplife). White-space opportunities include mustard oil fortification in India and Bangladesh, canola oil enrichment in Canada, and red palm oil variants in West Africa, segments where consumer preference and supply-chain infrastructure exist but fortified offerings remain underdeveloped. Emerging disruptors include direct-to-consumer e-commerce brands that bypass traditional trade margins and invest savings into consumer education, subscription models, and influencer partnerships, creating a virtuous cycle where higher engagement drives retention and word-of-mouth.

Technology is a key battleground: encapsulation techniques (spray drying, nanoemulsion) that protect vitamin stability during cooking enable brands to substantiate "guaranteed potency" claims with third-party lab data, a differentiator that justifies premium pricing in competitive retail environments. Private-label fortified oils, offered by supermarket chains at 15-20% discounts versus branded equivalents, reached 12-15% penetration in European modern retail by 2025, pressuring branded players to either invest in innovation (multi-vitamin blends, functional benefits) or accept margin compression. Regulatory compliance is an emerging competitive advantage: brands with dedicated regulatory affairs teams can navigate the patchwork of fortification standards, nutrient-claim regulations, and labeling requirements across jurisdictions, enabling faster market entry and broader geographic reach than smaller players who lack this capability. The market's moderate concentration and fragmented retail landscape suggest that M&A activity will accelerate as volume leaders seek to acquire regional brands with established distribution and consumer trust, while ingredient suppliers forward-integrate to capture downstream margins.

Fortified Edible Oils Industry Leaders

Cargill Inc

Archer-Daniels-Midland (ADM)

AWL Agri Business Ltd

Bunge Ltd

Fuji Oil Holdings Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Sidel launched a laser-blown PET bottle for edible oils, weighing 16.5 grams versus the conventional 20.5 grams and incorporating 100% recycled PET, delivering a 20% weight reduction that lowers transportation emissions and per-unit material cost.

- October 2025: Adani Wilmar introduced Fortune Sunflower oil with a "17% less oil absorption" claim, positioning the fortified product at the intersection of health and economy.

- July 2025: India Gate Foods launched a campaign introducing India Gate Uplife Gut Pro Oil, the country's first cooking oil fortified with Pro Digest. The oil contains natural antioxidants and anti-inflammatory properties to aid digestion. This product is part of the company's Uplife wellness range. The brand developed this product based on consumer research and functional benefits to differentiate itself in the market.

- June 2025: Marico launched Saffola Cold Pressed oil, marketed on minimal processing and retention of natural antioxidants. While not explicitly fortified, the product competes directly with fortified variants for health-conscious consumers, forcing fortified-oil brands to articulate why added vitamins deliver superior outcomes versus naturally occurring nutrients.

Global Fortified Edible Oils Market Report Scope

Fortified edible oil refers to cooking oils enriched with essential vitamins and nutrients, such as vitamins A and D, to improve nutritional value and address dietary deficiencies. The fortified edible oil market is segmented by oil type, packaging type, distribution channel, and geography. By oil type, the market includes palm oil, soybean oil, sunflower oil, canola/rapeseed oil, mustard oil, and other oils. Based on packaging type, the market is categorized into PET/HDPE bottles, flexible pouches and sachets, tinplate/metal containers, and other packaging formats. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other channels. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market sizes and forecasts for each region. For each segment, market sizing and forecasts have been done on the basis of value (USD million) and volume (Liters).

| Palm Oil |

| Soybean Oil |

| Sunflower Oil |

| Canola/Rapeseed Oil |

| Mustard Oil |

| Others |

| PET/HDPE Bottles |

| Flexible Pouches and Sachets |

| Tinplate/Metal Containers |

| Others |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Oil Type | Palm Oil | |

| Soybean Oil | ||

| Sunflower Oil | ||

| Canola/Rapeseed Oil | ||

| Mustard Oil | ||

| Others | ||

| By Packaging Type | PET/HDPE Bottles | |

| Flexible Pouches and Sachets | ||

| Tinplate/Metal Containers | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the fortified edible oil market today and where will it be by 2031?

The fortified edible oil market size is USD 14.01 billion in 2026 and is forecast to reach USD 17.44 billion by 2031, reflecting a 4.49% CAGR over 2026-2031

Which oil type leads global fortified sales?

Palm oil holds the lead with 40.87% fortified edible oil market share in 2025 thanks to its cost advantage and vitamin stability.

Which region will grow fastest through 2031?

Middle East and Africa is projected to log a 5.75% CAGR from 2026-2031 as Ethiopia, Nigeria, and others enforce new mandates.

What packaging solutions are gaining traction?

Lightweight rPET bottles and small flexible sachets are expanding fastest, the latter at 5.94% CAGR, driven by rural affordability and circular-economy rules.

Page last updated on: