Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 35.09 Billion |

| Market Size (2026) | USD 36.24 Billion |

| Market Size (2031) | USD 42.59 Billion |

| Growth Rate (2026 - 2031) | 3.29% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Athletic Footwear Market Analysis by Mordor Intelligence

The Europe athletic footwear market size is expected to grow from USD 35.09 billion in 2025 to USD 36.24 billion in 2026 and is forecast to reach USD 42.59 billion by 2031 at 3.29% CAGR over 2026-2031. The region’s steady growth reflects a mature yet resilient consumer base that continues to embrace performance innovation, gender-inclusive product lines, and omnichannel shopping habits. Stability prevails despite inflationary pressures because brands are widening price ladders, introducing sustainable materials, and leveraging digital engagement to keep purchase intent high. Women’s sports participation, marathon tourism, and outdoor recreation are redefining demand patterns, while premiumization encourages consumers to trade up for comfort, durability, and eco-friendly credentials. Competitive intensity remains elevated as global brands, niche innovators, and powerful retailers all vie for share, but technological advances in cushioning foams, carbon plates, and bio-based polymers provide clear levers for differentiation in the Europe athletic footwear market.

Key Report Takeaways

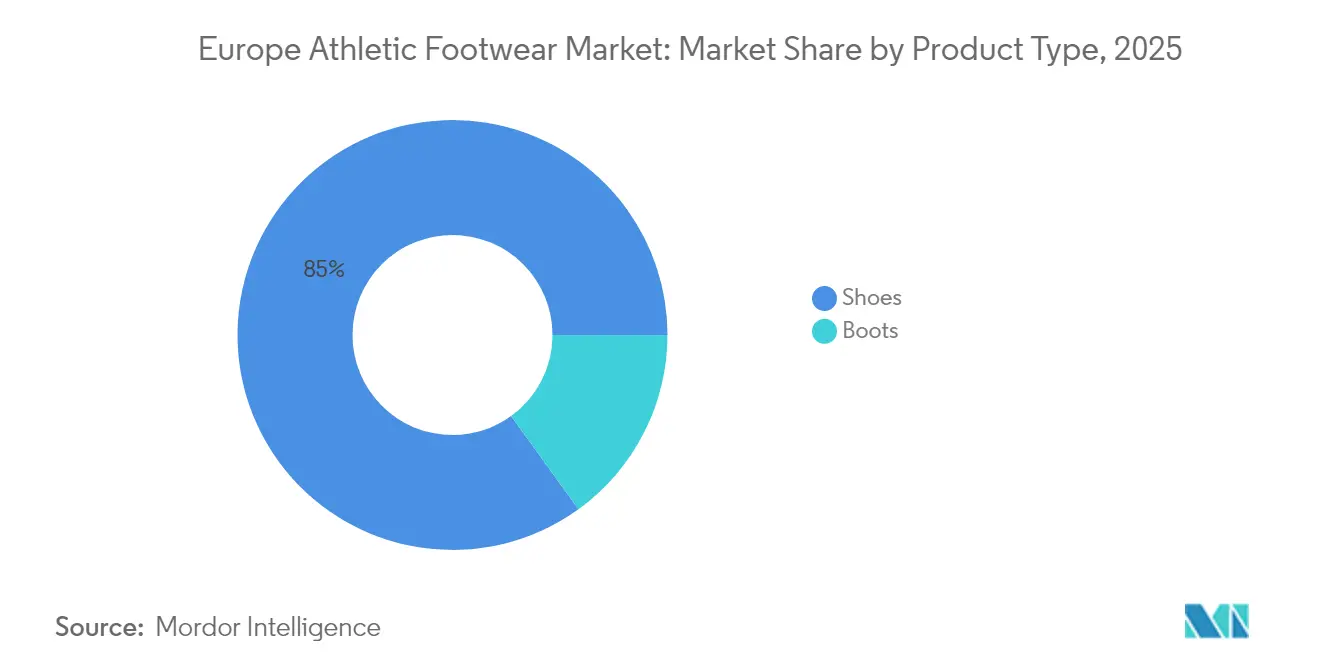

- By product type, shoes led with 84.96% revenue share in 2025, while boots are projected to expand at a 4.65% CAGR through 2031.

- By activity, sports shoes accounted for 47.10% of the Europe athletic footwear market share in 2025; running shoes are set to grow at a 4.43% CAGR.

- By end user, men commanded 63.10% share in 2025, whereas women’s footwear is forecast to accelerate at a 4.90% CAGR.

- By category, mass offerings captured 61.85% of the Europe athletic footwear market size in 2025 and premium lines are poised for a 4.18% CAGR.

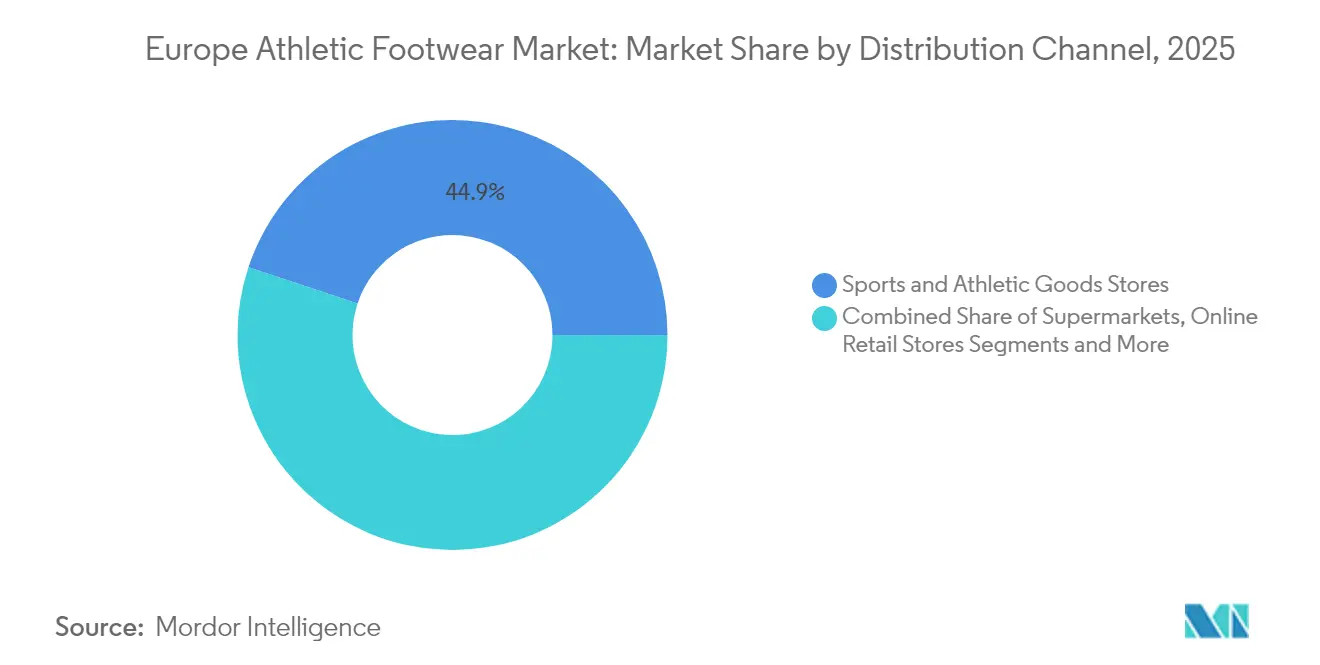

- By distribution channel, sports and athletic goods stores held 44.90% share in 2025, with online retail climbing at a market-leading 5.92% CAGR.

- By geography, the United Kingdom represented 19.10% of regional sales in 2025 and the Netherlands is on pace for a 4.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Athletic Footwear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Significant growth in women sports participation rate | +0.8% | Regional, with strongest gains in United Kingdom, France, Netherlands | Medium term (2-4 years) |

| Influence of social media platforms and celebrity endorsements | +0.6% | Regional, concentrated in urban markets across major European countries | Short term (≤ 2 years) |

| Increasing participation in organized sports events, marathons, and outdoor activities | +0.7% | Europe-wide, with peak impact in Germany, United Kingdom, Austria | Medium term (2-4 years) |

| Technological advancements in footwear materials for better comfort, durability, and performance | +0.5% | Europe-wide, specifically with Research and Development centers in Germany, Netherlands | Long term (≥ 4 years) |

| Strong presence and investments by major international brands | +0.4% | Europe-wide, concentrated in major retail markets | Short term (≤ 2 years) |

| Product personalization trends attracting consumers seeking customized footwear | +0.3% | Premium markets in Germany, United Kingdom, France, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Significant growth in women sports participation rate

A significant rise in women’s participation in sports is emerging as a key driver for the Europe athletic footwear market, with growing engagement in activities such as running, fitness training, yoga, and team sports fueling higher demand for performance-oriented and stylish footwear tailored to female consumers. According to Sport England, from November 2023 to November 2024, more than 18.1 million women in England engaged in sports or physical activities, highlighting the strong momentum behind this trend [1]Source: Sport England, "Female sports participation drives increase in Active People Survey figures", sportengland.org. The increasing focus on health and wellness, coupled with government initiatives and grassroots programs promoting female sports participation, is further accelerating market expansion. Moreover, the influence of prominent female athletes, social media fitness influencers, and the ongoing popularity of athleisure wear are encouraging women to invest in high-quality athletic footwear that blends comfort, durability, and fashion appeal, thereby strengthening the market’s growth outlook.

Influence of social media platforms and celebrity endorsements

The growing influence of social media platforms and celebrity endorsements is a key driver of the Europe athletic footwear market. According to Eurostat, in 2024, 97% of people in the EU aged 16–29 years reported using the internet every day, compared with 88% of the total population, highlighting the strong digital engagement among younger consumers [2]Source: Eurostat, "97% of young people in the EU use the internet daily", ec.europa.eu. This highly connected demographic is extensively exposed to promotional campaigns, product launches, and lifestyle content across social media platforms such as Instagram, TikTok, and YouTube, where athletes, fitness influencers, and celebrities frequently endorse leading athletic footwear brands. Such visibility not only strengthens brand recognition but also fosters aspirational purchasing behavior, positioning sports shoes as both performance-driven necessities and fashion-forward lifestyle products. As a result, digital influence and celebrity-driven marketing continue to shape consumer preferences and significantly boost market demand across Europe.

Increasing participation in organized sports events, marathons, and outdoor activities

Increasing participation in organized sports events, marathons, and outdoor activities is a major driver of the Europe athletic footwear market. In 2024, the BMW-Berlin Marathon stood out as Germany’s biggest marathon, with nearly 54,000 finishers, highlighting the massive scale and popularity of such sporting events [3]Source: Marathon Ergebnisse, "Marathon-Finisher pro Lauf", marathon-ergebnis.de. Similarly, the Haspa Marathon Hamburg attracted around 11,200 participants, making it the second-largest in the country. These large-scale events not only underscore the growing enthusiasm for running and endurance sports but also directly contribute to higher demand for athletic footwear that ensures durability, comfort, and performance. As marathons, community runs, and outdoor recreational activities expand in scale and visibility, consumers are increasingly investing in premium sports footwear, thereby accelerating market growth across the region.

Technological advancements in footwear materials for better comfort, durability, and performance

Technological advancements in footwear materials are emerging as a significant driver of the Europe athletic footwear market, as consumers increasingly seek products that deliver superior comfort, durability, and performance. Leading brands are investing in innovative materials such as lightweight engineered mesh for breathability, advanced foams and cushioning systems for enhanced shock absorption, and sustainable fabrics made from recycled plastics and bio-based materials to align with rising eco-consciousness. The integration of technologies like carbon-fiber plates for energy return and adaptive midsoles that respond to individual running styles is redefining performance standards, particularly in high-intensity sports and marathon running. Additionally, antimicrobial linings, water-resistant coatings, and improved outsole traction materials are further enhancing product functionality, making modern athletic footwear suitable for a wide range of indoor and outdoor activities. This continuous innovation not only drives consumer preference for premium, technologically advanced shoes but also enables brands to differentiate themselves in a highly competitive market, thereby accelerating overall growth in the region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit products | -0.4% | Regional, with highest impact in Eastern Europe, Southern Europe | Short term (≤ 2 years) |

| High competition leading to price wars and reduced profit margins | -0.3% | Europe-wide, most intense in Germany, United Kingdom, France | Short term (≤ 2 years) |

| Limited penetration in some Eastern European and emerging markets | -0.2% | Eastern Europe, particularly Romania, Bulgaria, emerging CEE markets | Medium term (2-4 years) |

| Concerns over sustainability and sourcing | -0.2% | Europe-wide, driven by regulatory compliance requirements | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

The proliferation of counterfeit products poses a significant restraint to the Europe athletic footwear market, undermining both brand reputation and consumer trust. The growing availability of fake athletic shoes, often sold at lower prices through unregulated online marketplaces, street vendors, and unauthorized retail channels, directly impacts the sales of genuine products from well-established brands. These counterfeit items typically lack the advanced materials, durability, and performance benefits of authentic footwear, leading to consumer dissatisfaction and, in some cases, risk of injuries. Moreover, the widespread presence of counterfeit products dilutes brand value, reduces profit margins, and creates unfair competition for legitimate players investing heavily in innovation, quality, and marketing. Despite ongoing government regulations and brand-led initiatives to curb illegal trade through stricter intellectual property enforcement and awareness campaigns, the challenge remains prevalent, making counterfeiting a persistent barrier to the sustainable growth of the athletic footwear market in Europe.

High competition leading to price wars and reduced profit margins

High competition leading to price wars and reduced profit margins is a major restraint for the Europe athletic footwear market. The region is home to numerous global and regional players, all striving to capture market share through aggressive pricing strategies, frequent product launches, and extensive promotional campaigns. While this competitive environment benefits consumers by providing a wide variety of choices and affordable options, it creates significant pressure on brands to maintain profitability. Companies are often forced to cut prices or offer heavy discounts to stay competitive, which erodes margins and limits the resources available for research, development, and innovation. Additionally, with rising raw material and production costs, sustaining profitability in the face of price-driven competition becomes increasingly challenging. Premium players, in particular, struggle to differentiate themselves in a crowded market where cost-sensitive consumers are lured by affordable alternatives from fast-fashion retailers and emerging local brands. As a result, intense competition and the resulting price wars threaten long-term profitability and pose a considerable barrier to sustainable market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shoes Dominance Faces Boot Innovation

The shoes segment dominates the Europe athletic footwear market, commanding an overwhelming 84.96% share in 2025. This strong presence is largely attributed to the segment’s broad versatility, as shoes are widely worn across multiple sports disciplines as well as for everyday casual and athletic purposes. They offer consumers both performance and style, making them equally relevant for professional athletes and fitness enthusiasts, as well as those seeking comfortable fashion choices. The growing trend of athleisure has further fueled this demand, as shoes seamlessly blend functionality with lifestyle appeal. Additionally, continuous innovation in cushioning technologies, lightweight materials, and sustainable designs has reinforced consumer interest in this segment. With their ability to cater to almost every consumer demographic, shoes remain the primary revenue driver in the European athletic footwear industry and are expected to maintain their dominance throughout the forecast period.

In contrast, the boots segment, though currently representing a smaller share of the market, exhibits the fastest growth potential. Forecasted to expand at a CAGR of 4.65% through 2031, this growth is being driven by the rise in adventure sports, trekking, hiking, and other outdoor activities gaining popularity across Europe. Consumers are increasingly investing in footwear that combines durability and comfort with enhanced protection in rugged environments, which makes boots an appealing choice. Innovations in water resistance, breathability, and material strength are also contributing to their expanding adoption. Furthermore, the shift toward active outdoor lifestyles among younger consumers and tourists is amplifying demand in this category. Although the segment lags behind shoes in market size, its accelerating growth underscores its emerging importance within the overall European athletic footwear market.

By Activity: Running Shoes Outpace Sports Shoes Growth

Sports shoes retained the leading position in the Europe athletic footwear market in 2025, accounting for a substantial 47.10% share. Their dominance stems from their ability to serve a diverse set of activities, ranging from professional team sports to general fitness and training purposes. This versatility makes them a preferred choice among both athletes and recreational users who value performance, comfort, and durability. The category continues to be supported by innovation in lightweight materials, advanced traction designs, and cushioning technologies that enhance athletic performance. Additionally, the rising popularity of multi-purpose athletic footwear, which seamlessly transitions from sports to casual settings, has further reinforced demand in this segment. With strong consumer acceptance across age groups and sports categories, sports shoes remain the backbone of revenue generation in the European athletic footwear market and are positioned to sustain their leadership in the years ahead.

Running shoes, on the other hand, stand out as the fastest-growing segment in the market, with a promising CAGR of 4.43% projected through 2031. This growth significantly exceeds the overall market’s expansion rate and underscores the impact of evolving health and fitness trends in Europe. The surge in marathon and recreational running participation, along with increasing awareness of the benefits of an active lifestyle, has positioned running shoes as a priority purchase for many consumers. Manufacturers are responding with designs that emphasize enhanced cushioning, flexibility, energy return, and lightweight construction tailored to diverse running needs. The segment also benefits from endorsements by fitness influencers and global sporting events, which continually promote running as an accessible and rewarding activity. Although running shoes currently trail sports shoes in overall market size, their strong momentum signals long-term growth and an expanding role in shaping the future of European athletic footwear demand.

By End User: Women's Segment Drives Growth Acceleration

Men’s athletic footwear continues to dominate the European market, capturing a commanding 63.10% share in 2025. This leadership position is rooted in the segment’s historical development, where product innovation and marketing efforts have traditionally targeted male consumers. Higher sports participation rates among men, especially in team sports and competitive athletics, have reinforced steady demand for performance-focused footwear. Established global brands maintain strong portfolios catered specifically to male athletes, offering a wide variety of designs that emphasize durability, advanced cushioning, and style. Additionally, cultural associations of masculinity with sports and outdoor activities have long contributed to the segment’s dominance. While the men’s category faces maturity in several sub-markets, it continues to hold the largest revenue share and serves as a foundation for the region’s athletic footwear industry.

In contrast, the women’s athletic footwear segment has emerged as the fastest-growing category, with a projected CAGR of 4.90% through 2031, well above the overall industry rate. This momentum reflects a clear demographic transformation as women increasingly engage in fitness routines, sports participation, and active lifestyle choices across Europe. Athletic footwear brands are responding by expanding women-specific product lines that combine performance with style, ensuring greater appeal across both functional and fashion-driven use cases. The rising influence of wellness culture, coupled with social media-driven fitness trends, is fueling purchases of running shoes, training footwear, and athleisure-oriented designs tailored for women. Furthermore, growing advocacy for gender inclusivity in sports has strengthened female consumer confidence in investing in high-performance athletic footwear. Although the women’s segment currently represents a smaller share than men’s, its rapid growth trajectory highlights the shifting dynamics of consumer demand and positions it as a critical driver of future market expansion.

By Category: Premium Segment Capitalizes on Quality Demand

Mass market products hold the dominant position in the Europe athletic footwear industry, capturing 61.85% of the market share in 2025. This leadership underscores the importance of affordability and accessibility in shaping consumer preferences, particularly in a region where price sensitivity remains strong. The segment benefits from widespread acceptance among budget-conscious consumers who prioritize value and functionality without compromising on fundamental performance. The mass footwear market often appeals to a broad demographic, ranging from school-aged athletes to adults seeking multipurpose sports shoes. Retail expansion through supermarkets, hypermarkets, and online channels has further bolstered accessibility, ensuring mass products remain widely available and affordable. As a result, this category continues to anchor overall industry revenues and is expected to maintain its commanding presence through sustained consumer reliance on cost-effective offerings.

In contrast, the premium segment represents the fastest-growing category, with a forecast CAGR of 4.18% through 2031 that outpaces the broader market. This growth highlights a clear shift in consumer attitudes, where quality, innovation, and sustainability are prioritized over price alone. Increasing demand for technologically advanced footwear—featuring performance-enhancing designs, eco-friendly materials, and fashion-forward elements—is fueling expansion within this segment. Consumers, particularly younger professionals and high-income groups, are increasingly willing to pay more for shoes that align with both athletic needs and lifestyle aspirations. The influence of brand prestige, celebrity endorsements, and unique collaborations also plays a significant role in elevating the appeal of premium products. Although the segment’s overall market share remains smaller compared to mass market offerings, its strong growth trajectory reflects evolving consumer preferences and positions it as a crucial engine for future value-driven expansion in Europe’s athletic footwear market.

By Distribution Channel: Online Retail Transforms Shopping Patterns

Sports and athletic goods stores retained the largest share of distribution in the Europe athletic footwear market, accounting for 44.90% in 2025. Their prominence is driven by the specialized services they provide, including expert product fitting, personalized performance consultation, and access to premium and brand-exclusive collections. Consumers continue to view these outlets as trusted destinations where professional guidance ensures they purchase the most suitable footwear for specific sporting needs. Strong partnerships with leading athletic footwear brands reinforce their role as vital distribution channels, offering the latest product launches and innovation-driven assortments. The in-store experience, emphasizing trial, comfort checks, and technical support, further enhances consumer confidence and loyalty. Despite intensifying competition from digital platforms, sports and athletic goods stores remain the cornerstone of athletic footwear distribution, particularly for performance-focused buyers seeking assurance of quality and functionality.

Online retail stores, however, represent the fastest-growing distribution channel in the European athletic footwear market, expanding at a robust CAGR of 5.92% through 2031. This growth rate nearly doubles that of the overall market, highlighting the transformative shift in consumer purchasing behavior toward digital platforms. Online channels offer unmatched convenience, wider product assortments, and competitive pricing, drawing in both budget-conscious and tech-savvy consumers. Features such as virtual try-on tools, AI-driven personalization, and fast delivery services are further accelerating the adoption of e-commerce. Additionally, the integration of exclusive online launches, influencer collaborations, and omnichannel strategies is strengthening consumer engagement with brands through digital mediums. While physical retail maintains a strong presence, the rapid ascent of e-commerce signals a fundamental restructuring of distribution dynamics and establishes online channels as a critical engine for future growth.

Geography Analysis

Western European markets, with their deep-rooted sports cultures and high disposable incomes, are witnessing a steady growth in athletic footwear adoption. In 2025, the United Kingdom commands a 19.10% share of the market, solidifying its status as Europe's top destination for athletic footwear. This dominance is bolstered by the nation's fervent football culture, government investments in sports infrastructure, and a consumer base eager to splurge on premium athletic products. Additionally, the growing trend of athleisure, where consumers integrate athletic footwear into everyday fashion, further drives market growth in this region. Meanwhile, Germany and France, with their diverse sports participation and strong retail networks, cater to both the mass market and premium segments. The increasing focus on product innovation, such as lightweight and performance-enhancing footwear, is also contributing to the growth of the athletic footwear market in Western Europe.

The Netherlands is on an upward trajectory, boasting an impressive 4.28% CAGR projected through 2031. This growth can be attributed to savvy market development strategies by international brands and a surge in sports participation, especially among the youth, who are increasingly shaping athletic footwear consumption trends. Furthermore, the Dutch government's initiatives to promote physical activity and sports participation have created a favorable environment for market expansion. These efforts, combined with the rising popularity of sustainable and eco-friendly footwear options, are influencing consumer preferences and driving demand in the Netherlands. The growing presence of local and regional players offering customized and affordable athletic footwear is also playing a significant role in the market's development.

In Central and Eastern Europe, the landscape is evolving. Expanding retail infrastructures, rising disposable incomes, and a shift in consumer preferences towards branded athletic footwear are all contributing to a complex yet promising growth scenario. Moreover, the increasing penetration of e-commerce platforms in these regions is making branded athletic footwear more accessible to a broader consumer base. This digital transformation, coupled with growing awareness of fitness and health, is expected to further accelerate market growth in Central and Eastern Europe over the forecast period. Additionally, the rising influence of Western fashion trends and the growing popularity of international sports events are encouraging consumers in these regions to invest in branded athletic footwear, further driving market expansion.

Competitive Landscape

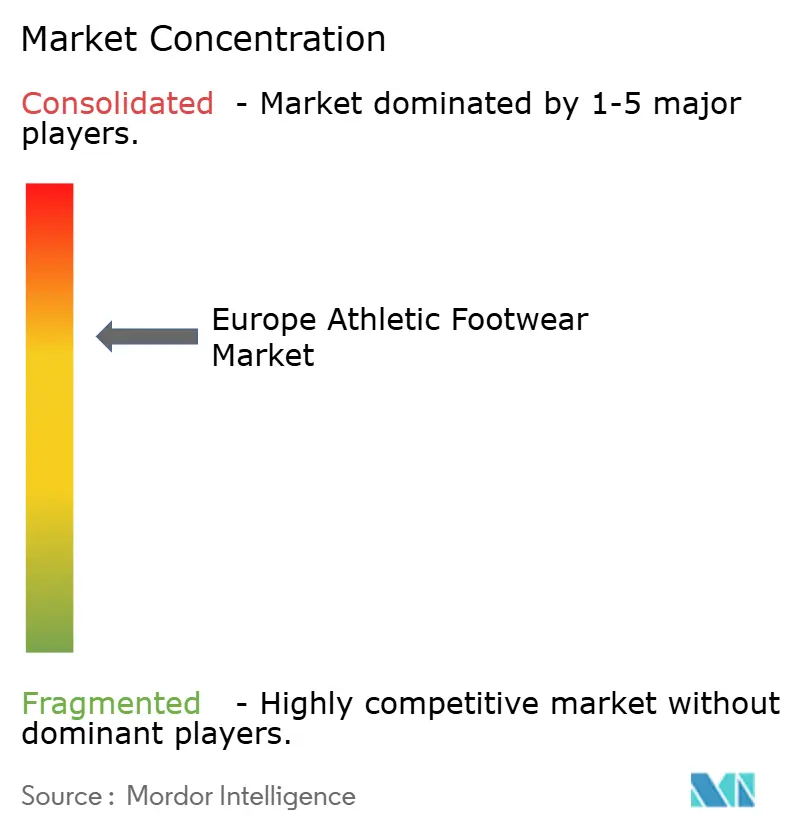

With a concentration score of 7, the European athletic footwear market showcases a balanced landscape. This score highlights a fragmentation level that allows both established giants and emerging specialists to carve out their niches using distinct positioning strategies. Industry titans like Nike, Adidas, and PUMA bolster their dominance through vast retail networks, high-profile endorsements, and relentless product innovation. However, they now contend with mounting challenges from direct-to-consumer brands and niche performance firms, both honing in on targeted consumer segments. Additionally, the rise of e-commerce platforms has further intensified competition, enabling smaller players to reach broader audiences without the need for extensive physical retail infrastructure.

In today's market, technology isn't just an add-on; it's a pivotal differentiator. Brands are channeling significant investments into material innovations, personalized offerings, and sustainable practices. These efforts not only justify premium price tags but also foster deep consumer loyalty. A case in point: Nike's debut of the AirImagination AI platform, enabling bespoke Air Max designs. This move underscores how industry frontrunners harness AI and historical assets, crafting unique consumer experiences that pose a challenge for smaller players to match. Furthermore, advancements in wearable technology, such as smart insoles and connected footwear, are reshaping consumer expectations and driving innovation across the market.

Consumer preferences in the European athletic footwear market are also evolving, with a growing emphasis on sustainability and ethical production practices. Leading brands are responding by incorporating recycled materials, reducing carbon footprints, and adopting transparent supply chain practices. These initiatives not only align with consumer values but also serve as a competitive advantage in a market increasingly driven by environmental consciousness. Meanwhile, emerging players are leveraging their agility to introduce eco-friendly products at a faster pace, further intensifying the competition. The interplay between established brands and new entrants continues to shape the market dynamics, making sustainability a key battleground for differentiation.

Europe Athletic Footwear Industry Leaders

-

Adidas AG

-

Puma SE

-

New Balance Athletics Inc.

-

Nike, Inc.

-

ASICS Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Puma, the renowned German sportswear giant, is set to unveil its inaugural European flagship store on London's iconic Oxford Street in autumn 2025. Spanning 24,000 sq ft, the store promises an immersive experience, seamlessly merging sports performance and technology with avant-garde streetwear designs.

- March 2025: ASICS unveiled the GEL-NIMBUS™ 27 shoes, boasting cloudlike cushioning, a premium fit, and a plush feel. The design, re-imagined by Scottish middle and long-distance runner Eilish McColgan, is a limited-edition tribute. Drawing from Eilish’s Scottish roots and steadfast determination, the shoes encapsulate her resilience and perseverance as an elite athlete.

- January 2025: PUMA officially began its long-term partnership with the Portuguese Football Federation, replacing Nike's 27-year sponsorship relationship and securing rights to supply all Portuguese national teams including men's, women's, youth, futsal, beach soccer, and e-sports teams ahead of major tournaments.

- April 2024: Nike, ahead of the Paris 2024 Olympic Games, introduced its latest elite footwear collection, asserting that AI is igniting a "super cycle" of innovation. Featured in the lineup are the Nike GT Hustle 3 basketball shoe, the 2024 Nike Mercurial football boot, and the Nike Victory 2 and Nike Maxfly 2 spikes tailored for sprinting and middle-distance track events.

Europe Athletic Footwear Market Report Scope

Athletic footwear include shoes that are used in sporting and fitness activities. The European athletic footwear market is segmented by product type, end-user, distribution channel, and geography. By product type, the market is segmented into running shoes, sports shoes, trekking/hiking shoes, and other product types. By end user, the market is segmented into men, women, and children. By distribution channel, the market is segmented into sports and athletic goods stores, supermarkets/hypermarkets, online retail stores, and other distribution channels. By geography, the market is segmented into Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Shoes |

| Boots |

By Activity

| Running Shoes |

| Sports Shoes |

| Adventure Sports Shoes |

| Other Product Types |

By End User

| Men |

| Women |

| Kids/Children |

By Category

| Mass |

| Premium |

By Distribution Channel

| Sports and Athletic Goods Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Belgium |

| Poland |

| Sweden |

| Rest of Europe |

| By Product Type | Shoes |

| Boots | |

| By Activity | Running Shoes |

| Sports Shoes | |

| Adventure Sports Shoes | |

| Other Product Types | |

| By End User | Men |

| Women | |

| Kids/Children | |

| By Category | Mass |

| Premium | |

| By Distribution Channel | Sports and Athletic Goods Stores |

| Supermarkets/Hypermarkets | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Belgium | |

| Poland | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe athletic footwear market in 2026?

The market is valued at USD 36.24 billion in 2026, with a forecast to reach USD 42.59 billion by 2031.

Which product type is growing fastest within European athletic footwear?

Boots are set to rise at a 4.65% CAGR through 2031, driven by adventure sports and outdoor recreation.

Why are women’s athletic shoes gaining share so quickly?

Increased female sports participation and targeted government funding are pushing women’s footwear toward a 4.90% CAGR.

What channel is expanding sales faster than others?

Online retail stores are climbing at a 5.92% CAGR as mobile shopping, size-matching AI, and quick delivery gain traction.

Which country offers the highest growth opportunity?

The Netherlands leads with a 4.28% CAGR thanks to strong club sports culture and high digital adoption.

Page last updated on: