Gluten-free Pizza Crust Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.03 Billion |

| Market Size (2031) | USD 5.23 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

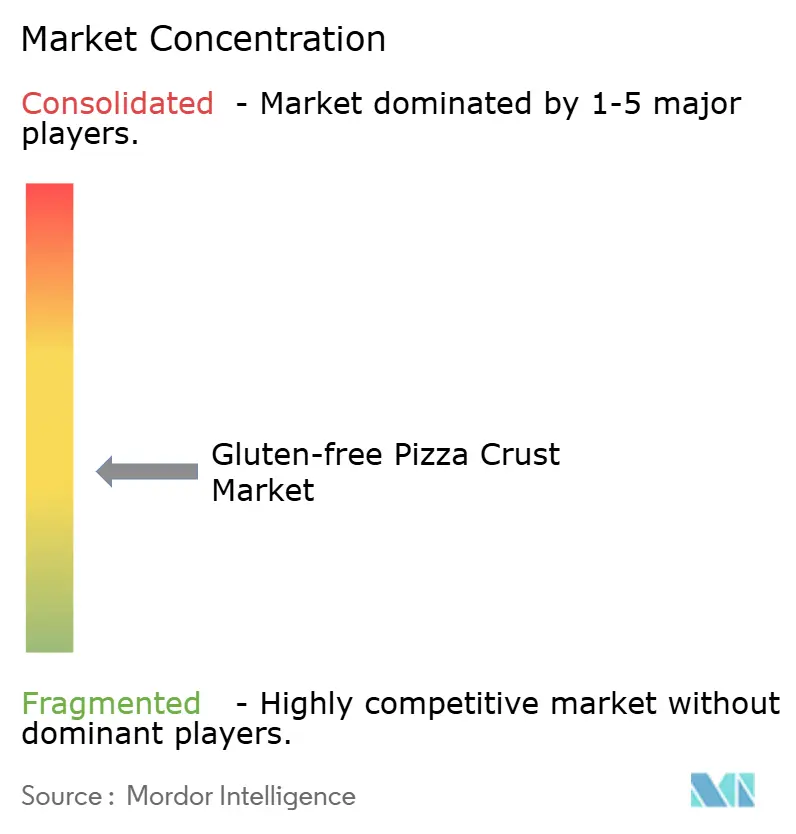

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gluten-free Pizza Crust Market Analysis by Mordor Intelligence

The gluten-free pizza crust market size is expected to increase from USD 3.83 billion in 2025 to USD 4.03 billion in 2026 and reach USD 5.23 billion by 2031, growing at a CAGR of 6.39% over 2026-2031. In 2025, rice-flour crusts anchored the category's value. However, cauliflower-based and ancient-grain formulations are gaining momentum. Consumers increasingly associate vegetable content, macrobalanced nutrition, and clean labels with wellness. Improvements in the cold chain, FDA's alignment with the <20 ppm rule, and the rapid expansion of quick-service outlets have elevated gluten-free menu penetration to 42.7% by mid-2024, enhancing mainstream visibility. Established brands are safeguarding their market share through high-moisture extrusion patents, direct-to-consumer subscriptions, and third-party certifications. Meanwhile, challengers are capitalizing on opportunities in plant-protein hybrids and regional fresh programs. The gluten-free pizza crust market is witnessing moderate consolidation, yet there's ample room for product and channel innovation. Shopper loyalty is notably high among medically-driven buyers, while lifestyle users remain more exploratory.

Key Report Takeaways

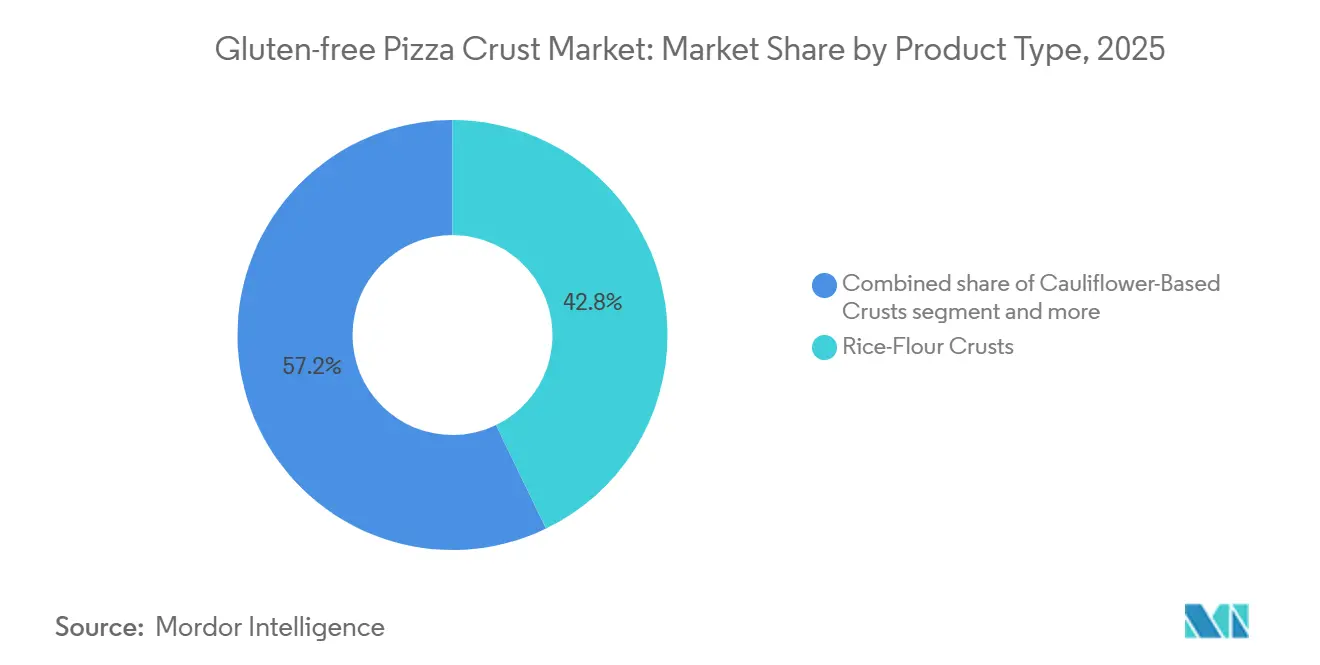

- By product type, rice-flour crusts led with 42.83% revenue share in 2025; cauliflower-based variants are projected to record 6.84% CAGR through 2031.

- By form, frozen formats captured 61.55% share of the gluten-free pizza crust market size in 2025, while fresh formats are advancing at an 8.39% CAGR over 2026-2031.

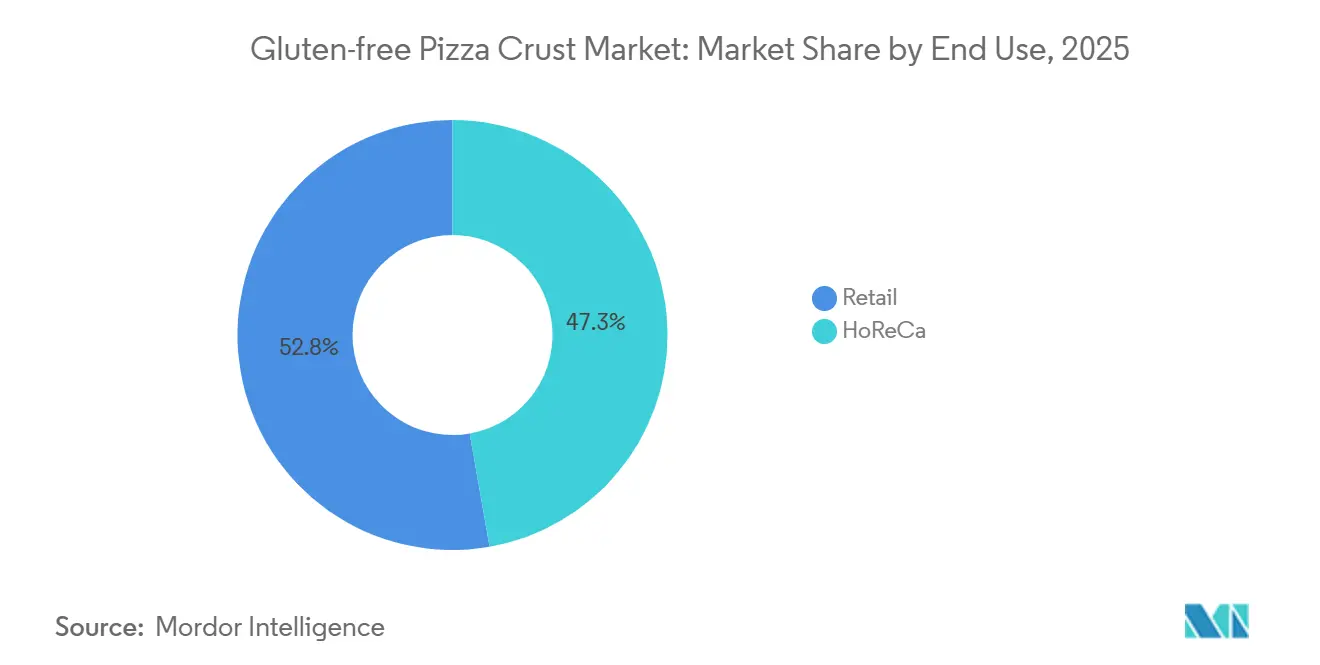

- By end user, retail channels accounted for 52.75% revenue share of the gluten-free pizza crust market size in 2025, and HoReCa is forecast to expand at a 9.55% CAGR to 2031.

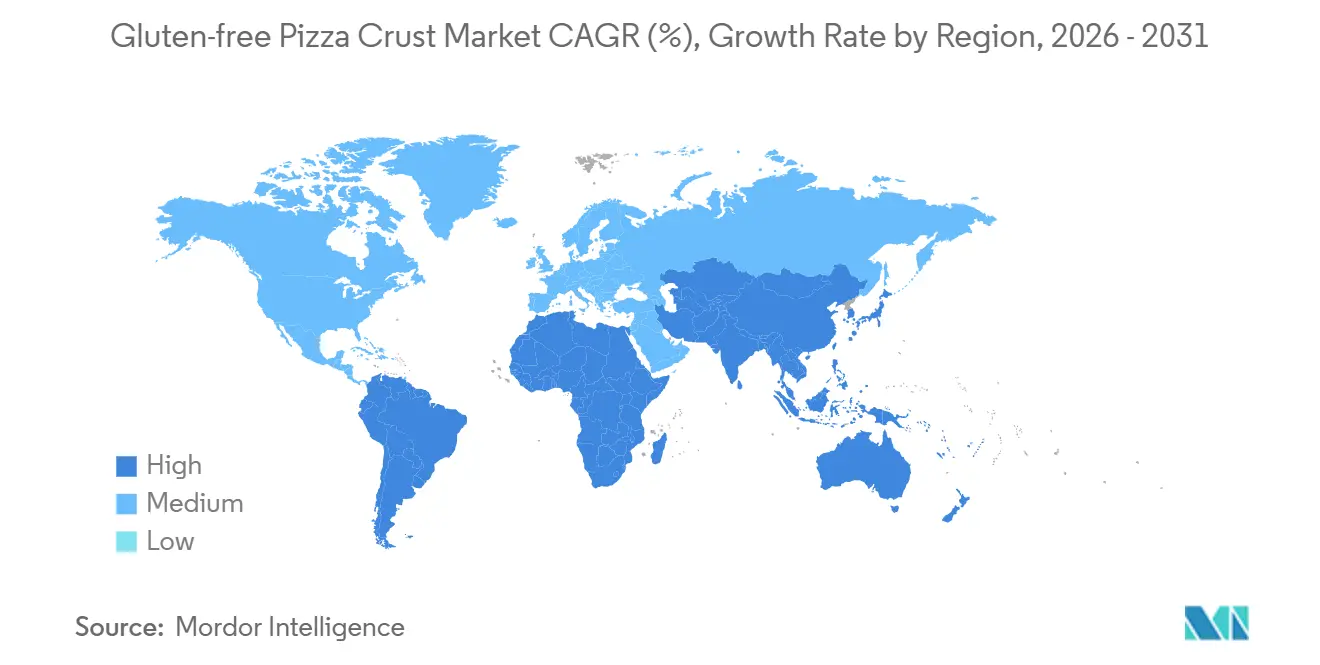

- By geography, North America held 37.19% of the gluten-free pizza crust market share in 2025; Asia-Pacific is recording the highest 7.18% CAGR during 2026-2031.

- Dr. Schär, Conagra Brands, Rich Products, and Schwan’s Company together controlled about one-half of the gluten-free pizza crust market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gluten-free Pizza Crust Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising celiac disease and non-celiac gluten sensitivity prevalence | +1.2% | Global focus in North America and Europe | Medium term (2-4 years) |

| Expansion of mainstream restaurant and QSR gluten-free menus | +1.5% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Advances in frozen and ready-to-bake technologies | +0.8% | Global | Medium term (2-4 years) |

| Certification and clean-label momentum | +0.6% | Global | Long term (≥ 4 years) |

| High-moisture extrusion achieving wheat-like texture | +0.5% | North America and Europe | Long term (≥ 4 years) |

| Direct-to-consumer subscription models | +0.4% | North America, Europe, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising celiac disease and non-celiac gluten sensitivity prevalence

Globally, 0.7% to 2.9% of the population is affected by celiac disease. In the U.S., about 3.3 million people manage this condition, highlighting a significant and expanding market for gluten-free products[1]Source: DrSchar Institute, "Celiac disease: prevalence and incidence", drschaer-institute.com. In the United Kingdom, 676,000 diagnosed consumers shelled out GBP 3.3 billion on certified foods in 2025, signaling a lucrative commercial opportunity for manufacturers and retailers catering to this niche. With females being diagnosed at twice the rate of males, there's a noticeable push for smaller-format SKUs and a diverse range of flavors to meet varying consumer preferences. Commodity relief in April 2025 saw rice prices at USD 14.20 per cwt, bolstering profit margins for producers by reducing input costs. Furthermore, regulatory clarity from the FDA and GFCO diminishes litigation risks, providing a stable framework for product development and certification. Together, these elements are driving the expansion of the gluten-free pizza crust market, making it an attractive segment for stakeholders.

Expansion of mainstream restaurant and QSR gluten-free menus

By mid-2024, gluten-free menu mentions surged over 30% in just four years, achieving a notable 42.7% penetration in U.S. restaurants. This shift has elevated the gluten-free pizza crust from a specialty item to a staple. Major chains like Pizza Hut, Papa John’s, and Domino’s have rolled out certified gluten-free crusts, bolstering household purchase signals. Despite these advancements, Coeliac UK reports that 77% of diners still inadvertently consume gluten[2]Source: Coeliac UK, "New Coeliac UK report highlights the progress and challenges of eating out", coeliac.org.uk. In response, chains are investing in segregated production lines and third-party audits, a move that's not only boosting consumer trust but also increasing the average ticket value. Highlighting the industry's direction, the National Restaurant Association has spotlighted allergen-friendly icons as one of its top trends for 2026, underscoring the synergy between regulation and revenue. With consumers enjoying safe gluten-free pizza dining out, many are now recreating that experience at home with retail frozen crusts, driving growth across multiple channels.

Advances in frozen and ready-to-bake technologies

High-moisture extrusion, utilizing 30-70% water and fine-tuned screw speeds, crafts rice-based doughs with elastic networks akin to wheat, effectively bridging the historical texture divide that has long challenged gluten-free products. This process ensures that gluten-free doughs achieve a texture and elasticity comparable to their wheat-based counterparts, enhancing their appeal to consumers. Techniques like ultrasound-assisted and pressure-shift freezing generate micro-ice crystals, which not only reduce drip loss but also ensure a 12-18 month shelf life without compromising product quality. These advancements address critical challenges in maintaining the freshness and structural integrity of gluten-free products over extended periods. These innovations pave the way for notable product launches, including Rich Products’ cauliflower pinsa, which offers a unique take on traditional pizza bases, and T. Marzetti’s gluten-free Texas Toast, catering to consumers seeking diverse gluten-free options. Together, these advancements significantly expand the offerings in the gluten-free pizza crust market, addressing both quality and variety demands while meeting the growing consumer preference for gluten-free alternatives.

Certification and clean-label momentum

Harmonized thresholds set by the FDA at <20 ppm, GFCO at 10 ppm, and the EU at 20 mg/kg, enable recipes to cater to multiple regions, ensuring compliance across diverse regulatory landscapes. These unified standards reduce the complexity of product formulation and streamline global distribution. Recently, Saudi Arabia, Argentina, and India adopted similar limits, simplifying export processes and reducing the need for region-specific adjustments, thereby enhancing operational efficiency for manufacturers. Clean-label cues significantly boost consumer trust; in 2026, Simple Mills, after securing Non-UPF verification on 20 SKUs, swiftly claimed prominent shelf space, reflecting the growing demand for transparent and health-conscious products. This achievement highlights the increasing importance of certifications in influencing consumer purchasing decisions. With certification costs soaring to 8-12% of COGS, a significant barrier emerges, fortifying loyalty among incumbents in the gluten-free pizza crust market by deterring new entrants, fostering brand reliability, and creating a competitive advantage for established players.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High ingredient and production costs | -0.9% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Regulatory and certification complexities | -0.5% | Emerging markets in South America, MEA, Asia-Pacific | Medium term (2-4 years) |

| Limited shelf life of fresh crusts | -0.3% | North America and Europe fresh segments | Short term (≤ 2 years) |

| Climate-driven volatility in cauliflower supply | -0.4% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High ingredient and production costs

While broader commodity markets have softened, specialty gluten-free flours continue to command premium prices. In April 2024, lentils fetched an average of USD 36.10 per cwt. Chickpeas, on the other hand, were priced between USD 26.40 and USD 31.10 per cwt. Rice, which makes up 42.83% of the market volume, traded at USD 14.20 per cwt. This marked a USD 3.10 decline from the previous year, yet rice prices remained 15–20% higher than conventional wheat flour when accounting for protein content. The output of pulse-based flours, crucial for ancient-grain blends, saw significant growth: chickpea production jumped by 30%, and lentil output skyrocketed by 72%. This surge in supply exerted downward pressure on spot prices throughout 2024 and 2025. Downstream processes like milling, sieving, and microbial testing added an extra 25–35% to landed costs. This increase in costs particularly squeezed margins for mid-tier brands that couldn't secure long-term supply agreements. Brands maintaining dedicated gluten-free production lines, performing allergen tests, and undergoing facility audits faced an additional overhead of 8–12% compared to those using shared-line operations. Regulatory bodies like the FDA and EFSA enforce strict compliance thresholds, capping at under 20 ppm, underscoring the non-negotiable nature of these measures. Yet, heightened price sensitivity in retail channels constrains manufacturers' ability to transfer these accumulated costs to consumers.

Regulatory and certification challenges

Gluten-free labeling compliance varies globally: the FDA enforces under 20 ppm, GFCO sets 10 ppm, the EU follows Regulation 828/2014, Argentina's ANMAT applies 10 ppm via Joint Resolution 32/2023, Brazil's ANVISA enforces Law 10.674, and Saudi Arabia's SFDA adheres to GSO 1021. Each jurisdiction's unique requirements complicate supply chains and increase costs. From April 2025, Saudi Arabia mandates gluten-free certificates for imported cereals, ready meals, and infant foods under GSO 1021[3]Source: Saudi Food and Drug Authority, "Conditions and Requirements for Food Clearance", sfda.gov.sa. Retail products must include Arabic translations and SFDA registration, raising entry barriers for North American and European exporters. Argentina's ANMAT uses the ELISA R5 Méndez method and requires a "libre de gluten" symbol, while Brazil's ANVISA enforces presence/absence labeling. These mandates force manufacturers to create multiple labels, reducing economies of scale in international distribution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rice-Flour Dominates yet Vegetable Hybrids Surge

In 2025, rice-flour crusts led the gluten-free pizza crust market, capturing 42.83% of the total revenue. Their dominance stems from the ready availability of raw materials, priced at approximately USD 14.20 per cwt, and a robust milling infrastructure that guarantees a steady supply and scalability. Furthermore, the adoption of pregelatinized rice flour, combined with advanced extrusion technologies, streamlines production. These efficiencies empower manufacturers to create frozen crusts boasting an 18-month shelf life, all while maintaining texture and quality. Consequently, rice-based crusts stand out as the most economical and widely embraced choice in the market.

Cauliflower-based crusts are the market's fastest-growing segment, with projections indicating a CAGR of 6.84% through 2031. This surge is fueled by a rising consumer shift towards vegetable-based alternatives, bolstered by perceived health advantages. Innovations, like Caulipower’s high-protein product debut in 2026, further amplify this trend. However, while cauliflower crusts are gaining popularity, their production is not without challenges. The formulations necessitate extra moisture extraction for binding, leading to a 20% uptick in energy costs relative to rice-based methods. This complexity not only elevates the price point but also carves out a premium market position. As a result, cauliflower crusts are emerging as a distinct, health-centric choice in the gluten-free arena.

By Form: Frozen Retains Scale, Fresh Wins Craft Credentials

In 2025, frozen gluten-free pizza crusts dominated the market, accounting for 61.55% of total sales. Their market leadership stems from a shelf stability of 12–18 months, a penetration rate in freezers exceeding 95%, and robust retailer backing, with 8–12 linear feet of shelf space dedicated to certified products. The incorporation of cryoprotectants like trehalose prevents recrystallization, ensuring a consistent texture and easing long-distance distribution. This logistical edge enables frozen products to efficiently scale across regions, solidifying their status as the cornerstone of the gluten-free pizza crust market. With the global enhancement of cold-chain infrastructure, frozen formats are poised to uphold their dominant stance.

Fresh gluten-free pizza crusts are emerging as the fastest-growing segment, with projections indicating a CAGR of 8.39%. This surge is attributed to urban consumers who are increasingly willing to pay a premium for products they perceive as artisanal and freshly made. Yet, the gluten-free nature of these crusts compromises elasticity, leading to retrogradation within 28 days, even when refrigerated, thus curtailing shelf life. To counteract this challenge, brands frequently set up localized production in major metropolitan hubs like New York and London. This strategy not only safeguards texture and quality but also, while it may limit expansive distribution, bolsters niche growth and amplifies product differentiation in tier-1 urban markets.

By End User: Retail Tops, HoReCa Accelerates with QSR Endorsements

In 2025, retail claimed the lion's share of the gluten-free pizza crust market, making up 52.75% of total expenditures. Supermarkets and hypermarkets have bolstered this dominance by dedicating entire aisles to gluten-free frozen meals, enhancing product visibility and accessibility. Coupled with robust in-store merchandising and a diverse product range, these strategies have fostered repeat purchases. Furthermore, online grocery platforms are amplifying this growth, offering bundled purchases shipped with dry ice to maintain product integrity. Collectively, these elements cement retail's status as the leading sales channel.

Meanwhile, the HoReCa segment is on a rapid ascent, with projections indicating a CAGR of 9.55%. This surge is largely attributed to industry giants like Pizza Hut, Domino’s, and Papa John’s, who are now incorporating certified gluten-free crusts into their menus. Such mainstream acceptance not only bolsters consumer trust but also normalizes gluten-free offerings in casual dining. To further enhance food safety, operators are adopting practices like using wrapped prebaked crusts and dedicated utensils to avoid cross-contact. As diners grow accustomed to these offerings, it not only boosts restaurant sales but also stimulates retail demand, driving the market's overall expansion.

Geography Analysis

In 2025, North America commanded a 37.19% market share, buoyed by FDA-compliant labeling, widespread freezer availability, and leadership from quick-service restaurants (QSRs) deploying certified dough nationwide. U.S. consumers shell out USD 5-7 for frozen options and USD 8-12 for fresh ones, reflecting a willingness to pay a premium for gluten-free alternatives. With celiac disease prevalence hovering around 1%, a consistent medical base emerges, driving demand for gluten-free products. Canada mirrors these regulations, facilitating smoother cross-border transactions and ensuring product consistency, while Mexico's adoption is primarily urban-centric, with demand concentrated in metropolitan areas where awareness and accessibility are higher.

Europe reaps benefits from the harmonization of Regulation 828/2014 and boasts a substantial diagnosed demographic. Notably, in the U.K., gluten-free expenditures hit GBP 3.3 billion in 2025, underlining the region's strong consumer base and growing preference for gluten-free options. Dr. Schär is channeling EUR 28 million to triple its cauliflower production across Italy, Spain, and Germany, targeting Germany's estimated 800,000 celiac individuals and addressing the rising demand for innovative gluten-free products. While Brexit-related paperwork has introduced costs, it hasn't dampened consumption in the U.K., where gluten-free products remain widely available. Scandinavia and Benelux report high per-capita consumption, driven by strong awareness and established supply chains, but Eastern Europe remains in its infancy, with limited infrastructure and lower consumer awareness.

Asia-Pacific leads with a robust 7.18% CAGR, driven by India's FSSAI implementing Chapter 2.14 and affluent Chinese consumers purchasing frozen products on platforms like Tmall and JD.com. The gluten-free pizza crust market sees further expansion with cold-chain developments and an increasing presence of Western QSRs in cities like Jakarta, Bangkok, and Manila. Japan and Australia, with their stringent regulations and comprehensive shelf presence, highlight mature niches. In Latin America, Brazil and Argentina spearhead growth, thanks to ANVISA Law 10.674 and ANMAT's 10 ppm stipulation. Meanwhile, the Middle East gains traction, bolstered by the Saudi SFDA's GSO 1021 regulation safeguarding certified imports. Despite cold-chain deficiencies hindering growth in deep rural areas, premium urban markets ensure the global ascent of the gluten-free pizza crust market.

Competitive Landscape

Major players, including Dr. Schär, Conagra’s Udi’s, Rich Products, and Schwan’s, dominate a moderately fragmented market. These incumbents operate dedicated gluten-free lines, audited to GFCO or NSF protocols, ensuring they meet the <10 ppm thresholds. This compliance secures them prime slots in major supermarkets, allowing them to maintain a strong foothold in the market. With robust cash flows, these leaders invest in high-moisture extrusion equipment, enabling them to replicate a wheat-like chew and broaden the reach of gluten-free pizza crusts. Such investments not only enhance product quality but also help cater to the growing consumer demand for gluten-free alternatives.

Disruptors such as Caulipower, Simple Mills, and Cappello’s leverage narratives centered on plant-forward and clean-label trends. Recognizing the potential, private equity firms have made strategic moves: Urban Farmer and Paine Schwartz acquired Caulipower in 2025, swiftly channeling funds into reseach and development, direct-to-consumer logistics, and developing protein-fortified SKUs. These efforts have enabled Caulipower to expand its product portfolio and strengthen its market presence. Meanwhile, Flowers Foods made headlines with its USD 795 million acquisition of Simple Mills, securing assets that boast Non-UPF verification, a feature highly valued by retailers. This acquisition has allowed Flowers Foods to tap into the increasing consumer preference for minimally processed and health-conscious products.

In this competitive landscape, technology and certification play pivotal roles. Patents on extrusion parameters, dehydration sequences, and freeze curves serve as barriers against imitation, ensuring that companies can protect their proprietary processes. Concurrently, third-party seals provide a quick reference for safety assurance, building consumer trust and brand credibility. Regional bakeries, experimenting with cassava or fermented rice recipes, first test their offerings at farmers’ markets, infusing cultural diversity into their products and gauging consumer interest before scaling production. As private equity platforms eye local brands for acquisition, a wave of consolidation looms, promising to diversify the gluten-free pizza crust market further while enabling smaller brands to access broader distribution networks and resources.

Gluten-free Pizza Crust Industry Leaders

-

Dr. Schär AG/SPA

-

Conagra Brands

-

Rich Products Corp.

-

Venice Bakery

-

Caulipower

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Flowers Foods finalized its USD 795 million purchase of Simple Mills, securing USD 240 million in net sales. This acquisition also enables Flowers Foods to broaden its distribution network, enhancing its market presence and strengthening its product portfolio.

- October 2024: Papa John's has broadened its gluten-free pizza crust offerings, now crafted from ancient grains. The company has also invested in staff training and dedicated production equipment for this line.

- September 2024: In response to the FDA's updated allergen-labeling guidance, the industry has voiced concerns, emphasizing the necessity for more transparent gluten disclosures. Stakeholders argue that clearer labeling is essential to ensure consumer safety and to address the growing demand for detailed allergen information, particularly for individuals with gluten sensitivities or celiac disease.

Global Gluten-free Pizza Crust Market Report Scope

Gluten-free pizza crusts are defined as pizza bases made without wheat, barley, rye, or other gluten-containing ingredients, typically utilizing alternative flours and starches such as rice, corn, almond, or potato. The scope of the market includes product type, form, end use, and geography. By product type, the market is segmented into rice flour crusts, cauliflower-based crusts, ancient-grain crusts, and other types of pizza crusts. Based on the form, the market is segmented into frozen crust and fresh crust. Based on end use, the market is segmented into HoReCa and retail. The report provides a detailed analysis of major economies across North America, Europe, Asia-Pacific, South America, the Middle East, and Africa.

| Rice-flour Crusts |

| Cauliflower-based Crusts |

| Ancient-Grain Crusts |

| Other Types |

| Frozen Crust |

| Fresh Crust |

| HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Grocery Stores | |

| Online Retail Stores | |

| Other Retailers |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Poland | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Product Type | Rice-flour Crusts | |

| Cauliflower-based Crusts | ||

| Ancient-Grain Crusts | ||

| Other Types | ||

| By Form | Frozen Crust | |

| Fresh Crust | ||

| By End User | HoReCa | |

| Retail | Supermarkets/Hypermarkets | |

| Grocery Stores | ||

| Online Retail Stores | ||

| Other Retailers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Poland | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the gluten free pizza crust market?

The gluten free pizza crust market size is valued at USD 4.03 billion in 2026 and is forecast to reach USD 5.23 billion by 2031.

Which region leads the market today?

North America holds the largest share at 37.19% in 2025, supported by strong regulatory oversight and widespread product availability.

Which product type is growing fastest?

Cauliflower-based crusts are expected to post a 6.84% CAGR through 2031, benefiting from plant-based and clean-label demand.

Why do gluten-free crusts cost more than regular pizza bases?

They rely on specialised flours, dedicated production lines and third-party certification, all of which increase manufacturing costs by roughly 2–2.5 times.

Page last updated on: