Gluten-Free Pasta Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.96 Billion |

| Market Size (2031) | USD 5.26 Billion |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

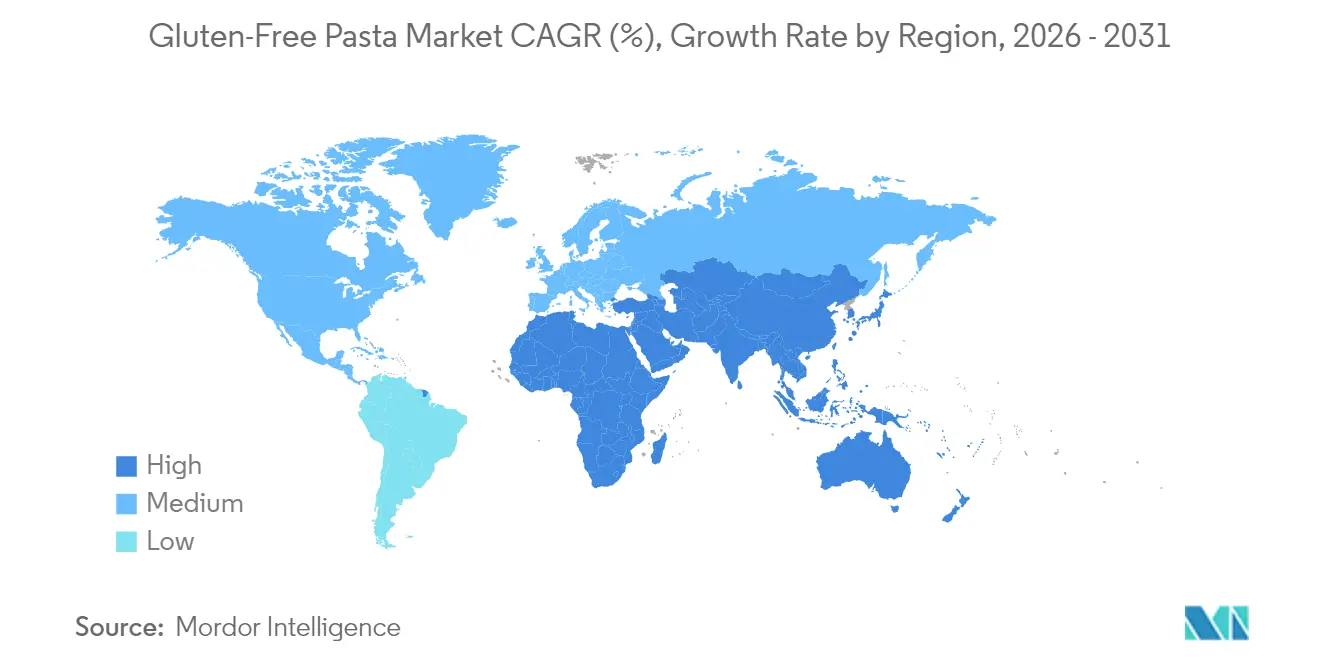

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

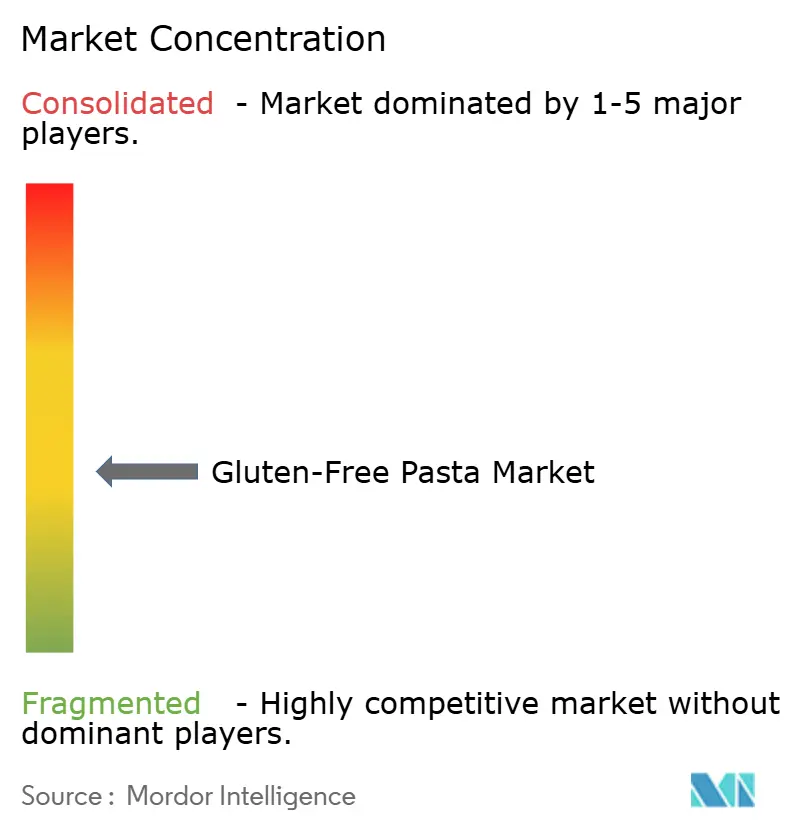

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gluten-Free Pasta Market Analysis by Mordor Intelligence

The gluten-free pasta market size is expected to grow from USD 3.74 billion in 2025 to USD 3.96 billion in 2026 and is forecast to reach USD 5.26 billion by 2031 at 5.85% CAGR over 2026-2031. The market expansion is primarily attributed to heightened consumer awareness regarding gluten-related health conditions, specifically celiac disease and non-celiac gluten sensitivity, coupled with an increasing shift toward health-conscious and allergen-free dietary preferences. Market demand is driven by both medical requirements and wellness-oriented lifestyle modifications. Manufacturing entities are strengthening their market position through product enhancement initiatives, focusing on improving organoleptic properties and nutritional composition by incorporating alternative grain sources, including rice, corn, quinoa, millet, and legumes. The market trajectory is additionally influenced by the rising adoption of plant-based and clean-label food products, particularly among younger demographics and urban populations. The market penetration has been facilitated by extensive distribution networks encompassing supermarkets, hypermarkets, and the rapidly expanding e-commerce channels.

Key Report Takeaways

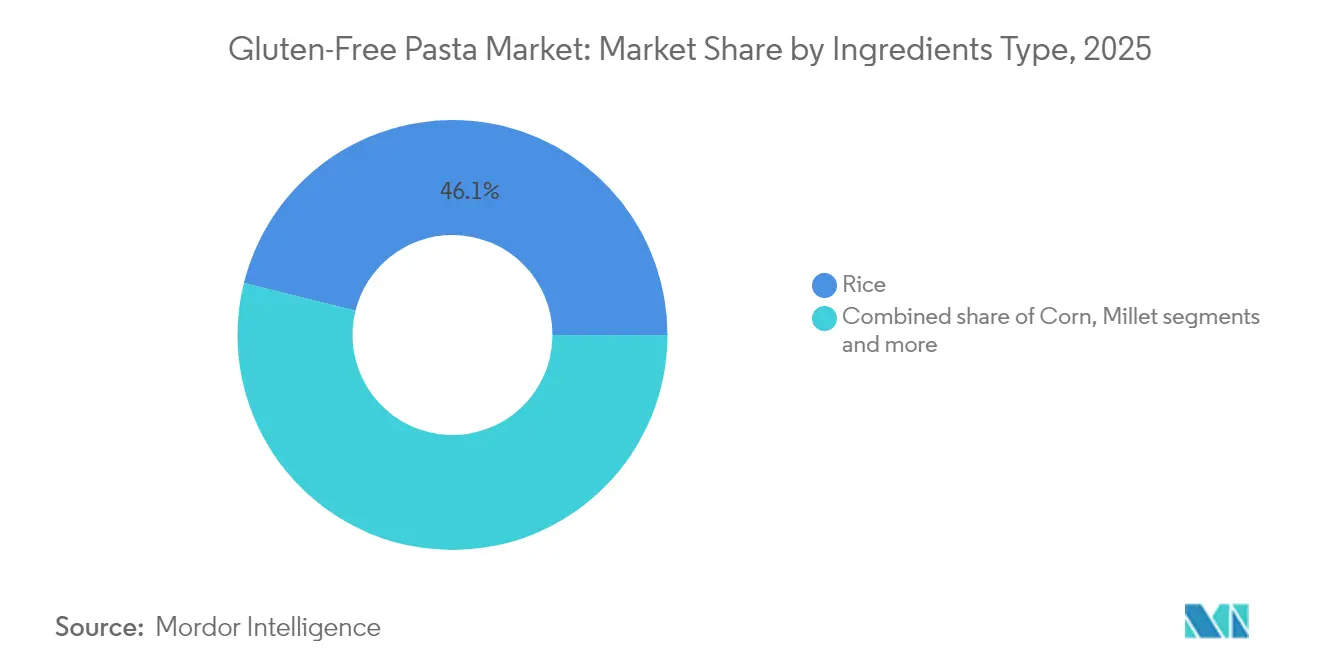

- By ingredients type, rice-based products led with 46.12% of gluten-free pasta market share in 2025, while millet-based products are projected to record a 6.74% CAGR through 2031.

- By product type, dried formats accounted for 66.55% of the gluten-free pasta market size in 2025; instant variants are forecast to expand at 7.05% CAGR.

- By shape, spaghetti dominated with 77.62% revenue share in 2025, whereas macaroni shows the quickest growth at 6.62% CAGR.

- By distribution channel, supermarkets/hypermarkets controlled 55.10% of sales in 2025; online retail is advancing at a 6.85% CAGR.

- By geography, Europe held 38.55% of global revenue in 2025, while Asia-Pacific is set to grow at 6.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gluten-Free Pasta Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of gluten-free diets as lifestyle choices | +1.2% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| Improved taste and texture in gluten-free pasta offerings | +0.9% | Global | Short term (≤ 2 years) |

| Launch of multi-ingredients pasta catering to nutritional needs | +0.8% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Increase prevalence of celiac disease and gluten intolerance | +1.1% | Global | Long term (≥ 4 years) |

| Increasing disposable income in developing countries | +1.0% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Technological advancements in gluten-free pasta production | +0.7% | Global, led by Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adoption of Gluten-Free Diets as Lifestyle Choices

The gluten-free pasta market demonstrates significant expansion attributed to the widespread adoption of gluten-free dietary preferences as a lifestyle choice. This market growth is primarily driven by increased health consciousness among consumers, evolving dietary patterns, and enhanced awareness regarding the potential health benefits of gluten-free consumption, particularly among individuals without diagnosed celiac disease or gluten sensitivity. Consumer perception of gluten-free pasta has evolved substantially, with many individuals considering it a superior nutritional alternative, correlating its consumption with enhanced digestive function and improved overall health outcomes, thereby extending market penetration beyond medical necessity. According to GS1 Italy, the gluten-free food products represented 11.1% of total food sales value in Italy during 2023., illustrating the substantial mainstream market penetration and lifestyle-oriented adoption of gluten-free food products, specifically pasta [1]Source: GS1 Italy, “Immagino Observatory, Fifteenth Edition 2024”, servizi.gs1it.org . This market trajectory aligns with the increasing consumer demand for plant-based alternatives, organic food products, and clean-label offerings, as gluten-free pasta, manufactured from alternative ingredients, fulfills both nutritional requirements and accommodates diverse dietary specifications.

Improved Taste and Texture in Gluten-Free Pasta Offerings

The market demonstrates substantial growth driven by significant advancements in product formulation, particularly in taste and texture enhancement. Traditional gluten-free pasta products previously encountered substantial market resistance due to suboptimal organoleptic properties, including compromised taste profiles, inconsistent textural attributes, and restricted product diversification compared to conventional wheat-based alternatives. Contemporary technological innovations in food processing methodologies, coupled with sophisticated ingredient development, have fundamentally transformed product quality parameters, facilitating market penetration among both medical necessity consumers and lifestyle-oriented demographics. The market evolution is substantially attributed to the strategic incorporation of alternative grain compositions, including brown rice, lentils, quinoa, corn, and chickpea formulations, frequently utilized in precise combinations to optimize structural integrity, sensory characteristics, and nutritional composition. For instance, in January 2024, Suma Wholefoods introduced a new range of oat pastas manufactured using oat, corn, and rice flours instead of conventional wheat.

Launch of Multi-Ingredients Pasta Catering to Nutritional Needs

The gluten-free pasta market demonstrates significant growth potential through the strategic introduction of multi-ingredient formulations designed to address diverse nutritional requirements. Market expansion is primarily attributed to the increasing prevalence of gluten intolerance, coupled with the substantial adoption of plant-based dietary preferences. Manufacturing entities are implementing advanced product development strategies, specifically focusing on innovative grain blend formulations to meet these evolving consumer requirements. For instance, in June 2024, Nuttee Bean Co. introduced its premium offering, Favalicious Fava Protein Pasta, a specialized fava bean-based formulation comprising three essential ingredients. The product delivers substantial nutritional value with 19 grams of protein content, 16 grams of dietary fiber, and maintains 13 net carbohydrates per serving, while adhering to gluten-free, non-GMO, vegan, and zero-sugar specifications. This product development initiative directly corresponds to the evolving preferences of health-conscious consumer segments, particularly Millennials and Generation Z demographics, who demonstrate increased demand for clean-label and high-protein nutritional options.

Increase Prevalence of Celiac Disease and Gluten Intolerance

The increasing prevalence of celiac disease and non-celiac gluten sensitivity is driving growth in the gluten-free pasta market. Health concerns related to these conditions are influencing consumer dietary choices. Enhanced awareness among medical professionals and the public has led to more frequent diagnoses. In Italy, according to the Ministry of Health, approximately 265,000 individuals were affected by celiac disease in 2023, with Lombardy being the region that recorded the highest number at over 49,200 cases [2]Source: Ministry of Health, "Annual Report To Parliament On Celiac Disease – Annual 2023", static.celiachia.it . Individuals with non-celiac gluten sensitivity experience symptoms including gastrointestinal discomfort, headaches, and fatigue when consuming gluten. The necessity to manage these conditions through gluten-free diets has increased the demand for alternatives, including pasta. Public awareness campaigns and dietary recommendations from healthcare professionals have further emphasized the importance of gluten-free products. These factors are expected to create growth opportunities for the gluten-free pasta market during the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher price compared to conventional pasta | -1.3% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Limited consumer awareness in emerging markets | -0.8% | Asia-Pacific, Middle East and Africa, Latin America | Medium term (2-4 years) |

| Strict regulatory requirements for gluten-free certification | -0.5% | Global, varying by jurisdiction | Long term (≥ 4 years) |

| Competition from other alternative pasta products | -0.7% | Global, intensifying in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Price Compared to Conventional Pasta

The premium pricing of gluten-free pasta creates significant market penetration barriers, especially in price-sensitive segments and emerging economies where limited disposable income restricts specialty food adoption. Gluten-free pasta products command a 50-100% price premium compared to conventional wheat-based pasta due to higher raw material costs, specialized manufacturing processes, and smaller production volumes that limit economies of scale. The Food and Drug Administration (FDA) regulations for gluten-free labeling require products to contain less than 20 parts per million of gluten, necessitating dedicated production facilities and extensive testing protocols that increase operational costs. This price gap becomes more significant during economic downturns when consumers focus on essential purchases rather than premium food items. However, advancing manufacturing technologies and increasing production volumes may reduce costs, potentially decreasing the price difference between gluten-free and conventional pasta during the forecast period.

Limited Consumer Awareness in Emerging Markets

A significant restraint for the gluten-free pasta market, particularly in emerging markets, is the limited consumer awareness regarding gluten intolerance, celiac disease, and the benefits of gluten-free diets. Despite the rising prevalence of gluten-related disorders worldwide, many consumers in developing regions remain unaware of gluten's health impacts and the availability of gluten-free alternatives, which hampers market penetration and growth. In countries across Asia-Pacific, Africa, and parts of Latin America, gluten-free diets are often misunderstood or not widely recognized unless medically prescribed, which restricts the potential consumer base to those with confirmed health conditions. Many consumers in these regions associate gluten-free products with weight-loss trends or luxury diets, resulting in skepticism or disinterest. The situation is further complicated by insufficient labeling transparency, inadequate regulatory oversight, and limited public health initiatives to promote understanding of gluten-related health concerns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredients Type: Rice Dominates While Alternatives Emerge

In 2025, rice-based formulations accounted for 46.12% of the gluten-free pasta market. The market expansion is primarily driven by the increasing prevalence of celiac disease and gluten sensitivity among consumers worldwide. Rice's neutral flavor, established supply chain infrastructure, and broad consumer acceptance across regions drive this market dominance. The neutral taste of rice makes it compatible with various sauces and ingredients, serving as an effective wheat pasta substitute. According to the United States Department of Agriculture (USDA), rice production reached 535.8 million metric tons in 2024/25, ensuring a stable raw material supply for manufacturers . This availability maintains consistent production costs and supports large-scale manufacturing and distribution across developed and emerging markets.

Millet-based formulations are expected to grow at a CAGR of 6.74% from 2026 to 2031. This growth is driven by millet's nutritional profile, which includes high protein content, essential minerals, and dietary fiber. The increasing consumer preference for alternative grains, particularly in emerging economies, combined with the growing adoption of plant-based diets, strengthens millet-based pasta's market position. The rising health consciousness among consumers and the growing demand for nutrient-dense, gluten-free options contribute to market expansion. Additionally, millet's agricultural sustainability and adaptability to various climatic conditions make it a reliable raw material for gluten-free pasta production. Government initiatives promoting millet cultivation and consumption, particularly in developing regions, further support market growth.

By Product Type: Dried Formats Lead While Instant Gains Momentum

Dried pasta maintains a dominant position in the gluten-free pasta market, accounting for 66.55% market share in 2025. This dominance stems from consumer preferences for shelf-stable products that offer convenience and extended storage life without refrigeration. Dried gluten-free pasta serves diverse consumer groups, including families and individuals seeking simple meal solutions, due to its long shelf life and widespread availability through retail and online channels. The consistent performance and adaptability of dried pasta have established it as the primary choice for consumers seeking gluten-free alternatives that maintain quality in taste and texture.

The instant pasta segment is projected to grow at 7.05% CAGR through 2031, driven by consumers requiring quick meal preparation while adhering to gluten-free diets. While canned and frozen varieties primarily serve foodservice operations where portion management and efficient preparation are essential, the instant segment's growth reflects evolving consumer preferences for time-efficient meal options. Manufacturers have enhanced instant pasta formulations to address quality concerns, developing products that retain structural integrity and nutritional value despite quick preparation requirements. The segment's expansion aligns with increasing urbanization and evolving work schedules, particularly among younger consumers willing to pay more for convenience-oriented products.

By Shape: Spaghetti's Cultural Dominance Persists

In the gluten-free pasta market, spaghetti maintains a predominant market position, accounting for 77.62% market share in 2025. This substantial market concentration in spaghetti variants demonstrates the persistent consumer preference for conventional pasta configurations within gluten-free alternatives. The significant market presence of gluten-free spaghetti is attributed to its operational versatility, standardized preparation protocols, and comprehensive substitution capabilities for traditional wheat-based variants across multiple culinary applications, establishing its fundamental position in global dietary consumption patterns.

The macaroni segment exhibits a substantial growth trajectory, projecting a CAGR of 6.62% through 2031. This growth progression is primarily attributed to increasing consumer demand for diversified pasta configurations that facilitate enhanced preparation efficiency in domestic culinary operations, particularly in standardized household meal preparation and nutritional recipe formulations. The extensive retail distribution infrastructure for gluten-free macaroni variants, combined with systematic product development initiatives focusing on organoleptic property enhancement and nutritional optimization, has facilitated increased consumer integration into standardized meal preparation protocols.

By Distribution Channel: Retail Dominance with E-commerce Acceleration

Supermarkets/hypermarkets currently command 55.10% of the gluten-free pasta distribution market in 2025. Their market leadership position is attributed to their established physical retail infrastructure, comprehensive product assortment, and capacity to fulfill immediate consumer requirements. These retail establishments function as primary distribution points for consumers seeking established manufacturers and efficient access to gluten-free alternatives. Retail chains establish strategic distribution partnerships with manufacturers to maintain product availability. This is evidenced by Pasta Rummo's strategic expansion in the United States market in July 2023, wherein the company introduced 11 product variants, including gluten-free spaghetti, across the entire Whole Foods Market retail network.

The online retail distribution segment demonstrates superior growth potential with a projected CAGR of 6.85% during 2026-2031. This growth trajectory is attributed to comprehensive product portfolios, structured subscription-based procurement systems, and enhanced market penetration in regions with limited physical retail infrastructure. E-commerce platforms facilitate the distribution of multiple gluten-free pasta manufacturers through optimized logistics networks and systematic subscription programs. The digital retail segment exhibits market expansion through implemented direct-to-consumer distribution frameworks, structured digital promotional strategies, and health-oriented marketing initiatives.

Geography Analysis

Europe holds a 38.55% share of the gluten-free pasta market in 2025, supported by high celiac disease awareness, established diagnosis protocols, and the importance of pasta in Mediterranean diets. The region's market growth is reinforced by regulatory frameworks, including prescription subsidies for celiac patients in Italy and the United Kingdom. The diverse European culinary traditions enable consumers with dietary restrictions to maintain their cultural eating habits through gluten-free pasta options.

Asia-Pacific shows the highest growth rate with a 6.89% CAGR (2026-2031), attributed to urbanization, increased disposable incomes, and health awareness among middle-class consumers. China and India's position as major rice producers supports market development. The increasing consumption of processed foods, including gluten-free pizza, pasta, and bakery products, drives market expansion. Manufacturers are developing region-specific flavors to meet local preferences, supporting continued market growth.

North America demonstrates a strong market presence with extensive product variety. The United States Department of Agriculture (USDA)'s Crop Production reports show corn production at 14.9 billion bushels in 2024, providing raw materials for gluten-free pasta production. The region exhibits a premium product trend, with consumers accepting higher prices for nutritional benefits and clean-label products. Besides, South America and the Middle East and Africa show growth potential in urban areas and higher-income segments, despite awareness and distribution limitations. These challenges are being addressed through consumer education programs and retail network expansion.

Regulatory Landscape

Gluten-free pasta labeling is governed by jurisdiction-specific thresholds and verification expectations that shape formulation, testing, and facility controls. In the United States, FDA rules under 21 CFR 101.91 set a less than 20 parts per million gluten threshold for voluntary "gluten-free" claims, with added recordkeeping expectations where validated analytical methods are limited (notably in fermented or hydrolyzed products). In the European Union, Commission Implementing Regulation (EU) No 828/2014 similarly limits "gluten-free" to foods containing no more than 20 mg/kg (20 ppm) gluten and reserves "very low gluten" for certain processed products up to 100 mg/kg, while also specifying that oats used in products carrying these statements must be specially produced and handled to prevent contamination.

Regulatory attention continues to focus on labeling clarity and cross-contact controls as gluten-free demand expands beyond medically diagnosed consumers. In the United States, the FDA issued a Request for Information in early 2026 on labeling and preventing cross-contact of gluten for packaged foods, indicating increased scrutiny on ingredient disclosure practices and manufacturing controls that reduce unintended gluten presence. For manufacturers selling across regions, the shared 20 ppm anchor in the U.S. and EU provides a common technical target, but it also raises the need for supplier verification, dedicated lines where feasible, and documented testing programs to support gluten-free claims across retail channels.

Competitive Landscape

The gluten-free pasta market features moderate fragmentation, with both large food companies and specialized manufacturers competing in the market. Companies like Barilla Group and Ebro Foods S.A. use their extensive distribution networks and established brands to serve mainstream markets, while specialized firms such as Dr. Schär AG and Jovial Foods compete through focused product development and expertise in gluten-free consumer preferences.

The market has evolved from serving primarily medical needs to becoming a mainstream health food category, attracting both established food manufacturers and new companies targeting specific consumer segments. Besides, the competitive landscape is characterized by strategic partnerships, mergers, and acquisitions aimed at expanding market presence and achieving economies of scale. For instance, Saco Foods acquired Ancient Harvest and Pamela's brands in August 2024, which enhances the company's gluten-free portfolio and leverages shared services for growth.

Moreover, companies are investing in advanced extrusion equipment and ingredient processing technologies to enhance product quality and production efficiency. The competitive environment emphasizes research and development capabilities, with firms developing proprietary formulations and manufacturing processes. Success in the market depends on companies' ability to combine product innovation with efficient cost management, as consumers demand high-quality products at competitive prices compared to traditional pasta. Market players are also differentiating themselves through sustainable practices and clean-label ingredients to meet evolving consumer preferences.

Gluten-Free Pasta Industry Leaders

-

Dr. Schar AG

-

Barilla Group

-

Ebro Foods S.A.

-

Jovial Foods, Inc.

-

Eden Foods, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity additions and localization of manufacturing create space for brands to widen availability, stabilize supply, and meet retailer expectations for consistent allergen controls. In North America, May 2026 announcements highlighted two moves: Andriani S.p.A. (Felicia) started production at a new allergen-free, gluten-free facility in London, Ontario (65,000 square feet, USD 55 million, 15,000 tonnes annual capacity), while Barilla began a two-phase expansion at its Avon, New York site with an initial USD 145 million phase and a 52,000 square-foot building addition to add production and packaging lines. These investments align with the market shift toward broader mainstream distribution, where supermarkets and hypermarkets remain the largest channel (55.10% share in 2025), while online retail keeps expanding access to assortment for specialty diets.

Product opportunity also centers on improving texture and nutrition without diluting clean-label positioning, particularly as the category moves beyond rice-only formulations (rice held 46.12% share in 2025) toward multi-ingredient and pulse-based blends. Recent product activity in the sector, including multi-ingredient and protein-forward launches referenced in the report context, suggests consumer openness to trade up for higher protein and fiber claims, while technical work across extrusion and ingredient systems (hydrocolloids, psyllium, and protein enrichment from legume sources) targets the key performance gap versus wheat pasta. With strict "gluten-free" thresholds in both the U.S. and EU at 20 ppm, another opportunity lies in compliance-ready sourcing and manufacturing documentation, which can support brand trust and facilitate expansion into additional geographies and private-label programs that require strong allergen management.

Recent Industry Developments

- May 2026: Andriani S.p.A. (Felicia) started production at a new allergen-free and gluten-free facility in London, Ontario, adding in-market capacity and shortening supply lines for North American customers. The site was positioned to support better-for-you pasta demand with dedicated allergen controls, which can strengthen retailer confidence in gluten-free claims and consistency.

- February 2026: Ebro Foods S.A. completed the acquisition of the remaining 30% stake in Bertagni 1882 SpA, consolidating ownership of the Italian premium pasta business. The acquisition supports tighter operational control and portfolio integration, improving the group ability to align product development and manufacturing decisions across its pasta assets.

- January 2026: A renewable energy upgrade at Dr. Schar's German production sites in Dreihausen and Apolda involved adopting certified renewable electricity. The shift reinforces operational sustainability credentials and supports retailer and consumer expectations for responsible sourcing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers retail and foodservice sales of packaged gluten-free pasta products made without wheat gluten, which are commonly produced from rice, corn, legumes, or similar gluten-free flours, across all major regions.

Scope exclusions: We exclude naturally gluten-free plain rice staples sold as commodity grains (including bulk rice) and count only gluten-free pasta products positioned and sold as pasta.

Segmentation Overview

-

By Ingredients Type

- Rice

- Corn

- Millet

- Other Ingredients

-

By Product Type

- Dried

- Instant

- Canned and Frozen

-

By Shape

- Spaghetti

- Penne

- Fusilli

- Macaroni

- Others

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Store

- Online Retail Stores

- Other Distribution Channel

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand boundary and to collect external signals on gluten-free consumption and packaged pasta demand over time. We relied on public and official sources such as the US FDA for gluten-free labeling guidance, the USDA for food category context, the NIH and CDC for health and prevalence references that influence gluten-free adoption, FAOSTAT for agriculture production context, and UN Comtrade style customs statistics for directional trade signals.

To translate that context into a workable model, we also reviewed company annual reports, SEC-style filings, investor presentations, retailer category pages, and association websites to understand pack sizes, channel patterns, and ingredient shifts (such as rice-based versus legume-based). A paid subscription for company financials and news was used selectively to cross-check revenue direction and material events like distribution expansion. This list is illustrative only, and other public sources were also checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what desk sources cannot show consistently, mainly the real channel mix, price ladders, and repeat-buy behavior for gluten-free pasta across regions. We spoke with a spread of stakeholders such as brands, ingredient suppliers, contract manufacturers, distributors, and retail or foodservice buyers, and then used their inputs to confirm assumptions on volumes, pricing, and how products are labeled and merchandised.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | APAC: 40% |

| Mid tier: 54% | Functional/Unit leaders: 28% | EMEA: 33% |

| Smaller Players: 19% | Managers: 57% | Americas: 27% |

Market-Sizing & Forecasting

The core build used a top-down approach where gluten-free packaged pasta demand was reconstructed from a conventional pasta consumption pool, and then filtered using gluten-free adoption signals, labeled product availability, and expected penetration by channel and region. Once the first cut was formed, selective bottom-up approximations were used to corroborate totals, such as sampled shelf prices times observed product availability, plus distributor and retailer checks on turnover.

Key inputs used as sizing fingerprints included the share of rice-based gluten-free pasta, the dominance of dried formats, supermarket and hypermarket contribution versus online, and region-level differences in gluten-free adoption. When country-level detail was thin, proxy ratios were applied from similar markets based on income level, modern trade depth, and observed gluten-free shelf presence, and then adjusted after interview feedback.

For forecasting, scenario analysis was applied around a base case that links growth to label awareness, modern retail expansion, and pricing normalization, and then tested against expert expectations on how quickly shoppers repurchase in each region. Where inflation effects were material, price progression was treated separately from unit growth so the forecast stayed traceable.

Data Validation & Update Cycle

Outputs were checked against independent signals such as retail assortment changes, product launch intensity, and observed pricing bands, and then reworked when implied demand curves did not align with these checks. If a large variance showed up in a region or channel, the assumptions were rechecked, and targeted re-contact was done with interviewees to confirm whether the change was real or driven by the model.

Before sign-off, a multi-step analyst review was completed, including consistency checks across regions, ingredient mix, and channels, followed by a final pass to remove arithmetic and currency-timing issues. The report is refreshed annually, with interim updates for material events, and then a fresh validation pass is completed before delivery so clients receive the latest view.

Mordor Intelligence's Global Gluten Free Pasta Rice Market Market Size Compared With Other Published Estimates

Published market sizes for gluten-free pasta and for gluten-free pasta plus rice can be far apart because the product scope is not treated the same way, and because the year and currency timing behind pricing assumptions are often not aligned. Differences also show up when some models start from a broad gluten-free foods pool, while others start from pasta demand and then apply adoption logic.

By refreshing channel mix and pack-price assumptions each year, and then checking which items are labeled and sold as pasta, Mordor Intelligence keeps the count tied to gluten-free pasta sales and avoids pulling in plain rice staples or wider gluten-free pantry categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.74 B (2025) | |

| Global Data Platform A | USD 0.46 B (2025) | This estimate is published as a pasta-and-rice segment inside a wider gluten-free products tracking view, which can restrict what is counted to a narrow classification and miss parts of gluten-free pasta sold through certain channels or formats. |

| Industry Publisher B | USD 24.06 B (2025) | This estimate appears to use a much broader gluten-free pasta and rice scope, which can pull in adjacent gluten-free staple foods and inflate totals when the definition is not limited to pasta items that are marketed and purchased as pasta. |

The spread in the table is mainly explained by scope boundaries around pasta versus rice staples, followed by how price progression and channel coverage are treated in the current year. When assumptions are kept visible and reconciled with interview checks, the resulting number stays easier to replicate and update year after year.

Key Questions Answered in the Report

What is the current value of the gluten-free pasta market?

The gluten-free pasta market generated USD 3.96 billion in 2026 and is forecast to reach USD 5.26 billion by 2031.

Which region holds the largest share of gluten-free pasta sales?

Europe leads with 38.55% of global revenue in 2025, supported by stringent labeling regulations and high consumer awareness.

Which distribution channel is growing fastest?

Online retail is the quickest-growing channel, advancing at a 6.85% CAGR as consumers embrace e-commerce for specialized dietary needs.

What ingredient dominates gluten-free pasta formulations?

Rice-based pasta remains dominant, holding 46.12% share in 2025 because of its neutral taste and reliable texture.

Page last updated on: