Gluten-Free Bakery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

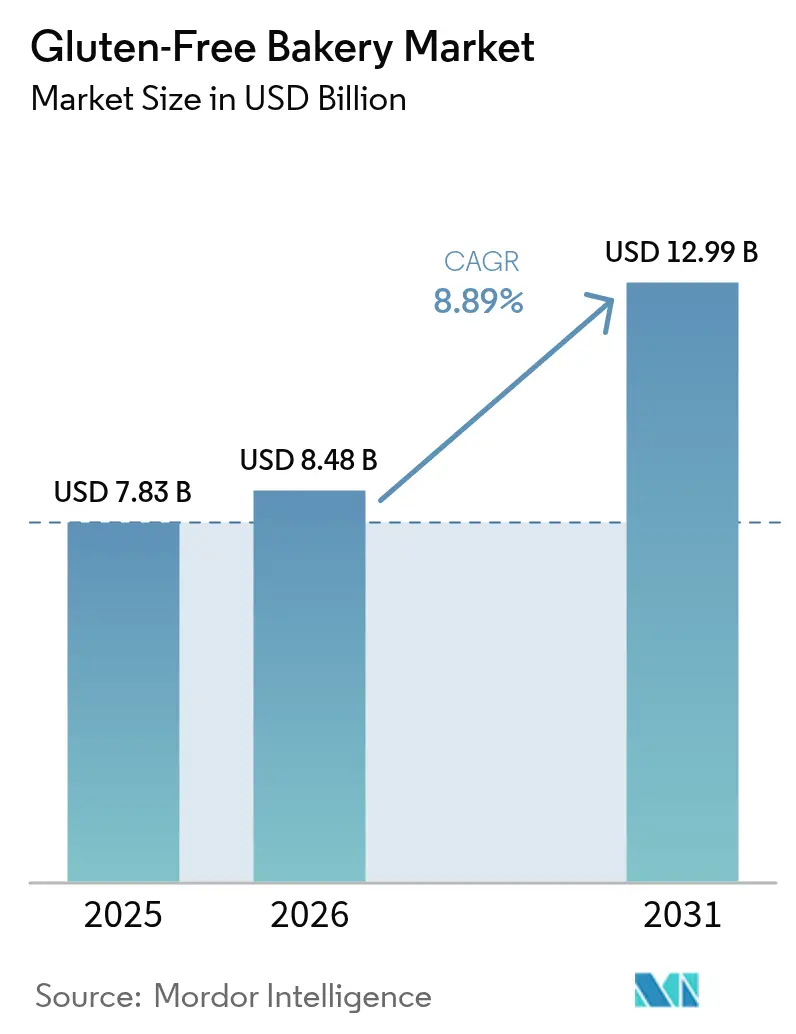

| Market Size (2026) | USD 8.48 Billion |

| Market Size (2031) | USD 12.99 Billion |

| Growth Rate (2026 - 2031) | 8.89% CAGR |

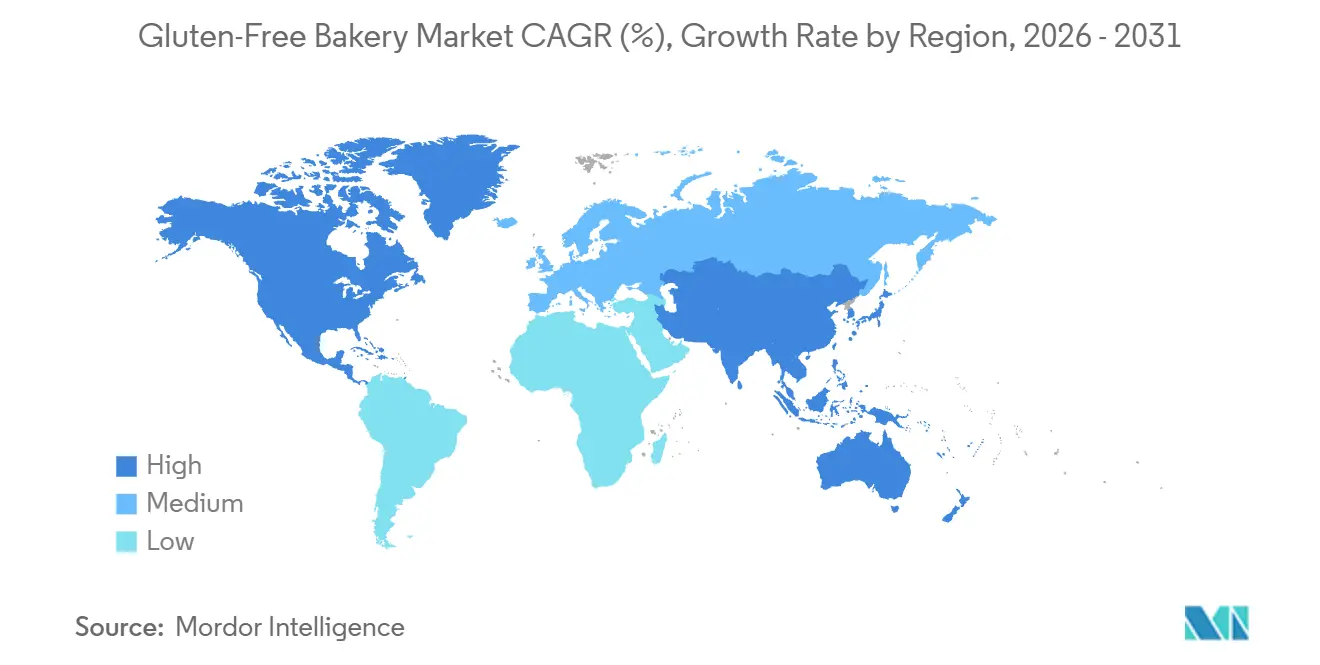

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gluten-Free Bakery Market Analysis by Mordor Intelligence

The Gluten-Free Bakery Products market size is expected to grow from USD 7.83 billion in 2025 to USD 8.48 billion in 2026 and reach USD 12.99 billion by 2031, with a CAGR of 8.89% from 2026 to 2031. Several factors are driving this growth, including increased detection of celiac disease, stricter regulations on cross-contact thresholds, stable specialty-flour costs due to record rice and corn harvests, and a shift by major food manufacturers toward premium clean-label recipes. Supermarkets are expanding their allergen-friendly product ranges, while e-commerce platforms are helping niche brands grow without needing physical stores. Climate-related challenges in rice and corn production have led to long-term sourcing contracts, reducing cost fluctuations. Manufacturers are combining functional benefits with indulgent textures, which is helping them raise average selling prices and attract flexitarian consumers. These consumers may not have gluten intolerance but are interested in the perceived digestive and wellness benefits of gluten-free products.

Key Report Takeaways

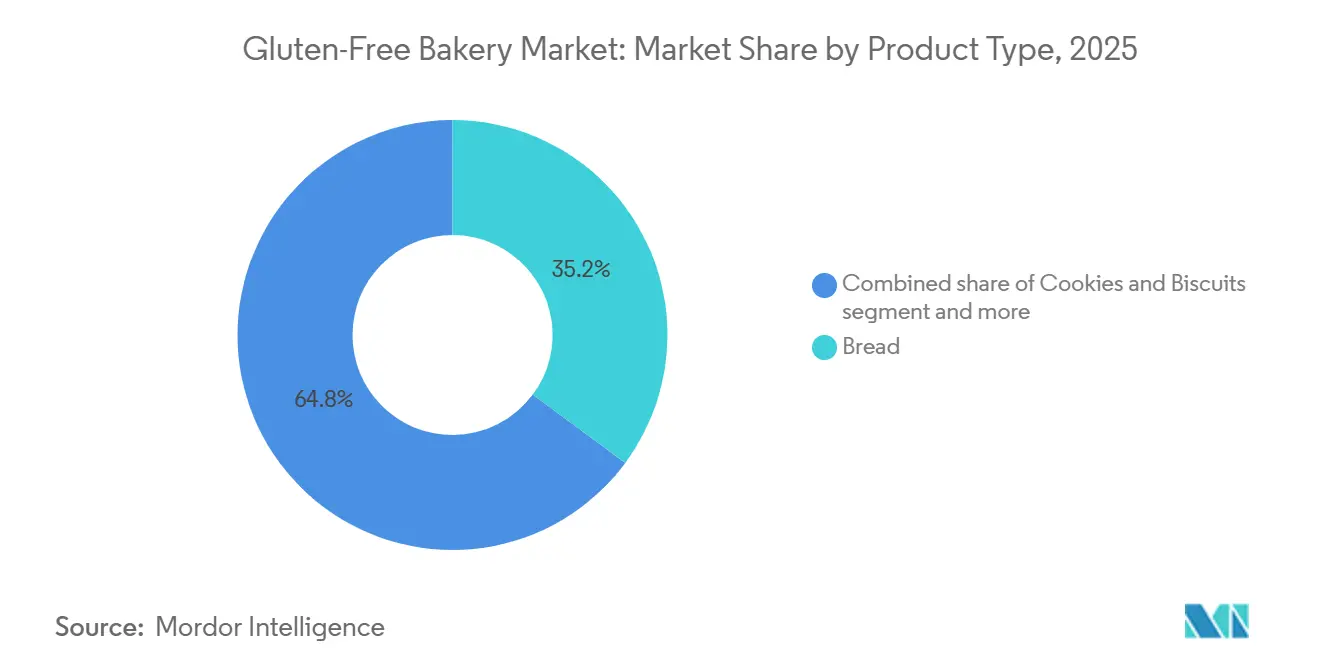

- By product type, bread led with 35.16% of the Gluten-Free Bakery Products market share in 2025, while cookies and biscuits are projected to post the fastest 10.09% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets accounted for 44.63% of 2025 revenue, whereas online retail is set to expand at a 11.89% CAGR through 2031.

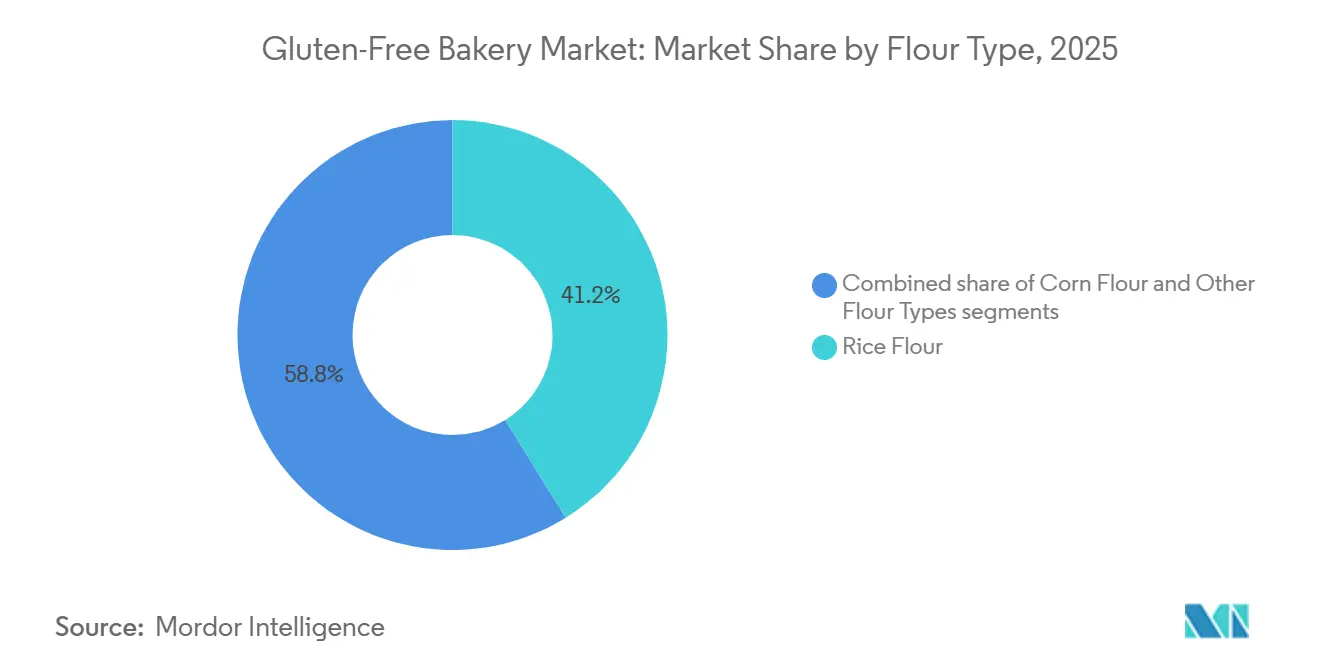

- By flour type, rice flour accounted for 41.16% of 2025 sales, and other flour type is forecast to grow at a 10.02% CAGR over 2026-2031.

- By geography, North America commanded 38.46% of the gluten-free bakery market share in 2025, whereas Asia-Pacific is expected to advance at a 10.53% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gluten-Free Bakery Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing celiac disease diagnoses | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Product innovation in textures | +1.5% | Global, led by North America and Europe R&D hubs | Short term (≤ 2 years) |

| Clean-label and natural ingredients | +1.2% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Expansion of e-commerce channels | +2.0% | Global, accelerating in Asia Pacific and North America | Short term (≤ 2 years) |

| Allergen-friendly labeling standards | +0.8% | North America and Europe, with spillover to Asia Pacific | Long term (≥ 4 years) |

| Rise of functional bakery items | +1.3% | Global, early adoption in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Celiac Disease Diagnoses

Improved diagnostic methods and greater clinical awareness are increasing the number of celiac disease diagnoses, turning previously unmet dietary needs into growing market demand. According to the Celiac Disease Foundation, about 1 in 100 people worldwide have celiac disease, but most remain undiagnosed[1]Source: Celiac Disease Foundation, "Create A World Free of Celiac Disease", celiac.org. This presents a significant opportunity as screening programs become more common in primary-care settings. The market is also expanding due to rising cases of non-celiac gluten sensitivity and wheat allergies. Many younger individuals are identifying as gluten-intolerant, often because of perceived digestive benefits. Retailers are addressing these trends by offering more gluten-free products, moving them from niche health-food aisles to mainstream bakery sections. This change is making gluten-free diets more widely accepted and reducing the stigma around specialty diets. Regulations like the FDA's gluten-free labeling rule, which requires products to contain less than 20 parts per million of gluten, provide a clear framework for manufacturers. This allows them to scale production while avoiding legal risks. Certification programs such as NSF Protocol P404 also offer third-party validation, appealing to consumers who value safety and reliability.

Product Innovation in Textures

Gluten-free bakery products have traditionally struggled to match the texture of wheat-based goods. Early versions were often crumbly, dry, and quick to go stale. Recent advancements in hydrocolloid systems, such as xanthan gum, guar gum, and hydroxypropyl methylcellulose, along with enzyme technologies that mimic gluten's properties, are closing this gap. These improvements help manufacturers create products with better crumb structure and mouthfeel, appealing to a wider audience rather than just serving as substitutes. In 2024, the Canadian Food Inspection Agency updated its gluten-free guidelines to focus on preventing cross-contact[2]Source: Canadian Food Inspection Agency, "Gluten-Free Claims: Guidance for Food Manufacturers." canada.ca. This change has encouraged investments in dedicated production lines, allowing manufacturers to test new binders and aerating agents without contamination risks. Flowers Foods resolved production capacity issues in fiscal 2024, enabling Canyon Bakehouse, the leading gluten-free bread brand in the U.S. with USD 170 million in retail sales, to increase production of its improved products. These reformulated items, made with enzyme-modified starches, offer longer shelf life and better slice integrity. These innovations reduce the drawbacks of gluten-free products, attracting not only those with celiac disease but also flexitarians and health-conscious consumers looking for perceived health benefits.

Clean-Label and Natural Ingredients

Consumers are paying closer attention to ingredient lists, avoiding synthetic additives, artificial colors, and preservatives. Instead, they prefer simple, minimally processed ingredients. In March 2025, Hain Celestial announced that its U.S. portfolio is completely free from FD&C artificial colors, using only natural-source colorants. This highlights the growing clean-label trend influencing the gluten-free bakery market. This trend also aligns with the broader "free-from" approach, including gluten-free, dairy-free, and non-GMO products, which attract consumers who associate simpler ingredients with better health, even without scientific proof. However, manufacturers face challenges in maintaining clean-label standards while ensuring shelf-life and product quality. Natural preservatives like rosemary extract and cultured dextrose provide shorter protection compared to synthetic options. As a result, companies must improve packaging, strengthen cold-chain logistics, and manage inventory efficiently to prevent spoilage. Although the FDA does not require clean-label claims, its focus on "natural" terminology forces brands to prove their sourcing and processing methods. This increases compliance costs but also creates barriers for new entrants, favoring established companies with strong quality-control systems.

Expansion of E-Commerce Channels

Digital commerce is removing geographic and assortment barriers that once limited gluten-free bakery products. Specialty brands can now reach wider audiences without investing in physical stores. Online retail channels are projected to grow at a 9.01% CAGR through 2031, surpassing traditional formats. Subscription models, curated platforms, and direct-to-consumer websites are driving this growth by bypassing retailers and increasing margins. The COVID-19 pandemic accelerated e-commerce in grocery, while investments in last-mile delivery and temperature-controlled centers have made home delivery of fresh and frozen gluten-free products viable. In January 2025, Flowers Foods acquired Simple Mills for USD 795 million, funded by a USD 500 million credit facility and senior notes. This deal allows Flowers Foods to use Simple Mills' strong e-commerce presence to sell Canyon Bakehouse products through owned and third-party online platforms. Combining manufacturing scale with digital distribution highlights the importance of omnichannel integration. Companies that excel in personalized marketing, subscription retention, and data-driven product strategies will gain a competitive edge.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium price versus conventional bakery items | -0.9% | Global, most acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Cross-contamination risks in shared facilities of emerging markets | -0.5% | Asia Pacific, South America, Middle East & Africa | Medium term (2-4 years) |

| Shorter shelf-life of clean-label gluten-free bread | -0.4% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Climatic volatility affecting specialty flour supply | -0.6% | Global, with acute impact in rice/corn-producing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium price versus conventional bakery items

Gluten-free bakery products are priced 50% to 200% higher than wheat-based options due to costly specialty flours, dedicated production to avoid cross-contact, and smaller production runs that lack economies of scale. This price gap limits adoption among budget-conscious households and restricts growth in emerging markets with lower disposable incomes. In fiscal Q1 2026, Hain Celestial reported a 17% drop in organic snack sales in North America, driven by slower sales and distribution losses. This shows that premium pricing without strong sensory appeal reduces repeat purchases. In February 2026, the company sold its North American snacks business for USD 115 million, retreating from categories where price outweighs brand loyalty. Private-label grocers are leveraging this price sensitivity by offering cheaper gluten-free options. While these may lack texture or ingredient quality, they appeal to budget-focused consumers and reduce branded market share. Manufacturers must cut costs—by optimizing flour blends, automating production, and renegotiating supplier contracts—while maintaining clean-label standards and product quality. This challenge will grow as input costs rise and retailers push for more promotions.

Cross-contamination risks in shared facilities of emerging markets

Producing gluten-free bakery products in facilities that also handle wheat-based goods poses cross-contact risks, which can harm celiac patients and damage brand trust. However, the high cost of dedicated production lines discourages investment in regions with low demand and fragmented distribution networks. Emerging markets in Asia Pacific, South America, and the Middle East often lack strong regulations and certification systems like those in North America and Europe, leading to inconsistent quality and consumer doubts. While the FDA and CFIA emphasize cleaning protocols, environmental testing, and allergen control, these standards mainly apply to products for developed markets. Testing methods like ELISA and standards from AOAC International and NSF ensure gluten levels stay below 20 parts per million, but their high costs and technical requirements are barriers for small producers in low-income regions. This creates a market divide: global brands with strong quality systems can charge premium prices and secure better shelf space, while local manufacturers compete on price but risk reputational damage from contamination, slowing growth in high-potential areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bread Anchors Market, Indulgent Formats Accelerate

In 2025, bread contributed 35.16% of gluten-free bakery revenues, highlighting its importance as a dietary staple and a go-to option for newly diagnosed celiacs seeking wheat alternatives. Flowers Foods' Canyon Bakehouse, which achieved USD 170 million in retail sales in fiscal 2024, resolved capacity issues to meet growing demand. Texture innovations, like enzyme-modified starches and hydrocolloid blends, helped the brand deliver bread with slice integrity and mouthfeel similar to traditional loaves. While the segment benefits from frequent purchases and high household penetration, growth is slowing due to a saturated base of diagnosed celiacs. Future growth depends on attracting flexitarian consumers who value sensory quality over medical necessity. Clean-label formulations, which avoid synthetic preservatives, create challenges like shorter shelf life and higher waste. These issues favor vertically integrated companies with strong supply chains and retailers willing to accept faster turnover for premium products.

Cookies and Biscuits are projected to grow at a CAGR of 10.09% through 2031, outpacing the market average. Consumers are shifting to portion-controlled treats enriched with functional ingredients like plant-based proteins, prebiotic fibers, and omega-3 fatty acids. This segment benefits from discretionary spending and impulse purchases in coffee shops, convenience stores, and online subscription boxes, where premium pricing faces less resistance than in staple bread. General Mills' fiscal 2026 plans to increase innovation investments reflect the industry's focus on moving beyond basic gluten-free bread to higher-margin products that justify R&D and compete with private labels. The popularity of macro-tracking diets and satiety-focused nutrition is driving demand for protein-rich muffins and fiber-packed brownies. These products combine wellness benefits with indulgent taste, appealing to a broader audience, including athletes, older consumers, and those managing weight.

By Distribution Channel: Mass Retail Dominates, Digital Disrupts

In 2025, supermarkets and hypermarkets accounted for 44.63% of gluten-free bakery sales. These retailers use their scale, promotions, and allergen-friendly shelves to attract consumers seeking convenience and one-stop shopping. Their cold-chain systems and frequent restocking allow them to pair gluten-free bakery items with products like dairy-free spreads, organic produce, and functional beverages, boosting spending per visit. However, Hain Celestial's fiscal 2025 first-quarter results showed a decline in meal-preparation and snack sales as customers opted for private-label alternatives. This shift highlights that mass-market distribution does not guarantee brand loyalty when price sensitivity rises. Retailers are increasingly focusing on private-label products, which offer better margins and store differentiation. This trend challenges branded manufacturers, especially in segments where products lack uniqueness and premium pricing is hard to justify.

Online retail channels are expected to grow at a 11.89% CAGR through 2031, driven by subscriptions, curated platforms, and direct-to-consumer websites that appeal to digital-first consumers. In January 2025, Flowers Foods acquired Simple Mills for USD 795 million, funded by a USD 500 million credit facility and senior notes. This deal strengthens their e-commerce presence and enables cross-selling of Canyon Bakehouse products through online platforms. E-commerce supports personalized marketing, subscription retention, and data-driven product selection, creating strong customer loyalty. However, its growth depends on investments in delivery networks, temperature-controlled facilities, and packaging to maintain freshness, favoring larger players over smaller regional brands.

By Flour Type: Rice Flour Leads, Corn Flour Innovates

In 2025, rice flour contributed 41.16% to gluten-free bakery revenues. Its neutral flavor, fine texture, and strong supply networks across Asia, North America, and Europe supported its dominance. Global rice production reached 561.6 million metric tons in the 2025/26 crop year, with rising stocks and stable-to-lower prices benefiting manufacturers using rice-based formulations[3]Source: Food and Agriculture Organization of the United Nations, "World Food Situation: Cereal Supply and Demand Brief." fao.org. U.S. rice ending stocks hit 44.5–52.9 million hundredweight, the highest in a decade, while farm prices ranged from USD 11.60 to USD 15.60 per hundredweight, reflecting ample supply and low inflation. Rice flour remains popular for bread, cookies, and cakes due to its compatibility with hydrocolloids that mimic gluten properties. However, the segment's maturity limits innovation, prompting manufacturers to mix rice flour with protein-rich legume flours like chickpea and lentil to improve nutrition and attract health-conscious consumers.

Other flour types is projected to grow at a 10.02% CAGR through 2031, driven by demand for non-GMO and organic options. These certifications appeal to clean-label advocates and offer a cost-effective alternative amid wheat-price volatility. In 2024-25, U.S. corn ending stocks were 1.8–2.1 billion bushels, with farm prices between USD 4.00 and USD 4.40 per bushel, making corn-based formulations more affordable than specialty flours like almond or coconut. Corn flour's sweet flavor and yellow color help brands market it as artisanal or heritage-inspired, standing out from rice-flour products. However, El Niño-driven droughts in Brazil and Argentina in 2024 disrupted maize production, and ongoing weather risks threaten supply stability. Manufacturers without diversified sourcing or forward contracts may face margin pressures. The segment's growth depends on innovations in enzyme and fermentation technologies to improve baking performance and reduce reliance on synthetic additives, aligning with clean-label trends.

Geography Analysis

In 2025, North America accounted for 38.46% of gluten-free bakery revenues, driven by strong celiac-awareness campaigns, strict FDA regulations like the gluten-free labeling rule, and allergen-friendly retail setups in grocery stores. The FDA's January 2026 proposal to update gluten-free labeling may tighten cross-contact limits and standardize advisory statements. While this could increase compliance costs, it would also boost consumer trust. Flowers Foods resolved production issues in 2024 and acquired Simple Mills for USD 795 million in January 2025, strengthening its position as the top U.S. gluten-free bakery manufacturer. Canyon Bakehouse generated USD 170 million in retail sales, while Simple Mills added USD 240 million. However, the region's mature market limits growth, with future gains relying on attracting flexitarian consumers through texture and nutritional innovations rather than expanding the stable 1% diagnosed celiac population.

Asia Pacific is expected to grow the fastest, with an 10.53% CAGR through 2031, driven by urbanization, rising incomes, and the spread of Western-style bakeries in India, China, and Southeast Asia. Celiac disease has been underdiagnosed in the region due to low awareness and traditional wheat-light diets. However, increasing wheat consumption from globalized food habits is raising gluten sensitivity diagnoses. Challenges include fragmented distribution, weak cold-chain infrastructure in smaller cities, and cross-contamination risks in shared facilities lacking strong regulations. Manufacturers must balance affordability with the high costs of dedicated gluten-free production and testing. Joint ventures with local food companies are often preferred over starting new facilities.

Europe, South America, and the Middle East & Africa make up the rest of the market. Europe benefits from unified EU allergen-labeling rules and strong advocacy groups like Coeliac UK. South America and MEA face slower growth due to low diagnosis rates, limited specialty stores, and affordability issues. In February 2026, Hain Celestial sold its North America snacks business for USD 115 million to focus on higher-margin categories like tea, yogurt, and meal preparation. This reflects a trend of companies exiting crowded gluten-free markets to focus on more profitable areas. Growth in these regions depends on local product innovation, such as using cassava in Africa and quinoa in South America, and partnerships with retailers willing to invest in allergen-friendly products despite slower initial sales.

Competitive Landscape

Established manufacturers and new entrants vie for dominance in the gluten-free bakery market, which is witnessing moderate consolidation. Key players like Dr. Schar AG/SpA and Grupo Bimbo SAB de CV are broadening their reach through e-commerce and specialty stores. Meanwhile, local bakeries cater to regional tastes with fresh, premium offerings. As awareness of gluten intolerance grows and health-centric products gain traction, the market continues its upward trajectory.

In response to the health-conscious trend, companies are unveiling premium lines of gluten-free bakery items, emphasizing clean-label, organic, and functional attributes. Through retail partnerships, independent certifications, and a commitment to ongoing product innovation, these firms are solidifying their market foothold. Such strategies not only cater to the rising demand for healthier options but also set them apart in a crowded marketplace.

Data analytics has become essential for optimizing distribution and inventory management. It empowers companies to forecast demand, minimize waste, and guarantee product availability, all of which boost operational efficiency. As major food corporations broaden their gluten-free portfolios, the market leans towards consolidation. However, specialized producers with direct-to-consumer models maintain their autonomy, bolstered by premium positioning and strong customer loyalty. These niche players harness their expertise and personalized engagement to carve out a competitive advantage.

Gluten-Free Bakery Industry Leaders

-

Dr. Schär AG/SPA

-

Grupo Bimbo, S.A.B. de C.V.

-

Flowers Foods, Inc.

-

Warburtons Holdings Limited

-

Conagra Brands, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Warburtons acquired the Roberts Bakery Ilkeston factory. This site produces specialty breads such as pittas and thins, significantly boosting Warburtons' manufacturing capacity for value-added segments.

- June 2025: Tooru launched a new product line from its gluten-free food specialist subsidiary Juvela. The brand has introduced a new brand and range, "OAF", supported by a new allergen-free bakery, to expand its presence in the growing 'free-from' market segment.

- May 2025: Tim Tam, the Australian chocolate biscuit brand, introduced its gluten-free products in the United States through Albertsons stores nationwide. The expansion addressed the increasing consumer demand for gluten-free alternatives while maintaining the brand's signature indulgent taste.

- March 2025: Doughlicious launched a range of vegan and gluten-free gourmet cookies in Double Chocolate Chip, Salted Caramel, Chocolate Chip, and Banana Good Granola variants. The company established distribution channels through Hunt's Food Group and Amazon to serve independent convenience retailers.

Global Gluten-Free Bakery Market Report Scope

Gluten-free bakery refers to bakery products that do not contain gluten - a protein found in many cereal grains such as wheat, barley, etc.

The global gluten-free bakery market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into bread, cookies and biscuits, cakes and muffins, and other gluten-free products. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialist stores, online channels, and others. By geography, the global gluten-free bakery market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

For each segment, the market sizing and forecasting have been done in value terms (USD million).

| Bread |

| Cookies and Biscuits |

| Cakes, and Muffins (includes cupcakes) |

| Other Gluten-Free Bakery Products |

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Specialist Stores |

| Online Retail Stores |

| Other Distribution Channels |

| Corn Flour |

| Rice Flour |

| Other Flour Types |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Bread | |

| Cookies and Biscuits | ||

| Cakes, and Muffins (includes cupcakes) | ||

| Other Gluten-Free Bakery Products | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Specialist Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Flour type | Corn Flour | |

| Rice Flour | ||

| Other Flour Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the Gluten-Free Bakery Products market?

The Gluten-Free Bakery Products market stands at USD 8.48 billion in 2026.

How fast will the Gluten-Free Bakery Products market grow through 2031?

The category is projected to register an 8.89% CAGR from 2026 to 2031, reaching USD 12.99 billion by the end of the period.

Which product type generates the highest revenue?

Bread remains the leading product, contributing 35.16% of 2025 sales due to its staple positioning among medically diagnosed consumers.

Which region will expand the quickest?

Asia Pacific is forecast to post the fastest regional CAGR of 10.53% through 2031 as urban incomes rise and Western-style bakery formats proliferate.

Page last updated on: