Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

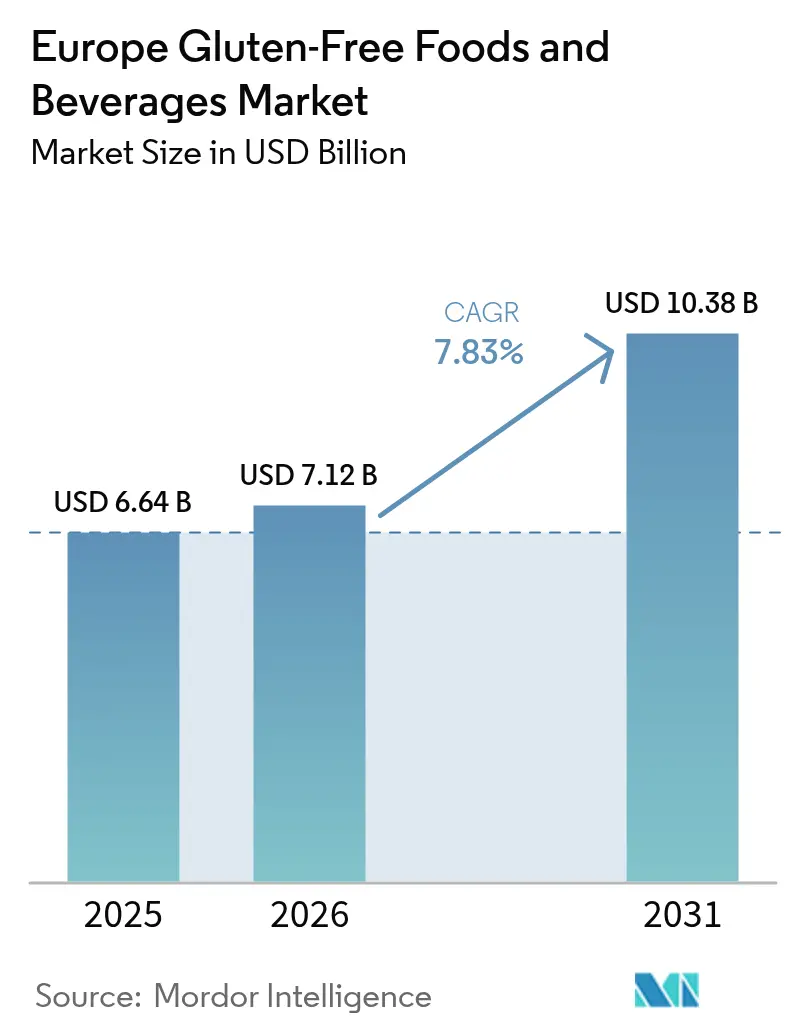

| Base Year Market Size (2025) | USD 6.64 Billion |

| Market Size (2026) | USD 7.12 Billion |

| Market Size (2031) | USD 10.38 Billion |

| Growth Rate (2026 - 2031) | 7.83% CAGR |

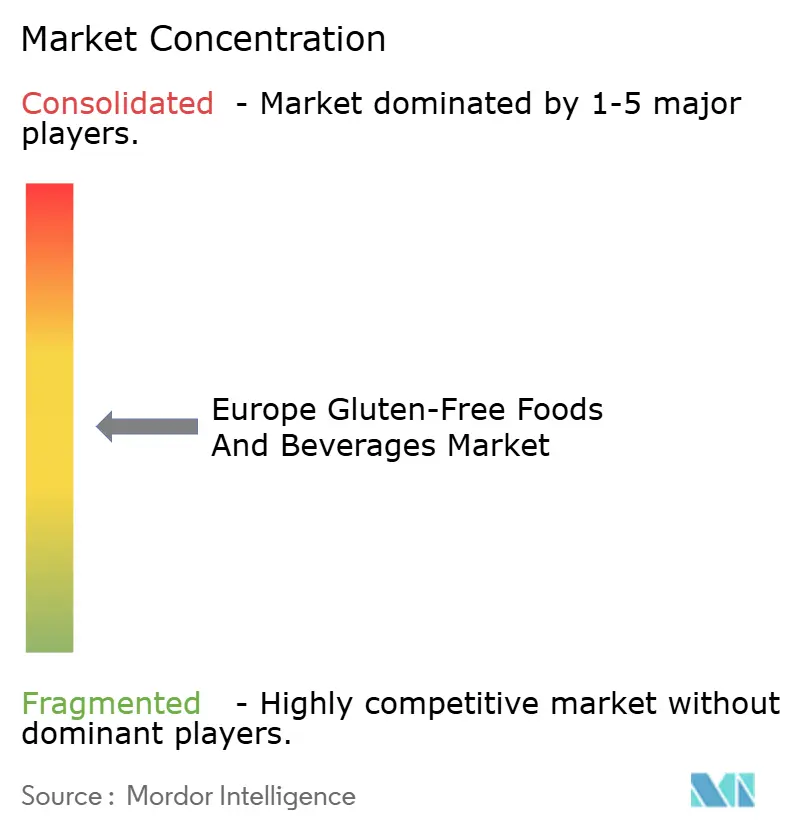

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Gluten-Free Foods And Beverages Market Analysis by Mordor Intelligence

The Europe gluten-free foods and beverages market size is expected to grow from USD 6.64 billion in 2025 to USD 7.12 billion in 2026 and is forecast to reach USD 10.38 billion by 2031 at 7.83% CAGR over 2026-2031. The increasing diagnosis of celiac disease, growing adoption of wellness-focused lifestyles, and the rapid expansion of e-commerce are driving demand, despite intensified price competition from private-label products. Germany remains the leading market in terms of value; however, countries like the Netherlands and Denmark, along with other digitally advanced and health-conscious markets, are achieving higher growth rates through online subscription models that circumvent traditional shelf-space limitations. Innovation within the category includes enzyme-treated beer, chickpea-based snacks, and yeast-derived binding agents, which address long-standing challenges related to taste and texture. European Union Regulation 828/2014, along with voluntary certification programs, is enhancing consumer trust. High capital requirements for dedicated production and traceability systems continue to benefit established players such as Dr. Schär AG, while smaller niche companies are capitalizing on opportunities in organic, clean-label, and direct-to-consumer offerings.

Key Report Takeaways

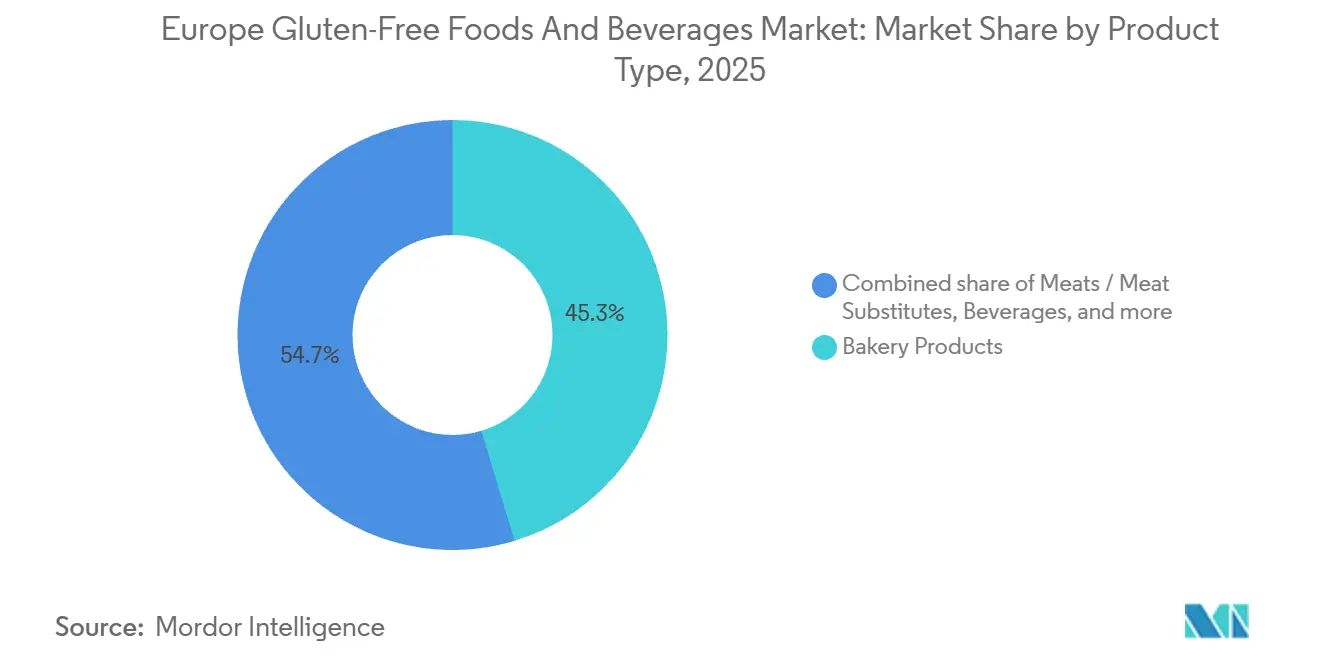

- By product type, bakery products led with 45.34% of the Europe gluten-free food and beverage market share in 2025; beverages are projected to record the fastest 8.12% CAGR through 2031.

- By nature, conventional offerings accounted for 86.48% share of the Europe gluten-free food and beverage market size in 2025, while organic lines are forecast to expand at a 10.13% CAGR up to 2031.

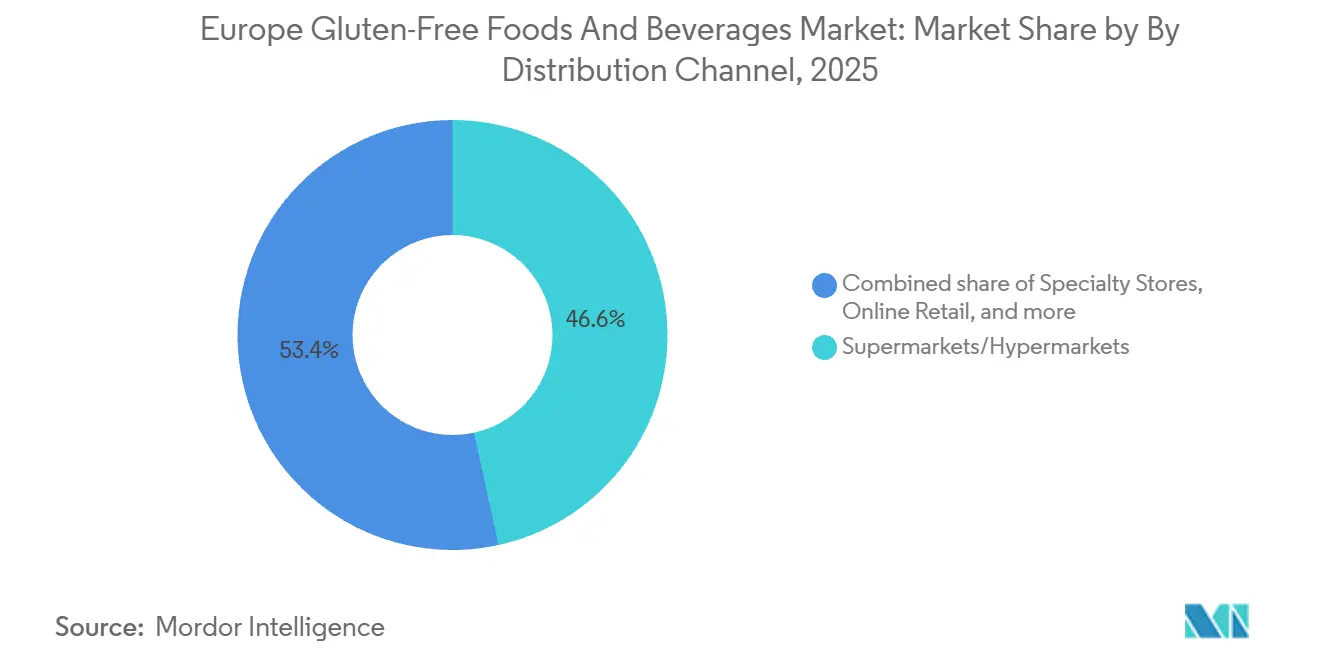

- By distribution channel, supermarkets and hypermarkets held 46.56% of 2025 value, whereas online retail is set to grow at a 10.17% CAGR through 2031.

- By geography, Germany captured 19.79% revenue share in 2025, while the Netherlands is slated for a 9.55% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Gluten-Free Foods And Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising celiac disease diagnosis rates increase baseline demand | +1.2% | Germany, Italy, United Kingdom, with emerging gains in Spain and Portugal | Medium term (2-4 years) |

| Growing awareness of non-celiac gluten sensitivity expands consumer base | +1.5% | Netherlands, Belgium, Switzerland, Scandinavia | Short term (≤ 2 years) |

| Lifestyle adoption by non-celiac consumers boosts premium positioning | +1.8% | Western Europe core (Germany, France, United Kingdom), spillover to Austria and Switzerland | Long term (≥ 4 years) |

| Clean-label preferences drive demand for natural ingredients | +1.3% | European Union-wide, strongest in Netherlands, Denmark, Sweden | Medium term (2-4 years) |

| Innovation in alternative flours and binding agents enhances product appeal | +1.1% | Germany, Italy, Spain (production hubs), distributed consumption across region | Medium term (2-4 years) |

| Regulatory support for standardized labeling builds consumer trust | +0.9% | European Union member states, United Kingdom post-Brexit alignment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising celiac disease diagnosis rates increase baseline demand

In 2024, the prevalence of biopsy-confirmed celiac disease in Europe was 0.8%, while serological screening identified diagnostic markers in 1.3% of the population. The incidence of celiac disease is increasing at an annual rate of 7.5%, driven by the adoption of proactive testing protocols by gastroenterologists for patients with non-specific gastrointestinal symptoms. In Germany, an estimated 800,000 to 900,000 individuals are affected by celiac disease. However, in 2023, only a small percentage of the national population purchased gluten-free foods, indicating that diagnosed patients constitute a minority of category buyers, with lifestyle-driven demand dominating market volume. Italian cohort studies conducted in 2022, involving thousands of celiac patients, reported high rates of dietary adherence. However, a notable portion of these patients occasionally consumed gluten-containing products due to factors such as price, taste, or availability. This indicates that medical necessity alone does not guarantee consistent purchasing behavior. In Germany, the Celiac Society's certification program, which ensures product compliance with the threshold of 20 parts per million gluten, has significantly expanded its approved product list since 2024. This growth reflects manufacturers' recognition of third-party validation as a means to build consumer trust in a market where it remains fragile. While rising diagnosis rates provide a stable foundation for demand, the primary growth driver for the gluten-free segment is the significantly larger group of non-celiac consumers. This group, which far exceeds the diagnosed population, views gluten avoidance as a wellness choice rather than a medical necessity.

Growing awareness of non-celiac gluten sensitivity expands consumer base

In 2024, the prevalence of non-celiac gluten sensitivity in Europe reached 12%, with 40% of affected individuals adhering to gluten-free diets despite not having biopsy-confirmed celiac disease. This consumer segment focuses on symptom relief rather than strict dietary compliance and tolerates occasional cross-contamination. Finnish longitudinal data revealed an increase in non-celiac gluten sensitivity diagnoses from 0.2% in 2000 to 0.7% in 2011, with the trend accelerating after 2020 due to the adoption of telemedicine consultations and direct-to-consumer antibody testing, which reduced diagnostic barriers. Research conducted in Portugal in 2024 identified gluten intolerance in a significant portion of the population, with a majority of respondents regularly consuming functional foods. This indicates that gluten-free product positioning aligns with broader clean-eating and gut-health trends, appealing to consumers beyond those with formal diagnoses. The non-celiac segment demonstrates higher price sensitivity and brand-switching behavior compared to medical users, presenting opportunities for private-label programs and direct-to-consumer subscription models that emphasize convenience over clinical endorsement.

Lifestyle adoption by non-celiac consumers boosts premium positioning

The organic market in the United Kingdom has experienced notable growth, with gluten-free organic products commanding a higher price premium compared to conventional gluten-free alternatives. This growth highlights the increasing consumer interest in organic and allergen-free options; however, market penetration remains constrained due to limited retail distribution channels and persistent consumer skepticism regarding the tangible benefits of dual certification [1]Source: Soil Association, “Organic Market Report,” soilassociation.org. According to the Nutrition Report from Germany, a significant proportion of respondents identified as flexitarian, reflecting an increase compared to previous years, while a smaller percentage reported daily consumption of vegan or vegetarian meals. These demographic shifts indicate a growing preference for flexible dietary choices, creating opportunities for gluten-free brands to strategically position their products within plant-based and allergen-free shelf categories. Nevertheless, lifestyle adopters, who often experiment with gluten-free products as part of broader dietary trends, exhibit higher churn rates than medical users when product performance does not meet expectations. To address this challenge and ensure long-term category growth, achieving sensory parity with gluten-containing counterparts is critical and should remain a top priority for manufacturers.

Clean-label preferences drive demand for natural ingredients

The European Food Safety Authority's survey highlighted that a significant majority of consumers prioritize food safety information, with many identifying safety as a key factor influencing their purchasing decisions [2]Source: European Food Safety Authority, “Food safety in the EU,” efsa.europa.eu. Clean-label gluten-free brands have responded to this preference by removing synthetic emulsifiers, preservatives, and stabilizers, which are often accepted by medical users but avoided by lifestyle buyers. In the same year, Genius Foods invested a substantial amount to reformulate its bread line, eliminating xanthan gum, which is a hydrocolloid used to enhance texture but is viewed negatively by clean-label advocates. This decision highlights how ingredient transparency has become just as important as the absence of gluten in setting products apart within the category. According to the Soil Association, a large proportion of consumers in the United Kingdom seek independent verification for organic and clean-label claims. However, only a small percentage of gluten-free products currently hold dual certifications, presenting an opportunity for brands capable of managing the costs and complexities associated with meeting parallel compliance standards. Clean-label positioning increases production costs significantly due to factors such as shorter shelf life, specialized ingredient sourcing, and smaller batch sizes. These higher costs compress margins for mid-tier players but allow premium brands to justify higher price points, which are typically less acceptable to buyers with medical dietary needs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict regulatory compliance increases certification burdens | -0.8% | European Union member states, United Kingdom | Medium term (2-4 years) |

| Cross-contamination risks erode consumer confidence | -1.0% | Germany, Italy, France, Spain (high manufacturing density) | Short term (≤ 2 years) |

| Manufacturing complexity demands dedicated facilities | -0.9% | European Union-wide, acute in smaller markets with limited production infrastructure | Long term (≥ 4 years) |

| Nutritional imbalances like micronutrient gaps raise health concerns | -0.7% | Northern Europe (Netherlands, Denmark, Sweden) with high health literacy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict regulatory compliance increases certification burdens

European Union Regulation 828/2014 requires gluten-free claims to be verified through enzyme-linked immunosorbent assay (ELISA) testing [3]Source: European Union, “Implementing regulation - 828/2014 - EN - EUR-Lex,” eur-lex.europa.eu. However, the lack of harmonized sampling protocols across member states compels manufacturers to perform redundant batch testing for cross-border distribution, significantly increasing compliance costs. The Gluten-Free Certification Organization imposes annual fees that vary based on facility size and product count, in addition to per-product testing costs. These expenditures reduce profit margins for mid-tier brands and discourage small artisan producers from seeking third-party certification. Post-Brexit regulatory divergence between the European Union and the United Kingdom has resulted in dual-compliance requirements for exporters. Among surveyed manufacturers, a notable percentage reported that differences in labeling and testing standards delay product launches by several months and add substantial administrative costs annually. In 2024, Germany's Federal Office of Consumer Protection and Food Safety issued multiple gluten-contamination warnings, leading to product recalls that cost affected brands significantly in lost inventory, retailer penalties, and reputational damage. This risk profile discourages new market entrants and consolidates market share among established players with strong quality-management systems.

Cross-contamination risks erode consumer confidence

A survey conducted in 2024 across multiple European countries, involving thousands of gluten-free consumers, highlighted significant challenges. Nearly 80% of respondents reported difficulties in finding gluten-free products, while 66% expressed concerns about product quality. For individuals medically diagnosed with celiac disease, fears of cross-contamination were identified as the main reason for avoiding repeat purchases. In 2025, the European Food Safety Authority (EFSA) discovered residual immunogenic peptides in enzyme-treated barley beer samples. This finding led to the suspension of product listings by retailers and reformulation efforts by manufacturers. The incident amplified consumer skepticism toward innovative processing methods and increased the preference for naturally gluten-free options. Germany's Federal Office of Consumer Protection and Food Safety documented several gluten-contamination incidents in 2024. These included recalls of bread, pasta, and snack products that exceeded the permissible gluten threshold. These events generated significant social media impressions and caused a noticeable decline in category sales across affected retail chains for several weeks following the incidents. Research conducted in Italy in 2022 among celiac patients revealed that a significant proportion occasionally consumed gluten-containing foods due to limited availability or social pressures. However, the majority adhered to their dietary requirements overall. This paradox highlights how contamination concerns drive over-purchasing and pantry stockpiling behaviors, which temporarily boost sales volumes but mask underlying dissatisfaction. Trust in gluten-free labeling received an average score of just over three out of five in a European consumer survey conducted in 2021. This moderate rating reflects ongoing doubts about manufacturing standards and regulatory enforcement, particularly for private-label products that lack established brand heritage or third-party certification seals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bakery Anchors Volume While Beverages Lead Innovation

Bakery products are projected to account for 45.34% of the European gluten-free market value in 2025. This dominance is driven by the daily consumption of bread and biscuits by celiac patients. Beverages are expected to grow at a compound annual growth rate (CAGR) of 8.12% through 2031, marking the fastest growth among product types. This growth is attributed to innovations in gluten-free beer, such as rice-malt formulations and sorghum-quinoa craft brews, which achieve gluten levels below 5% parts per million while maintaining sensory profiles comparable to conventional lagers. In May 2025, White Rabbit introduced gluten-free biscotti and gnocchi through Sainsbury's and Ocado, targeting premium consumers willing to pay GBP 3.50 per 200-gram pack. This strategy highlights how artisan brands cater to the 35% of European shoppers dissatisfied with the healthy-product assortment at their primary grocery stores.

Meats and meat substitutes, dairy and dairy substitutes, and sauces, dressings, and seasonings collectively account for 28% of the category's value. In these segments, gluten-free claims often serve as secondary attributes, following plant-based, organic, or high-protein positioning. As a result, dedicated product development is limited, and gluten-free variants are typically introduced as line extensions rather than standalone products. Manufacturers are addressing micronutrient deficiencies, a key health concern in the gluten-free category, with innovations such as rice-chickpea extruded snacks fortified with passion fruit fiber. Prozymi Biolabs' enzyme technology, launched in February 2025, enables the degradation of gluten peptides in wheat flour to levels below 20% parts per million. However, regulatory concerns, including the European Food Safety Authority's 2025 warning about residual immunogenic peptides in enzyme-treated barley, have delayed commercial adoption. This has reinforced consumer preference for naturally gluten-free grains, particularly in the bakery products segment.

By Nature: Organic Niche Expands as Clean-Label Mandate Intensifies

Conventional gluten-free products accounted for 86.48% of the European market value in 2025, driven by consumers purchasing out of medical necessity, prioritizing the absence of gluten over the origin of ingredients. However, organic gluten-free products are projected to grow at a compound annual growth rate (CAGR) of 10.13% through 2031, surpassing the overall market growth by 230 basis points. This growth is fueled by lifestyle consumers seeking dual certifications that ensure both allergen safety and agricultural sustainability. In the United Kingdom, the organic market has expanded, with organic products being twice as likely to be purchased online compared to conventional alternatives. Gluten-free organic brands are leveraging this trend through subscription models and direct-to-consumer platforms, which help them overcome shelf-space limitations in physical retail stores.

Genius Foods' GBP 1 million investment in 2025 to remove xanthan gum from its bread formulations highlights the clean-label trend driving growth in the organic segment. This aligns with consumer behavior, as 77% of European consumers closely examine ingredient lists, and 61% are willing to switch brands for products with "natural" claims. These preferences benefit artisan producers over mass-market competitors. According to Soil Association data, 87% of United Kingdom consumers demand independent verification for organic claims. However, only 23% of gluten-free products currently hold dual certifications, presenting an opportunity for brands ready to invest in the EUR 5,000 to EUR 20,000 annual cost of maintaining parallel compliance standards.

By Distribution Channel: Online Retail Disrupts Traditional Shelf Allocation

In 2025, supermarkets and hypermarkets are expected to account for 46.56% of the European gluten-free market value, supported by dedicated free-from aisles from retailers such as Tesco, Carrefour, and Edeka. At the same time, online retail is anticipated to grow at a compound annual growth rate (CAGR) of 10.17% through 2031, representing the fastest growth among distribution channels. This growth is driven by subscription boxes and direct-to-consumer brands, which address shelf-space limitations and use first-party data to provide personalized product assortments. Specialty stores, including health-food retailers and pharmacies, continue to serve as discovery channels for newly diagnosed celiac patients seeking expert guidance and premium product options. However, their market share is declining as mainstream retailers expand their gluten-free offerings and online platforms improve access to niche products that were previously limited to specialty outlets.

Other distribution channels, such as foodservice, convenience stores, and direct sales, collectively account for 18% of the market value. Within this segment, ready-to-eat and food-to-go formats are experiencing growth, driven by urbanization and the rising demand for portable, allergen-safe meal solutions among dual-income households. The increasing preference for convenience and time-saving options continues to influence consumer behavior in this category.

Geography Analysis

Germany is set to lead the European gluten-free market, projected to account for 19.79% of its value by 2025. This leadership is supported by an estimated 800,000 to 900,000 celiac patients and a regulatory framework strengthened by the German Celiac Society's certification program, which expanded its approved product portfolio by 18% since 2024. Despite this, only 3% of the German population purchased gluten-free foods in 2023, indicating that lifestyle preferences, rather than medical necessity, are driving much of the market growth. In 2023, Dr. Schär invested 13.2 million euros in a German biscuit facility and expanded its Alagón, Spain plant in 2024 with a new production line for sweet and savory bakery products. These investments enable the company to effectively address the needs of both medical and lifestyle consumer segments. Additionally, awareness of the Nutri-Score nutritional labeling system in Germany rose significantly, from 44% in 2021 to 88% in 2024, reflecting growing consumer interest in healthier food choices.

The Netherlands is expected to be the fastest-growing segment in the European gluten-free market, with a compound annual growth rate (CAGR) of 9.55% through 2031. This growth is driven by a 12% prevalence of non-celiac gluten sensitivity and a strong digital-first retail infrastructure. Notably, 23% of organic purchases in the Netherlands occur online, compared to 13% for non-organic products, highlighting the country's advanced e-commerce ecosystem. This robust digital presence, combined with increasing health awareness, positions the Netherlands as a key growth market for gluten-free products in Europe. These factors make the Netherlands a standout performer in the region, with its focus on health-conscious consumers and digital retail channels.

Other key markets in the European gluten-free industry include the United Kingdom, France, Italy, Spain, and smaller countries such as Russia, Switzerland, Belgium, Austria, Portugal, and Denmark, which collectively contribute a significant portion of the regional market value. In the United Kingdom, Warburtons dominates the gluten-free bread market through its Newburn bakery, which operates at reduced throughput compared to conventional lines but benefits from premium pricing and prominent shelf placement in major retailers such as Tesco, Sainsbury's, and Morrisons. In Italy, a study involving thousands of celiac patients showed a high adherence to gluten-free diets, although some occasionally consumed gluten-containing foods due to challenges related to price, taste, or availability. In Spain, the food-tech sector introduced rice-chickpea extruded snacks fortified with passion fruit fiber, offering significantly higher protein content compared to standard gluten-free alternatives. Switzerland's high per-capita income supports gluten-free organic product penetration rates that are double the European average, although its small population limits overall market volume. In France, Groupe Barilla's Novara plant has shifted its focus toward free-from and rich-in product ranges, though the company's report indicates that gluten-free products remain a secondary priority for the conglomerate.

Regulatory Landscape

The European Union regulatory baseline for gluten-related claims is Commission Implementing Regulation (EU) No 828/2014, adopted under Regulation (EU) No 1169/2011 on food information to consumers. Under this framework, products using a "gluten-free" claim must contain no more than 20 mg/kg (ppm) gluten in the food as sold to the final consumer, while "very low gluten" claims apply up to 100 mg/kg for foods made from processed gluten-reduced cereals.

For oats used in foods labelled "gluten-free" or "very low gluten", the regulation requires production, preparation, and processing conditions that avoid contamination from wheat, rye, or barley, and the final gluten content must not exceed 20 mg/kg. In practice, these EU-wide thresholds and claim conditions set the minimum compliance bar for brands operating across member states, while additional voluntary statements, for example wording indicating products are specifically formulated for coeliacs, must still be consistent with the mandatory rules on substantiation and consumer information.

Competitive Landscape

The Europe gluten-free food and beverage market exhibits moderate concentration, with Dr. Schär leading at a pan-European level. The company reported an 11% increase in turnover compared to the previous year, driven by strategic acquisitions, including the purchase of Hero's Nordic Semper brand for SEK 1.5 billion. Despite this growth, regional specialists such as Warburtons in the United Kingdom, which dominates the bread segment, and Promise Gluten Free in Ireland, with revenues of EUR 68.1 million, maintain strong local positions. Their dedicated manufacturing capabilities and robust retailer partnerships create significant challenges for multinational entrants attempting to replicate their success.

Vertical integration remains a critical strategy for market leaders. Dr. Schär operates 18 sites across 11 countries, while Warburtons relies on its standalone Newburn bakery. This infrastructure facilitates end-to-end quality control and accelerates innovation cycles. However, the substantial upfront capital investments required, ranging from EUR 2 million to EUR 50 million, act as a barrier for mid-tier players, consolidating market capacity among larger incumbents. Opportunities are emerging in gluten-free organic product lines, which are projected to grow at a rapid compound annual growth rate. Technological advancements in enzyme platforms are addressing sensory gaps in gluten-free products. Examples include ACI Group's Synevo GR1 Gluten Replacer and Prozymi Biolabs' peptide-degradation systems. However, these innovations face regulatory challenges, such as the 2025 European Food Safety Authority warning regarding residual immunogenic peptides in enzyme-treated barley.

Emerging disruptors are introducing innovative solutions to the market. For instance, Netherlands-based Revyve launched a yeast-based egg replacer in September 2024, catering to clean-label formulations for vegan and allergen-sensitive consumers. Additionally, Spanish startups are developing coeliac-safe wheat flour through enzymatic treatment. If approved by regulatory bodies, these innovations could disrupt the naturally gluten-free grain supply chain. Retail media spending is projected to grow significantly, doubling from EUR 14 billion in 2024 to EUR 31 billion by 2028. This trend benefits brands with strong digital marketing capabilities and first-party data assets, favoring direct-to-consumer specialists and large multinationals over mid-tier players reliant on traditional trade spending. Mergers and acquisitions activity intensified in 2024, with notable transactions such as Morato Group acquiring majority stakes in Massimo Zero and Grupo Bimbo purchasing Amaritta. These deals underscore private equity interest in consolidating fragmented national markets and achieving synergies through shared manufacturing and procurement. However, the complexity of integration and potential cultural misalignment have historically posed challenges, tempering enthusiasm for roll-up strategies in the food industry.

Europe Gluten-Free Foods And Beverages Industry Leaders

General Mills Inc.

Dr. Schär AG/SPA

Genius Foods Ltd

Warburtons Ltd

Hain Celestial Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity additions and supply-chain moves by established manufacturers and ingredient suppliers are creating space for broader portfolios and more consistent availability across Europe, particularly in bakery and cereals where cross-contamination risk is a purchase barrier. Dr. Schar announced a EUR 28 million 2026 investment plan focused on expanding production facilities in Italy, Spain, and Germany, which reinforces the advantage of dedicated lines and traceability systems in a category where compliance with EU gluten-free thresholds (20 mg/kg under Regulation 828/2014) is non-negotiable.

Upstream ingredient security and cleaner functionality are also supporting new product-development lanes. In June 2026, Cereal Docks announced the acquisition of 75% of Pasini Riso e Derivati (rice and oat ingredients for gluten-free applications), strengthening access to core alternative grains used in European formulations. In June 2026, FERM FOOD ApS launched a fermented binder based on buckwheat and fava beans aimed at improving dough structure while reducing additive complexity in industrial gluten-free bread, aligning with the clean-label reformulation trend already visible in the region.

Recent Industry Developments

- May 2026: Freee Foods launched new gluten-free Swiss-style and Chocolate muesli SKUs, listed in selected Tesco stores and via Ocado. The rollout targets everyday breakfast occasions where private label is aggressive, and strengthens branded differentiation through mainstream retail plus online reach.

- September 2025: Genius Foods launched its Naturally Genius bread range after a GBP 1 million upgrade at its Bathgate, Scotland facility for new dough processing and metal detection technology. The move reinforces the shift toward clean-label positioning and tighter quality controls in a segment where repeat purchase is heavily influenced by perceived safety and texture parity.

- September 2024: Revyve launched a yeast-based egg replacer aimed at clean-label formulations for vegan and allergen-sensitive products. For gluten-free bakery and prepared foods, this ingredient innovation supports simpler labels and functional performance without relying on conventional additives, helping manufacturers address taste and texture constraints.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers packaged foods and beverages that are labeled and formulated as gluten-free, meaning they are made to avoid gluten-containing grains and related ingredients, and they are sold through retail channels across Europe.

Scope exclusions: Food service sales and non-labeled naturally gluten-free staples are excluded, and we do not count gluten-free ingredients sold for industrial use.

Segmentation Overview

- By Product Type

- Bakery Products

- Meats/Meat Substitutes

- Dairy/Dairy Substitutes

- Sauces, Dressings, and Seasonings

- Snacks and RTE Products

- Beverages

- Other Product Types

- By Nature

- Conventional

- Organic

- By Distribution Channel

- Supermarkets / Hypermarkets

- Specialty Stores

- Online Retail

- Other Distribution Channels

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Switzerland

- Belgium

- Austria

- Portugal

- Denmark

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by building a clean list of what is treated as gluten-free in packaged foods and beverages, and how this is labeled and policed across Europe. We used public references such as European Commission food labeling guidance, national food safety agencies, and selected customs and trade statistics to understand category definitions and cross-border movement.

Next, we pulled directional demand signals from sources such as Eurostat household expenditure series, trade association publications for packaged food categories, and peer-reviewed nutrition and celiac prevalence literature. Company annual reports, investor presentations, reputable retail and consumer press, and a paid subscription covering company financials and news were then used to cross-check category growth narratives, pricing direction, and channel mix shifts. The desk sources listed here are illustrative only, and many other public documents were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating the demand pool and price ladder for gluten-free items across major European markets, since labeling, consumer adoption, and retail positioning vary across countries. We spoke with packaged food producers, specialty gluten-free brands, retailers and distributors, and category experts, and then used their inputs to test assumptions on channel splits, typical price premiums, and which product groups drive most of the value.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | |

| Mid tier: 48% | Functional/Unit leaders: 43% | |

| Smaller Players: 15% | Managers: 45% |

Market-Sizing & Forecasting

Sizing was built using a mix of top-down and bottom-up checks. On the top-down side, we reconstructed a country-level demand pool for packaged gluten-free foods and beverages by combining category consumption signals and retail channel structure, and then applying gluten-free penetration and price premium assumptions that were validated through expert inputs.

To keep totals realistic, the model was corroborated with selective bottom-up approximations such as sampling brand and private-label price points, mapping typical pack sizes, and using supplier and retailer channel checks to confirm volumes and the share of gluten-free within relevant categories. Where direct signals were thin, especially in smaller countries, we used proxy variables like modern trade share, online grocery penetration, and specialty store density, then adjusted these after interviews.

Key inputs used as practical fingerprints included category-level gluten-free penetration by product type (bakery, dairy and dairy substitutes, sauces and seasonings, frozen desserts, beverages, and other foods), average price premium versus standard equivalents, distribution channel mix (supermarkets and hypermarkets, specialty stores, online retail, and other stores), and country demand differences linked to health-driven adoption. Forecasts were built using scenario analysis that ties growth to pricing direction, channel expansion, and expected penetration changes, and then reviewed with market participants to confirm the forward curve aligns with what they are seeing.

Data Validation & Update Cycle

Before sign-off, outputs were triangulated across multiple angles, including country totals versus expected retail scale and category mix logic. Variance checks were run to catch jumps in penetration, pricing, or channel shares that did not match interview feedback, and those cases triggered a re-check of assumptions and, when needed, a follow-up outreach.

A multi-step internal review was used so that calculation sheets, definitions, and year-to-year transitions remain consistent, and so the forecast path stays explainable. Reports are refreshed annually, and interim updates are made when major events materially change consumer demand, labeling enforcement, or pricing dynamics. Before delivery, a final pass is completed to ensure the numbers reflect the latest public signals and validated assumptions.

Mordor Intelligence's Europe Gluten Free Foods Beverages Market Market Estimate Compared With Other Published Estimates

Published market sizes for gluten-free foods and beverages in Europe often do not match, even when the topic sounds similar at first glance. The differences usually come from how each publisher treats the product scope, which year is used as the base, and how pricing and penetration are carried forward into forecasts.

Some sources lean toward a narrower packaged-products reading or use older starting points that miss the recent rise in modern retail and online mixes, and that can pull the current value down. Others push higher growth by applying strong penetration gains across all categories without checking whether key groups like bakery and dairy substitutes are already maturing in certain countries, and currency timing can add another layer of spread. These gap drivers are visible in how the included categories are defined, how price premiums are modeled, and how often the model is refreshed based on new retail and labeling signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.64 B (2025) | |

| Industry Publisher A | USD 3.62 B (2024) | Uses an earlier base year and can understate the recent value if retail price premiums and channel shifts are not fully carried into the current year, and the conversion timing across European currencies is not always transparent. |

| Industry Publisher B | USD 2.83 B (2025) | Frames the market as gluten-free products across selected food categories, which can miss beverage value and some labeled sub-categories that sit outside their product list, thereby reducing the total even in the same year. |

The spread in the table mainly comes from category coverage and base-year handling, followed by how price premiums are translated into value by channel. For Mordor Intelligence, foods and beverages are counted only when they are packaged, labeled gluten-free, and mapped to the listed retail channels, and adjacent naturally gluten-free staples and food service are kept out so the demand pool stays consistent and repeatable.

Key Questions Answered in the Report

How large will Europe’s gluten-free food and beverage sector be by 2031?

It is projected to reach USD 10.38 billion by 2031, up from USD 7.12 billion in 2026.

Which product category is growing the fastest?

Beverages, led by enzyme-treated beer and plant-based drinks, are forecast to grow at an 8.12% CAGR to 2031.

Why is online retail important for gluten-free brands?

E-commerce solves in-stock issues that 79% of shoppers report and is expected to grow at a 10.17% CAGR, outpacing store channels.

What drives premium pricing in gluten-free goods?

Lifestyle consumers pay for clean-label, organic, and sensory-improved formulations that command 2–3 times conventional prices.

Which country will lead growth rates through 2031?

The Netherlands, with 9.55% CAGR, will be the fastest-expanding market thanks to high digital retail usage and health awareness.

Page last updated on: