Mucosal Atomization Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.78 Billion |

| Market Size (2031) | USD 1.09 Billion |

| Growth Rate (2026 - 2031) | 6.91% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mucosal Atomization Devices Market Analysis by Mordor Intelligence

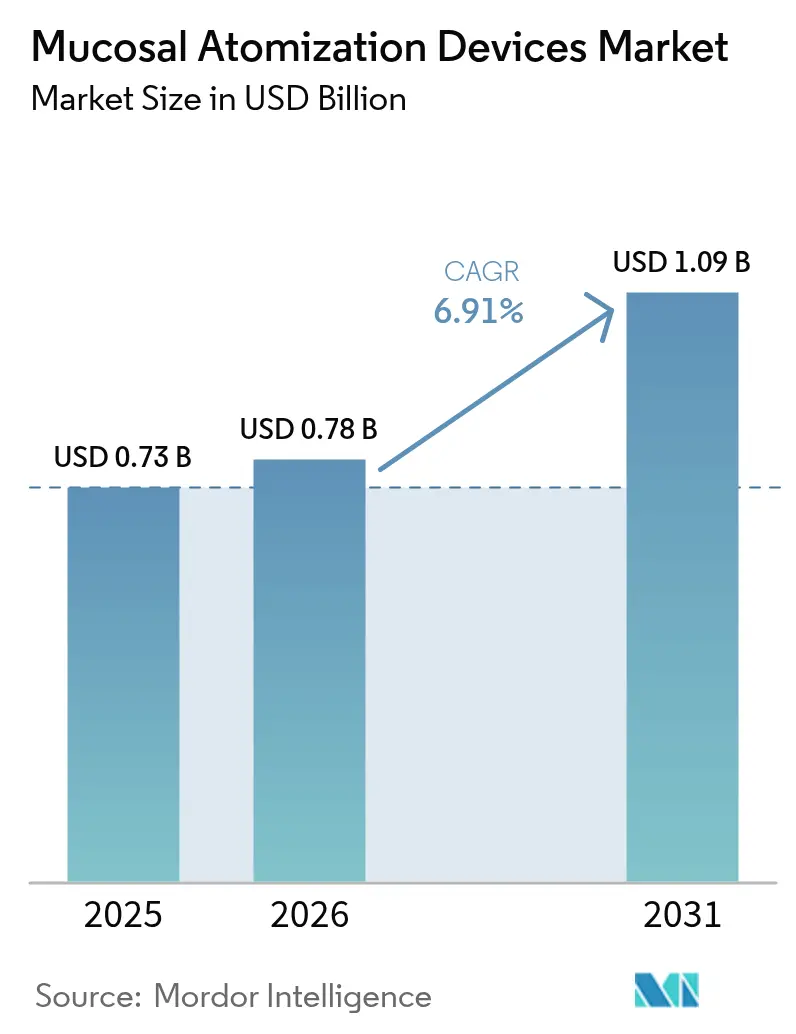

The mucosal atomization devices market size was valued at USD 0.73 billion in 2025 and estimated to grow from USD 0.78 billion in 2026 to reach USD 1.09 billion by 2031, at a CAGR of 6.91% during the forecast period (2026-2031). This trajectory underscores the sector’s shift toward needle-free delivery, growing hospital and clinic adoption rates, and favorable regulatory actions such as the FDA’s 2024 approval of neffy epinephrine nasal spray [1]ARS Pharmaceuticals Operations, Inc. ,"ARS Pharmaceuticals Announces Filings for Approval of neffy in China, Japan and Australia," ir.ars-pharma.com. Steady launches of propellant-free and smart, dose-counting platforms are widening the addressable base in emergency medicine, chronic allergy care, and preventive immunization, while sustainability mandates are steering product development away from hydrofluorocarbon propellants. M&A momentum, illustrated by Aptar Pharma’s purchase of SipNose’s assets and Paratek Pharmaceuticals’ acquisition of Optinose, is concentrating intellectual property and accelerating integrated device–drug offerings. Growth prospects are further strengthened by rising intranasal vaccine research funding, battlefield analgesia protocols that prefer nasal delivery when venous access is limited, and environmental incentives rewarding low-carbon atomizer formats.

Key Report Takeaways

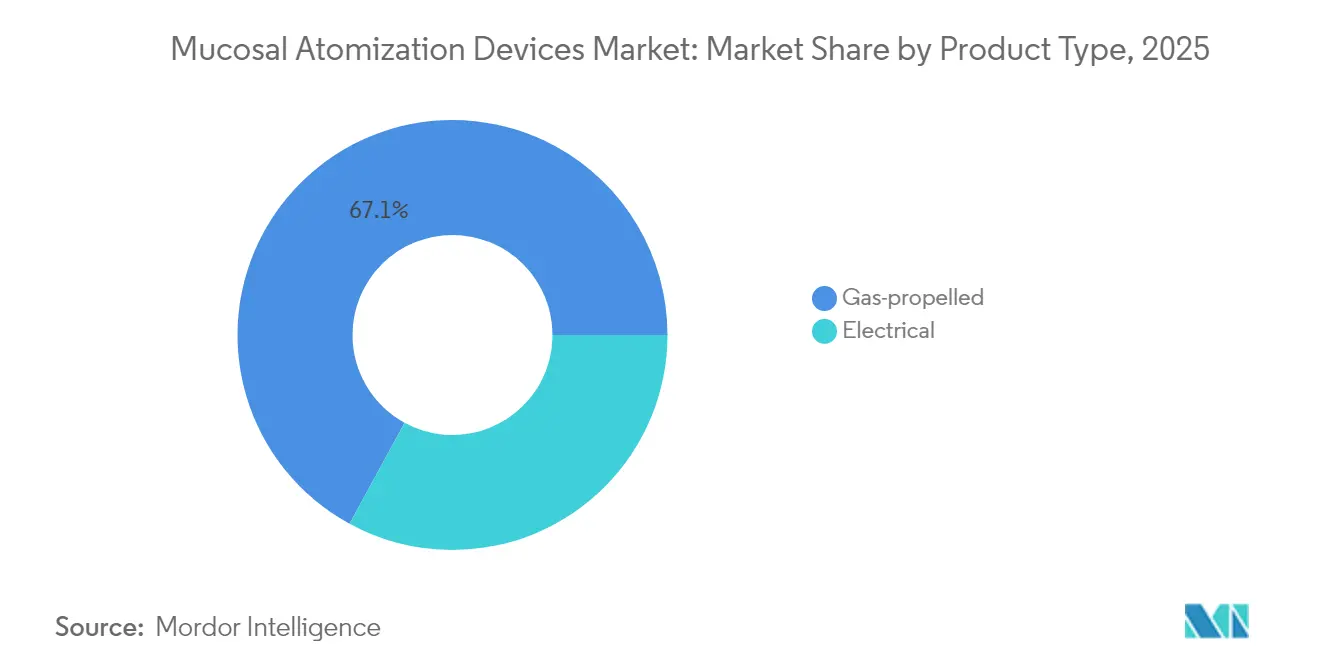

- By product type, gas-propelled devices led with 67.05% revenue share in 2025; electrical atomizers are projected to expand at an 8.51% CAGR to 2031.

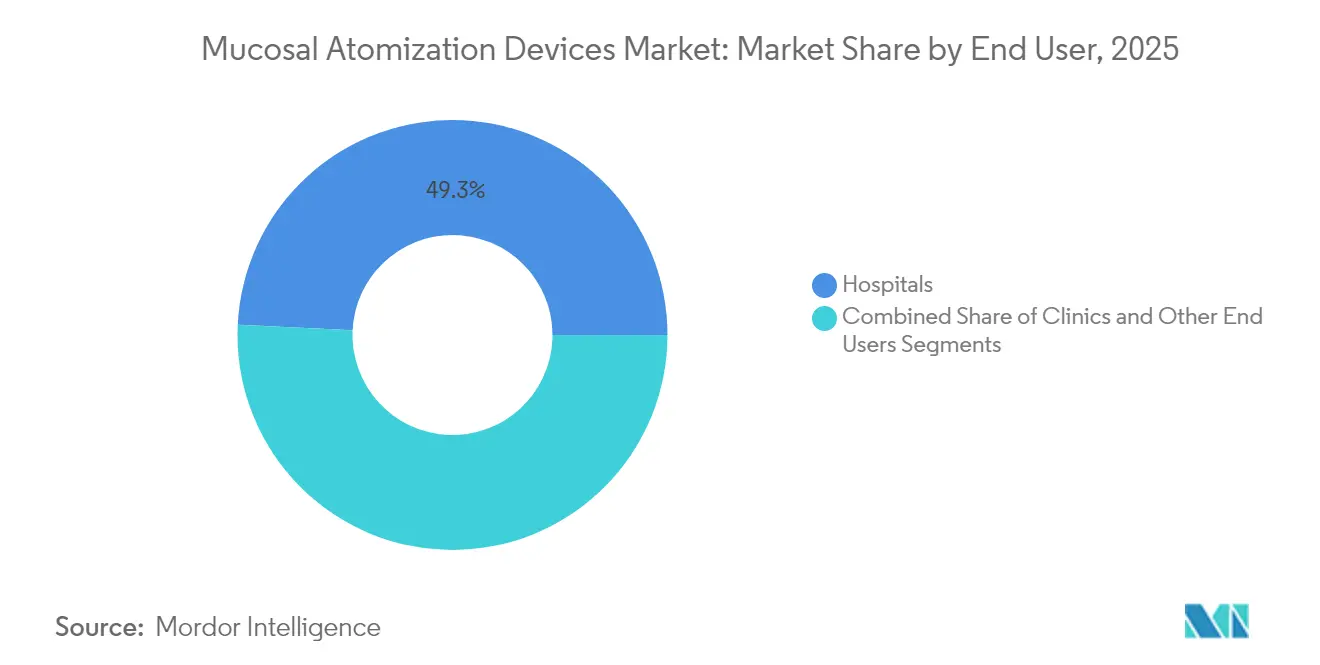

- By end user, hospitals held 49.25% of the mucosal atomization devices market share in 2025, while clinics are forecast to grow at an 8.59% CAGR through 2031.

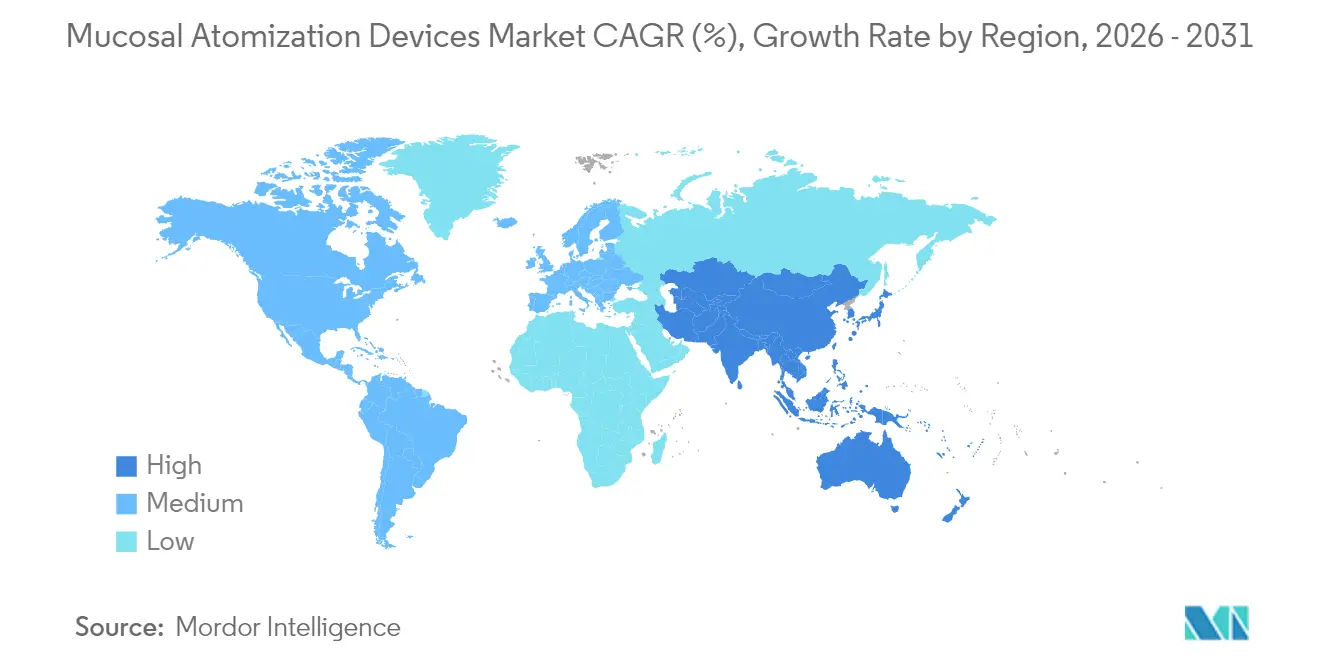

- By geography, North America commanded 41.62% mucosal atomization devices market share in 2025 and Asia-Pacific is advancing at an 8.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mucosal Atomization Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of allergic rhinitis & sinusitis | +1.8% | Global, highest in North America & Europe | Medium term (2-4 years) |

| Technological advancements in atomizer design | +1.5% | Global, led by North America & Asia-Pacific | Long term (≥ 4 years) |

| Rising intranasal vaccine / drug-delivery R&D funding | +1.2% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Adoption in pre-hospital & battlefield analgesia | +0.9% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Regulatory push for needle-free vaccination in LMICs | +0.7% | Asia-Pacific, Middle East & Africa, South America | Medium term (2-4 years) |

| Integration with smart dose-counter IoT modules | +0.6% | North America & Europe, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Allergic Rhinitis & Sinusitis

Allergic rhinitis now affects 1 in 6 Americans and comparable shares of European populations, creating a consistent stream of patients dependent on rapid symptom relief via intranasal therapy. Network meta-analyses released in 2024 concluded that atomized nasal formulations outperform oral agents on onset of action and safety, supporting higher prescription volumes for steroid, antihistamine, and emergent biologic sprays [2]Bernardo Sousa-Pinto, "Efficacy and safety of intranasal medications for allergic rhinitis: Network meta-analysis," European Journal of Allergy and Clinical Immunology, onlinelibrary.wiley.com. Demand is reinforced by studies linking particulate-rich urban air to rising rhinitis incidence, especially in Asia and Latin America, underscoring the global relevance of the mucosal atomization devices market. The addition of monoclonal antibodies such as omalizumab and dupilumab, which require precise mucosal targeting to optimize bioavailability, has further entrenched device use in specialty allergy clinics [3]Xiangning Cheng, "Recent Studies and Prospects of Biologics in Allergic Rhinitis Treatment," MDPI, mdpi.com. Expert panels now recommend nasal anticholinergics including ipratropium bromide through atomizers for patients with persistent rhinorrhea unresponsive to standard therapy, boosting replacement cycles and unit volumes.

Technological Advancements in Atomizer Design

Device engineering breakthroughs are raising dosing precision, stability of biologics, and user adherence. Bespak’s single-use NasaDose platform employs unit-dose blisters that protect fragile peptides from humidity until actuation. Academic–industry collaborations inspired by squid jet propulsion have produced prototype no-needle systems capable of deeper turbinate penetration and lower residual volume, improving bioavailability by double-digit percentages in pre-clinical models. Trudell Medical’s AEROCOUNT integrates Bluetooth and cloud telemetry, allowing clinicians to track dose events in real time and adjust regimens remotely—functionality now reimbursed by several U.S. payers. Nanostructured lipid carrier research suggests atomized particles below 150 nm can cross the olfactory epithelium and deliver small molecules to the CNS, widening future indications. Meanwhile, temperature-controlled radiofrequency tools for nasal obstruction are cutting surgical costs by USD 20 million over four years for large insurers, indirectly driving awareness of intranasal therapeutic solutions.

Rising Intranasal Vaccine / Drug-Delivery R&D Funding

Federal agencies earmarked unprecedented grants for nasal vaccines after observing mucosal immunity advantages during the COVID-19 response, channeling funds through NIH’s RADx program and BARDA contracts. The FDA’s Center for Biologics Evaluation and Research cleared 24 biological device applications in 2024—five involving atomized nasal delivery—signaling regulatory confidence in the modality. Multicenter trials demonstrated that live-attenuated intranasal influenza candidates reduced viral shedding more effectively than intramuscular comparators, driving new entrants into the mucosal atomization devices market. Veterinary vaccine researchers are also applying spray-drying and nano-carriers to poultry and swine respiratory diseases, expanding the technology’s manufacturing base and lowering component costs. Patents covering thermostable excipient blends, granted in 2025, are removing cold-chain constraints for remote immunization programs in low- and middle-income countries.

Adoption in Pre-Hospital & Battlefield Analgesia

Emergency medical services view intranasal routes as the fastest alternative when intravenous access is delayed. National protocols in the United States added 8 mg naloxone sprays to ambulatory kits in 2024 to counter fentanyl analogs, elevating procurement volumes. French special forces published case series confirming that 1.5 mg/kg ketamine via nasal atomizer reduced evacuation-time pain scores by 40% compared with historical morphine controls. Experimental long-acting naloxone nanoparticles delivered intranasally maintained therapeutic plasma levels for 48 hours, potentially preventing renarcotization in overdose clusters. Deployment of low-barrier distribution boxes in West Virginia dispensed 2,383 naloxone kits in six months, proving community-level scalability for atomizer-ready medications. These operational gains anchor sustained device reorder cycles, boosting the mucosal atomization devices market across EMS and defense channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Side effects due to overdose / mist leakage | −0.8% | Global, higher in developing markets | Short term (≤ 2 years) |

| Availability of alternative delivery routes | −1.2% | Global, particularly in developed markets | Medium term (2-4 years) |

| Supply-chain fragility of specialty nozzle materials | −0.6% | Global, acute in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Environmental concerns over canned-gas propellants | −0.9% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Side Effects Due to Overdose / Mist Leakage

Device misfires and droplet backflow can lead to sub-therapeutic exposure or adverse events, especially when administered by minimally trained users. Observational studies covering 1,200 pre-hospital naloxone reversals linked inconsistent spray plume geometry with withdrawal-related agitation in 7% of cases. The FDA now mandates tighter droplet-size thresholds in new 510(k) submissions, increasing quality-assurance costs and prolonging design-validation cycles. Manufacturers respond by adding visual color-change indicators that confirm full actuation, yet learning curves remain steep for community responders. Adoption headwinds in resource-constrained markets thus temporarily temper the mucosal atomization devices market growth rate.

Availability of Alternative Delivery Routes

Competing transdermal, buccal, and microneedle formats are advancing rapidly and lure prescribers with familiar reimbursement codes. Microneedle system revenue exceeded USD 10 billion in 2024 and promises painless sustained release, challenging intranasal dominance in chronic pain and hormone therapy. Oral mucoadhesive films, some combining permeation enhancers and taste-masking polymers, reached USD 55 billion in global sales forecasts for 2030, diverting R&D funding away from nasal projects. Pharmaceutical strategists also favor injectable wearables that stream real-time pharmacokinetic data, a feature not yet standard in atomizers. These factors subtract 1.2 percentage points from the projected CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gas-Propelled Dominance Faces Environmental Pressures

Gas-propelled platforms represented the largest slice of the mucosal atomization devices market size, accounting for USD 0.49 billion and 67.05% of 2025 revenue. Their entrenched status stems from clinician familiarity, proven dose consistency, and straightforward filling operations. Nevertheless, environmental policy shifts are compelling reformulation. The U.S. Consumer Product Safety Commission and the Environmental Protection Agency proposed phase-down schedules for HFC-134a and HFC-152a, prompting manufacturers to pilot low-global-warming blends that deliver at least 90% carbon reduction without compromising plume mass median aerodynamic diameter. Clinical bridging studies indicate pharmacokinetic equivalence, paving regulatory pathways for commercial rollout beginning 2027. Electrical atomizers, by comparison, posted only 32.95% of 2025 sales but generate headline growth of 8.51% CAGR as hospitals gravitate toward propellant-free options with programmable spray volumes and IoT telemetry. Absence of canned gases streamlines global shipping compliance, trimming logistics expenses by 12% on average and mitigating supply chain exposure to propellant shortages. Higher unit cost remains the principal barrier, though total-cost-of-ownership models that factor in environmental levies increasingly favor electric solutions across developed economies.

These dynamics reinforce the expected tilt: gas-propelled units maintain core emergency-medicine dominance through 2026, after which new ESG-motivated procurement policies tip the sales mix toward electrical formats. Manufacturers with hybrid pipelines—able to supply both propellant and propellant-free versions—are positioned to defend share and capture sustainability premiums, preserving competitive balance within the mucosal atomization devices market.

By End User: Hospital Leadership Shifts Toward Clinic Expansion

Hospitals generated the highest revenue in 2025, capturing 49.25% of the mucosal atomization devices market size through emergency department protocols and perioperative pain management pathways. Monthly stock-rotation programs ensure continuous ordering as atomizers serve multiple purposes, from naloxone reversal to sedation and topical hemostasis. Group purchasing organizations increasingly negotiate portfolio contracts that bundle multi-drug compatibility and pediatric nozzles, encouraging standardization around widely validated platforms. Conversely, clinics, urgent care centers, and physician offices embody the fastest¬-growing channel, advancing at 8.59% CAGR. Drivers include consumer preference for needle-free allergy and migraine therapy administered during scheduled visits, as well as improved reimbursement for office-based drug administration codes. The FDA’s approval of neffy for pediatric anaphylaxis opened a large new cohort for outpatient dispensing, triggering incremental unit sales, especially during high-pollen seasons.

Home-health and long-term-care environments contribute a smaller but rising slice as device ergonomics improve. Battery-operated actuators with audible dose cues allow elderly or vision-impaired patients to self-administer therapies, minimizing caregiver burden. Broadening use cases across settings suggests hospitals will gradually concede share to ambulatory and at-home channels, yet they will remain critical gatekeepers for high-acuity and formulary decisions until the close of the forecast period.

Geography Analysis

North America, anchored by the United States, delivered 41.62% of global sales in 2025, buoyed by an FDA framework that streamlines chemistry-manufacturing-controls submissions and enables 510(k) plus NDA-combination filings. National naloxone distribution initiatives and state-level standing orders bolster everyday demand, while advanced payer systems incentivize smart dose-tracking atomizers. Canada’s Health Canada fast-track for nasal epinephrine products signals regional alignment, shortening launch timelines for cross-border entrants.

Asia-Pacific records the steepest trajectory with an 8.73% CAGR. Japan’s Pharmaceuticals and Medical Devices Agency accepted Aculys Pharma’s diazepam nasal spray application in 2024, the first antiepileptic of its kind, establishing a visible regulatory precedent. China’s National Medical Products Administration and Australia’s Therapeutic Goods Administration evaluated neffy under parallel review pathways, highlighting converging standards that favor multinational submissions. Expanding middle-class healthcare spend and high prevalence of allergic rhinitis in urbanizing economies underpin durable device volume growth.

Europe offers mature but steady expansion as the EU’s Medical Device Regulation imposes stringent post-market surveillance, creating competitive openings for suppliers with robust clinical data and environmental credentials. Adoption of Green Deal targets exerts pressure on propellant-based products, accelerating the pivot to electric atomizers and low-GWP propellants. Emerging territories in Latin America, the Middle East, and Africa represent nascent opportunities: modernization of emergency medical systems and donor-funded vaccination drives stimulate demand, yet structural hurdles—from limited cold-chain networks to clinician training deficits—moderate penetration rates for the mucosal atomization devices market.

Regulatory Landscape

In the United States, mucosal atomization devices (MAD) used for topical anesthesia delivery generally operate under the FDA medical device framework, with laryngo-tracheal topical anesthesia applicators classified as Class II under 21 CFR 868.5170 (product code CCT), typically requiring 510(k) clearance. October 2024 is an example of continuing regulatory activity, when the FDA issued 510(k) clearance to Dualams, Inc. (dba AirKor) for its UltraEzAir (UEA1A) laryngo-tracheal mucosal atomization device (K240114), demonstrating ongoing entry and iteration within cleared, predicate-based pathways.

In Europe, atomization devices that are supplied as part of, or assessed alongside, medicinal products need to comply with the EU Medical Device Regulation (EU) 2017/745 (MDR). For combination configurations, additional requirements can be triggered, including those linked to Article 117 when a device is used with a medicinal product. On the drug-quality side, EMA guidance for pharmaceutical quality of inhalation and nasal medicinal products sets expectations around dose uniformity, plume and droplet characteristics, and the quality documentation required for nasal delivery systems used with medicines, tightening the interface between device engineering and medicinal product dossiers.

Value Chain Analysis

The value chain for mucosal atomization devices starts with specialized raw materials, including medical-grade polymers, elastomers, adhesives, and, for certain formats, propellant-related components. It then moves through precision manufacturing steps such as micro-nozzle fabrication, assembly, and sterile packaging. Design control and verification activities are linked to regulated performance attributes, including consistent atomization and targeting. In the US, the supply chain also spans device categories that include Class II laryngo-tracheal topical anesthesia applicators (product code CCT) and related aerosol delivery devices tracked under FDA listings.

Demand is directed downstream through hospital anesthesia, airway management, emergency medicine, and EMS procurement channels, using a mix of direct sales, group purchasing organizations, and specialized medical distributors. Manufacturers with scaled production footprints and quality systems can support shorter lead times for regulated devices and multiple clinical workflows. Teleflex, for instance, markets MAD platforms for anesthesia and atomization applications and operates manufacturing operations that include Teleflex Medical de Tecate, S. de R.L de C.V., supporting supply continuity for high-throughput clinical customers.

Competitive Landscape

The landscape is moderately fragmented yet trending toward consolidation. Aptar Pharma’s USD 12.5 million purchase of SipNose fortified its early-stage biologics atomization capabilities, while Paratek Pharmaceuticals’ USD 330 million acquisition of Optinose diversified its revenue stream beyond antibiotics. Patent litigation at the U.S. International Trade Commission underscores the strategic value of nozzle geometry and dose-metering algorithms; successful enforcement can secure multi-year royalties. Tier-one firms wield vertically integrated manufacturing across elastomer molding and drug-device assembly, delivering scale economies coveted by smaller peers.

Competitive vectors increasingly center on sustainability and digitalization. Companies pioneering HFO-1234ze propellant blends or battery-free piezoelectric drivers attract hospital procurement committees seeking ESG compliance. Simultaneously, IoT-equipped actuators generate real-world evidence that supports health-economics dossiers and payer negotiations. White-space segments—pediatric-specific tips, CNS-targeted nano-carriers, and AI-driven adherence platforms—remain largely uncontested, offering entry points for nimble newcomers willing to navigate regulatory complexity.

Mucosal Atomization Devices Industry Leaders

-

Teleflex Incorporated

-

DeVilbiss Healthcare LLC

-

Becton, Dickinson and Company

-

Cook Medical

-

Integra LifeSciences

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White-space opportunities concentrate in procedure-driven airway and anesthesia use cases where atomization functions as a workflow enabler, rather than a single-drug accessory. This supports broader compatibility with clinician-selected medications. FDA clearance activity continues to validate new devices for these settings, including the October 2024 510(k) clearance for Dualams, Inc. (dba AirKor) for the UltraEzAir laryngo-tracheal mucosal atomization device (K240114). This reinforces the space for differentiated catheter geometry, targeting, and ease-of-use improvements in bronchoscopy, awake intubation, and related topical anesthesia procedures.

A second opportunity is at the device-drug development interface for nasal delivery, where quality expectations for nasal products and combination configurations can translate into a premium for platforms that demonstrate strong dose consistency and documented spray performance. These requirements sit alongside EMA guidance for pharmaceutical quality of inhalation and nasal medicinal products and MDR requirements for combination scenarios. In parallel with acute care, expanding clinical research that uses commercial mucosal atomization platforms for controlled intranasal administration can help suppliers deepen evidence packages and standardize protocols across sites, supporting uptake of higher-precision platforms already present in the competitive landscape, including propellant-free and connected formats.

Recent Industry Developments

- May 2026: A controlled human influenza infection study published in Cell reported use of a Teleflex mucosal atomization device for intranasal inoculation in a research setting. The publication reinforces the device category's role in standardized intranasal administration protocols and supports broader clinical confidence in repeatable delivery performance across sites.

- March 2025: Paratek Pharmaceuticals completed its acquisition of Optinose and its chronic rhinosinusitis nasal spray Xhance for up to USD 330 million. The deal concentrated device-drug commercialization capabilities under a larger portfolio owner and increased competitive intensity around integrated intranasal therapy offerings.

- December 2024: ARS Pharmaceuticals reported that partners in China, Japan, and Australia filed neffy 2 mg packages following trial results cited by the company. These submissions extended the regulatory footprint of a high-profile nasal rescue therapy and raised the bar for atomization performance and usability in pediatric and emergency-use contexts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers devices that convert liquid medication into a fine mist for delivery across mucosal surfaces, most commonly for intranasal use in clinical care. We size the market in value terms based on device sales used in hospitals, clinics, and similar care settings.

Scope exclusions: Excludes the drug value delivered through these devices and excludes general-purpose nebulizers that are not designed for mucosal atomization use cases.

Segmentation Overview

-

By Product Type

- Gas-propelled

- Electrical

-

By End User

- Hospitals

- Clinics

- Other End Users

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the foundation for demand drivers, clinical usage context, and the market boundaries. We referred to public sources such as the US FDA device databases, Centers for Disease Control and Prevention (CDC) clinical publications, the World Health Organization (WHO) guidance notes, and peer reviewed journals that cover intranasal delivery and emergency care protocols.

In parallel, we reviewed company filings, investor presentations, product literature, and reputable press to understand pricing ranges, product positioning, and channel patterns. Where needed, paid subscriptions for company financials and intelligence, patent databases, and import export shipment level data were used to cross check product presence, manufacturing footprints, and trade flows. These are illustrative examples, and many other public sources were also used for data collection, validation, and clarification during research.

Primary Interviews and Surveys

Primary work focused on confirming real world adoption and purchasing behavior, especially in emergency care, anesthesia support, and outpatient procedures where atomization is used for fast, needle free delivery. We spoke with a mix of manufacturers, distributors, clinicians, and procurement led respondents across APAC, EMEA, and the Americas, so model assumptions could be challenged and adjusted where gaps were found.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | APAC: 41% |

| Mid tier: 58% | Functional/Unit leaders: 29% | EMEA: 35% |

| Smaller Players: 14% | Managers: 59% | Americas: 24% |

Market-Sizing & Forecasting

The sizing starts from a top down logic where procedure volumes and care setting activity are used to reconstruct the addressable device demand pool, which is then translated into value using typical replacement rates and observed pricing. To keep the totals realistic, we corroborated the output using selective bottom-up approximations such as sampled average selling price (ASP) checks, distributor channel feedback, and a roll up of visible supplier presence in key regions.

Inputs that mattered most included emergency department and outpatient procedure volumes linked to intranasal administration, anesthesia and pain management protocol adoption, the share of facilities using atomization instead of alternative delivery routes, replacement cycles for reusable components, and ASP progression by device type (gas-propelled versus electrical). When a country had limited direct signals, the gap was handled by using proxy indicators such as hospital count, bed density, and comparable adoption ratios from similar health systems, and then pressure testing those assumptions in interviews.

For forecasting, scenario analysis was used so growth could be tied to measurable drivers like care setting expansion, procurement normalization after one-off spikes, and gradual shifts toward needle free administration. Assumptions were kept simple and aligned to expert consensus on likely adoption pace and pricing changes across the forecast window.

Data Validation & Update Cycle

Validation is done through several checks so the final number is not dependent on a single input. We compare model outputs against independent signals such as procedure activity trends, import export movement where relevant, and plausible spend per facility, and then we recheck any large variances before sign off.

A second analyst reviews the calculations, assumptions, and year to year movements. Any anomalies trigger a re contact to primary respondents for clarification. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory changes, pricing shocks, or supply disruptions. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Mucosal Atomization Devices Market Estimate Compared With Other Published Estimates

Published market values for mucosal atomization devices often differ because each study may count a different set of device categories, care settings, and countries, and then apply different price and replacement assumptions. We present the comparison below to make the main sources of spread easier to understand.

Procedure activity signals and care setting adoption checks are the main evidence points used to keep Mordor Intelligence's estimate aligned to actual clinical usage, which can reduce overcounting from broader nasal delivery device scopes. Differences also come from whether estimates include adjacent atomization tools used outside routine hospital and clinic procurement, the way ASP is trended over time, and how currency conversion timing is treated when markets move quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.78 B (2026) | |

| Global Consultancy A | USD 0.61 B (2025) | Uses a different base year and a wider product family that can fold in broader nasal delivery devices beyond mucosal atomization, which can shift the starting value when ASP and adoption are averaged across more categories. |

| Industry Research Desk B | USD 0.63 B (2025) | Relies on a base year that is closer to early demand patterns and applies a higher growth curve with fewer visible checks tied to facility level usage and replacement cycles, which can move the total upward in the near term. |

Across the three figures, the spread is mainly explained by scope boundaries, base year choice, and how pricing and replacement are carried through the model. Our approach stays traceable because the key steps are tied to observable care setting demand indicators and then cross checked with practical ASP and channel feedback before totals are finalized.

Key Questions Answered in the Report

What is the current mucosal atomization devices market size and how fast is it growing?

The mucosal atomization devices market size is USD 0.78 billion in 2026 and is projected to expand at a 6.91% CAGR to reach USD 1.09 billion by 2031.

Which geographic region is expected to record the highest growth rate through 2031?

Asia-Pacific is forecast to grow at an 8.73% CAGR, the fastest among all regions, supported by favorable approvals in China, Japan, and Australia.

Which device category is showing the strongest growth momentum?

Electrical atomizers are advancing at an 8.51% CAGR as healthcare buyers pivot toward propellant-free, IoT-enabled platforms.

Why do hospitals currently account for the largest share of demand?

Hospitals hold 49.25% of the mucosal atomization devices market share because emergency departments rely on nasal delivery for rapid administration of naloxone, ketamine, and other critical drugs.

What recent regulatory milestone has accelerated market adoption?

The FDA’s 2024 approval of neffy epinephrine nasal spray validated intranasal delivery for life-threatening allergic reactions, spurring broader adoption across pediatric and adult populations.

How are sustainability regulations influencing product development?

Proposed U.S. restrictions on high-GWP HFC-134a and HFC-152a propellants are driving manufacturers to develop low-carbon propellant blends and switch to electrical atomizers that meet upcoming environmental standards.

Page last updated on: