Smart Pills Diagnostics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.34 Billion |

| Market Size (2031) | USD 2.19 Billion |

| Growth Rate (2026 - 2031) | 10.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

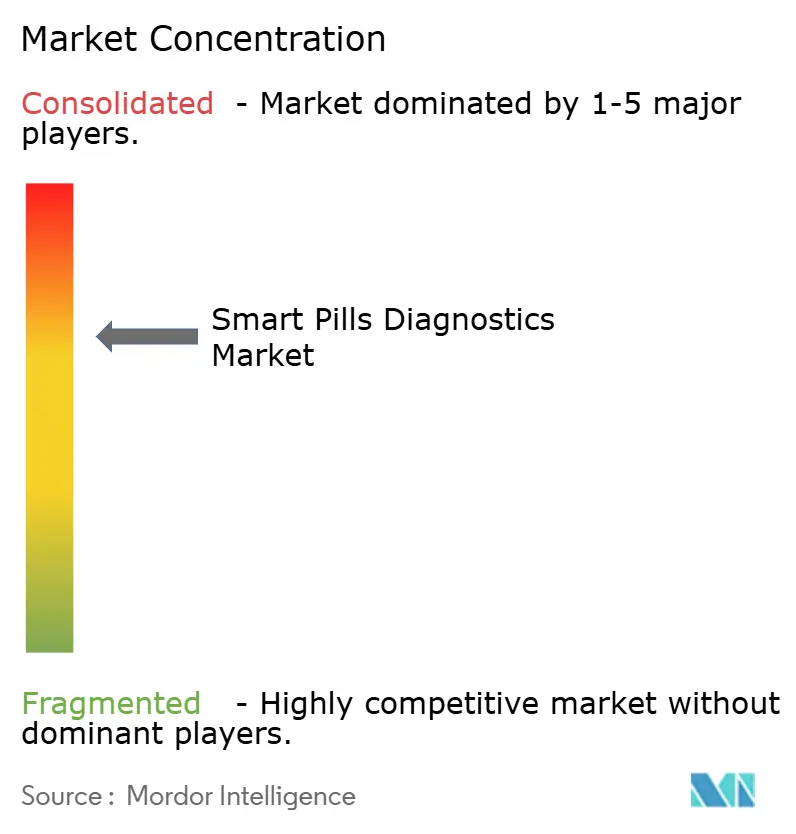

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Pills Diagnostics Market Analysis by Mordor Intelligence

The Smart Pills Diagnostics Market size is expected to grow from USD 1.21 billion in 2025 to USD 1.34 billion in 2026 and is forecast to reach USD 2.19 billion by 2031 at 10.38% CAGR over 2026-2031.

The performance of the market underscores several converging forces: the widening burden of gastrointestinal (GI) disease, increasingly favorable reimbursement policies across major OECD economies, and the migration of ultra-low-power telemetry—originally engineered for spaceflight—into commercial capsule platforms. U.S. FDA clearance of CapsoVision’s CapsoCam Plus for pediatric use in January 2025[1]U.S. Food and Drug Administration, “510(k) Premarket Notification — CapsoCam Plus,” FDA.govbroadens the eligible patient pool, while Medtronic’s PillCam Genius SB, cleared in May 2024, illustrates the competitive tempo among leading device makers. Cloud-hosted AI reading tools, cost advantages in ambulatory settings, and streamlined regulatory timelines in Asia-Pacific collectively expand clinical access and sharpen pricing pressures across the value chain.

Key Report Takeaways

- By indication, gastrointestinal bleeding accounted for 39.10% of smart pills diagnostics market share in 2025. Crohn’s disease is advancing at a 12.88% CAGR through 2031, the fastest rate among all indications.

- By component, capsule endoscopes held a 56.45% share of smart pills diagnostics market size in 2025. Imaging software and workstations are growing at a 13.65% CAGR through 2031, the highest among components.

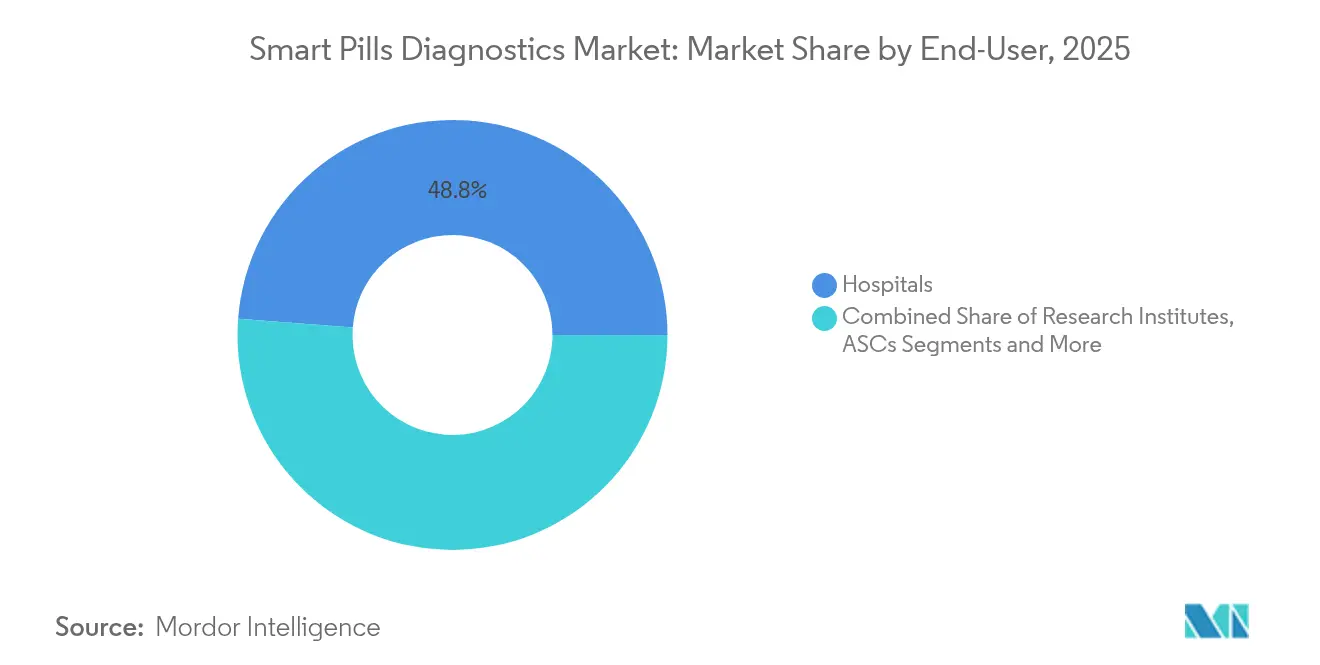

- By end user, hospitals captured 48.80% of 2025 revenue, while ambulatory surgery centers are expanding at a 12.05% CAGR to 2031.

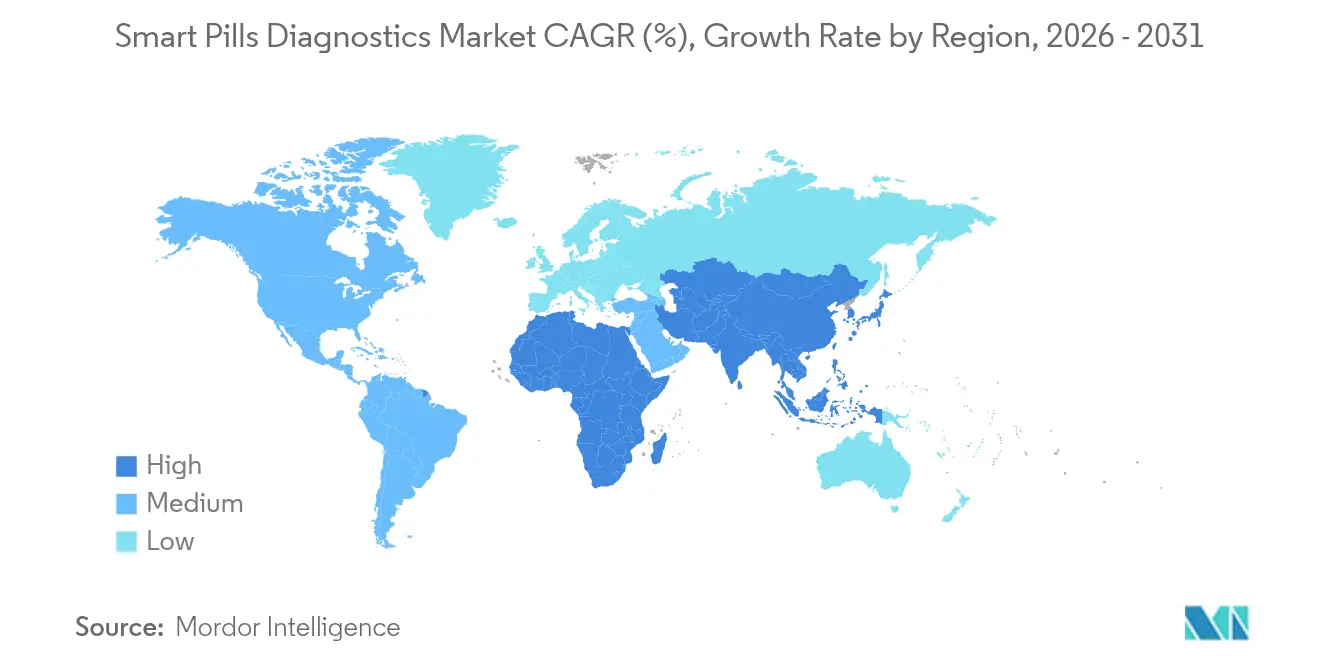

- By geography, North America led with 40.85% of 2025 revenue; Asia-Pacific is forecast to post a 12.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Pills Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of gastrointestinal disorders | 2.3% | Global, with highest burden in North America & EU | Medium term (2-4 years) |

| Demand for minimally-invasive diagnostic modalities | 2.1% | OECD markets, spillover to APAC urban centers | Short term (≤ 2 years) |

| Favorable reimbursement for capsule endoscopy in OECD markets | 1.8% | North America, Western Europe, Japan | Short term (≤ 2 years) |

| Rapid CMOS sensor & AI image-analysis advances | 2.0% | Global, led by North America & East Asia | Medium term (2-4 years) |

| Integration of gas-sensing capsules for microbiome diagnostics | 1.2% | North America, Australia, select EU markets | Long term (≥ 4 years) |

| Space-flight R&D spin-offs enabling ultra-low-power telemetry | 1.2% | Global, with early adoption in US & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Gastrointestinal Disorders

Inflammatory bowel disease now affects 3.1 million U.S. adults, with global incidence climbing 2%–3% annually as diet, urbanization, and enhanced diagnostic awareness shift disease patterns.[2]Centers for Disease Control and Prevention, “Inflammatory Bowel Disease Data and Statistics,” CDC.govPersistent conditions such as Crohn’s disease and ulcerative colitis require repeated mucosal assessments, making capsule imaging a recurring revenue stream. Early detection of small-bowel tumors through capsule visualization reduces the need for exploratory surgery and accelerates oncologic intervention. The doubling of celiac disease prevalence over two decades further boosts demand for second-line capsule imaging when biopsy results are inconclusive. These epidemiologic trends align most strongly with aging, higher-BMI populations in North America and Europe. The World Health Organization estimates that non-communicable digestive disorders will claim 15% of global disability-adjusted life years by 2030, reinforcing the strategic value of early, noninvasive diagnostics.[3]World Health Organization, “Non-Communicable Digestive Diseases,” WHO.int

Demand for Minimally Invasive Diagnostic Modalities

Patient preference for sedation-free, same-day discharge procedures is reshaping GI workflows. Capsule endoscopy eliminates bowel insufflation and anesthesia risks, aligning with value-based care incentives. A 2024 study in Gastrointestinal Endoscopy reported that 78% of patients preferred capsules when clinically appropriate, citing comfort and convenience. Ambulatory surgery centers offer capsule imaging 30%–50% below hospital prices, accelerating uptake among self-pay and high-deductible patients. CMS broadened capsule coverage in 2024 for suspected small-bowel bleeding, easing prior authorization and spurring immediate demand. Pilot programs in Australia and Canada mirror these U.S. shifts, signaling international momentum.

Favorable Reimbursement for Capsule Endoscopy in OECD Markets

Medicare reimburses capsule endoscopy under CPT codes 91110 and 91113 at USD 485 and USD 520, removing a key financial barrier for an estimated 64 million U.S. beneficiaries. Private insurers such as Aetna, Cigna, and UnitedHealthcare have aligned their diagnostic pathways with these codes, giving hospitals a clear revenue stream and accelerating equipment pay-back periods. In Europe, the United Kingdom’s National Health Service pays providers GBP 450 per procedure, while Germany’s statutory funds cover the exam without patient copay, creating consistent cash flow for high-volume centers. Japan boosted reimbursement by 12% in April 2024, a shift that signals governmental confidence in capsule imaging for early cancer detection and inflammatory bowel disease surveillance. With payment clarity in place, providers can justify capital outlays, and manufacturers benefit from faster repeat sales of consumable capsules. These dynamics are expected to keep procedure volumes on an upward trajectory through at least 2027.

Rapid CMOS Sensor and AI Image-Analysis Advances

Current CMOS sensors deliver one-megapixel resolution at six frames per second while drawing under 100 milliwatts, a 40% power cut compared to 2020-vintage capsules, which extends battery life and small-bowel transit coverage. Convolutional neural networks trained on more than one million annotated frames now reach 94% sensitivity for polyp detection and 92% specificity for bleeding, trimming radiologist reading time by 35% and reducing false negatives. CapsoVision plans to launch real-time AI lesion detection in late 2025, a move that could erode Medtronic’s long-held software edge and shift competition toward analytics rather than hardware. Olympus and Philips are already hosting cloud-based reading suites, allowing rural clinicians to obtain rapid subspecialty interpretation without onsite experts. Compliance with the IEC 60601-1-2 electromagnetic standard assures clinicians that these AI-enabled capsules will not disrupt pacemakers or other implants, further smoothing hospital procurement decisions. Together, sensor efficiency and algorithm accuracy transform capsule systems from niche devices into mainstream diagnostic workhorses poised for broad adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront device & reader costs | -1.5% | Emerging markets in APAC, MEA, South America | Short term (≤ 2 years) |

| Uneven reimbursement in emerging economies | -1.3% | India, China, Brazil, South Africa | Medium term (2-4 years) |

| Patient reluctance to swallow electronic devices | -0.8% | Global, with higher incidence in elderly cohorts | Short term (≤ 2 years) |

| Electromagnetic interference concerns in pacemaker patients | -0.6% | North America, Europe (aging populations) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Device & Reader Costs

Capital requirements of USD 40,000–80,000 for recorders and workstations hinder adoption in community facilities, while single-use capsules priced at USD 500–2,000 strain budgets where reimbursement is partial or absent. A 2024 survey of Indian GI practices found 62% citing equipment cost as the top barrier to offering capsule studies, despite strong clinical demand. Pay-per-use and leasing models are emerging but depend on robust credit infrastructure seldom present in low-income regions, sustaining a cost headwind through the near term.

Uneven Reimbursement in Emerging Economies

Outside OECD markets, payment policies vary widely. Brazil’s public system omits capsule studies from its essential list, while private insurers under-reimburse by up to 50%, dampening provider interest. China added capsule imaging to its catalog in 2023, yet provincial implementation remains inconsistent, and South Africa restricts coverage to suspected tumors, excluding inflammatory disorders. This fragmentation is expected to persist beyond mid-decade, capping volume growth in otherwise high-potential regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: Crohn’s Disease Drives Fastest Growth

Crohn’s disease leads with a 12.88% CAGR to 2031 as biologic therapy monitoring requires serial mucosal imaging. Gastrointestinal bleeding maintained 39.10% of smart pills diagnostics market share in 2025 thanks to its acute presentation and limited alternative diagnostics. Small-bowel tumors benefit from full intestinal visualization unavailable in traditional scopes, while celiac disease remains a stable, secondary niche. A 2024 Lancet study found capsule imaging altered management in 42% of Crohn’s patients, accelerating biologic initiation and lowering hospitalization rates. Regulatory fast-track pathways for indication-specific capsules shorten development cycles, enabling manufacturers to target these high-growth chronic indications.

By Component: AI Software Platforms Outpace Hardware

Imaging software and workstations are rising at 13.65% CAGR as cloud analytics cut reading time and enable remote subspecialty interpretation. Capsule endoscopes retained 56.45% of 2025 revenue, yet hardware commoditization squeezes margins. Medtronic’s integrated reading suite trims case review to under 30 minutes, while CapsoVision’s AI-driven lesion detection—scheduled for late-2025 release—signals a pivot toward subscription software revenue. Accessories such as patency capsules add incremental value but remain minor contributors

By End User: Care Delivery Moves Closer to Home

Hospitals accounted for 48.80% of 2025 revenue, given their established infrastructure and reimbursement flows. Yet home-based programs are forecast for a 14.85% CAGR as 5G connectivity enables secure cloud upload of capsule data packages. Patient autonomy and convenience align with payer goals to limit costly facility visits, making at-home capsule kits an attractive alternative.

Diagnostic Centers retain relevance for complex case interpretation and high-throughput reading services, especially when multi-sensor capsules generate large datasets requiring subspecialist review. Research Institutes maintain a steady share by coordinating clinical trials that validate new disease applications. Collectively, end-user diversification enhances resilience across the smart pills diagnostics market, reducing reliance on any single care setting.

Geography Analysis

North America held 40.85% of 2025 revenue, supported by Medicare reimbursement and a dense network of inflammatory bowel disease centers. FDA pediatric clearance of CapsoCam Plus in 2025 further widens the addressable base. Canada pilots capsule imaging for iron-deficiency anemia, cutting colonoscopy waits, whereas Mexico’s private sector drives urban uptake amid public-budget limits.

Asia-Pacific is projected to expand at a 12.31% CAGR, the fastest globally, propelled by streamlined approvals in China, Japan, and India. Japan’s 12% reimbursement boost in 2024 underscores its emphasis on early detection, while India’s shortened approval timelines encourage both domestic and foreign entrants. Australia and South Korea extend coverage for broader indications, bolstering tertiary-care adoption.

Europe, the Middle East & Africa, and South America grow more steadily. Germany funds capsule imaging with no copay for documented small-bowel pathology, while the U.K. reimburses GBP 450 per procedure but faces staffing constraints. Gulf states adopt rapidly via medical tourism channels. South Africa and Brazil remain constrained by partial or absent reimbursement, tempering near-term volume gains.

Regulatory Landscape

In the United States, smart pills diagnostics such as capsule endoscopy and related ingestible diagnostic systems are regulated by the US Food and Drug Administration (FDA), with many products advancing via the 510(k) pathway when substantial equivalence to a predicate exists. The market continues to be shaped by device-specific controls for ingestible gastrointestinal capsule imaging systems and by software documentation expectations that affect cloud-connected readers and AI-enabled analysis modules, including cybersecurity documentation such as a Software Bill of Materials (SBOM) required in medical device submissions under Section 524B of the FD&C Act (effective for applicable submissions since October 2023).

In Europe, market access is governed by Regulation (EU) 2017/745 (MDR), with conformity assessment via a Notified Body and alignment to the MDR General Safety and Performance Requirements, which elevates documentation and post-market obligations for manufacturers commercializing capsule platforms and associated software. For drug-device combinations that incorporate ingestible sensors as part of a medicinal product, companies must manage interface requirements spanning medical device and medicinal product oversight, typically supported by ISO 13485 quality management expectations and relevant IEC electromagnetic compatibility requirements referenced by providers during procurement for use in patients with implanted devices.

Value Chain Analysis

The value chain begins with specialized component supply for imaging and telemetry, including CMOS sensors, LEDs, batteries, antennas, and medical-grade housings and coatings, followed by device design, firmware/software development, and system integration into recorders, receivers, and reading workstations. Manufacturing and final assembly are generally performed under medical device quality systems, after which products move through distribution models that include direct sales to hospitals and diagnostic centers, group purchasing and tender-driven procurement in certain markets, and increasing attachment of software subscriptions and cloud hosting for AI-supported reading.

Downstream, service elements such as clinician training, procedure kits, data management, and maintenance of reading platforms drive recurring revenue and influence switching costs for providers. Bottlenecks concentrate around qualified microelectronics and capsule-grade materials, while commercialization is increasingly coupled to reimbursement and workflow integration (hospital GI departments and ambulatory surgery centers). Competitive differentiation is moving along the chain toward image-analysis software, remote reading capability, and data governance readiness for cross-border deployments, rather than capsule hardware alone.

Competitive Landscape

Medtronic, Olympus, and CapsoVision jointly command roughly major share of revenue, yet regional players in East Asia and niche innovators are eroding share. Medtronic’s installed base and first mover advantage underpin more than 3.5 million cumulative PillCam procedures. Olympus cross-sells capsules with legacy scope portfolios, leveraging bundled pricing. CapsoVision’s USD 30 million IPO filing in May 2025 will finance AI roll-out and scaled production, challenging incumbents on software capability. Atmo Biosciences targets gas-sensing capsules for functional GI disorders, creating white-space differentiation. Technology races center on ultra-low-power telemetry and cloud-hosted AI analytics. Compliance with IEC 60601-1-2 electromagnetic standards remains a gating factor to pacemaker-safe deployment.

Smart Pills Diagnostics Industry Leaders

Olympus Corporation

CapsoVision Inc.

Medtronic plc

IntroMedic Co., Ltd.

Jinshan Science & Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are opening around next-generation sensing and ultra-low-power communication that expand the clinical envelope beyond conventional small-bowel visualization. In June 2026, MIT reported a miniaturized ingestible temperature sensor using backscatter communication operating at extremely low power, highlighting a technology pathway for longer-duration sensing in smaller form factors that fits pediatric and ambulatory monitoring use cases. Parallel academic progress in 2026 on magnetically actuated robotic capsules and advanced optical approaches such as near-infrared-II fluorescent capsule imaging underscores whitespace for multimodal capsules that combine improved localization, deeper tissue interrogation, and higher signal-to-noise detection for oncology and complex inflammatory disease workups.

Commercial whitespace also sits at the intersection of AI-enabled reading and expanded indications. The market already shows strong pull for imaging software and workstations, and the addition of AI-assisted modules and broader upper-GI and colon workflows supports vendor strategies that bundle capsules, readers, and cloud analytics into repeatable service lines for hospitals, diagnostic centers, and ambulatory settings. As reimbursement clarity strengthens in OECD markets and providers seek to reduce reading time and standardize interpretation, vendors that can validate performance, manage cybersecurity documentation, and offer scalable cloud or hybrid deployments have a clearer route to capture share through software-led differentiation and workflow integration.

Recent Industry Developments

- May 2026: CapsoVision initiated a clinical study for its CapsoCam UGI capsule endoscope in pancreatic cancer detection, enrolling the first patient during the month. The move broadens capsule endoscopy development beyond small-bowel applications and supports evidence generation for expanded clinical use cases that can pull through software, readers, and procedure volumes.

- December 2025: CapsoVision submitted a 510(k) application to the US FDA for an AI-assisted reading module designed for the CapsoCam Plus capsule endoscope. This reinforces competition shifting toward analytics and workflow efficiency, where software capability becomes a differentiator for provider adoption and recurring revenue.

- May 2024: Medtronic received US FDA clearance for the PillCam Genius SB capsule endoscopy kit. The clearance strengthened Medtronic’s position in small-bowel capsule endoscopy and intensified competitive cadence around integrated kits and reading ecosystems for hospital and outpatient GI settings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers ingestible diagnostic capsules and the related hardware and software that help clinicians visualize and interpret the gastrointestinal tract, using a swallowable device plus external receivers and analysis tools.

Scope exclusions: We exclude general smart pill drug delivery, adherence tracking pills without a diagnostic purpose, and non-ingestible GI imaging systems.

Segmentation Overview

- By Indication

- Gastrointestinal Bleeding

- Crohn’s Disease

- Small-Bowel Tumors

- Celiac Disease

- Other GI Diagnoses

- By Component

- Capsule Endoscope

- Imaging Software & Workstations

- Data Recorder & Receivers

- Other Accessories

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Surgery Centers

- Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the clinical and demand backdrop and to keep our assumptions realistic. We reviewed public health statistics and disease burden signals such as those from the CDC, the World Health Organization, and the National Institutes of Health, along with procedure and care-setting references published by groups such as the American Gastroenterological Association.

To keep the model grounded, we also checked trade and regulatory signals, including FDA device databases and public recall and safety communications, plus peer-reviewed studies on capsule endoscopy outcomes, completion rates, and utilization patterns. Company annual reports, investor presentations, and reputable press were used to understand product launches and geographic exposure, and paid subscriptions for company financials and patent databases were selectively used to validate timelines and pipeline activity. The sources listed here are illustrative only, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on verifying what gets purchased and used in real care pathways, and how pricing and replacement cycles behave across hospitals, imaging centers, and ambulatory settings. We spoke with a mix of device-side leaders, clinical stakeholders, and channel-side respondents across APAC, EMEA, and the Americas so assumptions like procedure mix, upgrade cadence for recorders and workstations, and software attach rates could be corrected and then rechecked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 45% |

| Mid tier: 56% | Functional/Unit leaders: 32% | EMEA: 30% |

| Smaller Players: 16% | Managers: 53% | Americas: 25% |

Market-Sizing & Forecasting

The core sizing starts with a top-down build where epidemiology and diagnostic demand indicators are translated into an addressable procedure pool for capsule-based GI evaluation, and then converted into annual revenues through device and component spending. To keep the totals practical, the output is then stress-tested using selective bottom-up checks such as sampled average selling prices times expected unit volumes for capsule endoscopes, plus channel checks for recorder and workstation refresh cycles.

Key inputs that influence the model include capsule endoscopy procedure volumes, GI bleeding and inflammatory bowel disease case loads, the share of patients routed to capsule endoscopy versus other diagnostic options, average capsule pricing by major region, and attach rates for imaging software and data recorders. Where component-level data was patchy, we used conservative gap-handling by anchoring accessory and software revenue to observed installation base patterns and expected replacement timing, before results were reconciled back to the total spend.

For forecasting, we mainly rely on scenario analysis that is tied to a small set of drivers that respondents could validate, including adoption in ambulatory settings, regional reimbursement and guideline movement, and technology-driven changes in procedure throughput. Growth paths were adjusted only after the driver trends and the resulting revenue per procedure stayed consistent across regions and care settings.

Data Validation & Update Cycle

Validation is done in several passes so the market number does not depend on a single dataset or one strong assumption. Model outputs are checked against independent signals like procedure utilization trends, regional adoption commentary, and observed pricing ranges, and then anomalies are reviewed and corrected before sign-off.

If a major variance appears, we re-contact relevant respondents and re-check the assumption chain, starting from procedure pool and ending at revenue conversion. Reports are refreshed annually, with interim updates when material events occur such as regulatory actions, major pricing changes, or meaningful shifts in adoption. Before delivery, an analyst runs a fresh pass on key numbers and assumptions so clients receive an up-to-date view.

Mordor Intelligence's Smart Pills Diagnostics Market Estimate Compared With Other Published Estimates

Published market values for smart pills diagnostics can look far apart because the boundaries are drawn differently and the update timing is not the same. Differences usually come from what is counted as diagnostics, how components are bundled, and whether the estimate is updated after major price or adoption changes.

A big gap driver is refresh cadence and currency timing, since this market has a mix of higher-priced capsules and installed-base components that move at different speeds, and Mordor Intelligence ties ASP updates and validation checks to the latest regional price points and procedure signals before converting to USD for the stated year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.34 B (2026) | |

| Industry Publisher A | USD 0.78 B (2025) | Uses an earlier base year and a narrower view that leans toward capsule endoscopy value only, which can undercount recurring software, recorders, receivers, and accessory spending, and can also miss price resets that happened after the base year. |

| Global Publisher B | USD 1.40 B (2026) | Applies broader smart pills assumptions that may blend adjacent non-diagnostic uses, and it typically relies on smoother ASP progressions, which can overstate value if recorder and workstation replacement cycles slow in certain regions. |

The spread in the table is mostly explained by whether the estimate is capsule-only or includes the full diagnostic workflow, and by how quickly pricing and adoption inputs are refreshed. When scope and currency timing are kept consistent, and the procedure pool is cross-checked with component attach and refresh patterns, the final number becomes easier to trace and repeat.

Key Questions Answered in the Report

What is the current value of the smart pills diagnostics market?

The market is valued at USD 1.34 billion in 2026.

How fast will the market grow through 2031?

Revenue is projected to rise at a 10.38% CAGR, reaching USD 2.19 billion.

Which clinical indication is expanding the quickest?

Crohn’s disease leads with a 12.88% CAGR thanks to demand for repeat mucosal assessments.

Why are ambulatory surgery centers gaining share?

CMS payment incentives and 30%–50% lower procedure costs drive volume migration to outpatient settings.

Which region will post the fastest growth?

Asia-Pacific is set to grow at a 12.31% CAGR on the back of streamlined approvals and rising GI disease prevalence.

What technological advances shape next-generation capsules?

Ultra-low-power telemetry and cloud-based AI reading platforms extend battery life and cut radiologist review time.

Page last updated on: