Stable Isotope Labeled Compounds Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

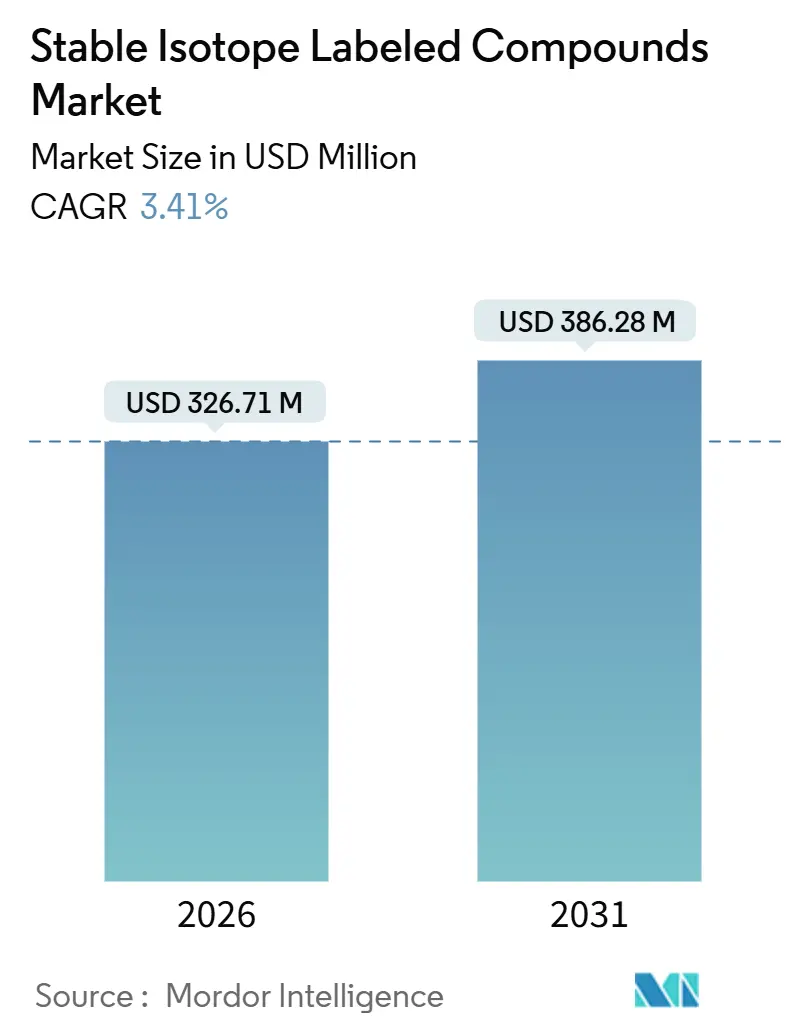

| Market Size (2026) | USD 326.71 Million |

| Market Size (2031) | USD 386.28 Million |

| Growth Rate (2026 - 2031) | 3.41% CAGR |

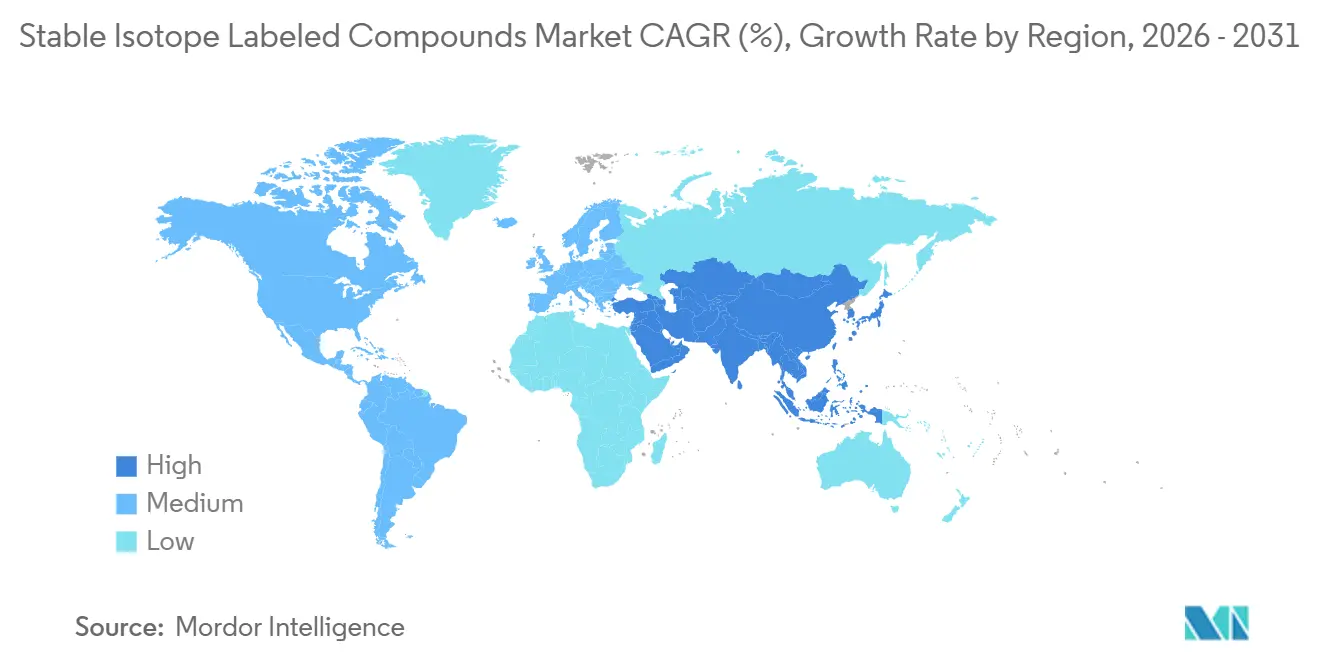

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

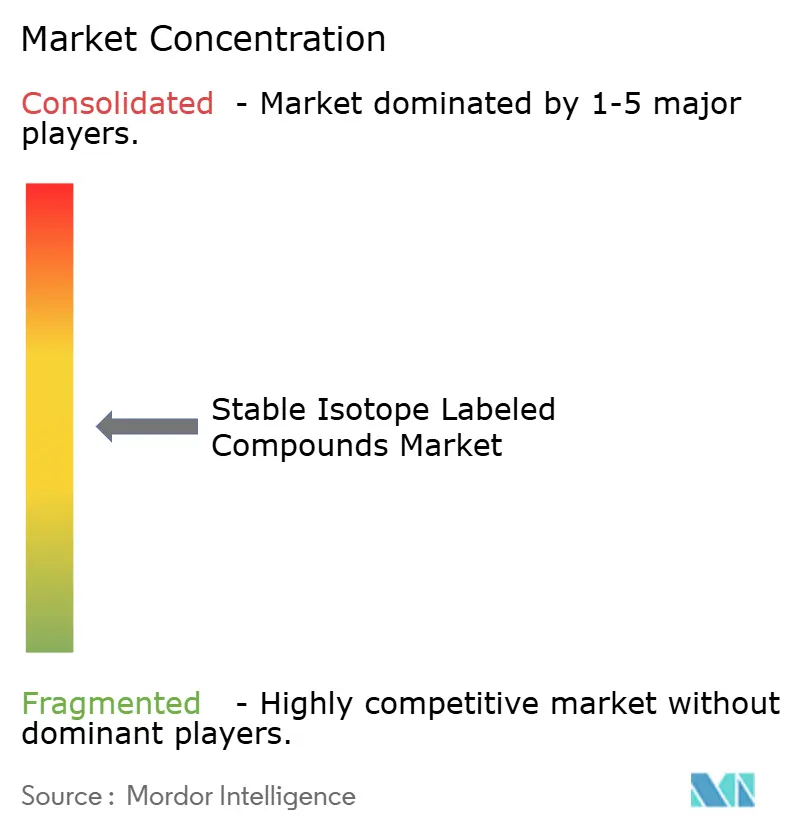

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stable Isotope Labeled Compounds Market Analysis by Mordor Intelligence

The Stable Isotope Labeled Compounds Market size is estimated at USD 326.71 million in 2026, and is expected to reach USD 386.28 million by 2031, at a CAGR of 3.41% during the forecast period (2026-2031).

The continued uptake of isotope-dilution mass spectrometry in drug development workflows, the establishment of fresh domestic enrichment capacity in the United States, and regulatory clarity on microdosing are the primary growth pillars. Pharmaceutical sponsors are outsourcing synthesis to Asian contract laboratories to contain costs, while suppliers face persistent bottlenecks for oxygen-18 water and nitrogen-15 precursors that restrain rapid capacity additions. The U.S. Food and Drug Administration finalized guidance on radiolabeled mass-balance studies in September 2024, reducing uncertainty for early-phase developers that rely on carbon-13 APIs. In parallel, the U.S. Department of Energy brought the Stable Isotope Production and Research Center online at Oak Ridge National Laboratory in 2025, restoring domestic enrichment capability for multiple heavy isotopes. Contract research and manufacturing organizations in China, India, and South Korea are scaling isotope-labeling suites to meet rising offshore demand. Still, export-control rules for dual-use isotopes continue to lengthen lead times and favor established suppliers with robust compliance programs.

Key Report Takeaways

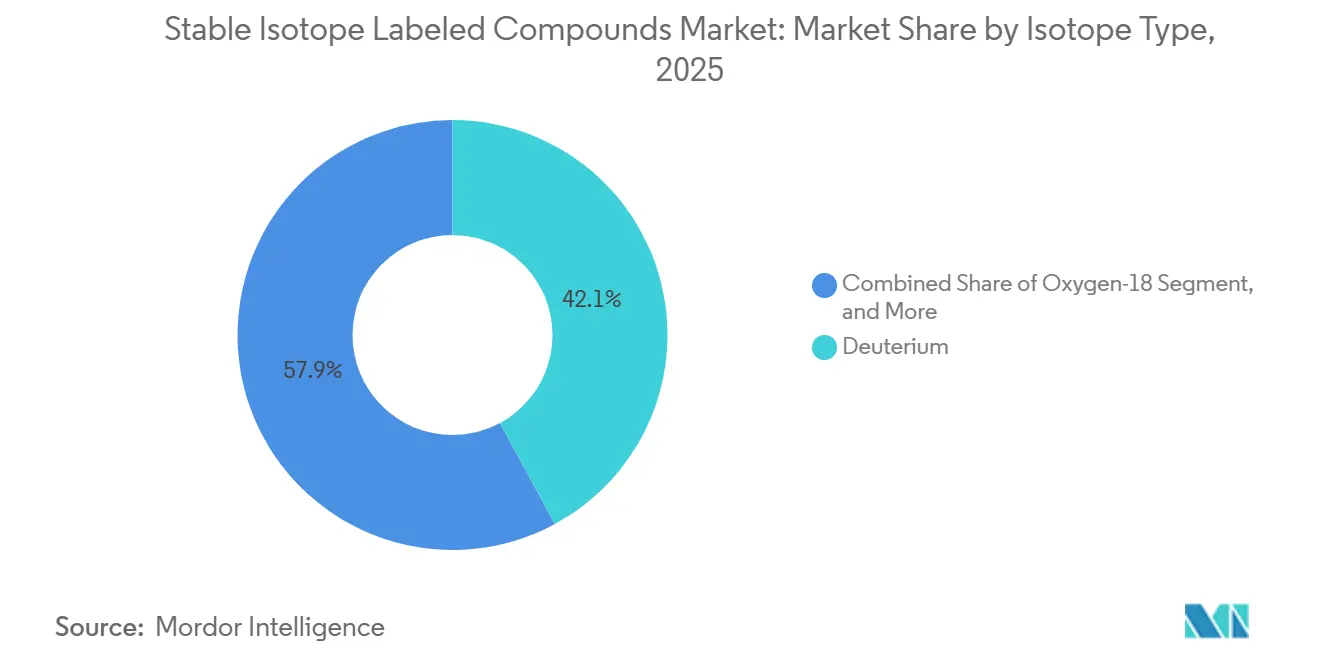

- By isotope type, deuterium compounds led with 42.11% revenue share in 2025; oxygen-18 materials are projected to expand at a 7.02% CAGR through 2031.

- By compound category, amino acids and peptides accounted for a 36.83% share of the stable isotope-labeled compounds market size in 2025. In contrast, active pharmaceutical ingredients are projected to advance at a 7.48% CAGR between 2026 and 2031.

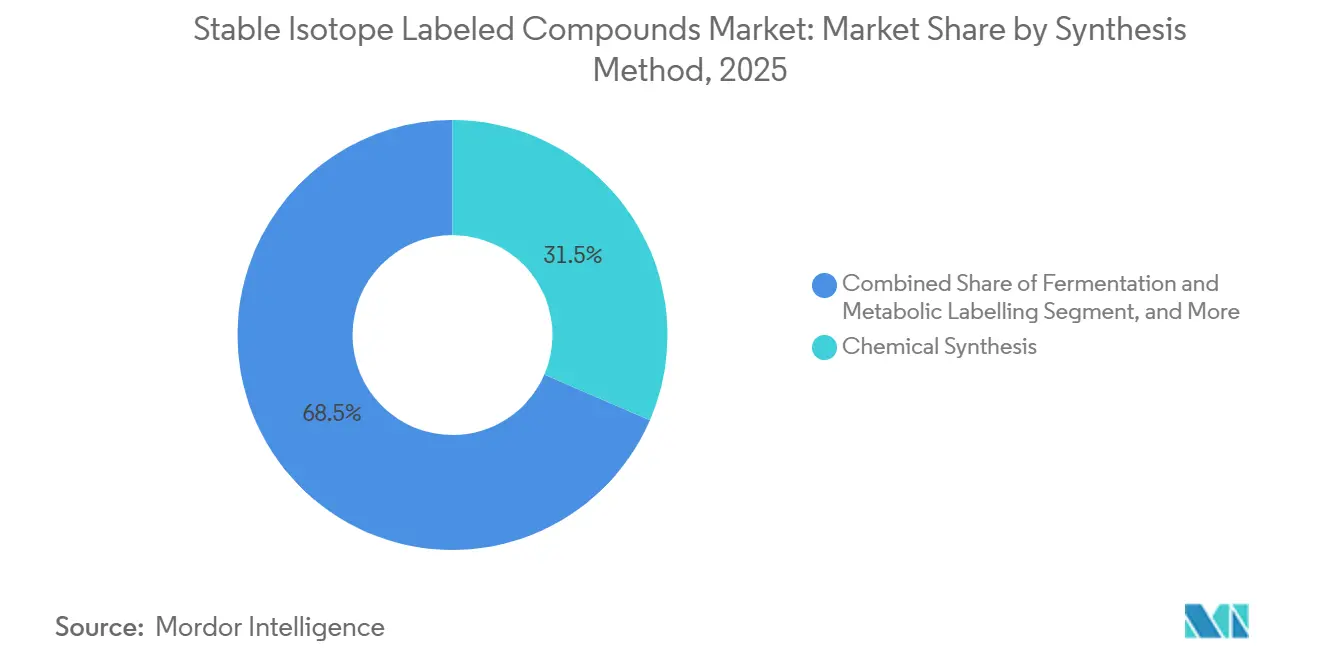

- By synthesis method, chemical synthesis accounted for 31.48% of the 2025 revenue; fermentation and metabolic labeling are forecast to post a 6.13% CAGR through 2031.

- By application, research use captured a 44.64% share in 2025, while clinical diagnostics is expected to expand at an 8.85% CAGR to 2031.

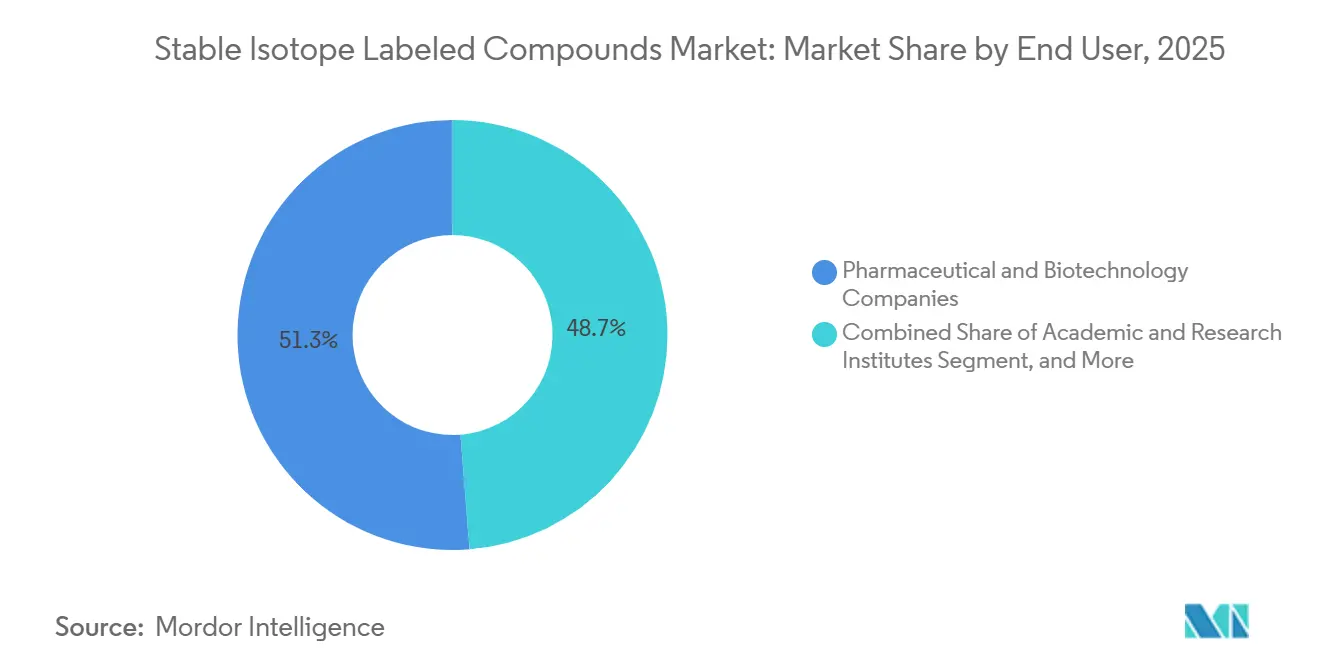

- By end-user, pharmaceutical and biotechnology companies commanded 51.26% share in 2025, whereas contract research and manufacturing organizations are growing at an 8.04% CAGR over the same period.

- By geography, North America retained a 43.38% stable isotope labeled compounds market share in 2025; Asia-Pacific is projected to grow at a 6.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Stable Isotope Labeled Compounds Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Quantitative Proteomics & Metabolomics | +0.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Expansion of SIL-based Companion Diagnostics | +0.7% | North America & EU, early adoption in Japan | Medium term (2-4 years) |

| Growing 13C-labelled APIs for Micro-Dosing Regulatory Studies | +0.5% | North America & EU regulatory zones | Short term (≤ 2 years) |

| Heightened Biopharma Outsourcing to Isotope CROs in Asia | +0.6% | APAC core, spill-over to Middle East | Long term (≥ 4 years) |

| Commercialisation of Deep-labeled Reference Standards for PFAS Tracing | +0.4% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Development of Green, Electro-Enzymatic Isotope-Exchange Synthesis | +0.3% | Global, led by Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Quantitative Proteomics & Metabolomics

Proteomics and metabolomics laboratories rely on stable isotope-labeled amino acids, peptides, and metabolites to push detection limits below the picomolar range in complex biological matrices. The National Institute of Standards and Technology introduced carbon-13 and nitrogen-15 labeled peptide reference materials in 2024, enabling laboratories to harmonize their calibration protocols.[1]National Institute of Standards and Technology, “Reference Materials for Mass Spectrometry,” nist.gov Academic cores and pharmaceutical discovery groups now require gram-scale supplies of uniformly labeled substrates, steering producers toward fermentation platforms that deliver higher isotopic purity than multi-step chemical routes. Fermentation runs last up to two weeks, constraining throughput when sponsors need custom compounds rapidly. Suppliers are therefore balancing batch-size economics against time-to-delivery commitments, a tension that is shaping capital-investment priorities for 2026 and beyond.

Expansion of SIL-based Companion Diagnostics

Regulators are approving isotope-dilution assays for an expanding roster of targeted therapies, valuing the method’s specificity at low nanogram-per-milliliter biomarker concentrations. The FDA cleared several liquid chromatography mass spectrometry tests for therapeutic drug monitoring in 2025, each anchored by deuterium or carbon-13 internal standards.[2]U.S. Food and Drug Administration, “Mass Balance Studies in Human ADME Trials,” fda.gov Diagnostic laboratories prefer these assays over immunoassays when metabolite interference poses a threat to accuracy. Japan’s Ministry of Health, Labour and Welfare shortened approval timelines for isotope-based in-vitro diagnostics in 2024, accelerating commercialization. Reimbursement reforms in the United States and parts of Europe further strengthen demand, offsetting cost sensitivities in emerging economies.

Growing 13C-Labelled APIs for Micro-Dosing Regulatory Studies

Micro-dosing protocols that administer sub-pharmacological doses of carbon-13 APIs reduce early-stage attrition and animal-use requirements. The FDA’s September 2024 mass-balance guidance explicitly endorses high-resolution LC-MS as an alternative to radiolabels. Roughly 15% of investigational new drug applications filed in North America and Europe during 2025 referenced carbon-13-enriched candidates, a sharp uptick from negligible usage three years earlier. Contract research organizations report lead times of six to nine months for custom carbon-13 synthesis, prompting pharmaceutical sponsors to pre-order labeled precursors during the lead optimization process. This shift is inflating order sizes and stabilizing revenue for isotope suppliers even as headline market growth remains modest.

Heightened Biopharma Outsourcing to Isotope CROs in Asia

Chinese, Indian, and South Korean contract laboratories expanded isotope labeling capacity in 2024 and 2025, attracted by double-digit growth in outsourced synthesis requests. WuXi AppTec added ISO 17034-accredited clean-room suites for peptide labeling, allowing overseas sponsors to save 30% to 40% on high-volume compounds.[3]WuXi AppTec, “Isotope Synthesis Services,” wuxiapptec.com Lower labor expenses offset freight costs; however, North American and European sponsors still reserve proprietary scaffolds for in-house synthesis to avoid intellectual property leakage. The outsourcing wave boosts the contract research and manufacturing organizations segment, which posts the strongest end-user CAGR in the forecast window. Export-control compliance remains a hurdle; shipments of deuterium oxide and nitrogen-15 often require individual licenses, which can add up to 12 weeks to delivery.

Restraints Impact Analysis of Stable Isotope Labeled Compounds Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost & Limited Availability of 18O-Water Feedstock | -0.4% | Global, acute in North America & Europe | Medium term (2-4 years) |

| Complex Export-Control Regulations for Dual-Use Isotopes | -0.3% | Global, most restrictive in North America & EU | Long term (≥ 4 years) |

| Supply-Chain Sensitivity to Enriched Uranium Tails for 15N | -0.3% | Global, concentrated supply in Netherlands & Russia | Medium term (2-4 years) |

| Analytical-Grade Isotope Scarcity for Emerging Ultra-High-Res MS | -0.2% | North America & Europe, emerging in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost & Limited Availability of 18O-Water Feedstock

Oxygen-18 water sells for more than USD 1,000 per gram at 97% enrichment, and global production capacity remains under 2,000 kilograms per year. Taiyo Nippon Sanso operates a 600-kilogram column in Japan that frequently runs at full tilt. Pharmaceutical and environmental laboratories often ration allocations or shift to deuterium-labeled surrogates when supplies are tight, thereby delaying studies. Building new cryogenic-distillation columns costs above USD 50 million and requires multi-year permitting, discouraging new entrants. Elevated feedstock prices, therefore, cap growth in cost-sensitive applications such as industrial quality control.

Complex Export-Control Regulations for Dual-Use Isotopes

Deuterium oxide, nitrogen-15, and select carbon-13 compounds are listed on the U.S. Commerce Control List and comparable schedules elsewhere, as they can support nuclear or defense activities. Export licenses add eight to 12 weeks to lead times and require extensive end-use documentation that smaller laboratories struggle to provide. Compliance costs favor incumbents with established licensing frameworks, reinforcing market concentration. Sponsors in emerging economies face additional hurdles when local customs authorities request redundant paperwork, which extends clearance times and effectively dampens demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Stable Isotope Labeled Compounds Market Segment Analysis

By Isotope Type:

Deuterium Anchors Revenue, Oxygen-18 Drives GrowthDeuterium compounds generated 42.11% of the 2025 revenue for the stable isotope-labeled compounds market, reflecting their routine use as internal standards in liquid chromatography-mass spectrometry and as solvents for nuclear magnetic resonance spectroscopy. Pharmaceutical laboratories consume kilograms of deuterium-labeled amino acids, peptides, and small molecules annually, benefitting from mature synthesis routes that deliver 98% purity at relatively low cost. Oxygen-18 labeled materials account for a smaller slice but are forecast to expand at a 7.02% CAGR through 2031, driven by the production of positron-emission tomography tracers and environmental tracing of per- and polyfluoroalkyl substances.

Feedstock availability governs the outlook. Deuterium oxide is plentiful, but oxygen-18 water remains supply-constrained, and nitrogen-15 relies on enrichment tails from uranium-processing facilities dominated by Urenco and Russian producers. Cambridge Isotope Laboratories doubled its carbon-13 capacity in October 2024, following the commissioning of the North Star plant, which insulates North American buyers from geopolitical disruptions. Suppliers are exploring membrane-based enrichment for oxygen-18, yet commercial scalability remains elusive.

By Compound Category:

Amino Acids Lead, APIs SurgeAmino acids and peptides captured 36.83% of 2025 revenue, reflecting widespread adoption in quantitative proteomics workflows that require uniformly labeled leucine, lysine, and arginine. Fermentation platforms offer incorporation rates above 99%, making them the method of choice for kilogram-scale production. Active pharmaceutical ingredients form the fastest-growing compound category, advancing at a 7.48% CAGR as micro-dosing gains regulatory acceptance. Roughly 15% of investigational new drug applications now specify carbon-13 APIs, catalyzing investment in modular synthesis lines capable of turning around custom molecules in four months.

Metabolites and lipids serve disease-profiling programs, and nitrogen-15 or carbon-13 nucleic acids underpin structural biology and RNA-therapeutics research. Solvents such as deuterated chloroform remain staples in nuclear magnetic resonance, but growth mirrors broader synthetic chemistry activity rather than life sciences innovation.

By Synthesis Method:

Chemical Routes Dominate, Fermentation Gains ShareChemical synthesis accounted for 31.48% of 2025 revenue, prized for its flexibility in positioning heavy isotopes within complex molecules. Catalytic exchange, halogen displacement, and multi-step organic transformations remain indispensable for the synthesis of bespoke scaffolds. Fermentation and metabolic labeling are projected to grow at 6.13% CAGR to 2031, driven by demand for uniformly labeled peptides and nucleotides used in proteomics and structural biology. Enzymatic or exchange methods occupy a niche today but promise greener credentials by cutting solvent waste and energy use, aligning with corporate sustainability goals.

Fermentation cycle times of seven to 14 days restrict throughput; however, ongoing work on continuous bioreactors could potentially compress these timelines. Chemical synthesis will likely retain dominance for oxygen-18 compounds, as biological systems rarely incorporate heavy oxygen efficiently. Cambridge Isotope Laboratories and IsoSciences have filed patents on continuous-flow enzymatic platforms that reduce reaction times from days to hours; however, large-scale Good Manufacturing Practice validation is still pending.

By Application:

Research Dominates, Clinical Diagnostics AcceleratesResearch applications held 44.64% of 2025 demand, with academic and pharmaceutical groups purchasing standards for pathway mapping and target validation. Clinical diagnostics is the fastest-growing segment at an 8.85% CAGR, buoyed by FDA clearances of isotope-dilution therapeutic-drug monitoring assays. Hospitals appreciate the method’s low interference and coefficient of variation, which is below 5%. Industrial and environmental testing remains relatively small but is poised to benefit from the Environmental Protection Agency’s 2024 update to its analytical methods for fluorinated contaminants.

Reimbursement tailwinds in the United States and Japan strengthen the economic case for isotope-based assays, while European laboratories leverage mutual-recognition agreements to reduce duplicate validations. Academic budgets remain under pressure, yet they are critical for testing emerging applications, such as single-cell proteomics.

By End-User:

Pharma Leads, CROs Expand RapidlyPharmaceutical and biotechnology companies represented 51.26% of 2025 revenue, relying on stable isotope-labeled compounds for metabolism, bioavailability, and biomarker studies. Outsourcing momentum lifts contract research and manufacturing organizations, which post an 8.04% CAGR as sponsors divest in-house labeling functions. ISO 17034 facilities in China and India now attract routine projects for high-volume compounds, while proprietary molecules and export-controlled isotopes stay within sponsor walls.

Academic and research institutes remain early adopters of novel labeling strategies, although constrained budgets limit volume. Hospitals and diagnostic centers purchase smaller batches but benefit from expanded assay menus reimbursed by insurance payers.

Geography Analysis

North America Stable Isotope Labeled Compounds Market

North America held 43.38% share of 2025 revenue, anchored by pharmaceutical headquarters, leading mass-spectrometry instrument vendors, and clear regulatory frameworks. The Oak Ridge National Laboratory facility, commissioned in 2025, restored domestic enrichment capabilities for carbon-13, nitrogen-15, and oxygen-18, thereby reducing exposure to Russian and Chinese suppliers. Canada’s National Research Council supplies regional demand, while Mexico adopts isotope-dilution for bioequivalence trials mandated by COFEPRIS. Although sponsors are increasingly outsourcing synthesis to Asia, North America remains the epicenter for method development and standards setting.

APAC Stable Isotope Labeled Compounds Market

Asia-Pacific is projected to grow at a 6.04% CAGR through 2031. WuXi AppTec and other regional CROs expanded isotope-synthesis suites in 2024 and 2025, capturing demand from cost-sensitive sponsors. Japan’s Taiyo Nippon Sanso operates the world’s largest commercial oxygen-18 facility and is evaluating capacity expansions to alleviate chronic shortages. India harmonizes its bioequivalence guidelines with those of the International Council for Harmonisation, stimulating domestic purchases. Export-control approvals remain a bottleneck, but incremental licensing reforms in South Korea and Australia could reduce friction by 2027.

EMEA and South America Stable Isotope Labeled Compounds Market

Europe maintained a mid-20s percentage share in 2025, with Germany, the United Kingdom, and France leading the way in consumption. Urenco Stable Isotopes supplies nitrogen-15 from its Dutch plant, feeding proteomics laboratories across the continent. The European Medicines Agency updated bioanalytical guidelines in 2024, aligning with FDA standards and facilitating cross-jurisdiction submissions. The Middle East and Africa, as well as South America, remain smaller markets; however, Gulf Cooperation Council nations invest in mass-spectrometry diagnostics, and Brazilian pharmaceutical hubs apply isotope dilution to meet export market quality requirements.

Regulatory Landscape

Regulatory expectations for stable isotope labeled compounds are increasingly shaped by harmonized bioanalytical method validation requirements and clinical study governance. The ICH M10 guideline (implemented through FDA and EMA frameworks) reinforces the need for well-characterized internal standards, which increases demand for documented identity, isotopic purity, and stability, supported by Certificates of Analysis where stable isotope labeled internal standards are used in mass spectrometry methods.

On the clinical development side, FDA guidance and policy on when studies can be conducted without an IND (including references commonly used by institutional human-subjects offices) affects how sponsors position stable (non-radioactive) tracers in basic research versus regulated clinical protocols. At the same time, export-control regimes for dual-use isotopes (notably deuterium oxide, nitrogen-15, and select carbon-13 compounds) remain a compliance anchor that can extend cross-border shipment timelines and favor suppliers with established licensing and end-use documentation processes.

Competitive Landscape

The stable isotope labeled compounds market features moderate concentration. The top five suppliers, Cambridge Isotope Laboratories, Merck KGaA, Thermo Fisher Scientific, Urenco Stable Isotopes, and Toronto Research Chemicals, account for a significant share of the global revenue. Barriers to entry include capital costs exceeding USD 50 million for enrichment infrastructure and stringent export-control licensing requirements. Smaller firms, such as Alsachim, IsoSciences, and Omicron Biochemicals, differentiate themselves through custom synthesis and technical support rather than price competition.

Cambridge Isotope Laboratories’ North Star carbon-13 line, commissioned in October 2024, doubled capacity and reduced dependence on Russian and Chinese feedstock. Suppliers are racing to patent electro-enzymatic deuteration, a technology that reduces solvent waste and energy use, aligning with pharmaceutical sustainability goals. Oxygen-18 scarcity offers pricing power to producers with distillation columns, while fermentation-based labeling of complex biologics remains a white-space opportunity. Acquisition activity is likely as incumbents seek feedstock security and product-portfolio breadth, a pattern echoed by Merck KGaA’s historical purchases of niche isotope firms.

Stable Isotope Labeled Compounds Industry Leaders

PerkinElmer Inc

Merck KGaA

Cambridge Isotope Laboratories, Inc.

Medical Isotopes, Inc.

Rosatom

- *Disclaimer: Major Players sorted in no particular order

Stable Isotope Labeled Compounds Market Companies Covered in this Report

- Alsachim

- Cambridge Isotope Laboratories

- CDN Isotopes

- Euriso-Top

- Isoflex

- IsoSciences

- JSC Isotope

- LGC Standards

- Medical Isotopes

- Merck

- Omicron Biochemicals

- PerkinElmer

- Rotem Industries

- Sercon Hylab

- Taiwan Advance Nanotech

- Taiyo Nippon Sanso

- TCI Chemicals

- Thermo Fisher Scientific

- Toronto Research Chemicals

- Trace Sciences International

- Urenco Stable Isotopes

- Zeochem

Market Opportunities and Future Outlook

Clinical mass spectrometry provides a clear whitespace for suppliers that can combine stable isotope labeled internal standards with validation-ready documentation and consistent lot performance, matching regulated laboratory expectations around accuracy, precision, and limits of quantification under frameworks such as CLIA. Pull-through is supported as regulators clear and laboratories adopt isotope-dilution LC-MS assays for therapeutic drug monitoring, which increases demand for deuterium and carbon-13 standards and enables product-extension opportunities in higher-complexity panels, including metabolites, lipids, and peptide markers.

Method innovation is also broadening the addressable product mix beyond routine reagents. In 2026, the publication of updated technical references on isotopically labeled compounds and stable isotope tracing, along with peer-reviewed reports of new labeled syntheses (for example, deuterated norepinephrine routes), points to continued expansion of labeling chemistry into more complex and clinically relevant molecules. Suppliers with constrained feedstocks have near-term differentiation options through circularity and yield improvements, such as recovery and re-enrichment programs, and through GMP-grade offerings that support IND-enabled clinical research workflows where stable isotopes substitute for radiolabels in certain mass-balance and microdosing study designs.

Recent Industry Developments in Stable Isotope Labeled Compounds Market

- April 2026: Cambridge Isotope Laboratories, Inc. announced that its fully owned subsidiary Eurisotop began serving as a direct supplier of CIL Environmental Standards across Europe, effective April 1, 2026. The shift tightens regional fulfillment and customer support for regulated environmental and analytical workflows that depend on stable isotope labeled standards.

- October 2025: Cambridge Isotope Laboratories, Inc. launched ISOAPI-D, a brand of deuterated intermediates positioned for API synthesis supply chains. The release expands CILs portfolio further upstream into deuterated building blocks, supporting sponsors that use labeled intermediates for microdosing, ADME, and quantitative LC-MS studies.

- December 2024: Cambridge Isotope Laboratories, Inc. implemented a benzene-d6 recovery and re-enrichment program aimed at addressing cost and supply constraints for OLED display manufacturing customers. The circularity focus helps stabilize availability of scarce isotope materials and reduce reliance on fresh enrichment throughput.

Stable Isotope Labeled Compounds Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenue from stable isotope labeled compounds sold as reagents, standards, or intermediates, where a non-radioactive isotope is incorporated into a molecule for tracing and quantification in lab workflows.

Scope exclusions: it excludes radioactive isotopes, unlabeled isotope gases sold as feedstock, and standalone labeling services when a labeled compound is not delivered.

Segments Covered in This Report

- By Isotope Type

- Deuterium

- Carbon-13

- Nitrogen-15

- Oxygen-18

- Others

- By Compound Category

- Amino Acids & Peptides

- Metabolites & Lipids

- Active Pharmaceutical Ingredients

- Nucleic Acids

- Solvents & Reagents

- By Synthesis Method

- Chemical Synthesis

- Fermentation & Metabolic Labelling

- Enzymatic / Exchange

- By Application

- Research (Proteomics, Metabolomics, Flux Analysis)

- Clinical Diagnostics

- Industrial & Environmental Testing

- Other Applications

- By End-User

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Hospitals & Diagnostic Centers

- Contract Research & Manufacturing Organisations

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by setting the demand context for labeled materials and the labs that use them, then it narrows down to what is actually traded and priced as labeled compounds. We refer to public sources such as the US FDA and NIH pages on bioanalytical methods and clinical research, the US International Trade Commission for trade classifications, Eurostat for import-export statistics, and OECD indicators to track R&D intensity over time.

On the supply side, annual reports, investor decks, and product catalogs are reviewed to understand portfolio breadth, typical pack sizes, and where custom synthesis is positioned versus off-the-shelf standards. We also use paid subscriptions for company financials and intelligence, patent databases, and shipment-level import-export records, mainly to check whether activity is moving in the same direction as the modeled demand rather than to copy a published market number. The sources listed here are illustrative, and multiple other public documents and datasets were reviewed during data collection and clarification.

Primary Interviews and Surveys

Primary work relies on interviews and structured surveys with people across custom synthesis, catalog reagents, CRO and CDMO procurement, and academic lab purchasing. Pricing and mix can change quickly by isotope and purity, so respondent input was used to refine which products fit the market definition and to confirm the portion of revenue that should be counted. Since this is a global market, views were balanced across major consumption hubs and manufacturing centers, and any unclear assumptions from desk research were taken back to experts for confirmation before totals were finalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 16% | APAC: 48% |

| Mid tier: 51% | Functional/Unit leaders: 24% | EMEA: 29% |

| Smaller Players: 19% | Managers: 60% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where R&D and clinical diagnostics activity is translated into a practical demand pool for labeled standards and tracers, then converted into value using observed pricing ranges. To keep the model grounded, we cross-check outputs with selective bottom-up approximations such as sampled catalog SKU pricing multiplied by estimated volumes, channel checks with distributors, and a light roll-up of custom synthesis revenue signals where disclosure is available.

A few inputs that matter most in this market are the volume of bioanalytical testing and pharmacokinetic studies, growth in proteomics and metabolomics sample runs, clinical diagnostics test adoption where isotope standards are used for quantitation, isotope mix by label type (for example deuterium versus carbon-13), and typical purity and enrichment requirements that affect ASPs. Forecasts use scenario analysis tied to expected R&D funding direction, clinical trial intensity, and lab instrument utilization, then the growth path is calibrated through expert feedback so short-term spikes are not overstated. When bottom-up indicators have gaps, we use conservative interpolation based on nearby product families and end-user mix, and these assumptions are documented and re-tested during validation.

Data Validation & Update Cycle

Validation is done by comparing modeled totals against independent signals such as trade movement for relevant chemical categories, trends in research spending, and the observed pace of method adoption in bioanalysis and diagnostics. If a country or segment result looks out of line, the inputs are rechecked, the math is reviewed by another analyst, and primary respondents are re-contacted when the variance cannot be explained by mix or pricing.

Each report is refreshed annually, and interim updates are triggered when there are material events such as major capacity additions, regulation changes affecting diagnostic workflows, or sudden shifts in research funding. Before delivery, we run a final pass to ensure the latest public updates and expert feedback are reflected in the numbers provided to clients.

Mordor Intelligence's Stable Isotope Labeled Compounds Market Size Compared Against Other Published Estimates

Published market values for stable isotope labeled compounds can differ widely because the scope can sound similar while counted items and the timing of price assumptions differ. Variation also comes from how each publisher treats custom synthesis versus catalog sales, and whether the figure is anchored to lab activity signals or to broader chemical market proxies.

Radioisotope labeled tracers sit outside Mordor Intelligence's scope, which can make some other figures look larger when nuclear medicine related items are blended into the same total. The spread also increases when an estimate uses a higher-growth scenario for clinical diagnostics expansion, applies stronger ASP escalation for high enrichment grades, or converts currencies using a different reference period in volatile years.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 326.71 M (2026) | |

| Global Consultancy A | USD 341.67 M (2025) | Uses a different base year and a longer forecast window, and it can embed higher assumed growth for clinical diagnostics adoption, which lifts the near-term starting point when back-cast assumptions are not fully shown. |

| Industry Publisher B | USD 291.82 M (2023) | Anchors the base year earlier and may not fully capture later pricing and mix shifts in high-purity standards, which can hold the starting value down even if long-run growth is similar. |

Across the three figures, most of the variance can be explained by timing, what gets counted alongside labeled compounds, and how ASP and mix are progressed from the base year. By keeping inputs tied to observable lab activity indicators and then rechecking them with supplier and buyer feedback, we arrive at a figure that is easier to trace and update when the market changes.

Key Questions Answered in the Report

How large is the stable isotope labeled compounds market in 2026?

It reached USD 326.71 million in 2026 and is projected to climb to USD 386.28 million by 2031.

Which isotope type holds the largest share?

Deuterium compounds led with 42.11% revenue share in 2025.

What is driving demand for carbon-13 APIs?

FDA guidance in 2024 validated micro-dosing protocols that rely on carbon-13, prompting sponsors to specify labeled APIs in more investigational applications.

Why is oxygen-18 supply tight?

Global capacity is under 2,000 kilograms per year, with Taiyo Nippon Sanso operating the largest commercial column, keeping prices above USD 1,000 per gram.

Which region is growing fastest?

Asia-Pacific is forecast to post a 6.04% CAGR through 2031, powered by capacity build-outs in China, India, and South Korea.

Page last updated on: