Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

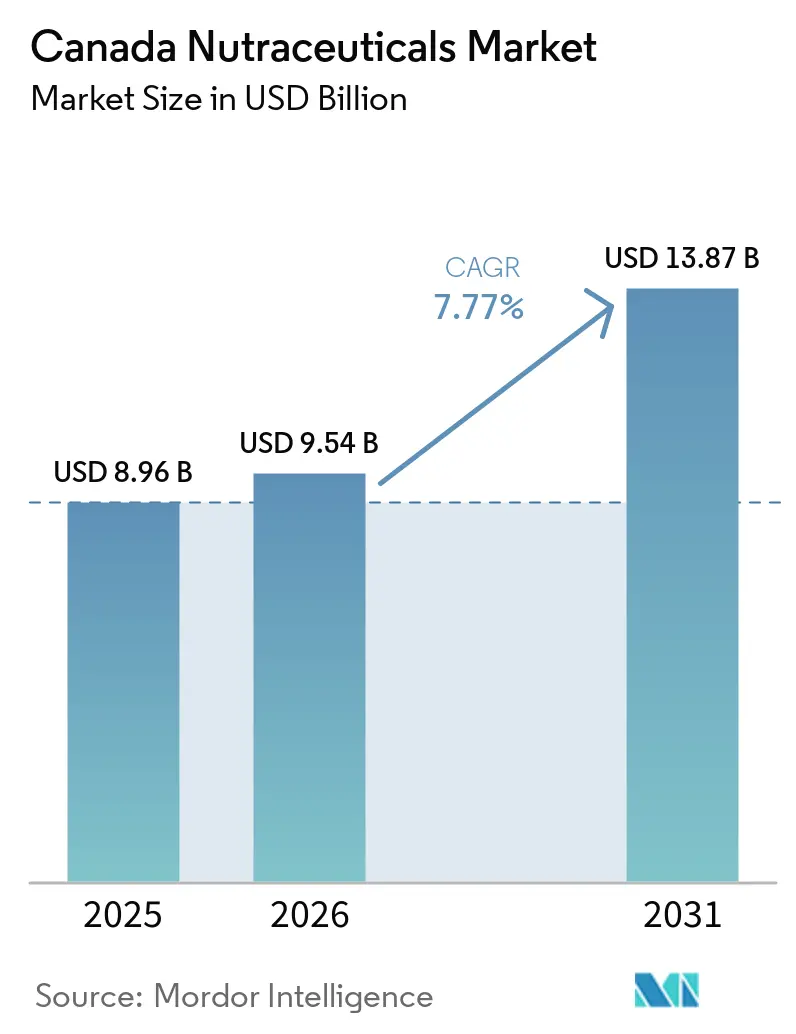

| Base Year Market Size (2025) | USD 8.96 Billion |

| Market Size (2026) | USD 9.54 Billion |

| Market Size (2031) | USD 13.87 Billion |

| Growth Rate (2026 - 2031) | 7.77% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Nutraceuticals Market Analysis by Mordor Intelligence

The Canada natural health products market size is projected to grow from USD 8.96 billion in 2025, and USD 9.54 billion in 2026 to USD 13.87 billion by 2031, registering a CAGR of 7.77% during the forecast period of 2026-2031. This growth is driven by a shift from symptom-focused treatment to preventive self-care, with consumers increasingly adopting functional foods, beverages, and dietary supplements to manage metabolic risks and enhance cognitive health. Companies that provide peer-reviewed evidence to support product claims and obtain Health Canada Natural Product Numbers (NPNs) are leveraging regulatory compliance to build consumer trust. Additionally, direct-to-consumer models are streamlining supply chains and improving the price-value proposition across the market. The market is also witnessing a growing preference for natural, plant-based, and sustainable nutraceuticals, reflecting consumers' environmental and health-conscious values. Health Canada's stringent regulatory frameworks further ensure product safety, bolstering consumer confidence and facilitating market growth. Other factors contributing to the market's expansion include the rise of digital shopping, innovations in products such as microencapsulated probiotics and plant-based omega-3s, and increased industry consolidation, particularly with the entry of pharmaceutical companies.

Key Report Takeaways

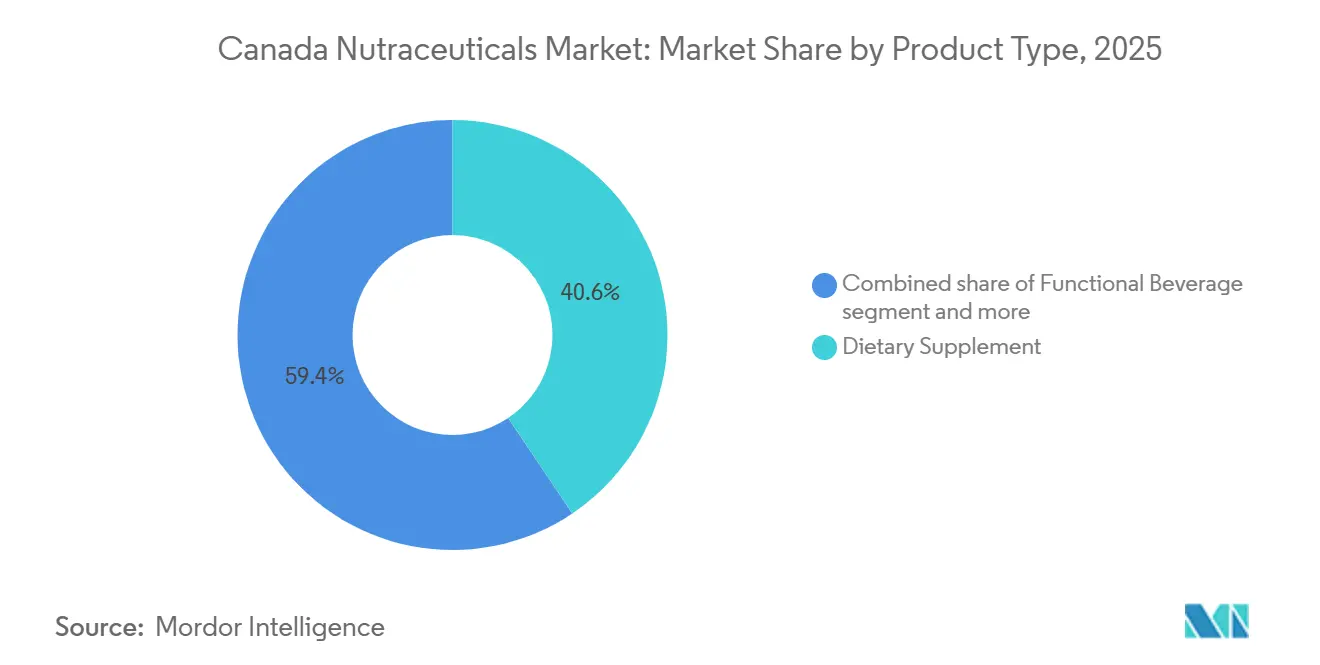

- By product type, the dietary supplement segment held 40.59% of revenue in 2025, while the functional beverage segment is forecast to post the fastest 8.59% CAGR through 2031.

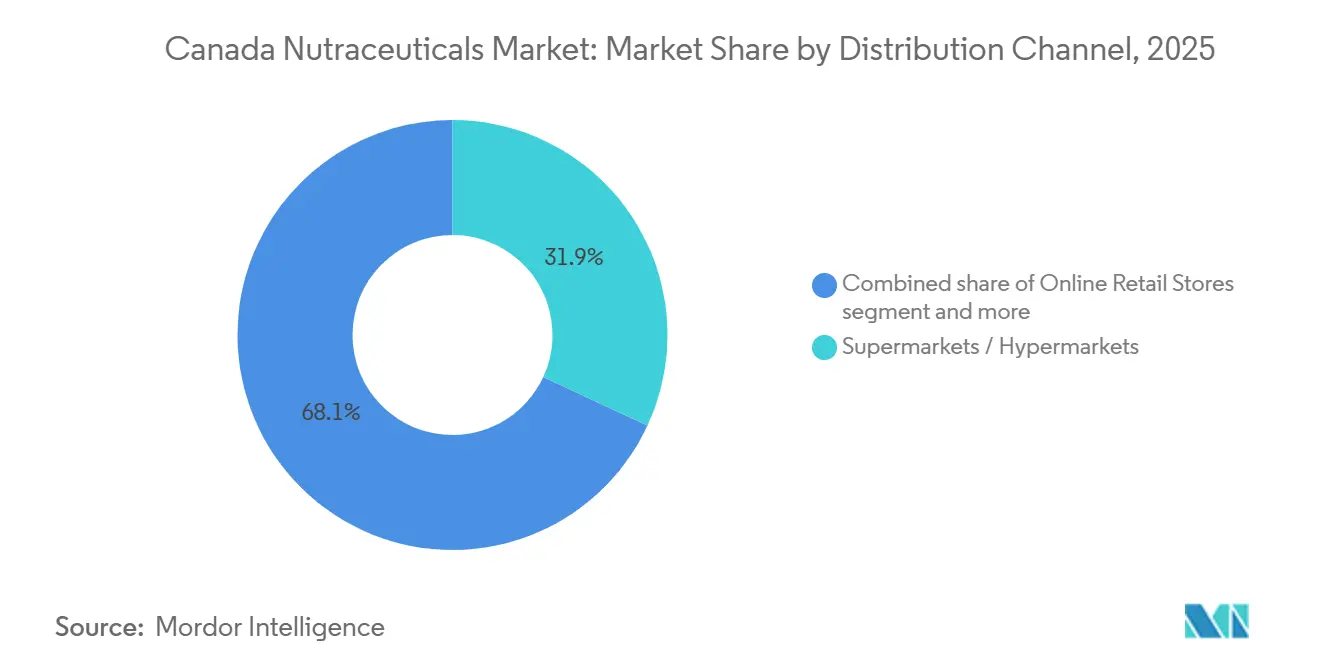

- By distribution channel, supermarkets/hypermarkets accounted for 31.92% of sales in 2025, whereas online retail stores are set to expand at a 9.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Nutraceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population seeking preventative health solutions | +1.4% | National, with concentration in British Columbia, Ontario, Quebec | Long term (≥ 4 years) |

| Rising incidence of lifestyle diseases (obesity, diabetes) | +1.6% | National, elevated in Atlantic provinces and rural communities | Medium term (2-4 years) |

| Preference for natural and plant-based products | +1.2% | National, urban centers (Toronto, Vancouver, Montreal) leading adoption | Medium term (2-4 years) |

| Expansion of functional foods and beverages | +1.3% | National, with retail penetration highest in Ontario and Alberta | Short term (≤ 2 years) |

| Government regulatory support fostering trust | +0.9% | National, Health Canada NNHPD framework applies uniformly | Long term (≥ 4 years) |

| Shift toward science-based wellness products | +1.1% | National, early adoption in metropolitan areas with higher education levels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging population seeking preventative health solutions

The increasing aging population in Canada is a significant driver of the nutraceuticals market, as older adults actively seek solutions to maintain health, prevent chronic diseases, and support overall wellness. According to Statistics Canada, approximately 7.6 million Canadians were aged 65 and older as of July 1, 2023, representing nearly one-fifth (18.9%) of the total population. By 2030, seniors are projected to account for 21.4% to 23.4% of the population [1]Source: Statistics Canada, "The older people are all right", statcan.gc.ca. Unlike previous generations, which viewed aging as an inevitable decline, today's seniors adopt preventive measures, such as omega-3 fatty acids for brain health, collagen peptides for mobility, and vitamin D3 for bone density, well before symptoms arise. This proactive approach is further supported by provincial healthcare systems, with regions like British Columbia and Quebec offering subsidies for nutrition counseling and chronic disease prevention programs. The transition from reactive treatment to preventative nutrition extends product lifecycles, as consumers adhere to supplement routines over decades rather than using them sporadically. This shift fundamentally enhances revenue predictability for manufacturers and retailers.

Rising incidence of lifestyle diseases (obesity, diabetes)

The increasing prevalence of lifestyle diseases is a key factor driving the growth of the Canadian nutraceuticals market. In Canada, approximately 44% of adults have at least one chronic condition, which accounts for 67% of all deaths [2]Source: Canadian Public Health Association, "Chronic Disease and Public Health in Canada", cpha.ca. This has led to heightened consumer awareness of preventive health, boosting demand for nutraceutical products aimed at managing risk factors and promoting overall wellness. Products targeting heart health, metabolic balance, and weight management are in high demand as individuals seek to reduce the long-term impacts of chronic diseases. For instance, in 2024, about 12% of adults in Newfoundland and Labrador were diagnosed with diabetes, while in Ontario, approximately 9% of adults were living with the condition [3]Source: Statistics Canada, "Health indicator statistics, annual estimates ", statcan.gc.ca. The rising incidence of Type 2 diabetes, particularly among working-age populations, is driving demand for blood sugar management formulations. Ingredients such as berberine, chromium picolinate, and cinnamon extract, which mimic pharmaceutical mechanisms without requiring prescriptions, are gaining popularity. This trend favors research and development-focused companies capable of innovation, reinforcing a shift toward science-backed, specialized nutraceutical products that address multiple lifestyle-related health concerns.

Preference for natural and plant-based products

Consumer preference for natural, plant-based, and clean-label products is a key driver of the Canadian nutraceuticals market. Health-conscious individuals increasingly seek supplements made from botanical sources, organic ingredients, and minimally processed formulations, which are perceived as safer and more sustainable. This trend is further supported by growing awareness of ingredient transparency, ethical sourcing, and environmental impact, influencing purchasing decisions across various age groups. As of 2024, approximately 2.3 million Canadians identify as vegetarian, and 850,000 as vegan [4]Source: The Vegan Society, "Worldwide growth of veganism", vegansociety.com. This substantial demographic fuels demand for plant-based nutraceuticals, such as protein powders, fortified beverages, herbal extracts, and vitamin supplements free from animal-derived ingredients. Brands addressing these dietary preferences are leveraging opportunities to develop vegan-certified, allergen-free, and sustainably sourced products that align with both lifestyle choices and ethical values.

Expansion of functional foods and beverages

The growth of functional foods and beverages is a significant factor influencing the Canadian nutraceuticals market, driven by changing consumer preferences for convenience, effectiveness, and multi-functional solutions. Functional beverages are gaining traction by offering hydration, electrolytes, probiotics, and cognitive enhancers in formats that align with busy, on-the-go lifestyles. These products leverage "functional stacking," combining ingredients such as B vitamins for energy, electrolytes for hydration, and adaptogens for stress relief in a single serving, reducing the reliance on multiple supplements and streamlining daily wellness routines. This segment also provides a notable profit opportunity for manufacturers. Ready-to-drink formats typically command higher retail prices per serving compared to traditional powdered or pill-based alternatives, motivating consumer packaged goods (CPG) companies to reformulate existing products into liquid delivery systems. By addressing diverse health needs in a single, convenient format, functional foods and beverages not only boost sales but also foster brand loyalty and repeat purchases. As consumers increasingly value efficiency, personalization, and holistic health solutions, the functional foods and beverages category is expected to remain a key driver of growth in the Canadian nutraceuticals market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent NHP evidence and label-claim requirements | -0.8% | National, uniform Health Canada NNHPD enforcement | Long term (≥ 4 years) |

| High cost and complexity of product development | -0.6% | National, disproportionately affects small and mid-sized manufacturers | Medium term (2-4 years) |

| Lack of extensive clinical evidence | -0.5% | National, particularly for emerging botanicals and novel formulations | Medium term (2-4 years) |

| Consumer misinformation and overuse risks | -0.4% | National, amplified by social media and influencer marketing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent NHP evidence and label-claim requirements

Health Canada's NNHPD requires manufacturers to provide clinical evidence, safety data, and quality assurance documentation to support every health claim before issuing Natural Product Numbers (NPNs). This process can take 18 to 36 months and cost over CAD 500,000 (USD 368,000) per product. This regulatory framework poses challenges for innovation, as companies are reluctant to invest in new botanicals or synergistic formulations without assurance of approval. As a result, product portfolios often focus on line extensions of established ingredients, such as vitamin D3, omega-3, and probiotics, rather than introducing novel therapies. Additionally, the requirement for bilingual labeling (English and French) and Good Manufacturing Practices (GMP) certification increases operational complexity, particularly for foreign companies unfamiliar with Canada's regulatory environment. While these measures safeguard consumers from unsafe or fraudulent products, they also delay time-to-market, enabling U.S. competitors to release similar formulations months earlier in less regulated markets.

High cost and complexity of product development

Developing a clinically validated natural health product in Canada necessitates expertise across multiple disciplines, including formulators, toxicologists, regulatory consultants, and clinical researchers. Small and mid-sized manufacturers often lack the resources to conduct randomized controlled trials or manage Health Canada's pre-market review process. This limitation forces them to either license formulations from larger companies, which can be costly and limit their control over the product, or abandon innovation efforts altogether, stifling growth and competitiveness. The process becomes even more challenging for combination products, such as functional foods that incorporate probiotics, prebiotics, and botanicals. These products require each ingredient to undergo individual safety assessments, including evaluations for potential interactions and cumulative effects, adding layers of complexity to the development and approval process.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Beverages Outpace Traditional Supplements

Dietary supplements accounted for 40.59% of the market share in 2025, driven by established consumer habits surrounding daily multivitamins, omega-3 capsules, and mineral tablets. However, functional beverages are projected to grow at a compound annual growth rate (CAGR) of 8.59% through 2031, marking the fastest growth among product types. This growth is attributed to ready-to-drink formats that address pill fatigue and offer multi-benefit formulations in single servings. Functional foods, which include cereals, bakery products, dairy, and snacks, occupy a middle ground by providing fortification, such as added fiber, protein, and vitamins, within familiar meal contexts. Cereal manufacturers are reformulating traditional products to reduce sugar content and incorporate plant-based proteins, aligning with front-of-package nutrition labeling regulations that highlight high sodium and saturated fat levels.

The bakery and confectionery segments face challenges from clean-label requirements, as consumers increasingly reject artificial preservatives and demand recognizable ingredients. These reformulation efforts often increase costs without guaranteeing volume growth. Snacks, including protein bars, nut mixes, and fortified chips, benefit from their portability and portion control, appealing to consumers with busy lifestyles who often skip traditional meals. While dietary supplements remain the largest segment, they face commoditization pressures. Vitamins and minerals primarily compete on price, whereas botanicals, enzymes, and fatty acids command higher premiums due to clinical validation and proprietary extraction processes.

By Distribution Channel: Online Retail Transforms Market Access

Supermarket/hypermarkets accounted for 31.92% of the distribution share in 2025, supported by features such as dedicated health and wellness aisles, in-store dietitians, and private-label brands priced 20-30% lower than national manufacturers. Online retail stores are projected to grow at a CAGR of 9.11% through 2031. This growth is fueled by subscription models ensuring recurring revenue, personalized recommendation engines that promote complementary products, and direct-to-consumer brands offering clinical-grade formulations at mid-market prices by bypassing retail markups. Major players like Amazon Canada, Shoppers Drug Mart's online platform, and Walmart.ca dominate the digital market. However, smaller brands such as Genuine Health and Prairie Naturals utilize Shopify storefronts and influencer partnerships to attract millennial and Gen Z consumers who are often skeptical of mass-market retail options.

Drug stores and pharmacies play a unique role by positioning natural health products alongside over-the-counter medications and prescription services. This approach enhances credibility and allows for pharmacist consultations, which encourage trials among first-time users. The channel benefits from Health Canada's regulatory framework, as pharmacists prioritize stocking NPN-certified products and provide guidance on interactions with prescription drugs, effectively serving as gatekeepers for evidence-based formulations. Although convenience stores account for a smaller market share, they are essential for impulse purchases. Products such as energy drinks, electrolyte beverages, and single-serve protein shakes are particularly popular among shift workers and travelers who value accessibility over price.

Geography Analysis

Ontario, British Columbia, and Quebec together account for over 60% of the national supplement expenditure, driven by their population density and higher disposable incomes. Urban centers such as Toronto and Vancouver demonstrate strong demand for plant-based, non-GMO, and scientifically formulated products, reflecting their cosmopolitan consumer preferences. The Prairie provinces are experiencing faster unit growth in functional beverages, supported by distribution efficiencies linked to established agricultural supply chains.

Atlantic Canada reports the highest obesity rates in the country, driving increased consumption of metabolic-support powders and fortified meal replacements, primarily distributed through pharmacies and grocery stores. In rural areas, there is a higher-than-average preference for ready-to-drink formats, addressing challenges related to limited access to fresh food. In Nunavut and the Northwest Territories, logistical challenges result in higher landed costs, reducing the variety of available SKUs and encouraging a preference for shelf-stable multivitamins over refrigerated probiotics.

Retailers are increasingly customizing end-cap displays to align with provincial health priorities, such as cardiovascular health in Quebec and joint health in Saskatchewan. Digital-first brands are leveraging geo-targeted messaging down to the FSA postal code level to reach specific micro-clusters. Provincial government wellness incentives also influence adoption trends; for example, British Columbia’s subsidy for nutrition counseling is associated with increased adherence to condition-specific supplements. These factors collectively highlight the regionally diverse growth trajectory of the natural health products market in Canada.

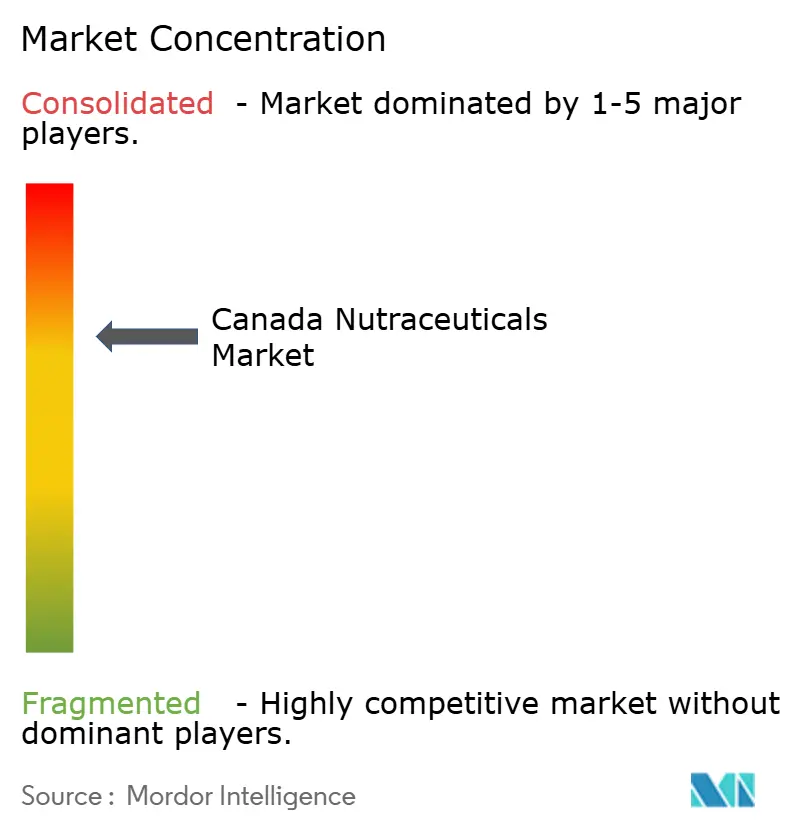

Competitive Landscape

The Canadian natural health products market exhibits moderate consolidation. Multinational consumer packaged goods (CPG) companies such as PepsiCo, Nestlé, and Danone dominate high-volume functional beverage categories, leveraging extensive advertising capabilities and nationwide distribution networks. Meanwhile, domestic players like Jamieson Wellness, Natural Factors, and Genuine Health have built strong consumer trust by using locally sourced ingredients and securing Natural Product Number (NPN) certifications for clinical validation, allowing them to position their products at premium price points.

Market strategies are divided into two primary approaches. Established companies are upgrading legacy stock-keeping units (SKUs) by incorporating ingredients like probiotics or omega-3s to enhance profit margins. On the other hand, emerging brands are focusing on direct-to-consumer models, enabling them to collect first-party data, offer personalized product bundles, and minimize price-related barriers. Intellectual property continues to play a critical role in the market. For instance, Lallemand Health Solutions’ approval for its Cerenity strain provides a temporary competitive advantage through monopoly pricing until competing strains achieve similar regulatory approvals.

Private-label offerings from retailers are intensifying competition in commoditized vitamin categories, prompting national brands to invest in clinical studies or license patented ingredients to differentiate their products. Growth opportunities are emerging in areas such as personalized nutrition, CBD-based health products (pending regulatory clarity), and innovative delivery systems designed for convenience-oriented consumers. New entrants are leveraging direct-to-consumer models and subscription services to bypass traditional retail constraints. In response, established players are adopting omnichannel strategies and strengthening their digital engagement efforts.

Canada Nutraceuticals Industry Leaders

-

PepsiCo Inc.

-

Nestlé S.A.

-

Jamieson Wellness Inc.

-

Danone S.A.

-

Herbalife Nutrition Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Vitux has enhanced its Concordix chewable emulsion delivery platform by securing extended patent protection and expanding its portfolio to include over 60 launch-ready nutraceutical product concepts. These concepts span categories such as immunity, longevity, and general wellness. The platform offers improved delivery of both oil- and water-soluble ingredients, providing better bioavailability, taste masking, and stability compared to traditional supplement formats.

- August 2025: free product for Canadian consumers. The product provides functional hydration through a scientifically formulated amino acid blend aimed at restoring electrolyte balance after physical activity, heat exposure, travel, or other active pursuits, without the inclusion of sugar.

- February 2025: Apotex Inc., a leading pharmaceutical company, has expanded into the natural health products market by acquiring CanPrev. This acquisition includes a portfolio of over 445 products under the CanPrev, Cyto-Matrix, and Orange Naturals brands.

- January 2025: General Mills has finalized the sale of its Canadian yogurt business to Sodiaal, a French dairy cooperative. The transaction includes local operations of brands such as Yoplait and Liberté, as well as a manufacturing facility located in Saint-Hyacinthe, Québec.

- January 2024: Celsius Holdings, Inc., the manufacturer of the CELSIUS energy drink brand, has entered international markets. This expansion strengthens the company's global sales and distribution network, providing consumers in Canada, the United Kingdom, and Ireland with access to CELSIUS energy drinks.

Canada Nutraceuticals Market Report Scope

Nutraceuticals are products that provide nutrition, along with other health benefits. It has many physiological benefits, protecting the human body against chronic diseases. Canada's Nutraceuticals Market is segmented by type and distribution channel. By type, the market is segmented as functional food, functional beverages, and dietary supplements. The functional food category is further sub-segmented into functional cereals, functional bakery & confectionary, functional dairy products, functional snacks, and other functional foods. Similarly, functional beverages are sub-segmented into energy drinks, sports drinks, fortified juices, dairy & dairy alternative beverages, and other functional beverages, and dietary supplements are sub-segmented into vitamins, minerals, botanicals, enzymes, fatty acids, proteins, and other dietary supplements. Further, based on distribution channels, the market is segmented as specialty stores, supermarkets/hypermarkets, convenience stores, drug stores/pharmacies, online retail stores, and other distribution channels. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Functional Food | Cereal |

| Bakery and Confectionery | |

| Dairy | |

| Snacks | |

| Other Functional Foods | |

| Functional Beverage | Energy Drink |

| Sports Drink | |

| Fortified Juice | |

| Dairy and Dairy-Alternative Beverage | |

| Other Functional Beverages | |

| Dietary Supplement | Vitamins and Minerals |

| Mineral | |

| Botanical | |

| Enzyme | |

| Fatty Acid | |

| Other Supplements |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Drug Stores/Pharmacies |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Functional Food | Cereal |

| Bakery and Confectionery | ||

| Dairy | ||

| Snacks | ||

| Other Functional Foods | ||

| Functional Beverage | Energy Drink | |

| Sports Drink | ||

| Fortified Juice | ||

| Dairy and Dairy-Alternative Beverage | ||

| Other Functional Beverages | ||

| Dietary Supplement | Vitamins and Minerals | |

| Mineral | ||

| Botanical | ||

| Enzyme | ||

| Fatty Acid | ||

| Other Supplements | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Drug Stores/Pharmacies | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

How big is the Canada nutraceuticals market in 2026?

It is valued at USD 9.54 billion in 2026, with a forecast to reach USD 13.87 billion by 2031.

Which product category is growing fastest?

Functional beverages are projected to post an 8.59% CAGR over 2026-2031, the quickest across major categories.

What channel is expected to gain the most share?

Online retail stores should expand at a 9.11% CAGR through 2031 as consumers migrate to subscription-based purchasing.

Why does regulatory approval matter in Canada?

Health Canada’s NPN system demands clinical evidence, so approval signals product safety and efficacy, driving retailer and consumer trust.

Page last updated on: