Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 88.54 Billion |

| Market Size (2026) | USD 92.83 Billion |

| Market Size (2031) | USD 117.66 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Nutraceutical Market Analysis by Mordor Intelligence

The European nutraceutical market size was valued at USD 88.54 billion in 2025 and estimated to grow from USD 92.83 billion in 2026 to reach USD 117.66 billion by 2031, at a CAGR of 4.85% during the forecast period (2026-2031). This growth is driven by increasing spending on preventive healthcare, supportive policies for functional nutrition. Rising obesity rates and the related economic costs are pushing the market toward evidence-based solutions to delay the onset of chronic diseases. Among product types, functional foods held the largest market share, while dietary supplements are expected to grow the fastest. In terms of source, plant-based ingredients generated the highest revenue in 2024, while microbial-based alternatives are expected to grow rapidly. In terms of distribution channels, supermarkets/hypermarkets accounted for the largest market share, but online retail stores are projected to grow significantly. In terms of geography, Germany led the market, while the United Kingdom is expected to record the highest CAGR by 2030. The market remains fragmented, with agile companies using direct-to-consumer models to target specific health needs, while established food and pharmaceutical companies such as Glanbia PLC, Amway Corp., and others expand their clinical-claim portfolios to maintain their market position.

Key Report Takeaways

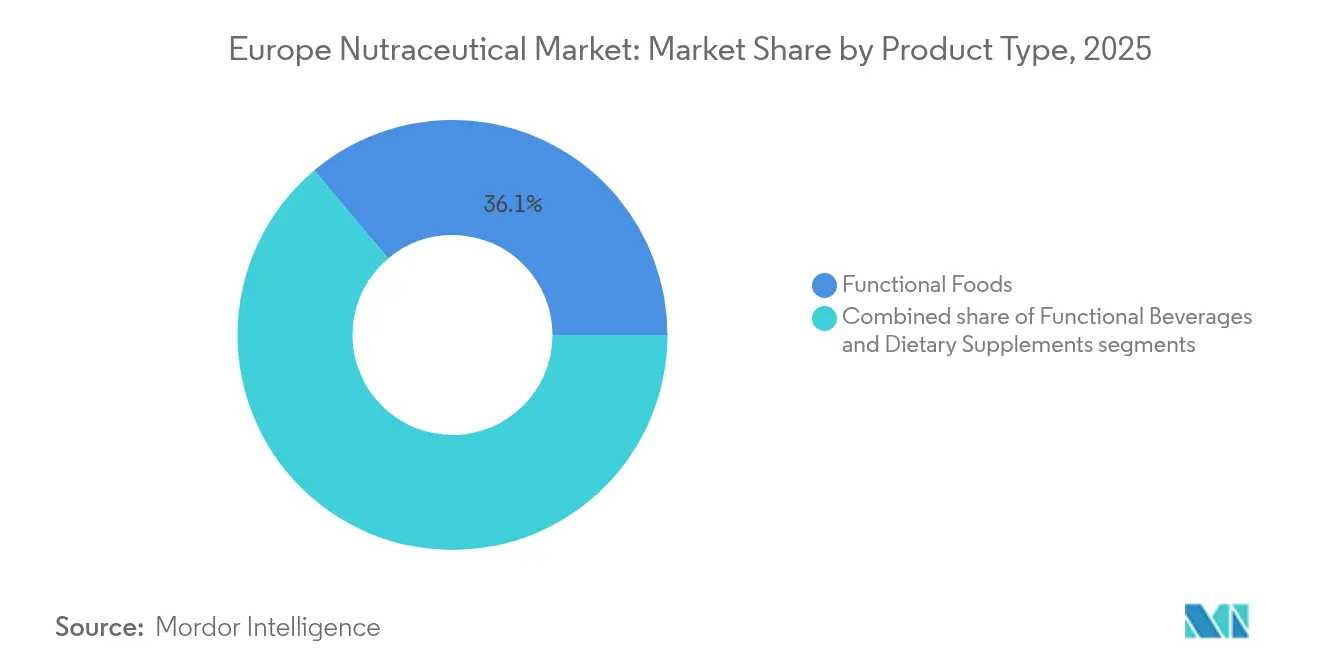

- By product type, functional foods commanded 36.12% of the Europe nutraceutical market share in 2025, whereas dietary supplements are projected to register the fastest 6.68% CAGR through 2031.

- By source, plant-based ingredients delivered 54.05% revenue share in 2025, while microbial-based alternatives are forecast to accelerate at 6.92% CAGR to 2031.

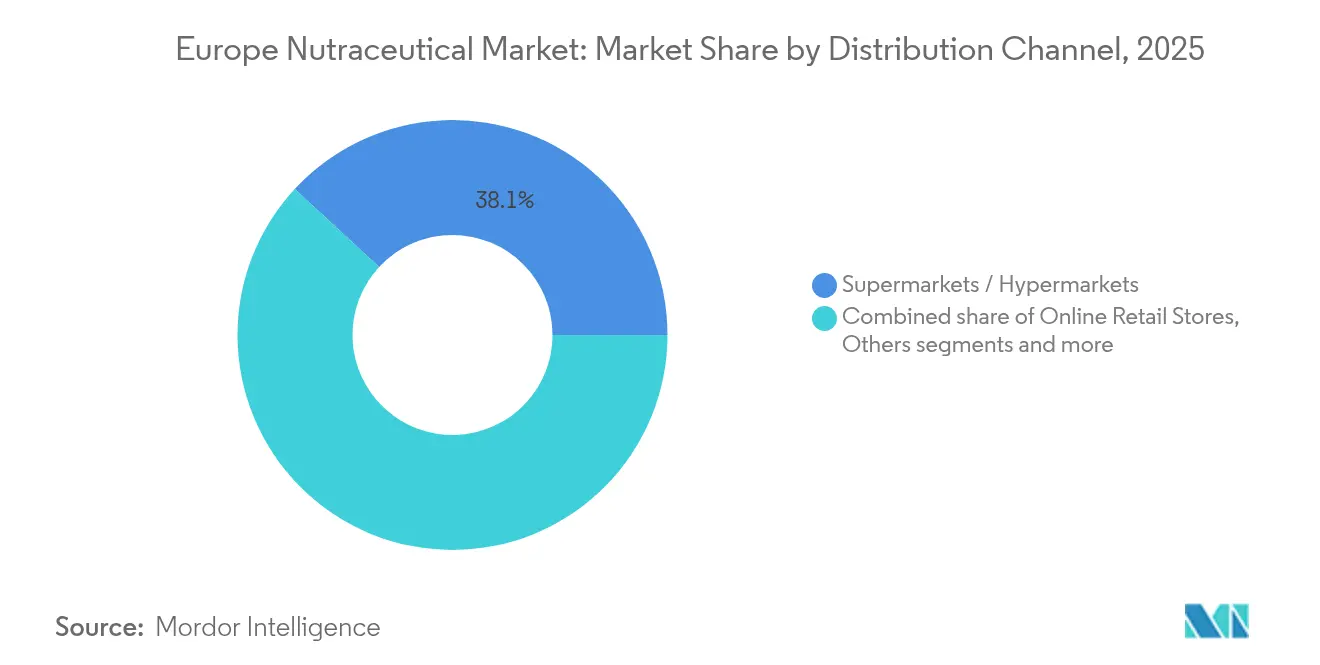

- By distribution channel, supermarkets/hypermarkets held 38.11% of the 2025 Europe nutraceutical market size, yet online retail stores are set to expand at a 7.12% CAGR over the outlook period.

- By geography, Germany led with 19.22% market share in 2025, whereas the United Kingdom is on track for the highest 7.38% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Nutraceutical Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer focus on preventive health and wellness nutrition | +1.2% | Strongest adoption in Germany, Netherlands, Sweden | Medium term (2-4 years) |

| Ageing population boosting functional intake | +1.5% | Europe-wide, particularly Germany, Italy, France with highest elderly populations | Long term (≥ 4 years) |

| Rising demand for clean-label and natural products | +0.8% | Western Europe core, expanding to Central and Eastern Europe | Short term (≤ 2 years) |

| High sports and fitness participation rates | +0.6% | Northern Europe (Sweden, Netherlands, United Kingdom) with spillover to urban centers | Medium term (2-4 years) |

| Obesity and weight management concerns | +1.0% | Pan-European, with acute focus in United Kingdom, Germany, Malta showing highest obesity rates | Short term (≤ 2 years) |

| Integration with public health programs | +0.4% | France, Netherlands, Sweden leading integration models | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging population boosting functional intake

Europe’s aging population is increasing the demand for nutraceuticals that support cognitive health, bone strength, and heart health. As of January 2024, Europe’s overall population was estimated at 449.3 million, with over 21.6% aged 65 and older, according to the European Union[1]Source: European Union, "Population Structure and Ageing", ec.europa.eu. With 1 in 6 Europeans dying from noncommunicable diseases before the age of 70, as per PubMed Central, as of May 2025, policymakers are encouraging preventive nutrition through subsidies to lower long-term healthcare costs[2]Source: PubMed Central, "From Inertia to Impact: Delivering Real Solutions For Non-Communicable Diseases", pmc.ncbi.nlm.nih.gov. This has led to a rise in products like omega-3 supplements for cholesterol control and collagen peptides for joint health, aimed at seniors focused on staying active as they age. Recent product launches in Europe have introduced advanced formulations that combine these functional ingredients to address the specific needs of older adults. Companies focusing on senior health in their product development benefit from supportive policies, such as VAT reductions on medically targeted supplements and faster European Food Safety Authority (EFSA) approvals for health claims related to aging.

Rising consumer focus on preventive health and wellness nutrition

The European nutraceutical market is growing as more people focus on preventive health and wellness. This shift has increased demand for products that help prevent chronic diseases and support overall health. Consumers are looking for supplements and functional foods that boost immunity, improve digestion, increase energy, and promote well-being. According to the World Health Organization, by 2025, 8.9 million more people in Germany are expected to experience better health, reflecting a broader trend of health awareness across Europe[3]Source: World Health Organization, "Germany: Health Data Overview For The Federal Republic of Germany", data.who.int. At Vitafoods Europe 2024, a leading industry event, companies showcased innovative products to meet these needs. For example, Evonik launched AvailOm, an omega-3 powder with Boswellia extract for joint health, and IN VIVO BIOTICS, a synbiotic solution to enhance gut health and immunity. These developments highlight the market’s focus on creating effective and convenient nutraceutical products that align with the growing interest in preventive health.

Obesity and weight-management concerns

Obesity and weight management are major health challenges in Europe, leading governments to implement various measures to address the issue. These include sugar taxes, clear front-of-pack nutritional labeling, and reforms in school meal programs to reduce the consumption of high-calorie foods. According to the World Population Review 2025, Russia has the highest obesity rate in Europe at 30.3%[4]Source: World Population Review, "European Obesity Rates by Country 2025", worldpopulationreview.com. In response, consumers are increasingly relying on nutraceuticals to support their weight management goals. Companies are emphasizing European Food Safety Authority (EFSA)-approved claims related to weight control to differentiate their products from general wellness supplements. Pharmacies are creating specialized sections focused on anti-obesity solutions, offering a combination of measurement tools and clinically validated supplements. This growing focus on targeted solutions reflects the rising demand for effective and science-backed products to combat obesity and promote healthier lifestyles across the region.

Rising demand for clean-label and natural products

Consumers in Europe are increasingly looking for clean-label and natural nutraceutical products due to growing awareness about ingredient transparency and a preference for healthier, minimally processed options. They want products without artificial additives, preservatives, or synthetic ingredients, choosing those with simple, natural components that fit a healthy lifestyle. This shift has pushed manufacturers to update existing products and create new ones that highlight organic certifications, natural extracts, and eco-friendly packaging. For instance, at Vitafoods Europe 2024, companies launched clean-label products like Naturacare’s Vital Extend, a bilayer tablet with natural energy-boosting ingredients, and SIRIO Pharma’s PureOrganix™ range, which includes organic gummies made with ingredients like evening primrose oil and flaxseed oil, catering to the growing demand for natural and transparent formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EFSA health-claim validation processes | -0.8% | Europe-wide, with particular impact on smaller companies lacking regulatory resources | Medium term (2-4 years) |

| High product development and compliance costs | -0.6% | Pan-European, with acute pressure on SMEs and new market entrants | Short term (≤ 2 years) |

| Consumer backlash against ultra-processed 'health' foods | -0.4% | Western Europe initially, spreading to Eastern European markets | Medium term (2-4 years) |

| Counterfeit and low-quality products online | -0.3% | concentrated effects in European high-penetration e-commerce markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent European Food Safety Authority (EFSA) health-claim validation processes

The strict health-claim approval process by the European Food Safety Authority (EFSA) creates significant hurdles for the European nutraceutical market. Companies must undergo a lengthy approval process, often taking 3 to 5 years, which includes conducting expensive clinical trials to validate health claims. The updated European Regulation 2015/2283, effective from 2025, has introduced stricter rules, requiring detailed documentation of production processes. This has further extended approval timelines and increased the complexity of bringing new products to market. As a result, larger multinational companies with dedicated regulatory teams are better positioned to navigate these challenges. While the market continues to grow, the pace of innovation has slowed. Each time the European Food Safety Authority (EFSA) introduces new rules or updates existing ones, it creates uncertainty for product developers, making it harder for companies to plan and launch new products.

High product development and compliance costs

Launching a new ingredient in the European nutraceutical market is both expensive and time-consuming due to strict regulatory requirements. Companies must conduct toxicology studies, follow good manufacturing practices (GMP), and ensure compliance with detailed labeling rules. For example, in the Netherlands, the supplement-notification system has a few tiers, with high-risk products requiring safety evaluations similar to those needed for novel-food approvals. These complex and costly processes often force smaller companies to depend on contract manufacturers, which limits the growth of niche and artisanal brands. This has led to increased consolidation in the industry, as larger companies with more resources dominate the market. Investors are now focusing on how efficiently companies manage regulatory costs, such as the expense of obtaining approved health claims. This highlights how regulatory compliance plays a critical role in shaping competition and overall market trends.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Foods Hold Lead as Supplements Accelerate

Functional Foods lead the European nutraceutical market in 2025, holding a 36.12% share. The popularity of fortified cereals, probiotic dairy drinks, and protein-enriched bakery products drives this dominance. These items benefit from strong visibility in supermarkets, reduced sugar content, and high consumer loyalty. Fiber-fortified breakfast items and slow-digesting proteins remain household staples, while confectionery brands include plant sterols and omega-3s to cater to healthier snacking trends. Lactose-free specialty dairy drinks with probiotics further strengthen their position by addressing digestive health needs across all age groups.

Dietary Supplements are expected to grow the fastest, with a 6.68% CAGR through 2031, significantly contributing to the European nutraceutical market size during the forecast period. This growth is fueled by precise dosing, tele-nutrition services, and condition-specific products like enzyme blends for digestion or botanicals for menopause relief. Personalized daily sachets improve adherence and customer retention, while clean-label sports-nutrition capsules attract a broader audience beyond athletes. As e-pharmacy regulations tighten in the region, brands offering clinically backed products in convenient formats are well-positioned to gain market share in both physical and online stores.

By Source: Plant-Based Ingredients Dominate, Microbial Path Gains Momentum

Plant-based ingredients made up 54.05% of the European nutraceutical market share in 2025, driven by the region’s strong history with botanical extracts, herbal remedies, and fruit-based antioxidants. Consumers associate plant-based products with safety and sustainability, encouraging retailers to highlight eco-friendly labels and farm-to-table stories. Established suppliers use vertical integration and fair-trade certifications to ensure a steady supply of raw materials, while manufacturers combine different botanicals to create products targeting immunity, sleep, and metabolism. Examples like collagen from citrus peel and fermented soy isoflavones show how even traditionally animal-based or synthetic ingredients are shifting to plant-based options, helping maintain their leading position.

Microbial-based production is expected to grow at the fastest rate, with a 6.92% CAGR by 2031, making precision fermentation a key driver of the European nutraceutical market growth. Fermentation-based ingredients like riboflavin, resveratrol, and new postbiotic peptides avoid agricultural challenges, meet clean-label requirements, and reduce carbon footprints, appealing to environmentally conscious consumers. Collaborations between ingredient manufacturers and biotech startups have cut production costs compared to traditional methods, making these products more affordable. European Food Safety Authority (EFSA) approvals for fermented bioactives further validate this approach, attracting investments for developing new strains and boosting their use in supplements and fortified foods.

By Distribution Channel: Supermarkets Stay Anchor While E-Commerce Surges

Supermarkets/Hypermarkets remained the leading sales channel, holding 38.11% of the European nutraceutical market share in 2025. This dominance is due to high customer traffic, dedicated wellness sections, and loyalty programs that combine functional foods with supplements. In-store pharmacists and dietitians guide customers on European Food Safety Authority (EFSA)-approved claims, building trust during purchases. Private-label products, priced lower than national brands, attract budget-conscious buyers, while prominent placement of immunity shots and protein bars makes these items regular purchases. Some stores are even testing refill stations for vitamin gummies, showcasing innovation in physical retail.

Online Retail Stores are expected to grow at a 7.12% CAGR through 2031, increasing their share in the European nutraceutical market. Simplified compliance tools now allow products to be listed across countries in minutes. E-commerce platforms use AI-based quizzes and subscription offers to boost sales and retain customers, while fast urban delivery expands access to chilled probiotics. Features like QR codes and blockchain tracking help address concerns about counterfeit products, encouraging more purchases of premium items. As cross-border logistics improve under the European Union Digital Services Act, online stores will continue to gain market share, especially among younger consumers who prefer the convenience of shopping on their phones.

Geography Analysis

In 2025, Germany accounted for 19.22% of the European nutraceutical market share, driven by its strong focus on clinical testing and adherence to strict quality standards. These factors make German products highly appealing to health-conscious and cautious consumers. The country also complies with rigorous European Food Safety Authority (EFSA) requirements, ensuring product safety and reliability. German companies actively collaborate with partners across Europe, sharing research and expertise. This commitment to quality and innovation has built a strong reputation for Germany, positioning it as a key leader in the European nutraceutical market.

The United Kingdom is the fastest-growing market, with a projected CAGR of 7.38% through 2031. Since Brexit, the United Kingdom has been quicker to approve new foods and adapt labeling regulations, giving it an advantage in the market. Local brands are focusing on innovative products like gummies for cognitive health and beverages for stress relief, which align with growing consumer interest in mental and physical well-being. This adaptability and focus on evolving health needs have positioned the United Kingdom as a dynamic and rapidly expanding market for nutraceuticals.

Southern Europe offers diverse growth opportunities in the nutraceutical market. Italy leads in per-capita supplement spending, driving demand for premium anti-aging products. Spain incorporates functional foods into its Mediterranean diet, promoting items like olive-oil-based spreads and fiber-enriched gazpacho. France combines its culinary traditions with expertise in beauty products, boosting the popularity of nutricosmetics such as collagen supplements for skin health. These regional trends highlight the unique consumer preferences and growth potential across Southern Europe.

Competitive Landscape

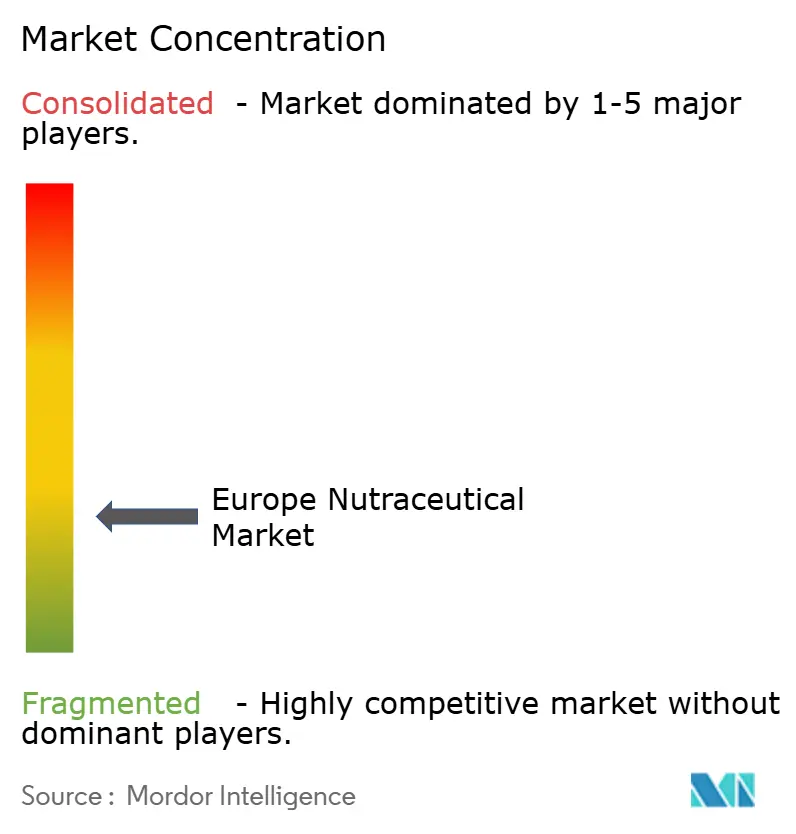

The European nutraceutical market is highly competitive, with no single company dominating the industry. Leading companies like Nestlé SA, Glanbia PLC, and Herbalife Nutrition Ltd. are working to expand their operations across the value chain, from sourcing raw materials to delivering finished products. Despite their efforts, their combined market share remains below 30%, leaving significant opportunities for smaller and innovative companies to enter and grow. This competitive environment encourages innovation and allows new players to focus on specific consumer needs. Smaller companies often succeed by offering unique products or targeting niche segments, which helps them carve out a space in the market.

Technology is becoming a key factor in driving growth and innovation in the nutraceutical market. For instance, Danone’s acquisition of The Akkermansia Company has enhanced its expertise in microbiome research, enabling the development of advanced gut-health products. These advancements are helping companies meet the growing demand for tailored and effective health products, which health-conscious consumers increasingly seek. Technology is also enabling companies to create more personalized solutions, which appeal to consumers looking for products that address their specific health needs.

Collaborations between companies are also playing a significant role in shaping the market by fostering innovation and improving efficiency. For example, Arla has partnered with Volac to establish a high-protein production hub in Wales, while AstaReal and Polaris are working together to create algae-based astaxanthin combined with plant omega-3s for athletic recovery. Startups are using regulatory technology to simplify compliance with European Food Safety Authority (EFSA) requirements, enabling faster market entry or licensing opportunities. These partnerships and advancements are helping companies remain competitive while addressing increasing regulatory challenges.

Europe Nutraceutical Industry Leaders

-

The Coca-Cola Company

-

Nestlé S.A.

-

Amway Corp.

-

Herbalife Nutrition Ltd.

-

Glanbia PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Danone completed the acquisition of The Akkermansia Company, which provided it with access to the EFSA-approved pasteurized Akkermansia muciniphila strain. This strain was recognized for its potential in addressing cardiometabolic health issues, allowing Danone to strengthen its position in the growing market for advanced gut-health solutions.

- May 2025: Rousselot introduced Nextida GC collagen peptides at Vitafoods Europe, aiming to support balanced glucose levels. This launch highlighted the company's focus on addressing specific health concerns through innovative collagen-based solutions.

- April 2025: Azelis expanded its nutraceutical portfolio in Spain through the acquisition of Solchem Nature S.L. This strategic move allowed Azelis to strengthen its position in the Spanish market by integrating Solchem Nature's expertise in high-quality nutraceutical ingredients.

- January 2025: The Italian hair care brand Nutrire entered the market. Its products utilize a blend of naturally-derived ingredients designed to block DHT, which is associated with hair shedding.

Europe Nutraceutical Market Report Scope

Nutraceutical products are substances that have physiological benefits, protect against chronic diseases, improve health, delay aging, and increase life expectancy. The European nutraceuticals market is segmented by product type into functional food, functional beverages, and dietary supplements. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into the United Kingdom, Germany, France, Spain, Italy, Russia, and the Rest of Europe. For each segment, the market sizing and forecasts have been done based on value (in USD Million).

By Product Type

| Functional Foods | Breakfast Cereals |

| Bakery and Confectionery | |

| Snacks | |

| Dairy Products | |

| Other Functional Foods | |

| Functional Beverages | Energy Drinks |

| Sports Drinks | |

| Fortified Juices | |

| Other Functional Beverages | |

| Dietary Supplements | Vitamins and Minerals |

| Botanicals | |

| Enzymes | |

| Omega | |

| Other Dietary Supplements |

By Source

| Plant Based |

| Animal Based |

| Microbial Based |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Pharmacies and Drug Stores |

| Online Retail Stores |

| Others |

By Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Poland |

| Switzerland |

| Russia |

| Rest of Europe |

| By Product Type | Functional Foods | Breakfast Cereals |

| Bakery and Confectionery | ||

| Snacks | ||

| Dairy Products | ||

| Other Functional Foods | ||

| Functional Beverages | Energy Drinks | |

| Sports Drinks | ||

| Fortified Juices | ||

| Other Functional Beverages | ||

| Dietary Supplements | Vitamins and Minerals | |

| Botanicals | ||

| Enzymes | ||

| Omega | ||

| Other Dietary Supplements | ||

| By Source | Plant Based | |

| Animal Based | ||

| Microbial Based | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Pharmacies and Drug Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Switzerland | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How big is the Europe nutraceuticals market in 2026?

The Europe nutraceuticals market size is valued at USD 92.83 billion in 2026.

What is the forecast growth rate for nutraceuticals across Europe?

The market is projected to advance at a 4.85% CAGR, reaching USD 117.66 billion by 2031.

Which product category is growing the fastest?

Dietary Supplements are poised for the quickest expansion at a 6.68% CAGR through 2031.

Which country is expected to grow the quickest?

The United Kingdom leads forecast growth with a 7.38% CAGR.

Page last updated on: