Kitchen Furniture And Fixtures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

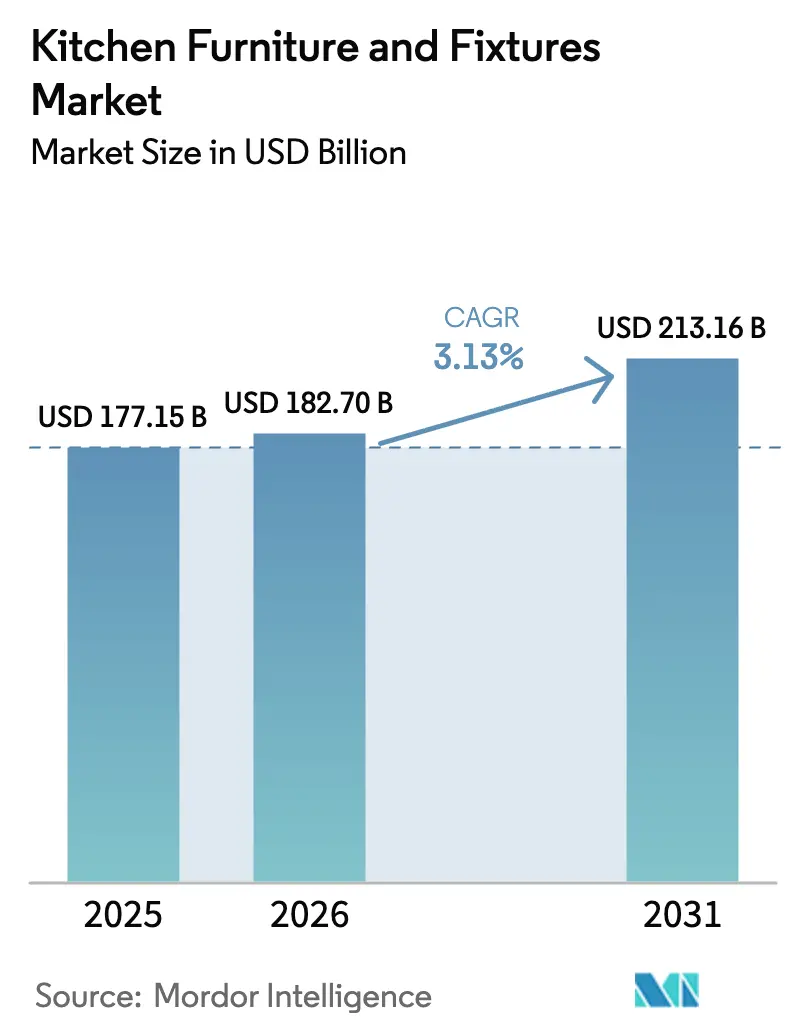

| Market Size (2026) | USD 182.70 Billion |

| Market Size (2031) | USD 213.16 Billion |

| Growth Rate (2026 - 2031) | 3.13% CAGR |

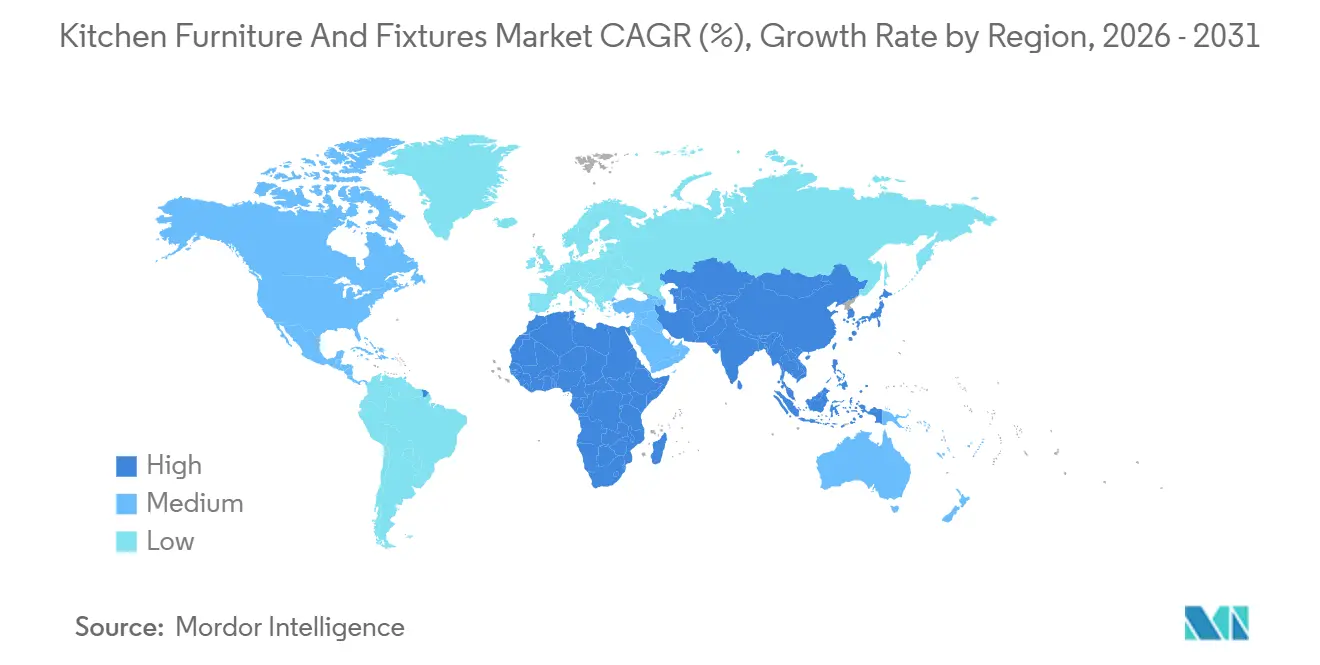

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kitchen Furniture And Fixtures Market Analysis by Mordor Intelligence

The kitchen furniture and fixture market size is expected to grow from USD 177.15 billion in 2025 to USD 182.70 billion in 2026 and is forecast to reach USD 213.16 billion by 2031 at a 3.13% CAGR over 2026–2031. This growth is driven by a combination of mature demand factors, including aging housing stock that requires renovations and upgrades, as well as standardized procurement practices in commercial and institutional projects. The increasing adoption of modular and smart-ready kitchen solutions is further driving market expansion, as these offerings offer flexibility, efficiency, and technological integration. Manufacturers are also responding to margin pressures from rising input costs and tariff exposure by offering pre-engineered products that reduce jobsite complexity and labor requirements. In addition, growing regulatory compliance requirements for formaldehyde emissions and low-VOC content are pushing the market toward factory-controlled materials and finishes, which streamline quality assurance and documentation processes. In the commercial sector, particularly hospitality and multi-family developments, there is a clear trend toward standardized kitchenettes and kit-of-parts casework. These solutions help accelerate project timelines, improve speed to occupancy, and stabilize fitout schedules, reinforcing demand growth across both residential and commercial segments.

Key Report Takeaways

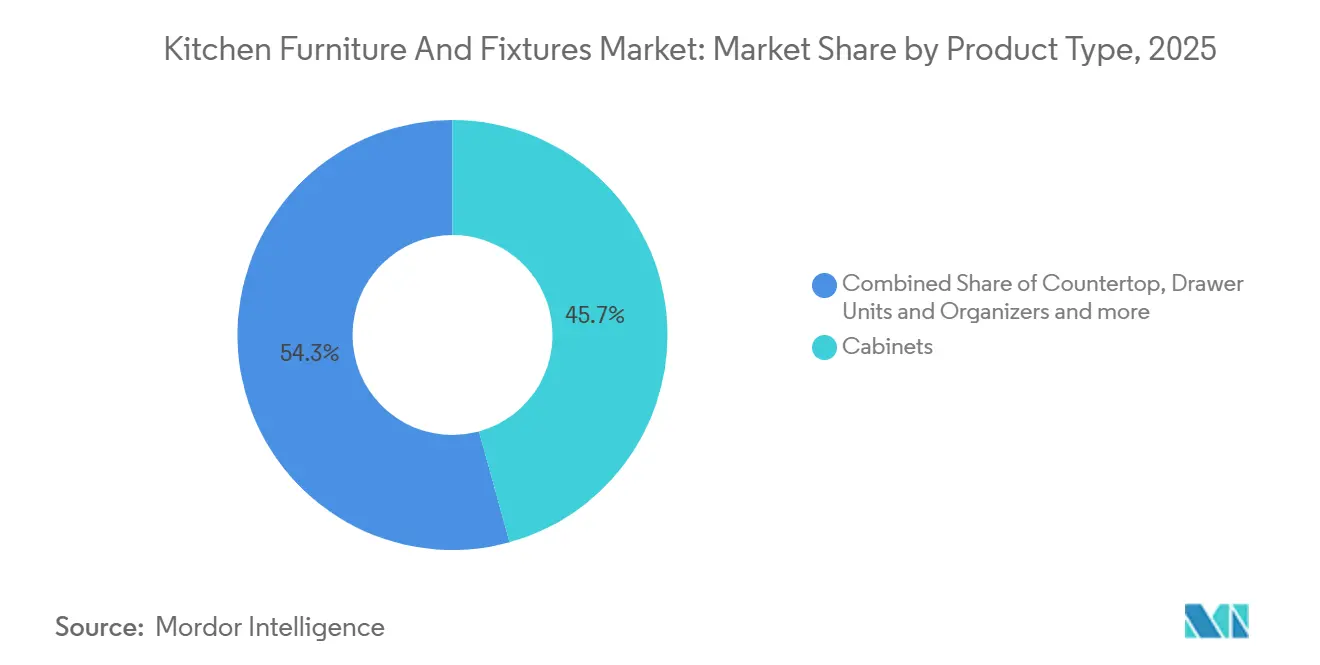

- By product type, cabinets led with 45.73% of the kitchen furniture and fixtures market share in 2025, while kitchen islands posted the fastest growth at a 3.81% CAGR through 2031.

- By material, wood-based substrates held 45.91% of the kitchen furniture and fixtures market share in 2025, while plastic and laminates recorded the highest growth at a 3.67% CAGR.

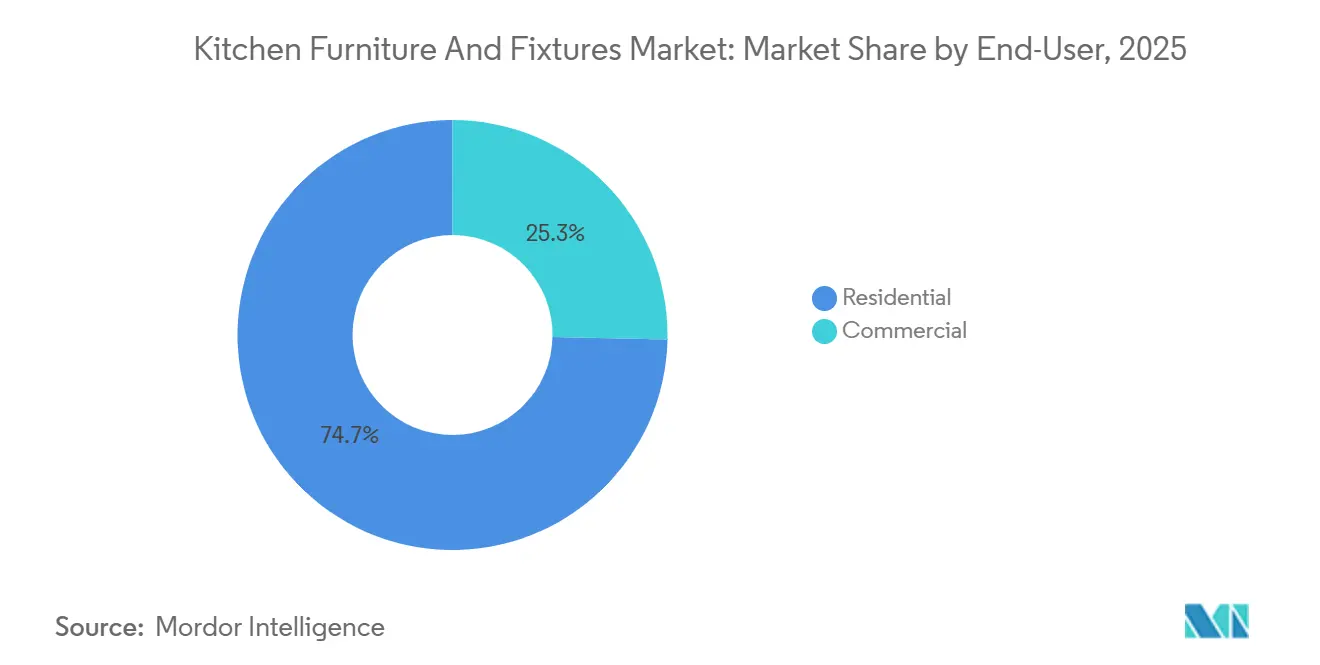

- By end-user, residential accounted for 74.67% of the kitchen furniture and fixtures market share in 2025, while commercial applications advanced at a 4.12% CAGR.

- By distribution channel, offline captured 76.68% of the kitchen furniture and fixtures market share in 2025, while online expanded at a 4.54% CAGR.

- By geography, North America represented 32.41% of the kitchen furniture and fixtures market share in 2025, while Asia-Pacific posted the fastest trajectory at a 4.91% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Kitchen Furniture And Fixtures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Shift to Modular & Pre-Engineered Kitchen Systems | +0.9% | Global, with early gains in North America, Northern Europe, and the Asia-Pacific urban centers | Medium term (2-4 years) |

| Kitchen-Centric Home Renovation Spending | +0.8% | North America and Europe leaders, emerging in the Asia-Pacific Tier II cities | Short term (≤ 2 years) |

| Shift Toward Modular & Smart Kitchens | +0.7% | North America, Europe, and the Asia-Pacific | Medium term (2-4 years) |

| Growth of Outdoor Kitchen Installations | +0.4% | Primarily North America, with emerging markets in the Middle East | Long term (≥ 4 years) |

| Contract-Led Demand from Hospitality & Foodservice Projects | +0.6% | Global, concentrated in North America, the Middle East, and the Asia-Pacific | Medium term (2-4 years) |

| Functional Upgrades Through Smart Fixtures & Storage Hardware | +0.5% | North America, Europe, and the Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift To Modular And Pre-Engineered Kitchen Systems

Factory-built modules compress design and installation timelines and reduce jobsite errors, which is valuable where skilled labor supply is tight and wage rates are elevated. Large-format players sustain standardized ranges at scale and pair them with centralized procurement that stabilizes pricing and keeps throughput resilient in 2026. Integrated lighting, power management, and sensor-ready features are increasingly built into casework platforms so installers can complete jobs with fewer site visits and less specialized commissioning. Software-led configuration and CNC machining continue to raise precision and repeatability, which helps configured-to-order programs scale without excessive lead-time risk in the kitchen furniture and fixtures market. Environmental rules, such as the United States Environmental Protection Agency’s TSCA Title VI Formaldehyde Emission Standards for Composite Wood Products, require composite wood panels and finished goods to meet strict emission limits, undergo third-party testing, and be certified and labeled as compliant, effectively normalizing low-VOC substrates and finishes as baseline specifications for 2026 projects[1]Source: U.S. Environmental Protection Agency, “Formaldehyde Emission Standards for Composite Wood Products,” EPA.gov.. Compliance with these standards reinforces the value of factory-controlled production, as off-site manufacturing ensures consistent material quality, regulatory adherence, and safer end products.

Kitchen-Centric Home Renovation Spending

Kitchen scopes remain the focal point of homeowner budget allocation as households prioritize storage, workflow, lighting, and code-compliant ventilation upgrades. In 2025, over half of United States homeowners undertook renovations, with kitchens among the top investments. Median spending on large kitchen remodels was around USD 55,000, while high-end projects exceeded USD 150,000, and homeowners increasingly relied on contractors, keeping kitchen upgrades a central focus of renovation budgets [2] Source: Houzz Inc., “Home Renovation Activity Remains Strong Amid Softening Spend,” Houzz.com, 2025.. Remodeling outlays signaled solid momentum in 2025, which supported pipelines for cabinets, fixtures, and surfaces that anchor the kitchen bill of materials. Associations report that minor kitchen improvements often deliver stronger cost recovery than major gut renovations, sustaining demand for cabinet refacing and hardware refreshes in the kitchen furniture and fixtures market. Contractors continue to include price and schedule safeguards as material and logistics conditions evolve, and homeowners favor pre-engineered options that limit change orders and site disruption, while lumber pricing and tariffs remain watchpoints that can shift project timing and scope selection across regions.

Shift Toward Modular And Smart Kitchens

Smart-ready casework moves into mainstream specifications as designers integrate task lighting, soft-close systems, and sensor-enabled drawers that boost access and usability. The United States EPA’s ENERGY STAR Smart Home Energy Management Systems program highlights connected appliances that automate and optimize energy use, supporting the adoption of smart, networked devices, key enablers for modular and technology-driven kitchens[3]Source: U.S. Environmental Protection Agency, “Smart Home Energy Management Systems,” ENERGY STAR. Extended-stay and hospitality pilots refine repeatable templates that reduce energy use and enhance operating visibility, which then inform residential and mixed-use standards. Specifiers navigate interoperability concerns by favoring compact ecosystems and cabinet-embedded features that minimize commissioning complexity at handover. Building codes also push toward connected controls in commercial settings, accelerating the adoption of demand-control ventilation and integrated lighting across high-capacity kitchens. Manufacturers that align compliant substrates with integrated power and lighting lift total value without raising on-site complexity in the kitchen furniture and fixtures market.

Contract-Led Demand From Hospitality And Foodservice Projects

Hospitality, build-to-rent, and foodservice operators prioritize standardized kitchenette kits that reduce fitout variability, which keeps plant utilization healthy when retail channels soften. Extended-stay properties and multi-family units favor compact modular configurations that fit consistent footprints and speed unit turnover across programs. Suppliers address these needs with pre-integrated lighting, code-compliant surfaces, and quick-install hardware that help project teams reduce punch lists and accelerate closeout. Export-oriented producers with automated lines and software-driven configuration can serve multi-country programs and route around tariff-exposed inputs when needed. Reinvestment cycles in hotels and foodservice continue to refill pipelines in 2026, which supports steady order flow for cabinetry, fixtures, and related surfaces in the kitchen furniture and fixtures market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Inflation in Engineered Wood, Stone & Metal Inputs | -0.6% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Skilled Installer Shortages | -0.4% | North America, Europe, and the emerging Asia-Pacific | Medium term (2-4 years) |

| Stricter Formaldehyde & VOC Limits | -0.2% | North America and Europe, spreading to the Asia-Pacific | Medium term (2-4 years) |

| Anti-Dumping Tariffs on Flat-Pack Imports | -0.3% | North America, with select EU actions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost Inflation In Engineered Wood, Stone, And Metal Inputs

Lumber and panel volatility raises budget risk and pushes designers toward standardized, pre-finished components that limit rework and waste on site. Company disclosures in 2025 highlighted elevated export duty burdens and the flow-through of input pressures across downstream millwork and cabinetry lines. Engineered stone and quartz costs remain sticky due to resin inputs and logistics factors, which lead some projects to consider alternative surfacing strategies in the kitchen furniture and fixtures market. Compliance for formaldehyde emissions and low-VOC finishes remains an added cost, yet it enables factory control and clear documentation for code reviews. Distributors respond with inventory planning and supplier consolidation to stabilize pricing, while pass-through to end buyers remains uneven when competition is intense.

Skilled Installer Shortages

Trade labor scarcity remains a gating factor for kitchen throughput as contractors compete for licensed electricians and experienced installers, which raises wage rates and extends completion timelines. The shift toward pre-engineered and modular systems reduces on-site hours and compresses schedules, which helps mitigate bottlenecks in busy urban markets. Developers of multi-family and hospitality assets increasingly favor prefabricated modules that reduce field labor dependence during tight construction windows. Training and apprenticeship initiatives are expanding but will take time to restore capacity, so project planning in 2026 continues to emphasize predictable installation paths in the kitchen furniture and fixtures market[4]Source: National Kitchen & Bath Association, “2025 Kitchen & Bath Market Outlook,” NKBA, kb.nkba.org. Manufacturers invest in plant automation and quick-install hardware to move assembly hours from the jobsite to the factory floor and stabilize cycle times.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Diversification Meets Design Premiumization

Cabinets accounted for 45.73% of the kitchen furniture and fixtures market revenue in 2025, reflecting their dual role as essential storage infrastructure and the primary visual anchor in both residential and commercial spaces. Flat-pack and modular cabinet formats are increasingly adopted as e-commerce and direct-to-consumer models improve transparency and shorten lead times, supporting steady market momentum. Kitchen islands are the fastest-growing segment, expanding at a 3.81% CAGR, driven by open-plan layouts, multiuse work zones, and integrated power and cooking features. Hospitality and multi-family developments often include islands and peninsula configurations with pre-integrated outlets, lighting, and seating to streamline installation and align with standardized layouts. Hardware, fixtures, and task lighting are playing a growing role in kitchen performance, with soft-close systems and integrated illumination enhancing usability and ergonomics. These trends collectively reinforce the importance of design-led functionality and convenience in shaping consumer and commercial preferences.

Countertops and fixtures continue to capture a significant share of project budgets, as surface durability, hygiene, and water management are critical to everyday function and perceived quality. Resilient, low-maintenance surfaces with a premium appearance are increasingly preferred, while sinks, faucets, and lighting are specified for water efficiency, accessibility, and ease of service. Hardware and accessories remain key margin drivers for suppliers, with consistent finishes, damping quality, and integrated lighting delivering tangible performance improvements valued by homeowners and operators. Modular inserts, organization systems, and space-saving solutions are being refined to maximize storage in small-footprint kitchens without compromising functionality. This combination of functional upgrades, ergonomic enhancements, and design-focused features supports broad product mix resilience across the kitchen furniture and fixtures market. Overall, market growth is reinforced by innovations that balance efficiency, aesthetics, and long-term usability.

By Material: Engineering’s Triumph Over Tradition

Wood-based materials accounted for 45.91% of kitchen furniture and fixtures revenue in 2025, driven by buyer preferences for longevity, repairability, and premium finishes in semi-custom and custom programs. Engineered wood panels provide consistent machining tolerances and reliable fastener performance, making them ideal for modular systems and flat-pack logistics. Compliance with formaldehyde and VOC regulations is steering demand toward factory-finished substrates and low-emitting adhesives, simplifying documentation and inspections. Material choices increasingly balance durability, price stability, and the ability to integrate lighting and hardware without compromising structural integrity. These trends support both residential and commercial applications, where long-lasting, high-quality finishes remain a priority. Overall, wood-based materials continue to dominate due to their versatility, performance, and aesthetic appeal.

Plastic and laminates are the fastest-growing segment, expanding at a 3.67% CAGR as high-pressure laminates and thermofoil-wrapped components offer improved scratch resistance and moisture performance for busy homes and commercial kitchens. Their adoption is also influenced by supply chain resilience, providing alternatives when solid wood availability is affected by tariffs or freight constraints. Laminates and thermofoil solutions ensure color consistency across production batches and allow quick replacements in commercial fleets requiring uniformity. Metal cabinets occupy a niche role in high-hygiene environments, such as commercial foodservice, where cleanability and heat resistance are critical. Glass and ceramic elements are increasingly used in backsplashes and accent areas, delivering reflective finishes and easy-to-clean surfaces that enhance lighting and maintenance in compact spaces. Together, these material trends reflect a market-wide shift toward predictable, code-compliant, and performance-driven finishes in kitchen furniture and fixtures.

By End-User: Residential Resilience Versus Commercial Velocity

Residential end users accounted for 74.67% of kitchen furniture and fixtures demand in 2025, driven by upgrade cycles in aging housing stock and a focus on layout efficiency, storage, and accessible design. Homeowners continued to prioritize kitchen improvements as renovation spending remained strong, supported by home equity cushions and a preference for stay-in-place strategies during high-interest-rate conditions. Minor renovations and cabinet refacing often deliver higher cost recovery at resale compared with full gut remodels, sustaining demand for cabinet fronts, hardware, and lighting upgrades. Accessibility features, including pull-out shelves and easier-to-reach storage, are increasingly adopted in multigenerational households and aging-in-place retrofits. These trends support a balanced mix of price points and product tiers tailored to diverse project scopes.

Commercial applications grew at a 4.12% CAGR, led by hospitality, multi-family turnkey units, and foodservice back-of-house upgrades that standardize specifications. Extended-stay hospitality formats now incorporate compact kitchenettes in a growing share of rooms, while multi-family projects deploy repeatable layouts that simplify procurement and installation. Foodservice programs prioritize high-throughput, easy-to-clean casework with integrated lighting and storage that withstands heavy use and speeds nightly resets. Code compliance is a key driver in commercial installations, with energy management, ventilation, and other controls often pre-integrated for faster commissioning. These factors support durable demand across both new-build and retrofit schedules. Collectively, the commercial segment benefits from standardized solutions that reduce complexity, accelerate timelines, and enhance operational efficiency.

By Distribution Channel: Offline Dominance Under Digital Siege

Offline channels accounted for 76.68% of kitchen furniture and fixtures revenue in 2025, driven by specialty showrooms, builder networks, and professional channels that manage complex scoping, templating, and code documentation for high-stakes projects. In-person design consultations remain critical for premium projects, while builder-direct procurement captures volume through negotiated programs on standardized models. Retailers and home centers adjust assortments and price points to address tighter budgets, balancing inventory and tariff pressures that affect mid-market offerings. Suppliers with modular ranges and quick-ship inventories gain share as contractors focus on controlling schedules and minimizing change orders. The industry continues to rely on offline coordination to integrate appliances, ventilation, and finishes for intricate projects.

Online channels recorded the fastest growth, expanding at a 4.54% CAGR, as visualization tools and direct-to-consumer models allow buyers to explore configurations and pricing earlier in the decision process. Mobile apps and web-based configurators help reduce returns and increase buyer confidence by simulating fit and color under realistic lighting. Flat-pack, RTA-compatible products benefit most from online sales, while fully custom millwork remains tied to offline channels due to templating and site coordination needs. Online-direct players are enhancing transparency around lead times and installation support, gradually increasing the addressable market. As AR and configurator tools improve, the overall channel mix is slowly rebalancing. Despite this growth, professional networks and in-person coordination continue to play a critical role in complex or high-value scopes.

Geography Analysis

North America accounted for 32.41% of global kitchen furniture and fixtures revenue in 2025, as remodeling outlays remained resilient, supporting steady program pipelines. Home improvement spending stayed strong despite slower overall home sales in a high-interest-rate environment. Professional channels and service-led assortments stabilized cabinet and fixture orders. Tariff shifts and lumber price movements shaped pricing and delivery plans, keeping value-engineered designs and modular kits in focus. Warmer states saw growth in outdoor kitchen adoption, where integrated cooking and refrigeration zones became increasingly practical year-round.

Europe sustained a significant share of global activity, with strong modular penetration in core markets such as Germany. Macro softness and slower discretionary spending weighed on overall consumer demand in 2025. Automated production lines and configured-to-order software enabled competitive pricing and shorter lead times for large retailers and contract programs. Suppliers adapted sourcing to meet environmental certifications and trade restrictions while maintaining throughput for private-label ranges. Showrooms increasingly integrated smart-ready features and sustainable materials into mainstream modular kitchen offerings, reflecting cross-border design diffusion.

Asia-Pacific posted the fastest growth, with a 4.91% CAGR through 2031, driven by urbanization, rising household incomes, and the adoption of builder-standard modular kitchens. Export-oriented clusters balanced domestic demand with global shipments, while tariff regimes influenced sourcing of hardware and flat-pack casework. Developers emphasized speed, repeatability, and durability in compact floor plans, reinforcing the use of engineered substrates and pre-finished components. Configured-to-order modules optimized through software and validated with visualization tools became standard before production. These trends strengthened the region’s leadership in modular kitchen penetration and mixed-channel sales heading into 2026.

Competitive Landscape

The kitchen furniture and fixtures market remains highly fragmented, with the leading players capturing only a modest portion of overall revenue. Regional specialists and vertically integrated contract manufacturers continue to thrive by aligning closely with local codes, design preferences, and service expectations. Companies differentiate themselves through tight supply chain control, from material sourcing to in-house finishing, which helps manage volatility and maintain predictable lead times. Compliance-ready substrates and documented emissions testing have become essential for cross-border sales and public-sector procurement. Leading firms leverage scale in procurement and manufacturing while coordinating broad supplier networks to keep everyday price points competitive. Meanwhile, local and regional players focus on agility and service excellence to sustain their presence in niche markets.

Inter IKEA Group continues to apply its scale advantage across sourcing and production, ensuring competitive pricing across global markets. Other major players refine channel strategies to balance dealer-based assortments with big box and mass-market demand, while navigating input costs and trade dynamics. European leaders advance modular efficiencies and automation as part of footprint optimization to protect margins amid softer consumer demand. Hardware and lighting integration by top casework brands has increased perceived value without adding complexity during installation, contributing to steadier project close rates in professional channels. Supply chains increasingly emphasize sustainability, transparency, and traceable materials to meet evolving customer expectations. These approaches collectively reinforce resilience in a fragmented and competitive market environment.

Several strategic themes emerged in 2026 that shaped industry priorities. Modular hospitality concepts have expanded from pilot projects to full program implementations, supporting suppliers of compact kitchenettes and quick-install casework. Software-enabled visualization and configured-to-order workflows shorten sales cycles, reduce returns, and improve cash conversion while stabilizing backlogs. Trade compliance and material transparency have become baseline requirements for large buyers, enabling participation in public-sector and multi-country programs. Emissions documentation and low-VOC finishes now play a central role in procurement decisions, reflecting heightened regulatory and sustainability focus.

Kitchen Furniture And Fixtures Industry Leaders

Inter IKEA Group

MasterBrand Cabinets Inc.

American Woodmark Corp.

Masco Corp. (KraftMaid)

Nobilia GB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Inter IKEA Group issued plans to acquire approximately 24,000 hectares of forestland in Latvia and Lithuania, strengthening its commitment to responsible forest management and long‑term access to sustainably sourced wood. The acquisition supports local wood processing, community collaboration, and climate‑resilient, biodiversity-smart forestry practices.

- August 2025: MasterBrand and American Woodmark announced an all-stock merger, creating a leading cabinetry company with combined scale, complementary brands, and expected cost synergies of USD 90 million annually, strengthening market reach and operational efficiency.

- January 2025: Austrian retailer XXXLutz acquired approximately 140 furniture stores from the Porta Group across Germany, the Czech Republic, and Slovakia, expanding its footprint and reinforcing its omnichannel retail strategy in key European markets.

- January 2025: American Woodmark Corporation announced the closure of its Dallas, TX, distribution facility and Orange, VA, manufacturing plant, recognizing USD 4.6 million in restructuring charges to align with forecasted demand.

Global Kitchen Furniture And Fixtures Market Report Scope

The kitchen furniture and fixtures market refers to the industry that designs, manufactures, and sells products related to the kitchen, including cabinets, countertops, sinks, faucets, and other fixtures. The report covers a complete background analysis of the kitchen furniture and fixtures market. It includes a parental market assessment, emerging trends by segments and regional markets, significant changes in market dynamics, and a market overview.

The Kitchen Furniture And Fixtures Market Is Segmented By Type (Kitchen Furniture And Kitchen Fixtures), End User (Household And Commercial), And Geography (North America, South America, Asia-Pacific, Middle East & Africa, And Europe). The Report Offers The Market Sizes And Forecasts In Value (USD) For All The Above Segments.

| Cabinets (Base, Wall , Tall/Pantry) |

| Countertop |

| Drawer Units & Organizers |

| Backsplashes & Panels |

| Shelving & Storage Units (Open Shelves, Closed Storage Units, Corner Units) |

| Kitchen Islands (Fixed, Mobile, Multi-functional) |

| Fixtures (Sinks, Faucets, Lighting Fixtures) |

| Hardware & Accessories (Handles & Knobs, Hinges, Drawer Slides, Pull-out Systems, Racks) |

| Others (Waste Bins, Modular Inserts, Soft-close Systems) |

| Wood (Solid,Engineered,Bamboo / Reclaimed) |

| Metal (Stainless Steel, Aluminum) |

| Plastic & Laminates |

| Glass & Ceramics |

| Composites |

| Residential |

| Commercial |

| Offline |

| Specialty Stores & Showrooms |

| Home-Improvement / DIY Chains |

| Furniture Retailers |

| Builders / Contractors |

| Online |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Cabinets (Base, Wall , Tall/Pantry) | |

| Countertop | ||

| Drawer Units & Organizers | ||

| Backsplashes & Panels | ||

| Shelving & Storage Units (Open Shelves, Closed Storage Units, Corner Units) | ||

| Kitchen Islands (Fixed, Mobile, Multi-functional) | ||

| Fixtures (Sinks, Faucets, Lighting Fixtures) | ||

| Hardware & Accessories (Handles & Knobs, Hinges, Drawer Slides, Pull-out Systems, Racks) | ||

| Others (Waste Bins, Modular Inserts, Soft-close Systems) | ||

| By Material | Wood (Solid,Engineered,Bamboo / Reclaimed) | |

| Metal (Stainless Steel, Aluminum) | ||

| Plastic & Laminates | ||

| Glass & Ceramics | ||

| Composites | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | Offline | |

| Specialty Stores & Showrooms | ||

| Home-Improvement / DIY Chains | ||

| Furniture Retailers | ||

| Builders / Contractors | ||

| Online | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the kitchen furniture and fixtures market size and growth outlook through 2031?

The kitchen furniture and fixtures market size is estimated at USD 182.70 billion in 2026 and is projected to reach USD 213.16 billion by 2031 at a 3.13% CAGR, reflecting a mature category shaped by modular adoption and commercial standardization.

Which product categories are leading the growth in global kitchen programs?

Cabinets lead revenue with a 45.73% share in 2025, while kitchen islands record the fastest growth at a 3.81% CAGR through 2031 as open-plan layouts and multiuse work zones drive larger, feature-rich islands.

How is the channel mix evolving for kitchen furniture and fixtures?

Offline channels still dominate with a 76.68% share in 2025 because showroom consultation and installation coordination are critical, while online is the fastest-growing at a 4.54% CAGR through 2031 due to visualization tools and direct-to-consumer models.

What end-user segment contributes most to global demand?

Residential accounted for 74.67% of demand in 2025 due to ongoing upgrade cycles and aging housing stock, while commercial leads on growth with a 4.12% CAGR through 2031 tied to hospitality and multi-family programs.

Which regions are shaping demand dynamics?

North America contributed the largest share at 32.41% in 2025 on remodeling strength, while Asia-Pacific shows the fastest growth at 4.91% through 2031 on urbanization and builder-standard modular formats.

Page last updated on: