Automated Blinds and Shades Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

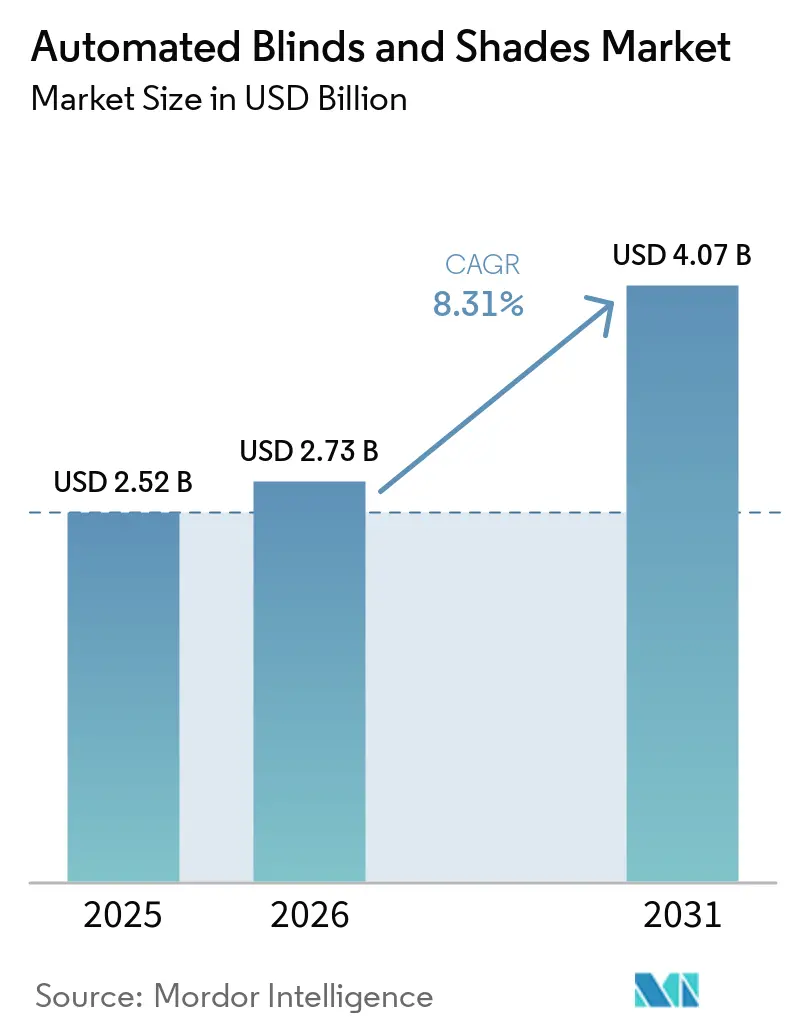

| Market Size (2026) | USD 2.73 Billion |

| Market Size (2031) | USD 4.07 Billion |

| Growth Rate (2026 - 2031) | 8.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automated Blinds and Shades Market Analysis by Mordor Intelligence

The Global automated blinds and shades market size was valued at USD 2.52 billion in 2025 and estimated to grow from USD 2.73 billion in 2026 to reach USD 4.07 billion by 2031, at a CAGR of 8.31% during the forecast period (2026-2031). This brisk expansion is underpinned by building-energy regulations that now embed automatic daylight controls in code, declining IoT motor costs, and smart-home adoption that has left the experimental stage and entered mainstream renovation budgets. California’s Title 24, the 2024 International Energy Conservation Code (IECC), and federal rules under 10 CFR Part 434 collectively ensure that every newly erected or deeply retrofitted building in key regions must include intelligent shading. Parallel demographic trends—especially a growing cohort of older homeowners determined to age in place—are steering demand toward touch-free, voice-activated window coverings. These forces, together with hotel chains’ post-COVID preference for contactless guest rooms and the White House-backed push for domestic semiconductor output, give the automated blinds and shades market durable tailwinds.

Key Report Takeaways

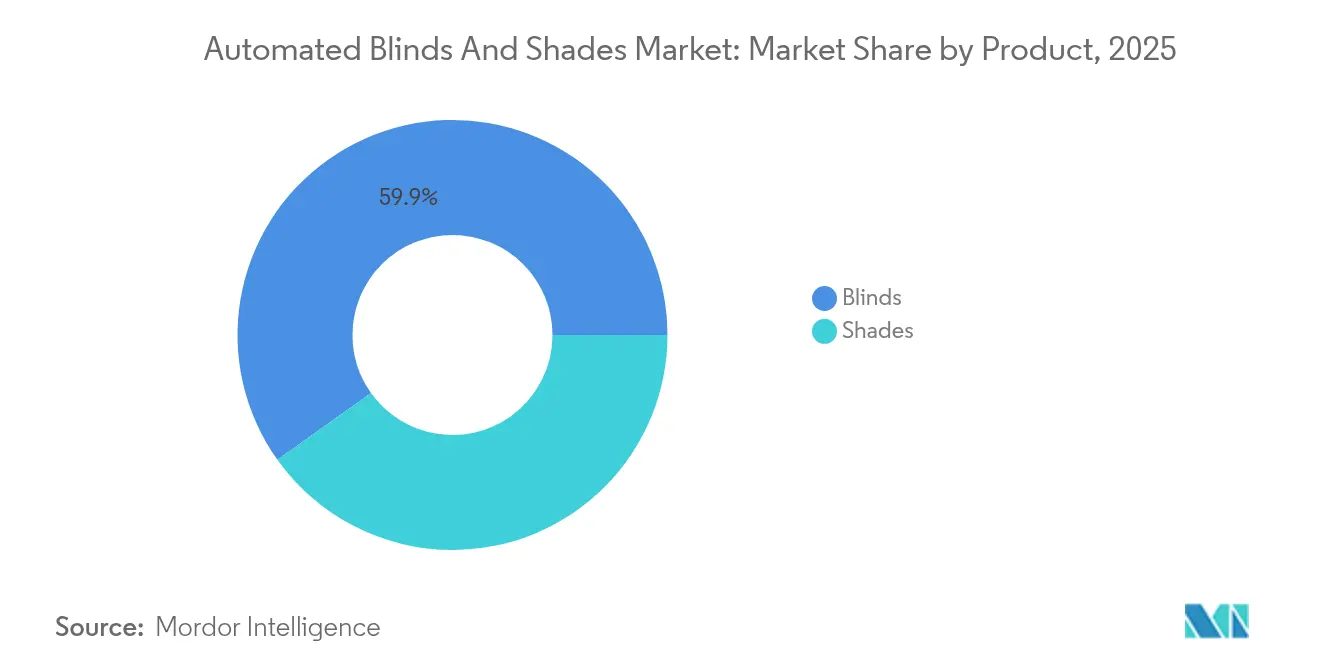

- By product, blinds led with 59.85% revenue share in 2025, while shades are projected to expand at a 8.98% CAGR through 2031.

- By control type, motorized systems held 69.90% of the automated blinds and shades market share in 2025; smart-enabled products are set to grow at an 10.72% CAGR to 2031.

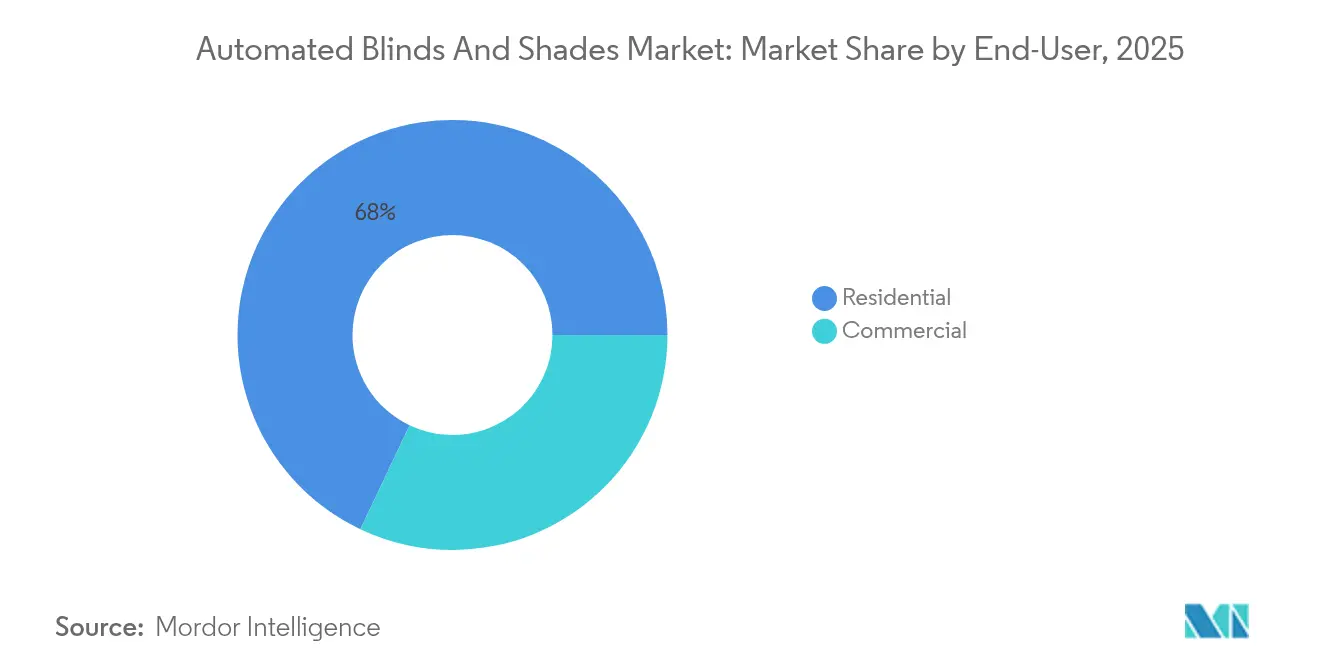

- By end-user, residential applications accounted for 67.95% share of the automated blinds and shades market size in 2025, while commercial segments are moving ahead at a 10.25% CAGR through 2031.

- By distribution channel, B2C retail commanded 71.80% share of the automated blinds and shades market size in 2025; B2B direct sales are positioned to rise at a 9.62% CAGR over the same horizon.

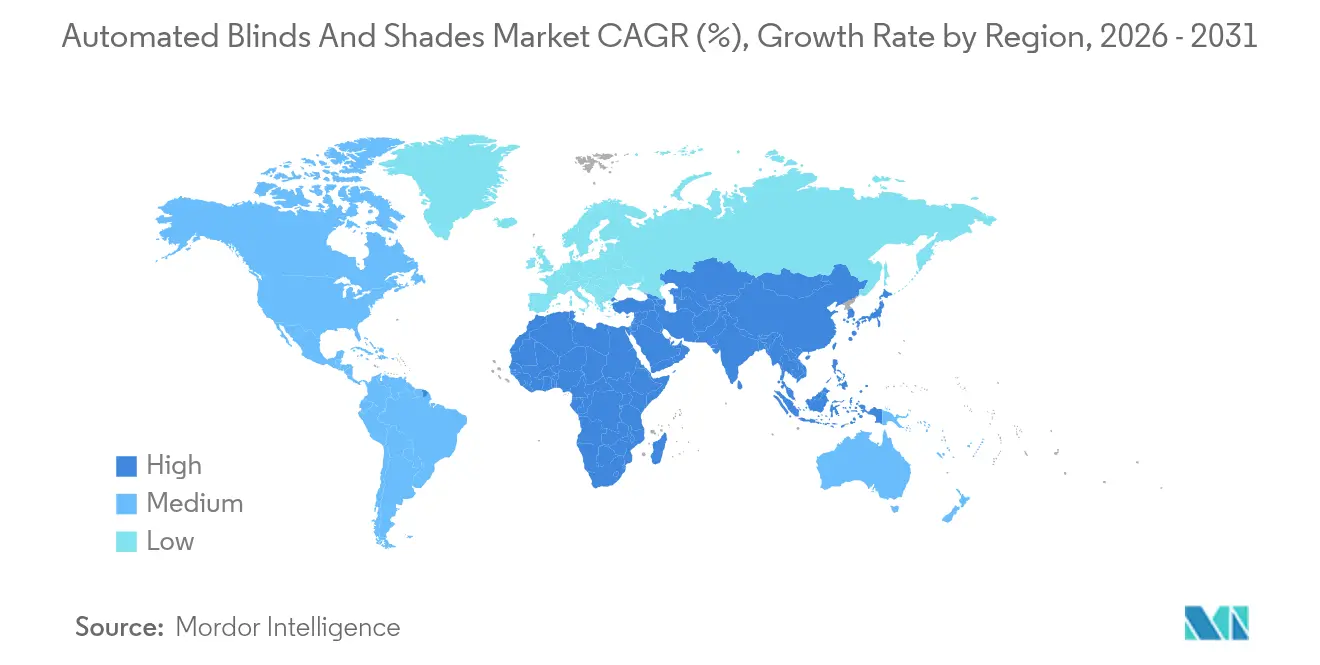

- By geography, North America captured 38.55% revenue share in 2025, whereas Asia-Pacific is forecast to post a 9.18% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automated Blinds and Shades Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-home penetration surge | +2.8% | Global, with North America & Europe leading adoption | Medium term (2-4 years) |

| Energy-efficiency regulations on glazing & façades | +2.1% | North America & EU core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Cost decline of IoT motors & batteries | +1.9% | Global manufacturing, cost benefits in Asia-Pacific first | Short term (≤ 2 years) |

| Aging-in-place retrofits demand touch-free shading | +1.4% | North America & Europe, with Japan leading Asia-Pacific | Medium term (2-4 years) |

| Daylight-harvesting mandates in green-building codes | +1.2% | North America & Europe regulatory frameworks | Long term (≥ 4 years) |

| Hospitality push for contact-free guest rooms post-COVID | +0.9% | Global hospitality hubs, concentrated in urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Energy-Efficiency Regulations on Glazing & Façades

The 2024 IECC trimmed allowable U-factors and mandated automatic daylight controls in commercial zones, channeling non-discretionary budgets toward intelligent shading hardware. Title 24 stipulates Net-Zero Energy performance in California residential construction, effectively guaranteeing automated daylight harvesting on every new build. Federal facilities must meet 10 CFR Part 434, a rule set expanded in 2025 to cover leased buildings, magnifying public-sector opportunity. In Europe, ASHRAE/IES 90.1-2022 underpins nine-percent site-energy cuts largely attributed to automated glare mitigation, and similar directives are surfacing in Asia-Pacific capitals. These codes decouple demand from macro construction cycles and protect the automated blinds and shades market against short-term real-estate slowdowns[1]U.S. Department of Energy, “Benefits Analysis of ASHRAE/IES Standard 90.1-2022,” energy.gov .

Cost Decline of IoT Motors & Batteries

Volume silicon production and refined motor winding processes have carved double-digit costs out of brushless DC drives since 2022. Lithium battery densification allows two-to-three-year service intervals, reducing homeowner maintenance anxiety. Somfy’s Sonesse 40 PoE motor bypasses separate power wiring altogether, simplifying installation and trimming labor hours by up to 18%[2]Hunter Douglas, “PowerView Integration Partners List,” hunterdouglas.com . Meanwhile, the CHIPS and Science Act is steering USD 39 billion into domestic fabs that will mitigate semiconductor shortages by 2027, smoothing component supply and preserving margin headroom for manufacturers in the automated blinds and shades market.

Aging-In-Place Retrofits Demanding Touch-Free Shading

Nearly 80% of adults over 65 reside in existing homes, and arthritis prevalence nudges many to seek voice or phone-operated shades rather than manual pulls. Medicare-adjacent funding pilots rolled out in 2025 now treat automated blinds as a qualified home-modification device in nine U.S. states, shaving up-front costs for seniors. Japanese municipalities fund similar installs under long-term-care insurance, turning metropolitan Tokyo into a hotspot for accessible shading projects. AI-driven timers that predict glare from local weather APIs minimize user input, easing tech apprehension among the elderly. Retrofit momentum in this segment alone adds a steady baseline to the automated blinds and shades market demand.

Smart-Home Penetration Surge

Spiking smart-device adoption has moved intelligent window coverings from a premium niche to a mainstream necessity. Interoperability breakthroughs such as the Matter protocol finally let automated shades converse with lighting, HVAC, and security platforms without proprietary bridges, unclogging a long-standing adoption bottleneck. Energy dashboards in consumer apps now calculate kilowatt-hour savings derived from scheduled shading, reinforcing perceived value and shortening payback periods for homeowners. Voice control, once a novelty, is the default interaction model for persons with mobility constraints, helping contractors upsell from manual to automated blinds and shades market solutions. Global smart-home revenue that crossed USD 200 billion in 2024 provides a wide funnel for future shade-automation retrofits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront installation cost | -1.8% | Global, particularly impacting price-sensitive segments | Short term (≤ 2 years) |

| Motor & chip supply-chain volatility | -1.4% | Global manufacturing, concentrated in Asia-Pacific supply chains | Short term (≤ 2 years) |

| Inter-brand interoperability gaps | -1.2% | Global, with fragmented standards adoption | Medium term (2-4 years) |

| Cybersecurity and data privacy concerns | -0.9% | North America & EU regulatory focus, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Installation Cost

Hardware prices have fallen, yet a professional install still commands a 15-25% labor premium, making do-it-yourself aspirants think twice. Retrofit jobs in existing masonry often require conduit routing or battery replacements in inaccessible clerestory windows, pushing total invoices beyond comfort levels for cost-conscious buyers. Commercial budgets also face capital-allocation scrutiny when juxtaposing shading automation against HVAC upgrades. Utility rebates exist but remain patchy, with only 27 U.S. investor-owned utilities offering incentive programs in 2025. Until financing products normalize, cost friction will shave points off the automated blinds and shades market growth, particularly in emerging economies.

Inter-Brand Interoperability Gaps

Matter has solved discovery and authentication, but legacy Zigbee, Z-Wave, and proprietary RF ecosystems still dominate installed bases, forcing dual-stack gateways or wholesale replacement. Integrators routinely charge extra design hours to reconcile disparate protocols, a burden felt most acutely in mid-market multifamily projects. Hospitality chains rolling out brand-standard control apps must vet each shading vendor’s API security posture, prolonging procurement cycles. Full convergence will require another hardware refresh, likely coinciding with the 2028 Matter specification. Until then, protocol gridlock restrains the automated blinds and shades market from achieving frictionless plug-and-play status.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Blinds Maintain Dominance Through Innovation

Blinds held 59.85% revenue in 2025, giving them the commanding height within the automated blinds and shades market. Venetian formats benefit from incremental slat-tilt motor design that offers fine lumen control, vital for open-plan offices pursuing glare-free laptop environments. Roller variants capitalize on minimalist aesthetics prized by modern architects, while vertical blinds remain indispensable for expansive glazing in convention centers. Over the forecast, wood and faux-wood models are expected to migrate to recycled composites, a shift that pairs sustainability credentials with resistance to warping.

Shades, advancing at a 8.98% CAGR, are pulling spend away from blinds in thermally demanding zones. Cellular (honeycomb) constructions can cut heat gain by up to 46%, a metric now embedded in many U.S. utility rebate calculators. Roman and pleated silhouettes dovetail with luxury residential interiors, prompting premium positioning by top brands. Manufacturers bundle these styles with ultra-quiet micro-motors that operate at sub-35 dB, satisfying noise-sensitive hospital patient rooms. Among specialty models, light-transmitting but opaque fabrics meet WELL Building Standard glare criteria, broadening shade appeal in commercial retrofits.

By Control Type: Smart Systems Drive Future Growth

Motorized devices remain the mass-market workhorse, representing 69.90% of 2025 spend. They suit spec-grade apartment blocks that need reliable motion but not full cloud integration, and their installers value stable RS-485 or dry-contact wiring that aligns with existing building automation systems. Battery-powered versions particularly thrive in retrofit skylights where rewiring would breach vapor barriers.

Smart-enabled lines, rising at 10.72% CAGR, splice Wi-Fi, Thread, or Matter chips directly into the headrail. Facility managers accessing dashboards such as Somfy SDN Connect gain motor-health telemetry, which cuts downtime and service calls. Voice-assistant compatibility is now a table-stakes, with 78% of U.S. smart-speaker households having issued at least one shading command in 2024. Predictive algorithms tethered to weather forecasts adopt a pre-emptive stance, lowering shades ahead of afternoon heat spikes and trimming HVAC usage. This closed-loop automation underscores why connected products will keep enlarging their automated blinds and shades market footprint.

By End-User: Commercial Acceleration Challenges Residential Dominance

Residential owners generated 67.95% of 2025 revenue, cementing the category’s historic priority in the automated blinds and shades market. Single-family dwellings account for most installations because electrical layouts can be tailored during remodeling. Condominium retrofits are catching up; property managers now specify low-profile battery packs that slide behind valances, avoiding homeowners-association electrical approvals. Aging residents appreciate voice control that lets them change daylight levels without reaching cords, boosting safety and independence.

Commercial adoption, pacing at 10.25% CAGR, is reshaping vendor sales funnels. Hotels integrating contact-free guest-room packages bundle motorized drapery, smart thermostats, and occupancy sensors to reassure hygiene-minded travelers. Office landlords, squeezed by hybrid-work vacancies, use dynamic shading to elevate tenant experience and cut operating expenses, marketing certified energy savings to eco-conscious lessees. Healthcare facilities employ touch-free shades as part of infection-control regimes, reducing high-touch surfaces in surgical and isolation wards. Retail and educational segments round out demand as code-mandated daylight harvesting becomes ubiquitous.

By Distribution Channel: B2B Growth Reflects Commercial Momentum

B2C retail outlets rang up 71.80% of 2025 sales, driven by in-store demonstrations that let shoppers experience motor speed and fabric opacity firsthand. Specialty showrooms leverage augmented-reality apps to preview shade colors on a customer’s phone, easing choice anxiety. Online platforms have scaled virtual consultations but remain confined to standard window dimensions, limiting full e-commerce penetration.

B2B direct sales, forecast to climb 9.62% annually, mirror the commercial upshift in the automated blinds and shades market. Architects value early-stage engineering support, and contractors prefer consolidated warranties when integrating shades with controls. Vendor-hosted configurators now export BIM objects that drop into Revit models, accelerating approval cycles. Direct channels also accommodate millimeter-perfect custom sizes necessary for curtain walls, an advantage mass retail cannot replicate.

Geography Analysis

North America, holding 38.55% of 2025 revenue, sits at the intersection of mature smart-home adoption and the continent’s tightest energy codes. California’s Title 24 revision and Canada’s National Energy Code for Buildings each force automated daylight control into mainstream building budgets. The United States additionally benefits from the Inflation Reduction Act tax credits that reimburse up to 30% of installed shading systems when part of a whole-home energy upgrade, cushioning payback concerns. Contractors, however, must navigate high union labor costs that can extend project ROI timelines.

Asia-Pacific is the growth pacesetter with a 9.18% CAGR, propelled by urban megaprojects in China and India, where curtain-wall façades dominate skylines. Beijing’s dual-carbon target has birthed provincial incentives that cover 15% of intelligent façade costs, driving adoption among Grade-A office developers. India’s Smart Cities Mission added daylight-responsive shades to its 2025 tender specifications, fortifying municipal demand. Japan registers high penetration in elder-care retrofits, and Southeast Asia’s hospitality boom, especially in Singapore and Bangkok, pulls large lots of motorized drapery into four- and five-star hotels.

Europe enjoys steady replacement demand anchored in renovation waves funded by the EU’s “Fit for 55” program. Germany leads with KfW low-interest loans that reward energy-efficient retrofits, while France’s RE2020 building regulation tightens solar-heat-gain coefficients, nudging developers toward advanced shading. Nordic countries champion motorized blackout fabrics that mitigate extremes of midnight sun and polar night, whereas Mediterranean states emphasize reflective blinds to block peak-season insolation. Post-Brexit United Kingdom must juggle divergence from EU codes and alignment with net-zero commitments, yet premium consumer tastes keep average selling prices high.

Competitive Landscape

Market concentration is moderate, with a nucleus of global brands surrounded by regional specialists. Hunter Douglas exploits its PowerView platform to integrate shades with over 30 third-party control ecosystems, maintaining a first-mover advantage[3]Somfy Systems, “Sonesse 40 PoE Technical Sheet,” somfysystems.com. Somfy guards more than 2,000 patents and deploys 500 R&D engineers, allowing annual motor refresh cycles that outpace smaller rivals. Lutron’s co-optimization of lighting and shading yields bundled efficiency gains prized in LEED Platinum pursuits. Continental European firms like Griesser and Warema tailor products to local climatic nuances, striking distribution deals to penetrate cross-border markets.

Innovation revolves around quieter motors, sustainability, and open-protocol connectivity. Fabrics spun from recycled ocean plastics now carry Environmental Product Declarations, catering to green building certifications. Manufacturers embed tiny ambient-light sensors into bottom rails, removing the need for wall-mounted photocells and slashing commissioning time. AI and machine learning enter predictive maintenance dashboards that flag torque anomalies before motor failure, appealing to facility-management outsourcing firms.

Supply chain resilience is an emerging battlefield. Brands diversify contract assemblers beyond Shenzhen, opening new capacity in Mexico and Eastern Europe to hedge geopolitical risks. The U.S. CHIPS and Science Act encourages localization of critical microcontrollers, aligning with corporate ESG narratives on transparency. Midsize players acquire software firms to shorten development cycles for app-based controls, while global leaders scout battery-technology startups to extend cycle life. These maneuvers collectively intensify competition yet preserve healthy differentiation across price tiers.

Automated Blinds and Shades Industry Leaders

Hunter Douglas NV

Springs Window Fashions, LLC

Somfy Systems S.A.

Lutron Electronics Co., Inc.

Legrand S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Legrand reported Q3 2024 net sales of EUR 6,229 million with emphasis on building-automation product lines.

- October 2024: Hunter Douglas expanded PowerView automation with new motorized drapery hardware, broadening design options for integrators.

- August 2024: Resideo Technologies completed the acquisition of Snap One, reinforcing its distribution clout in connected-home automation.

- June 2024: Hunter Douglas introduced the Custom Integrator Program to streamline smart-shade installation with AV control systems.

Global Automated Blinds and Shades Market Report Scope

The Blinds and Shades Market covers various residential, commercial, and industrial window coverings. The market boasts a wide selection of products, including vertical blinds, roller blinds, Roman shades, Venetian blinds, and advanced smart blinds, which can be controlled manually or via automated systems. The Automated Blinds and Shades Market is segmented by product, fabric, end-user, application, distribution channel, and geography. By Product, the market is segmented into fully automatic and semi-automatic. By end-user, the market is segmented into residential and commercial. By distribution channel, the market is segmented into online and offline. And by geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report offers the market size in value terms in USD for all the above-mentioned segments.

| Blinds | Venetian |

| Vertical | |

| Roller | |

| Others | |

| Shades | Cellular |

| Roman | |

| Pleated | |

| Others |

| Motorized |

| Smart |

| Residential | |

| Commercial | Hospitality |

| Offices | |

| Healthcare | |

| Other Commercial End-Users |

| B2C / Retail Channels | Multi-Brand Stores |

| Specialty Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Directly From Manufacturers |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest Of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, And Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, And Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, And Philippines) | |

| Rest Of Asia-Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest Of Middle East And Africa |

| By Product | Blinds | Venetian |

| Vertical | ||

| Roller | ||

| Others | ||

| Shades | Cellular | |

| Roman | ||

| Pleated | ||

| Others | ||

| By Control Type | Motorized | |

| Smart | ||

| By End-User | Residential | |

| Commercial | Hospitality | |

| Offices | ||

| Healthcare | ||

| Other Commercial End-Users | ||

| By Distribution Channel | B2C / Retail Channels | Multi-Brand Stores |

| Specialty Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Directly From Manufacturers | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest Of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, And Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, And Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, And Philippines) | ||

| Rest Of Asia-Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest Of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current value of the automated blinds and shades market?

The automated blinds and shades market stands at USD 2.73 billion in 2026 and is on track to reach USD 4.07 billion by 2031.

Which product category dominates the automated blinds and shades market?

Blinds remain ahead, accounting for 59.85% of 2025 revenue, although shades are growing faster at a 8.98% CAGR.

Why is Asia-Pacific the fastest-growing region?

Rapid urbanization, supportive government energy policies, and a booming hospitality sector drive the region’s 9.18% CAGR through 2031.

How do energy-efficiency regulations influence market demand?

Mandatory daylight-control provisions in the 2024 IECC, Title 24, and similar codes make automated shading a compliance requirement, insulating demand from construction cycles.

Page last updated on: