Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 35.37 Billion |

| Market Size (2031) | USD 46.29 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

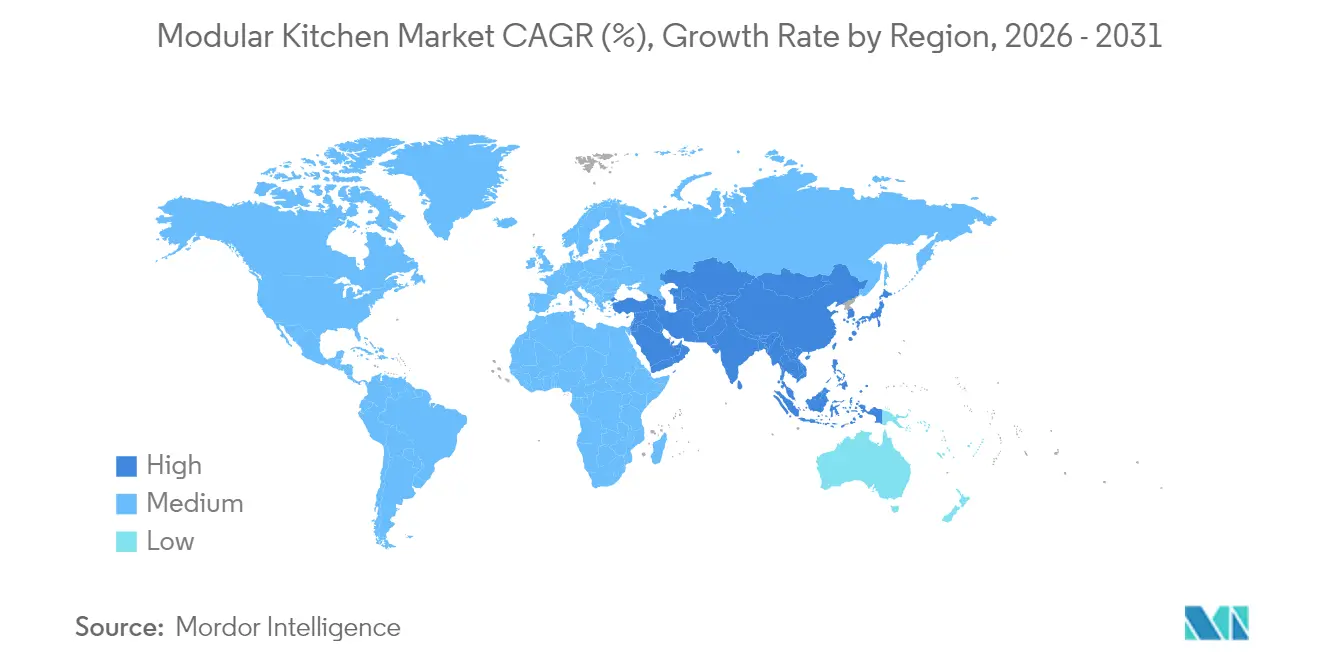

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

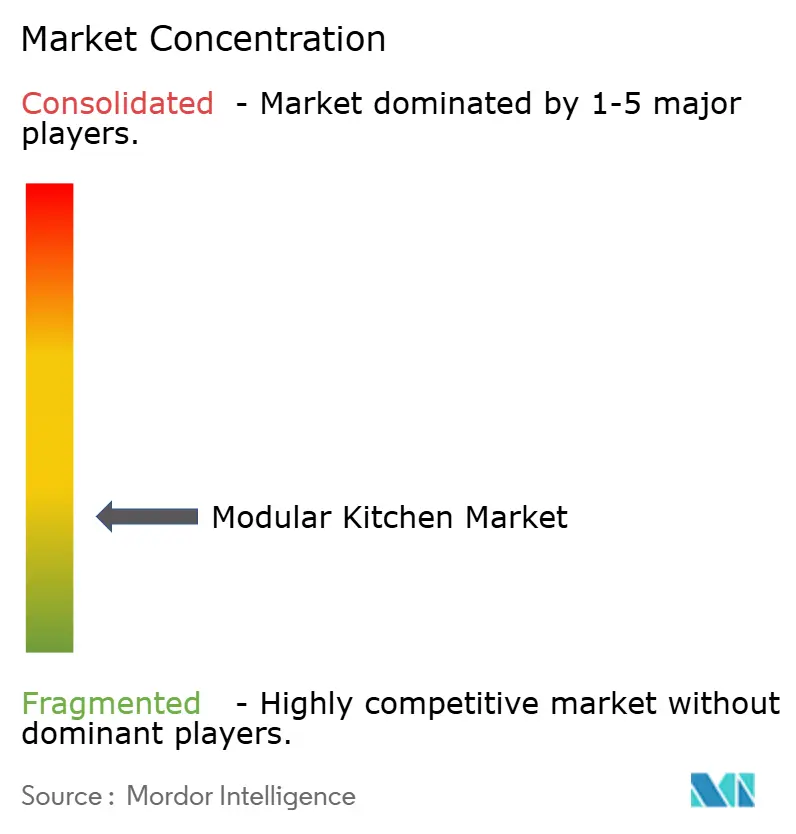

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Modular Kitchen Market Analysis by Mordor Intelligence

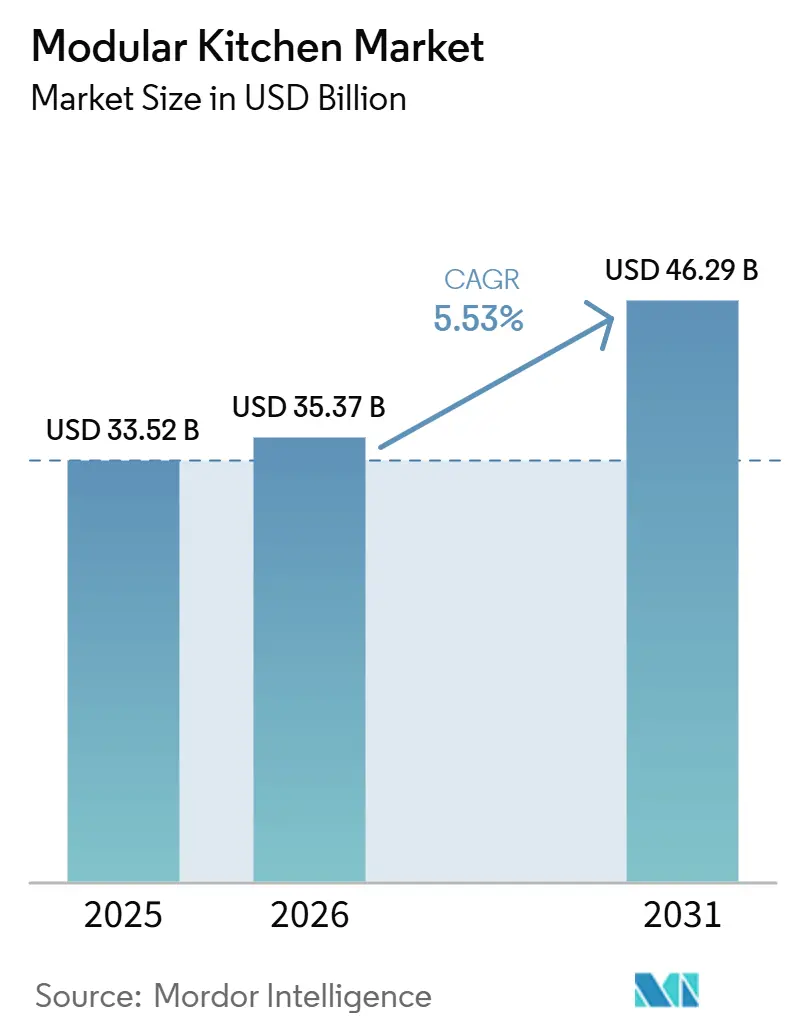

The Modular Kitchen Market size is expected to grow from USD 33.52 billion in 2025 to USD 35.37 billion in 2026 and is forecast to reach USD 46.29 billion by 2031 at 5.53% CAGR over 2026-2031.

Urbanization is compressing living spaces and pushing households toward modular solutions that optimize every square foot while maintaining visual appeal. Rising renovation budgets in post-pandemic economies, the growing role of e-commerce in design-to-delivery, and consumer insistence on certified sustainable materials are expanding addressable demand across income tiers. Competitive intensity is increasing as digital-native entrants challenge established brands on speed, price transparency, and online visualization tools. Manufacturers are turning to smart components, flexible sourcing, and installer partnerships to protect margins and ensure consistent service quality.

Key Report Takeaways

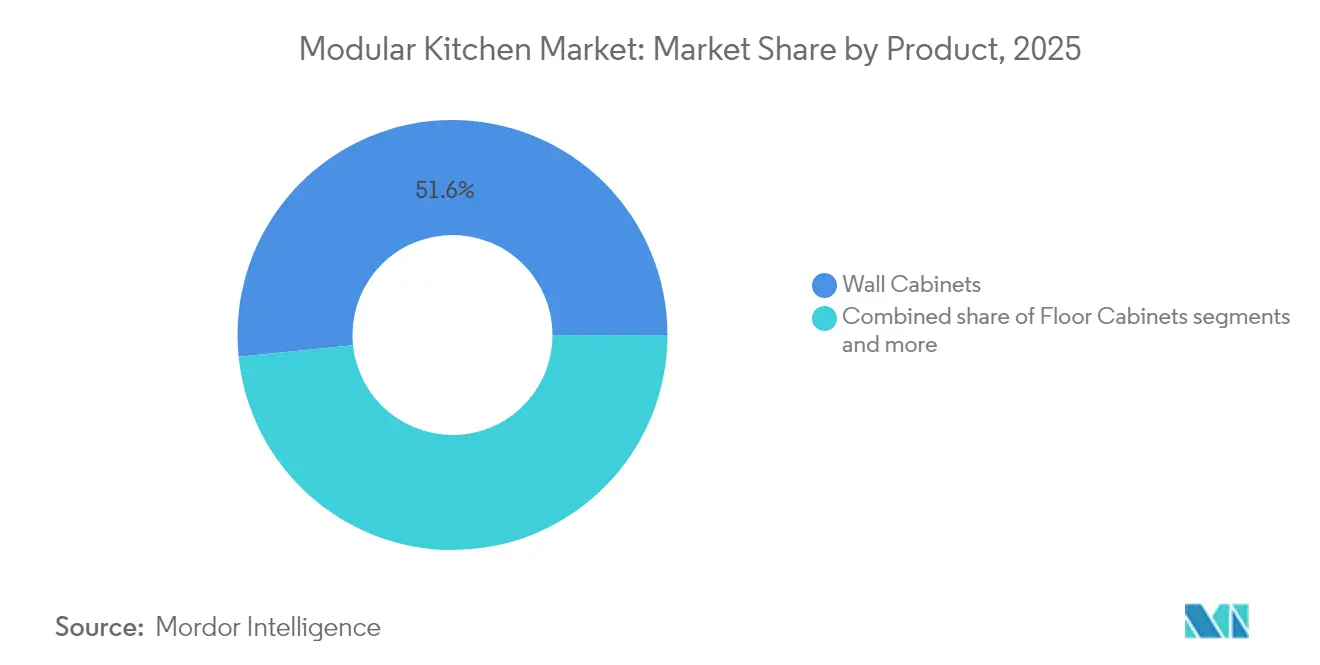

- By product, wall cabinets led with 51.62% of the modular kitchen market share in 2025; other cabinets are projected to post a 6.24% CAGR through 2031.

- By design layout, L-shaped configurations held 33.40% revenue share in 2025, while parallel or galley formats are set to expand at a 6.40% CAGR to 2031.

- By material, wood accounted for 59.20% of the modular kitchen market size in 2025, whereas fiber/plastic composites are advancing at a 6.02% CAGR.

- By price range, the mid-range tier captured 49.10% of 2025 revenues; the economy tier is forecast to grow the fastest at 5.93% CAGR.

- By end user, residential installations represented 69.35% of the market in 2025 and are rising at a 5.72% CAGR through 2031.

- By distribution channel, B2C and retail outlets commanded 59.40% of 2025 revenues, with the B2C online sub-segment climbing at a 5.62% CAGR.

- By geography, Europe secured 32.70% of global revenues in 2025, while Asia-Pacific is projected to deliver a 6.70% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Modular Kitchen Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization and smaller households | +1.2% | Asia-Pacific, Europe, Latin America | Long term (≥ 4 years) |

| Post-pandemic home-renovation spend | +0.9% | North America, Europe, and affluent Asia-Pacific | Medium term (2–4 years) |

| E-commerce design-to-delivery platforms | +0.8% | Global | Medium term (2–4 years) |

| Shift to eco-friendly certified materials | +0.7% | Europe, North America, Japan, South Korea | Long term (≥ 4 years) |

| Rapid Expansion of Affordable Housing Projects Across Emerging & Developed Regions | +0.6% | Asia-Pacific (particularly India, China), Middle East, and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urbanization and Smaller Household Sizes Fueling Demand for Space-Efficient Kitchens

Urban living now anchors demographic growth, and shrinking apartment footprints are forcing consumers to prioritize functionality. In emerging markets like India, where urbanization is occurring at 2.3% annually, the impact is proportionally higher. India illustrates the trend, with its modular kitchen market expanding at more than 20% each year on rising condominium supply and aspirational spending. In contrast, European cities echo the shift, where strict space codes favor modular overheads and corner systems that minimize workflow obstruction. Product design now centers on ergonomic reach zones and slim appliances that reduce aisle widths without sacrificing performance. Manufacturers competing in these dense markets are bundling installation plans with space audits, giving buyers confidence that every cubic inch is fully optimized.

Surging Global Home-Renovation Spend in the Post-Pandemic Era

Kitchen upgrades absorb the largest share of today’s renovation budgets as households reassess interiors for work, learning, and dining. Houzz reports that the median outlay for a major U.S. kitchen revamp climbed 22% to USD 55,000 in 2024; 42% of owners cited aesthetics and 35% cited functionality as the main goal. Consumers perceive modular systems as investments that lift resale value and allow phased upgrades over several years. Design catalogs increasingly spotlight reconfigurable carcasses, enabling homeowners to expand storage or add smart appliances without discarding earlier units. Financing programs offered by retailers in mature markets cover nearly half of installations, smoothing large ticket purchases and supporting wider adoption of premium hardware.

E-Commerce Design-to-Delivery Platforms Accelerating Adoption

Digital channels now compress the design cycle from weeks to days through 3D configurators, augmented-reality previews, and transparent pricing. Buyers can visualize finishes in situ, approve shop drawings online, and schedule installation from a single portal, eliminating multiple showroom visits. While offline showrooms still dominate conversion, customers started their journey online, and people use AR apps to simulate configurations at home. Manufacturers that combine online visualization with last-mile assembly teams report faster decision times and lower return rates. As e-commerce penetrates tier-2 cities in Asia-Pacific and Latin America, direct-to-consumer platforms are enabling smaller factories to bypass wholesale networks and reach new households with competitively priced packages.

Consumer Shift Toward Certified Eco-Friendly Materials and Circular Designs

Environmental scrutiny is driving material innovation. Certified sustainable modular kitchens outgrew the overall market by a factor of five in 2024 as recycled glass, bamboo, and reclaimed timber moved from niche to mainstream. European regulations favoring circular construction have accelerated the shift, and the price premium paid for eco labels has narrowed to 8% from 15% two years earlier. Suppliers now publish lifecycle assessments and carbon footprints alongside finish catalogs, giving architects verifiable data for green-building certifications. As supply chain transparency becomes an expectation, brands that can trace raw wood to responsibly managed forests or show closed-loop recycling of composite boards are capturing mindshare and improving channel margins.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front cost versus traditional carpentry | -0.4% | Asia-Pacific, Latin America, Africa | Medium term (2–4 years) |

| Raw-material cost volatility | -0.3% | Global | Short term (≤ 2 years) |

| Shortage of Skilled Modular Installers & Lack of Universal Installation Codes | -0.2% | Global, most acute in rapidly growing markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Costs versus Traditional Carpentry in Price-Sensitive Markets

In regions with low labor rates, custom carpentry undercuts modular kitchens by as much as 40%, discouraging adoption among middle-income households. Only 15% of modular buyers in emerging economies have access to installment financing, compared with 45% in developed markets, widening the affordability gap. Although lifetime ownership costs often favor modular solutions through reduced maintenance and higher resale values, this benefit is not always clear to first-time buyers. Manufacturers are mitigating the hurdle with starter lines that use standardized modules, laminate finishes, and pared-back hardware, cutting entry prices by roughly 15% since 2023. Leasing options for developers and step-up upgrade paths are also emerging to distribute costs over time.

Raw-Material Cost Volatility Disrupting Global Supply Chains

Premium hardwood prices jumped 18% in 2024, forcing producers to raise list prices or compress margins. Shipping delays and container shortages compound the challenge, extending lead times and elevating inventory needs. Imports account for a significant share of higher-grade veneer and hardware in several markets, making local assemblers vulnerable to currency swings. Manufacturers are countering volatility through long-term supply contracts, diversification into engineered boards, and in-house lamination that substitutes scarce veneers. Some have shifted to mixed-material approaches—combining solid fronts with engineered carcasses—to stabilize costs while retaining perceived quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wall Cabinets Anchor Storage Efficiency

Wall cabinets held 51.62% of 2025 revenues, confirming their status as the most visible element of modern kitchen compositions. Glass-fronted and illuminated variants fetch up to 40% premiums, particularly in Europe and North America, where open-plan living exposes cabinetry to adjacent spaces. The modular kitchen market size for wall cabinets is forecast to climb steadily as manufacturers introduce height-adjustable suspension systems and deep-frame designs that integrate small appliances behind lift-up fronts. Floor cabinets remain essential for heavy cookware, yet have plateaued in share given consumers’ preference for eye-level access. Specialty towers, pantry pull-outs, and appliance garages—grouped as other cabinets—are on track for a 6.24% CAGR through 2031 as households demand purpose-built zones for everything from bulk groceries to countertop gadgets.

Investment in soft-close hinges, push-to-open latches, and factory-fitted LED strips is moving from premium to baseline expectation. Smart modules equipped with humidity sensors and voice-activated lighting are in pilot production, allowing brands to differentiate beyond finishes. Compatibility across cabinet families now drives repeat purchases; homeowners can add matching towers years later without color mismatches, reinforcing customer loyalty and smoothing revenue cycles for manufacturers.

By Design Layout: Configuration Choices Reflect Spatial Realities

L-shaped kitchens accounted for 33.40% of global installations in 2025, due to their adaptable workflow triangle and suitability for both closed and semi-open rooms. Parallel or galley arrangements deliver the fastest projected growth at 6.40% CAGR as condo dwellers in urban cores maximize narrow footprints. A modular kitchen market share analysis shows L-shapes still dominate in detached homes, whereas galley formats are winning studios and rental units where every inch counts. U-shaped layouts appeal to enthusiastic cooks who prioritize expansive prep surfaces, while straight one-wall configurations meet the needs of secondary units and serviced apartments.

The surge in galley popularity is nudging manufacturers to design slimmer countertops and front-venting cooktops that save aisle width. Integrated toe-kick drawers and pull-out spice racks make tight corridors more functional. As social cooking rises, designers are rethinking the classic work triangle, opting for parallel stations that let multiple users cook simultaneously without collision.

By Material: Wood Leads as Composites Gain Ground

Wood maintained 59.20% of 2025 revenues, favored for its tactile warmth and broad finish palette. Yet, sustainability pressure and moisture performance are steering many buyers toward fiber or plastic composites, which promise dimensional stability and low upkeep. Composites are projected to advance at 6.02% CAGR through 2031, aided by digital printing that convincingly replicates grain patterns. Metal retains a niche role in professional-style settings, prized for hygiene and temperature resilience.

Recycled content is gaining contractual preference in public projects, and water-resistant medium-density fiberboard is extending engineered panels into sink zones once reserved for plywood. Hybrid carcasses—solid wood doors mounted on composite boxes—balance premium aesthetics with cost control. Bamboo, which reaches maturity in five years, now appears in entry-level lines and eco collections alike, underscoring how material choices are evolving under supply chain uncertainty and green-building mandates.

By Price Range: Mid-Range Captures Value Seekers

The mid-range tier attracted 49.10% of 2025 spending, offering an accessible mix of factory precision and customizable accents. Mobility in this tier is rising as brands offer semi-custom dimensions, multiple choices, and soft-close hardware without luxury surcharges. Entry-level collections trimmed costs by limiting door colours and standardizing carcass depths, setting the stage for a 5.93% CAGR in the economy segment. Premium lines, while still niche in volume, set design direction and technological benchmarks later adopted downstream.

Manufacturers are responding to entry-level growth with mass-personalization models: a core cabinet catalog, optional door styles, and modular inserts that buyers can add over time. This framework reduces inventory risk, supports faster delivery, and allows households to stage investments across renovation phases. In the high end, the definition of luxury shifts from ornate fronts to invisible hinges, antimicrobial finishes, and integrated home-automation protocols.

By End User: Residential Renovation Drives Volume

Residential customers generated 69.35% of 2025 sales and will outpace commercial accounts through 2031 with a 5.72% CAGR. Repeat remodels are gaining prominence; homeowners in mature markets now replace kitchens every 10–12 years instead of the previous 15–20. Rising cooking frequency—78% of owners cook more than pre-pandemic—elevates the kitchen as a multifunctional hub. Developers of multi-unit housing see factory-finished modules as quality guarantees that shorten construction schedules and boost marketability. Commercial demand remains steady in hospitality and institutional applications, centered on stainless components and code compliance.

Health-and-hygiene consciousness is reshaping residential specifications. Requests for touchless faucets, high-capacity ventilation, and easy-clean surfaces are climbing. Flexible storage zones double as homework or remote-work stations, further broadening the modular kitchen market appeal to families juggling multiple activities under one roof.

By Distribution Channel: Omnichannel Journeys Dominate

B2C and retail accounts absorbed 59.40% of 2025 revenues, anchored by physical showrooms where shoppers test drawers, inspect finishes, and evaluate ergonomics. Online journeys are gaining hefty at a 5.62% CAGR as visualization software narrows the sensory gap between screen and store. Hybrid models—book an online design session, finalize in-store, then track installation through an app—are emerging as the preferred path for time-pressed buyers.

Manufacturers now curate social media content that feeds directly into configurators, shortening inspiration-to-purchase cycles. Direct-to-consumer shipping of flat-pack cabinets appeals to DIY enthusiasts and remote locations, though installer networks remain crucial for full-service experiences. Project-channel volumes tied to residential developers and commercial contractors stabilize factory utilization and support long-run production planning.

Geography Analysis

Europe retained the lead with 32.70% of 2025 revenues on the strength of its engineering legacy and design leadership. Germany and Italy anchor continental production and export premium kits worldwide. Renovation, rather than new construction, fuels 62% of installations as aging housing stock requires modernization. Western European demand centers on aesthetics and sustainability; Eastern Europe is growing faster as household incomes climb, and consumers shift from carpenter-made to factory-built solutions. Circular economic directives are accelerating recycled content and take-back schemes, giving early-adopting brands a competitive edge.

The Asia-Pacific modular kitchen market is on track for a 6.70% CAGR through 2031, propelled by urbanization, rising disposable income, and expanding retail footprints. India alone is projected to advance 20.09% annually, buoyed by government urban-housing initiatives and shifting consumer aspirations toward standardized quality. China’s market is maturing; growth now concentrates in premium upgrades, while Southeast Asia represents a fresh frontier requiring localized designs for varied cooking styles and space norms. Regional suppliers are leveraging cost advantages and cultural insight to compete with global incumbents, forcing multinationals to balance platform scale with market-specific customization.

North America remains lucrative due to high per-unit values and sizable kitchen footprints that accommodate comprehensive modular systems. Renovations comprise 75% of installations, with sustainability features doubling their market share year over year. Smart-home compatibility, especially voice-controlled lighting and appliance monitoring, is becoming a standard upsell. South America shows mixed momentum; Brazil leads demand amid urban consolidation, while currency volatility tempers near-term imports. Across the Middle East and Africa, affluent Gulf states pursue premium European lines, whereas broader uptake hinges on affordable packages that fit smaller apartments and withstand hot climates.

Competitive Landscape

The global modular kitchen market is moderately fragmented. European leaders such as Nobilia, Nobia, and Veneta Cucine dominate premium tiers through consistent engineering and brand heritage, commanding higher price points in export destinations. Multinationals like IKEA, local assemblers, and a rising cohort of e-commerce-first start-ups share mass-market volumes. Market boundaries blur as entry-level brands upgrade finish options and premium houses launch sub-brands targeting aspirational buyers seeking affordable luxury.

Technology now underpins competitive positioning. Oppein Home Group, for example, has invested in proprietary software that lets customers drag-and-drop modules in real-time and receive instant quotations, trimming design approval times dramatically. Digitally networked production lines enable mass customization at cost structures once limited to fully standardized ranges. Meanwhile, partnerships with appliance and IoT specialists are embedding smart features—touch displays, inventory sensors, and remote diagnostics—directly into cabinetry, turning the kitchen into a connected ecosystem.

Supply chain resilience is another battleground. Players are diversifying boards and hardware sourcing to buffer raw-material price swings and guarantee timely delivery. Vertical integration, including engineered-panel factories and installer academies, is gaining traction to ensure consistent workmanship across markets where certified fitters are scarce. Brands that can pair digital design speed with dependable after-sales support are best positioned to capture share as customer expectations move beyond product aesthetics to a holistic ownership experience.

Modular Kitchen Industry Leaders

IKEA

Nobilia Kitchen Furnishing GmbH

Nobia AB

Oppein Home Group Inc.

Howdens Joinery Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Veneta Cucine unveiled its “Nocte Venetiis” series at Casa Decor Madrid, blending IoT-ready storage with sculpted stone islands.

- December 2024: Oppein Home Group opened showrooms in Qatar, Vietnam, Kuwait, Panama, and Ontario and earned six MUSE Design Awards for product innovation.

- October 2024: 21 Invest acquired TheNiceKitchen to accelerate international expansion in the design and furniture sector.

- April 2024: Veneta Cucine outlined plans to add 100 French stores within three years to deepen its European footprint.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global modular kitchen market as the yearly invoice value of new, factory-produced cabinet modules, countertops, and integrated fittings supplied to residential and small commercial kitchens. Modules are factory machined.

Scope exclusion: We exclude on-site carpentered builds, second-hand cabinets, and flat-pack kits sold without a manufacturer warranty.

Segmentation Overview

- By Product

- Floor Cabinets

- Wall Cabinets

- Other Cabinets

- By Design Layout

- L-Shaped

- U-Shaped

- Straight / One-Wall

- Parallel / Galley

- Other Design Layouts

- By Material

- Wood

- Metal

- Fiber/Plastic

- Other Material

- By Price Range

- Economy

- Mid-Range

- Premium

- By End User

- Residential

- Commercial

- By Distribution Channel

- B2C/Retail

- Offline

- Online

- B2B /Project

- B2C/Retail

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed cabinet makers, hardware suppliers, big-box retailers, and installation contractors across Europe, North America, and Asia-Pacific.

Their views on average selling prices, material choices, and channel splits anchored our assumptions.

Desk Research

Our analysts mined Eurostat furniture trade tables, UN Comtrade codes 9403 and 9405, the U.S. Joint Center for Housing Studies renovation tracker, and housing ministry dashboards in India and China, which clarify dwelling completions and kitchen-remodel spend.

Company 10-Ks, investor decks, and trade-association white papers broadened context.

Select intelligence from D&B Hoovers, Dow Jones Factiva, and patent flow on Questel refined price bands and material shifts before cross-checking.

The sources cited are illustrative, not exhaustive.

Market-Sizing and Forecasting

We first build a top-down demand pool from new dwelling completions and median kitchen-remodel spend, then test it with a sampled bottom-up roll-up of supplier shipments.

Key variables, such as urban housing starts, per-capita disposable income, medium-density fiberboard prices, online design-tool adoption, and cabinet import values, feed a multivariate regression that extends the outlook, while scenario analysis buffers commodity swings.

Gaps in bottom-up evidence are bridged through price-volume substitution ranges shared during primary calls.

Data Validation and Update Cycle

Outputs pass three-layer variance checks, peer review, and then senior sign-off.

Mordor analysts refresh the model every twelve months, with mid-cycle updates triggered by tariff or policy shifts.

Before publication, an analyst re-runs dashboards so clients receive the latest view.

Why Mordor's Modular Kitchen Baseline Commands Credibility

Published estimates often diverge because each firm selects its own scope, driver basket, and refresh rhythm. Our disciplined filters on product definition, currency conversion, and annual update cadence keep the baseline stable yet current.

Key gap drivers include whether installation labor is booked, how price inflation is applied, and the depth of supplier sampling in fast-growing Asia. Some studies add DIY kits or rely on single-country price proxies, which inflates or depresses totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 33.52 Bn (2025) | Mordor Intelligence | - |

| USD 36.93 Bn (2025) | Global Consultancy A | Includes replacement doors and worktops, uses single ASP for all regions |

| USD 25.84 Bn (2024) | Industry Data Hub B | Excludes online direct-to-consumer sales, constant-2020 pricing |

| USD 39.04 Bn (2024) | Research Publisher C | Adds DIY flat-pack kits and appliance bundles |

These contrasts show that Mordor Intelligence delivers a balanced, transparent baseline grounded in verifiable production and spending metrics that decision-makers can trace and reproduce with confidence.

Key Questions Answered in the Report

What is the current size of the global modular kitchen market?

The market reached USD 35.37 billion in 2026 and is forecast to grow to USD 46.29 billion by 2031 at a 5.53% CAGR.

Which geographic region leads the modular kitchen market?

Europe holds the largest share at 32.70% of 2025 revenues, driven by German and Italian manufacturing strength.

Which region is growing the fastest?

Asia-Pacific is projected to post a 6.70% CAGR from 2026 to 2031, with India advancing 20.09% a year.

What product category dominates sales?

Wall cabinets accounted for 51.62% of global revenues in 2025 due to their role in maximizing vertical storage.

How important are online channels for purchasing modular kitchens?

Online sales are expanding at a 5.62% CAGR as 3D design tools and augmented-reality previews speed decision making.

Which material type is gaining share because of sustainability concerns?

Fiber and plastic composites are growing at a 6.02% CAGR as consumers seek moisture-resistant and eco-friendly options.

Page last updated on: