Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 97.22 Billion |

| Market Size (2026) | USD 100.53 Billion |

| Market Size (2031) | USD 118.83 Billion |

| Growth Rate (2026 - 2031) | 3.40% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Home Furniture Market Analysis by Mordor Intelligence

The Europe home furniture market size is projected to be USD 97.22 billion in 2025, USD 100.53 billion in 2026, and reach USD 118.83 billion by 2031, growing at a CAGR of 3.4% from 2026 to 2031. Demand is stabilizing as consumers adapt to higher living costs and prioritize essential upgrades, which keeps replacement cycles steady in core categories. The Europe home furniture market is adjusting to regulatory shifts that will change sourcing, product specifications, and data transparency across the value chain. The European Union Deforestation Regulation will require geolocation evidence and due diligence statements for wood-based products by late 2026, which raises compliance and supplier management needs for brands serving the region [1]CSR Germany, “EU Regulation on Deforestation-free Products,” CSR Germany, csr-in-deutschland.de. In parallel, the Ecodesign for Sustainable Products Regulation brings Digital Product Passports to furniture, which will reward traceable, durable, and repairable designs after sector-specific rules are finalized. National building renovation plans under the revised Energy Performance of Buildings Directive will also support demand from interior refits as member states execute measures through 2030 and 2040 milestones.

Key Report Takeaways

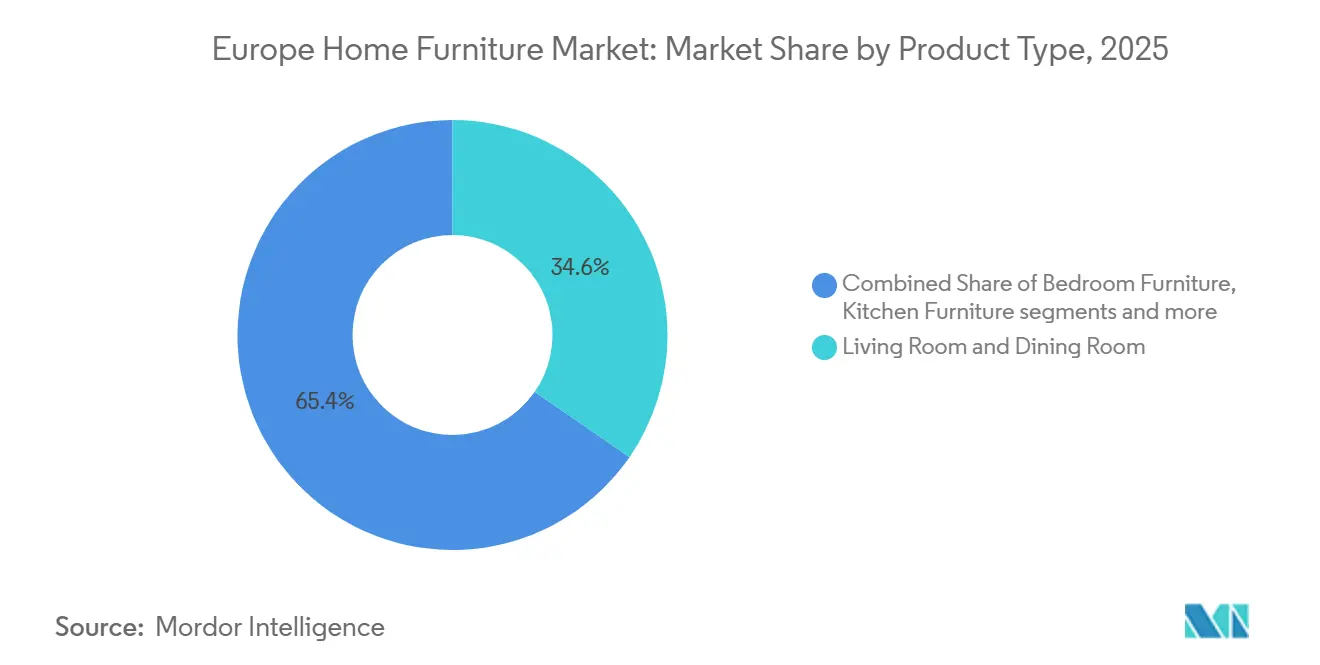

- By product, living room and dining room furniture led with 34.62% of the Europe home furniture market share in 2025, while home office furniture is projected to expand at a 3.87% CAGR through 2031.

- By material, wood accounted for 53.71% of the Europe home furniture market share in 2025, whereas plastic and polymer are forecast to grow at a 4.60% CAGR through 2031.

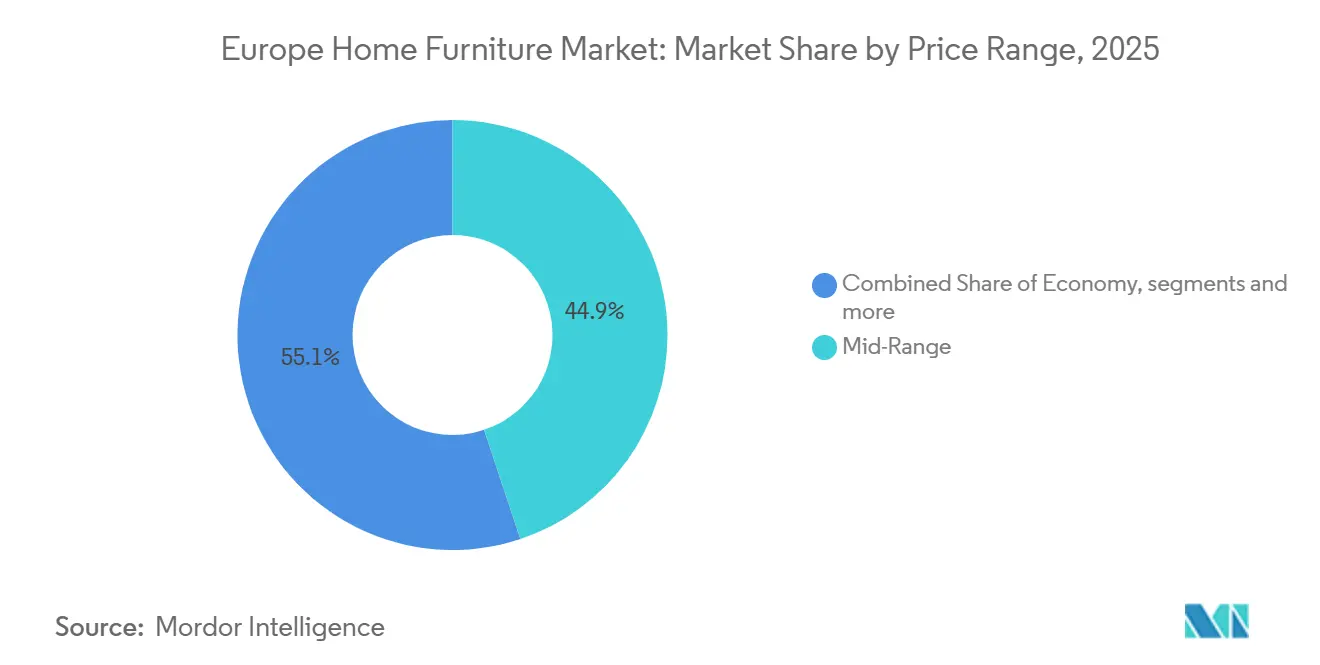

- By price range, mid-range held 44.88% of the Europe home furniture market share in 2025, while premium is set to grow at a 4.34% CAGR through 2031.

- By distribution channel, home centers captured 45.12% of the Europe home furniture market share in 2025, whereas online is expected to advance at a 5.12% CAGR through 2031.

- By geography, Germany and the United Kingdom together represented 35.74% of the Europe home furniture market share in 2025, while Poland is anticipated to post a 4.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Home Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| European Union Renovation Wave and housing-energy retrofits lifting interior refits | +0.7% | France, Belgium, the Netherlands, and Germany | Medium term (2-4 years) |

| ESPR and Digital Product Passports accelerating sustainable, durable designs | +0.5% | European Union-wide | Medium term (2-4 years) |

| Rising e-commerce and omnichannel adoption in furniture retail | +0.9% | Nordic countries, the United Kingdom, and Spain | Short term (≤ 2 years) |

| Shift to sustainable wood and certified materials in the home segments | +0.4% | Germany, France, Benelux, Nordics | Medium term (2-4 years) |

| Nearshoring and faster lead-times favoring European Union-made modular and RTA | +0.6% | Poland, Romania, Spain, Baltic states | Short term (≤ 2 years) |

| Hybrid living needs sustaining demand post-pandemic | +0.8% | United Kingdom, Germany, France, Netherlands, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

European Union Renovation Wave and Housing-Energy Retrofits Lifting Interior Refits

National building renovation plans under the revised Energy Performance of Buildings Directive must be finalized by December 31, 2026, with interim drafts due in 2025, which sets a clear policy anchor for retrofit programs and funding across member states. These plans set milestones for 2030 and 2040 and move Europe toward a zero-emission building stock by 2050, which increases demand for materials, fixtures, and interior updates that align with improved energy and comfort standards. As residential envelopes are upgraded and ventilation improved, homeowners typically refresh kitchens, storage, and living spaces to match improved layouts and space efficiency goals. Retailers and manufacturers that support measured retrofit workflows, such as modular kitchens and storage systems that fit standardized footprints, are well placed to convert subsidy-driven projects into steady order flow. The Europe home furniture market benefits indirectly from the retrofit wave because every deep energy upgrade raises the likelihood of linked interior refits within the lifecycle of a property. Program execution varies by country, yet the policy direction is consistent across the bloc and creates a long runway for interior improvement activity tied to energy performance [2]European Commission, “National Building Renovation Plans,” European Commission, europa.eu.

ESPR And Digital Product Passports Accelerating Sustainable, Durable Designs

Furniture is a priority category in the Commission’s 2025 working plan for the Ecodesign for Sustainable Products Regulation, which sets the stage for product-specific rules by 2028 and then market surveillance through the early 2030s. Digital Product Passports will require structured, machine-readable data on composition, substances of concern, durability, and recyclability, which moves compliance into the design and product lifecycle management phase. Brands that invest early in Digital Product Passport architecture and bill-of-materials traceability build an advantage because their data can substantiate claims, unlock procurement routes, and support secondary life services like repairs and take-backs. Retailers that already run buyback or refurbishment programs can feed passport data from intake to resale, which supports circular models and strengthens brand trust in regulated categories. For furniture OEMs, this shifts compliance from retrospective labeling to proactive design-for-circularity: products must embed traceability from the bill-of-materials stage, document geolocation for EUDR-covered wood, and prove repair/disassembly pathways. Early adopters like Ingka Group (IKEA) are piloting DPP infrastructure across their buyback service (686,500 used products sourced in FY2025) and second-hand marketplace, treating passport data as a competitive moat rather than a regulatory burden [3]ITLN, “Ingka Group steps up circular push and low-carbon operations,” ITLN, itln.in. Collaboration projects funded by the European Union, such as consortia working on circular design, data spaces, and product-service systems, lower the barrier for small and mid-size firms to adopt DPP-aligned processes.

Rising E-Commerce and Omnichannel Adoption in Furniture Retail

Unified order management and ship-from-store capabilities allow furniture retailers to improve availability while keeping inventories lean, which raises conversion and lowers stockouts for bulky items and decor. Store networks that connect inventory pools across warehouses and shops can route orders to the best node for speed or cost, which supports both home delivery and click-and-collect. Visual configuration tools and room planning services integrate digital discovery with in-store consultation so shoppers can finalize designs and measurements quickly. The ability to sell both proprietary products and marketplace items within the same basket broadens selection without heavy capital use. As consumers expect faster lead times, omnichannel stacks help retailers reassign store roles toward fulfillment and service while maintaining experience-led showrooms. The Europe home furniture market will keep shifting toward hybrid journeys that start online, use store services for assurance, and end with a mix of home delivery and installed services where needed [4]OneStock, “Maisons du Monde partners with OneStock,” OneStock, onestock-retail.com.

Hybrid Living Needs Sustaining Demand Post-Pandemic

Hybrid work is now a steady pattern for a large share of working adults in major European economies, which keeps attention on ergonomic seating, adjustable desks, and storage that can be reconfigured during the day. In the United Kingdom, formal hybrid models reported by employers and workplace designers continue to anchor home workspace investments for knowledge workers who split time between home and office. Modular kitchen and living solutions that hide clutter and open social space are gaining traction, with new fittings that rotate, lift, and convert storage to open shelves as daily needs change. Bedroom systems that integrate smart storage and approachable price points appeal to households seeking to refresh layouts without full renovations. Premium brands are extending circular principles into design for disassembly and long-life components, which support service and resale pathways later in the product life. The Europe home furniture market will keep aligning product roadmaps to small-space optimization, multipurpose use, and wellness features tied to routine hybrid use at home.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-of-living squeeze delaying big-ticket purchases | -1.1% | Germany, the United Kingdom, France, Italy | Short term (≤ 2 years) |

| Timber and raw material volatility are challenging pricing | -0.7% | Nordic exporters, Central European mills, United Kingdom importers | Medium term (2-4 years) |

| EUDR compliance costs and wood traceability bottlenecks | -0.3% | European Union-wide, especially SMEs | Medium term (2-4 years) |

| Skilled-trade bottlenecks are elongating lead times | -0.2% | Germany, the Netherlands, and France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-Of-Living Squeeze Delaying Big-Ticket Purchases

Household budgets remain sensitive to energy and housing costs in several large economies, which continues to delay discretionary purchases of kitchens, living room suites, and bedroom sets. Transaction volumes in housing markets affect furniture orders because moves and major renovations often trigger full-room updates, and slow pipelines can hold back category growth. Retailers are responding with financing, room bundles, and value-led assortments that meet constrained budgets while preserving perceived quality. Premium tiers are steadier, where affluent buyers continue with planned refresh cycles, which helps defend margins even when mid-market volumes soften. Brands that streamline assortments and focus on faster-moving constructions can manage working capital better during periods of cautious spending. The Europe home furniture market should see gradual improvement as real wages normalize and consumer confidence stabilizes, yet recovery will depend on local housing and labor conditions that vary by country.

EUDR Compliance Costs and Wood Traceability Bottlenecks

The European Union Deforestation Regulation requires operators to collect geolocation data for plots used in wood sourcing and submit due diligence for products placed on the market, which adds new obligations to multi-tier supply chains. Some upstream suppliers need time to map plots and update documentation, which has created early administrative friction for downstream brands preparing their compliance systems. While certification frameworks can simplify parts of the verification trail, they do not replace EUDR obligations, including geolocation capture for wood-derived inputs. Companies are budgeting for audits, data platforms, and supplier training to meet the regulations, which creates recurring overhead for mid-size importers and downstream integrators. Non-compliance risks range from fines to product seizures and temporary market exclusion, which elevates the need for robust supplier consolidation and traceability tools. The Europe home furniture market will see moderate short-term pressure from these changes, while first movers that solve provenance early can turn compliance into competitive assurance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Home Office Accelerates as Hybrid Work Takes Hold

Living Room and Dining Room furniture remained the anchor with 34.62% of Europe home furniture market share in 2025, yet growth is steady rather than rapid as replacement cycles normalize. The Europe home furniture market reflects how communal spaces retain priority status in household budgets even when consumers defer certain discretionary upgrades. Home Office furniture is forecast to expand at a 3.87% CAGR, supported by hybrid work patterns that have settled into durable routines in the United Kingdom and across major European economies. The focus has shifted from stopgap desks to ergonomic seating, height-adjustable systems, and storage that blends with living areas. Kitchen and storage categories should continue to benefit indirectly from national renovation plans that aim to raise energy performance and modernize building stock through 2030 and 2040 milestones. Bathroom furniture moves with vanity and mirror integration trends that package lighting and storage in clean layouts. Outdoor items remain linked to seasonal use and space constraints, though interest persists where balconies and terraces are part of everyday routines in urban settings.

Product development is tilting toward multiuse spaces and integrated components that improve comfort, serviceability, and lifespan. In kitchens, brands are experimenting with modular fittings that convert hidden compartments into open shelves with smooth lift and rotating actions, which address daily switching between cooking, working, and social modes. Premium and design-led players are also investing in digital and material innovations that support future compliance and differentiation. Smart-kitchen prototypes show how sensors, inductive power, and user guidance can be embedded into work surfaces, then documented via digital data for post-sale service. In bathroom fittings, recent portfolio moves strengthen regional supply in the Nordics, which can support adjacent bathroom furniture assortments. The Europe home furniture market will keep aligning product lines to hybrid living needs and energy-aware renovations that refresh storage, seating, and work surfaces in tandem.

By Material: Plastic and Polymer Innovation Outpaces Traditional Wood

Wood continued to lead with 53.71% of revenue in 2025 as it remains foundational across casegoods, kitchens, and storage in the Europe home furniture market. Forward sourcing now depends on traceability because regulated market access requires documentation that wood inputs come from non-deforested land and meet due diligence obligations. Chain-of-custody certifications remain common for public and private buyers in Europe as part of proof-of-origin and sustainability practice. Plastic and polymer are projected to grow at a 4.60% CAGR for the Europe home furniture market size as circular material science and low-carbon chemistries improve performance in upholstery and shells. Manufacturers are shifting to recycled and bio-content inputs where design and durability match indoor use cases and aesthetic goals, which pulls in new supply partnerships. A leading example is the move toward recycled polymers and blends for seating that lower virgin plastic use while maintaining finish quality and structural integrity. Chemical suppliers are also expanding low-carbon polyurethane portfolios that use renewable power and process improvements to cut embedded emissions, which supports consumer and procurement criteria for climate targets.

Metal retains a measured growth path in frames, bases, and outdoor sets because it delivers durability, repeatable strength, and finish options that fit minimalist styling. The “Others” category covers glass, textiles, and emerging bio-composites that use plant fibers and mycelium to reduce fossil-derived content while meeting structural needs in shells and panels. European Union-funded projects are scaling research for biocomposites and large-scale processing techniques, which could accelerate adoption in select product lines as cost curves improve. Biomaterials are also moving from concept to commercial pilots in premium applications where early adopters value novel textures and verified sourcing. Over the forecast period, the Europe home furniture market will balance proven wood constructions with faster innovation cycles in recycled polymers and bio-based materials to meet design, durability, and regulatory expectations.

By Price Range: Premium Lifts on Verified Sustainability and Design

Mid-Range captured 44.88% of revenue in 2025 because it meets broad affordability needs and is present across generalist channels that serve everyday remodeling and refresh cycles in the Europe home furniture market. The core mid-tier continues to adapt with durable finishes, serviceable hardware, and modern formats that give value without complex installation. Premium is projected to grow at a 4.34% CAGR for the Europe home furniture market size as households with higher discretionary income pursue longevity, verified materials, and brand-led design. Premium positioning now leans on design for disassembly, take-back services, and certificated inputs that can be documented through Digital Product Passports later in the decade. The signal is consistent across leading design houses that align collections to circular principles without compromising aesthetics.

At the same time, accessible premium and entry premium ranges target shoppers who want refined surfaces, soft-close hardware, and integrated lighting without a full bespoke spend. New kitchen lines launched for the 2026 cycle illustrate how manufacturers can offer ergonomic layouts and structured surfaces at approachable price points supported by partner finance offers. As circular requirements mature under ESPR, premium brands that make durability and serviceability central to the value proposition can differentiate further through warranty support and refurbishment options. Supplier partnerships in polymers and biomaterials also extend the storytelling around product carbon footprints and end-of-life pathways. The Europe home furniture market will see a clearer split between base-value sets optimized for price and premium sets optimized for longevity, repair, and responsible sourcing.

By Distribution Channel: Online Scales as Omnichannel Orchestration Improves

Home Centers held 45.12% share in 2025, which reflects the importance of physical advisory and installation support for kitchens, bathrooms, and storage projects. The format still anchors high-touch purchases where measuring, templating, and logistics matter, while trade professionals rely on quick availability and consistent assortments. Online is forecast to grow at a 5.12% CAGR, helped by order management systems that route to the fastest or most efficient fulfillment node and by ship-from-store programs that shorten delivery timelines. Click-and-collect and scheduled delivery models broaden convenience for heavy items, and marketplaces extend reach without large capital outlays.

Omnichannel maturity now depends on unified inventory and the ability to present real-time stock to customers across web and store screens, which reduces lost sales from out-of-stocks. Retailers that orchestrate B2C, B2B, and marketplace flows in a single stack can consolidate demand signals and adjust assortments more quickly. Specialist formats continue to matter for configured projects and premium goods that require design consultation, specification, and white-glove delivery. On the B2B side, project partnerships that integrate design, logistics, and installation keep lead times tight for builders and developers, especially in kitchen programs where accuracy is key. The Europe home furniture market will rely on blended journeys that start online, validate in-store, and finish with delivery and fitting services tailored to the project scope.

Geography Analysis

The Germany home furniture market, along with the United Kingdom, represented 35.74% of the European home furniture market share in 2025, reflecting their combined consumer base, retail infrastructure, and domestic manufacturing links into adjacent categories such as kitchens and storage. The two markets continue to adjust to household budget constraints and slower housing transactions, which have historically driven a large share of furniture purchase events. Policy support for energy-efficiency improvements and building upgrades should create steady retrofit demand, which benefits storage and kitchen refresh cycles in existing homes. The Europe home furniture market in these countries will see gradual normalization as inflation cools and household confidence steadies, with retailers focusing assortments on mid-range value and service packages.

Italy, Spain, and the BENELUX countries present a balanced picture. Italy’s design heritage sustains premium exports in seating and systems, while domestic spending trends are cautious and vary by region. Spain’s ecosystem is active in trade promotion and design showcases, which support brand exposure across residential and contract channels. BENELUX markets are early adopters of sustainability criteria in public and private procurement, which encourages verified materials and pushes manufacturers to evidence chain-of-custody. The Europe home furniture market across these countries continues to shift toward modular storage, contemporary kitchens, and textile-led seating that aligns with small-space living.

Poland and the broader Rest of Europe cluster are projected to grow the fastest through 2031, supported by nearshore manufacturing capacity in ready-to-assemble case goods and kitchens. Local suppliers that can deliver within tight lead times and meet compliance needs are gaining partners in Western European retail and contract channels. As logistics costs and compliance requirements are internalized, regional sourcing can reach landed-cost parity with distant imports for many SKUs, which improves responsiveness. The Europe home furniture market in Central and Eastern Europe also benefits from rising urban disposable incomes and continued improvements in retail logistics networks. Given the regulatory direction on traceability and circularity, these regions are well-positioned to scale compliant, quick-turn production with integrated supply programs that serve German, French, and Benelux demand.

Competitive Landscape

The competitive field is diverse and regionally fragmented, which keeps rivalry centered on capabilities rather than simple price. Early movers on Digital Product Passports and ecodesign will shape category standards as delegated acts land later in the decade, with pilots already underway in large retailers that run take-back and resale services. Manufacturers are expanding design-for-repair, durability documentation, and bill-of-materials traceability so that products meet upcoming data requirements at the model or batch level. The Europe home furniture market will reward brands that link material choices to verifiable sustainability data while balancing cost, aesthetics, and service support.

Strategic partnerships illustrate how leaders are preparing for the next wave of category differentiation. Kitchen companies are showcasing integrated technology concepts that bring sensors, inductive power, and guided cooking features into work surfaces, which can be tracked through product passports for service over time. Order orchestration platforms now unify inventory across stores and warehouses for large lifestyle retailers, which reduces stockouts and unlocks ship-from-store for faster local delivery. On the materials side, furniture makers are adopting recycled and bio-based inputs for shells and cushions as chemical partners bring lower-carbon polyurethane families to market.

Manufacturers and retailers are also preparing circular scale by expanding repair options, component standardization, and take-back channels that can be integrated with Digital Product Passports. Biomaterial innovations are moving into premium collections where early adopters value novelty and verified origin, which could seed broader use as cost curves improve. Premium and contemporary design brands are aligning the 2026 cycle to modular storage and small-space living concepts that can evolve with household needs. The Europe Home data and market remains a race to validate provenance under EUDR, embed DPP-ready data, and deliver omnichannel service quality that meets consumer expectations across discovery, delivery, and installation.

Europe Home Furniture Industry Leaders

IKEA Industry

Nobilia

Nolte Küchen

Hülsta-Werke Hüls

Rauch Möbelwerke

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Ingka Group (IKEA) announced plans to open 20 new compact-format stores across Europe and North America within six months, each carrying 2,000+ products for immediate purchase with full-range pick-up/delivery, as part of a EUR 5 billion three-year investment to expand its footprint and improve existing locations. The compact-store rollout (2,000 m² in Limoges, France; over 4,000 m² in Coimbra, Portugal; Białystok, Poland by year-end) positions IKEA closer to where people already shop daily, reducing reliance on large out-of-town warehouses and cutting last-mile delivery costs.

- March 2026: Natuzzi S.p.A. disclosed an investment plan exceeding EUR 53 million over three years (averaging EUR 18 million annually) to achieve break-even by 2028, with funds allocated to retail network development, R&D, and production-facility strengthening in Italy. The company scrapped 476 planned redundancies, pivoting its 2026–2028 strategy toward relaunching operations and reshoring Natuzzi Editions production for North America from China back to Italy/Romania, a move designed to mitigate US tariffs and fully utilize Italian factory capacity.

- January 2026: Ingka Group (IKEA) expanded its second-hand marketplace to Sweden (launched January 28, 2026), making it live in five European countries (Sweden, Spain, Norway, Portugal, Poland), targeting 170,000 active listings by year-end. The peer-to-peer platform allows customers to scan IKEA products, receive instant price recommendations and professional photography, and choose cash payment or a 15% bonus with an IKEA digital refund card, supporting circular-economy goals and extending product lifecycles.

- November 2025: Nobilia introduced the LOOK Collection for 2026, an entry-level kitchen range featuring structured surfaces, soft-close runners/hinges, integrated LED lighting, and premium ergonomic design at accessible price points, available in LOOK Coffee and LOOK Sand finishes.

Europe Home Furniture Market Report Scope

Home furnishings are pieces of furniture that can be moved around the house or office to make it more comfortable to live and work in it.

The Europe Home Furniture Market Report is Segmented by Product (Living Room & Dining Room Furniture, Bedroom Furniture, Kitchen Furniture, Home Office Furniture, Bathroom Furniture, Outdoor Furniture, and Other Furniture), Material (Wood, Metal, Plastic & Polymer, and Others), Price Range (Economy, Mid-Range, and Premium), Distribution Channel (Home Centers, Specialty Furniture Stores, Online, and Other Distribution Channels), and Geography (United Kingdom, Germany, France, Spain, Italy, BENELUX, NORDICS, and Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

By Product

| Living Room & Dining Room Furniture |

| Bedroom Furniture |

| Kitchen Furniture |

| Home Office Furniture |

| Bathroom Furniture |

| Outdoor Furniture |

| Other Furniture |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Others |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By Distribution Channel

| Home Centers |

| Specialty Furniture Stores |

| Online |

| Other Distribution Channels |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Product | Living Room & Dining Room Furniture |

| Bedroom Furniture | |

| Kitchen Furniture | |

| Home Office Furniture | |

| Bathroom Furniture | |

| Outdoor Furniture | |

| Other Furniture | |

| By Material | Wood |

| Metal | |

| Plastic & Polymer | |

| Others | |

| By Price Range | Economy |

| Mid-Range | |

| Premium | |

| By Distribution Channel | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the Europe home furniture market size outlook through 2031?

The Europe home furniture market size is projected at USD 100.53 billion in 2026 and USD 118.83 billion by 2031, at a 3.4% CAGR over 2026 to 2031.

Which product categories are leading the growth in Europe Home Furniture?

Living Room and Dining Room led revenue in 2025, while Home Office is the fastest-growing category, supported by embedded hybrid work and ongoing ergonomic needs.

How will European Union regulations affect the Europe home furniture market?

EUDR will require geolocation and due diligence for wood inputs by late 2026, and ESPR will bring Digital Product Passports by the late 2020s, which makes traceability, durability, and repairability central to market access.

Which materials are gaining share in the Europe home furniture market?

Wood remains the largest, while Plastic and polymer are the fastest growing as recycled and bio-content solutions mature, supported by supplier advances in low-carbon polyurethane chemistries.

What channels are shaping sales in Europe Home Furniture?

Home Centers still anchor complex projects, while online growth is faster due to unified order management, ship-from-store, and marketplaces that expand reach without large capital use.

Which regions show the strongest momentum in Europe Home Furniture?

Germany and the United Kingdom remain the largest combined markets, while Poland and the rest of Europe are projected to grow the fastest due to nearshore capacity and improving retail logistics.

Page last updated on: