Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.51 Billion |

| Market Size (2026) | USD 1.59 Billion |

| Market Size (2031) | USD 2.03 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Kitchen Furniture Market Analysis by Mordor Intelligence

The Australia kitchen furniture market size in 2026 is estimated at USD 1.59 billion, growing from 2025 value of USD 1.51 billion with 2031 projections showing USD 2.03 billion, growing at 5.06% CAGR over 2026-2031. Sustained residential renovation activity, lifestyle shifts favouring open-plan layouts, and accelerating technology adoption anchor expansion. Homeowners continue to prioritize kitchen upgrades for property value retention, while rising interstate migration drives new housing demand in growth corridors. Manufacturers differentiate through modular formats, smart-ready storage, and eco-friendly materials that address evolving consumer expectations. Competitive intensity remains moderate as global retailers, local specialists, and direct-to-consumer brands pursue omnichannel strategies to reach urban and regional buyers.

Key Report Takeaways

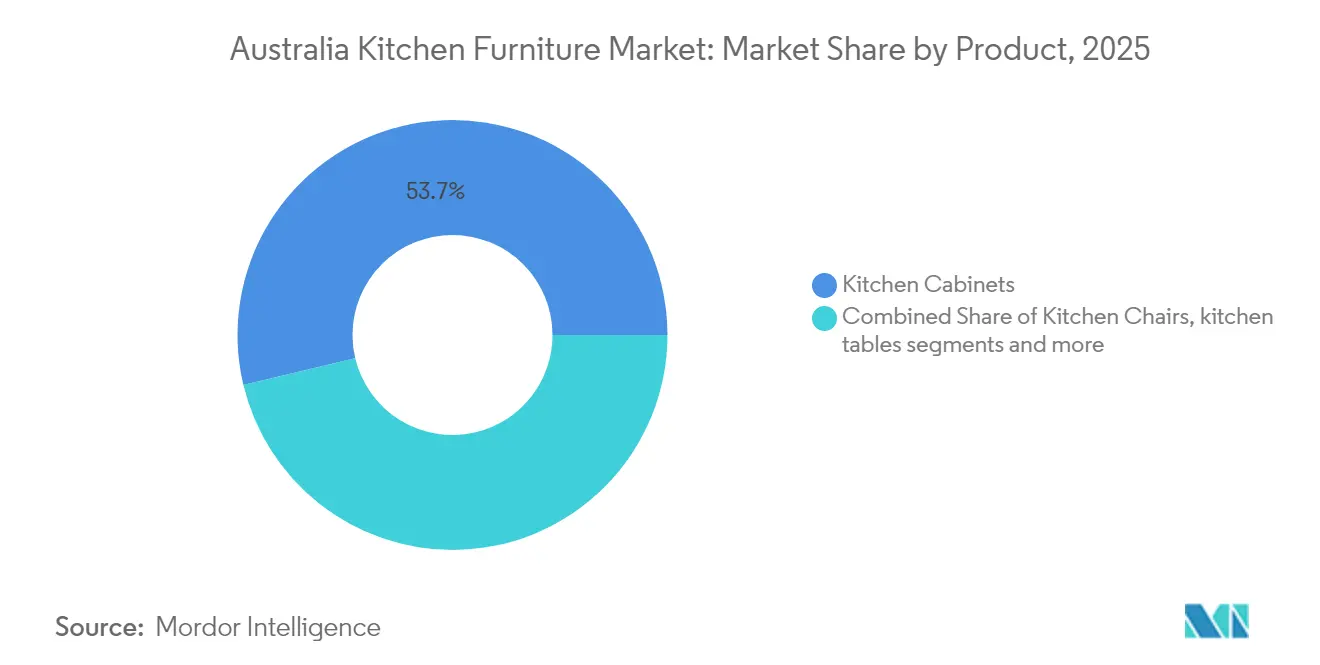

- By product, kitchen cabinets held 53.74% of the Australia kitchen furniture market share in 2025, while accessories such as trolleys and pantry shelves are forecast to expand at a 5.58% CAGR through 2031.

- By material, wood retained a 60.62% share of the Australia kitchen furniture market size in 2025, whereas metal components are advancing at a 6.52% CAGR to 2031.

- By end-user, residential applications captured 76.05% of the Australia kitchen furniture market size in 2025, whereas commercial installations are projected to grow at a 6.63% CAGR through 2031.

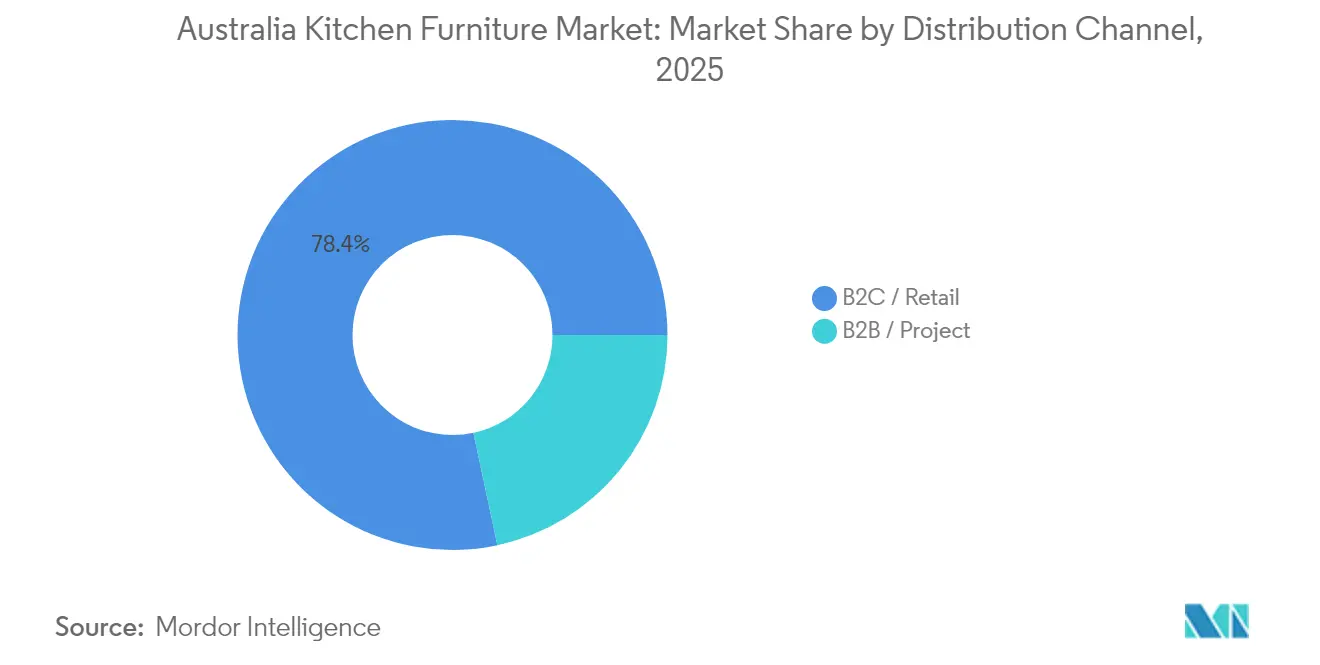

- By distribution channel, B2C retail controlled 78.35% of value in 2025, while B2B project sales are recording a 6.41% CAGR as builders embed premium kitchen solutions in new dwellings.

- By region, New South Wales led with 34.18% revenue share in 2025; Queensland is the fastest-growing state at 6.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Kitchen Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising residential renovation spending | +1.2% | National, concentrated in NSW and Victoria | Medium term (2-4 years) |

| Open-plan living boosting modular demand | +0.8% | Urban centers nationwide | Long term (≥ 4 years) |

| Expanding online furniture retail | +0.6% | National, stronger in regional areas | Short term (≤ 2 years) |

| Adoption of smart kitchen technologies | +0.5% | Metropolitan areas, spreading to regional centers | Medium term (2-4 years) |

| Energy-efficient home incentives | +0.4% | Victoria leading, widening to other states | Medium term (2-4 years) |

| Circular-economy marketplaces emergence | +0.3% | Major metropolitan areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Residential Renovation Spending and Kitchen Upgrades

Average kitchen renovation budgets climbed to AUD 35,000–45,000 in 2024 as millennials entered peak ownership years and baby boomers downsized into lifestyle-oriented residences[1]Envision Kitchens, “Kitchen Renovation Costs and Trends,” envisionkitchens.com.au. Low interest rates and targeted state incentives maintained momentum, supporting premium cabinetry and multifunctional furniture uptake. Brisbane registered the highest aggregate renovation spend, while Geelong posted leading per-capita outlays, demonstrating demand breadth beyond traditionally dominant metros. Although construction-material inflation now moderates discretionary budgets, value-engineered modular solutions help sustain replacement cycles. Manufacturers offering rapid installation and financing packages capture share in this budget-sensitive environment.

Growing Prevalence of Open-Plan Living Driving Demand for Modular Kitchen Cabinets

More than two-thirds of newly built dwellings incorporated open-plan layouts in 2024, positioning the kitchen as a social hub contiguous with living zones. This architectural preference elevates demand for modular cabinets that double as room dividers and visual focal points. Standardized unit sizing simplifies logistics while color and hardware customization maintain design flexibility. Apartment developers in Sydney and Melbourne increasingly specify corner pull-outs, tall pantries, and breakfast-bar modules to maximize usable area. The trend supports premium pricing for slim-profile doors, concealed hinges, and integrated LED lighting that harmonize with adjacent décor.

Increasing Online Furniture Retail Penetration Expanding Customer Reach

Digital channels captured roughly 18% of national furniture sales in 2024, with kitchen categories outpacing broader sector growth[2]Kitchen Warehouse, “E-commerce Growth in Australian Furniture Market,” kitchenwarehouse.com.au. Augmented-reality planning tools and virtual consultations mitigate the tactile limitations of e-commerce. Regional households benefit most, gaining access to premium ranges previously limited to metropolitan showrooms. Direct-to-consumer platforms compress supply chains, lowering acquisition costs for value-conscious renovators. Nonetheless, showroom experiences remain critical for material selection and hardware testing, prompting retailers to integrate click-and-collect, live video walkthroughs, and pop-up studios into omnichannel models.

Growing Adoption of Smart Kitchen Technologies

Roughly 50% of Australian households owned at least one smart kitchen device by end-2024, up from 36% in 2023[3]Smart Kitchen Technology Report, “Smart Kitchen Adoption in Australia,” smartkitchentech.com.au. Voice-activated drawers, sensor-lit shelves, and IoT-enabled hinges migrate from luxury to mainstream segments. Cabinet designers now allocate dedicated charging nooks and cable management channels as baseline features. Younger demographics prioritize app-based inventory monitoring that reduces food waste, while aging populations welcome automated lift-system shelving for ergonomic access. Component suppliers coordinating with appliance brands accelerate ecosystem compatibility, reinforcing replacement demand for technology-ready furniture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated timber and raw material costs | −0.7% | Nationwide, acute need for local producers | Short term (≤ 2 years) |

| Intensifying import competition | −0.6% | National, strongest in price-sensitive segments | Medium term (2-4 years) |

| Skilled labor shortages in cabinetmaking | −0.5% | Nationwide, severe in regional areas | Medium term (2-4 years) |

| Building-code variability across states | −0.4% | National, state-specific rules | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevated Timber and Raw-Material Costs Squeezing Manufacturer Margins

Construction-grade timber prices climbed 22% year-over-year in 2024 amid supply bottlenecks and export demand, pressuring local cabinetmakers[4]Housing Industry Association, “Skills Shortage Report,” hia.com.au. Hardware, adhesives, and veneer costs followed upward, narrowing gross margins across small and mid-sized workshops. Some producers shifted toward engineered panels and hybrid composites to reduce exposure to volatile lumber prices. Larger manufacturers leveraged bulk procurement and alternative sourcing from New Zealand plantations to stabilize inputs. Retailers introduced transparent price-adjustment clauses, yet consumer pushback intensified, prompting value-tier brands to emphasize entry-level laminate assortments.

Intensifying Import Competition from Flat-Pack Asian Suppliers

Asian exporters expanded shipments of ready-to-assemble ranges priced 15–20% below domestic equivalents in 2024. Aggressive factory-gate pricing, container-level consolidation, and localized after-sales networks erode market share for local players targeting cost-conscious consumers. Domestic brands counter with made-to-measure services, shorter delivery windows, and sustainability certifications. Government deliberations on anti-dumping duties remain ongoing but have yet to yield protective tariffs. Price competition compresses retailer margins, especially within the lower mid-range, where differentiation rests largely on finish options and warranty length.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Cabinets Maintain Primacy While Accessories Accelerate

Kitchen cabinets captured 53.74% of value in 2025, generating the largest slice of the Australian kitchen furniture market share. High ticket sizes and long replacement cycles secure their role as cornerstone investments in both new builds and renovations. Core demand clusters around full-height pantry units, island modules with integrated seating, and soft-close drawer systems that elevate user experience. Premium plywood carcasses and UV-cured finishes support durability expectations among affluent homeowners.

Accessories encompassing trolleys, carts, and modular pantry shelves posted the fastest growth at 5.58% CAGR, reflecting surging apartment development in Sydney, Melbourne, and Brisbane. These mobile or plug-and-play solutions offset space constraints and suit rental properties where permanent installations face restrictions. Manufacturers focus on slim steel frames, foldable worktops, and locking casters that allow flexible reconfiguration. The segment’s lower price points encourage impulse upgrades and repeat purchases, reinforcing recurring revenue streams. Smart sensors measuring inventory levels or reminding users of expiry dates illustrate how accessories increasingly integrate technology to boost perceived value.

By Material: Wood Dominance Faces Metal-Driven Innovation

Wood continued to command 60.62% market share in 2025 within the Australia kitchen furniture market. Consumers value its aesthetic warmth and perceived craftsmanship, especially in suburban detached homes where natural finishes complement open-plan interiors. Solid hardwood doors, thermally modified veneers, and water-borne sealants extend lifespan and meet sustainability expectations. Royal-ite oak and Tasmanian blackwood lines sell robustly in premium brackets despite cost pressures.

Metal components are rising at a 6.52% CAGR as designers seek slim profiles, industrial aesthetics, and compatibility with smart hardware. Powder-coated aluminum frames facilitate handle-less fronts and concealed hinges, satisfying contemporary tastes. Stainless-steel drawer boxes paired with timber fronts create hybrid constructions balancing durability and visual appeal. Increasingly stringent fire safety standards in high-density dwellings further boost demand for non-combustible substrates, positioning metal as a pragmatic alternative. Composite boards and high-pressure laminates serve cost-focused segments, yet they seldom displace wood’s entrenched cultural appeal.

By End-User: Residential Reigns While Commercial Momentum Builds

Residential buyers generated 76.05% of 2025 revenues, reflecting lifestyle-driven cycles that hinge on property appreciation and personal amenity priorities. Detached houses average 15- to 20-year replacement intervals, while apartment refurbishments trend closer to 10 years due to evolving tenancy and design fashions. Smart-ready cabinetry, integrated charging hubs, and antimicrobial surfaces gain traction among urban professionals who favor convenience and health safeguards.

Commercial installations, spanning restaurants, hotels, offices, and learning facilities, are projected to log a 6.63% CAGR to 2031. The hospitality rebound post-pandemic spurs kitchen redesigns emphasizing speed, hygiene, and customer-visible preparation zones. Co-working providers specify barista-style kitchenettes that double as collaboration spaces, elevating functional requirements. Commercial buyers demand stainless-steel frames, heavy-duty runners, and high-wear laminates built for daily intensive use. Suppliers tailor maintenance contracts and rapid replacement guarantees to meet stringent uptime expectations.

By Distribution Channel: Retail Dominance Shifts Toward Project-Led Sales

B2C retail outlets—including home centers, specialty showrooms, and pure-play e-commerce—controlled 78.35% of spend in 2025. DIY-inclined households gravitate toward flat-pack systems that feature intuitive assembly instructions and online configuration tools. Regional branches of hardware chains broaden reach, while store-within-store concepts provide premium brand exposure in big-box formats.

Project-based B2B channels are forecast to grow 6.41% annually as builders pre-select complete kitchen packages for off-the-plan developments. Volume contracts yield cost efficiencies, favoring suppliers able to guarantee consistent quality across hundreds of units. Turnkey renovation services bundle design, demolition, supply, and installation, appealing to time-pressed homeowners. Showrooms increasingly host dedicated trade desks, facilitating specification alignment and after-sales warranty processing. Yet, project pipelines remain tied to macro construction cycles, necessitating risk mitigation through diversified order books.

Geography Analysis

New South Wales retained leadership with 34.18% of the national value in 2025, underlined by Sydney’s high per-capita disposable income and a seasoned renovation workforce. Mature stock drives replacement demand for upgraded storage, soft-close hardware, and energy-efficient lighting. Proximity to Port Botany streamlines import flows, enabling competitive pricing for international brands. Supply-side efficiencies reinforce consumer choice breadth, from budget flat-packs to artisanal bespoke suites.

Queensland’s 6.14% CAGR underscores demographic influx and lifestyle-centric building activity, particularly in coastal enclaves. Developers emphasize breezy layouts with oversized islands and outdoor servery hatches to support entertainment. State-specific cyclone and humidity considerations spur uptake of galvanized steel substructures and moisture-resistant boards. Government subsidy programs for energy-positive homes also catalyze demand for low-VOC finishes and solar-compatible lighting strips.

Victoria, Western Australia, and South Australia collectively contribute roughly one-third of national revenues, each leveraging localized production ecosystems and skilled joinery talent. Perth’s distance from east-coast suppliers motivates vertically integrated manufacturers who capture design-to-install value. Tasmania and the Northern Territory remain niche but display rising appetite for direct-to-consumer shipments that bypass limited retail footprints. State-level building-code divergence necessitates adaptive product lines, further highlighting the regionalized nature of the Australia kitchen furniture market.

Competitive Landscape

The Australia kitchen furniture market exhibits moderate fragmentation. IKEA combines global sourcing scale with localized planning studios to target value-oriented consumers, supported by a three-year delivery alliance with Australia Post that covers remote regions. Bunnings’ Kaboodle brand dominates DIY upgrades, leveraging widespread store coverage and intuitive online configurators. Freedom Kitchens positions itself at the premium end, offering design consultation services and extended warranties to differentiate from mass retailers.

Technology serves as a key competitive battleground. Modulr’s ultrasonic WoodWelding® technique delivers cabinets 30% stronger than conventional joinery while reducing assembly time. Starlight Kitchens Group deploys CNC automation to cut lead times to under two weeks for custom orders. Sustainability credentials are equally instrumental: IKEA’s Adelaide outlet achieved renewable-energy-positive status in 2025, showcasing energy autonomy through rooftop PV and battery storage.

Circular-economy initiatives gain prominence as companies pilot refurbished-component buy-back schemes, appealing to eco-conscious consumers and offsetting raw-material inflation. Domestic manufacturers capitalize on made-in-Australia branding, accentuating shorter delivery windows and compliance alignment. Overall, players capable of marrying manufacturing efficiency with memorable customer experiences and omnichannel convenience retain a competitive edge in the Australian kitchen furniture market.

Australia Kitchen Furniture Industry Leaders

IKEA Group

Kaboodle Kitchen (Bunnings Group Limited)

Freedom Kitchens (Steinhoff Asia-Pacific Group)

Kinsman Kitchens (Fletcher Building Ltd.)

Harvey Norman Holdings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: IKEA announced its Adelaide store will operate as the nation’s first renewable-energy-positive retail site.

- February 2025: Starlight Kitchens Group installed new CNC lines, cutting custom lead times to one to two weeks.

- January 2025: Modulr introduced WoodWelding® ultrasonic assembly, enhancing cabinet strength by 30%.

- January 2025: Freedom Kitchens launched AFRDI-approved lines with seven-year warranties to bolster premium positioning.

Australia Kitchen Furniture Market Report Scope

The Australia Kitchen Furniture Market has a lot of elements from basic ameneties like sinks and cabinets to the latese trends of smart modern kitchens and built in furnitures. The Australian market is dominated by Imports mainly from china and Vietnam. Australia Kitchen Furniture Market an be segmented by the type of furniture used ( kitchen cabinets, sinks, worktops, smart appliances/built in furniture and others), by the material used ( stainless steel, plywood, MDF, particle boards, laminate, acrylic, PU, glass, and others), by end user ( residential and commercial), and by the distribution channels (online, offline, imports and exports). This Report offers market size forecasts for the Australia Kitchen Furniture Market in sales by type and value for all the above segments.

By Product

| Kitchen Cabinets |

| Kitchen Chairs |

| Kitchen Tables |

| Other Products (kitchen trolley, cart, pantry shelves, etc.) |

By Material

| Wood |

| Metal |

| Plastic and Polymer |

| Other Materials |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Project |

By Region

| New South Wales |

| Victoria |

| Queensland |

| Western Australia |

| South Australia |

| Tasmania |

| Australian Capital Territory & Northern Territory |

| By Product | Kitchen Cabinets | |

| Kitchen Chairs | ||

| Kitchen Tables | ||

| Other Products (kitchen trolley, cart, pantry shelves, etc.) | ||

| By Material | Wood | |

| Metal | ||

| Plastic and Polymer | ||

| Other Materials | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Project | ||

| By Region | New South Wales | |

| Victoria | ||

| Queensland | ||

| Western Australia | ||

| South Australia | ||

| Tasmania | ||

| Australian Capital Territory & Northern Territory | ||

Key Questions Answered in the Report

What is the current value of the Australian kitchen furniture market?

The Australian kitchen furniture market size reached USD 1.59 billion in 2026 and is projected to grow to USD 2.03 billion by 2031.

Which product segment leads sales?

Kitchen cabinets lead, holding 53.74% of the national value in 2025.

Which state shows the fastest growth?

Queensland is forecast to expand at a 6.14% CAGR through 2031 thanks to migration-driven housing demand.

How significant is online retail for kitchen furniture?

Digital channels already capture around 18% of sales and continue to grow as virtual planning tools improve.

What materials are gaining popularity?

Metal components are the fastest-growing material category, registering a 6.52% CAGR due to durability and smart-system compatibility.

How fragmented is the competitive landscape?

The market is moderately concentrated with the top five players holding just under 40% share, giving a concentration score of 6.

Page last updated on: