Hydrolyzed Wheat Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

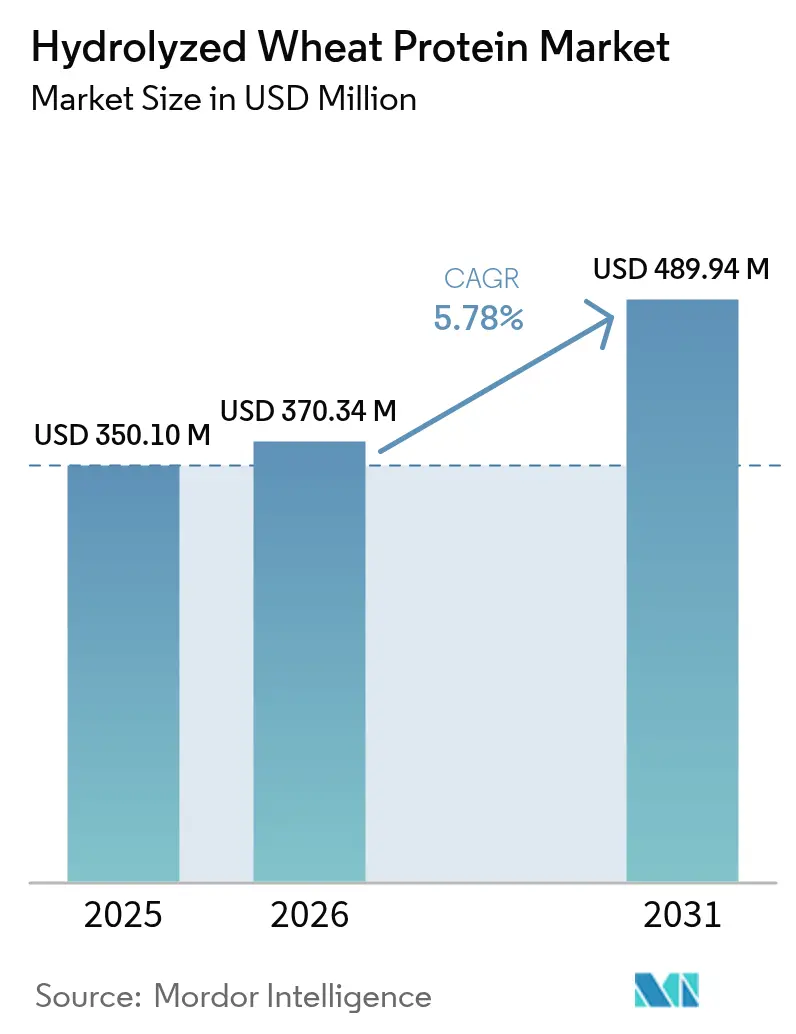

| Market Size (2026) | USD 370.34 Million |

| Market Size (2031) | USD 489.94 Million |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

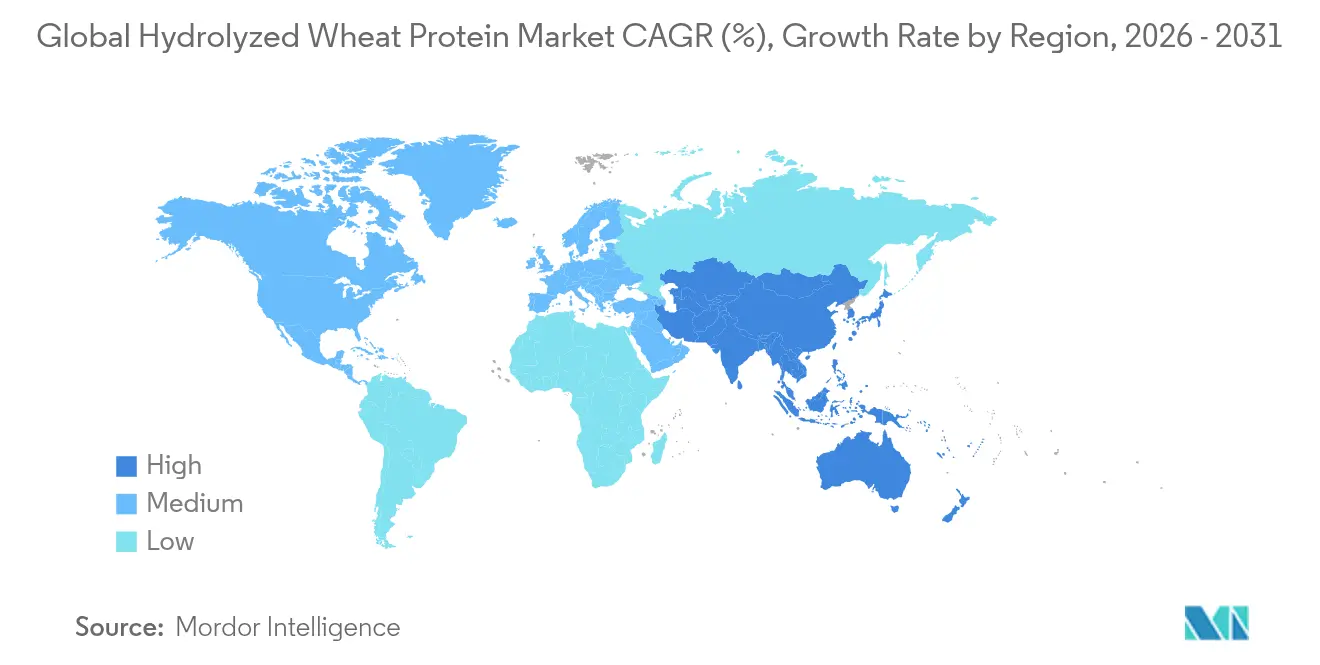

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hydrolyzed Wheat Protein Market Analysis by Mordor Intelligence

The hydrolyzed wheat protein market size is expected to grow from USD 350.10 million in 2025 to USD 370.34 million in 2026 and is forecast to reach USD 489.94 million by 2031 at 5.78% CAGR over 2026-2031. Expanding adoption in cosmetics, premium pet food, and functional beverages is broadening demand well beyond the category’s long-standing bakery core. Growing consumer preference for plant-based nutrition, a sharp rise in clean-label reformulations, and steady progress in extraction technologies are reinforcing this momentum. Powder formats still dominate, but liquid variants are scaling quickly in personal care owing to superior bioavailability. Regionally, Europe retains leadership on the strength of its mature food‐processing base, while Asia-Pacific is accelerating most rapidly as domestic brands commercialize wheat-derived proteins for both food and beauty products.

Key Report Takeaways

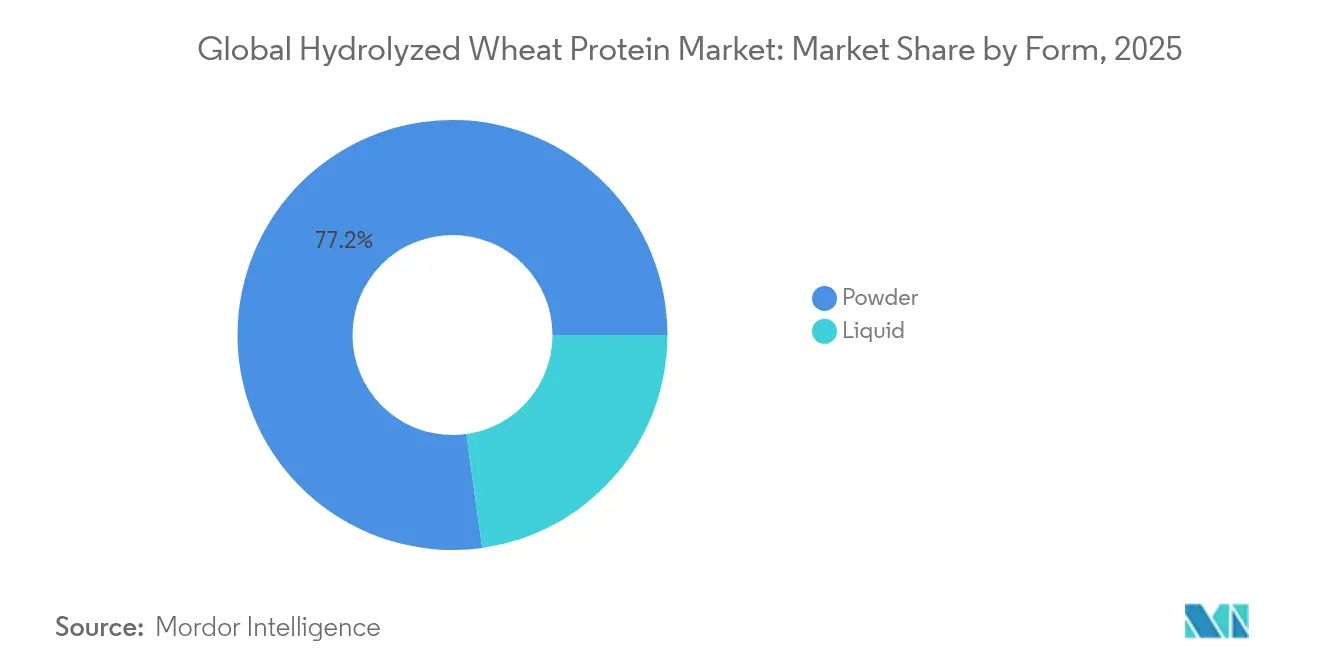

- By form, powder captured 77.21% of the hydrolyzed wheat protein market share in 2025; liquid is advancing at a 5.95% CAGR through 2031.

- By source, conventional wheat protein held 84.10% of the wheat protein market size in 2025, while organic is projected to expand at 8.55% CAGR to 2031.

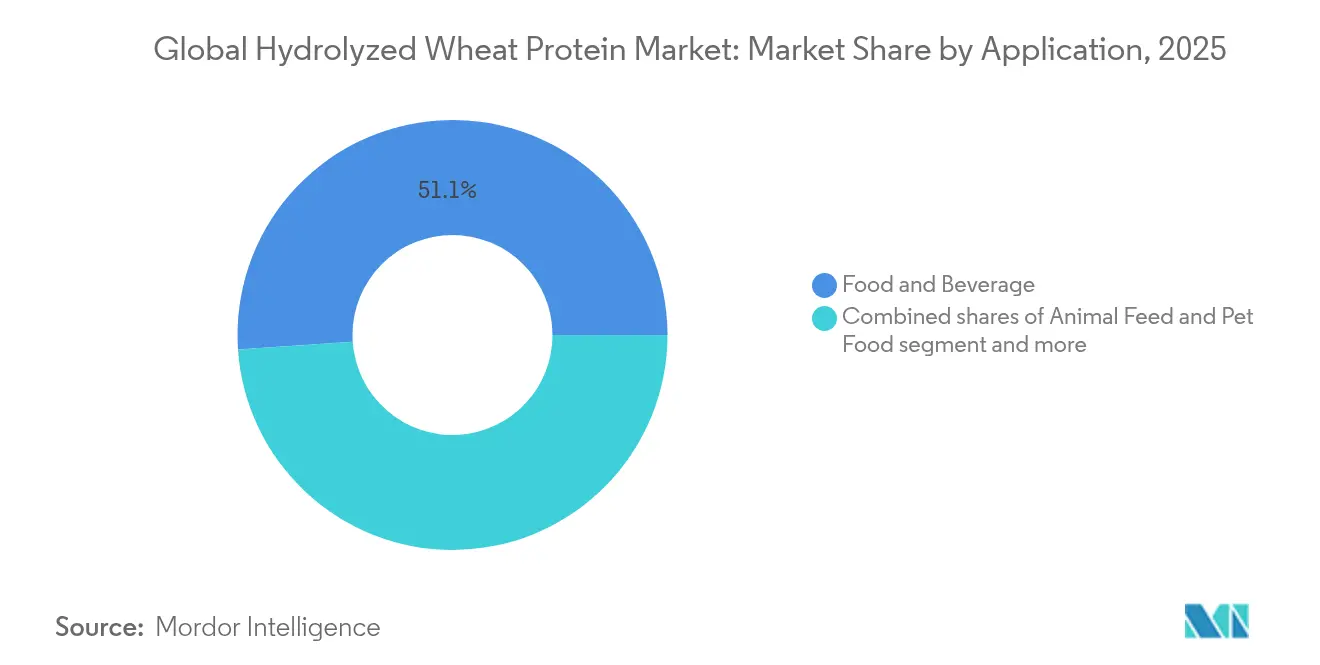

- By application, food and beverage led with 51.07% revenue share in 2025; the cosmetics and personal care segment is forecast to grow at 7.01% CAGR through 2031.

- By geography, Europe accounted for 33.72% of global consumption in 2025, whereas Asia-Pacific is poised for a 6.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydrolyzed Wheat Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of clean-label protein ingredients in functional foods | +1.5% | Global, with stronger influence in Europe and North America | Medium term (2-4 years) |

| Rising demand for hair and skin care products | +1.2% | Global, particularly strong in Asia-Pacific and Europe | Medium term (2-4 years) |

| Innovations in ingredient processing and hydrolysis techniques | +0.9% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Premiumization of pet nutrition | +0.6% | North America and Europe | Medium term (2-4 years) |

| Adoption in sports nutrition and performance products | +0.5% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Increasing incorporation in fortified breakfast cereals and snack bars | +0.4% | Global, particularly strong in North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Clean-Label Protein Ingredients in Functional Foods

The clean-label movement is driving significant growth in wheat protein applications, as consumers increasingly demand transparency in ingredient lists. Backed by Ingredion’s decade-long research and its latest ATLAS findings, clean-label claims have emerged as the leading factor influencing consumers’ willingness to pay premium prices, with such products expected to make up over 70% of portfolios in the European food industry as of 2024[1]Source: Vegconomist, "Ingredion Releases Significant Consumer Insights: Clean-Label is King, 73% of EU Consumers Seek Natural Ingredients", vegconomist.com. This accelerating shift toward clean-label formulations is driving increased adoption of hydrolyzed wheat protein in functional foods, as manufacturers leverage its natural, minimally processed appeal to meet consumer demand for transparency, simple ingredient lists, and perceived healthfulness. This trend is particularly prominent in the bakery and cereal segments, where wheat proteins improve texture and extend shelf life while supporting clean-label compliance. Wheat protein has emerged as a key growth driver within the clean-label food market. Additionally, advancements in gluten-free formulations have expanded the use of wheat protein hydrolysates, as these modified protein hydrolysates maintain functionali ty while addressing allergen-related challenges.

Rising Demand in Hair and Skin Care Products

The integration of wheat protein hydrolysates is witnessing significant growth in premium cosmetic formulations, driven by their superior film-forming capabilities and moisture-retention properties, which deliver measurable performance improvements. In the skincare market, wheat bran extracts are gaining attention for their strong antioxidant and enzyme-inhibitory activities, making them highly effective in anti-aging product applications. As the cosmetics industry increasingly shifts toward naturally-derived and sustainable ingredients, wheat protein is positioning itself as a valuable replacement for synthetic polymers in hair care formulations, offering enhanced combability and a marked reduction in hair breakage, thereby aligning with consumer demand for high-performance, eco-friendly solutions. In 2024, "Natural Skin Care" emerged as the leading global skincare trend on social media, amassing 13,314,140 searches, according to Cult Beauty. This trend reflects a growing consumer preference for products that incorporate natural ingredients and adhere to sustainable practices, indicating a significant transformation in purchasing patterns within the skincare market.

Innovations in Ingredient Processing and Hydrolysis Techniques

Technological advancements in protein extraction and modification are transforming the business potential of wheat protein. Enzymatic hydrolysis has emerged as a highly efficient method for improving the functional properties of wheat gluten. For instance, optimizing pH and temperature conditions significantly enhances hydrolysis efficiency. Membrane filtration and fractionation technologies enable the production of hydrolysates with specific peptide profiles, improving solubility and bioavailability. Process innovations reduce energy consumption and operational costs, making hydrolyzed wheat protein commercially viable for food, cosmetic, and nutraceutical applications. Furthermore, ultrasound-assisted processing has become a critical innovation, expediting reactions to produce bioactive peptides with superior nutritional profiles. These developments are empowering manufacturers to design wheat protein ingredients with tailored functional characteristics, opening new market opportunities beyond traditional applications. A 2025 patent filing introduced a novel fermentation process leveraging specific microbial strains to hydrolyze wheat protein into short peptide chains, delivering improved solubility, enhanced digestibility, and cost efficiencies in production.

Premiumization of Pet Nutrition

The increasing humanization of pets has raised nutritional standards in pet food, driving demand for functional wheat protein ingredients. Premium pet food brands are leveraging hydrolyzed wheat proteins to enhance digestibility and reduce allergen risks while maintaining high protein quality. This approach aligns with broader market strategies, as demonstrated by Post Holdings' focus on premium pet food brands that prioritize superior protein sources. The increase in pet ownership and strengthening human-animal bonds are driving higher demand for premium pet nutrition products focused on health benefits. According to the American Veterinary Medical Association (2024), 45.5% of United States' households own dogs (59.8 million homes) and 32.1% own cats (42.2 million homes)[2]Source: American Veterinary Medical Association, "U.S. pet ownership statistics", avma.org . This large pet population creates a significant consumer base seeking specialized diets that emphasize digestibility, protein quality, and health benefits. Hydrolyzed wheat protein, which offers improved absorption, lower allergenicity, and supports muscle and gut health, is becoming more common in premium pet foods, making it an important ingredient in this growing market segment. Wheat protein hydrolysates are particularly valued in premium formulations for their role in improving palatability and digestibility, as well as supporting muscle maintenance in aging pets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Allergen concerns related to gluten content | -0.9% | Global, particularly significant in North America and Europe | Medium term (2-4 years) |

| Competition from alternative plant proteins (pea, rice) in clean-label formulations | -0.6% | Global, with stronger impact in North America and Europe | Long term (≥ 4 years) |

| High production costs associated with hydrolyzed wheat protein | -0.7% | Global, with particular impact in price-sensitive markets | Short term (≤ 2 years) |

| Limited consumer awareness in emerging markets | -0.5% | Asia-Pacific, Latin America, and Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Allergen Concerns Related to Gluten Content

Increased awareness of gluten sensitivity and celiac disease is hindering the growth of the wheat protein market, particularly in regions with strict allergen labeling regulations and high diagnosis rates. The rising prevalence of gluten-related disorders has driven manufacturers to focus on alternative formulations, thereby limiting the application potential of wheat protein. The ongoing challenges in developing gluten-free products that deliver functional properties comparable to wheat-based alternatives. However, advancements in enzymatic hydrolysis are addressing these challenges by creating wheat protein derivatives with reduced allergenicity while retaining functional benefits. These modified proteins are gaining acceptance in markets with heightened gluten sensitivity awareness, although regulatory barriers and consumer perception issues remain significant obstacles.

Competition from Alternative Plant Proteins (Pea, Rice) in Clean-Label Formulations

The rapid advancement of alternative plant-based proteins is creating significant competitive dynamics within the wheat protein market. Among these alternatives, pea protein has emerged as a prominent contender, driven by its hypoallergenic properties and its classification as a complete protein with a comprehensive amino acid profile. Beyond Meat's 2025 financial report underscores this trend, revealing the incorporation of a protein blend, including pea protein, rice protein, faba bean protein, and wheat gluten, into their latest product formulations. This development highlights the intensifying competition posed by alternative proteins. Nevertheless, wheat protein continues to hold a strategic advantage in specialized applications, where its distinctive viscoelastic properties provide functional benefits that remain unmatched by other substitutes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Form: Liquid Formulations Gain Momentum in Specialized Applications

The hydrolyzed wheat protein market remains dominated by powder formulations, which held 77.21% market share in 2025, owing to their stability, ease of transportation, and versatility across multiple applications. However, liquid wheat protein variants are emerging as the fastest-growing segment, with a projected CAGR of 5.95% from 2026 to 2031. This growth is primarily attributed to increasing demand in the cosmetics and personal care industry, where liquid formulations integrate effectively into water-based systems and deliver improved bioavailability.

Powder formats continue to dominate food applications due to their extended shelf life and compatibility with dry mixing processes, particularly in bakery premixes and protein-enriched flour blends. Advancements in microencapsulation technology have enhanced the dispersibility of powdered wheat proteins, addressing previous functionality challenges while retaining the operational benefits of dry formats.

Source: Organic Segment Outpaces Conventional Despite Premium Pricing

Conventional wheat protein dominated the market with 84.10% share in 2025, benefiting from established supply chains and cost advantages. However, the organic segment is anticipated to grow at a robust 8.55% CAGR through 2031, significantly outpacing the overall market. This growth highlights the increasing demand for certified organic ingredients, particularly in premium food and personal care industries. Although organic wheat protein commands a price premium of 30-40% over conventional options, its adoption remains strong in high-value applications where clean-label positioning justifies the higher costs.

European manufacturers are expanding their organic wheat protein production capacity to meet the growing consumer demand for plant-based proteins. Several facilities have obtained dual certification for organic and conventional production methods, allowing them to efficiently serve both conventional and organic markets. The yield gap between organic and conventional wheat cultivation decreased to 15% in 2024 from 25% in 2020, driven by improved farming techniques and technological advancements in organic agriculture. This reduction in the yield gap has significantly improved the economic feasibility of organic wheat protein production, making it more attractive for manufacturers to invest in organic product lines.

Application: Cosmetics and Personal Care Emerges as Growth Hotspot

The food and beverage sector dominated the wheat protein market in 2025, representing 51.07% of total consumption. Bakery products, including bread, pastries, and baked snacks, led the segment's growth due to wheat protein's ability to enhance dough strength and texture. The meat alternatives subsegment emerged as the second-largest application, where wheat gluten's unique viscoelastic properties effectively mimic the fibrous structure and chewy texture of conventional meat products. The protein's functional characteristics, such as water absorption and binding capabilities, make it particularly suitable for these applications.

The cosmetics and personal care segment is anticipated to grow at the fastest rate, with a projected CAGR of 7.01% through 2031, driven by the increasing adoption of wheat protein hydrolysates in premium hair care and skincare products. Wheat bran extracts demonstrate significant enzyme-inhibitory properties against collagenase and elastase, reinforcing their effectiveness in anti-aging skincare solutions. Furthermore, the animal feed and pet food segment has exhibited strong growth, particularly in the premium pet nutrition market, where hydrolyzed wheat proteins enhance digestibility, improve nutritional profiles, and address allergenicity concerns.

Geography Analysis

Europe maintained its position as the largest regional market for wheat protein in 2025, accounting for 33.72% of global consumption. This leadership is driven by the region's advanced food processing industry, strong consumer demand for plant-based proteins, and regulatory frameworks promoting clean-label ingredients. Germany, France, and the UK dominate the European wheat protein market, with bakery applications serving as the primary growth driver. Recent regulatory approvals, such as the European Food Safety Authority's endorsement of hydrolyzed wheat protein as a food ingredient, have further enhanced the market's growth potential.

Asia-Pacific is anticipated to be the fastest-growing market, with a projected CAGR of 6.66% through 2031. This growth is attributed to the rapid industrialization of food processing, rising disposable incomes, and increasing consumer awareness of plant-based proteins. China and India present significant growth opportunities, leveraging domestic wheat production to achieve cost-efficient protein extraction. The cosmetics and personal care segment is experiencing robust growth in Asia-Pacific, with wheat protein hydrolysates increasingly used in premium hair care products tailored to regional consumer preferences. This diversification is enabling manufacturers to develop market-specific formulations that cater to local application needs and consumer demands.

North America, while a mature market, continues to drive innovation, with wheat protein applications expanding into high-value segments such as cosmetics and premium pet nutrition. The region's emphasis on clean-label formulations has positioned wheat protein as a preferred alternative to synthetic ingredients across various industries. The United States leads regional consumption, while Canada and Mexico are emerging as growing markets.

Competitive Landscape

The hydrolyzed wheat protein market demonstrates moderate fragmentation, comprising a mix of large multinational ingredient corporations and specialized protein producers. Key players such as Archer Daniels Midland Company, Cargill, Incorporated, Roquette Frères, MGP Ingredients, Inc., and Kerry Group plc leverage their integrated supply chains and advanced research and development capabilities to sustain their competitive advantage. These companies frequently establish agreements and partnerships with local firms to expand their global footprint and launch products aligned with shifting consumer preferences. Markets with a significant consumer base serve as critical hubs for hydrolyzed wheat protein manufacturers.

Businesses are increasingly emphasizing technological advancements as a core strategy to achieve differentiation in the competitive landscape. They are strategically allocating resources and investing in cutting-edge extraction and modification processes to develop wheat protein ingredients with enhanced functional properties. This approach not only addresses shifting consumer preferences but also strengthens their market positioning and long-term growth potential.

Emerging players are identifying growth opportunities in niche segments, particularly in organic wheat protein and customized hydrolysates for specific applications. These smaller firms utilize their agility and specialized expertise to deliver tailored solutions for high-value markets, fostering a competitive environment despite the dominance of established players. Additionally, the growing emphasis on sustainability and clean-label formulations has created opportunities for companies capable of offering wheat protein ingredients with strong environmental credentials and transparent supply chains.

Hydrolyzed Wheat Protein Industry Leaders

-

Archer Daniels Midland Company

-

Cargill, Incorporated

-

Roquette Frères

-

MGP Ingredients, Inc.

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2023: Roquette inaugurated its new Food Innovation Center at its site in Lestrem, France. The center provides formulators with technical and research and development support, equipment, laboratories, and scale-up testing facilities. The facility aims to support innovation and expedite new product development for market introduction.

- February 2022: MGP Ingredients, Inc. planned to build a USD 16.7 million extrusion plant next to its facility in Atchison, Kansas. The plant, designed by Sabetha-based 1 Solutions Group, was completed in late 2023. The facility produces up to 10 million pounds of ProTerra, MGP's texturized plant-based protein line, per year.

Global Hydrolyzed Wheat Protein Market Report Scope

Hydrolyzed Wheat Protein, a water-soluble protein, originates from wheat kernels and is processed into smaller peptides. The hydrolyzed wheat protein market is segmented by form, source, application, and geography. Based on form, the market is segmented into powder and liquid. Based on the source, the market is segmented into conventional wheat and organic wheat. Based on application, the market is segmented into food & beverage, animal feed, and cosmetics & personal care. The food & beverage segment is further segmented into bakery, cereals & cereal products, confectionery, RTD beverages & powder mixes, and others. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Powder |

| Liquid |

| Conventional Wheat |

| Organic Wheat |

| Food and Beverage | Bakery |

| Cereals and Cereal Products | |

| Confectionery | |

| RTD Beverages and Powder Mixes | |

| Others | |

| Animal Feed and Pet Food | |

| Cosmetics and Personal Care |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Powder | |

| Liquid | ||

| By Source | Conventional Wheat | |

| Organic Wheat | ||

| By Application | Food and Beverage | Bakery |

| Cereals and Cereal Products | ||

| Confectionery | ||

| RTD Beverages and Powder Mixes | ||

| Others | ||

| Animal Feed and Pet Food | ||

| Cosmetics and Personal Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What factors are driving growth in the hydrolyzed wheat protein market?

Demand for clean-label food reformulations, expanding use in cosmetics, and technology-driven improvements in protein extraction are the principal growth engines detailed above.

Which form of wheat protein is growing fastest?

Liquid wheat protein is forecast to advance at 5.95% CAGR through 2031 as personal-care formulators prefer fully soluble actives.

How significant is Asia-Pacific to future market expansion?

Asia-Pacific is projected to deliver the highest regional CAGR at 6.66% to 2031, led by China and India.

Why is wheat protein attractive to pet food manufacturers?

Hydrolyzed wheat protein offers easy digestibility and low allergenicity, enabling premium positioning in senior-pet and limited-ingredient diets.

Page last updated on: