North America Wheat Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

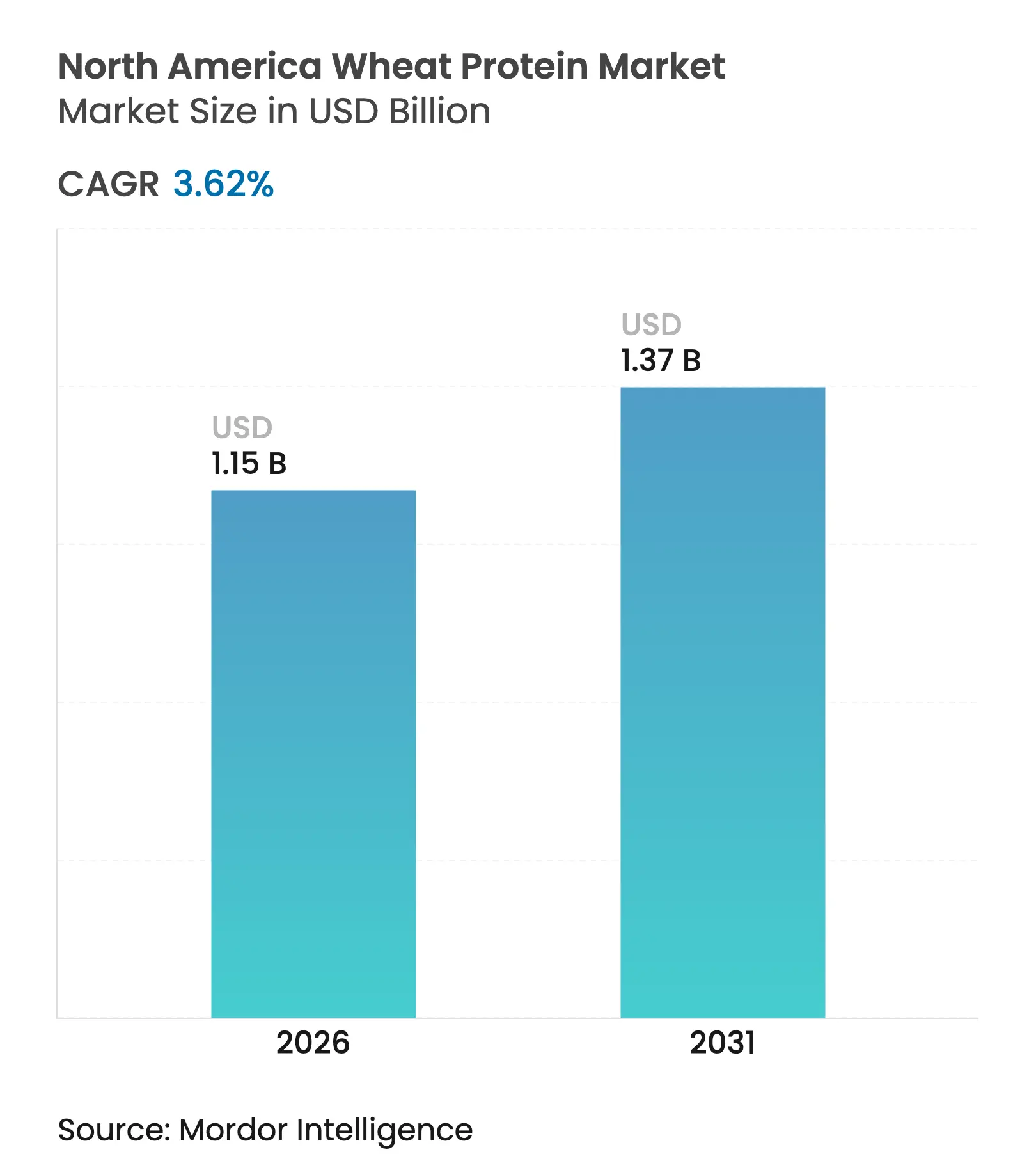

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 1.37 Billion |

| Growth Rate (2026 - 2031) | 3.62 % CAGR |

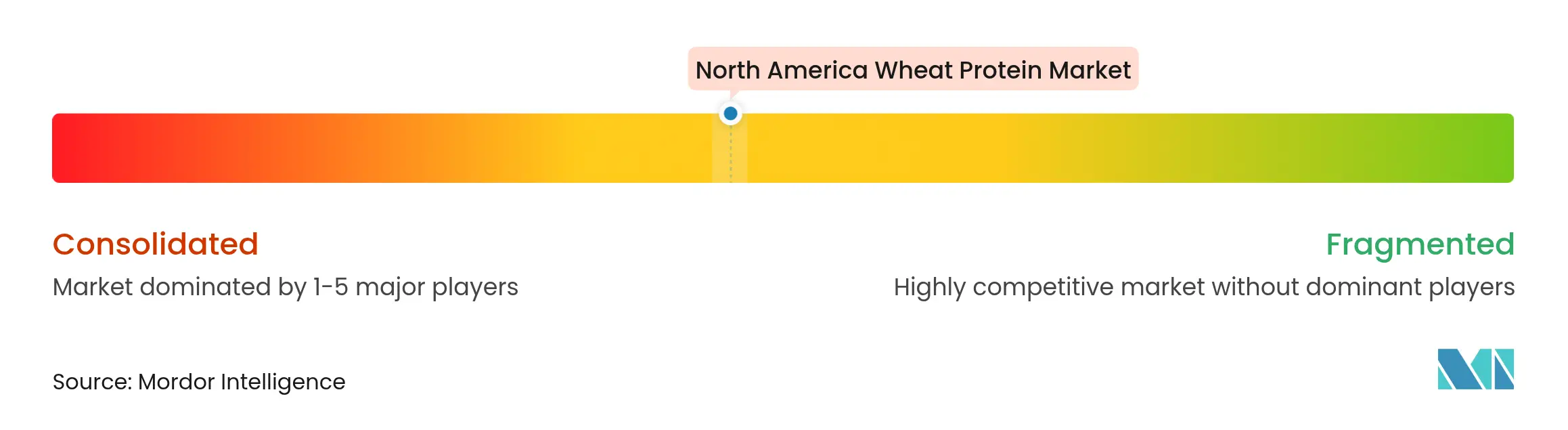

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

North America Wheat Protein Market Analysis by Mordor Intelligence

The North American wheat protein market size was valued at USD 1.11 billion in 2025 and estimated to grow from USD 1.15 billion in 2026 to reach USD 1.37 billion by 2031, at a CAGR of 3.62% during the forecast period (2026-2031). Steady growth reflects stable wheat production, rising demand for plant-based proteins, and clean label preferences. U.S. wheat output climbed to 1.97 billion bushels in 2024, the highest level in eight years, while Canadian production is projected at 35.6 million tonnes for 2025-26, creating an abundant raw-material supply, according to the United States Department of Agriculture[1]Source: USDA Economic Research Service, “Wheat Data Highlights,” usda.gov. Technological differentiation in isolates and hydrolyzed variants is unlocking premium applications across food, feed, and cosmetics. Regenerative agriculture programs in Canada are scaling organic wheat protein, capturing sustainability premiums, and reinforcing the North American wheat protein market’s resilience.

Key report Takeaways

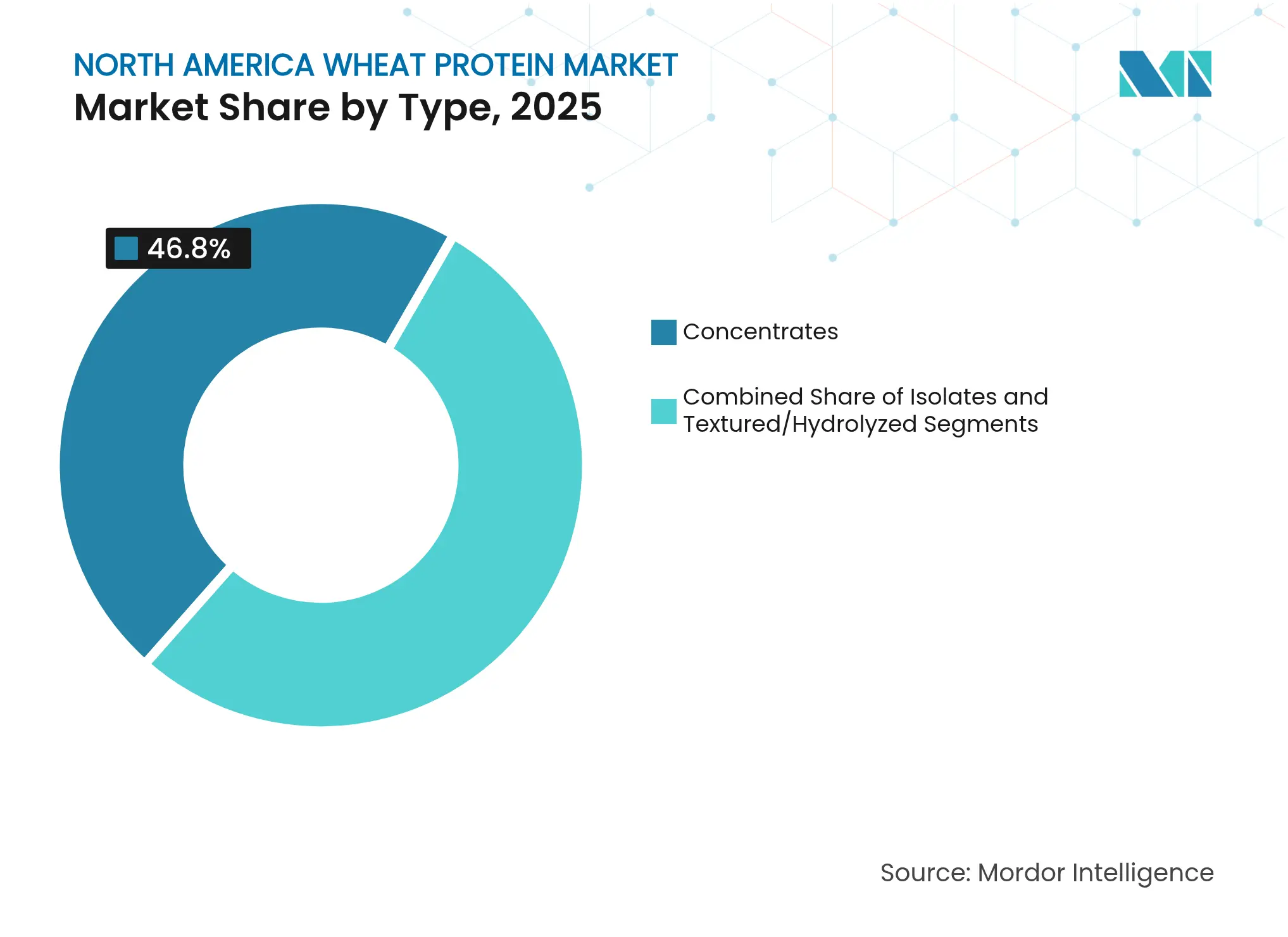

- By type, concentrates led with 46.80% of the North American wheat protein market share in 2025, while textured/hydrolyzed variants are projected to grow at a 4.95% CAGR during 2026-2031.

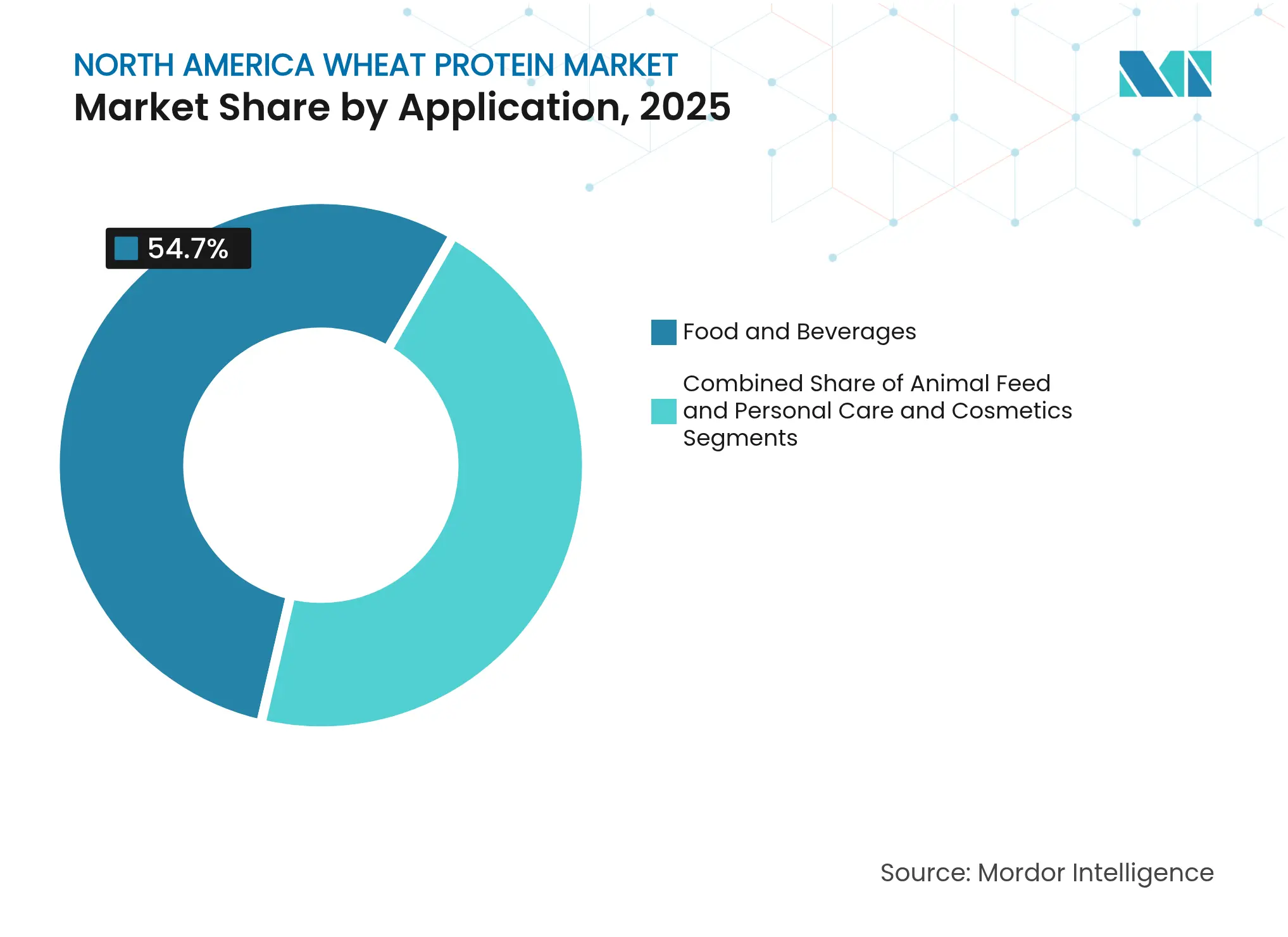

- By application, bakery and snacks held 54.70% of the North American wheat protein market size in 2025; animal feed is advancing at a 4.68% CAGR through 2031.

- By nature, conventional products commanded a 91.40% share in 2025, whereas organic wheat proteins are forecast to expand at a 5.64% CAGR to 2031.

- By geography, the United States captured 83.90% revenue share in 2025; Canada is projected to log the highest 4.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Wheat Protein Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecasts | Geographic relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Expanding Applications in Processed Foods Expanding Applications in Processed Foods | +0.8% | North America, with concentration in US Midwest processing hubs | Medium term (2-4 years) | (~) % Impact on CAGR Forecasts:+0.8% | Geographic relevance:North America, with concentration in US Midwest processing hubs | Impact Timeline:Medium term (2-4 years) |

Rising Demand for Clean Label and Non-GMO Product Categories Rising Demand for Clean Label and Non-GMO Product Categories | +0.6% | US and Canada, particularly urban markets | Short term (≤ 2 years) | |||

Rising Demand for Plant-Based Proteins in Plant-Based Meat Alternatives Rising Demand for Plant-Based Proteins in Plant-Based Meat Alternatives | +0.7% | North America, led by US West Coast and Canadian urban centers | Medium term (2-4 years) | |||

Canadian Regenerative Wheat Farming Unlocking Scalable Organic Protein Supply Canadian Regenerative Wheat Farming Unlocking Scalable Organic Protein Supply | +0.4% | Canada, with spillover to US organic markets | Long term (≥ 4 years) | |||

Hydrolyzed Wheat Protein Uptake in Personal Care Products Hydrolyzed Wheat Protein Uptake in Personal Care Products | +0.3% | North America, concentrated in cosmetics manufacturing regions | Medium term (2-4 years) | |||

Growing Adoption of Wheat Protein in Animal and Pet Food Growing Adoption of Wheat Protein in Animal and Pet Food | +0.5% | North America, particularly aquaculture regions and pet food manufacturing centers | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Expanding Applications in Processed Foods

The processed food sector's protein fortification drive is reshaping wheat protein demand patterns beyond traditional bakery applications. MGP Ingredients' Arise wheat protein isolate has gained traction in keto-friendly snack formulations, where its viscoelastic properties enable high-protein content without compromising texture. This application expansion reflects a broader industry shift toward functional ingredients that address multiple nutritional objectives simultaneously. The trend is particularly pronounced in ready-to-eat and ready-to-cook food segments, where wheat protein serves as both a nutritional enhancer and a processing aid. Protein integration in baked goods has evolved beyond simple fortification to include fermented protein applications that create complete amino acid profiles. The processed food sector's embrace of wheat protein is accelerating as manufacturers seek declaration-friendly alternatives to synthetic additives, positioning wheat protein as a clean-label solution that meets consumer transparency demands.

Rising Demand for Clean Label and Non-GMO Product Categories

Clean label imperatives are driving wheat protein adoption as food manufacturers eliminate synthetic additives and embrace recognizable ingredients. U.S. Wheat Associates has identified clean label implications as a critical factor influencing wheat food production strategies, with manufacturers increasingly prioritizing ingredient transparency. The movement extends beyond simple ingredient substitution to encompass supply chain transparency, where wheat protein's agricultural traceability provides competitive advantages. BENEO's BeneoPro VWG wheat protein exemplifies this trend, offering clean label status alongside high solubility and excellent binding capacity for diverse food applications. The regulatory environment supports this trend, with FDA guidance emphasizing early safety evaluation of new proteins while maintaining established pathways for traditional wheat derivatives.

Rising Demand for Plant-Based Proteins in Plant-Based Meat Alternatives

Plant-based meat manufacturers are increasingly incorporating wheat gluten to achieve authentic texture profiles that replicate traditional meat characteristics. Beyond Meat's formulation strategy demonstrates this approach, utilizing wheat gluten alongside pea, rice, and faba bean proteins to create complex protein matrices that deliver meat-like sensory experiences. The alternative protein market's evolution toward hybrid formulations reflects technical challenges in achieving optimal texture using single protein sources, where wheat protein's unique viscoelastic properties provide critical functionality. Research on ingredient functionality reveals that wheat protein's heat response characteristics differ significantly from other plant proteins, offering distinct advantages in extrusion processing for meat analogues. This growth trajectory is supported by increasing consumer acceptance of plant-based products and technological advances in protein processing that enhance wheat protein's functionality in meat alternative applications.

Canadian Regenerative Wheat Farming Unlocking Scalable Organic Protein Supply

Canadian regenerative agriculture initiatives are establishing sustainable wheat protein supply chains that address organic market demands while improving soil health. Ceres Global Ag Corp's expanded partnership with Miller Milling has grown from 4,500 acres to 16,800 acres, focusing on nutrient use efficiency and greenhouse gas emission reduction throughout the wheat production cycle. This scaling demonstrates how regenerative practices can achieve commercial viability while meeting sustainability objectives. The Canadian wheat production forecast of 35.6 million tonnes for 2025-26 provides substantial raw material availability for protein extraction, with quality improvements supporting premium applications, according to the Foreign Agricultural Service. Regenerative farming's integration with wheat protein supply chains represents a strategic response to consumer demands for environmentally responsible ingredients, positioning Canadian producers to capture premium pricing in organic and sustainable protein markets.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Prevalence of Gluten Sensitivity and Celiac Disease Rising Prevalence of Gluten Sensitivity and Celiac Disease | -0.4% | North America, particularly among non-Hispanic whites | Short term (≤ 2 years) | (~) % Impact on CAGR Forecasts:-0.4% | Geographic Relevance:North America, particularly among non-Hispanic whites | Impact Timeline:Short term (≤ 2 years) |

Growing Popularity of Gluten-Free Alternatives Growing Popularity of Gluten-Free Alternatives | -0.3% | US and Canada, concentrated in health-conscious demographics | Medium term (2-4 years) | |||

Availability and Preference for Other Plant-Based Proteins Availability and Preference for Other Plant-Based Proteins | -0.5% | North America, led by pea and soy protein adoption | Medium term (2-4 years) | |||

Fluctuating Raw Material Prices Fluctuating Raw Material Prices | -0.2% | North America, particularly US wheat-producing regions | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of Gluten Sensitivity and Celiac Disease

According to Celiac Australia[2]Source: Celiac Australia, "Celiac Diseases", www.coeliac.org.au data from 2024, 1 in 70 Australians has celiac disease. The condition affects patients beyond gastrointestinal symptoms, with manifestations that impact overall quality of life and require strict gluten-free diets. This dietary requirement influences market segmentation, as companies must balance developing wheat protein products for non-sensitive consumers while considering gluten-sensitive populations, which affects the addressable market size in certain demographics. The prevalence of celiac disease has prompted food manufacturers to invest in research and development of alternative protein sources and gluten-free formulations. Additionally, the growing awareness of celiac disease and gluten sensitivity has led to increased demand for clear product labeling and dedicated manufacturing facilities to prevent cross-contamination, further impacting production costs and market dynamics. The rise in diagnosis rates and improved testing methods have also contributed to market growth, with manufacturers expanding their product portfolios to include specialized gluten-free options. Furthermore, regulatory bodies have implemented stricter guidelines for gluten-free certification and labeling requirements, ensuring consumer safety while creating additional compliance considerations for industry participants.

Growing Popularity of Gluten-Free Alternatives

The gluten-free product category's expansion reflects both medical necessity and lifestyle choices, with about 7% of the population following gluten-free diets in the United States, according to the International Food Information Council data from 2024[3]Source: International Food Information Council, "Gluten-Free Food Consumption in the United States", www.foodinsight.org. This trend creates competitive pressure on wheat protein applications as manufacturers develop alternative protein solutions to capture gluten-sensitive consumers. The pet food industry's previous embrace of grain-free formulations, despite subsequent FDA warnings about potential health risks, demonstrates how gluten-free trends can reshape entire market segments. Food fraud concerns in plant-based proteins, including wheat derivatives, have intensified scrutiny of ingredient authenticity and labeling accuracy, potentially affecting consumer confidence in wheat protein products. The gluten-free alternative market's growth trajectory suggests sustained competitive pressure on wheat protein applications, requiring strategic positioning that emphasizes unique functional benefits unavailable in gluten-free alternatives while acknowledging market segmentation realities.

Segment Analysis

By Type: Concentrates Lead While Hydrolyzed Variants Drive Innovation

Wheat protein concentrates command 46.80% market share in 2025, reflecting their established role in traditional food applications where moderate protein content and cost-effectiveness drive adoption. The concentrates segment's dominance stems from its versatility across bakery, snack, and processed food categories, where protein levels provide sufficient functionality without premium pricing. Isolates represent a smaller but growing segment, targeting specialized applications requiring higher protein purity and specific functional characteristics.

Textured and hydrolyzed wheat proteins emerge as the fastest-growing segment at 4.95% CAGR through 2031, driven by innovation in plant-based meat alternatives and personal care applications where modified protein structures deliver enhanced functionality. The type segmentation's evolution reflects technological advancement in protein processing, with hydrolyzed variants gaining traction in cosmetic formulations and specialized food applications. The textured segment's growth trajectory aligns with plant-based meat market expansion, where wheat protein's unique viscoelastic properties provide texture advantages that complement other plant proteins in hybrid formulations.

Note: Segment shares of all individual segments available upon report purchase

By Nature: Conventional Dominance Challenged by Organic Acceleration

Conventional wheat proteins maintain 91.40% market share in 2025, reflecting established supply chains and cost advantages that support mass market applications. The conventional segment's dominance is reinforced by wheat gluten's GRAS status under FDA regulations, providing regulatory certainty for food manufacturers. However, organic wheat proteins accelerate at 5.64% CAGR through 2031, driven by consumer preferences for sustainable and transparent ingredients. This growth differential signals a strategic inflection point where organic premiums justify supply chain investments and processing modifications.

The organic segment's acceleration reflects broader clean label trends where ingredient transparency and environmental responsibility influence purchasing decisions. Research on perennial wheat varieties demonstrates higher protein content in sustainable farming systems, though processing challenges remain for commercial applications. The nature segmentation's evolution suggests that organic wheat proteins will capture increasing market share as supply chain capabilities mature and consumer willingness to pay premiums for sustainable ingredients strengthens.

By Application: Food and Beverage Dominance Meets Animal Feed Innovation

The food and beverages segment maintains 54.70% market share in 2025, leveraging wheat protein's traditional functionality in dough strengthening and texture enhancement. This application dominance reflects wheat protein's established role in bread, pasta, and snack manufacturing, where gluten's viscoelastic properties provide irreplaceable functionality. Ready-to-eat and ready-to-cook food products represent emerging opportunities within the food and beverages category, driven by protein fortification trends and convenience demands. Condiments and sauces applications utilize wheat protein for thickening and stabilization, though market share remains limited compared to primary food categories.

Animal feed emerges as the fastest-growing application at 4.68% CAGR through 2031, driven by aquaculture industry adoption and sustainable protein sourcing initiatives. Personal care and cosmetics applications represent a niche but growing segment, where hydrolyzed wheat protein provides conditioning and moisturizing properties in hair care and skin care formulations. Flint Hills Resources' USD 50 million investment in high-protein feed ingredient technology demonstrates industry commitment to animal nutrition applications. The application segmentation's evolution toward animal feed and personal care reflects wheat protein's versatility beyond traditional food uses, opening new revenue streams that complement core bakery applications.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

In 2025, the U.S. secured a dominant 83.90% share of the North American wheat protein market, thanks to its integrated supply chains that link wheat-producing regions directly to protein processing facilities and food manufacturers. Hard red spring wheat production in the Northern Plains provides high-protein raw materials essential for premium wheat protein applications, with protein content advantages driving export competitiveness. The domestic market benefits from diverse application demands spanning food processing, animal feed, and emerging personal care segments, creating stable demand foundations that support processing capacity investments. Regulatory advantages include established GRAS status for wheat gluten and comprehensive food safety frameworks that facilitate market access for wheat protein derivatives.

The Canadian wheat protein market is projected to grow at a CAGR of 4.52% through 2031. Canada, the world's third-largest wheat exporter, is bolstering investments in protein processing. As the quality of Canadian wheat improves, it opens doors to premium applications. Regenerative farming partnerships, exemplified by Ceres Global Ag Corp's expanded program with Miller Milling in September 2024, are establishing sustainable protein supply chains that command premium pricing in organic and environmentally conscious markets. Canadian wheat protein producers benefit from proximity to U.S. markets while accessing distinct regulatory frameworks that support organic and sustainable product positioning.

Mexico and the Rest of North America represent emerging opportunities with growth potential constrained by limited wheat production and processing infrastructure. Mexico's wheat protein market development depends on import relationships with U.S. and Canadian suppliers, creating opportunities for cross-border supply chain integration. The region's food processing industry growth, particularly in snack foods and convenience products, generates increasing wheat protein demand that exceeds domestic production capabilities. Trade relationships within the USMCA framework facilitate wheat protein flows across North American borders, supporting market integration and supply chain optimization.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

The North American wheat protein market shows moderate consolidation, with major agribusiness companies competing alongside specialized protein processors. Market leaders maintain their positions through vertical integration, controlling wheat sourcing, processing operations, and distribution channels. Companies implement comprehensive supply chain management strategies to ensure consistent product quality and market availability. These established players leverage their extensive resources and infrastructure to maintain cost efficiency and market dominance.

Companies focus on technological advancement to differentiate their products in an increasingly competitive landscape. Investments in protein modifications, clean label formulations, and sustainable sourcing practices drive product innovation and market growth. The industry's shift toward premium offerings reflects growing consumer demand for specialized wheat protein products. Market participants actively develop new processing techniques and formulations to capture higher-value market segments.

New market entrants target specialized applications and develop innovative processing methods that provide alternatives to conventional wheat protein products. Growth opportunities exist in personal care products, where hydrolyzed wheat protein serves as a natural alternative to synthetic ingredients, and in animal feed, where companies seek diverse protein sources for sustainability. Success in the market increasingly depends on technical innovation and supply chain transparency. Companies that demonstrate both product performance and environmental stewardship gain competitive advantages in this evolving market landscape.

North America Wheat Protein Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Tritica Biosciences launched the Wheat-Based Protein Synthesis platform. Tritica Biosciences LLC, along with three partners, collaborated with Ginkgo Bioworks of Boston on a USD 29 million contract with the Advanced Research Projects Agency for Health (ARPA-H). The contract spans two years.

- April 2025: ACI Group introduced high-performance plant-based proteins to help manufacturers address changing consumer dietary preferences. The product range includes wheat protein crispies and serves multiple applications, including dairy alternatives, beverages, desserts, and meat substitutes. The proteins enable manufacturers to achieve specific formulation requirements, including neutral flavor profiles, increased protein content, enhanced texture, and clean-label characteristics.

- November 2023: Amber Wave launched a wheat protein facility with investment from Summit Agricultural Group. The facility features a fully automated 27,500-centum Sangati Berga mill, automation technology and air handling systems from Kice Industries, gluten extraction and drying equipment from Flottweg and VetterTec, and packaging equipment from Premier Tech.

- February 2023: Amber Wave opened North America's largest protein facility in the United States. The facility produces the company's AmberPro Vital Wheat Gluten, which has applications in the pet food, specialty feed, commercial baking, alternative meat, and food ingredient industries.

Table of Contents for North America Wheat Protein Industry Report

1. INTRODUCTION

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Expanding Applications in Processed Foods

- 4.2.2Rising Demand for Clean Label and Non-GMO Product Categories

- 4.2.3Rising Demand for Plant-Based Proteins in Plant-Based Meat Alternatives

- 4.2.4Canadian regenerative wheat farming unlocking scalable organic protein supply

- 4.2.5Hydrolyzed Wheat Protein Uptake in Personal Care Products

- 4.2.6Growing Adoption of Wheat Protein in Animal and Pet Food

- 4.3Market Restraints

- 4.3.1Rising Prevelance of Gluten Sensitivity and Celiac Disease

- 4.3.2Growing Popularity of Gluten-Free Alternatives

- 4.3.3Availability and Preference for Other Plant-Based Proteins

- 4.3.4Fluctuating Raw Material Prices

- 4.4Supply-Chain Analysis

- 4.5Regulatory Outlook

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

- 4.8Patent Analysis

5. MARKET SIZE AND GROWTH FORECASTS

- 5.1By Type

- 5.1.1Concentrates

- 5.1.2Isolates

- 5.1.3Textured/Hydrolyzed

- 5.2By Nature

- 5.2.1Conventional

- 5.2.2Organic

- 5.3By Application

- 5.3.1Food & Beverages

- 5.3.1.1Bakery & Snacks

- 5.3.1.2Breakfast Cereals

- 5.3.1.3Meat/Poultry/Seafood and Meat Alternative Products

- 5.3.1.4RTE/RTC Food Products

- 5.3.1.5Condiments/Sauces

- 5.3.2Animal Feed

- 5.3.3Personal Care & Cosmetics

- 5.4By Geography

- 5.4.1United States

- 5.4.2Canada

- 5.4.3Mexico

- 5.4.4Rest of North America

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1Archer-Daniels-Midland Company

- 6.4.2Cargill, Incorporated

- 6.4.3MGP Ingredients Inc.

- 6.4.4Roquette Freres SA

- 6.4.5Tereos S.A.

- 6.4.6Manildra Group

- 6.4.7Crespel & Deiters GmbH & Co. KG

- 6.4.8Kroner-Starke GmbH

- 6.4.9Glico Nutrition Co. Ltd.

- 6.4.10Kerry Group plc

- 6.4.11Tate & Lyle PLC

- 6.4.12CropEnergies AG

- 6.4.13Ardent Mills LLC

- 6.4.14Permolex International L.P.

- 6.4.15PureField Ingredients LLC

- 6.4.16Jackering Gruppe

- 6.4.17Amber Wave USA

- 6.4.18BENEO GmbH

- 6.4.19Planture (US broker)

- 6.4.20American Key Food Products

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

North America Wheat Protein Market Report Scope

North America wheat protein market is segmented by type (wheat concentrate, wheat protein isolate, and textured wheat protein), by application (bakery and confectionery, dairy products, nutritional supplements, and others), and geography.