Fish Protein Hydrolysate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

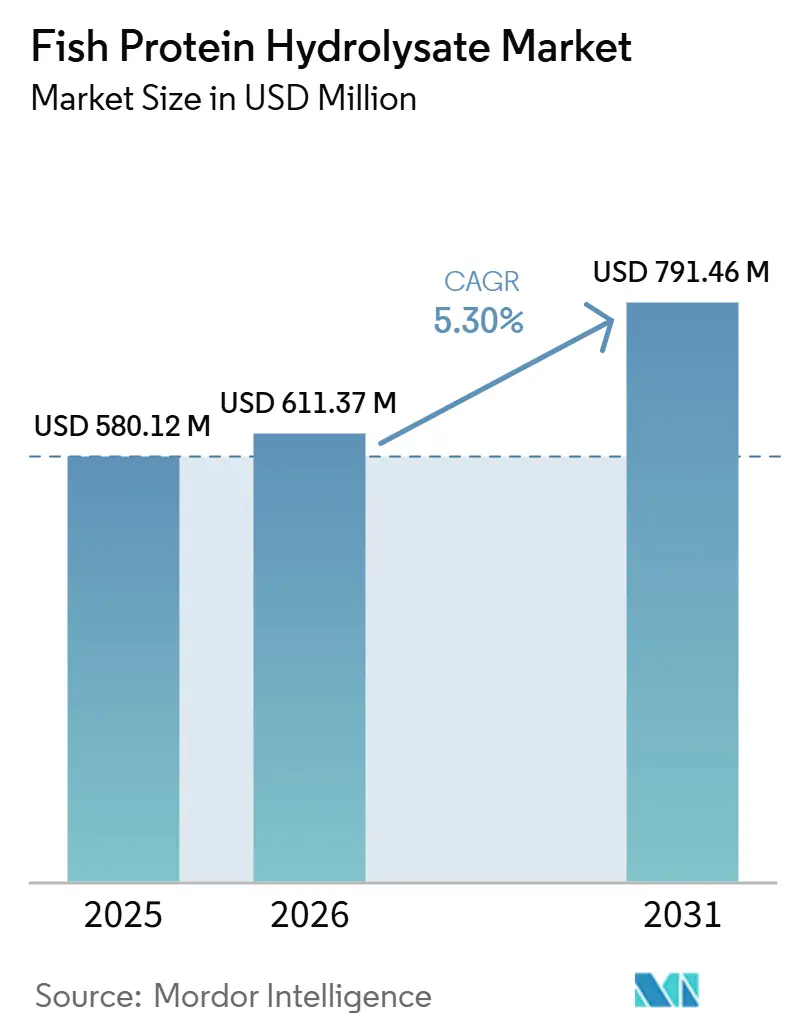

| Market Size (2026) | USD 611.37 Million |

| Market Size (2031) | USD 791.46 Million |

| Growth Rate (2026 - 2031) | 5.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

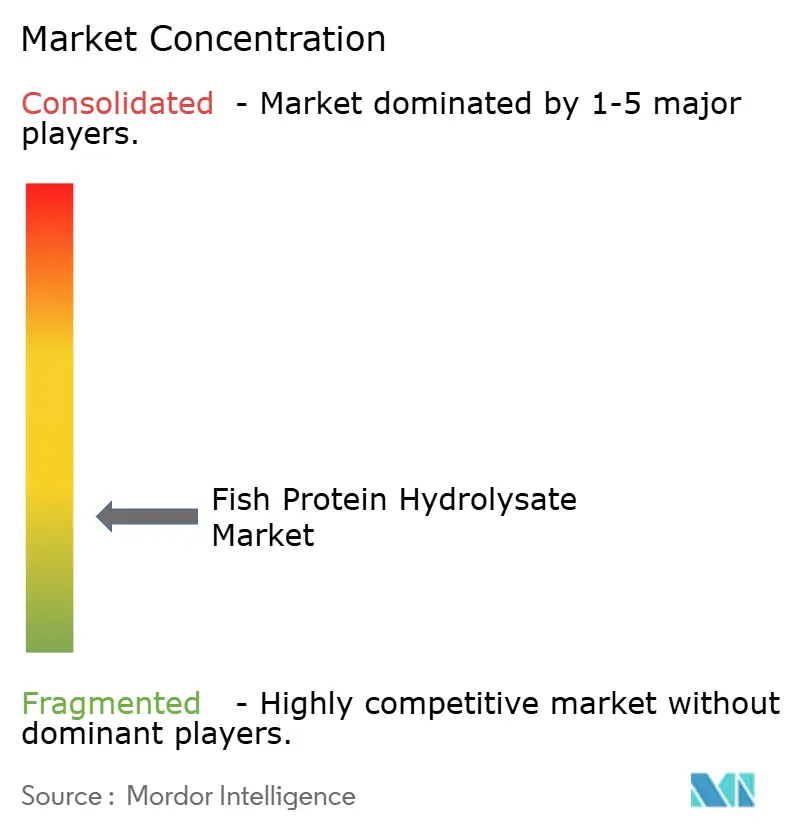

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fish Protein Hydrolysate Market Analysis by Mordor Intelligence

The global fish protein hydrolysate market size is expected to grow from USD 580.12 million in 2025 to USD 611.37 million in 2026 and is forecast to reach USD 791.46 million by 2031 at a 5.30% CAGR over 2026-2031. The global fish protein hydrolysate market is driven by the increasing demand for high-quality, easily digestible protein ingredients across applications such as animal feed, aquaculture, and nutraceuticals. Growing awareness of sustainable practices and waste-to-value initiatives is encouraging the use of fish processing by-products, aligning with circular economy goals in the seafood industry. In aquaculture, fish protein hydrolysates are gaining popularity due to their superior amino acid profile, which enhances feed efficiency, growth performance, and disease resistance in aquatic species. The expanding pet food industry is also boosting demand, as manufacturers incorporate hydrolyzed proteins to improve digestibility and reduce allergenicity. Furthermore, rising interest in functional foods and dietary supplements is driving the use of bioactive peptides from fish protein hydrolysates, valued for their potential health benefits, such as anti-inflammatory and immune-boosting properties. Advancements in enzymatic hydrolysis and processing technologies are improving product quality and scalability, facilitating broader adoption across various end-use industries.

Key Report Takeaways

- By source, salmon led with 33.23% of fish protein hydrolysate market share in 2025; crustacean is forecast to post the fastest 6.07% CAGR through 2031.

- By form, powder accounted for 47.87% of the fish protein hydrolysate market size in 2025, whereas liquid concentrates are projected to advance at a 6.16% CAGR between 2026-2031.

- By application, animal feed and aquaculture commanded 37.09% revenue in 2025, while dietary supplements are set to expand at a 5.96% CAGR to 2031.

- By geography, Europe held 34.89% share of the fish protein hydrolysate market in 2025, yet Asia-Pacific is anticipated to register a 6.23% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fish Protein Hydrolysate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of the aquaculture industry | +1.4% | Asia-Pacific core, spill-over to South America and Middle East | Medium term (2-4 years) |

| Increasing demand for sustainable and circular feed ingredients | +1.1% | Global, with early adoption in Europe and North America | Long term (≥ 4 years) |

| Growing adoption in premium pet food formulations | +0.9% | North America and Europe, emerging in Asia-Pacific urban centers | Short term (≤ 2 years) |

| Rising use in nutraceutical and functional food applications | +0.8% | Global, concentrated in North America, Europe, and Japan | Medium term (2-4 years) |

| Shift toward natural and clean-label ingredients | +0.6% | North America and European Union, regulatory influence spreading to Asia-Pacific | Medium term (2-4 years) |

| Technological advancements in enzymatic hydrolysis | +0.5% | Global, led by Norway, Iceland, and Japan research and development hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid expansion of the aquaculture industry

The global aquaculture industry's rapid growth is a significant factor driving the fish protein hydrolysate market, as producers prioritize nutritionally efficient and highly digestible feed ingredients to support intensive farming practices. Fish protein hydrolysates are valued for their superior amino acid profile, high bioavailability, and ability to improve feed intake, growth rates, and disease resistance in aquatic species, making them a key component in modern aquafeed formulations. This trend is particularly prominent in emerging aquaculture markets like India, where fish production increased from 95.79 lakh tonnes in FY 2013–14 to 197.75 lakh tonnes in FY 2024–25, representing a 106% growth. Additionally, farming efficiency has improved, with average aquaculture productivity reaching 4.77 tonnes per hectare, reflecting a shift toward more intensive and input-driven systems[1]Source: Ministry of Fisheries, Animal Husbandry & Dairying, “Fish production has increased to 197.75 lakh tonnes in FY 2024-25 from 95.79 lakh tonnes fish production in FY 2013-14 increasing a significant 106%,” pib.gov.in. These advancements are driving the demand for performance-enhancing feed ingredients such as fish protein hydrolysates, as farmers focus on optimizing yields, reducing mortality, and ensuring sustainability in high-density aquaculture operations.

Increasing demand for sustainable and circular feed ingredients

The rising demand for sustainable and circular feed ingredients is a significant driver of the global fish protein hydrolysate market, as industries aim to reduce waste and enhance resource efficiency within the seafood value chain. Fish protein hydrolysates are predominantly derived from fish processing by-products, including heads, frames, and viscera, converting materials traditionally regarded as waste into valuable nutritional inputs. This approach aligns with circular economy principles, emphasizing the optimal use of raw materials and minimizing environmental impact. Feed manufacturers and aquaculture producers are increasingly incorporating these ingredients to achieve sustainability objectives, decrease dependence on conventional fishmeal, and alleviate pressure on wild fish stocks. Furthermore, heightened regulatory and consumer focus on environmentally responsible sourcing is promoting the adoption of traceable, upcycled protein sources in aquafeed and pet food applications. Consequently, fish protein hydrolysates are emerging as an eco-friendly alternative that supports economic efficiency and long-term sustainability within the global feed industry.

Growing adoption in premium pet food formulations

The increasing use of fish protein hydrolysates in premium pet food formulations is a key factor driving market growth. Pet owners are placing greater emphasis on providing high-quality, functional, and easily digestible nutrition for their pets. Hydrolyzed fish proteins are particularly valued for their improved digestibility, low allergenicity, and high bioactive peptide content, making them suitable for specialized diets aimed at addressing sensitive digestion, skin health, and overall wellness. This trend toward premiumization is evident in ingredient usage patterns, with marine ingredients in United States dog and cat food experiencing a 95% increase in tonnage from 2020 to 2024, rising from 257,000 tonnes to 502,000 tonnes[2]Source: Institute for Feed Education & Research, “Pet Food Report,” ifeeder.org. This significant growth underscores the growing preference for marine-based, high-protein ingredients in pet nutrition. As pet humanization continues to shape consumer behavior, manufacturers are increasingly incorporating fish protein hydrolysates into premium and therapeutic pet food products, driving demand in both developed and emerging markets.

Rising use in dietary supplements and functional food applications

The increasing use of fish protein hydrolysates in dietary supplements and functional food applications is a significant driver of market growth, fueled by growing consumer emphasis on health, wellness, and preventive nutrition. These hydrolysates contain bioactive peptides that offer potential benefits such as enhanced muscle recovery, improved joint health, immune system support, and anti-inflammatory properties, making them valuable for nutraceutical formulations. Their high digestibility and rapid absorption further boost their suitability for sports nutrition and clinical nutrition products. Regulatory developments are also contributing to market growth. For instance, the United Kingdom Food Standards Agency approved the use of krill protein hydrolysate at levels of up to 25 grams per day in dietary supplements starting in 2025[3]Source: United Kingdom Food Standards Agency & Food Standards, "Safety Assessment on Krill Protein Hydrolysate Used as an Alternative Source of Protein in Food Supplements and Functional Protein Food and Drinks (RP1290)," science.food.gov.uk. This approval sets a key precedent for the broader acceptance of marine-derived hydrolysates in regulated markets. As demand for clean-label, protein-rich, and functional ingredients continues to grow, manufacturers are increasingly incorporating fish protein hydrolysates into various fortified foods and supplement products, driving sustained global demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong competition from alternative protein ingredients | -0.7% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Regulatory and safety compliance challenges | -0.4% | Asia-Pacific and South America, with European Union/United States setting precedent | Medium term (2-4 years) |

| Variability in raw material quality | -0.3% | Global, seasonal peaks in pelagic fisheries | Short term (≤ 2 years) |

| Challenges in standardization and product differentiation | -0.2% | Global, fragmented supply base | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong competition from alternative protein ingredients

Strong competition from alternative protein ingredients is a notable restraint on the growth of the global fish protein hydrolysate market. Feed and food manufacturers are increasingly diversifying their protein sources to manage cost, availability, and functionality. Plant-based proteins, such as soy, pea, and wheat gluten, along with other animal-derived inputs like poultry meal and insect protein, are gaining popularity due to their relatively lower price volatility and more stable supply chains. In aquafeed and pet food applications, these alternatives are improving in amino acid optimization and digestibility, reducing the performance gap with fish protein hydrolysates. Furthermore, sustainability concerns regarding marine resource utilization and fluctuating raw material availability are encouraging manufacturers to consider non-marine protein options. Consequently, the growing availability and technological advancements of substitute proteins are creating pricing pressures and limiting the adoption of fish protein hydrolysates, particularly in cost-sensitive markets.

Regulatory and safety compliance challenges

Regulatory and safety compliance challenges significantly restrain the global fish protein hydrolysate market, as manufacturers must address complex and fragmented approval processes across various regions and end-use applications. The production process, which utilizes animal-derived raw materials, is subject to stringent regulations concerning hygiene, traceability, contaminant limits, and labeling standards, particularly in regions with advanced food and feed safety systems. Differences in regulatory requirements across countries can lead to delays in product approvals, increasing both the cost and time required for market entry. Furthermore, issues such as heavy metals, microbial contamination, and allergenicity demand stringent quality control and testing protocols, adding to operational expenses. Adherence to evolving sustainability certifications and documentation requirements further complicates compliance efforts. These regulatory challenges can hinder production scalability and deter smaller players from entering the market, thereby limiting overall growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Salmon Leads, Crustacean Scales Fastest

Salmon-derived hydrolysates held a significant 33.23% market share in 2025. This growth is attributed to the ample availability of raw materials from the expanding global salmon processing industry, which produces substantial by-products such as heads, skin, and frames. These by-products are efficiently converted into high-value protein ingredients. Salmon-derived hydrolysates are highly regarded for their rich amino acid composition and bioactive peptides, making them suitable for applications in aquafeed, pet nutrition, and human health products. Their superior digestibility and palatability position them as ideal components for premium aquaculture and pet food formulations, where nutrient absorption and performance are critical. Furthermore, the increasing focus on sustainable production practices supports the utilization of salmon processing waste, aligning with circular economy principles and reducing environmental impact. Technological advancements in enzymatic hydrolysis are also improving product consistency and functional properties, facilitating broader adoption in nutraceutical and functional food sectors.

Crustacean-derived hydrolysates are experiencing notable growth, with a robust CAGR of 6.07% projected through 2031. These hydrolysates are gaining popularity due to their unique nutritional and functional properties, including high levels of essential amino acids, minerals, and bioactive compounds such as chitin derivatives and antioxidants. The global processing of shrimp, crab, and krill is generating significant shell and protein-rich waste, which is increasingly being converted into hydrolysates for applications in feed, agriculture, and nutraceuticals. In aquafeed, these hydrolysates serve as natural growth promoters and immunostimulants, enhancing disease resistance and survival rates in aquatic species. Additionally, their bioactive properties are driving interest in dietary supplements and functional foods targeting joint health, anti-inflammatory benefits, and overall wellness. Growing regulatory acceptance and advancements in extraction technologies are improving the commercial feasibility of crustacean hydrolysates. Sustainability considerations further support their adoption as an eco-friendly solution for converting seafood waste into valuable ingredients.

By Form: Liquid Concentrates Gain on Powder

The powder form segment dominated the market with a significant 47.87% share in 2025. The demand for powder-form fish protein hydrolysates is driven by their superior stability, extended shelf life, and ease of storage and transportation compared to liquid alternatives. These attributes make them highly suitable for global trade and large-scale industrial applications. Powdered hydrolysates provide better formulation flexibility, enabling precise dosing and seamless integration into dry pet food, aquafeed, dietary supplements, and functional food products. Their low moisture content minimizes the risk of microbial growth, ensuring product safety and consistency over prolonged periods. Additionally, advancements in drying technologies, such as spray drying, have enhanced solubility and preserved bioactive properties, improving their functional performance across various end-use industries. The increasing demand for convenient, shelf-stable, and high-protein ingredients in nutraceuticals and premium feed formulations further supports the widespread adoption of powdered fish protein hydrolysates.

The liquid hydrolysates segment is expected to grow at a robust 6.16% CAGR through 2031. Liquid fish protein hydrolysates are gaining popularity due to their high bioavailability, rapid absorption, and effectiveness in applications requiring immediate nutrient delivery, particularly in aquaculture and agriculture. Their liquid form facilitates easy mixing and uniform distribution in feed formulations, liquid fertilizers, and soil conditioners, making them ideal for enhancing nutrient uptake and growth performance. In aquafeed, liquid hydrolysates serve as natural feed attractants, improving palatability and feeding efficiency in fish and shrimp. Furthermore, the lower processing requirements compared to powdered forms can reduce production costs while retaining sensitive bioactive compounds. As demand increases for efficient, fast-acting nutritional solutions in both feed and agricultural sectors, liquid fish protein hydrolysates continue to experience growing adoption.

By Application: Dietary Supplements Outpace Feed

Animal feed and aquaculture applications held a significant 37.09% market share in 2025. The growth of fish protein hydrolysates in these applications is attributed to the increasing demand for high-performance, nutritionally efficient feed ingredients that promote faster growth, improved feed conversion ratios, and enhanced disease resistance. Fish protein hydrolysates offer a highly digestible source of peptides and free amino acids, making them particularly effective for early-stage feeding and species with sensitive digestive systems. In aquaculture, they function as natural feed stimulants, enhancing palatability and intake while boosting immunity and stress tolerance in fish and shrimp. The intensification of aquaculture practices, combined with the need to reduce dependence on conventional fishmeal, is further driving their adoption. Additionally, their contribution to improving survival rates and overall productivity aligns with the industry's focus on maximizing yield and operational efficiency, sustaining demand across global feed markets.

The dietary supplements segment is anticipated to grow at the highest rate, with a CAGR of 5.96% through 2031. The increasing use of fish protein hydrolysates in dietary supplements is driven by rising consumer awareness of preventive healthcare and the demand for bioactive, protein-rich ingredients with functional benefits. These hydrolysates contain peptides that support muscle recovery, joint health, skin health, and immune function, making them appealing for sports nutrition, aging populations, and wellness-focused consumers. Their rapid absorption and high bioavailability enhance their effectiveness compared to intact proteins, further increasing their attractiveness in nutraceutical formulations. Clean-label trends and a preference for marine-derived, natural ingredients are also encouraging manufacturers to incorporate fish protein hydrolysates into capsules, powders, and functional beverages. As the global supplement industry continues to grow, fueled by lifestyle changes and health-conscious consumption patterns, the demand for scientifically supported, multifunctional ingredients like fish protein hydrolysates is expected to rise steadily.

Geography Analysis

The European market maintained its leadership in fish by-product valorization, holding a significant 34.89% share in 2025. This dominance is attributed to robust regulatory support for sustainable resource utilization and a strong emphasis on circular economy practices, which promote the conversion of seafood processing by-products into value-added ingredients. The region’s advanced aquaculture industry, particularly in countries like Norway and Scotland, drives demand for high-quality, digestible feed inputs that enhance growth performance and fish health. Additionally, Europe’s mature pet food market is experiencing increased demand for premium and hypoallergenic formulations, where hydrolyzed proteins play a crucial role. The rising popularity of functional foods and nutraceuticals, supported by health-conscious consumers and stringent quality standards, further accelerates the adoption of bioactive marine-derived ingredients. This positions fish protein hydrolysates as a vital component in both feed and human nutrition sectors.

Asia-Pacific is emerging as the fastest-growing market for fish protein hydrolysates, with a notable CAGR of 6.23% projected through 2031. The region’s growth is primarily driven by the rapid expansion and intensification of aquaculture in countries such as China, India, Vietnam, and Indonesia. Increasing fish consumption and seafood production generate substantial volumes of processing by-products, creating opportunities for hydrolysate production. Efforts to improve aquaculture productivity and feed efficiency are boosting demand for high-performance protein ingredients that support faster growth and disease resistance. Furthermore, the expanding middle-class population and growing awareness of animal nutrition are driving the growth of premium pet food markets, further increasing demand. Simultaneously, rising interest in functional foods and traditional health supplements incorporating marine-derived ingredients supports the adoption of fish protein hydrolysates in human nutrition applications.

In North America, South America, and the Middle East & Africa, the fish protein hydrolysates market is driven by expanding aquaculture operations, growing pet food industries, and a focus on sustainable feed solutions. In North America, strong demand for premium pet nutrition and advanced feed formulations encourages the use of hydrolyzed proteins for their digestibility and functional benefits. South America, with its significant aquaculture and fisheries base, is utilizing fish processing waste to develop cost-effective protein ingredients, supporting both domestic consumption and exports. In the Middle East & Africa, rising investments in aquaculture and initiatives to enhance food security are creating demand for efficient and nutrient-rich feed inputs. Across these regions, efforts to reduce feed costs, improve animal performance, and adopt environmentally responsible practices collectively drive the adoption of fish protein hydrolysates.

Competitive Landscape

The fish protein hydrolysates market is marked by a highly fragmented competitive landscape, with numerous regional and specialized processors operating without a dominant player exerting significant control. Competition primarily revolves around access to consistent raw material supplies, proprietary enzymatic hydrolysis technologies, and the ability to develop customized formulations for specific end-use applications, including aquafeed, pet nutrition, and nutraceuticals. This fragmentation has created opportunities for consolidation, as companies increasingly pursue strategic acquisitions and partnerships to secure supply chains, enhance production capabilities, and strengthen their market presence. Companies that can ensure reliable, year-round sourcing of fish by-products while maintaining processing efficiency are better positioned to gain a competitive edge in this evolving market.

Operational control over feedstock collection and processing logistics has become a critical differentiator among market participants. Companies investing in integrated supply chain infrastructure, such as dedicated collection systems and rapid processing technologies, can minimize raw material degradation and preserve protein quality. Additionally, technological advancements in hydrolysis techniques are shaping competition by enabling improved functional properties, including enhanced bioactivity, reduced allergenicity, and higher nutritional value. These innovations allow manufacturers to move beyond commodity-grade products and develop specialized, high-performance ingredients for premium applications across feed, food, and health-related sectors.

The market is also experiencing growth in high-value segments such as medical nutrition and cosmeceuticals, where demand for clinically validated bioactive peptides is rising. Companies investing in scientific research and clinical validation can command premium pricing and differentiate their products in a competitive market. However, competition from alternative marine-derived ingredients offering distinct functional benefits is intensifying. This has prompted hydrolysate producers to focus on digestibility, peptide functionality, and application-specific performance. Consequently, the competitive environment is gradually shifting from volume-driven strategies to innovation, quality differentiation, and targeted expansion into specialized, high-margin applications.

Fish Protein Hydrolysate Industry Leaders

-

Bio-marine Ingredients Ireland

-

Copalis Sea Solutions

-

Biomega Group

-

Scanbio Marine Group

-

Hofseth BioCare ASA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: GC Rieber acquired Biomega Group, consolidating control over salmon and trout residual processing across Norway and Denmark.

- August 2025: Biomega Group announced strategic initiatives to support its global expansion in sustainable salmon peptides, proteins, and oils production. This effort strengthens Biomega’s position in the fish protein hydrolysate market by advancing environmentally responsible ingredient production and expanding presence in key markets such as China and the US.

- July 2024: NovoNutrients raised $18 million to scale its technology converting CO₂ emissions into high-protein ingredients for aquaculture, pet food, and plant-based alternatives, advancing sustainable protein production. This innovation supports the growing global demand in the fish protein hydrolysate market for eco-friendly, nutritious protein sources.

- April 2024: Hofseth BioCare ASA reported a 31% year-over-year increase in fish protein hydrolysate production, driven by expanded capacity and rising demand in pet health and nutraceuticals. The company advanced clinical research on bioactive peptides, supporting its leadership in sustainable marine protein solutions for global markets.

Global Fish Protein Hydrolysate Market Report Scope

| Molluscs |

| Anchovy |

| Crustacean |

| Salmon |

| Codfish |

| Tilapia |

| Others |

| Powder |

| Liquid |

| Paste |

| Animal Feed and Aquaculture |

| Pet Food |

| Food and Beverage |

| Dietary Supplements |

| Cosmetics and Personal Care |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Source | Molluscs | |

| Anchovy | ||

| Crustacean | ||

| Salmon | ||

| Codfish | ||

| Tilapia | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| Paste | ||

| By Application | Animal Feed and Aquaculture | |

| Pet Food | ||

| Food and Beverage | ||

| Dietary Supplements | ||

| Cosmetics and Personal Care | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global demand for fish-derived hydrolysates be by 2031?

The fish protein hydrolysate market size is projected to reach USD 791.46 million by 2031 at a 5.3% CAGR.

Which source currently dominates production volumes?

Salmon processing by-products account for 33.23% of global output, reflecting Nordic aquaculture scale.

What is the fastest-growing application segment?

Dietary supplements are expanding at a 5.96% CAGR on clinically backed health claims.

Which region offers the highest growth outlook?

Asia-Pacific leads with a 6.23% CAGR through 2031, driven by expanding aquaculture and rising protein demand.

Page last updated on: