Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

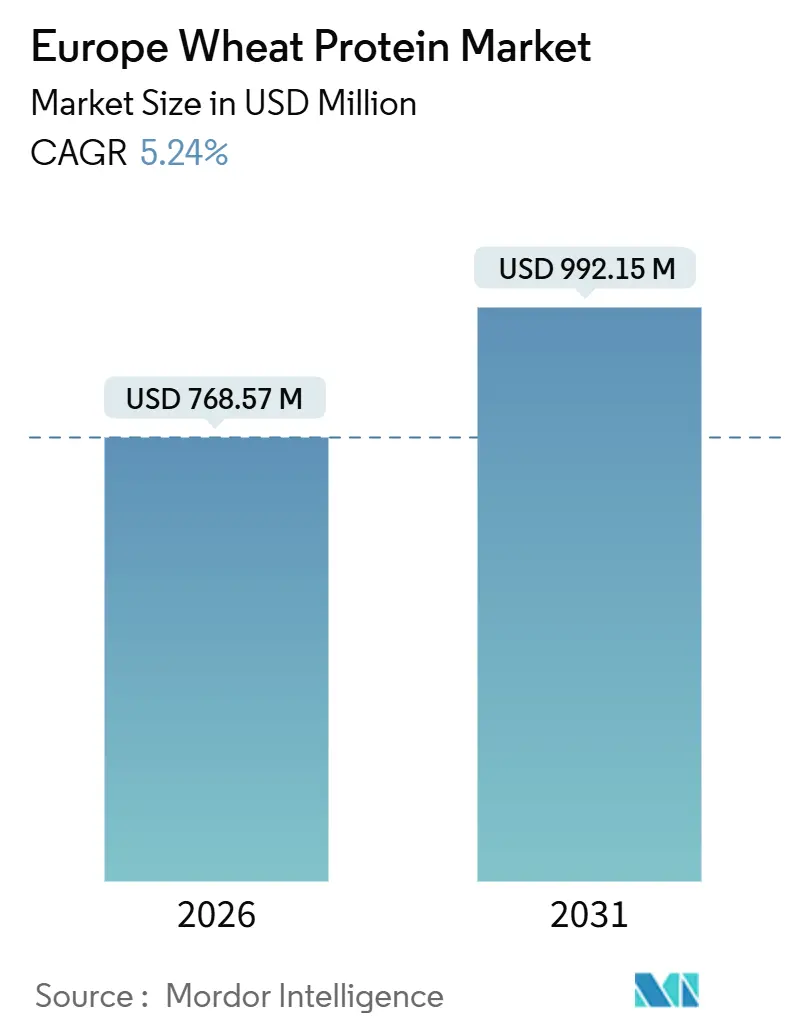

| Market Size (2026) | USD 768.57 Million |

| Market Size (2031) | USD 992.15 Million |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Wheat Protein Market Analysis by Mordor Intelligence

The European wheat protein market size is projected to grow substantially, increasing from USD 768.57 million in 2026 to USD 992.15 million by 2031, at a CAGR of 5.24%. In terms of market volume, the market is expected to grow from 192.04 thousand metric tons in 2026 to 243.35 thousand metric tons by 2031, at a CAGR of 4.85% during the forecast period (2026-2031). This growth is driven by the rising popularity of plant-based diets, a growing preference for clean-label, sustainable food options, and supportive government policies that foster sustainable food systems. Germany, France, and the United Kingdom dominate the market due to their advanced food-processing capabilities and strong retail distribution networks. To meet the evolving consumer demand, manufacturers are enhancing their production processes by adopting advanced extraction and fractionation technologies. These innovations are expanding the use of wheat protein across various applications, including bakery products, meat substitutes, sports nutrition, and personal care items. Such developments are enabling manufacturers to align with consumer preferences while contributing to the region's sustainability objectives.

Key Report Takeaways

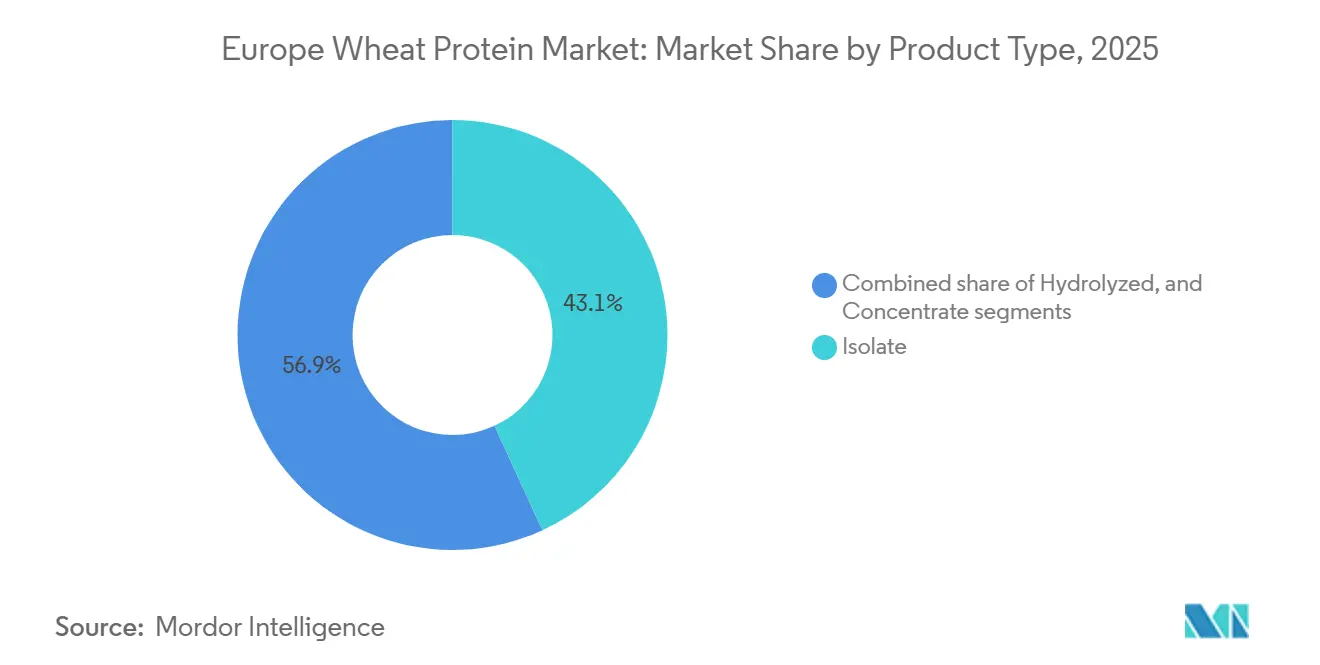

- By product type, isolates led with 43.12% of Europe wheat protein market share in 2025, while hydrolyzed wheat protein is forecast to expand at a 7.36% CAGR through 2031.

- By form, the dry format held 82.74% share in 2025; the liquid format is projected to grow at a 5.9% CAGR through 2031.

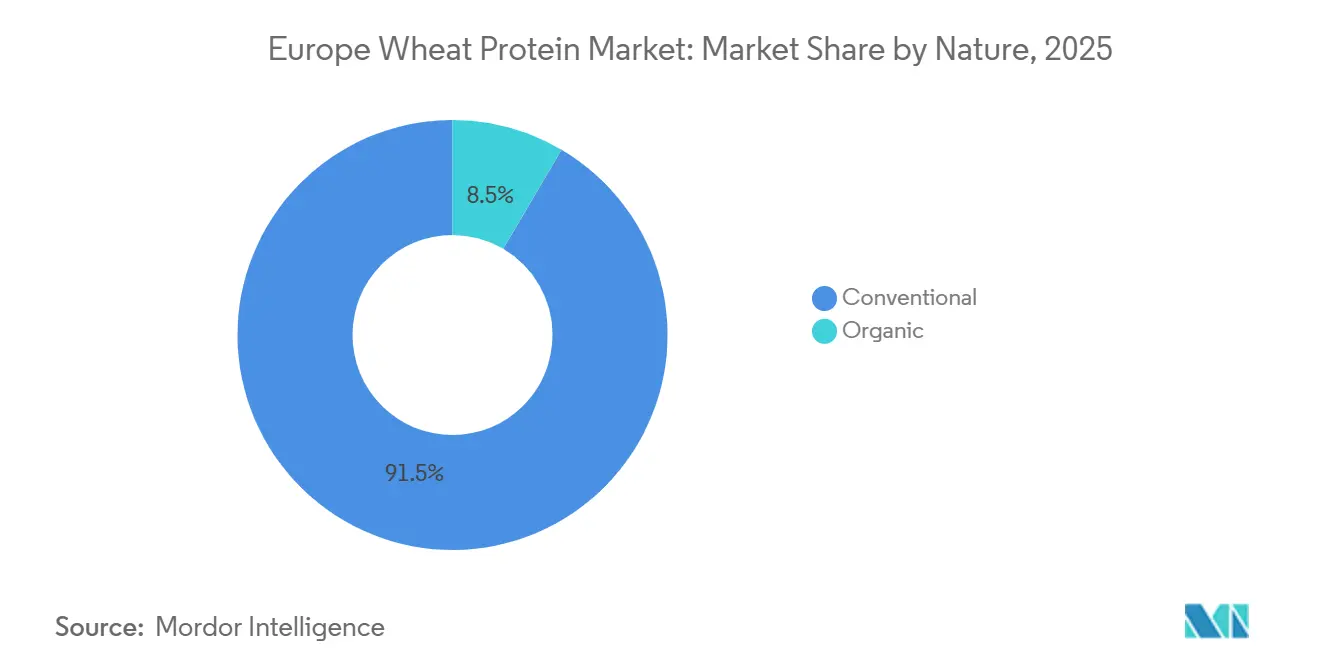

- By nature, the conventional segment accounted for 91.54% of the Europe wheat protein market size in 2025, whereas the organic segment is advancing at an 8.85% CAGR during 2026-2031.

- By application, food and beverage captured 80.42% share of the Europe wheat protein market size in 2025, while cosmetics and personal care are poised to grow at an 8.73% CAGR through 2031.

- By geography, Germany held 27.31% share in 2025; the Netherlands is projected to grow at a 8.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Wheat Protein Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing usage of wheat protein in vegan and plant-based products | +2.2% | Germany, United Kingdom, France, Netherlands | Medium term (2-4 years) |

| Rising demand for clean-label ingredients | +1.5% | Germany, France, United Kingdom, Nordics | Long term (≥4 years) |

| Increasing use in bakery and confectionery application | +1.3% | Germany, United Kingdom, France, Italy | Short term (≤2 years) |

| Fitness trends increase demand for wheat protein in supplements | +1.1% | Germany, United Kingdom, Netherlands, Nordics | Medium term (2-4 years) |

| Disruptions in animal protein supply boost wheat protein demand. | +0.8% | Global, with emphasis on Germany, France | Short term (≤2 years) |

| Research enhances wheat protein extraction and functionality | +0.7% | Germany, Netherlands, France | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing usage of wheat protein in vegan and plant-based products

In Europe, manufacturers are increasingly adopting wheat protein for vegan and plant-based products, driving market growth. Leveraging wheat's versatility, they are creating meat substitutes that appeal to both vegans and flexitarians, with innovations like PLNT's wheat protein-based lamb strips and chicken-style sausages. Germany is supporting this transition through initiatives such as allocating EUR 38 million in its 2024 budget to promote plant-based, cell-cultivated, and precision-fermented proteins. Technological advancements by companies like Bühler and Andritz are scaling wheat protein production through methods like extrusion and fermentation, reducing costs and improving accessibility across food segments such as ready-to-eat meals, snacks, and bakery products. Rising consumer demand for sustainable, health-conscious options and Germany's focus on reducing greenhouse gas emissions further bolster the adoption of wheat protein, which offers nutritional and functional benefits with a lower environmental footprint compared to animal-based proteins.

Rising demand for clean-label ingredients

The clean label movement in Europe is transforming wheat protein formulations as consumers demand minimally processed and transparently sourced ingredients. Technological advancements, such as enzymatic hydrolysis, are enhancing the solubility and functionality of plant proteins like wheat protein without chemical additives, making them suitable for a wider range of food applications. Research published in the Proceedings of the National Academy of Sciences highlights the effectiveness of enzymatic hydrolysis in addressing the low solubility of certain plant proteins. Initiatives by Wageningen University and Research further support clean label solutions by promoting simplified ingredient lists and familiar components to boost consumer acceptance and trust. Additionally, EIT Food and Foundation Earth introduced environmental food scoring standards in August 2024, aiming to educate consumers about the ecological impact of their food choices while reinforcing sustainability and ethical sourcing practices in the food industry.

Increasing use in bakery and confectionery application

In Europe, the bakery and confectionery sectors are increasingly adopting wheat protein due to evolving consumer preferences and industry innovations. Wheat protein enhances the texture, moisture retention, and nutritional profile of baked goods, making it a key ingredient in products like bread, pastries, cakes, and rolls. The rising demand for healthier eating, plant-based diets, and high-protein, low-carb bakery items has driven its adoption, with its role as a substitute for dairy and egg proteins appealing to the growing vegan demographic. France and Germany, as leading wheat producers, are utilizing advanced agricultural practices and strong research and development capabilities to produce premium wheat protein, catering to both traditional and gluten-free product demands. This shift addresses the needs of consumers with celiac disease or gluten sensitivities while reinforcing wheat protein's role in Europe’s culinary heritage. Additionally, increasing health consciousness, European Union sustainability initiatives, and advancements in protein extraction technologies are positioning wheat protein as a greener alternative to animal-based proteins with a smaller carbon footprint. As a result, the bakery and confectionery sectors are driving significant growth in the wheat protein market, which is poised for further expansion in the coming years.

Fitness trends increase demand for wheat protein in supplements

Rising fitness consciousness and active lifestyles are driving strong demand for wheat protein as a key ingredient in sports nutrition and dietary supplements. As consumers seek plant-based, allergen-friendly protein sources, wheat protein appeals to athletes and gym-goers looking for muscle recovery and performance-enhancing options beyond traditional whey. The growing popularity of vegan and flexitarian diets further amplifies interest in wheat protein supplements, as it offers a high-glutamine content beneficial for muscle repair. Brands are capitalizing on this trend by launching protein powders, bars, and ready-to-drink beverages featuring wheat protein isolates. Social media fitness influencers and personalized nutrition apps are also raising awareness of wheat protein’s benefits, accelerating adoption. Collectively, these dynamics are positioning wheat protein as a go-to solution in the booming global fitness and sports supplement markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in gluten intolerance and celiac disease cases | -1.8% | United Kingdom, Germany, Italy, Nordics | Long term (≥4 years) |

| Rising use of substitute protein sources | -1.2% | Germany, France, Netherlands, United Kingdom | Medium term (2-4 years) |

| Fluctuation in raw material prices | -0.9% | All European regions | Short term (≤2 years) |

| Trade tariffs affecting wheat imports and exports | -0.6% | United Kingdom, Russia, Rest of Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in gluten intolerance and celiac disease cases

As celiac disease increasingly impacts Europe's populace, traditional wheat protein products grapple with challenges. Data published by the European Food Safety Authority in May 2024 indicates that over 5 million people in the EU are living with celiac disease [1]Source: European Food Safety Authority, "Episode 18 - Celiac disease: living without gluten", efsa.europa.eu. However, this rising health concern simultaneously carves out niche opportunities for specialized wheat protein variants. Responding to these health issues, the EU has rolled out stringent gluten labeling regulations. In contrast to the US's more lenient and often voluntary standards, the EU enforces strict compliance. Underlining this commitment, the European Commission's Regulation (EU) No 828/2014 mandates that products labeled "gluten-free" must not exceed 20 parts per million (ppm) of gluten. This regulation seeks to bolster clarity and safety for gluten-sensitive consumers. Reflecting these shifts, the market is seeing innovations such as gluten-free wheat flours that mimic traditional wheat products. These advancements not only tackle concerns about taste and nutrition but also specifically target those with gluten sensitivities. Consequently, while conventional wheat protein remains a staple for the mainstream, the market is evolving: specialized and modified wheat proteins are emerging to cater to consumers with dietary restrictions.

Rising use of substitute protein sources

Europe's evolving protein landscape is putting increased pressure on wheat protein, as alternative sources, lauded for their distinct nutritional benefits and sustainability, gain popularity. Roquette's launch of NUTRALYS® Fava S900M, a fava bean protein isolate containing 90% protein, in Europe and North America on May 28, 2024, exemplifies this trend. Backed by a EUR 17 million grant from the EU's Horizon 2020 program, the PLENITUDE project is set to establish a biorefinery, targeting an annual protein production of 16,000 tonnes from sustainable feedstocks. This initiative aligns with the growing demand for plant-based and environmentally friendly protein sources, driven by consumer preferences and regulatory support for sustainable practices. In light of these shifts, wheat protein producers are being pushed to set their products apart, focusing on improved functionality, sustainability, and tailored formulations for specific applications. Additionally, manufacturers are exploring innovations in processing technologies and partnerships to enhance their competitive edge in a rapidly diversifying market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Isolates Lead, Hydrolyzed Accelerates

In 2025, wheat protein isolates command a dominant 43.12% share of the European market, owing to their high protein content and functional advantages in premium applications. According to the American Society of Baking, wheat protein isolate (WPI), boasting a minimum of 90% protein content, undergoes a wet-processing method. This process separates starch from wheat flour while retaining the desired protein properties. As a result, this high-protein ingredient finds its way into a myriad of products, from keto and low-calorie baked goods to baby food. Its ability to bolster dough strength and elasticity proves vital for high-speed baking. While the EU has yet to establish specific regulations for WPI composition, barring baby foods, this ambiguity fosters an innovative landscape, albeit with fundamental safety standards in place.

Hydrolyzed wheat protein is on the rise, projected to grow at a CAGR of 7.36% from 2026 to 2031. Its appeal lies in its superior digestibility and bioavailability, making it a sought-after ingredient in specialized nutrition and cosmetics. The European Food Safety Authority (EFSA) is on the front lines, scrutinizing novel foods and ingredients, including protein hydrolysates, to ensure they meet safety standards before they hit the market, as of July 2025[2]Source: European Food Safety Authority, "What are Novel Foods And Are they Safe for Me To Eat?", efsa.europa.eu. This segment's growth is bolstered by cutting-edge research in protein extraction and modification, amplifying the functional attributes and application scope of hydrolyzed wheat proteins in food, cosmetics, and pharmaceuticals.

By Form: Dry Dominates, Liquid Gains Momentum

In 2025, dry wheat protein dominates the market with an 82.74% share, due to its longer shelf life and logistical benefits in Europe's varied food manufacturing scene. For the 2024/2025 marketing year, the European Union's cereals market, a key supplier for wheat protein production, reported a soft wheat output of 111.0 million tonnes, as noted by the European Commission . This steady supply chain bolsters the leading position of dry wheat protein. Its handling and storage are less specialized than its liquid counterpart, making it the go-to choice for manufacturers across diverse application segments.

Liquid wheat protein is on a growth trajectory, boasting a CAGR of 5.9% from 2026 to 2031. Food and beverage manufacturers are gravitating towards these solutions, aiming to streamline production and ensure product consistency. The European Parliamentary Research Service underscores the role of alternative protein sources, including plant proteins, in bolstering food security and mitigating environmental impacts within the EU. This emphasis on sustainable protein is fueling innovations in liquid wheat protein formulations, especially in applications where swift incorporation and even distribution are paramount for quality and efficiency.

By Nature: Conventional Base, Organic Growth

In 2025, conventional wheat protein commands a dominant 91.54% share of the European market, underscoring its entrenched supply chains and cost benefits in mainstream food applications. Backing this dominance, the European Union's agricultural policy remains steadfast in its support for conventional wheat production. According to the European Commission, total cereal production is projected at 287.2 million tonnes for the 2025/2026 marketing year, marking a 13.1% uptick from the prior year. This robust output guarantees a consistent flow of raw materials for extracting conventional wheat protein, bolstering its leading market stance across diverse food and industrial sectors.

Meanwhile, organic wheat protein is on the rise, with a notable 8.85% CAGR forecasted for 2026-2031. This surge is fueled by a growing consumer inclination towards sustainably sourced, chemical-free ingredients. A detailed review in the journal Resources sheds light on the environmental ramifications of wheat production across different agrotechnical systems. It underscored the advantages of sustainable methods, particularly organic farming, in curbing ecological footprints. The research spotlighted the significance of organic fertilizers and conservation tillage in promoting sustainability, resonating with the heightened demand for organically certified wheat protein. Further bolstering this momentum, the European Parliament has rolled out a Protein Strategy, underscoring the pivotal role of sustainable plant-based proteins in modern food systems.

By Application: Food and Beverage Dominates, Cosmetics Accelerates

In 2025, the European wheat protein market sees the food and beverage sector leading with an 80.42% share. This dominance is attributed to wheat protein's versatile functional properties, which are leveraged across a range of products, from bakery goods and meat alternatives to snacks and ready-to-eat items. The food and beverage segment capitalizes on wheat protein's unique attributes: enhancing texture, providing structure, and boosting nutritional profiles, all while remaining cost-effective compared to other protein sources. The Agriculture and Horticulture Development Board (AHDB) plays a pivotal role, offering essential market data and analysis for the cereals and oilseeds sector, including wheat, thereby supporting the growth of food applications. The European Union, emphasizing the importance of a domestic plant-based protein supply for food security, sees Germany leading the charge with a Euro 38 million allocation for sustainable protein initiatives in 2024.

On another front, the meat alternatives segment is poised for significant growth, targeting an 8.62% CAGR from 2026 to 2031. Meanwhile, the Cosmetics and Personal Care sector emerges as the fastest-growing segment for wheat protein in Europe. This surge is fueled by a rising consumer preference for natural and sustainable beauty ingredients. Ongoing research into protein extraction and modification techniques is bolstering wheat protein's functional properties in cosmetics, especially hydrolyzed variants known for their skin conditioning and hair strengthening benefits. Animal Feed applications are also witnessing steady growth, thanks to wheat protein's nutritional value and cost-effectiveness for livestock and aquaculture. Furthermore, the European Parliamentary Research Service underscores the potential of alternative protein sources, like wheat, in bolstering food security and mitigating environmental impacts, thereby supporting growth across all application segments.

Geography Analysis

In 2025, Germany commands a dominant 27.31% share of the European wheat protein market, buoyed by a robust and consistently growing food processing industry. With a wheat production tally hitting 18.53 million metric tons in 2024, Germany stands out as a leading wheat producer, as reported by the Federal Statistical Office[3]Source: European Commission, "Cereals market situation", circabc.europa.eu. Pioneering advancements in wheat protein, especially for meat alternatives and bakery items, are being spearheaded by German manufacturers. A case in point is Crespel & Deiters Group's Loryma brand, which emphasizes wheat-based food ingredients, spanning wheat proteins, modified wheat starches, and functional blends. Driven by a commitment to sustainability and a penchant for premium ingredients, Germany's surging demand for wheat protein products is further amplified by a growing interest in organic and clean-label offerings.

The Netherlands is set to achieve the highest CAGR of 8.76%, making a pronounced shift towards plant-based proteins. Dutch producers of meat analogues are rapidly expanding, driven by increasing consumer demand for sustainable and plant-based food options. These manufacturers heavily depend on textured and vital wheat protein to meet the growing need for innovative meat substitutes. The Green Protein Alliance highlights a strong national focus on increasing plant-protein consumption, with supermarkets and food producers aligning their strategies to cater to this trend. This shift underscores the Netherlands' commitment to fostering a sustainable food ecosystem, positioning wheat protein as a critical ingredient in the plant-based protein market.

Wheat protein markets in the UK and France are evolving rapidly, driven by consumer preferences for health-focused and sustainable food options. In the UK, the food processing industry is adapting to challenges like rising ingredient costs and inflation by focusing on smaller packaging sizes and sourcing affordable ingredients. Despite these hurdles, the market is shifting towards clean-label and plant-based ingredients, creating opportunities for wheat protein. Meanwhile, France leverages its strong agricultural base and advanced food manufacturing sector to focus on bakery and premium food applications. With a rich culinary tradition, France values wheat protein for its ability to enhance the taste and texture of traditional products, further strengthening its position in the European wheat protein market.

Regulatory Landscape

Wheat protein ingredients sold into food and beverage applications in Europe operate under EU-wide food information and allergen rules, with wheat classified as a cereal containing gluten under Annex II of Regulation (EU) No 1169/2011, requiring clear allergen declaration and emphasis on labels. For gluten-related claims, the region enforces a harmonized threshold under Commission Regulation (EU) No 828/2014, where foods labeled "gluten-free" must not exceed 20 mg/kg, shaping QA testing, identity preservation, and risk management for wheat protein isolates, concentrates, and hydrolysates used in compound foods.

Formulation and processing choices also sit within EU safety frameworks for additives and processing aids. Regulation (EC) No 1333/2008 governs the use and safety of food additives via Union lists, and EFSA safety evaluations for wheat-derived food enzymes and ingredients place particular focus on downstream purification and residual protein or gluten content, influencing documentation and validation for refined or enzymatically modified wheat protein solutions.

Value Chain Analysis

The European wheat protein value chain is closely tied to the region's wheat milling and starch processing base. It typically starts with wheat cultivation and procurement (notably from major producing countries such as France and Germany), followed by milling and wet fractionation (hydromechanical separation) to split starch and gluten/protein streams. Downstream stages include concentration and drying for vital wheat gluten and isolates, and further refinement such as enzymatic hydrolysis to produce hydrolyzed wheat proteins for specialized food, sports nutrition, and cosmetics and personal care uses.

Midstream manufacturing is anchored by ingredient processors and integrated agrifood companies supplying standardized proteins and application-ready systems to food and beverage manufacturers (bakery, snacks, meat alternatives, and RTE/RTC), as well as to animal feed and personal care formulators. Compliance and QA checkpoints are embedded throughout distribution due to mandatory allergen labeling under Regulation (EU) No 1169/2011 and claim substantiation for "gluten-free" foods at 20 mg/kg, increasing the importance of traceability, segregation, and analytical testing across storage, blending, and finished-goods packaging before products move through distributors, private label channels, and industrial direct supply agreements.

Competitive Landscape

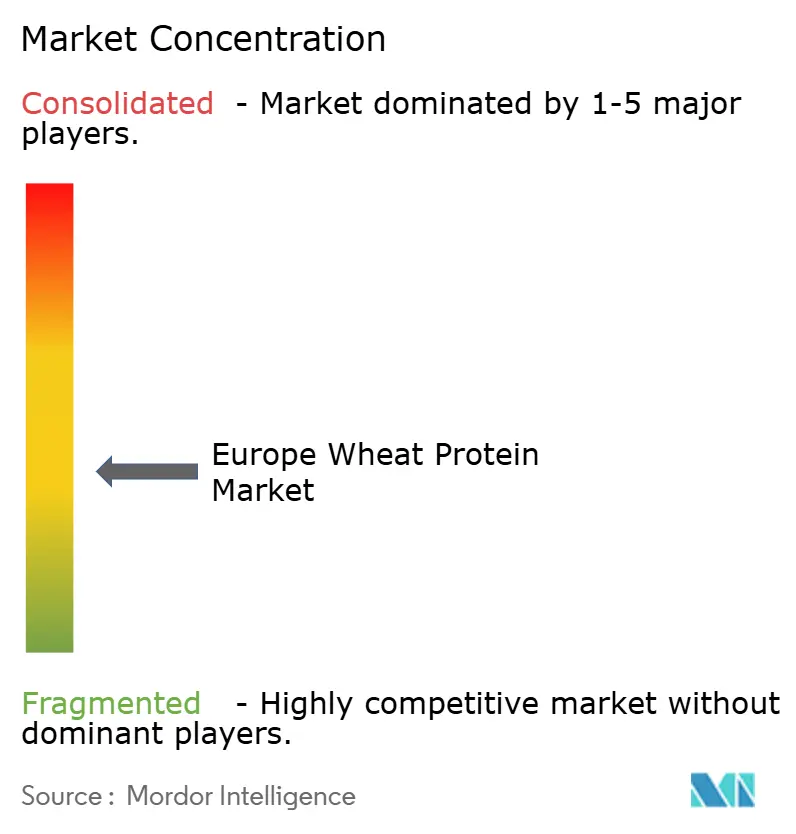

Europe wheat protein market exhibits moderate fragmentation. In the European wheat protein market, a blend of established giants and emerging players vie for dominance across isolates, concentrates, and hydrolyzed segments. Key players like the Archer-Daniels-Midland Company, Cargill, Incorporated, and Roquette Frères leverage integrated supply chains and diverse product portfolios. Meanwhile, niche firms are making strides through innovation and tailored formulations. Regional processors and private label manufacturers, attuned to local demands, further shape the market's competitive landscape. Additionally, strategic collaborations and capacity expansions are pivotal in defining these dynamics.

In a bid to enhance their technological capabilities and secure essential raw materials, companies are increasingly turning to strategic partnerships and vertical integration. Archer-Daniels-Midland Company (ADM) is making significant strides in sustainability, targeting regenerative agriculture practices on a global scale, covering four million acres by 2025. This initiative not only aims to strengthen its market position but also aligns with the growing demand for environmentally responsible practices in the industry.

New entrants are not merely joining the fray; they're establishing footholds in niche segments, such as organic wheat protein and hydrolyzed variants designed for cosmetics. These specialized offerings cater to evolving consumer preferences for natural and functional ingredients. This shift is nudging established players to expand their innovation pursuits to remain competitive.

Europe Wheat Protein Industry Leaders

-

The Archer-Daniels-Midland Company

-

Cargill, Incorporated

-

Roquette Freres

-

Tereos SCA

-

MGP Ingredients, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Product and application whitespace is expanding around higher-functionality formats that simplify plant-based formulation, especially textured wheat proteins and hydrolyzed variants that address texture, binding, and solubility requirements. A concrete signal of this direction is Roquette's June 2025 launch of NUTRALYS T WHEAT 600L, positioned for fibrous texture in meat alternatives and produced from European-sourced wheat, reinforcing the shift from commodity gluten toward application-specific, processing-compatible wheat protein solutions across Europe.

Policy momentum also supports investment and partnership activity across the wheat protein ecosystem by prioritizing stronger local protein value chains and processing capabilities. In July 2026, the European Commission published COM(2026) 355 final outlining actions toward a more autonomous EU protein system, emphasizing R&I for plant-based proteins and development of processing infrastructures. This backdrop underlines ongoing emphasis on traceability, sustainability, and collaborative initiatives among growers, processors, and manufacturers within the wheat protein space, while differentiating within a plant-protein landscape that includes rising competition from other protein sources.

Recent Industry Developments

- July 2026: The European Commission published COM(2026) 355 final outlining actions to build a more autonomous EU protein system, including emphasis on R&I for plant-based proteins and the development of processing infrastructures. The policy direction strengthens the case for localized sourcing, processing capacity, and collaborative projects that improve functionality and scalability of plant proteins used in food and beverage formulations, including wheat protein ingredients.

- June 2025: Roquette announced a major capacity expansion for NUTRALYS wheat protein production in Europe, signaling scale-up to meet growing demand for textured wheat proteins in meat alternatives.

- May 2024: The European Food Safety Authority highlighted the scale of celiac disease in the EU, with more than 5 million people living with the condition, reinforcing the importance of rigorous allergen and gluten-related compliance for wheat-based ingredients. This backdrop increases the operational priority of validated labeling, segregation, and testing across wheat protein supply chains, while also encouraging innovation in formulations and applications where gluten management is critical.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers wheat-derived proteins sold as ingredients in Europe, where demand is tracked across food, feed, and personal care uses, and values are measured in USD at the point of sale from ingredient suppliers.

Scope exclusions: We exclude finished packaged foods and supplements, and we also exclude non-wheat proteins such as pea, soy, dairy, and other cereals.

Segmentation Overview

-

By Product Type

- Isolate

- Concentrate

- Hydrolyzed

-

By Form

- Dry

- Liquid

-

By Nature

- Organic

- Conventional

-

By Application

-

Food and Beverage

- Bakery and Confectionery

- Snacks and Cereals

- Meat/Poultry/Seafood and Meat Alternatives

- RTE/RTC Food Products

- Other Application

- Animal Feed

- Cosmetics and Personal Care

-

Food and Beverage

-

By Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Poland

- Nordics (Sweden, Denmark, Finland, Norway)

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base for the model and to keep assumptions tied to Europe-specific production, trade, and use patterns for wheat-based ingredients. We typically start by mapping how wheat proteins move from milling and starch processing into ingredient channels, and then we align that flow with demand signals from key end uses.

Public sources such as Eurostat, FAOSTAT, UN Comtrade, the European Commission agriculture and trade releases, and scientific publications indexed in open literature were used to understand wheat availability, trade flows, and application trends. Alongside these, we reviewed company annual reports, investor presentations, association pages, and reputable press to cross-check capacity mentions, product mix shifts, and pricing commentary. A paid subscription for company financials and intelligence and a separate paid patent database were used selectively to validate ownership structures and to sanity-check innovation intensity. The list of desk research sources above is illustrative, and other sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating how demand is splitting between isolate, concentrate, and hydrolyzed formats, and how pricing is moving by form (dry versus liquid) in different buyer groups. We also spoke with a mix of ingredient sellers, distributors, and downstream users across major European markets, so the model could be corrected where secondary signals were either missing or too broad.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | |

| Mid tier: 49% | Functional/Unit leaders: 27% | |

| Smaller Players: 14% | Managers: 59% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where Europe demand is reconstructed from ingredient consumption pools and trade adjusted availability, and then translated into value using category-level pricing. Once the first total was formed, it was corroborated with selective bottom-up checks, such as sampled supplier revenue splits, distributor channel feedback, and volume-by-application spot checks, which are then used to adjust any clear overstatements.

A few practical inputs drove the model, including wheat processing output and import-export movements, the mix shift between isolates, concentrates, and hydrolyzed products, the share of dry versus liquid formats used by buyers, and typical application pull from food and beverage, animal feed, and cosmetics. Pricing was treated carefully because it can move with wheat and energy costs. We used a staged ASP progression by format and by end-use intensity rather than a single flat price for the whole market. When a specific country or application data point was missing, proxy ratios were applied from similar markets and then confirmed through expert feedback.

For forecasting, we relied on scenario analysis anchored to a short set of drivers that interviewees consistently pointed to, such as plant-based formulation activity, clean-label reformulation, and relative price competitiveness versus other plant proteins. Each scenario was then converted into annual growth rates by application, and the final forecast was blended toward the most likely case after review of recent trade and pricing direction.

Data Validation & Update Cycle

Validation was done through repeated cross-checks so the final numbers stay aligned with real-world signals, not just one spreadsheet output. We compared totals against independent indicators like trade balances, wheat-processing trends, and observed pricing bands, and then investigated any large jumps that could not be explained by a known driver.

Before sign-off, the model is reviewed in steps, first at the input level, then at the country and application roll-up level, followed by a final sense-check on growth logic. If major mismatches appear, experts are re-contacted to confirm whether the issue is scope, timing, or a one-off event. Reports are refreshed annually, with interim updates when material events occur, and a fresh pre-delivery pass is completed so the view reflects the latest available information.

Mordor Intelligence's Europe Wheat Protein Market Size Compared Against Other Published Estimates

It is normal to see different published market sizes for Europe wheat protein, even when sources appear to discuss the same topic. The gaps usually come from how the product scope is set, which years are treated as the base, and how pricing and volume are converted into a single USD value.

For this market, the biggest differences tend to come from whether adjacent ingredients are blended into the total, how dry versus liquid pricing is handled, and whether a broader protein ingredient definition is used instead of wheat-only. Some estimates also use earlier-year price levels or longer forecast windows, and those choices can raise or lower the implied current-year value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 768.57 M (2026) | |

| Market Publisher A | USD 920.50 M (2026) | Uses a longer 2026 to 2036 framing and typically assumes faster expansion in meat alternatives, which can lift the near-term level when back-calculated, and it is less clear how dry and liquid formats are priced separately. |

| Industry Reseller B | USD 730.30 M (2025) | Reports a different base year and may apply a blended average price across types and applications, which can compress the value versus a type and form specific price build, and it can also reflect earlier currency timing. |

The table shows that year choice, pricing treatment, and how tightly wheat-only scope is kept can explain most of the spread. When isolates, concentrates, and hydrolyzed products are counted only as wheat-derived ingredient sales in Europe, and when dry versus liquid pricing is modeled distinctly, the total comes out differently, a modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

How large is the Europe wheat protein market size today?

The market is valued at USD 768.57 million in 2026 and is forecast to reach USD 992.15 million by 2031.

Which segment shows the highest growth?

Hydrolyzed wheat protein, valued for enhanced digestibility and cosmetic functionality, exhibits the fastest CAGR at 7.36% between 2026 and 2031.

What are the main challenges?

Price volatility in wheat grain, increasing incidences of celiac disease, and competitive pressure from emerging plant proteins can affect growth trajectories.

Why is the Europe wheat protein market growing?

Continued expansion rests on rising plant-based demand, supportive policies such as Germany’s “Proteins-of-the-Future” funding, and the ingredient’s unique functional traits in bakery and meat alternatives.

Page last updated on: