High Tibial Osteotomy Plates Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 270.36 Million |

| Market Size (2031) | USD 330.78 Million |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

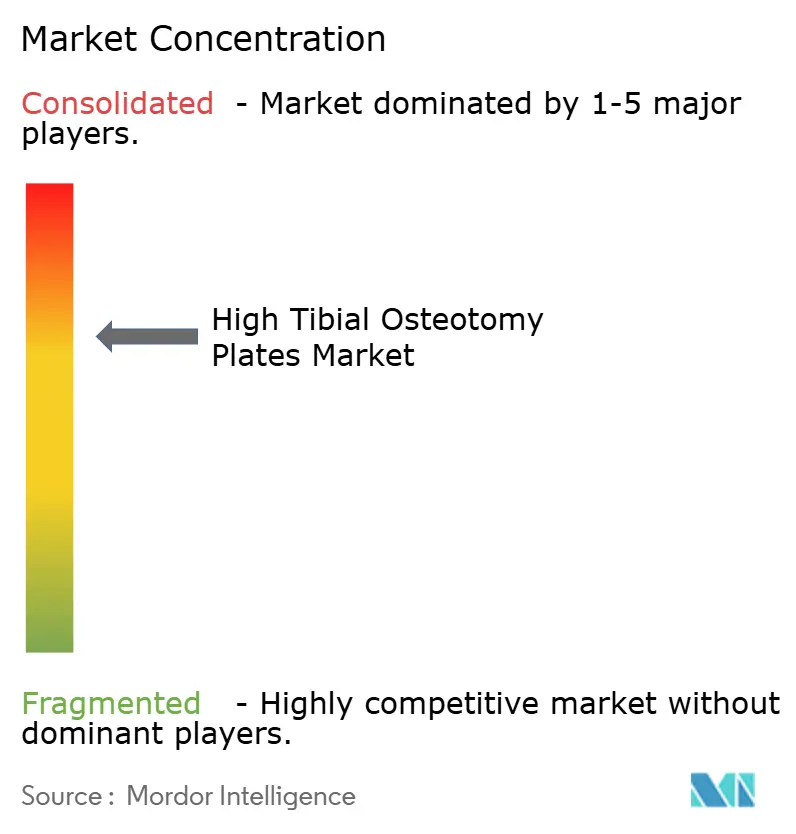

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Tibial Osteotomy Plates Market Analysis by Mordor Intelligence

The High Tibial Osteotomy Plates Market size is expected to grow from USD 259.67 million in 2025 to USD 270.36 million in 2026 and is forecast to reach USD 330.78 million by 2031 at 4.12% CAGR over 2026-2031.

Growth is fueled by surgeons’ preference for joint-preserving surgery over total knee arthroplasty, steady innovation in hybrid metal-polymer plates, and rising procedure volumes at ambulatory surgery centres. Wider adoption of radiolucent PEEK designs and patient-specific implants supports premium pricing. Meanwhile, revision rates that remain higher than primary arthroplasty create demand for more durable fixation solutions. Regulatory changes that align the FDA Quality Management System Regulation with ISO 13485:2016 may initially raise compliance costs but should streamline future approvals, shortening the product development cycle.

Key Report Takeaways

- By material, metals led with 64.83% of the high tibial osteotomy plates market share in 2025; polymers are projected to expand at a 5.64% CAGR to 2031.

- By technique, opening-wedge procedures accounted for 52.58% revenue in 2025, while hybrid plate-frame constructs are forecast to grow at 6.62% CAGR through 2031.

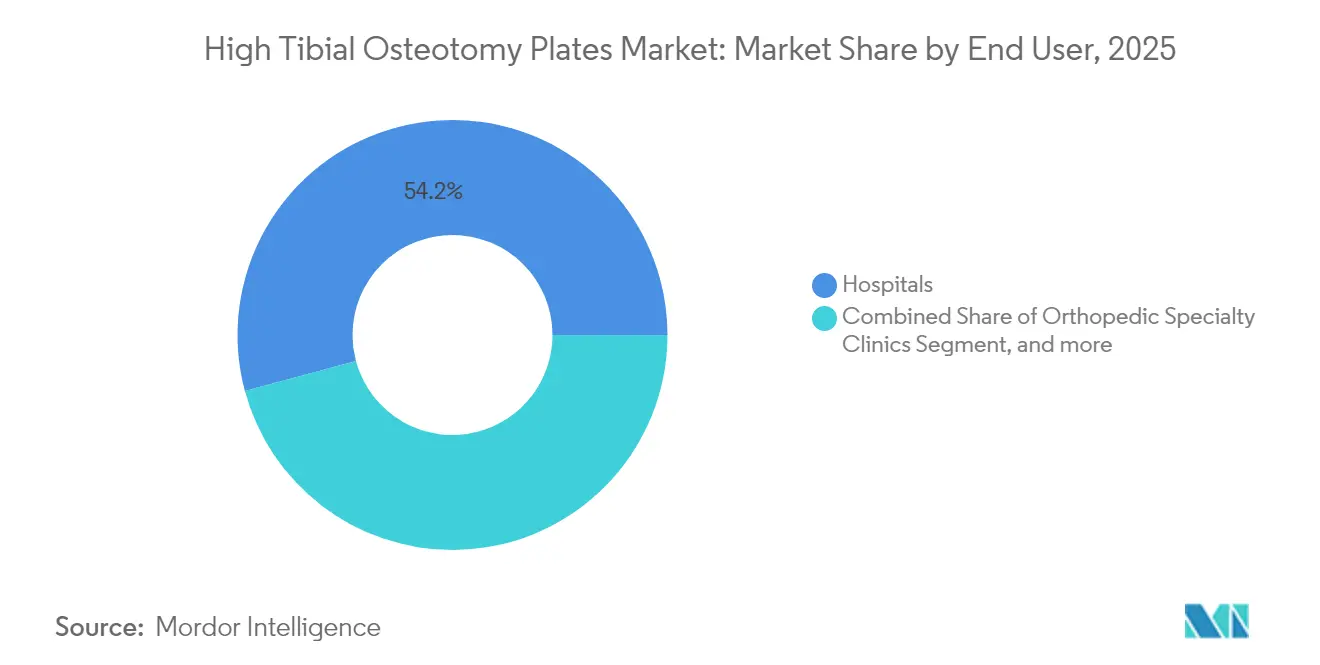

- By end user, hospitals held 54.19% of the high tibial osteotomy plates market size in 2025; ambulatory surgery centres record the fastest growth at 4.89% CAGR.

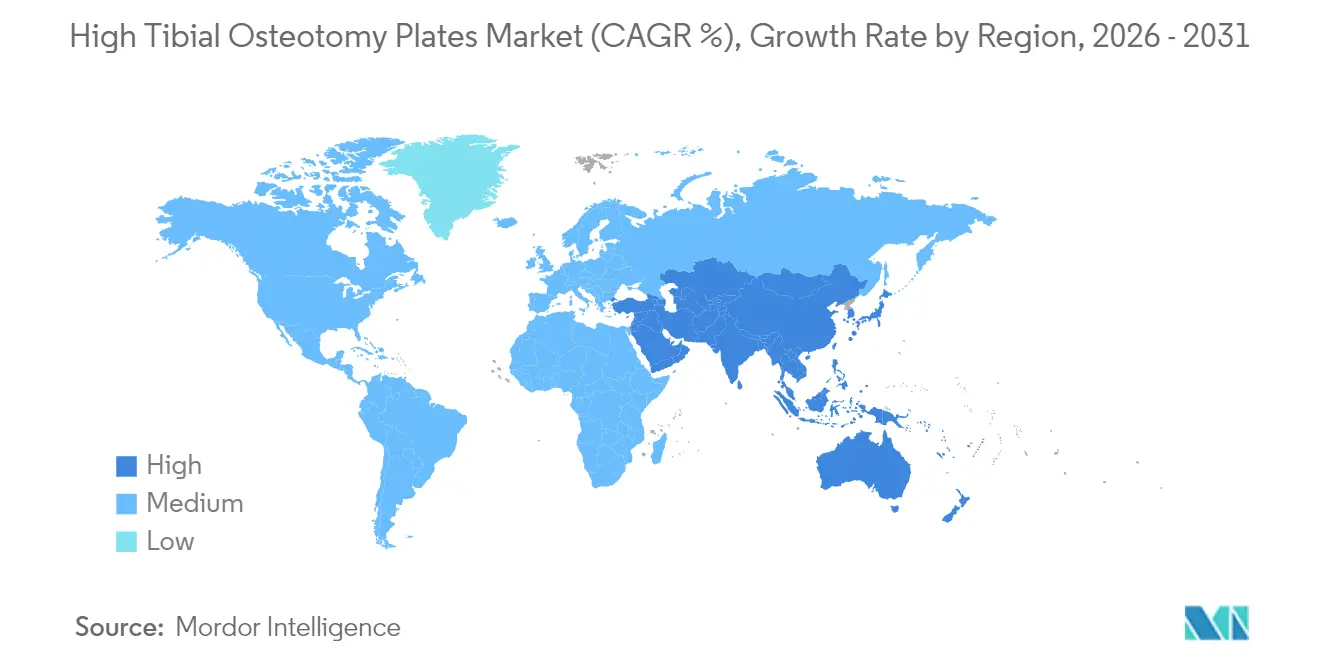

- By geography, North America captured 37.03% of 2025 revenue, yet Asia is advancing at a 5.49% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High Tibial Osteotomy Plates Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of osteoarthritis & varus knee deformities | +1.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Aging-athlete population boosting joint-preserving surgeries | +0.8% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Continuous plate innovations (low-profile, locking, hybrid metals-PEEK) | +0.6% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Patient-specific 3D printed plates entering clinical practice | +0.4% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Sports-medicine insurers covering HTO in APAC markets | +0.3% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Shift toward day-care HTO boosting ASC volumes in North America | +0.5% | North America, early adoption in Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Osteoarthritis & Varus Knee Deformities

Adults aged 30-44 already represent 32.97 million osteoarthritis cases worldwide, and electronic health-record analyses that combine narrative notes with coded data double prevalence estimates to 11.8% compared with diagnosis codes alone. Elevated BMI remains the leading modifiable risk factor. The surge in disease burden among younger, active adults sustains demand for joint-preserving options, positioning the high tibial osteotomy plates market as a durable growth story through 2030.[1]B. Kim et al., “Global incidence and prevalence of knee osteoarthritis,” biomedcentral.com

Aging-Athlete Population Boosting Joint-Preserving Surgeries

Retired professional footballers show 28% knee osteoarthritis prevalence versus 13% during their careers, underscoring the cumulative impact of repetitive stress. Long-term follow-up studies report 85% satisfaction after high tibial osteotomy and 95% survival at five years in optimally selected patients, encouraging surgeons to recommend osteotomy over arthroplasty for athletes under 50 with BMI < 25. The resulting willingness to pay supports rapid uptake of premium patient-specific plates.

Continuous Plate Innovations

Finite-element optimisation has delivered low-profile angular-stable systems such as TomoFix Anatomical plates that lower implant prominence and cut lateral-hinge stress. Carbon fibre-reinforced PEEK reduces stress shielding versus titanium yet maintains fixation strength, while protective screws decrease hinge-fracture risk by 62%. Johnson & Johnson’s VOLT Plating System illustrates how variable-angle locking and dynamic compression now converge in a single implant platform.[2]AO Foundation, “TomoFix anatomical plate system,” aofoundation.org

Patient-Specific 3D-Printed Plates Entering Clinical Practice

Additive manufacturing enables plates that match a patient’s tibial contour, reducing operating-room adjustments. The FDA approval of restor3d’s talus implant and the rapid 510(k) for Curiteva’s porous PEEK lumbar cage show regulators’ growing comfort with bespoke devices. Streamlined patient-matched guide guidance suggests that bench testing alone will suffice for some future submissions, accelerating time to market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedural & implant cost vs. TKA reimbursement gaps | -0.9% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Revision risk from hinge-fracture & non-union events | -0.7% | Global, higher impact in less experienced centers | Long term (≥ 4 years) |

| Slow regulatory clearance cycles for novel biomaterials | -0.5% | North America & Europe regulatory jurisdictions | Short term (≤ 2 years) |

| Limited surgeon training outside tier-1 orthopedic centers | -0.6% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procedural & Implant Cost vs. TKA Reimbursement Gaps

Direct medical costs favour high tibial osteotomy at USD 20,436 versus USD 24,637 for unicompartmental or total knee arthroplasty, yet payer schedules still reimburse arthroplasty more generously. In Canada and Japan, reimbursement misalignment leaves hospitals under-compensated for HTO despite its clinical benefits, limiting access in publicly funded systems.[3]S. Martin et al., “High tibial osteotomy cost-effectiveness versus arthroplasty,” jbjs.org

Revision Risk from Hinge-Fracture & Non-Union Events

Lateral hinge fractures occur in 25% of medial opening-wedge procedures and push overall complication rates beyond 15%. Type II and III fractures heighten instability and can delay union, while TKA performed after failed HTO shows 7.66% revision compared with 3.79% for primary TKA. These risks raise surgeon caution, particularly in centres with low case volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Metals Dominate Despite Polymer Innovation

Metals held 64.83% of 2025 revenue, anchoring the high tibial osteotomy plates significant market size. Surgeons rely on titanium for strength, biocompatibility, and broad instrument compatibility. Stainless steel retains a foothold in budget-sensitive settings despite fatigue concerns. The numerical leadership of metals reflects decades of outcome data and established reimbursement coding.

Polymers, chiefly PEEK, are growing at a 5.64% CAGR through 2031, the fastest of any material class. Carbon-fibre-reinforced PEEK diffuses load and improves imaging, while magnesium-based bio-absorbables show lower revision (1/275) versus titanium (18/111). Surface modifications such as hydroxyapatite coatings improve osteointegration, auguring a wider role for polymers. If hybrid designs meet durability benchmarks, polymer composites may approach one quarter of the high tibial osteotomy plates market by 2031.

By Technique: Opening-Wedge Leadership Challenged by Hybrid Innovation

Opening-wedge operations generated 52.58% of 2025 revenue. Familiar workflow, abundant instrumentation, and favourable anatomic corrections underpin this preference. However, single-plate constructs suffer lateral hinge stress that fuels 25% fracture incidence.

Hybrid plate-frame configurations are advancing at 6.62% CAGR. Biplanar cuts paired with lateral hinge screws lower instability, and retrotubercle modifications increase fixation by 62%. Greater slope control and reduced graft need make hybrids attractive for complex varus deformities. As long as training gaps close, hybrid constructs could command one third of the high tibial osteotomy plates market by 2031.

By End User: Hospital Dominance Erodes as ASCs Gain Momentum

Hospitals controlled 54.19% of global revenue in 2025, yielding major revenue in the high tibial osteotomy plates market. Integrated imaging, intensive-care support, and readiness for complex revisions keep hospitals at the centre of high-risk cases.

Ambulatory surgery centres are growing at 4.89% CAGR. Day-case opening-wedge procedures using intraosseous PEEK implants now discharge in 5.6 hours, with 77% of patients achieving clinically important improvements. The CMS removal of TKA from inpatient-only status signals payer comfort with outpatient orthopaedics, encouraging insurers to extend similar coverage to HTO. Partnerships between high-volume surgeons and ASC operators will accelerate share gains for this channel.

Geography Analysis

North America contributes 37.03% of 2025 sales, driven by early adoption of hybrid plates, widespread sports medicine coverage, and robust ASC infrastructure. Commercial insurers reimburse HTO at rates that approach arthroplasty, and the prevalence of sports injuries sustains high procedure volumes. The region’s regulatory clarity around 3D-printed implants further attracts new product launches.

Europe follows with stable uptake supported by ageing populations and strong public health systems. Germany and the Nordic countries favour joint preservation, although reimbursement caps in the United Kingdom temper growth. Continental centres of excellence disseminate training programs that slowly reduce complication variability across the bloc.

Asia-Pacific is the fastest-growing region at 5.49% CAGR. Korea’s high insurance approval rates for knee surgery and China’s expanding middle class are key demand drivers. Japan faces cost inflation that constrains hospital margins, yet rising osteoarthritis prevalence still expands the patient pool. Regulatory harmonisation under ASEAN Medical Device Directive will shape access timelines. Middle East & Africa and South America remain nascent, limited by surgeon density and capital budgets but poised to benefit from technology transfer.

Competitive Landscape

The high tibial osteotomy plates market remains moderately consolidated. DePuy Synthes anchors the field with TriLEAP and VOLT systems that combine low-profile contours and variable-angle locking. Zimmer Biomet followed with the Oxford Cementless Partial Knee, reinforcing its knee-preservation franchise. Stryker and Smith & Nephew focus on robotics integration, with the former leveraging the MAKO platform for precise osteotomy planning.

Specialist firms such as Arthrex and Integra LifeSciences concentrate on screw fixation enhancements and surgeon-specific kits. Meanwhile, Curiteva and restor3d pioneer 3D-printed patient-matched implants, creating a moat around custom instrumentation. FDA Predetermined Change Control Plans give established players a speed advantage in iterative improvements, potentially intensifying consolidation.

Future competition will hinge on digital workflow integration. Johnson & Johnson’s VELYS Robotic-Assisted Solution already covers unicompartmental knee arthroplasty; extending that guidance to osteotomy would differentiate its plate suite. Companies that bridge planning software, navigation, and advanced biomaterials are best positioned to grow share as surgeons prioritise reproducible outcomes and shorter theatre times.

High Tibial Osteotomy Plates Industry Leaders

Arthrex, Inc.

Smith & Nephew

Johnson & Johnson

Stryker Corporation

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Johnson & Johnson MedTech showcased advanced digital orthopaedics capabilities at AAOS 2025, highlighting the VELYS Robotic-Assisted Solution's FDA clearance for unicompartmental knee arthroplasty and introducing the VOLT Plating System with dynamic compression and variable angle locking technology

- November 2024: Zimmer Biomet received FDA approval for the Oxford Cementless Partial Knee, becoming the only cementless partial knee replacement implant approved in the United States, with commercial launch scheduled for Q1 2025

- August 2024: DePuy Synthes introduced the TriLEAP Lower Extremity Anatomic Plating System, featuring low-profile titanium plates designed for foot and ankle surgeons with enhanced customization capabilities

- June 2024: DePuy Synthes received 510(k) FDA clearance for the VELYS Robotic-Assisted Solution in Unicompartmental Knee Arthroplasty, expanding robotic capabilities beyond total knee replacement procedures

- February 2024: Curiteva Inc. achieved FDA 510(k) clearance for the Inspire 3D Printed Trabecular PEEK Lumbar Interbody Fusion System in under 60 days, representing the first novel 3D printing process for porous PEEK structures designed for enhanced biomechanical integration

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the high tibial osteotomy (HTO) plates market as all sterile, single-use fixation plates, metallic, polymeric, or composite, specifically engineered to realign the proximal tibia in varus or valgus knee deformities before the joint becomes irreversibly arthritic. We cover plates sold to hospitals, orthopedic specialty clinics, and ambulatory surgery centers across 17 major countries.

Scope exclusion: We do not count generic trauma plates used in other long-bone repairs or any implants intended for total or unicompartmental knee arthroplasty.

Segmentation Overview

- By Material

- Metals

- Titanium Plates

- Stainless-Steel Plates

- Polymers

- PEEK Plates

- Other High-Performance Polymers

- Bio-absorbable / Composite Plates

- Metals

- By Technique

- Opening-Wedge HTO

- Closing-Wedge HTO

- Biplanar / Distal-Tuberosity HTO

- Hybrid Plate-Frame Constructs

- By End User

- Hospitals

- Orthopedic Specialty Clinics

- Ambulatory Surgery Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with knee-preservation surgeons, distributor managers, and reimbursement advisors across North America, Europe, and Asia-Pacific. Their inputs helped us stress-test plate usage per surgery, average selling prices, and the growing shift of eligible cases to day-care settings, thereby tightening model assumptions generated from desk work.

Desk Research

We began with public health datasets, such as the WHO Global Musculoskeletal Disease Database, CDC Arthritis Surveillance, and OECD Health Statistics, which give us procedure prevalence and aging population trends. Customs trade codes for orthopedic implants (HS 902110) were mined through Volza, while implant patent activity was screened on Questel to flag upcoming technologies. Company 10-Ks, investor decks, national joint registries, and reputable associations like the International Society of Arthroscopy, Knee Surgery & Orthopaedic Sports Medicine added pricing and utilization color.

Our analysts also tapped paid repositories, including D&B Hoovers for supplier revenue splits and Dow Jones Factiva for press releases that confirm new regulatory approvals. The sources listed are illustrative; many additional publications supported data gaps, validation, and context building.

Market-Sizing & Forecasting

Using a top-down approach, we reconstructed the 2025 demand pool from country-level HTO procedure counts and then multiplied by validated plate-per-procedure ratios and weighted ASPs. Supplier revenue snapshots and channel checks created a bottom-up cross-check, allowing adjustments where divergence exceeded five percent. Key variables include osteoarthritis incidence, elective surgery backlog clearance, plate material mix shifts, ambulatory surgery penetration, and currency movement. We forecast with a multivariate regression that ties those drivers to volume and price trajectories, supported by expert consensus. Where bottom-up information was thin, we filled gaps through regional interpolation anchored to transparent assumptions.

Data Validation & Update Cycle

Outputs face anomaly checks, peer review, and management sign-off. Mordor refreshes every twelve months and reopens models sooner if recall notices, reimbursement changes, or large M&A events alter baselines; a final analyst pass ensures clients receive the latest view.

Why Mordor's High Tibial Osteotomy Plates Baseline Earns Trust

Published numbers seldom align because each firm chooses distinct scopes, base years, and price stacks.

Our team explains below how those choices drive gaps and why Mordor's disciplined mix of procedure analytics, real-time pricing, and timely refresh keeps decisions on firm ground.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 259.67 M (2025) | Mordor Intelligence | - |

| USD 238.9 M (2024) | Regional Consultancy A | Excludes bio-absorbable polymer plates and uses earlier exchange rates |

| USD 226.4 M (2022) | Global Consultancy B | Relies on older base year and assumes slower ambulatory shift |

| USD 266.07 M (2023) | Industry Association C | Applies blended trauma plate ASPs across femur and tibia segments |

The comparison shows that when plate categories, care settings, and currency timing are aligned, spreads narrow sharply, reinforcing that Mordor's transparent scope selection and yearly recalibration offer the most dependable baseline for stakeholders.

Key Questions Answered in the Report

What is the current size of the high tibial osteotomy plates market?

The high tibial osteotomy plates market size stands at USD 270.36 million in 2026 and is expected to reach USD 330.78 million by 2031.

Which material segment is growing fastest?

Polymer-based plates, mainly PEEK composites, expand at a 5.64% CAGR due to radiolucency and lower stress shielding.

Why are ambulatory surgery centres gaining share?

Same-day discharge protocols and insurer support allow opening-wedge procedures with PEEK implants to finish in 5.6 hours, driving 4.89% CAGR in ASC demand.

What geographic region is expanding most quickly?

Asia-Pacific posts the fastest growth at 5.49% CAGR, led by Korea’s high procedural volumes and China’s ageing population.

How do hybrid plate-frame constructs improve outcomes?

Hybrid systems distribute load more evenly and reduce lateral hinge fracture risk by up to 62%, supporting complex deformity correction and quicker rehabilitation.

What regulatory changes will affect manufacturers after 2026?

The FDA Quality Management System Regulation will align with ISO 13485:2016, raising compliance obligations yet promising smoother global approvals thereafter.

Page last updated on: