Golf Tourism Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

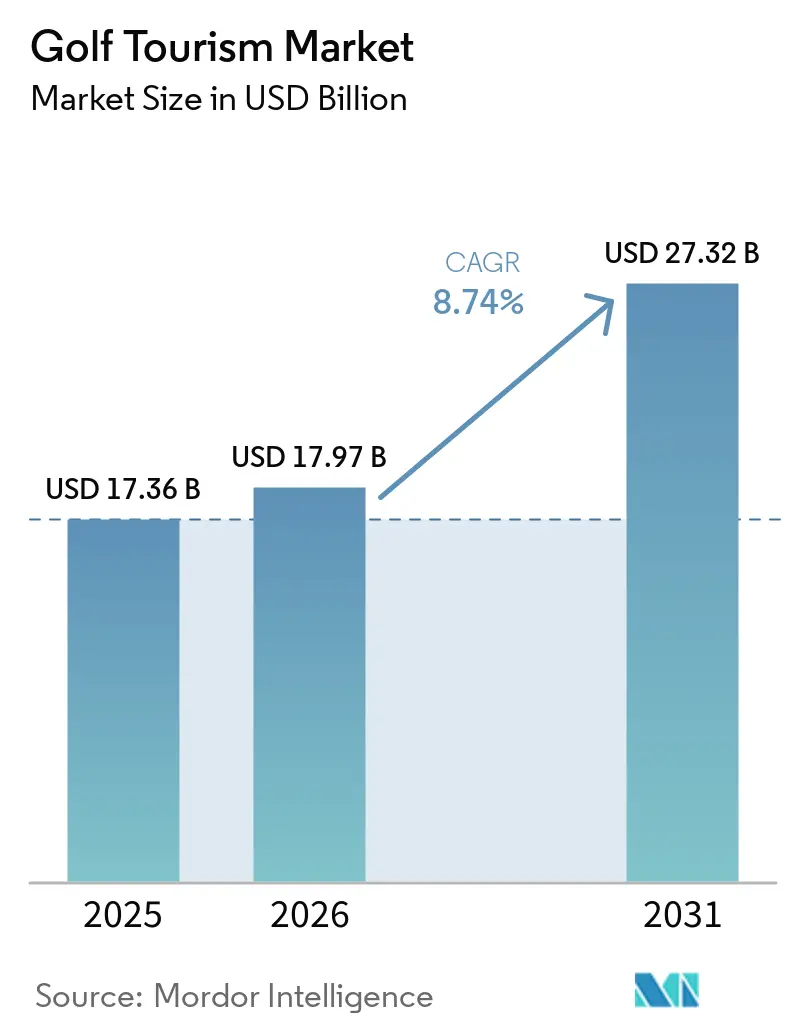

| Market Size (2026) | USD 17.97 Billion |

| Market Size (2031) | USD 27.32 Billion |

| Growth Rate (2026 - 2031) | 8.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Golf Tourism Market Analysis by Mordor Intelligence

The Golf Tourism Market size is projected to expand from USD 17.36 billion in 2025 and USD 17.97 billion in 2026 to USD 27.32 billion by 2031, registering a CAGR of 8.74% between 2026 to 2031.

The golf tourism market is expanding because high-spending leisure travelers now expect golf trips to include wellness, culture, and family-oriented resort experiences rather than only course access. The demand base is also widening, as the R&A reported that more than 100 million adults and juniors played golf across R&A-affiliated markets in 2024, with participation continuing to rise in 2025[1]RANDA.ORG https://www.randa.org/en/articles/over-100-million-golfers-in-randa-markets-as-global-participation-continues-to-grow. North America remained the largest regional revenue base in 2025, while Asia-Pacific is set to post the fastest expansion through 2031 as newer destinations convert broader leisure infrastructure into golf-led travel programs. The market also remains open to specialist operators because no single company controls a meaningful global position, although trade networks such as IAGTO continue to strengthen distribution efficiency and forward bookings across destinations. At the same time, water use and course sustainability are moving closer to the center of destination selection, especially after the USGA committed USD 30 million over 15 years to help courses reduce water use by 45%[2]USGA.ORG https://www.usga.org/content/usga/home-page/articles/2024/09/every-drop-counts.html..

Key Report Takeaways

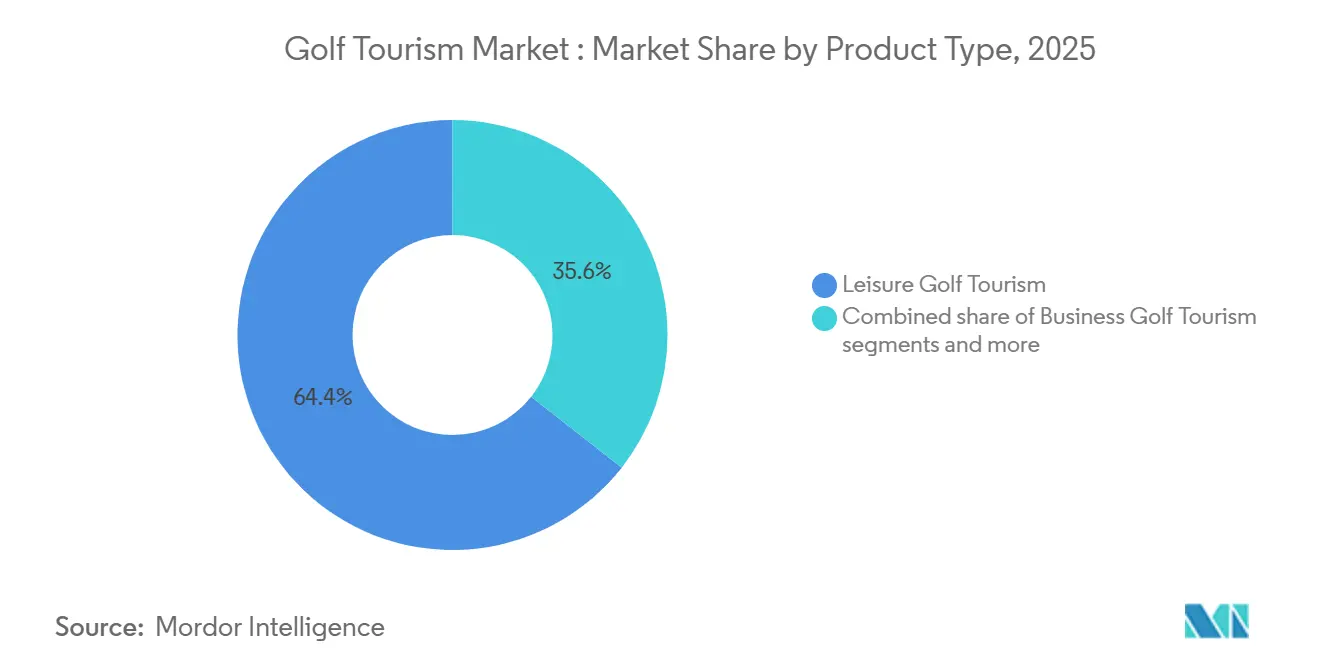

- By tourism type, leisure golf tourism held 64.4% of the global golf tourism market share in 2025, while tournament golf tourism is forecast to grow at a 9.6% CAGR through 2031.

- By tourist type, domestic travelers accounted for 58.0% of the global golf tourism market share in 2025, while international travelers are projected to expand at an 8.9% CAGR through 2031.

- By service type, professional tours represented 54.9% of the global golf tourism market share in 2025, while personal tours are expected to grow at a 9.6% CAGR through 2031.

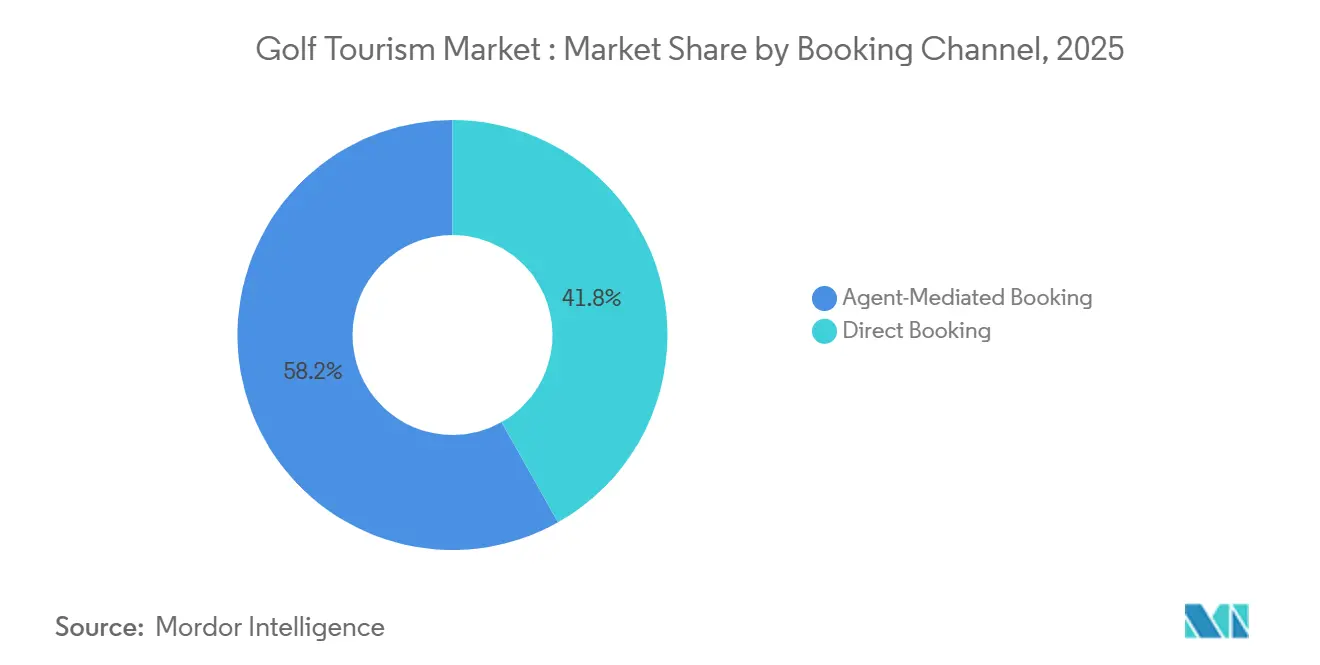

- By booking channel, direct bookings captured 41.8% of the global golf tourism market share in 2025 and are also the fastest-growing channel, with a projected 9.2% CAGR through 2031.

- By destination type, resort-based Golf held 52.3% of the global golf tourism market share in 2025, while international golf circuits are forecast to grow at a 10.1% CAGR through 2031.

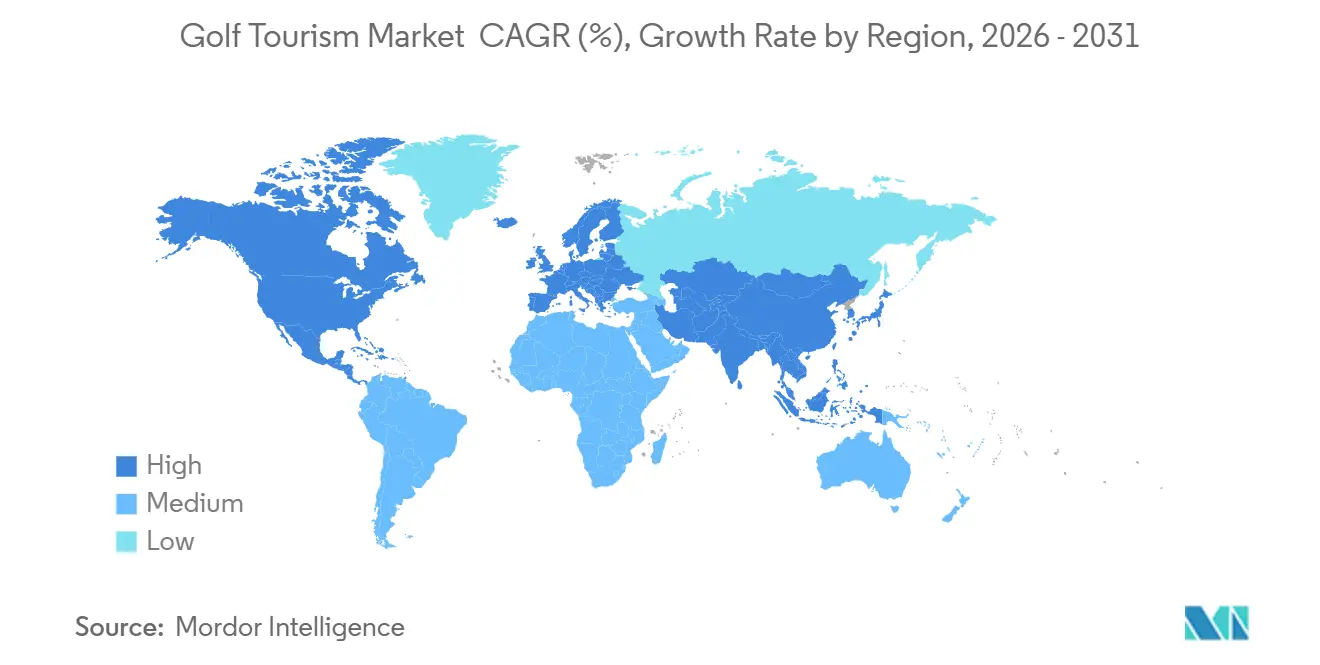

- By geography, North America held 39.9% of the global golf tourism market share in 2025, while Asia-Pacific is projected to expand at a 9.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Golf Tourism Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Spend on Premium Experiential Leisure Travel | +2.0% | Global, with concentrated uplift in North America, Europe, and the Middle East | Medium term (2-4 years) |

| Expansion of Golf Resorts and Tournament-Led Destination Infrastructure | +1.6% | Middle East, Asia-Pacific, and North Africa | Long term (≥ 4 years) |

| Digital Booking Adoption and Mobile Trip Discovery | +0.9% | Global, strongest in North America, the UK, South Korea, and Australia | Short term (≤ 2 years) |

| Rising Amateur Golf Participation and Leisure-Sport Crossover | +1.3% | Asia-Pacific core, with spillover to South and Southeast Asia | Medium term (2-4 years) |

| Shift Toward Golf-Plus Itineraries in Emerging Value Destinations | +0.7% | Asia-Pacific, the Middle East and Africa, and South America | Medium term (2-4 years) |

| IAGTO-Led Trade Pipeline Accelerating Forward Bookings | +0.4% | Global, with early gains in Europe, the Middle East and Africa, and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Spend on Premium Experiential Leisure Travel

The golf tourism market is benefiting from the broader shift toward premium leisure trips that combine activity, comfort, and longer stays. UNWTO reported that average international tourist spending reached USD 1,170 per trip in 2024, 17% above the pre-pandemic average, indicating that travelers continued to prioritize higher-value experiences[3]UNWTO-AP.ORG https://en.unwto-ap.org/news/worldtourismbarometer_jan2025. That pattern matters more in golf travel because the typical traveler is already prepared to pay for access, service quality, and time convenience. Resorts are responding by packaging golf with wellness, recovery, and dining so that more of the traveler's budget stays inside the property. This also improves repeat business, because travelers who receive dependable tee access and a seamless on-site experience are more likely to rebook similar trips.

Expansion of Golf Resorts and Tournament-Led Destination Infrastructure

The golf tourism market is gaining new supply from destination-building programs that combine resort construction with event visibility. Red Sea Global opened Shura Links in September 2025 as Saudi Arabia's first island golf course, linking the course to a larger resort destination on Shura Island. Tournament infrastructure is reinforcing the same trend, as LIV Golf said its 2025 UK event generated USD 63 million in local economic impact, and South Australia confirmed that Adelaide will remain the league's exclusive Australian host through at least 2031[4]LIVGOLF.COM https://www.livgolf.com/news/liv-golf-uk-and-global-economic-impact. These projects do more than add inventory, because they also create destination awareness that feeds later leisure bookings. Over time, the destinations with both premium resort stock and recurring event exposure are likely to capture a larger share of international demand.

Digital Booking Adoption and Mobile Trip Discovery

The golf tourism market is moving toward a split model in which self-directed booking and specialist operator support coexist. Repeat travelers are more comfortable researching destinations online and moving directly from course discovery to package selection when dates and availability are easy to confirm. At the same time, specialist operators remain important because golf trips still involve tee-time coordination, course access, accommodation planning, and local transport. This makes digital convenience more useful as a front-end discovery tool than as a full replacement for service depth across all trip types. The booking model gaining ground combines simple online browsing with reliable, specialist execution as itineraries become more complex.

Rising Amateur Golf Participation and Leisure-Sport Crossover

The golf tourism market has a durable demand pipeline, as the global player base continues to expand. The R&A reported that participation across its affiliated markets rose by nearly 3 million year over year, confirming that golf is adding new adult and junior players rather than only recycling the same traveler pool. A larger player base matters for tourism because even modest conversion from local play into travel creates meaningful package demand over time. The crossover from driving range and casual participation to full-on-course play also widens the addressable audience for future travel products. This supports a longer-term demand base for destinations that can offer accessible resort experiences, beginner-friendly formats, and short-stay packages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Trip Costs and Long-Haul Affordability Pressure | -1.6% | Global, most acute in South America, Africa, and price-sensitive Asia-Pacific segments | Medium term (2-4 years) |

| Water, Land-Use, and Chemical-Intensity Scrutiny on Golf Assets | -0.9% | Arid markets, including the Southwest United States, the Middle East, Southern Europe, and Australia | Long term (≥ 4 years) |

| Tee-Time Bottlenecks at Marquee Courses Limiting Scalable Package Inventory | -0.7% | North America, Scotland, and Ireland | Medium term (2-4 years) |

| Direct-Booking Disintermediation Compressing Tour-Operator Margins | -0.5% | Global, strongest in North America and Northern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Trip Costs and Long-Haul Affordability Pressure

The golf tourism market still relies on a premium pricing structure, which keeps a portion of future demand out of reach in lower-income source regions. UN Tourism identified high transport and accommodation costs among the main challenges for international tourism in 2025, which is especially relevant for golf travelers because their trips already involve above-average package values. The pressure is lower in North America and Northern Europe, where affluent golfers are less price-sensitive. It is more restrictive in newer source markets where participation is rising faster than outbound travel budgets. This means operators that build shorter-haul, better-value itineraries will be better positioned than those that rely solely on prestige-led pricing.

Water, Land-Use, and Chemical-Intensity Scrutiny on Golf Assets

The golf tourism market faces a longer-term supply issue because environmental compliance is becoming part of how regulators and travelers judge destinations. The GCSAA reported that U.S. golf facilities applied 1.63 million acre-feet of water in 2024, which keeps water efficiency at the center of operational planning in stressed regions. The USGA's 15/30/45 program shows that the sector itself expects tighter scrutiny and is funding practical reductions in water use rather than treating the issue as a branding exercise. Andalusia offers a more constructive template, as AECG said golf courses in the region used only 0.2% of conventional agricultural irrigation water and increasingly relied on regenerated water. The destinations that can document efficient water management are likely to defend their attractiveness better than those that cannot.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tourism Type: Tournament Formats Reshaping Revenue Mix

Leisure Golf Tourism accounted for 64.4% of revenue in 2025, making it the largest segment of the golf tourism market by travel purpose. That leadership reflects the large base of repeat leisure golfers, who still generate most of the package volume across resort and multi-course trips. Business Golf Tourism remained a smaller but steady category because it is linked to corporate hosting, networking trips, and incentive travel. Tournament Golf Tourism was smaller in 2025, but it is changing the direction of the golf tourism market because event schedules now shape destination visibility and trip timing more directly than before.

Tournament Golf Tourism is forecast to grow at a 9.6% CAGR through 2031, making it the fastest-moving revenue stream in the golf tourism market by tourism type. LIV Golf said its global economic impact has passed USD 1.5 billion, with USD 600 million generated in 2025 alone across 17 locations. The PGA of America also formalized golf travel as a more active commercial channel by naming Premier Golf its official golf vacation partner in January 2025. The main limit is not demand, because host destinations still need enough rooms, transport capacity, and premium tee-time inventory to convert event interest into extended stays.

By Tourist Type: International Segment Narrows the Gap

Domestic travelers accounted for 58.0% of revenue in 2025, making them the largest segment in the golf tourism market by tourist type. This base is supported by strong internal travel systems in countries such as the United States and by long-established domestic golf cultures in markets such as Japan. Japan also recorded 42.68 million inbound visitors in 2025, with total inbound tourism consumption reaching JPY 9.5 trillion, which was equivalent to USD 64 billion, showing how intense the competition for foreign visitor spending has become. Even with that competition, the golf tourism market still has room to increase the international mix, as golf travelers typically spend more time and money per trip than general visitors.

International travelers are projected to grow at a 8.9% CAGR through 2031, faster than the domestic side of the golf tourism market. Better air connectivity and easier cross-border travel within Asia and the Middle East are widening the pool of outbound golf travelers. International travelers also tend to stay longer and spend more on accommodation, transport, dining, and premium tee access. As a result, destinations that can combine airport access, multi-course itineraries, and resort convenience are likely to close the gap with more domestic-led markets.

By Service Type: Professional Tours Lead, but Personalization Gains Ground

Professional tours held 54.9% of the golf tourism market share in 2025, keeping them ahead of personal formats in service delivery. Many first-time international golfers still prefer packaged travel because it reduces the risk around tee times, lodging, local transfers, and on-ground coordination. That preference is especially strong on long-haul or multi-country trips, where a single booking error can disrupt the entire journey. For that reason, the golf tourism market continues to reward operators that can guarantee access and deliver dependable service on arrival.

Personal tours are forecast to grow at a 9.6% CAGR through 2031, showing that the golf tourism market is also shifting toward more customized trip building. The PGA of America's partnership with Premier Golf supports this change because brand-led endorsements help packaged providers stay relevant while they offer more flexible planning options. The likely outcome is a hybrid format where travelers choose from curated components rather than from rigid departures. That structure lets operators maintain quality control while giving experienced golfers greater flexibility over dates, courses, and stay length.

By Booking Channel: Direct Booking Dominates but Fuels Margin Debate

Direct Booking held 41.8% of revenue in 2025 and is also projected to grow at a 9.2% CAGR, giving it the strongest combined position in the golf tourism market by booking channel. Travelers increasingly value immediate price visibility and fast confirmation when they already know the destination and preferred course set. That makes direct booking especially effective for repeat trips and shorter-haul resort packages. Even so, the golf tourism market still supports agent-mediated demand because many golf trips remain too complex for fully self-managed planning.

Agent-mediated channels continue to matter in the golf tourism market for group itineraries, premium bucket-list travel, and any trip where protected inventory is critical. IAGTO said its global network includes 802 specialist tour operators in 66 countries, responsible for more than 90% of golf vacation packages sold worldwide, underscoring the scale of the specialist channel. That ecosystem remains valuable because licensed specialists can coordinate liability, scheduling, and supplier relationships more effectively than a simple booking interface. Margin pressure will increase for intermediaries that do not add clear value, but the channel is unlikely to disappear where local access and trip protection still matter.

By Destination Type: Resort Infrastructure Dominates, Circuits Accelerate

Resort-based golf accounted for 52.3% of the golf tourism market in 2025, reflecting the continued pull of integrated stay-and-play destinations. These locations combine course access, accommodation, dining, and wellness in one setting, reducing trip friction and encouraging longer stays. Mature destinations in the United States, Spain, Portugal, Scotland, and Ireland still benefit from this model because they have deep resort ecosystems and established reputations. For that reason, the golf tourism market remains anchored by resort destinations even as newer formats gain momentum.

International golf circuits are forecast to expand at a 10.1% CAGR through 2031, making them the fastest-growing destination type in the golf tourism market. LIV Golf's multi-country event strategy is part of that shift, and South Australia said LIV Golf Adelaide continued to support hotel demand and broader visitor spending in 2026. Event-led circuits help emerging destinations gain recognition more quickly by placing a new location into the travel consideration set almost immediately. Urban golf destinations and cruise packages remain smaller, but they serve distinct traveler groups that value convenience, variety, or a broader leisure itinerary.

Geography Analysis

North America accounted for 39.9% of revenue in 2025, while Europe remained the second-largest regional block, giving these two regions the strongest foundation in the golf tourism market, with deep infrastructure and established demand. North America benefits from dense course supply, strong domestic travel habits, and steady outbound demand from U.S. and Canadian golfers to Scotland, Ireland, Spain, and the Caribbean. Europe continues to draw strength from Spain's role as a gateway destination, and AECG said Spain received 1.4 million golf tourists and generated EUR 15.9 billion, which was equivalent to USD 17.3 billion, in total economic impact. AECG also said Spain's registered golfer base exceeded 305,600 at the end of 2024, showing that the domestic feeder base is expanding alongside international arrivals. This keeps the golf tourism market well supported in both regions, even though growth rates are now faster elsewhere.

Asia-Pacific is projected to grow at a 9.4% CAGR through 2031, which makes it the fastest-growing region in the golf tourism market. The region benefits from strong inbound tourism in Japan, established outbound demand in South Korea, and rising destination visibility across Southeast Asia. Japan's 2025 inbound total of 42.68 million visitors and JPY 9.5 trillion in travel consumption created a favorable backdrop for golf-led leisure products that sit outside the standard cultural itinerary. Australia is also strengthening its role in the golf tourism market through recurring event exposure, with South Australia confirming that LIV Golf Adelaide will continue through at least 2031 and move to North Adelaide Golf Course by 2028. The region's advantage is that it combines a growing player base with improving leisure infrastructure, which gives both domestic and cross-border demand more routes to convert into golf travel.

South America is forecast to grow at a 7.8% CAGR through 2031, while the Middle East and Africa remain the most visible emerging opportunity set in the golf tourism market. Saudi Arabia is pushing the strongest build-out, as Red Sea Global opened Shura Links in 2025 and GolfNorth, with Sumou Global Investment, announced new golf and lifestyle destinations across Riyadh, Jeddah, and Al Khobar. In South America, Brazil recorded 9.3 million international tourists in 2025, its highest-ever figure, and widened the inbound market that golf destinations can target. The golf tourism market in these regions still starts from a smaller installed base, but the direction of infrastructure investment and visitor growth is clearly positive.

Competitive Landscape

The golf tourism market remains highly fragmented, with the top player holding 3.2% of global share and the top five operators together accounting for 8.7%. This leaves most of the volume in the hands of regional specialists that compete through local access, destination expertise, and repeat relationships rather than on scale alone. In that setting, brands with a narrow regional focus can still build durable positions if they control trusted supplier networks and reliable itinerary execution. The golf tourism market, therefore, favors depth in selected destinations more than broad global coverage without strong local service. That structure also means competitive advantage often comes from product quality and course access rather than from price alone.

Several strategic moves show how companies are trying to strengthen their role in the golf tourism market without relying only on volume expansion. The PGA of America's partnership with Premier Golf in January 2025 strengthened Premier Golf's referral pathway into North America. It tied packaged travel more closely to a trusted industry institution. Red Sea Global's launch of Shura Links added a flagship asset that supports both destination branding and future resort-led package demand in the golf tourism market. LIV Golf's continued expansion across host markets also serves as a competitive supply catalyst, as event-led exposure helps destinations and travel sellers build packaged demand around a global schedule. These moves do not remove fragmentation, but they do raise the importance of brand partnerships, owned assets, and event-linked distribution.

Specialist networks still matter because the golf tourism market depends on coordination across operators, resorts, courses, and destination suppliers. IAGTO remains central to that structure, with 802 specialist tour operators in 66 countries and a role in more than 90% of golf vacation packages sold worldwide. Company disclosures also show that specialist reputation continues to matter, as Golfasian said it has served more than 192,000 golfers over 25 years in Asia. As a result, the golf tourism market is likely to remain open and fragmented even as stronger branded networks gradually improve their position.

Golf Tourism Industry Leaders

Golfbreaks

PerryGolf

Premier Golf

Golfasian

Carr Golf

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Fairways of Eden launched tailor-made golf holidays across Bangkok, Phuket, Pattaya, Hua Hin, Chiang Mai, Koh Samui, and other Thailand destinations, replacing fixed package formats with fully customizable trip architectures.

- February 2026: 360 Golf Holidays launched luxury Greece golf breaks featuring Costa Navarino Resort, adding four 18-hole championship courses designed by Bernhard Langer, Robert Trent Jones Jr., and José María Olazábal to its 2026-2027 portfolio.

- September 2025: Red Sea Global officially opened Shura Links, Saudi Arabia's first island golf course, as part of The Red Sea project, managed by Golf Saudi and accessible to 11 Shura Island resort hotels.

- April 2025: GolfNorth (Canada) and Sumou Global Investment (Saudi Arabia) announced a joint venture to develop luxury golf resort communities in Riyadh, Jeddah, and Al Khobar, with groundbreaking in 2025 and phased openings from 2027, targeting 100 total domestic Saudi golf venues.

- March 2025: Premier Golf and Magellan Jets announced an exclusive partnership bundling private aviation charter with bespoke golf vacations to Pebble Beach, Casa de Campo, and other top global destinations, targeting ultra-high-net-worth small groups and corporate clients.

Global Golf Tourism Market Report Scope

| Leisure Golf Tourism |

| Business Golf Tourism |

| Tournament Golf Tourism |

| Domestic |

| International |

| Personal Tours |

| Professional Tours |

| Direct Booking |

| Agent-Mediated Booking |

| Resort-based Golf |

| Urban Golf Destinations |

| International Golf Circuits |

| Golf Cruise Packages |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| APAC | Asia | India |

| China | ||

| Japan | ||

| South Korea | ||

| South East Asia | ||

| Rest of Asia | ||

| Oceania | Australia | |

| Rest of Oceania | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Tourism Type | Leisure Golf Tourism | ||

| Business Golf Tourism | |||

| Tournament Golf Tourism | |||

| By Tourist Type | Domestic | ||

| International | |||

| By Service Type | Personal Tours | ||

| Professional Tours | |||

| By Booking Channel | Direct Booking | ||

| Agent-Mediated Booking | |||

| By Destination Type | Resort-based Golf | ||

| Urban Golf Destinations | |||

| International Golf Circuits | |||

| Golf Cruise Packages | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Peru | |||

| Chile | |||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| BENELUX | |||

| NORDICS | |||

| Rest of Europe | |||

| APAC | Asia | India | |

| China | |||

| Japan | |||

| South Korea | |||

| South East Asia | |||

| Rest of Asia | |||

| Oceania | Australia | ||

| Rest of Oceania | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the golf tourism market in 2026?

The golf tourism market is valued at USD 18.0 billion in 2026 and is forecast to reach USD 27.3 billion by 2031, with an 8.7% CAGR.

Which region leads golf travel demand?

North America led in 2025 with a 39.9% revenue share, supported by deep course infrastructure and strong domestic and outbound travel demand.

Which region is growing the fastest for golf-related travel?

Asia-Pacific is the fastest-growing region with a projected 9.4% CAGR through 2031, supported by expanding leisure infrastructure and strong inbound momentum.

What is the largest travel format in this sector?

Leisure Golf Tourism is the largest tourism type, accounting for 64.4% of revenue in 2025, as repeat recreational travelers still drive most package demand.

Why are resort-based trips still dominant?

Resort-based Golf accounted for 52.3% of revenue in 2025, as golfers continue to prefer integrated stay-and-play packages that combine accommodation, dining, and wellness.

What is the biggest long-term challenge for golf destinations?

Environmental scrutiny is one of the biggest long-term constraints, especially around water use, land use, and compliance in arid regions.

Page last updated on: