Safari Tourism Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 41.35 Billion |

| Market Size (2031) | USD 56.16 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

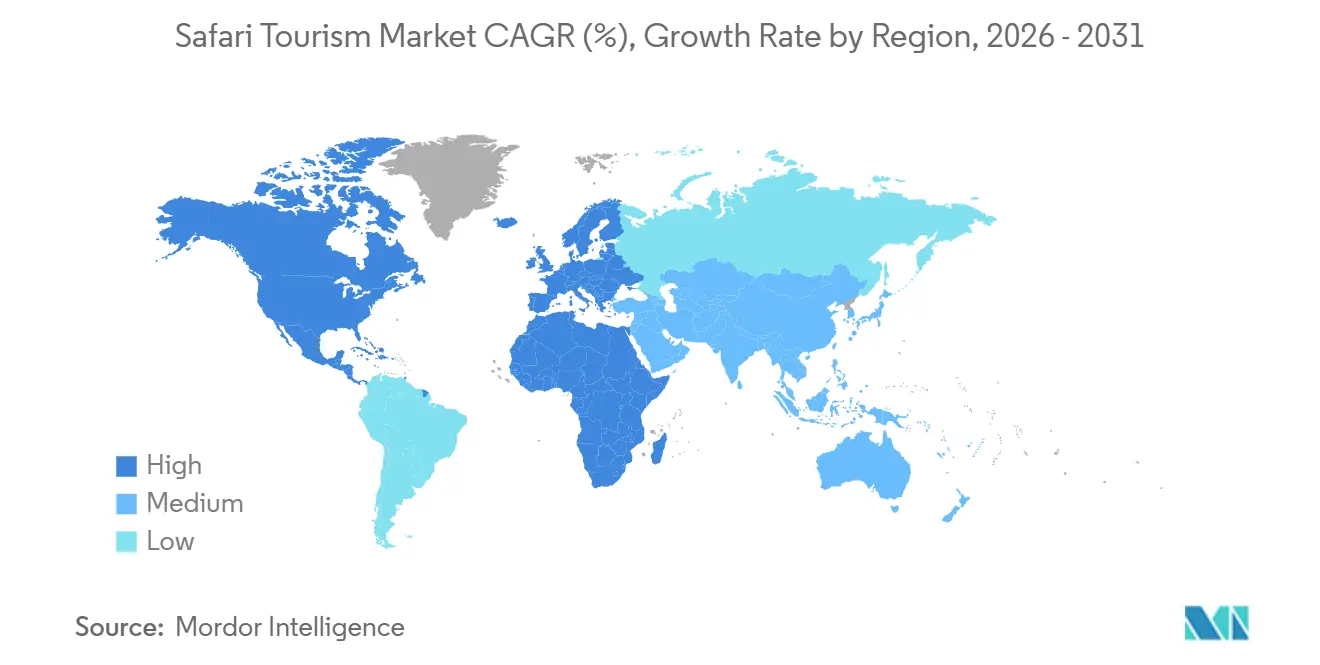

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Middle East and Africa |

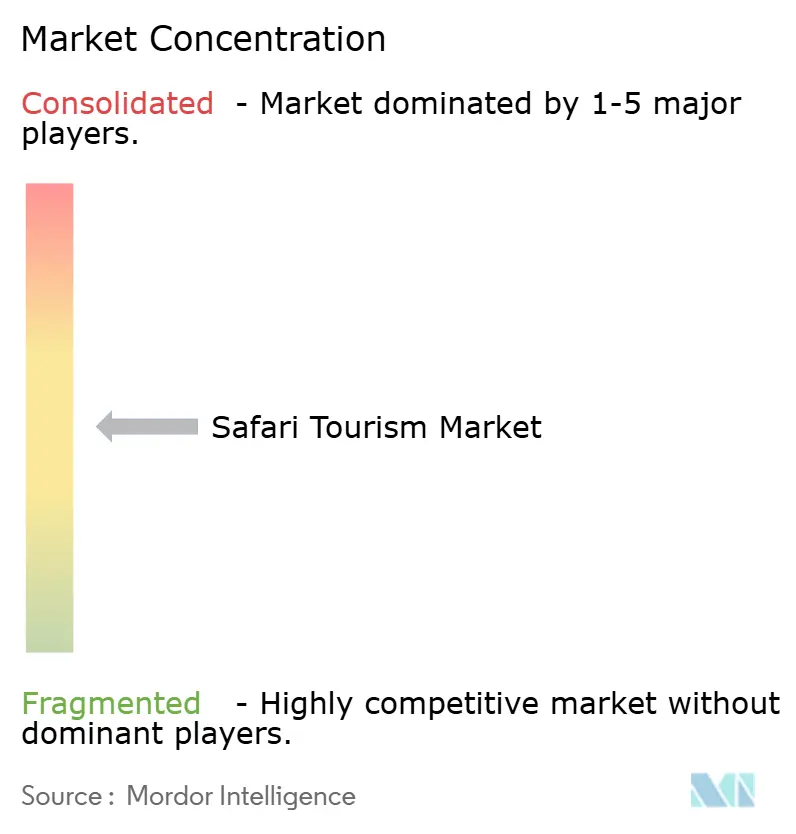

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Safari Tourism Market Analysis by Mordor Intelligence

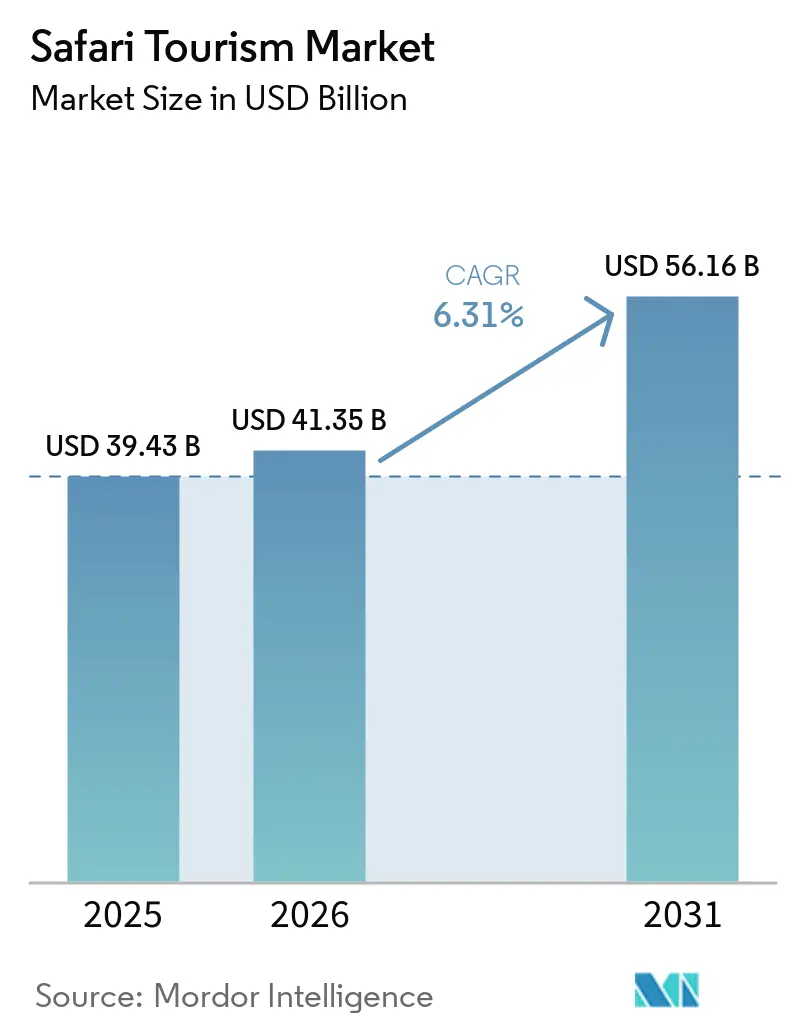

The Safari Tourism Market size is expected to increase from USD 39.43 billion in 2025 to USD 41.35 billion in 2026 and reach USD 56.16 billion by 2031, growing at a CAGR of 6.31% over 2026-2031.

Demand in the safari tourism market is no longer limited to a small set of affluent repeat travelers. It now draws a wider base from the United States, the United Kingdom, and a rising pool of Asian outbound travelers. Nature-based travel remains supported by a broad tourism base, with the wider travel and tourism economy contributing a significant share of global GDP, and protected areas receiving close to 8 billion annual visits. Average safari budgets rose notably year-on-year, which shows that travelers in the safari tourism market continued to accept higher trip values. The safari tourism market is also moving toward longer itineraries, premium accommodation, and add-on wildlife experiences that increase revenue per traveler beyond the core game-drive product. At the same time, fee revisions, climate variability, and tighter access rules in key ecosystems are making concession control, booking efficiency, and product exclusivity more important sources of competitive advantage across the safari tourism market.[1]World Bank, “Nature-Based Tourism,” World Bank, worldbank.org

Key Report Takeaways

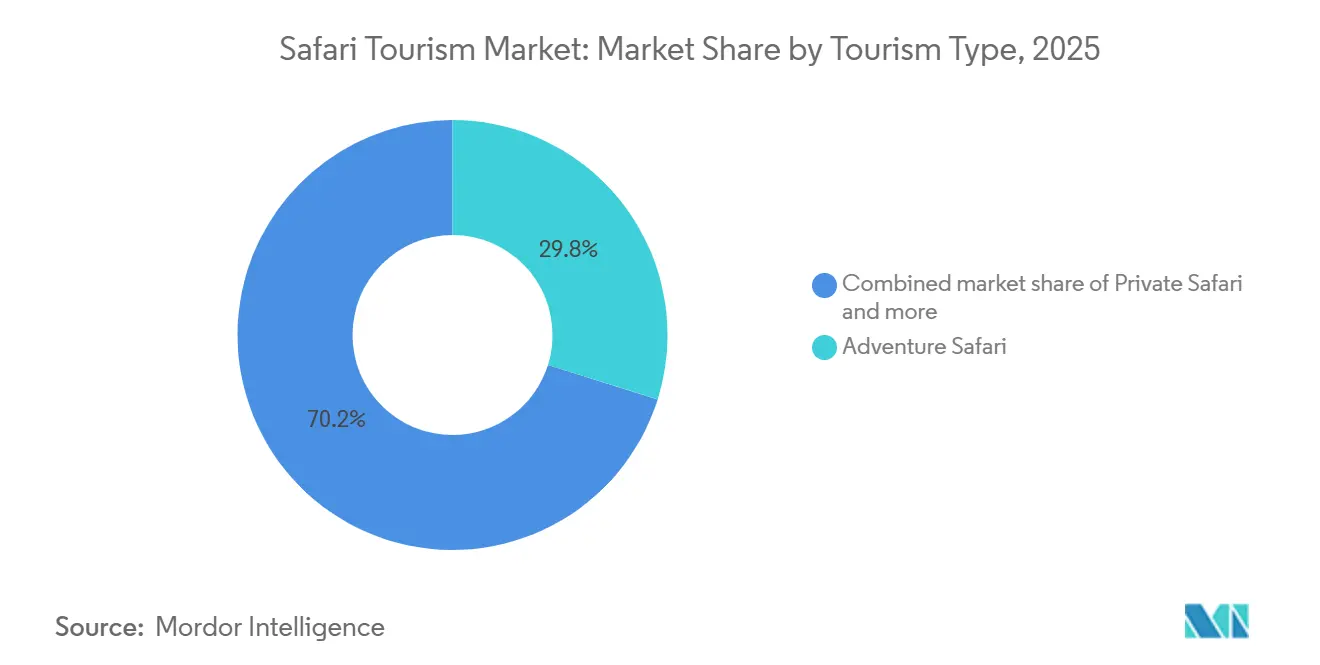

- By tourism type, Adventure Safari led with 29.84% of the safari tourism market share in 2025, while Luxury Safari is forecast to expand at a 6.72% CAGR through 2031.

- By accommodation type, Resorts and Lodges accounted for 38.63% of revenue in 2025, while Eco-lodges are projected to grow at a 7.57% CAGR through 2031.

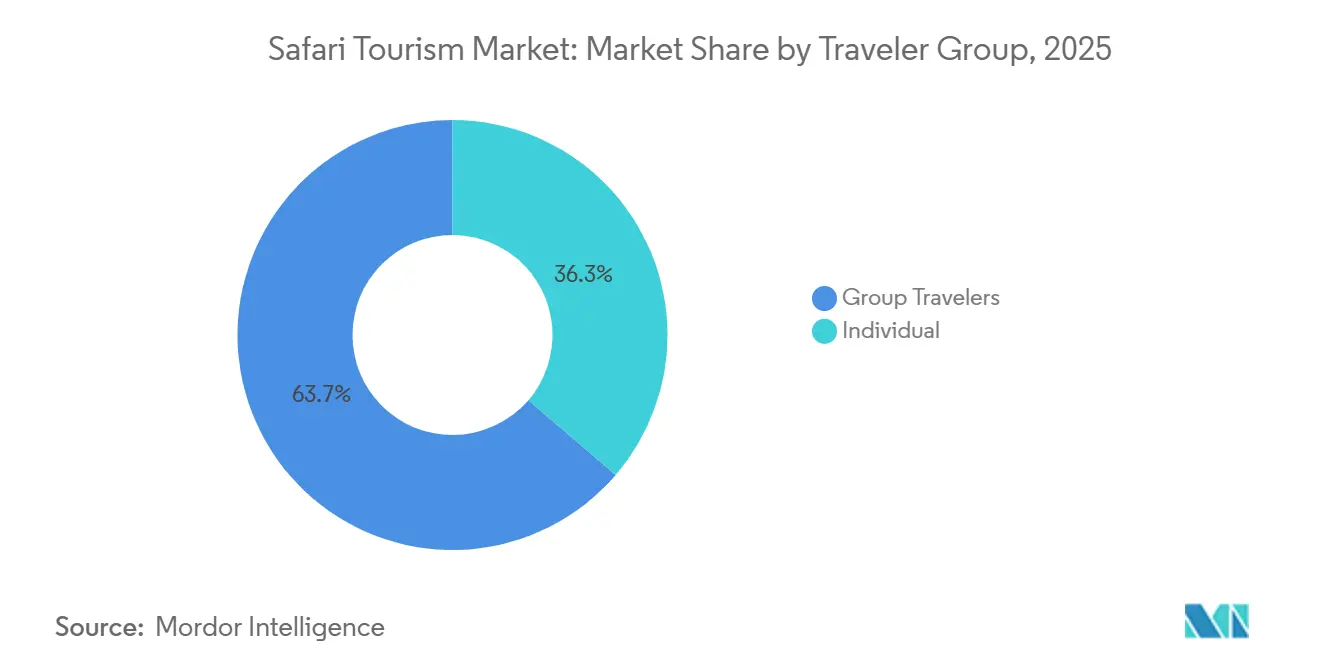

- By traveler group, Group Travelers accounted for 63.71% of revenue in 2025 and recorded the highest projected CAGR of 6.95% through 2031.

- By booking mode, Direct Booking held 42.94% of the safari tourism market share in 2025, while Online Travel Platforms are projected to grow at a 7.46% CAGR through 2031.

- By geography, the Middle East and Africa accounted for 49.85% of the safari tourism market size in 2025 and are projected to expand at a 7.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Safari Tourism Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Experiential Wildlife Travel Demand | +1.8% | Global, concentrated in MEA destinations and North American source markets | Short term (≤ 2 years) |

| Premiumization Of Private Safari Itineraries | +1.4% | East and Southern Africa, including Kenya, Tanzania, Botswana, and South Africa | Medium term (2-4 years) |

| Conservation-Led Travel Preferences | +1.0% | Global source markets and MEA destinations | Medium term (2-4 years) |

| Digital Discovery And Direct Booking Adoption | +0.8% | Global, with stronger impact in North America and emerging Asia-Pacific source markets | Short term (≤ 2 years) |

| Shoulder-Season Normalization Expands Sellable Inventory | +0.6% | East and Southern Africa, with spillover to the wider MEA region | Medium term (2-4 years) |

| Private Conservancy-Only Activities Widen Product Differentiation | +0.5% | Kenya, Botswana, Zimbabwe, and Tanzania conservation ecosystems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Experiential Wildlife Travel Demand Reshapes Itinerary Architecture

Travel demand in the safari tourism market is shifting away from passive game viewing toward more active wildlife experiences, such as walking safaris, night drives, ranger-led tracking, and conservation-linked visits. This change matters because higher-engagement formats tend to deliver stronger local economic returns than standard mass-tourism products. The World Bank reported that Bwindi Impenetrable National Park in Uganda generated economic benefits that vastly exceeded its operating budget, demonstrating how low-volume, high-value wildlife tourism can scale economic impact. Buyers are also deciding earlier in the purchase process, which means digital content now influences destination choice before many travelers contact an operator. Operators that combine wildlife viewing with cultural and conservation activities are therefore capturing a larger share of trip spending in the safari tourism market.

Premiumization of Private Safari Itineraries Drives Per-Capita Yield Outperformance

The safari tourism market continues to show a clear shift toward higher-value private itineraries even as overall inquiry growth has normalized. Average budgets rose significantly year-on-year, suggesting strong pricing acceptance at the upper end of the safari tourism market. Product formats such as private camp buyouts, private villas, and exclusive-use departures are gaining traction because they offer more control over pace, privacy, and guest experience. This trend is pushing revenue growth toward yield expansion rather than pure traveler volume. It also favors operators that control premium inventory in private concessions and can package it into longer, more personalized journeys.

Conservation-Led Travel Preferences Become a Purchasing Criterion

Travelers are increasingly treating conservation credibility as part of the booking decision in the safari tourism market rather than as a secondary brand message. Operators with traceable, measurable conservation programs are better positioned to defend pricing and reduce cancellations, especially among premium travelers. In July 2025, Gamewatchers Safaris and EarthAcre launched a traceable conservation payment model across the Ol Kinyei and Selenkay Conservancies in Kenya, using ecological metrics from Harvard's Davies Lab and targeting a scale of 35,000 acres to more than 1 million acres. The World Bank also found that conservation-based tourism creates strong local income multipliers, generating substantial local income per tourist dollar spent at destinations like Queen Elizabeth National Park and Madagascar's Nosy Be. As a result, the safari tourism market is rewarding operators that can show verified ecological outcomes, not just strong wildlife access.

Digital Discovery and Direct Booking Adoption Restructure Distribution Economics

Channel behavior in the safari tourism market is becoming more divided between high-value direct booking and faster-growing digital discovery. Direct Booking retained 42.94% of revenue in 2025 because travelers spending large sums still prefer direct relationships with specialist operators who can tailor itineraries and manage permits. At the same time, Online Travel Platforms are projected to grow at a 7.46% CAGR through 2031, indicating a younger, more digitally confident buyer base entering the safari tourism market. This creates a two-track distribution structure where digital platforms influence research and comparison, while direct operators remain stronger at conversion for more expensive trips. Operators that support both models through strong websites, live inventory visibility, and direct advisory capability are likely to capture more demand without weakening margins.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political, Health, And Safety Disruptions | -1.3% | East and Southern Africa, with spillover through travel advisory systems in North America and Europe | Short term (≤ 2 years) |

| Climate Variability Affects Wildlife-Viewing Predictability | -0.9% | East Africa, including Kenya and Tanzania, and Southern Africa, including Namibia and Botswana | Long term (≥ 4 years) |

| Flagship Sighting Overcrowding Erodes Premium Experience Value | -0.7% | Kenya, Tanzania, and Botswana | Medium term (2-4 years) |

| Permit And Conservation Fee Inflation Raises Trip Friction | -0.5% | Kenya, Uganda, and Rwanda | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Political, Health, and Safety Disruptions Introduce Systemic Demand Shocks

The safari tourism market remains exposed to political events, public health concerns, and travel advisories because many of its core destinations depend on long-haul demand. The World Tourism Cities Federation projected Africa's 2026 tourism growth with a very wide range of possible outcomes, highlighting how quickly travel outcomes can change when external risks rise. High-value safari circuits in East and Southern Africa are especially sensitive because routing, insurance, and traveler confidence all affect booking conversion. A destination does not always need to experience a direct shock for demand to weaken, since regional headlines can influence trip planning across neighboring countries. This makes geographic diversification and flexible itinerary design important operating safeguards in the safari tourism market.[2]World Tourism Cities Federation, “World Tourism Economy Trends Report 2026,” WTCF, en.wtcf.org.cn

Climate Variability Affects Wildlife-Viewing Predictability

Climate variability is becoming a long-horizon challenge for the safari tourism market because wildlife movement patterns and viewing quality depend heavily on rainfall and habitat stability. Research reported in December 2025 found that the wildebeest migration footprint in the Mara ecosystem had contracted sharply since 2020 under the combined pressure of habitat disturbance and climate-linked change. Namibia also declared a national drought emergency in 2024 following a prolonged dry period, and the country faces further warming risks that could affect the carrying capacity of desert-adapted wildlife. For operators, this reduces confidence in fixed seasonal marketing patterns that were built on more stable ecological cycles. The safari tourism market is therefore putting greater value on real-time tracking, multi-ecosystem routing, and the ability to shift guests across alternative wildlife areas.[3]Mongabay, “Climate Change Tests the Resilience of People and Desert-Adapted Wildlife in Namibia,” Mongabay, mongabay.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tourism Type: Adventure Leads Volume While Luxury Captures Margin Growth

Adventure Safari held 29.84% of the safari tourism market share in 2025, making it the largest tourism type by revenue. Its scale comes from broad accessibility across budget group departures, classic lodge circuits, and mid-market expedition formats. That breadth makes Adventure Safari the main volume engine of the safari tourism market. It also leaves the segment more exposed to pressure from overtourism in heavily trafficked parks, as many itineraries still rely on standard game-drive patterns. Luxury Safari is forecast to grow at a 6.72% CAGR through 2031, indicating that high-end demand is advancing faster than the broader safari tourism market.

Luxury growth is being supported by stronger demand for private camps, exclusive-use villas, and personalized guiding. These products command higher rates because they deliver privacy, longer stays, and greater control over guest experience. The safari tourism industry is therefore seeing revenue growth shift toward yield rather than only toward higher visitor counts. Photographic Safari, Walking Safari, and Gorilla and Primate Safari remain smaller but strategically important because they serve travelers seeking deeper engagement and are less comparable with standard game-drive products. Gorilla and primate trips in particular continue to trade on scarcity because permit availability is structurally limited and closely linked to conservation carrying capacity.

By Accommodation Type: Eco-Lodges Drive the Fastest Growth Amid Sustainability Premiums

Resorts and Lodges accounted for 38.63% of the safari tourism market in 2025, making them the largest accommodation type by revenue. Their position reflects established lodge networks, long-term operating agreements in core wildlife corridors, and the ability to serve both premium and upper mid-market demand. Eco-lodges are projected to grow at a 7.57% CAGR through 2031, making them the fastest-growing accommodation format in the safari tourism market. This reflects a clear overlap between premium pricing and visible sustainability credentials. The segment is benefiting from traveler preference for low-impact stays that still offer strong comfort and wildlife access.

In 2024, Great Plains Conservation launched Mara Toto Tree Camp in Kenya's Mara North Conservancy, demonstrating continued investment in high-value, design-led wilderness accommodation. Tented camps and bush camps also remain important because they preserve the traditional safari format and offer stronger wildlife proximity than more built-up properties. At the top end, water-based safari stays, treehouses, and other niche formats are pushing accommodation differentiation further by selling absolute scarcity and a more distinct sense of place. The safari tourism market is therefore moving toward product-led accommodation choice, where format matters almost as much as destination. The safari tourism industry is also rewarding operators that can combine environmental performance, exclusivity, and high service standards within a single asset.

By Traveler Group: Group Travel Dominates Revenue and Leads Forecast Growth

Group Travelers accounted for 63.71% of revenue in 2025 and are also projected to grow at 6.95% CAGR through 2031. This makes group travel both the largest and the fastest-growing traveler format in the safari tourism market. Organized departures benefit from pre-negotiated lodge rates, stronger occupancy planning, and lower distribution cost per traveler. These structural advantages help operators maintain accessible pricing while still participating in premiumization. The segment also includes higher-value formats such as multi-generational family departures and exclusive group buyouts, which means growth is not limited to budget-oriented products.

Individual Travelers represented 36.29% of revenue in 2025 and continue to skew toward higher spend per night because their itineraries are more customized. This cohort is important in the safari tourism market because it often drives demand for niche experiences such as walking safaris and primate-focused trips. Individual travel also requires more complex logistics, from vehicle planning to permit management and personalized pre-departure service. Operators serving both group and individual demand must segment inventory carefully so that shared departures do not weaken exclusivity at the high end. The safari tourism industry therefore favors platforms and operators that can balance scale with customization across different traveler formats.

By Booking Mode: Direct Channels Retain Share While Platforms Accelerate

Direct Booking accounted for 42.94% of revenue in 2025, making it the largest channel in the safari tourism market. This channel remains strong because safari trips usually involve high values, permit coordination, and the need for detailed pre-trip support. Travelers spending USD 8,000 or more per person often prefer direct contact with a specialist who can tailor routing, lodging, and wildlife priorities. Online Travel Platforms are projected to grow at a 7.46% CAGR through 2031, indicating that digital comparison and self-directed research are expanding rapidly in the safari tourism market. The result is a distribution model where trust-heavy itineraries still close directly, even when discovery starts online.

This pattern is especially relevant for younger travelers and first-time safari buyers who want transparent pricing and an easy way to compare itineraries before speaking with a consultant. Marketplace models and regional booking platforms remain smaller, but they are widening the reach of digital discovery and supplier access. Operators with real-time availability, clearer package logic, and strong advisory follow-up are likely to convert better across both direct and platform-led demand. The safari tourism market is therefore not moving away from direct sales, but it is becoming more digitally shaped at the research stage. This gives an advantage to operators that combine specialist human advisory capability with stronger technology support.

Geography Analysis

Middle East and Africa retained 49.85% of the safari tourism market share in 2025 and is projected to grow at a 7.02% CAGR through 2031. This dual lead reflects the region's position as the core supply base of the safari tourism market, supported by wildlife estates, bush aviation links, private conservancies, and lodge development pipelines. South Africa, Kenya, and Tanzania continue to anchor the regional structure because they combine established tourism ecosystems with broad product depth across price points. Botswana is also strengthening its position through ultra-premium and low-density wilderness products, with Singita's planned Elela opening reinforcing the long-term appeal of controlled concession access. Rwanda and Uganda remain distinct high-value, low-volume destinations within the safari tourism market because gorilla trekking operates on scarcity, permit controls, and premium pricing rather than on high visitor throughput.

North America and Europe remain the main source-market engine for global safari revenue. The United States continues to be the most important high-spend source market, while the United Kingdom remains a major contributor to European demand in the safari tourism market. These two regions matter because they support both luxury custom itineraries and organized group formats. Premium safari demand from these markets also shows lower resistance to higher nightly rates and more willingness to purchase itinerary extensions such as beach stays or primate trekking. That spending pattern reinforces the importance of direct relationships, trusted specialist brands, and high-service booking support across the safari tourism market.

Asia-Pacific is the fastest-developing source region in proportional terms within the safari tourism market. Growth from this region is being supported by rising outbound travel, stronger digital trip discovery, and a growing preference for experiential long-haul travel. The World Tourism Cities Federation expects Asia-Pacific tourism growth to remain positive across a broad range of 2026 scenarios, supporting the region's long-term conversion potential. For operators, this means source diversification is expanding beyond traditional Western markets, even though conversion to safari travel remains more mature in North America and Europe. The safari tourism market is therefore expanding geographically on the demand side while remaining structurally concentrated in Africa on the supply side.

Competitive Landscape

The safari tourism market is moderately consolidated at the ultra-premium end and fragmented across the broader mid-market and value tiers. A small cluster of luxury operators holds clear pricing power because it controls long-term concession access, lodge infrastructure, and curated wildlife experiences that are difficult to replicate. That advantage is strongest in remote, low-density ecosystems, where product quality depends on exclusive land rights rather than on brand alone. The wider field, however, remains crowded with regional specialists competing on guide quality, destination mix, and pricing flexibility. This keeps the safari tourism market competitive even though the highest-end supply is clearly more protected.

Capital deployment continues to shape the safari tourism market, as premium expansion requires access to land, permits, design capabilities, and conservation partnerships. Lindblad Expeditions increased its investment position in Natural Habitat Adventures, showing that strategic investors still see conservation-led wildlife travel as a scalable premium category. In 2024, Singita launched Singita Milele in Tanzania's Grumeti concession, reinforcing the role of exclusive-use villa products in capturing multigenerational and private-group demand. These moves show that premium positioning in the safari tourism market still depends on controlled inventory and long-duration asset commitments.

Competitive differentiation is also widening beyond land access alone. Operators are now competing on conservation credibility, itinerary depth, and the ability to match guests with more specialized wildlife products. In July 2025, Gamewatchers Safaris and EarthAcre introduced a model that links safari revenue directly to traceable conservation payments, which reflects how ecological accountability is becoming part of brand positioning. In July 2024, Volcanoes Safaris opened Kibale Lodge in Uganda, extending primate-focused product depth in a corridor already known for high-value gorilla and chimpanzee travel. The safari tourism market is therefore becoming more differentiated through a mix of concession control, conservation proof, and highly specific product design.

Safari Tourism Industry Leaders

Abercrombie & Kent

&Beyond

Wilderness

Singita

Micato Safaris

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Singita, a luxury ecotourism and conservation company, detailed the launch of its very first property in Botswana, Singita Elela. Slated for a December 2026 opening, the year-round, family-friendly luxury camp represents a major geographic expansion for the brand, situated on a massive 170,000-hectare private concession in the Okavango Delta.

- May 2026: Abercrombie & Kent unveiled its 2026 portfolio expansions, highlighted by the upcoming launch of Kitirua Plains Lodge. Set to open in 2026, this new A&K Sanctuary retreat features 13 organic suites located within a private 128-acre concession in Kenya's Amboseli National Park, expanding their premium footprint in East Africa.

- September 2025: Aman announced its highly anticipated debut into the African safari tourism market. The brand revealed plans to open Aman Karingani in Mozambique's Karingani Game Reserve (bordering Kruger National Park). The project will integrate Aman's signature luxury wellness pavilions and branded residences directly into the wildlife landscape.

- August 2025: Abercrombie & Kent (A&K) partnered with sister brand Crystal Cruises to launch a new chapter of expedition and cultural voyages. The collaboration merges A&K’s 60 years of remote expedition and safari-guiding expertise with Crystal’s luxury fleet, aiming to attract high-end travelers seeking land-and-sea exploration packages.

Global Safari Tourism Market Report Scope

| Adventure Safari |

| Private Safari |

| Luxury Safari |

| Photographic Safari |

| Walking Safari |

| Gorilla and Primate Safari |

| Safari Resorts and Lodges |

| Tented Camps and Bush Camps |

| Eco-lodges |

| Others (Houseboats, Water-Based Safari Stays, Treehouses, etc.) |

| Group |

| Individual |

| Direct Booking |

| Online Travel Platforms |

| Others (Marketplace Booking and others) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Tourism Type | Adventure Safari | |

| Private Safari | ||

| Luxury Safari | ||

| Photographic Safari | ||

| Walking Safari | ||

| Gorilla and Primate Safari | ||

| By Accommodation Type | Safari Resorts and Lodges | |

| Tented Camps and Bush Camps | ||

| Eco-lodges | ||

| Others (Houseboats, Water-Based Safari Stays, Treehouses, etc.) | ||

| By Traveler Group | Group | |

| Individual | ||

| By Booking Mode | Direct Booking | |

| Online Travel Platforms | ||

| Others (Marketplace Booking and others) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in safari tourism through 2031?

Growth is being supported by rising trip values, wider source-market demand, premium itinerary design, and stronger interest in conservation-linked experiences. The sector is forecast to grow at a 6.31% CAGR through 2031.

Which tourism type leads revenue in safari travel?

Adventure Safari led with 29.84% revenue share in 2025, while Luxury Safari is expanding faster at a 6.72% CAGR through 2031.

Which accommodation format is growing the fastest?

Eco-lodges are the fastest-growing accommodation format, with a projected 7.57% CAGR through 2031, reflecting stronger traveler preference for sustainability-linked stays.

Why does direct booking still matter in safari travel?

Direct Booking held 42.94% of revenue in 2025 because travelers often want specialist support for permits, routing, lodge selection, and in-destination coordination.

Which region leads safari demand and supply?

Middle East and Africa held 49.85% of revenue in 2025 and is also the fastest-growing regional segment with a 7.02% CAGR through 2031.

What are the main risks affecting future performance?

The main risks are political and health disruptions, climate-driven changes in wildlife visibility, overcrowding in flagship sighting areas, and rising permit and conservation fees.

Page last updated on: