Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

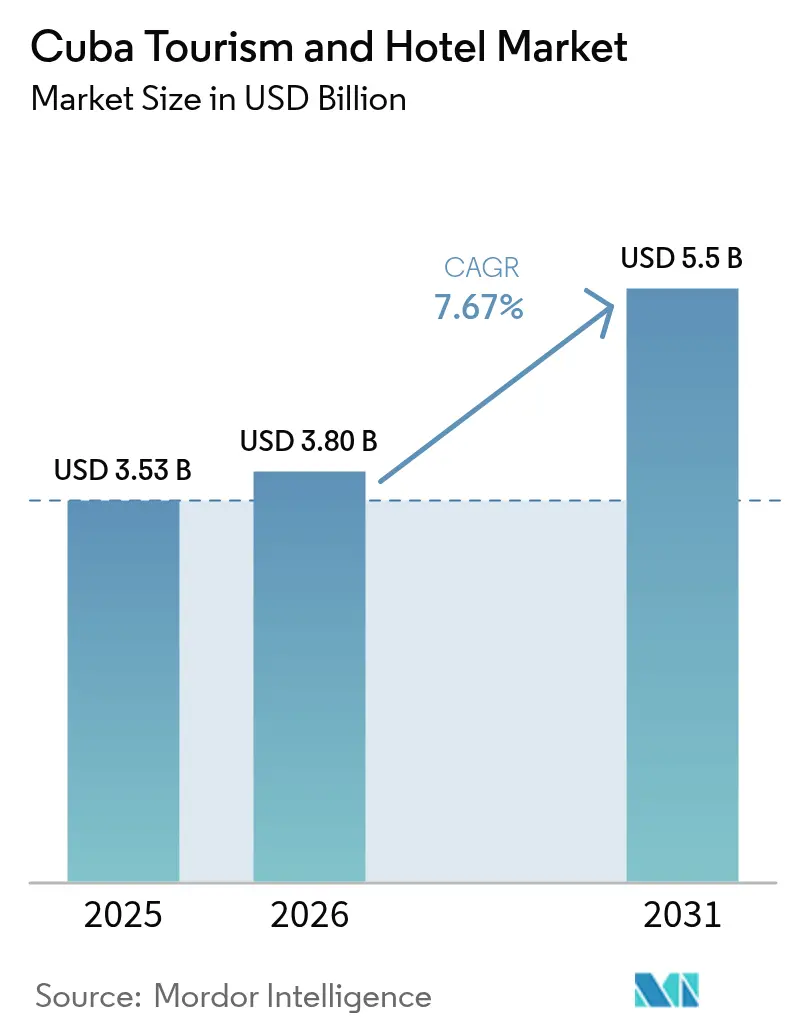

| Base Year Market Size (2025) | USD 3.53 Billion |

| Market Size (2026) | USD 3.80 Billion |

| Market Size (2031) | USD 5.5 Billion |

| Growth Rate (2026 - 2031) | 7.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cuba Tourism And Hotel Market Analysis by Mordor Intelligence

The Cuba tourism and hotel market size is expected to grow from USD 3.53 billion in 2025 to USD 3.8 billion in 2026 and is forecast to reach USD 5.5 billion by 2031 at 7.67% CAGR over 2026-2031. Visitor spending growth banks on premium positioning, Chinese outbound demand and recovering cruise traffic, yet rolling power cuts and chronic under-investment in basic utilities weaken service reliability. Operators therefore chase higher-yield Chinese and Russian travelers who typically spend up to 40% more per trip than mainstream Western guests. Online Travel Agencies (OTAs) scale quickly but face litigation risk under the United States embargo, forcing many hotels to juggle offline blocks with emerging direct-online tools. Environmental stress compounds operational complexity as sea-level rise of 6.77 cm since 1966 erodes beaches central to Cuba’s sun-and-sand appeal, prompting a USD 23.9 million mangrove-restoration program under the UN-backed MI COSTA project.

Key Report Takeaways

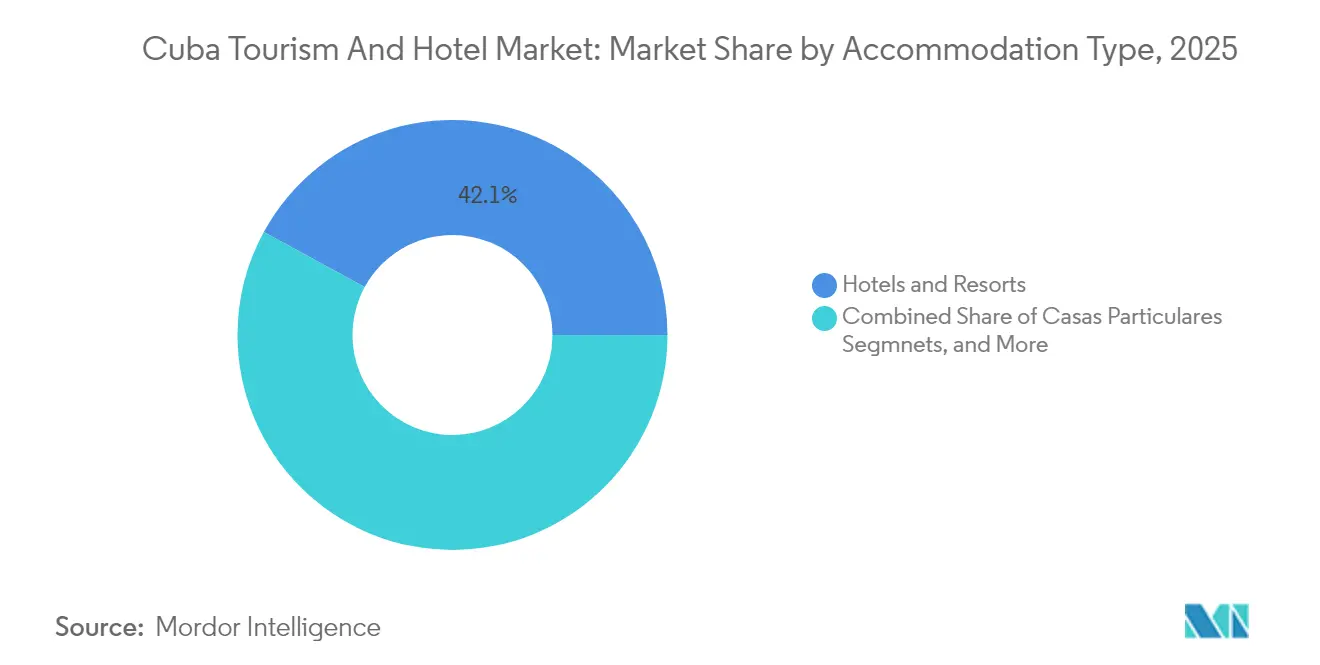

- By accommodation type, hotels and resorts led with 42.05% of the Cuba tourism and hotel market share in 2025, while boutique & lifestyle hotels are advancing at a 9.08% CAGR to 2031.

- By booking channel, direct offline captured 53.98% of the Cuba tourism and hotel market share in 2025, whereas OTAs posted the strongest 9.88% CAGR through 2031.

- By tourist type, domestic travelers accounted for 65.60% of the Cuba tourism and hotel market size in 2025, whereas international arrivals are projected to grow at 10.12% CAGR through 2031.

- By star rating, Mid-scale 3-star hotels controlled 40.85% of the Cuban tourism and hotel market share in 2025, yet luxury 5-star properties are forecast to expand at 9.97% CAGR through 2031 in the Cuban tourism and hotel market.

- By province, Western Cuba held 68.30% of of the Cuba tourism and hotel market size in 2025, while Eastern Cuba recorded the fastest 9.46% CAGR on the back of new investment pipelines.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Cuba Tourism And Hotel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cruise tourism expansion | +1.2% | Western Cuba, Central Cuba ports | Medium term (2-4 years) |

| Demand for authentic and immersive travel | +0.9% | Global, with concentration in Western and Central Cuba | Long term (≥ 4 years) |

| Diversification of tourism products | +0.8% | National, with early gains in Eastern Cuba provinces | Medium term (2-4 years) |

| Government support and strategic investments | +1.1% | National, prioritizing Western and East Central Cuba | Short term (≤ 2 years) |

| Growing international hotel partnerships | +0.7% | Global, focused on Western Cuba luxury segment | Medium term (2-4 years) |

| Increasing foreign investment | +0.6% | National, concentrated in Western Cuba | Long term (≥ 4 years) |

| Rise of private and boutique accommodations | +0.5% | Western Cuba, expanding to Central regions | Medium term (2-4 years) |

| Unique cultural and natural appeal | +0.4% | Global appeal, strongest in Western and Central Cuba | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cruise Tourism Expansion

The Cuban National Port Authority's commitment to enhanced docking facilities addresses a critical bottleneck that previously limited vessel size and passenger capacity. Major Caribbean cruise operators maintain contingency plans for Cuban market re-entry, recognizing the island's unique positioning as an authentic cultural destination unavailable elsewhere in the region. Berth lengthening allows larger vessels, and dual-gateway routing splits risk between west and east coasts, shortening transfer times to leading resort clusters. Caribbean cruise majors keep Cuba itineraries in contingency brochures, citing the island’s rarity value as a culturally authentic port call. Shore-to-hotel conversion strategies encourage passengers to prolong stays, boosting room-night sales across both state-run resorts and casa particulares. As port charges represent incremental state revenue, the driver adds steady foreign-exchange inflows that support broader infrastructure upgrades.

Demand for Authentic and Immersive Travel

Global travelers prefer heritage districts, live music and community-hosted dining over standardized resort compounds, elevating Havana Vieja, Trinidad and Santiago’s colonial centers in bucket-list rankings[1]Source: Editorial Staff, “Heritage Districts Attract Post-Covid Travelers,” Ministry of Foreign Affairs, minrex.gob.cu.. Iberostar Grand Packard’s global Top-5 vote in 2024 showcases service excellence achievable when utilities are stable. Independent casas particulares multiply in these cities, offering curated local engagement and channeling revenue to families who reinvest in property upkeep. Heritage prestige also lets operators price rooms at a double-digit premium to region-wide average daily rates. Authenticity demand thus aligns with policy aims to distribute income beyond beach corridors while incentivizing cultural conservation.

Diversification of Tourism Products

Vintage-car convoys, cigar-estate circuits and medical-wellness retreats add depth to the Cuba tourism and hotel market’s portfolio, helping carve space in an overcrowded Caribbean resort scene. Government targets of 10 million visitors by 2030 necessitate new demand pockets, and eastern provinces pilot eco-lodges that tap dense forests and bird-watching routes. Adventure segments show higher spend per guest than sun-seekers and occupy off-peak travel months, smoothing seasonality. Medical tourism leverages Cuba’s biotech strengths, with pilot cardiology and oncology packages already attracting Latin American patients. Each niche spreads load away from Varadero, lifts average length of stay and widens foreign-currency capture.

Government Support and Strategic Investments

Nearly 12% of Cuba’s 2024 state budget funded hospitality works, an unprecedented share that fast-tracks road links, bulk desalination, and Havana’s skyline additions like Torre K-23. The Foreign Investment Act eases joint-venture approvals, while the Mariel Special Development Zone grants decade-long tax holidays to tourism projects. The China-Cuba tourism corridor brings visa-free entry and thrice-weekly Beijing-Havana flights, exposing the island to a growing affluent segment that typically spends 40% more per trip than the global average. These state actions underpin premium-oriented development, but success hinges on parallel fixes to energy and digital payment bottlenecks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic power outages inflating operating costs | -2.1% | National, most severe in Eastern and Central Cuba | Short term (≤ 2 years) |

| Hospitality talent exodus eroding service quality | -1.3% | National, concentrated impact in Western Cuba | Medium term (2-4 years) |

| Rising cyber-payment fraud deterring OTAs | -0.8% | Global impact on online booking channels | Short term (≤ 2 years) |

| Sea-water intrusion accelerating beach erosion | -0.6% | Coastal regions, particularly Western and Central Cuba | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Power Outages Inflating Operating Costs

Hotels now budget up to 40% more for electricity by running diesel gensets during daily blackouts that sometimes stretch 20 hours. Fuel drains as much as 15% of operating expenditure, narrowing margins for both budget and upscale properties. Guests cite cancelled lifts, AC failures and cold showers in online reviews, tarnishing Cuba’s premium aspirations just as competitors like Dominican Republic deliver uninterrupted comfort. Energy volatility also deters international chains from expanding beyond Havana, dampening room-supply diversification.

Hospitality Talent Exodus Eroding Service Quality

An estimated 10% of Cuba’s population emigrated since 2020, siphoning multilingual front-office staff, chefs, and spa therapists to higher-paying Caribbean rivals. Hotels confront a wage spiral to retain remaining staff, yet still suffer service lapses that erode guest satisfaction scores. Training new recruits prolongs ramp-up cycles for planned openings, while language gaps hinder personalization strategies critical for luxury positioning. The exodus, therefore, drags brand reputation and could delay ROI timelines on capital-intensive projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Accommodation Type: Military Dominance Meets Boutique Innovation

Hotels and Resorts secured 42.05% of 2025 revenue within the Cuba tourism and hotel market, anchored by Gaviota-managed beach compounds in Varadero and Cayo Coco. Boutique & Lifestyle Hotels outpace at 9.08% CAGR thanks to global accolades such as Mystique Trinidad La Popa entering the world’s Top 20 rankings. All-inclusive resorts confront margin squeeze from generator fuel and imported food costs, while casas particulares thrive via Airbnb’s 1,000-plus Havana listings that attract authenticity-seeking travelers. Eco-lodges sprout in eastern biosphere reserves, boosted by MI COSTA grants that restore 11,427 ha of mangroves to protect coastal trails .

The dual structure means state-run luxury towers like Torre K-23 open doors even as private family homes capture word-of-mouth traffic. International brands bring systems expertise, but persistent outages test promise-to-delivery gaps, dampening repeat visitation. Boutique operators, meanwhile, sidestep large-scale utility needs, adopting solar micro-grids and localized supply chains. This adaptability positions them to expand share as authenticity and sustainability climb purchase criteria

By Booking Channel: Digital Disruption Meets Legal Complexity

Direct Offline avenues retained 53.98% share in 2025, reflecting legacy travel-agent allotments and state-mediated blocks that secure hard currency at set exchange rates. Yet OTAs log a 9.88% CAGR as Cuban hotels court millennials who book on mobile. U.S. embargo lawsuits—such as the USD 30 million judgment against Expedia—force periodic de-listings, pushing some hotels to proprietary booking engines hosted offshore.

Internet latency and patchy card gateways frustrate real-time confirmations, but 4G rollout across tourist corridors and adoption of Chinese UnionPay lower friction. As the Cuba tourism and hotel market size tied to OTAs rises, operators gain rate transparency yet sacrifice commission fees. Hybrid strategies emerge: direct-online offers add amenities while offline agents bundle charter flights to circumvent digital gaps.

By Tourist Type: Domestic Resilience Anchors International Recovery

Cuban nationals filled 65.60% of beds in 2025, cushioning foreign-visitor drop-offs and ensuring baseline cashflow for provincial hotels. Subsidized holiday vouchers underwrite local stays, and the CUP’s relative strength in local services keeps leisure trips affordable. International arrivals, projected to grow 10.12% CAGR to 2031, hinge on restored airlift from Canada and Europe plus new Beijing frequencies.

Canadian volume fell 31.8% in 2025, yet Russia climbed, aided by state-chartered flights bypassing EU airspace. Chinese visitors, spending 40% above regional norm, promise high yield if language services and e-wallet acceptance improve. Balancing peso-priced domestic rates with USD-denominated international tariffs challenges revenue managers but diversifies risk.

By Star Rating: Premium Positioning Amid Infrastructure Constraints

Mid-scale 3-Star hotels delivered 40.85% of 2025 turnover, serving mass domestic demand and budget foreigners. Luxury 5-Star stock, while under 15% of keys, grows at 9.97% CAGR through 2031 as state planners eye affluent segments tolerant of higher nightly rates. The Gran Hotel Manzana Kempinski blazed the trail, yet service disruptions expose reputation risk if utility fixes lag.

Budget 1-2 Star pensiónes face cost-line pressure because fuel and food inflation compress already slim margins. Upscale 4-Star resorts tread a middle ground but risk being squeezed if they cannot justify price gaps versus 3-Star, while lacking luxury cachet. Investment, therefore, clusters at both ends: flagship high-rise towers and simple rural casas with low overheads.

Geography Analysis

Western Cuba contributed 68.30% of 2025 hotel revenue, bolstered by Havana’s UNESCO-listed core, the Malecón revitalization and Varadero’s charter-linked airport that handled 2.5 million passengers last year. Luxury cranes dot the skyline—Torre K-23 and Selection La Habana alone represent more than USD 200 million in bricks and fittings—affirming faith in premium city-stay potential even amid power rationing. The region’s beaches, however, recede up to 1 m annually, prompting the MI COSTA mangrove belt to safeguard 11,427 ha of coastline.

Eastern Cuba accelerates at 9.46% CAGR through 2031 by activating under-served Santiago, Holguín and Baracoa circuits. Santiago de Cuba leverages Afro-Cuban rhythms, carnival calendar and historical fortresses to woo culture fans, while Holguín opens new all-inclusive keys with lower land costs than Varadero. A Barranquilla-to-Santiago direct flight launching July 2025 slashes Latin American transit times by four hours. Yet grid fragility and limited international gateways restrict rapid scale-up, requiring phased investment in solar farms and runway lengthening.

Central Cuba sits between the two poles, drawing architectural tourists to Trinidad’s cobblestone streets and Cienfuegos’ French layout. Boutique conversions of 18th-century mansions support higher average daily rates without mega-capex, ideal for investors wary of infrastructure risk. Road upgrades linking to the east-west Autopista Nacional now cut Havana-to-Trinidad drive time to under four hours, encouraging two-center itineraries. Hurricane exposure mandates resilient design; hence new builds in the province elevate electrical systems and water tanks above predicted surge levels.

Competitive Landscape

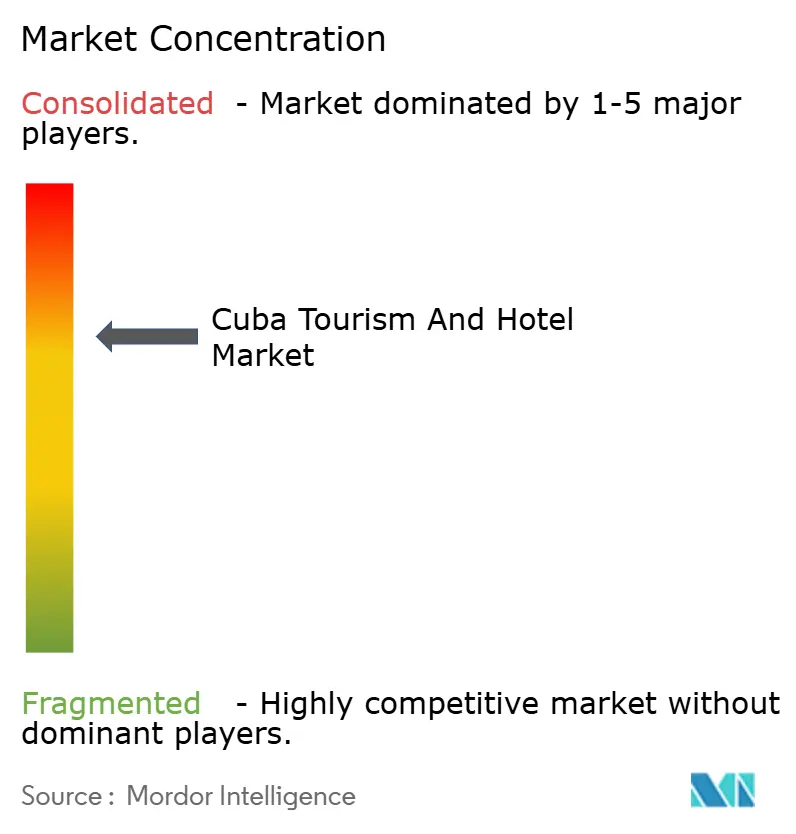

Five groups—Gaviota, Meliá, Iberostar, Blue Diamond, and Cubanacan—command most premium inventory, giving the Cuba tourism and hotel market a high-concentration profile. Gaviota alone controls more than 50 properties and holds USD 4.3 billion in cash reserves, reflecting the military conglomerate’s dominance. Foreign chains operate via management contracts or minority joint ventures because land remains state-owned.

Strategic thrusts emphasize luxury towers to offset volume dips, evidenced by Gaviota’s Playa Luxury Cayo Guillermo, a USD 50 million five-star unveiled in February 2025. Meliá deepens Chinese guest outreach through Mandarin-speaking concierges, while Iberostar exploits heritage refurb niches like Grand Packard to capture culturally inclined upsellers. Blue Diamond pushes price-sensitive Canadian charters, though current arrival declines prompta pivot toward higher-margin European markets [3]Source: Corporate Release, “Blue Diamond Resorts Continues Cuba Growth Strategy,” Blue Diamond Resorts, bluediamondresorts.com. .

White-space opportunities lie in eco-tourism lodges needing lighter infrastructure and medical-wellness retreats underpinned by Cuba’s biotech portfolio. Technology adoption remains patchy; reliable Wi-Fi and e-payments will be differentiation levers for new entrants. Joint-venture partners able to navigate licensing layers and hedge fuel risk stand to secure first-mover advantage in under-developed eastern micro-markets.

Cuba Tourism And Hotel Industry Leaders

Gaviota S.A. (GAESA)

Meliá Hotels International

Iberostar Hotels & Resorts

Blue Diamond Resorts

Cubanacan Hoteles

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Archipelago International confirmed Aston Panorama Havana will open within 12 months, bringing its Cuban footprint to six hotels.

- February 2025: Gaviota Tourist Group opened Playa Luxury Cayo Guillermo, a USD 50 million 5-star resort with 24/7 butler service and private pools.

- January 2025: Marriott International signed 67 Caribbean & Latin America deals in 2024; Cuba remains off-limits, yet the group monitors reform momentum for future entry.

Cuba Tourism And Hotel Market Report Scope

A complete background analysis of the market, including the analysis of market size and forecast, market shares, industry trends, growth drivers, and vendors, is provided. Additionally, the report features qualitative and quantitative assessments by analyzing the data gathered from industry analysts and market participants across key points in the industry's value chain. The Market is Segmented by tourism and hotel. By Tourism, the market is segmented into Domestic Tourism and International Tourism. By Hotel, the market is segmented into Budget and Economy Hotels, Mid and Upper Mid-scale Hotels, Luxury Hotels, and Others (Homestays, Hostels, etc.)). The report offers the market sizes and forecasts in value for the above segments.

By Accommodation Type

| Hotels and Resorts |

| Casas Particulares |

| All-Inclusive Resorts |

| Boutique and Lifestyle Hotels |

| Eco-lodges and Nature Resorts |

By Booking Channel

| Direct Offline |

| Direct Online |

| Online Travel Agencies (OTAs) |

| Tour Operators / Wholesalers |

By Tourist Type

| Domestic |

| International |

By Star Rating

| Luxury (5-Star) |

| Upscale (4-Star) |

| Mid-scale (3-Star) |

| Budget (1-2-Star) |

By Province / Destination

| Western Cuba |

| West Central Cuba |

| Central Cuba |

| East Central Cuba |

| Eastern Cuba |

| By Accommodation Type | Hotels and Resorts |

| Casas Particulares | |

| All-Inclusive Resorts | |

| Boutique and Lifestyle Hotels | |

| Eco-lodges and Nature Resorts | |

| By Booking Channel | Direct Offline |

| Direct Online | |

| Online Travel Agencies (OTAs) | |

| Tour Operators / Wholesalers | |

| By Tourist Type | Domestic |

| International | |

| By Star Rating | Luxury (5-Star) |

| Upscale (4-Star) | |

| Mid-scale (3-Star) | |

| Budget (1-2-Star) | |

| By Province / Destination | Western Cuba |

| West Central Cuba | |

| Central Cuba | |

| East Central Cuba | |

| Eastern Cuba |

Key Questions Answered in the Report

What is the current value of the Cuba tourism and hotel market?

The market is valued at USD 3.8 billion in 2026 and is projected to reach USD 5.5 billion by 2031.

How fast is the sector growing?

Forecast CAGR stands at 7.67% for 2026-2031, driven by premium room expansion, Chinese demand and cruise recovery initiatives.

Which accommodation segment is expanding quickest?

Boutique and lifestyle hotels lead with a 9.08% CAGR to 2031 thanks to authenticity-seeking travelers and global rankings that boost visibility.

Why are power outages a major concern for operators?

Blackouts lasting up to 20 hours force hotels to run diesel generators, inflating operating costs by as much as 40% and hurting guest satisfaction.

Which region shows the highest growth potential?

Eastern Cuba records a 9.46% CAGR through 2031 as Santiago and Holguín receive targeted investment in culture-oriented and eco-beach projects.

How concentrated is market ownership?

Five groups control most premium keys, giving the sector a concentration score of 7/10, though niche eco-lodges and casas particulares offer growing competitive alternatives.

Page last updated on: