Kefir Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.99 Billion |

| Market Size (2031) | USD 3.01 Billion |

| Growth Rate (2026 - 2031) | 8.63% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kefir Market Analysis by Mordor Intelligence

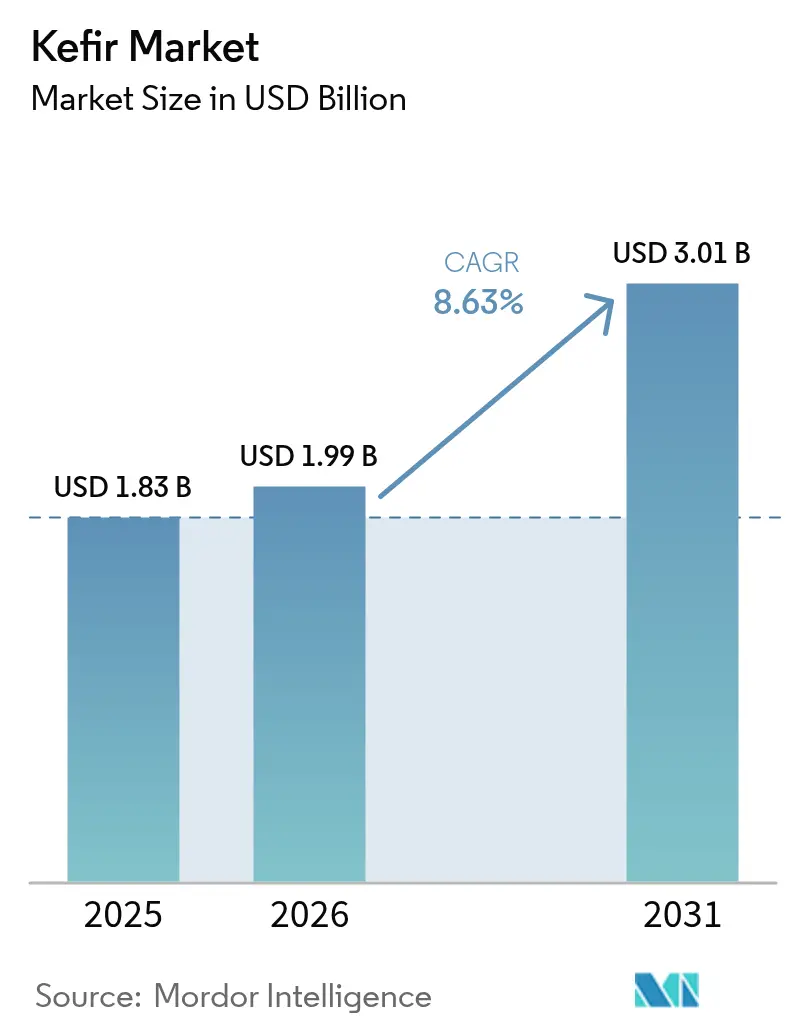

The kefir market size was valued at USD 1.83 billion in 2025 and estimated to grow from USD 1.99 billion in 2026 to reach USD 3.01 billion by 2031, at a CAGR of 8.63% during the forecast period (2026-2031). Rising clinical evidence supporting kefir’s superior gut-health benefits over many commercial probiotic supplements continues to shift consumer preference toward naturally fermented products, while the United States Food and Drug Administration’s 2024 qualified health-claim decision for yogurt has created a halo effect across the wider fermented dairy aisle, including kefir[1]Source: United States Food & Drug Administration, “Qualified Health Claim for Yogurt and Reduced Risk of Type 2 Diabetes,” fda.gov. Europe retains the highest regional demand, supported by long-standing consumption habits and a favorable regulatory climate, whereas Asia-Pacific is expanding fastest on the back of rapid urbanization and increasing awareness of digestive wellness. Conventional formulations dominate volume sales, yet premium organic, flavored, and plant-based variants capture consumers seeking clean-label, low-sugar, and lactose-free options, driving above-average growth in these sub-segments. Within distribution, supermarkets remain pivotal, but cafés and wellness-focused food service outlets are redefining trial exposure and brand storytelling through experiential formats.

Key Report Takeaways

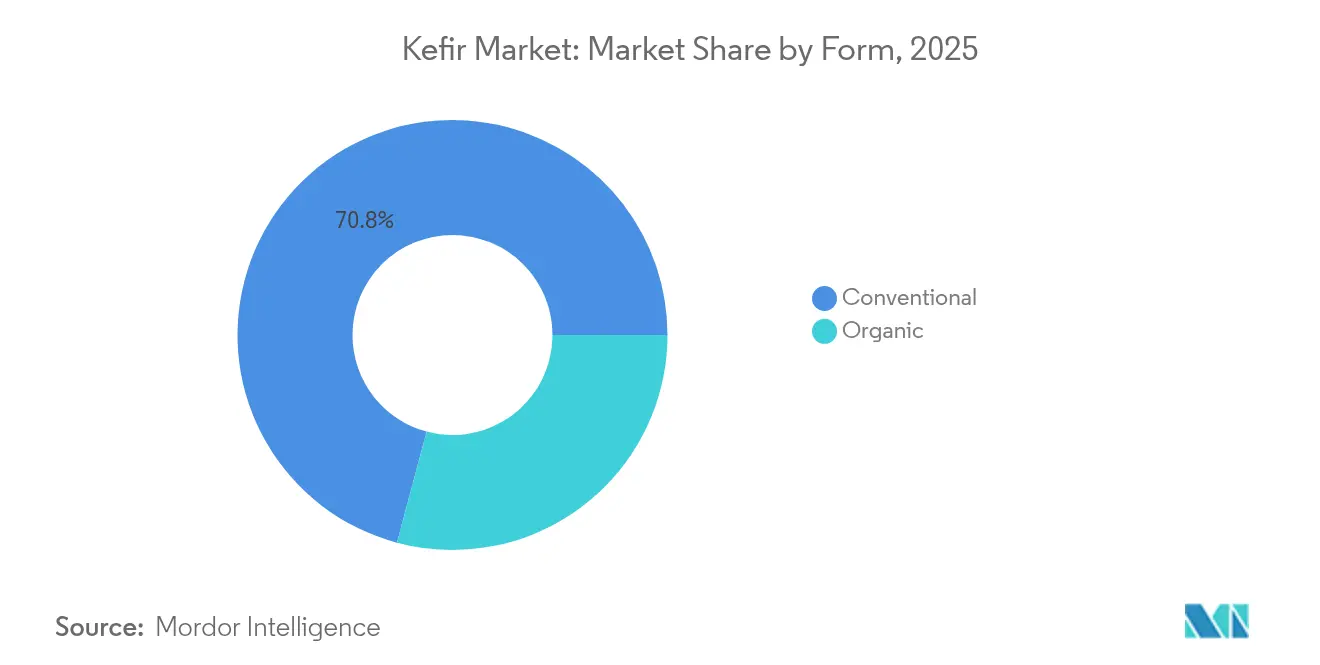

- By form, conventional products held 70.84% of the kefir market share in 2025, while organic variants are projected to climb at a 10.54% CAGR through 2031.

- By flavor, flavored offerings led with 63.45% revenue share in 2025; non-flavored kefir is forecast to expand at a 9.69% CAGR.

- By product type, milk kefir captured 79.72% of the kefir market size in 2025; water kefir is poised for the fastest 10.18% CAGR.

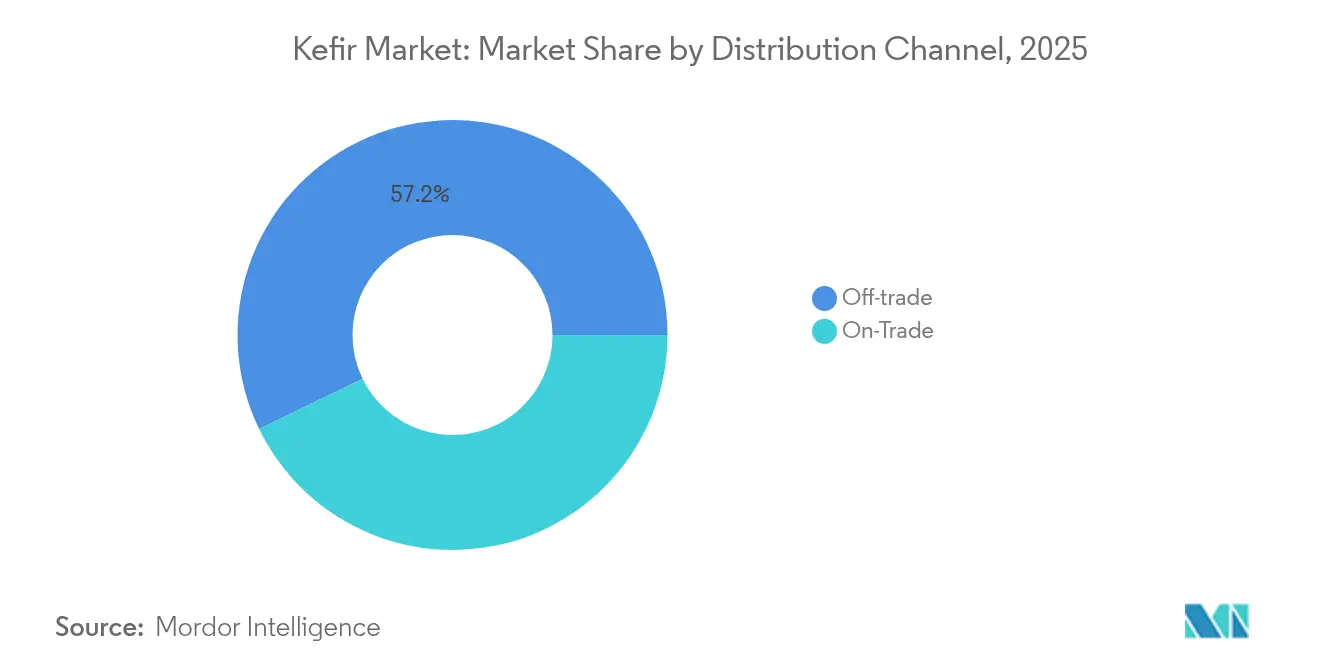

- By distribution channel, off-trade accounted for 57.20% of sales in 2025, whereas on-trade is advancing at a 10.39% CAGR to 2031.

- By packaging, bottles dominated with a 61.63% share in 2025; pouches are projected to register a 10.64% CAGR.

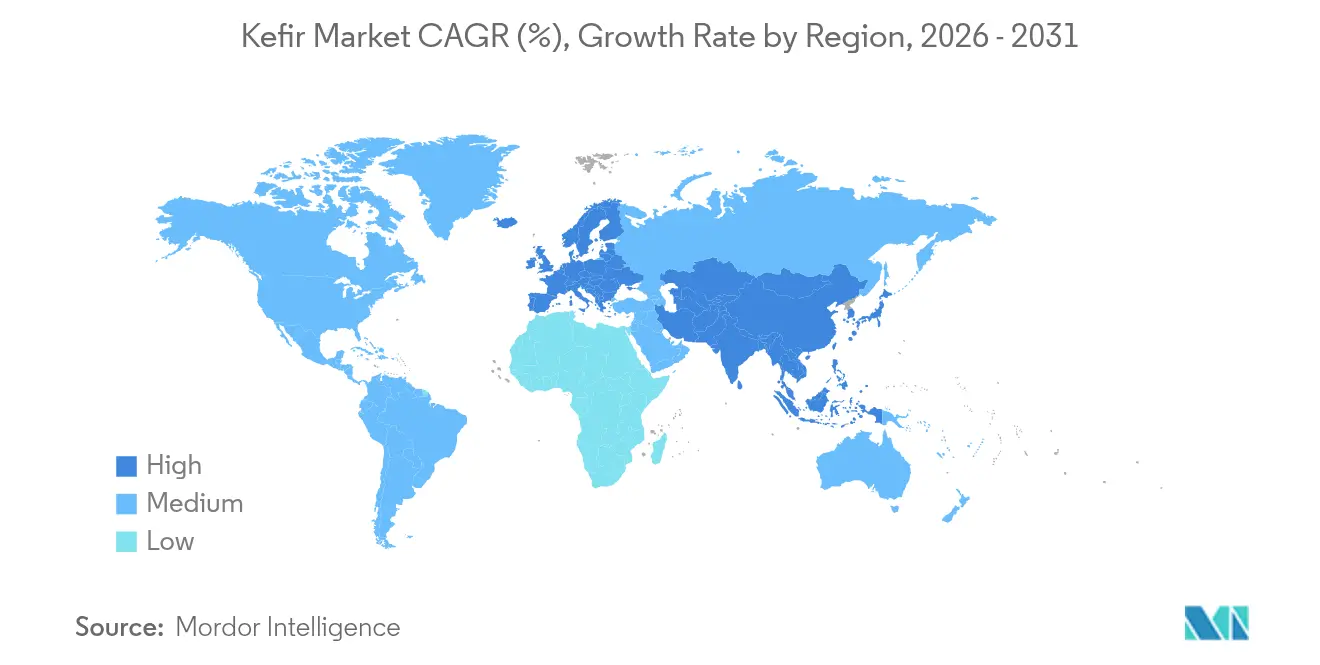

- By geography, Europe led with a 30.92% share in 2025, while Asia-Pacific is anticipated to post an 9.66% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Kefir Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer focus on gut health boosts kefir demand | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Growing popularity of probiotic-rich functional foods | +2.1% | Global, especially Asia-Pacific | Long term (≥4 years) |

| Innovation in flavors of kefir attracts wider demographics | +1.2% | North America and Europe, spreading to Asia-Pacific | Short term (≤2 years) |

| Celebrity and influencer endorsements enhance kefir’s image | +0.9% | North America and Europe | Short term (≤2 years) |

| Demand for clean-label, minimally processed beverages | +1.4% | Global, premium segments | Medium term (2-4 years) |

| Incorporation of kefir in weight-management and detox diets | +1.0% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Focus on Gut Health Boosts Kefir Demand

Dairy kefir contains a diverse range of beneficial microorganisms and bioactive compounds that improve gut microbiota composition and digestive health more effectively than probiotic yogurt and inulin-rich diets. The fermented dairy product's proven effectiveness in managing type 2 diabetes and cardiovascular diseases has increased its consumption among older consumers. Companies have successfully educated consumers about these health benefits through marketing campaigns and product labeling, which has driven market demand. Growing awareness of gut health benefits and digestive wellness among younger consumers has also expanded the market for premium kefir products, including organic and flavored variants.

Growing Popularity of Probiotic-Rich Functional Foods

The growing consumer awareness of probiotics and increased adoption of functional foods are expanding market opportunities, especially in plant-based probiotic products. The Food and Agriculture Organization's (FAO) proposed global probiotic guidelines, covering more than 200 countries, aim to standardize quality requirements and enhance international trade [2]Source: FAO Codex Alimentarius, “Proposed Guidelines on Probiotic Foods,” fao.org. Advancements in manufacturing processes, including improved strain selection and fermentation techniques, enable producers to maintain probiotic counts above 20 billion CFUs per serving, which is higher than traditional yogurt products. Kefir's positioning as a functional food allows for premium pricing while addressing health benefits, including digestive health and immune system support.

Innovation In Flavors of Kefir Attracts Wider Demographics

The kefir market is expanding through flavor diversification and product innovations, driven by increasing consumer demand for functional beverages and probiotic-rich foods. Manufacturers are investing in research and development to create unique formulations that combine traditional fermentation methods with modern flavor preferences. This expansion reflects broader industry trends toward healthier beverage options and personalized nutrition. In November 2024, Lifeway Foods introduced 10 new organic kefir flavors, including Pink Dragon Fruit, Passionfruit Lychee, and Matcha Latte, targeting younger consumers while retaining the product's probiotic properties. These new flavors combine traditional fermented milk with exotic fruit extracts and natural ingredients to create unique taste profiles that appeal to health-conscious consumers. The market growth extends to water kefir products made from plant-based ingredients such as chickpea, almond, and rice, addressing the needs of lactose-intolerant and vegan consumers.

Celebrity and Influencer Endorsements Boost Kefir’s Image

Social media promotion of kefir's health benefits through influencer endorsements is increasing consumer adoption, especially among millennials and Gen Z who value wellness products recommended by trusted personalities. The traditional story of kefir's health benefits in the Caucasus region provides authentic content that spreads naturally across digital platforms. Wellness influencers effectively promote kefir's benefits for gut and skin health, leading companies like Biotiful to develop kefir-based skincare products. Influencer content now includes recipes and lifestyle integration, showing kefir's uses in smoothies, marinades, and baking. Consumers value authentic endorsements from influencers who regularly use kefir products rather than one-time promotional posts. Social media's reach allows smaller kefir brands to gain market share through targeted influencer partnerships that encourage product trials and repeat purchases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from kombucha and yogurt-based beverages | -1.5% | Global, notably North America | Medium term (2-4 years) |

| Higher cost compared to regular dairy products | -1.2% | Emerging, price-sensitive markets | Long term (≥4 years) |

| High added-sugar perception among health-conscious consumers | -0.8% | Developed markets | Short term (≤2 years) |

| Limited shelf-life for water-kefir in tropical regions | -0.6% | Southeast Asia and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition From Kombucha and Yogurt-Based Beverages

The competitive landscape shows kombucha gaining market share as a non-dairy probiotic beverage appealing to younger consumers, while yogurt-based drinks maintain their position through established consumer preferences and production efficiencies. In the online retail segment, kefir faces strong competition from kombucha brands that demonstrate stronger digital marketing and subscription-based sales models. As consumers find it challenging to differentiate between probiotic claims across products, kefir manufacturers must increase investment in consumer education and scientific validation to maintain premium pricing. The market competition now includes new product categories, such as Wonder Veggies' planned launch of probiotic fresh produce, which may lead to further market segmentation. To maintain market position, kefir producers must highlight their core advantages, including diverse probiotic strains and traditional fermentation processes, while developing new products that incorporate popular flavors from other beverage categories.

Higher Cost Compared to Regular Dairy Products

The production costs of kefir are high due to its specialized fermentation processes and probiotic strains, which restrict its accessibility to price-sensitive consumers. These processes require specific temperature controls, precise fermentation timing, and carefully selected bacterial cultures, making production more complex and expensive. The rising costs in the dairy industry, where milk prices exceed production costs, compound this issue. During economic downturns, consumers typically opt for basic dairy products instead of functional beverages like kefir, especially in emerging markets where product awareness is increasing but disposable income remains constrained. The small-scale production nature of kefir and its cold-chain distribution requirements, including temperature-controlled storage and transportation facilities, result in higher retail prices compared to conventional dairy products. Additionally, the short shelf life of kefir necessitates frequent production cycles and rapid distribution, further increasing operational costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Organic Line Momentum Outpaces Conventional Scale

Conventional kefir products held 70.84% of the market share in 2025, while the organic kefir segment is expected to grow at a CAGR of 10.54% through 2031, driven by increasing consumer preference for clean-label and premium products. While conventional kefir continues to benefit from well-established supply chains and mainstream consumer promotions, it faces growth challenges as health-conscious buyers increasingly choose organic alternatives. Manufacturers have invested in improving their fermentation control methods to maintain consistent probiotic content without using synthetic stabilizers, a key requirement for organic certification. Several companies have found a middle ground by incorporating organic milk into standard processing methods, helping them manage costs while maintaining market credibility.

The evolving market landscape requires companies to build strong organic supply chain capabilities and develop certification expertise to remain competitive. Forward-thinking organic producers are distinguishing themselves by implementing automated milking systems and renewable energy solutions at the farm level, while adding value through non-GMO feed and grass-fed certifications. In response, conventional manufacturers are maintaining their market position by developing fortified product lines enriched with vitamin D, calcium, and collagen, particularly appealing to price-sensitive consumer segments.

By Flavor: Diversified Portfolios Extend Consumer Reach

The kefir market shows a clear consumer preference for flavored options, which currently command a 63.45% market share in 2025. This dominance reflects successful efforts by manufacturers to diversify their product offerings and make kefir more appealing to mainstream consumers. Meanwhile, non-flavored variants are experiencing notable growth, with a projected 9.69% CAGR through 2031, as consumers increasingly seek pure, minimally processed options. Lifeway's launch of 10 organic flavors, including innovative combinations like Taro Ube Latte and Pistachio Rose Vanilla, demonstrates how companies are actively responding to diverse consumer preferences, while non-flavored kefir continues to attract health-focused consumers who value its versatility in smoothies and cooking applications.

Market analysis reveals distinct regional patterns in flavor preferences, with tropical and Asian-inspired varieties performing particularly well in culturally diverse markets, while traditional berry and vanilla options maintain their appeal in established markets. Companies are responding to health-conscious consumer demands by developing reduced-sugar formulations that incorporate natural sweetening alternatives, ensuring that taste quality remains high while maintaining the product's probiotic benefits.

By Product Type: Water Kefir Disrupts Dairy Dominance

The kefir market continues to be dominated by traditional milk-based products, which account for 79.72% of market share in 2025. This dominance stems from widespread consumer acceptance and the product's well-documented probiotic benefits. Meanwhile, water kefir is emerging as a significant market player, with projections showing a robust CAGR of 10.18% through 2031, as consumers increasingly seek dairy-free alternatives to accommodate their dietary preferences and restrictions.

Recent technological breakthroughs in plant-based fermentation have enabled manufacturers to develop water kefir using chickpea, almond, and rice extracts. These alternatives now offer probiotic benefits comparable to traditional dairy-based versions. However, manufacturers must navigate several production hurdles, including product stability issues in tropical climates and the requirement for specialized knowledge in managing complex microbial cultures during the manufacturing process.

By Distribution Channel: Retail Remains Core While Foodservice Adds Experiential Value

Off-trade retailers, including supermarkets, hypermarkets, and convenience stores, account for 57.20% of the 2025 revenue through their established cold-chain logistics and high customer traffic. Multi-serve bottles are the primary packaging format in these outlets, with regular promotions driving household adoption. On-trade venues, particularly cafés and smoothie bars, are growing at a 10.39% CAGR as consumers experience kefir through blended beverages and breakfast bowls. This format enables potential customers to sample kefir before purchasing full bottles.

Manufacturers develop specific formulations for on-trade venues by modifying the product's viscosity and sweetness to enhance mixing capabilities. In the off-trade segment, direct-to-consumer online subscriptions maintain market share by offering convenient replenishment options, package deals, and collecting customer data for targeted marketing. The distribution across multiple channels helps stabilize the kefir market against variations in individual retail formats.

By Packaging Type: Bottles Retain Familiarity as Flexible Formats Gain Sustainability Kudos

Bottles held 61.63% share in 2025, valued for rigidity, shelf presence and a perceived premium feel. Glass versions, often reusable or returnable, win eco-minded consumers but add freight weight. Pouches, however, will register a 10.64% CAGR through 2031, propelled by lower material use and convenient, squeezable designs appropriate for on-the-go consumption. The kefir market size for pouch formats escalates as retailers devote more ambient floor-stand space to flexible packaging.

Aseptic technology allows both bottle and pouch SKUs to reach distant markets without strict refrigeration, albeit at the risk of eroding “freshly fermented” positioning. Smart labels that visualize probiotic viability are being piloted, strengthening consumer confidence and reducing wastage. Over the medium term, improvements in monomaterial recyclability promise to reconcile environmental and functional demands, positioning pouches as credible alternatives to traditional bottles

Geography Analysis

European consumers have embraced kefir products, giving the region a commanding 30.92% share of global consumption in 2025. This strong market position stems from generations of familiarity with fermented dairy products, supported by well-established distribution networks across Germany, United Kingdom, and France. Major food companies like Danone are capitalizing on this cultural acceptance by expanding their kefir offerings through new Activia product lines. While the region benefits from comprehensive regulatory frameworks that uphold probiotic health claims and quality standards, the varying interpretations of probiotic terminology and marketing regulations among Eurpean Union member states continue to present operational challenges .

Consumer behavior in Asia-Pacific is rapidly evolving, driving an impressive 9.66% CAGR through 2031 in the kefir market. The region's transformation is particularly evident in Japan, where consumers are increasingly choosing lactic acid beverages over traditional vegetable juices. This shift reflects broader regional trends of urbanization, rising disposable incomes, and growing health consciousness, making Asia-Pacific the most dynamic market for functional food products.

North America maintains its market strength through companies like Lifeway Foods, which dominates the United States kefir category. The region's innovation-friendly regulatory environment, featuring FDA qualified health claims and GRAS approvals for probiotic strains, continues to support product development. Meanwhile, the Middle East and Africa and South America show promise as emerging markets, driven by expanding middle-class populations and increasing health awareness. However, success in these regions requires carefully balanced strategies that address both infrastructure limitations and price sensitivity while maintaining product quality.

Competitive Landscape

The market demonstrates moderate fragmentation, with a balanced mix of global dairy companies and specialized fermented food producers working to capture consumer attention. Companies set themselves apart by investing in scientific validation of their bacterial strains, developing eco-friendly packaging, and creating new flavor profiles. Small and medium-sized producers maintain their market position through quick product development cycles and strong customer relationships, while larger firms leverage their resources for advanced technologies in fermentation, ingredient protection, and quality assurance.

The industry is moving toward consolidation as major dairy companies look to strengthen their presence in the kefir market, especially in Asia-Pacific. The market offers untapped potential in dairy-free alternatives and innovative product applications such as kefir-infused dressings and snack bars. Success increasingly depends on a company's ability to translate complex health benefits into clear, relatable messages that resonate across different cultural markets.

The growing influence of retailers and their private label products continues to shape market dynamics. This shift affects product placement decisions and creates pricing pressures for established brands, requiring companies to adapt their strategies to maintain market share and profitability.

Kefir Industry Leaders

Danone S.A.

Nestlé S.A.

Lifeway Foods Inc.

The Hain Celestial Group

Arla Foods AMBA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Lifeway Foods, based in Morton Grove, Illinois, has significantly expanded its retail presence in 2025 by securing thousands of new placements for its Lifeway Kefir and Farmer Cheese in major United States retailers. Fueled by rising consumer interest in gut-health and functional dairy drinks, Lifeway launched multiple product introductions: new 8 oz organic, lactose-free flavor fusion and kefir shot varieties at 61 Amazon Fresh stores; two 8 oz kefir SKUs at 268 BJ’s Wholesale locations; three 32 oz kefir flavors across CVS; and 32 oz kefir SKUs in 170 Winn-Dixie outlets

- April 2025: Arla Foods and Germany's DMK Group have announced plans to merge, forming Europe's largest dairy cooperative with a network of over 12,000 farmers. This consolidation aims to enhance operational resilience as European milk production faces projected declines. The merger will expand product portfolios and ensure sustainable milk prices for farmers.

- September 2024: Activia has expanded its product line by launching kefir products in both spoonable and drinkable formats, featuring 16 live culture strains. The products have secured shelf space in major UK retailers including Waitrose, Tesco, and Morrisons, as Danone strengthens its kefir portfolio to meet the growing consumer interest in digestive health products.

- September 2024: Bio&Me, the UK-based gut-health brand founded by Dr. Megan Rossi, expanded its kefir product line with two new 500 ml "Good for Your Gut" kefir drinks. The drinks, available in Natural and Vanilla flavors, were distributed through Sainsbury's and Whole Foods, including a promotional display at Whole Foods' Kensington flagship store.

Global Kefir Market Report Scope

Kefir is a fermented drink similar to thin yogurt made from kefir grains.

The kefir market is segmented based on form, category, type, distribution channel, and geography. By form, the market is segmented into organic and conventional. By category, the market is segmented into flavored and unflavored kefir. By product type, the market is segmented into milk and water-based kefir. By distribution channel, the market is segmented into supermarkets, hypermarkets, convenience stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market sizing and forecast have been done based on value (in USD million).

| Organic |

| Conventional |

| Flavored Kefir |

| Non-flavored Kefir |

| Milk Kefir |

| Water Kefir |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Retail Channels | |

| On-Trade |

| Bottles |

| Pouches |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Form | Organic | |

| Conventional | ||

| By Flavor | Flavored Kefir | |

| Non-flavored Kefir | ||

| By Product Type | Milk Kefir | |

| Water Kefir | ||

| By Distribution Channel | Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Retail Channels | ||

| On-Trade | ||

| By Packaging Type | Bottles | |

| Pouches | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current kefir market size?

The kefir market generated USD 1.99 billion in 2026 and is projected to hit USD 3.01 billion by 2031 at an 8.63% CAGR.

Which segment leads the kefir market by product type?

Milk kefir dominates with 79.72% of 2025 revenue, reflecting consumer familiarity and broad retail availability.

How fast is water kefir growing?

Water kefir is forecast to expand at a robust 10.18% CAGR between 2026 and 2031, driven by lactose-free and vegan demand.

Which region shows the fastest kefir market growth?

Asia-Pacific is projected to record an 9.66% CAGR through 2031, fuelled by rising disposable incomes and probiotic awareness.

What packaging trend is emerging in the kefir industry?

Flexible pouches are the fastest-growing format at a 10.64% CAGR, supported by sustainability credentials and on-the-go convenience.

Page last updated on: