Ketchup Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 18.73 Billion |

| Market Size (2031) | USD 23.61 Billion |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

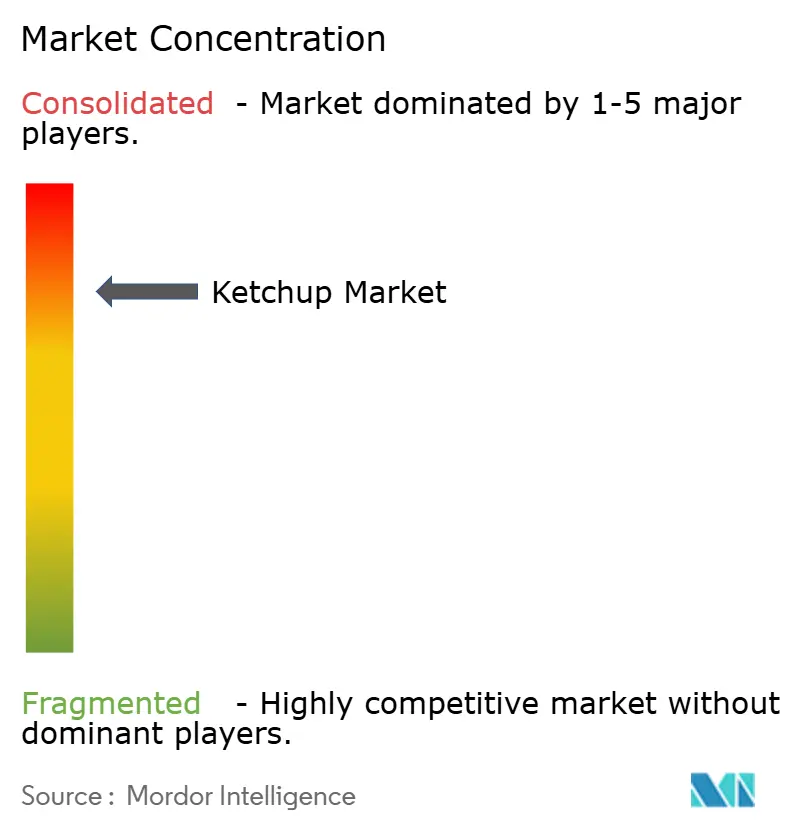

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ketchup Market Analysis by Mordor Intelligence

The ketchup market size is expected to grow from USD 17.88 billion in 2025 to USD 18.73 billion in 2026 and is forecast to reach USD 23.61 billion by 2031 at 4.74% CAGR over 2026-2031. Ketchup's growth is fueled by its deep-rooted presence in global dining and its nimbleness in adapting to trends like convenience, health, and premiumization. Its demand is widespread, encompassing traditional fast-food accompaniments, meal-kit enhancements, and gourmet applications that elevate home cooking experiences. This versatility ensures its relevance across diverse consumer preferences, culinary practices, and eating occasions. Brands bolster their resilience through climate-conscious tomato sourcing, pioneering flavor innovations, and eco-friendly packaging, which align with evolving consumer expectations for sustainability, quality, and ethical practices. Additionally, the rise of digital commerce broadens reach, enabling niche producers to explore markets and test consumer preferences without the burden of extensive physical distribution investments. This digital shift not only fosters innovation and competition but also allows smaller players to establish a foothold in the market, contributing to its dynamic growth.

Key Report Takeaways

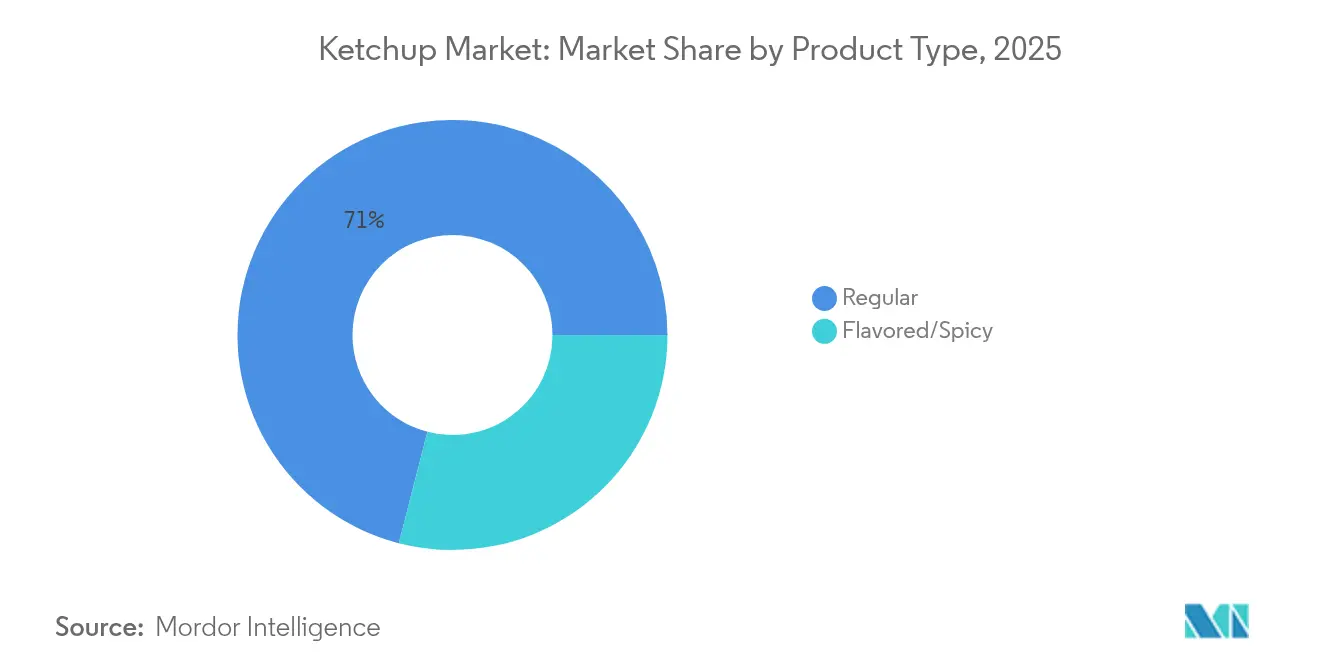

- By product type, regular ketchup led with 70.98% of ketchup market share in 2025, while flavored variants are on course for a 5.34% CAGR between 2026-2031.

- By category, conventional offerings controlled 82.93% share of the ketchup market size in 2025, whereas organic lines are poised for a 6.03% CAGR through 2031.

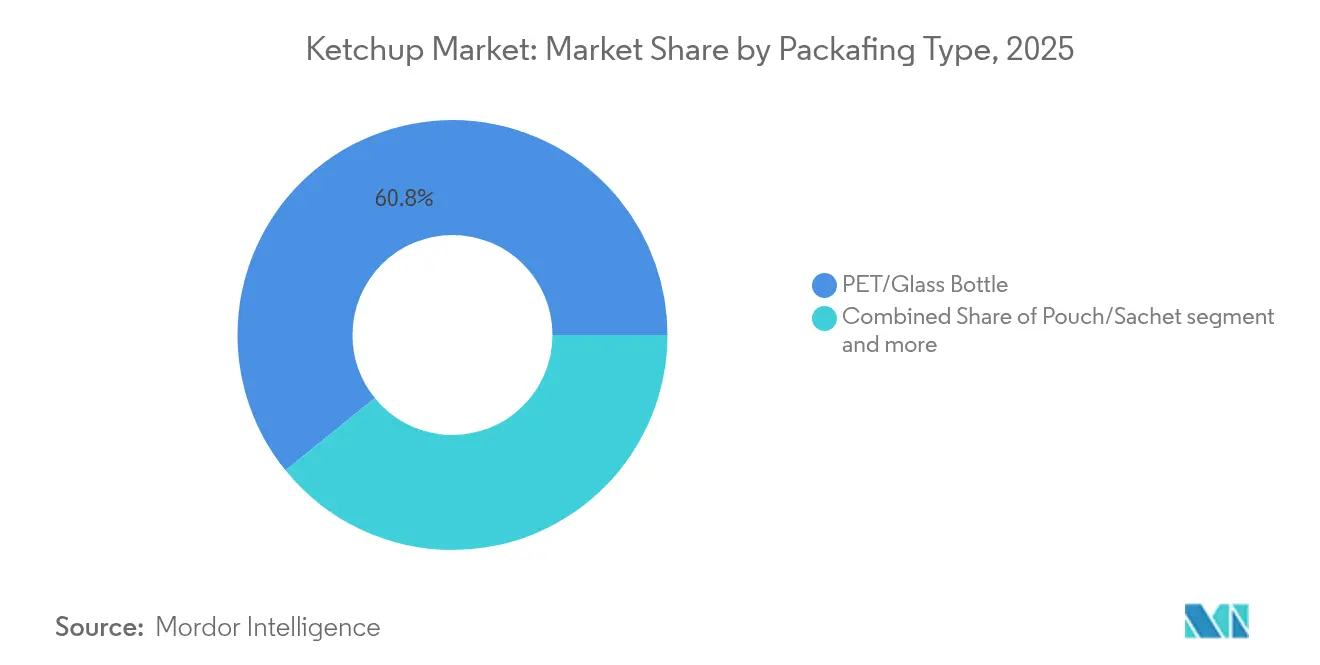

- By packaging, PET/glass bottles accounted for 60.84% of the ketchup market share in 2025; pouches and sachets are projected to grow at 5.56% CAGR to 2031.

- By distribution channel, off-trade held 62.45% of the ketchup market size in 2025, while on-trade is forecast to expand at 5.26% CAGR during 2026-2031.

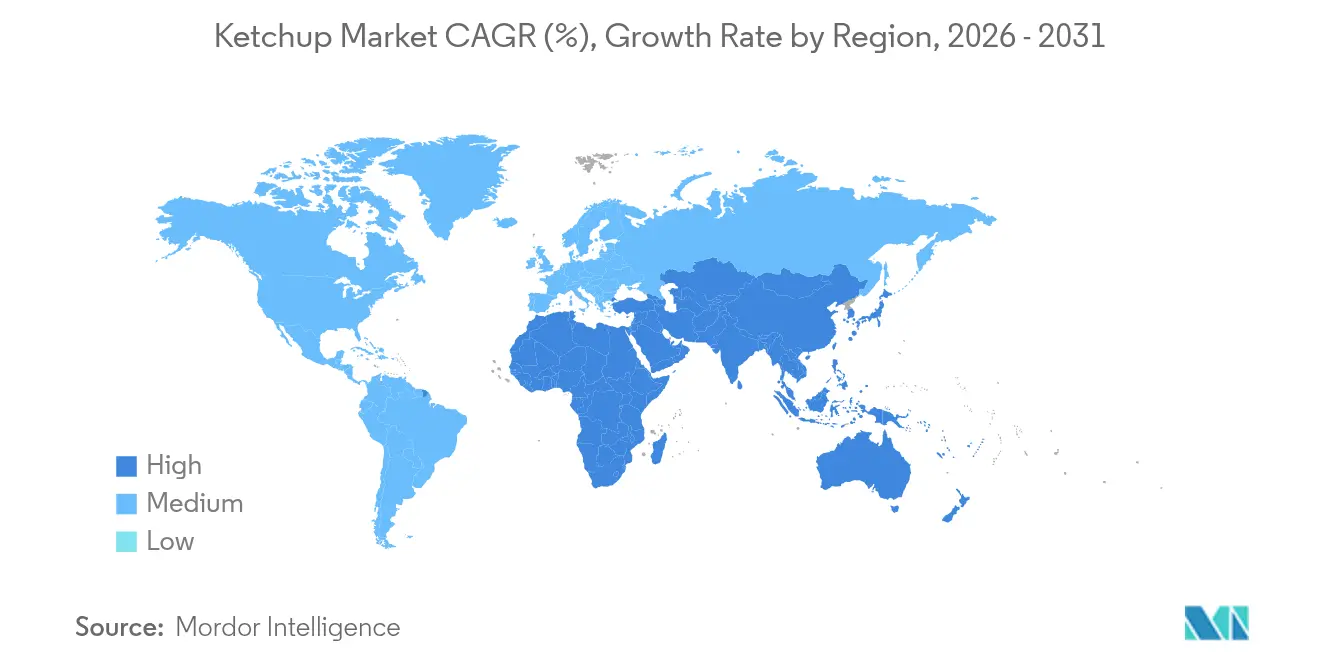

- By region, Europe secured 31.84% revenue share in 2025; Asia-Pacific is set to post the highest 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ketchup Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience-food demand spike | +1.2% | Global, with strongest impact in North America and Asia-Pacific | Medium term (2-4 years) |

| Fast-food expansion in emerging markets | +0.8% | Asia-Pacific core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Innovative packaging and flavor formats | +1.1% | Global, early adoption in Europe and North America | Short term (≤ 2 years) |

| Cross-border e-commerce reach | +0.6% | Global, concentrated in developed markets initially | Medium term (2-4 years) |

| Regenerative tomato-sourcing pull-through | +0.9% | North America and EU primary, expanding globally | Long term (≥ 4 years) |

| Growing demand for natural and clean-label ingredients | +0.7% | Global, led by North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Convenience-food demand spike

As lifestyles accelerate, the reliance on ready-to-eat items grows, amplifying ketchup's role as an instant flavor enhancer. Data from the USDA reveal that as dining out becomes more prevalent, condiment usage rises, leading to a surge in single-serve ketchup volumes[1]Source: United States Department of Agriculture," Food Consumption and Nutrient Intake Trends Emerge Over Past Four Decades," www.ers.usda.gov. These single-serve packs are particularly popular in fast-food chains, cafeterias, and convenience stores, where quick service and portability are key priorities. Shelf-stable, portion-controlled packs are designed for commuters and students who value portability, offering a convenient solution for on-the-go consumption. Thanks to its long shelf life, ketchup finds a place in emergency food kits and institutional meal plans, ensuring a reliable flavoring option in various scenarios. Manufacturers are experimenting with flavors, introducing smoky or spicy notes, to refresh traditional profiles while maintaining their familiar essence. These innovations aim to cater to evolving consumer preferences, keeping the product relevant in a competitive market. Regulatory mandates on transparent labeling empower consumers, allowing them to make informed choices even in the fast-paced world of quick eating, further bolstering demand.

Fast-food expansion in emerging markets

Across Asia-Pacific and Latin America, quick-service restaurant networks are rapidly expanding, leading to an uptick in ketchup usage. Both U.S. chains and local franchises are making ketchup a standard accompaniment, introducing it to new consumer groups and reinforcing its role in modern dining habits. As young urban populations with increasing disposable incomes adopt Western dining styles, ketchup becomes a staple in their daily meals, often complementing popular fast-food items like burgers, fries, and sandwiches. Menu localization introduces spicy or sweetened regional ketchup variants, promoting experimentation within the category and catering to diverse taste preferences. Furthermore, with governments backing foreign foodservice investments to boost employment and economic growth, the demand for ketchup remains robust, supported by the growing footprint of international and domestic foodservice chains.

Innovative packaging and flavor formats

Driven by EU Regulation 2025/40, brands are re-engineering bottles and pouches to incorporate higher recycled content, aiming to meet sustainability goals and regulatory compliance[2]Source: United States Department of Agriculture," European Union: European Union Finalizes New Rules for Packaging and Packaging Waste Reduction," fas.usda.gov. Brands that are quick to adapt are prominently highlighting their reduced carbon footprints on front labels, effectively appealing to eco-conscious consumers who prioritize environmentally friendly products. In markets where price sensitivity prevails, stand-up pouches are being utilized to lower unit costs, making them ideal for small trial packs that fit within weekly budgets and encourage consumer trials. On the premium side, glass containers with embossed labels are maintaining product purity perceptions, resonating strongly with the clean-label trend that emphasizes transparency and natural ingredients. Innovative flavors, ranging from chipotle-infused to basil-accented, are not only securing premium shelf space but also bolstering profit margins by catering to evolving consumer tastes and preferences. Additionally, rapid prototyping in pilot kitchens is accelerating the journey from idea to shelf, enabling companies to swiftly respond to fleeting flavor trends and gain a competitive edge in the market.

Cross-border e-commerce reach

Artisanal ketchup brands leverage direct-to-consumer platforms to reach expatriate communities and gourmet enthusiasts overseas, offering them niche and high-quality products that cater to their specific tastes. With India's online grocery sales expected to hit USD 10-12 billion by 2025, it's evident that digital platforms are playing a pivotal role in enhancing the visibility and accessibility of packaged condiments[3]Source: Invest India,"Retail & E-commerce," www.investindia.gov.in. Fulfillment centers now feature temperature-controlled zones, ensuring product integrity during extended transport, which is crucial for maintaining the quality of perishable goods like ketchup. Influencers in social commerce are shining a spotlight on small-batch organic ketchup, creating awareness and spurring impulse purchases internationally by showcasing unique product attributes. Thanks to customs harmonization efforts in ASEAN, paperwork has become more streamlined, resulting in reduced final prices, faster delivery times, and an expanded audience reach for artisanal ketchup brands.

Restraint Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health pushback on sugar/salt | -0.9% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Rising alternative-condiment rivalry | -0.6% | North America and Europe primary, expanding globally | Medium term (2-4 years) |

| Climate-driven tomato yield volatility | -0.8% | Global, acute in California and Mediterranean regions | Long term (≥ 4 years) |

| Availability of substitute | -0.4% | Global, varied by regional taste preferences | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health pushback on sugar/salt

Public health campaigns are pushing for a reduction in sweetened sauce consumption, leading parents to examine ketchup labels more closely. Many conventional SKUs fall outside the FDA's "healthy" claim band due to the agency's 2025 criteria, limiting on-pack promotional opportunities and potentially impacting consumer purchasing decisions. This shift is expected to drive manufacturers to explore healthier formulations to meet evolving regulatory and consumer demands. Reformulating ketchup to cut sugar while balancing acidity and viscosity drives up research and development costs, as manufacturers must invest in advanced techniques, ingredient testing, and sensory evaluations to maintain product quality. In Western Europe, retail chains are using traffic-light nutritional stickers, pushing high-sugar ketchups to lower shelf positions, which could reduce their visibility and sales. This trend reflects a broader movement toward promoting healthier food choices at the retail level. While flavor-house suppliers provide monk fruit and stevia solutions as sugar alternatives, their lingering aftertastes hinder widespread acceptance, posing a challenge for mass-market adoption and requiring further innovation in sweetener technology.

Climate-driven tomato yield volatility

California, responsible for processing roughly 30% of the globe's tomato market volume, now grapples with shorter harvest windows due to increasingly hotter summers. This shift strains the state's processing capacity, as processors struggle to handle the compressed timelines for harvesting and processing. Furthermore, extreme heat not only diminishes lycopene content, affecting color consistency, but also drives up costs due to the need for blending to maintain product standards. In response to these challenges, multinationals are diversifying their sourcing, turning to Spain, Turkey, and emerging farms in North Africa. However, this strategy comes with its own set of logistical expenses, including higher transportation costs and potential delays in supply chains. As weather-related crop failures become more frequent, insurance premiums have surged, putting a squeeze on farm earnings and amplifying the variability of raw material costs. Meanwhile, start-ups are championing controlled-environment agriculture for tomatoes, which offers a potential solution by mitigating weather-related risks and ensuring consistent quality. Yet, the high capital requirements of this approach, including investments in advanced technology and infrastructure, are hindering rapid expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Regular Dominance with Flavor Upside

In 2025, regular ketchup offerings command a dominant 70.98% market share, underscoring the consistency of global recipes and habitual consumer purchasing patterns. This quintessential red condiment is synonymous with staples like fries, burgers, and eggs, fueling steady demand and enabling efficient large-scale production. Its universal flavor profile and widespread recognition cultivate a dedicated customer base that views ketchup as an indispensable condiment. Major brands leverage economies of scale, ensuring competitive pricing and extensive availability. The sustained popularity of regular ketchup cements its status as the primary product driving global volume sales. For market leaders, this segment is pivotal, bolstering consistent revenue streams amidst a shifting condiment landscape.

On the other hand, flavored ketchup lines are the market's fastest-growing segment, boasting a CAGR of 5.34%. As adventurous millennials gravitate towards Chipotle, curry, sriracha, and other innovative blends of Western formats with local spices, leading ketchup brands are ramping up research and development investments. Their goal is to tap into these niche micro-segments without undermining their core regular ketchup sales. Often debuting as limited editions, these new flavors allow marketers to gauge consumer interest and swiftly adapt based on feedback, especially from social media polls. Retailers, keen on seasonal promotions, prominently display spicy flavored ketchups during grilling season to attract barbecue lovers. Meanwhile, foodservice operators are experimenting with regional flavors, adjusting quick-service menus to promote trials that could lead to mainstream retail adoption. Between 2026 and 2031, the flavored ketchup market is set to grow by an estimated USD 1.32 billion, bolstered by strategic cross-promotions with snack manufacturers that enhance reach and consumer engagement.

By Category: Conventional Scale, Organic Acceleration

In 2025, conventional ketchup commands a dominant 82.93% market share, thanks to cost-effective production and a long-standing consumer trust in its quality and flavor. This segment resonates especially with price-sensitive consumers in emerging markets, who favor multi-serve plastic bottles for added value. The widespread availability and recognition of conventional ketchup solidify its status as the go-to household condiment. Its established market presence, bolstered by economies of scale, ensures competitive pricing and a consistent supply across various regions. The combination of affordability and trust in this traditional product cements its foundational role in the ketchup industry. Furthermore, manufacturers are continually refining production processes to uphold profit margins while catering to a broad consumer base.

On the other hand, organic ketchup is the market's fastest-growing segment, boasting a CAGR of 6.03%. This surge is largely driven by health-conscious parents prioritizing pesticide-free staples for their families. While its current volume is modest, organic ketchup's share in specialty retail is set to leap to 22.60% by 2031, fueled by robust double-digit sales growth. Achieving organic certification involves stringent audits, allowing vertically integrated growers to fetch premium prices for their produce. E-commerce is pivotal in amplifying organic ketchup's visibility, navigating challenges like limited shelf space and steep fees in conventional hypermarkets. Retailers bolster this segment with promotions like “organic weeks,” pairing ketchup with other organic staples such as pasta and dairy to enhance overall sales. Major companies are also introducing dedicated sub-brands, tapping into the organic market while preserving the premium image of their flagship conventional lines, ensuring strategic expansion in this lucrative niche.

By Packaging: Bottles Endure as Flexible Gains Ground

In 2025, PET and glass bottles commanded a significant 60.84% share of the ketchup market. Their dominance stems from features like strong consumer familiarity, tamper-evident seals, and reliable stability on tables. Family-size squeeze bottles have emerged as staples in value-driven channels, providing households with convenience and ease. Meanwhile, at the premium tier, curved glass bottles are the top choice for gifting sets, bolstering perceptions of quality and luxury. These traditional packaging formats enjoy widespread acceptance and trust, ensuring sustained demand across diverse markets. Their robustness and aesthetic charm make them favorites for both daily use and special events. Manufacturers are innovating within these formats, striving for a balance between cost-efficiency and consumer desires for convenience and a premium look.

On the other hand, pouches and sachets are the fastest-growing packaging segment, boasting a CAGR of 5.56%. This growth is fueled by increasing out-of-home consumption and affordability in emerging markets like India, Indonesia, and Nigeria. Flexible packs are becoming the go-to choice for school canteens and airline catering, where portion control and convenience are paramount. The market for these flexible packaging formats is projected to double by 2030, indicating a surge in adoption. Producers are channeling investments into high-speed hot-fill lines tailored for laminated films. These innovations cut material use by up to 70% compared to traditional rigid packaging, marking a significant leap towards sustainability. Retailers are increasingly drawn to cube-efficient pouches, which boost shelf density and trim freight costs. Furthermore, with regulatory pressures mounting—like the EU's push for 65% recycled content in plastics by 2040—mono-material pouch structures are gaining traction. They not only meet compliance standards but also champion environmental sustainability.

By Distribution Channel: Retail Dominates, Food-Service Rises

In 2025, off-trade platforms ranging from hypermarkets and supermarkets to convenience stores and digital grocers commanded a dominant 62.45% share of the ketchup market. Their success is attributed to promotional price packs, loyalty program tie-ins, and strategic cross-merchandising with frozen snacks, all driving heightened product throughput. The surge in digital grocery shopping, especially in megacities where same-day delivery is standard, amplifies these sales. Furthermore, innovative QR-based promotions seamlessly connect shoppers from recipe videos to swift, one-click checkouts, bolstering both convenience and engagement. The extensive availability and visibility of ketchup through these channels solidify off-trade as the primary purchasing point for many consumers. Merging the strengths of traditional retail with the dynamism of e-commerce, this segment firmly establishes itself as the market leader.

On the other hand, the on-trade segment is witnessing the fastest growth, boasting a 5.26% CAGR. This surge is fueled by the resurgence of restaurants, the rise of cloud kitchens, and revamped hotel buffet offerings. Catering to this demand, food-service wholesalers are utilizing jumbo bag-in-box packaging, which not only reduces refill times but also minimizes waste, thereby enhancing operational efficiency. Additionally, menu engineering teams are increasingly seeking customized ketchup varieties, adjusting spice levels to align with regional tastes and specific chain profiles. Catering to large-scale foodservice needs, stadiums and event organizers are opting for nitrogen-flushed bulk packs, ensuring extended freshness post-opening. The evolution of this segment is further amplified by the blending of off-trade and on-trade channels, exemplified by quick-service brands retailing their signature ketchup in supermarkets. This crossover not only underscores the brand equity of restaurants but also signals a notable uptick in at-home consumption, showcasing a vibrant interplay between the two market segments.

Geography Analysis

In 2025, North America captured 36.22% of global revenue, bolstered by its long-standing industry presence. Even as the market matures and volumes moderate, North America continues to stand as a beacon of innovation. Stricter nutrient regulations from the FDA have not only spurred early reformulation in the U.S. but have also set a precedent for adoption in other countries. Facing climate challenges, California is diversifying its supply chains, turning to Mexico and controlled-environment greenhouses to ensure a steady flow of raw materials. Marketing strategies are tapping into patriotic sentiments, using themes like Fourth of July cookouts to rekindle emotional connections with ketchup. E-commerce is making waves, with subscription models allowing families to auto-replenish staples and customize flavor bundles based on data insights.

Asia-Pacific is on a growth trajectory, boasting the fastest CAGR of 7.12% through 2031, driven by urban households increasingly opting for quick-cook meal solutions. In China, tier-2 cities are witnessing a surge in hypermarket expansions, leading to a broader display of ketchup products. Meanwhile, India's organized retail landscape and the surge in online shopping are positioning it as a crucial demand hub. The region's diverse palate is giving rise to soy-blended and chili-fortified ketchup variants, broadening their appeal beyond traditional Western dishes. To navigate global trade fluctuations, domestic processors are turning to retort technology, ensuring they meet both export benchmarks and local cost demands.

Europe, with its rich tomato cultivation and a culture steeped in indulgent dining, stands as a pivotal market for ketchup. Here, consumers are willing to pay a premium for labels that boast regional authenticity, like “Made with Emilia-Romagna tomatoes,” underscoring ketchup's ties to local culinary heritage. The European Union's shelf tax is pushing brands to rethink their merchandising strategies; innovations like gravity-feed chilled rails and reusable glass jar deposit schemes are not just trends but tools to cultivate brand loyalty. With heightened regulatory scrutiny on plastic waste, brands are swiftly pivoting to paper-based multipacks, reaping rewards in shelf space for being early adopters.

Competitive Landscape

The global ketchup market exhibits moderate concentration, indicating established player dominance while maintaining competitive dynamics that prevent monopolistic control. Yet, regional disruptors and private labels introduce a lively competition in both pricing and flavor. Kraft Heinz, riding high on its iconic branding and extensive procurement, finds its territory nibbled at by nimble organic specialists. The company, hinting at a potential corporate split in July 2025, may soon see its ketchup division emerge as a standalone condiment powerhouse, reshaping its capital strategies and research and development pace. Meanwhile, Nestlé’s Maggi brand fortifies its foothold in the Asia-Pacific, tailoring recipes and pricing sachets to fit single-meal budgets.

In European supermarkets, private labels are on the rise, leveraging robust supply chains and a value-centric approach, particularly during inflationary periods. Retailers ink multi-year manufacturing deals, ensuring volume commitments while making slight recipe adjustments to avoid direct brand comparisons. O-I, a glass jar supplier, teams up with upscale ketchup startups, rolling out limited-edition embossed designs perfect for gifting. Sustainability takes center stage: Hunt’s pilots a refill station in U.S. bulk-buy outlets, aiming to cut down packaging waste.

Mergers and acquisitions are buzzing. Adani Wilmar’s takeover of GD Foods not only bolsters its footprint in India’s ketchup market but also tightens ties with local tomato farmers. Agro Tech Foods, in its acquisition of Del Monte Foods Pvt Ltd, gains access to established manufacturing in Tamil Nadu, speeding up market rollouts. Multinational giants eye plant-based mayonnaise brands, seeking to pair them with ketchup for enticing combo promotions, aiming to diversify household condiment choices. The health narrative intensifies as intellectual-property disputes flare over claims like “rich in lycopene antioxidants.”

Ketchup Industry Leaders

-

Conagra Brands, Inc.

-

The Kraft Heinz Company

-

Unilever PLC

-

Nestlé S.A.

-

Del Monte Foods Holdings Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Fly by Jing debuted its Chili Crisp Ketchup online, merging their signature chili crisp with traditional ketchup, and set the price at USD 15 per bottle. This product launch highlights the company's innovative approach to combining bold flavors with everyday condiments, aiming to attract adventurous and flavor-seeking consumers.

- May 2025: Thomas Biotech & Cytobacts Centre for Bioscience unveiled its latest creation, a papaya-infused ketchup dubbed "Papchup". This product leverages the natural sweetness and nutritional benefits of papaya, catering to consumers seeking healthier and unique alternatives in the ketchup market.

- April 2025: Granos introduced its "Better Ketchup", sweetened with jaggery. This innovation underscores the company's dedication to offering healthy, preservative-free products tailored for today's health-conscious consumers. By using jaggery as a natural sweetener, Granos aims to provide a product that aligns with the growing demand for clean-label and minimally processed food options.

- February 2025: Heinz UK rolled out "Tomato Ketchup Zero", boasting no added sugar or salt and featuring 35% more tomatoes, specifically targeting health-aware shoppers. This launch reflects Heinz's commitment to addressing the increasing consumer preference for healthier condiment choices without compromising on taste.

Global Ketchup Market Report Scope

Ketchup is a sweet and tangy sauce usually made with tomatoes, sweeteners, vinegar, salt, various seasonings, spices, and other additives and is a very popular condiment.

The ketchup market is segmented by product type, packaging, distribution channel, and geography. Based on product type, the market is segmented into regular ketchup and flavored ketchup. Based on packaging, the market is segmented into bottled and pouch. Based on the distribution channel, the market is segmented into on-trade and off-trade channels. The on-trade channel comprises food service channels, while off-trade is further segregated into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. Based on geography, the market segments are North America, Europe, Asia-Pacific, South America, and Middle-East & Africa.

For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Regular Ketchup |

| Flavored |

| Conventional |

| Organic |

| PET/Glass Bottle |

| Pouch and Sachet |

| Others |

| On Trade | |

| Off Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Regular Ketchup | |

| Flavored | ||

| By Category | Conventional | |

| Organic | ||

| By Packaging | PET/Glass Bottle | |

| Pouch and Sachet | ||

| Others | ||

| By Distribution Channel | On Trade | |

| Off Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the ketchup market in 2026?

The ketchup market size is USD 18.73 billion in 2026 and is projected to reach USD 23.61 billion by 2031.

Which region grows fastest through 2031

Asia-Pacific leads growth with a 7.12% CAGR, propelled by quick-service restaurant expansion and rising middle-class incomes.

What packaging format gains popularity?

Flexible pouches and sachets post a 5.56% CAGR thanks to convenience and cost advantages in emerging economies.

How does new FDA guidance affect ketchup?

The FDA’s 2025 “healthy” criteria limit added sugars and sodium, driving reformulation and cleaner labels among leading brands.

Which region has the biggest share in Ketchup Market?

In 2026, the North America accounts for the largest market share in Ketchup Market.

What is driving organic ketchup demand?

Health and sustainability concerns push organic ketchup to a 6.03% CAGR, even though it starts from a smaller base.

Page last updated on: