Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

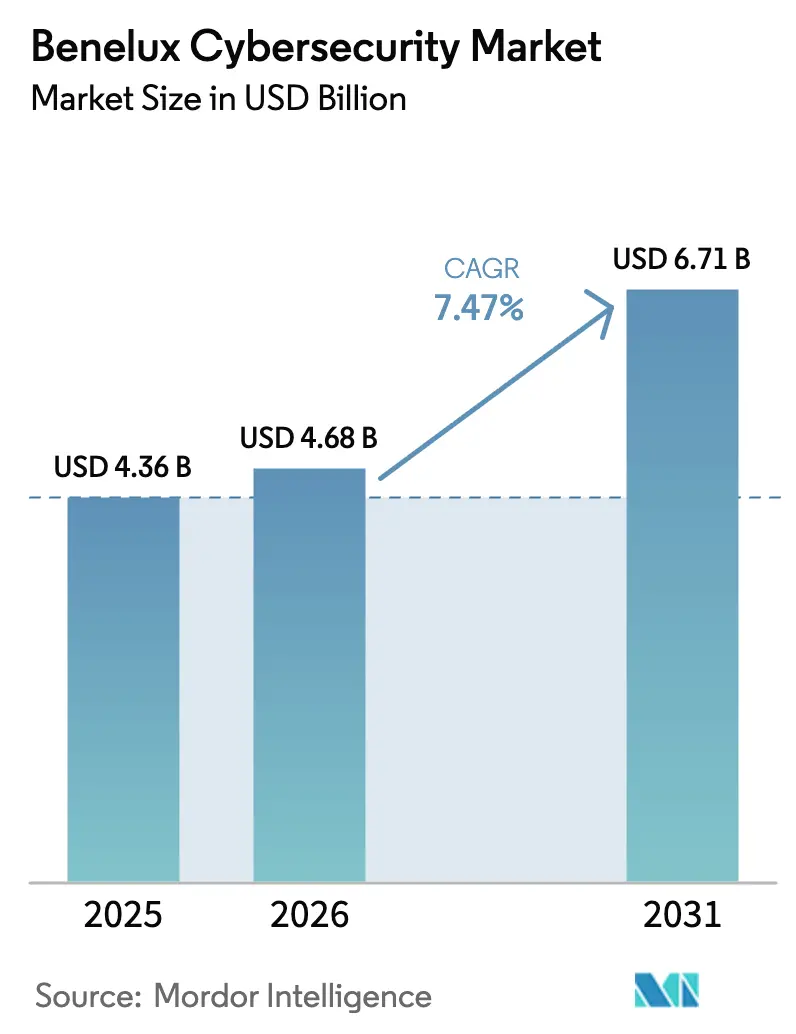

| Base Year Market Size (2025) | USD 4.36 Billion |

| Market Size (2026) | USD 4.68 Billion |

| Market Size (2031) | USD 6.71 Billion |

| Growth Rate (2026 - 2031) | 7.47% CAGR |

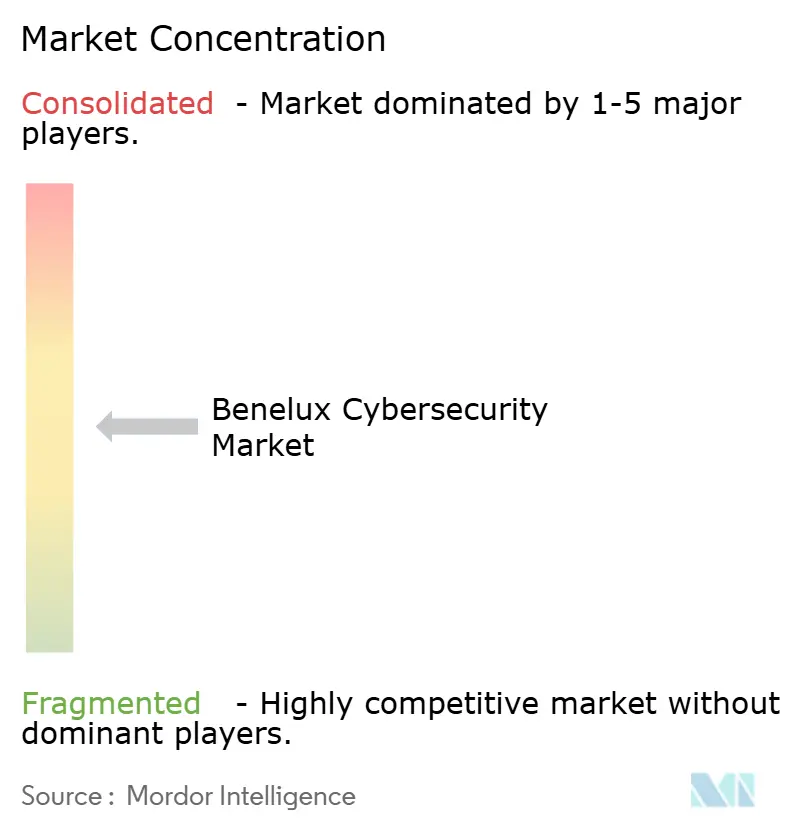

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benelux Cybersecurity Market Analysis by Mordor Intelligence

The Benelux cybersecurity market size is expected to grow from USD 4.36 billion in 2025 to USD 4.68 billion in 2026 and is forecast to reach USD 6.71 billion by 2031 at 7.47% CAGR over 2026-2031. Accelerated cloud migration, stricter enforcement of the EU Network and Information Security Directive 2 (NIS2), and the rising strategic value of operational-technology security around the ports of Rotterdam and Antwerp are the primary tailwinds. Belgium’s early transposition of NIS2 has made compliance technology a spending priority, while the Netherlands and Luxembourg face implementation delays that heighten regulatory risk and spur pre-emptive investments. Managed security service providers (MSSPs) are winning share as enterprises struggle to fill more than 13,500 vacant cyber positions across the region. Venture funding into privacy-enhancing computation startups clustered in The Hague Security Delta exceeded USD 130 million in 2025, underscoring investor confidence in data-sovereignty solutions for finance and healthcare.

Key Report Takeaways

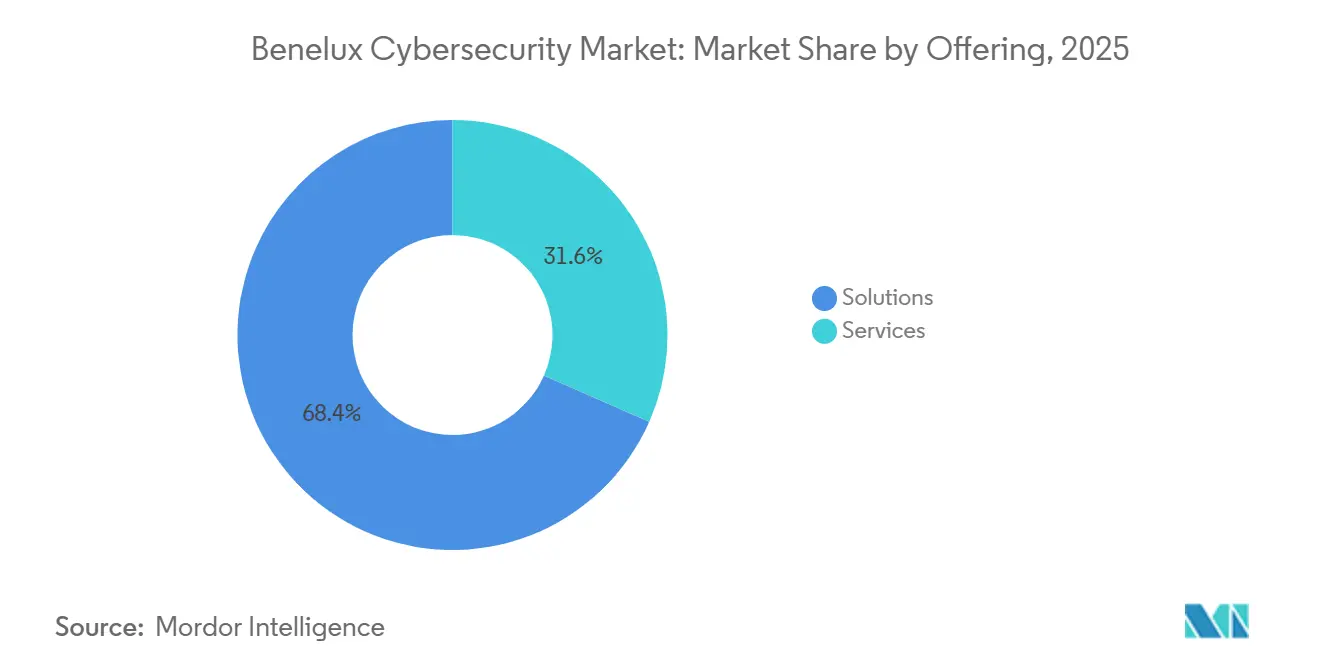

- By offering, solutions commanded 68.38% of the Benelux cybersecurity market share in 2025, while services are projected to record an 8.23% CAGR through 2031.

- By deployment mode, cloud held 63.21% share of the Benelux cybersecurity market size in 2025 and is forecast to expand at an 8.68% CAGR over 2026-2031.

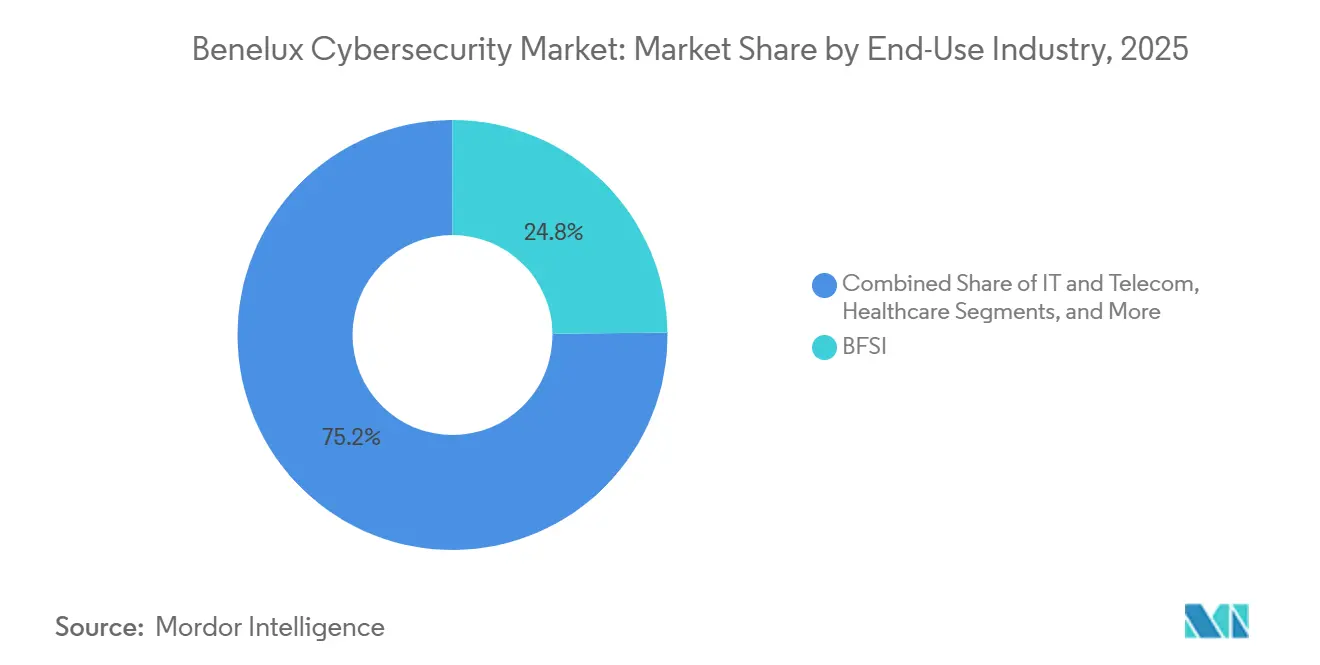

- By end-use industry, BFSI led with 24.82% of the Benelux cybersecurity market share in 2025; retail and e-commerce is advancing at a 9.12% CAGR to 2031.

- By enterprise size, large organizations accounted for 68.43% of the Benelux cybersecurity market size in 2025, whereas SMEs are growing at an 8.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Benelux Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Sophistication of Cyber Threats | +1.8% | Netherlands, Belgium, Luxembourg | Short term (≤ 2 years) |

| Accelerated Cloud Migration Across Enterprises | +1.5% | Netherlands (dominant), Belgium, Luxembourg | Medium term (2-4 years) |

| Mandatory Compliance With EU NIS2 Directive | +1.4% | Belgium (early mover), Netherlands, Luxembourg | Short term (≤ 2 years) |

| Surge in Cyber Insurance Premium Differentials | +1.0% | Netherlands, Belgium | Medium term (2-4 years) |

| Expansion of Port-Centric OT Networks | +0.9% | Netherlands (Rotterdam), Belgium (Antwerp) | Long term (≥ 4 years) |

| Emergence of Privacy-Enhancing Computation Startups | +0.6% | Netherlands (The Hague), spillover to Belgium | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Sophistication of Cyber Threats

Ransomware-as-a-service kits and state-linked advanced persistent-threat groups intensified their campaigns in 2025, producing a 35% jump in incidents against Dutch critical-infrastructure operators. Threat actors now pair double-extortion ransomware with data-exfiltration to raise pressure on victims, an approach that forced Belgian hospitals to harden endpoint protection and deploy data-loss-prevention controls. Luxembourgish banks faced credential-stuffing waves built on breach-derived datasets, prompting regulators to require session-monitoring tools. Attackers’ pivot from broad phishing to executive-impersonation spear-phishing stimulated demand for email gateways capable of natural-language inspection. Collectively, these dynamics elevate baseline security requirements and push enterprises toward behavior-analytics platforms that look beyond static signatures.

Accelerated Cloud Migration Across Enterprises

By 2025, 85% of Dutch companies ran at least one workload in a public cloud, exposing misconfiguration risks that accounted for one-third of the region’s reported breaches. Belgian firms, 72% of which now operate hybrid architectures, must reconcile fragmented identity and access policies across on-premises and multicloud estates.[1]Belgian Federal Public Service for Economy, “Digital Economy Survey 2025,” economy.fgov.be Luxembourg’s banks favor sovereign clouds that keep encryption keys within national borders, driving uptake of external key-management services. Widespread SaaS adoption has diluted centralized visibility, making cloud-access security brokers and cloud-security-posture-management tools essential. As retailers shift point-of-sale systems to cloud payment processors, tokenization and end-to-end encryption form the core of compliance strategies.

Mandatory Compliance With EU NIS2 Directive

Belgium applied NIS2 in October 2024, subjecting more than 1,200 entities to penalties up to EUR 10 million (USD 10.9 million) or 2% of global revenue for non-conformance.[2]European Commission, “Network and Information Security Directive 2,” Official Journal, eur-lex.europa.eu Dutch organizations, facing a mid-2025 deadline, accelerated security-information-and-event-management (SIEM) rollouts to satisfy the directive’s 24-hour incident-notification rule. Luxembourg’s financial sector confronts overlapping requirements from NIS2 and the Digital Operational Resilience Act, elevating demand for penetration testing and vendor-risk-management platforms. The directive’s emphasis on supply-chain assurance has compelled enterprises to audit third-party security posture, expanding the market for continuous-monitoring solutions that automate questionnaire workflows.

Surge in Cyber Insurance Premium Differentials

Underwriters cut premiums by 10-15% in 2025 for firms that evidence robust controls, such as multi-factor authentication and immutable backups, while simultaneously increasing rates for firms lacking response playbooks. Insurance penetration among Dutch midsize enterprises climbed to 42%, turning policy applications into de facto security audits. Belgian carriers exclude ransomware payments unless backups are air-gapped, spurring sales of backup-as-a-service platforms. The widening 30% premium gap between protected and unprotected firms gives budget-pressed SMEs a direct financial incentive to invest in baseline controls, reinforcing the growth momentum of managed detection and response offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Certified Cybersecurity Professionals | -1.2% | Netherlands, Belgium, Luxembourg | Medium term (2-4 years) |

| High Total Cost of Ownership for Multi-Layered Stacks | -0.9% | Belgium, Luxembourg (SME-heavy markets) | Short term (≤ 2 years) |

| Fragmented SMB Budgets Limiting Uptake | -0.7% | Netherlands, Belgium | Medium term (2-4 years) |

| Growing Open-Source Tool Adoption | -0.5% | Netherlands (tech-savvy SMEs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Cybersecurity Professionals

The Netherlands logged more than 10,000 unfilled roles in 2025, delaying internal security-center build-outs and channeling demand toward MSSPs. Belgium reported 3,500 vacancies, with a notable deficit in OT-security engineers needed to safeguard industrial control systems.[3]Belgian Federal Public Service for Economy, “Digital Economy Survey 2025,” economy.fgov.be Luxembourg banks bid salaries 22% above comparable IT positions, pushing median senior-engineer pay to EUR 95,000 (USD 103,550). Language-specific gaps in Dutch- and French-speaking analysts further complicate staffing, forcing some firms to offshore monitoring and raising data-sovereignty concerns. University pipeline expansions will not meaningfully relieve the bottleneck before 2028, keeping labor pressure elevated.

High Total Cost of Ownership for Multi-Layered Security Stacks

Belgian SMEs spend upward of EUR 150,000 (USD 163,500) per year on unified stacks that combine firewall, endpoint, email, and SIEM capabilities, a share equal to 8-12% of their total IT budgets. Integration complexity inflates labor costs by another EUR 80,000-120,000 (USD 87,200-130,800), as dedicated engineers fine-tune alert thresholds and maintain interoperability. Manufacturing firms with parallel IT and OT environments effectively double hardware outlays because legacy industrial-control components cannot host modern endpoint agents. Per-user licensing models penalize enterprises with seasonal staffing patterns, prompting a pivot toward consumption-based pricing that aligns cost with actual utilization. Heightened audit expenses under the Digital Operational Resilience Act further stretch bank budgets, incentivizing vendor consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain as Outsourcing Accelerates

Managed security services are expanding at an 8.23% CAGR between 2026 and 2031, outpacing traditional solutions while still operating within a Benelux cybersecurity market size that remains solutions-heavy. Solutions held 68.38% of 2025 spend, anchored by next-generation firewalls, SIEM platforms, and endpoint-detection software deployed during initial compliance waves. Rising complexity alongside the cyber-talent gap makes 24-hour external monitoring attractive for large enterprises that need immediate containment.

Professional-services demand is brisk as companies scramble for NIS2 readiness checks and red-team exercises. Dutch banks, for example, halved mean-time-to-detect intrusions from 287 days to under 24 hours after shifting to managed detection and response contracts. Vendors now bundle assessments, remediation guidance, and compliance dashboards, creating subscription models that offer predictable OPEX. The trajectory indicates that services could exceed one-third of total spend by 2031 if current vacancy rates persist.

By Deployment Mode: Cloud Dominates and Accelerates

Cloud deployments captured 63.21% of 2025 revenue and are forecast to compound at 8.68% through 2031 as security-as-a-service becomes the default in new projects. The Benelux cybersecurity market share held by cloud grew rapidly as Dutch enterprises embraced hybrid setups that span Amazon Web Services, Microsoft Azure, and Google Cloud. Cloud-native tools such as cloud-security-posture-management and workload-protection platforms now represent the fastest-scaling sub-categories.

On-premises installations endure in sovereignty-sensitive arenas, notably Luxembourgish finance and Dutch public agencies. Industrial plants with air-gapped networks also maintain hardware appliances, illustrating that the Benelux cybersecurity market size will not become exclusively cloud-based. Still, most greenfield workloads prefer subscription models that deliver automatic rule-set updates and elastic scalability, eroding the share of perpetual-license hardware.

By End-Use Industry: Retail Surges Amid E-Commerce Threats

BFSI retained 24.82% of 2025 revenue, the largest slice of the Benelux cybersecurity market. However, retail and e-commerce is set to grow the fastest at a 9.12% CAGR to 2031 as credential-stuffing and distributed-denial-of-service attacks spike around holiday peaks. The 2024 Coolblue breach, which triggered EUR 4.2 million (USD 4.6 million) in GDPR fines, galvanized sector-wide upgrades to web-application firewalls and bot-mitigation layers.

Healthcare is also escalating spend after Belgian hospitals faced double-extortion ransomware. Industrial manufacturing deploys OT-centric security to protect legacy supervisory protocols, while energy utilities guard grid-control traffic. Although BFSI remains the largest buyer, competitive dynamics within e-commerce ensure the segment will chip away at its lead.

By End-User Enterprise Size: SMEs Embrace Security Under Insurance Pressure

Large organizations captured 68.43% of spending in 2025, yet SMEs now represent the most vibrant growth pocket, expanding at 8.53% CAGR. Cyber insurance shapes this trend by rewarding documented controls with premium cuts that reach 30%. Cloud-delivered unified-threat-management appliances offer SMEs enterprise-grade defenses minus the capital burden, narrowing the protection gap.

The Benelux cybersecurity market size tied to SME demand is likely to rise as supply-chain mandates force small vendors to evidence baseline security before signing master-service agreements with multinationals. Large enterprises will continue investing in orchestration and automation platforms, but incremental growth momentum resides with smaller businesses catching up.

Geography Analysis

The Netherlands commanded the largest national share in 2025, buoyed by the Port of Rotterdam’s OT networks and an 85% public-cloud adoption rate that drove demand for cloud-access brokers, SIEM upgrades, and zero-trust architectures. Dutch compliance urgency around the mid-2025 NIS2 deadline pushed SIEM bookings forward, while a 35% rise in ransomware incidents accelerated segmentation projects in critical-infrastructure sectors.

Belgium’s market is growing rapidly on the back of its October 2024 NIS2 rollout. Enforcement authority to levy fines up to EUR 10 million (USD 10.9 million) has spurred spending across 1,200 newly regulated entities. Antwerp’s port logistics attacks underscored OT vulnerability, catalyzing investment in industrial intrusion-detection systems. A 72% hybrid-cloud penetration rate means unified-policy solutions remain top of mind, and workforce shortages push Belgian firms toward managed services.

Luxembourg, though smaller in absolute terms, has outsized strategic weight because of its EUR 5 trillion (USD 5.45 trillion) assets-under-administration financial sector.[4]European Central Bank, “Digital Operational Resilience Act Guidelines,” bankingsupervision.europa.eu Dual compliance with NIS2 and the Digital Operational Resilience Act makes the Grand Duchy a hotspot for sovereign-cloud adoption and zero-trust network-access pilots. Salary premiums for scarce cyber talent intensify service-provider opportunities, and local data-center investments by hyperscalers reduce latency in cloud-security workloads.

Competitive Landscape

Global vendors hold an aggregate 27% share, indicating moderate concentration within the Benelux cybersecurity market. Palo Alto Networks, Cisco Systems, and Fortinet differentiate through zero-trust capabilities and SASE integrations that appeal to hybrid-cloud adopters. AI-centric platforms such as Darktrace and CrowdStrike win contracts that demand autonomous response and identity-threat detection, including Darktrace’s OT deployment at the Port of Rotterdam.

Vendor consolidation shapes strategy. CrowdStrike’s 2025 acquisition of identity specialist Preempt Security strengthened its Falcon platform against lateral-movement tactics, while Cisco absorbed multiple cloud-security startups to flesh out its SASE stack. Simultaneously, regional MSSPs such as KPN and Proximus blend vendor technologies into outcome-based subscriptions that commoditize basic monitoring functions.

White-space opportunities linger in OT security for chemical and utility plants where IT-OT convergence expertise is scarce. Startups birthed in The Hague Security Delta, notably Roseman Labs and Passguard, target niche demand for privacy-enhancing computation and decentralized identity. Consumption-based pricing models from SentinelOne and Arctic Wolf lower entry barriers for SMEs, intensifying price pressure on incumbents that depend on perpetual-license hardware.

Benelux Cybersecurity Industry Leaders

Palo Alto Networks, Inc.

Cisco Systems, Inc.

Fortinet, Inc.

Check Point Software Technologies Ltd.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Palo Alto Networks partnered with ING Bank to roll out Prisma Cloud across hybrid environments in the Netherlands and Belgium.

- December 2025: Fortinet opened a 24-hour security-operations center in Brussels staffed by 45 analysts.

- November 2025: Darktrace secured a EUR 8.5 million (USD 9.3 million) OT-security contract with the Port of Rotterdam.

- October 2025: CrowdStrike acquired Netherlands-based Preempt Security for USD 96 million.

Benelux Cybersecurity Market Report Scope

The Cybersecurity Market encompasses global spending on solutions, software, and services designed to protect digital infrastructure, data, and operations across all industries, including cloud, network, endpoint, and application security; it includes enterprise, government, and SME segments but excludes physical security and pure consulting-only services, with the market evolving rapidly toward AI-driven automation, platform consolidation, and regulatory-driven transformation.

The Benelux Cybersecurity Market Report is Segmented by Offering (Solutions [Application Security, Cloud Security, Data Security, Identity and Access Management, Infrastructure Protection, Integrated Risk Management, Network Security, End Point Security], Services [Professional Services, Managed Services]), Deployment Mode (On-Premises, Cloud), End-Use Industry (IT and Telecom, BFSI, Healthcare, Industrial Manufacturing, Retail and E-commerce, Energy and Utilities, Aerospace, Military and Defense, Other End-Use Industries), and End-User Enterprise Size (Large Enterprises, Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End Point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premises |

| Cloud |

By End-use Industry

| IT and Telecom |

| BFSI |

| Healthcare |

| Industrial Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Aerospace, Military and Defense |

| Other End-use Industries |

By End-User Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End Point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| By End-use Industry | IT and Telecom | |

| BFSI | ||

| Healthcare | ||

| Industrial Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Aerospace, Military and Defense | ||

| Other End-use Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the projected value of cybersecurity spending in Benelux by 2031?

Spending is forecast to reach USD 6.71 billion by 2031.

How fast is cloud-based security adoption growing in the region?

Cloud deployments are advancing at an 8.68% CAGR between 2026 and 2031 as hybrid architectures multiply.

Which industry vertical shows the quickest cybersecurity growth?

Retail and e-commerce leads with a 9.12% CAGR through 2031, driven by bot attacks and payment fraud.

Why are SMEs increasing their cybersecurity budgets?

Insurers reward documented controls with premium cuts up to 30%, making security spending financially attractive.

What regulation exerts the strongest near-term influence on Benelux security investments?

The EU’s NIS2 Directive, fully enforceable between 2024 and 2025, mandates stricter controls and incident reporting across essential sectors.

Page last updated on: