Middle East Crime And Combat Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

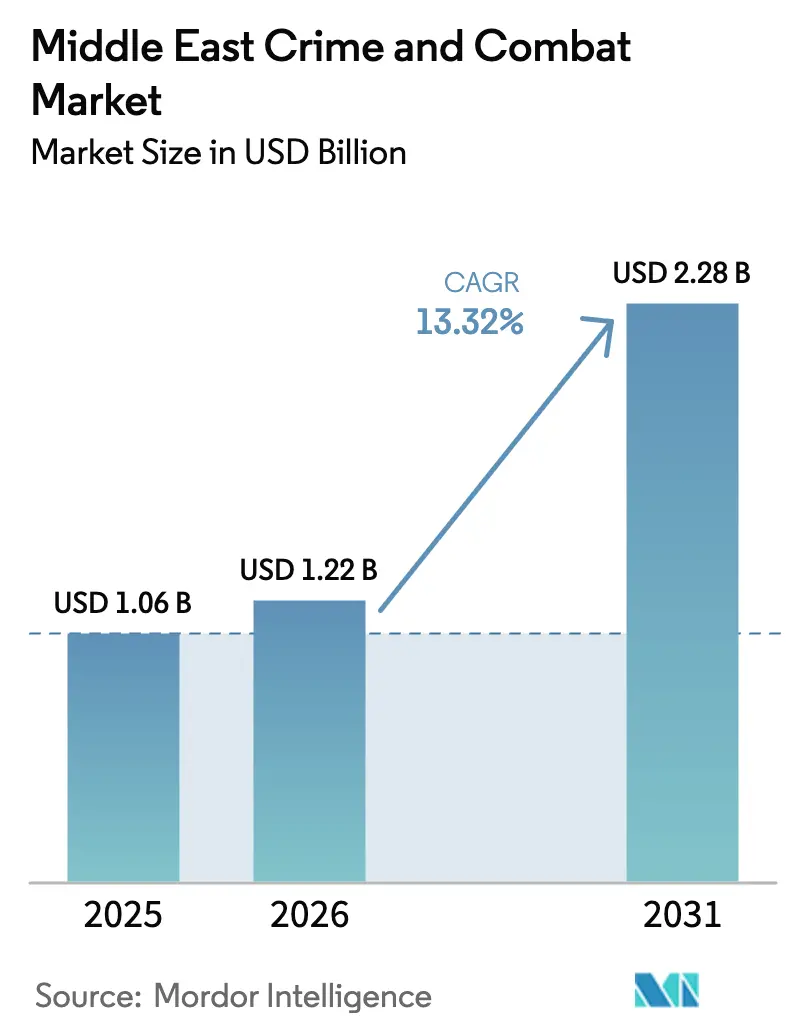

| Base Year Market Size (2025) | USD 1.06 Billion |

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 2.28 Billion |

| Growth Rate (2026 - 2031) | 13.32% CAGR |

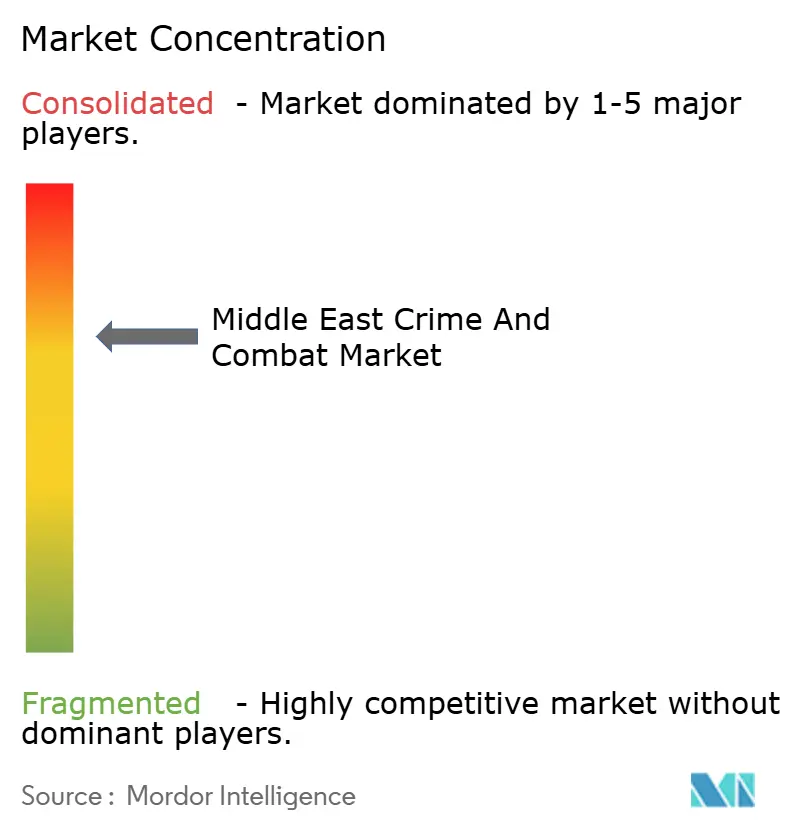

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Crime And Combat Market Analysis by Mordor Intelligence

The Middle East crime and combat market size is projected to expand from USD 1.06 billion in 2025 and USD 1.22 billion in 2026 to USD 2.28 billion by 2031, registering a CAGR of 13.3% between 2026 and 2031. Surging instant-payment volumes, more frequent Financial Action Task Force (FATF) mutual-evaluation cycles, and mandatory electronic know-your-customer (e-KYC) rollouts in the United Arab Emirates (UAE) and Kingdom of Saudi Arabia (KSA) are accelerating spending on automated financial-crime controls. Regional banks are replacing rule-based engines with machine-learning models that score risk in real time, while fintech adopt cloud-native compliance suites to satisfy the same anti-money-laundering (AML) standards as incumbents. Sovereign-wealth funds and trade-finance hubs in the UAE and KSA are catalysing demand for systems that fuse sanctions intelligence with cross-border cargo data. Explainable-artificial-intelligence (AI) dashboards have become must-have features for boards and supervisors because they translate complex model logic into plain Arabic and English narratives. These forces together position the Middle East crime and combat market as one of the world’s fastest-growing compliance-technology arenas.

Key Report Takeaways

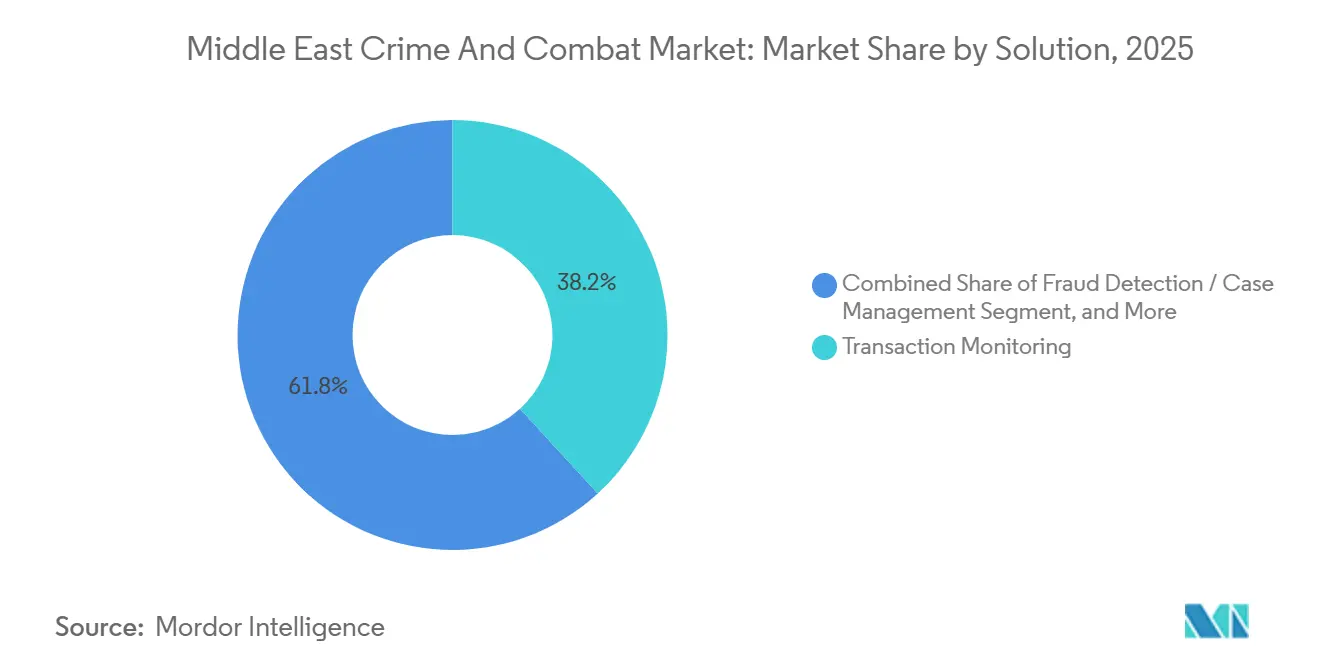

- By solution, transaction monitoring led with 38.19% of the Middle East crime and combat market share in 2025, while fraud detection and case-management tools are advancing at a 13.98% CAGR through 2031.

- By deployment mode, on-premises infrastructure accounted for 56.71% of the Middle East crime and combat market size in 2025, whereas cloud platforms are projected to rise at 14.04% between 2026 and 2031.

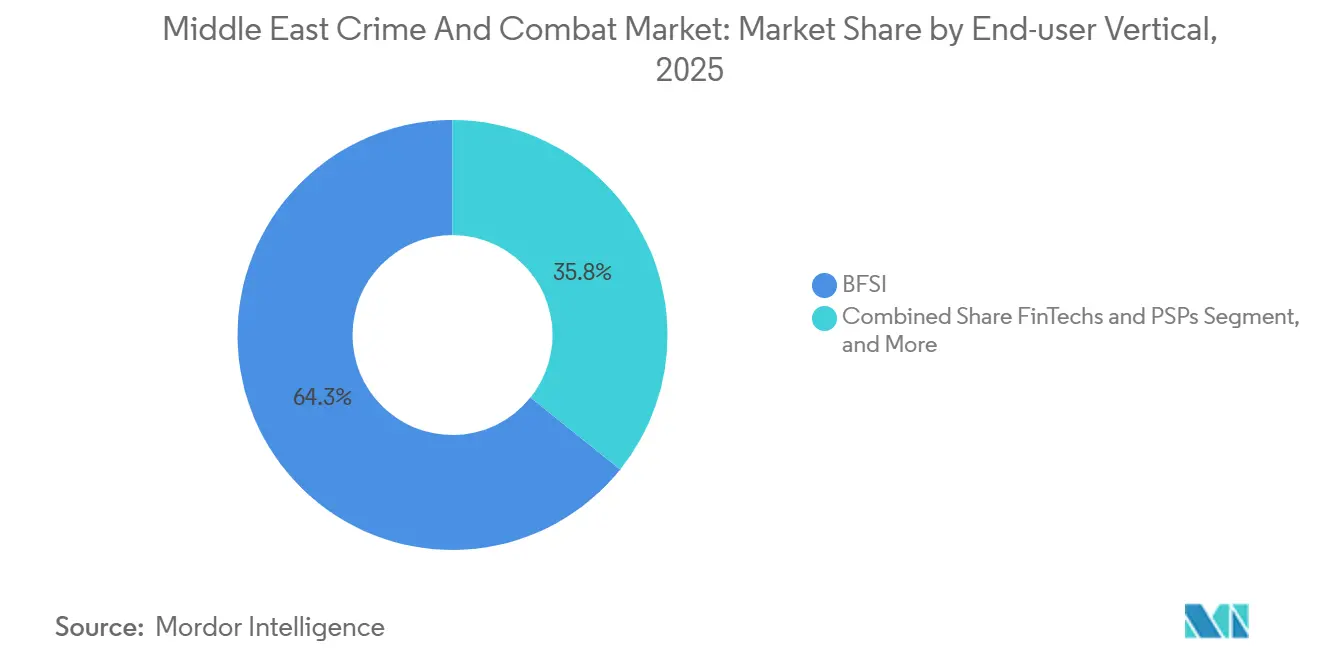

- By end-user vertical, banking, financial services, and insurance (BFSI) held 64.25% revenue share of the Middle East crime and combat market in 2025; fintech and payment service providers are expanding at a 13.58% CAGR to 2031.

- By application, AML dominated with 49.29% share in 2025; fraud and cyber-crime detection is the fastest growing at 13.71% through 2031.

- Geographically, the UAE controlled 27.78% of the Middle East crime and combat market in 2025, while Qatar is forecast to log the quickest 14.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Crime And Combat Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Digital-Payments Penetration | +2.80% | United Arab Emirates, Kingdom of Saudi Arabia, Qatar, Egypt | Medium term (2-4 years) |

| Intensifying GCC Cross-Border Trade Surveillance | +2.30% | United Arab Emirates, Kingdom of Saudi Arabia, Kuwait, Bahrain, Oman | Short term (≤ 2 years) |

| Mandatory e-KYC Frameworks (UAE, KSA) | +2.10% | United Arab Emirates, Kingdom of Saudi Arabia | Short term (≤ 2 years) |

| AI-Driven Anomaly Detection Adoption in Tier-1 Banks | +1.90% | United Arab Emirates, Kingdom of Saudi Arabia, Qatar | Medium term (2-4 years) |

| FATF Mutual-Evaluation Pressures Prompting Compliance Pre-Investment | +1.70% | Global, with concentration in United Arab Emirates, Kingdom of Saudi Arabia, Kuwait, Oman | Long term (≥ 4 years) |

| Generative-AI Explainability Toolkits Slashing False Positives | +1.50% | United Arab Emirates, Kingdom of Saudi Arabia, Qatar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Digital Payments Penetration

Digital payment volumes across Gulf Cooperation Council (GCC) economies reached USD 227 billion in 2025 and are expected to exceed USD 360 billion by 2030.[1]PwC Middle East, “GCC Payments Study 2026,” pwc.com Instant-payment rails in the UAE and KSA settle peer-to-peer transfers in seconds, compressing review windows and compelling banks to embed machine-learning engines that score risk on the fly. Migrant-worker remittances from the GCC to South Asia surpassed USD 50 billion in 2025, bringing informal channels under regulatory purview. Fintechs serving these corridors now carry mandatory e-KYC obligations, driving a scramble for cloud-based case-management suites able to absorb unpredictable traffic spikes. The sheer scale and immediacy of digital payments, therefore, power sustained growth across the Middle East crime and combat market.

Intensifying GCC Cross Border Trade Surveillance

GCC merchandise trade with Asia, Africa and Europe totalled USD 1.2 trillion in 2025, and customs agencies have begun piping trade-finance data into financial-intelligence units to catch invoice fraud and sanctions evasion.[2]Gulf Cooperation Council Secretariat, “Annual Trade Statistics 2025,” gcc-sg.org The UAE’s blockchain pilot links bills of lading to beneficial-ownership registries, exposing shell companies in near real time. KSA’s 2025 pre-arrival declaration rule creates structured container data that compliance engines parse for anomalies such as serial shipments of high-value electronics to low-risk jurisdictions. These innovations demand analytics suites that reconcile correspondent-banking messages with cargo movements, a capability absent in legacy AML tools, and this requirement is a key accelerant for the Middle East crime and combat market.

Mandatory e-KYC Frameworks in UAE and KSA

The UAE Digital Identity Authority directed all financial institutions to adopt national digital-ID verification by March 2025, while KSA’s National Information Center launched a centralized e-KYC utility in June 2025.[3]Central Bank of UAE, “Guidelines on Cloud Adoption,” centralbank.ae These mandates streamline onboarding for trustworthy customers but impose granular audit-trail duties. The KSA Capital Market Authority fined three brokerages SAR 12 million (USD 3.2 million) in August 2025 for outdated customer-risk profiles. Banks have responded by procuring API-enabled due-diligence engines that call government databases in real time, elevating cloud deployment to a strategic priority and propelling additional spend inside the Middle East crime and combat market.

AI-Driven Anomaly Detection in Tier-1 Banks

Tier-1 banks in the UAE and KSA introduced machine-learning transaction-monitoring models 40% faster in 2025 than in 2024. Emirates NBD and Saudi National Bank piloted graph-neural-network architectures that map intricate relationships among account holders, beneficiaries and shell entities, exposing layering schemes that evade threshold triggers. The UAE central bank now permits reliance on AI-generated risk scores if models pass annual validation and bilingual explainability reports are archived for seven years. Generative-AI modules that verbalize model logic in Arabic and English sharply reduce false positives, expanding analyst capacity and underpinning the rapid ascent of the Middle East crime and combat market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Arabic-Speaking Compliance Analysts | -1.60% | United Arab Emirates, Kingdom of Saudi Arabia, Qatar, Egypt, Kuwait | Medium term (2-4 years) |

| Fragmented Legacy Core-Banking Stacks | -1.30% | Egypt, Kuwait, Bahrain, Oman, Rest of Middle East | Long term (≥ 4 years) |

| High On-Premise System Switching Costs | -0.90% | Kingdom of Saudi Arabia, United Arab Emirates, Kuwait | Short term (≤ 2 years) |

| Carbon-Border Adjustment Mechanisms Extending AML Scope to ESG Data | -0.70% | United Arab Emirates, Kingdom of Saudi Arabia, Qatar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Arabic-Speaking Compliance Analysts

Vacancy rates for bilingual compliance analysts hit 35% in 2025, forcing banks to lean on expatriates who often miss regional nuances within transaction narratives. Universities in the UAE and KSA conferred fewer than 800 dual financial-crime and Arabic-linguistics qualifications in 2025 against market demand for more than 2,500 roles. Regulatory filing deadlines in Egypt and Kuwait require Arabic reports within 48 hours, stretching thinly staffed teams. Vendors are embedding Arabic natural-language models, but precision on Egyptian and Gulf dialects remains below 80%, reinscribing manual bottlenecks and tempering the Middle East crime and combat market’s attainable growth rate.

Fragmented Legacy Core-Banking Stacks

Banks in Egypt, Kuwait, Bahrain and Oman run core platforms installed between 2005 and 2015 that silo customer data by product, impeding real-time sanctions screening. Upgrading to API-driven cores takes 18-36 months and more than USD 50 million for mid-size lenders, an outlay boards hesitate to approve without regulatory compulsion. Hybrid patches introduce cyber-risk and operational complexity, slowing migration to modern cloud environments and dampening short-term growth prospects inside the Middle East crime and combat market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Transaction Monitoring Anchors Demand Amid Fraud Detection Surges

Transaction monitoring systems held 38.19% of the Middle East crime and combat market share in 2025, reflecting regulatory insistence that every instant-payment and trade-finance instruction be screened for sanctions, structuring, and terrorist financing. The Middle East crime and combat market size allocated to fraud detection and case-management tools is forecast to jump ata 13.98% CAGR through 2031 as synthetic-identity rings exploit digital wallets. Integrated dashboards that let analysts switch between AML and fraud typologies are in favour because they suppress alert backlogs and eliminate data duplication.

Oracle Financial Services Software and Fiserv leveraged long-standing GCC bank contracts to upsell fraud modules that reuse core customer records, whereas AI-native challengers such as Feedzai and Comply Advantage compress go-lives from 12 to 6 months by shipping pre-trained models. Compliance-reporting suites are growing briskly after the Qatar Central Bank mandated XML suspicious-transaction filings in January 2026. Auditing and analytics platforms that track model bias and governance have become board-level imperatives, cementing their foothold in the expanding Middle East crime and combat market.

By Deployment Mode: Cloud Gains Momentum Despite On-Premises Inertia

On-premises estates retained 56.71% of the Middle East crime and combat market size in 2025 owing to data-residency rules in the UAE and KSA and the sunk cost of legacy hardware. Cloud subscriptions, however, are on course to log a 14.04% CAGR between 2026 and 2031 as hyperscale data centers in Riyadh, Jeddah, Abu Dhabi and Dubai satisfy sovereignty mandates and provide elastic compute for model training.

The Central Bank of the UAE’s April 2025 guidance approved public-cloud compliance workloads if encryption, access controls and breach notifications match the National Electronic Security Authority framework. Large lenders are testing hybrid blueprints that keep personally identifiable data on-premises while off-loading heavy analytics tasks to the cloud, whereas fintech leap directly to cloud-native stacks to avoid capital expenditure. Vendors differentiate on multi-cloud orchestration, real-time data masking and low-latency regional zones, tilting future Middle East crime and combat market share in favour of subscription models.

By End-User Vertical: BFSI Dominance Persists as FinTech’s Accelerate

BFSI institutions generated 64.25% of 2025 revenue owing to high transaction volumes and stringent supervisory expectations. The Middle East crime and combat market size tied to BFSI continues to rise as tier-1 banks retrofit instant-payment gateways with AI-based screening and hire more investigators ahead of FATF assessments.

FinTech’s and payment service providers are projected to grow at a 13.58% CAGR through 2031 after the UAE Securities and Commodities Authority mandated travel-rule compliance for virtual-asset firms by December 2026. Government and law-enforcement agencies purchase platforms at a measured pace bound by budgets, while designated non-financial businesses and professions remain an under-penetrated segment that regulators increasingly target, offering untapped upside for the Middle East crime and combat market.

By Application: AML Leads While Fraud Detection Converges

AML engines held 49.29% of 2025 spend, underpinned by mature sanctions and suspicious-activity reporting workflows. The Middle East crime and combat market share for fraud and cybercrime detection is set to outstrip all categories at 13.71% CAGR through 2031 as social-engineering scams abuse instant-payment rails.

Counter-terrorist-financing analytics remain key for regional security agencies, while regulatory and tax-reporting suites answer Foreign Account Tax Compliance Act and Common Reporting Standard needs. The Qatar Financial Centre’s March 2025 rule compelling unified crime-risk assessments nudges buyers toward platforms that correlate AML, fraud, sanctions and cyber alerts in one queue, enlarging solution cross-sell potential within the Middle East crime and combat market.

Geography Analysis

The UAE held 27.78% of the Middle East crime and combat market in 2025 thanks to Dubai’s trade corridors, Abu Dhabi’s sovereign-wealth oversight and proactive regulators. Continuous commerce with more than 200 jurisdictions pushes firms to fuse sanctions data with cargo manifests. The central bank’s January 2026 AI model-validation consultation adds urgency around explainability, prompting several institutions to budget for platform upgrades this year.

KSA ranks second and remains a powerhouse of instant-payment innovation under Vision 2030. Riyadh’s real-time rail swells message volumes that legacy alert engines cannot absorb, driving adoption of graph-based anomaly detection and cloud elasticity. Qatar, meanwhile, is set to grow fastest at a 14.22% CAGR through 2031 after its 2025 directive requiring 24-hour anomaly detection across all licensees.

Egypt’s February 2025 rule that halved the reporting threshold to EGP 50,000 (USD 1,600) doubled alert totals overnight, sparking a race for automated case-management. Kuwait, Bahrain and Oman collectively form an important frontier as national champions modernize ahead of mutual-evaluation reviews. Bahrain’s fintech sandbox hastens cloud retch uptake, whereas Oman’s diversification pull drives trade-finance surveillance. Iraq, Jordan and Lebanon remain small due to macro-instability, but multinationals present there deploy enterprise suites to maintain baseline coverage, gradually expanding the overall Middle East crime and combat market.

Competitive Landscape

The five largest vendors SAS Institute, NICE Actimize, FICO, Oracle Financial Services Software and Fiserv controlled roughly 55% of 2025 bookings, giving the Middle East crime and combat market a moderate concentration profile. Their rule libraries, multilanguage interfaces and decade-long GCC references grant notable stickiness.

Challengers such as Feedzai, ComplyAdvantage, ThetaRay and Napier AI leverage pre-trained Arabic models, subscription pricing and six-month deployment promises to win fintech and mid-tier bank mandates. East Nets heightens competition by localizing user interfaces and linking directly to GCC real-time rails. Hyperscale cloud providers Amazon Web Services, Microsoft and Google Cloud bundle compliance-as-a-service with infrastructure contracts, squeezing traditional maintenance margins.

Vendors are racing toward explainable-AI supremacy and environmental, social and governance data convergence. NICE Actimize opened a Dubai hub with 50 consultants to shepherd cloud migrations, and Oracle spun up a Riyadh cloud instance used by 12 Saudi banks within six months. Carbon-border adjustment mechanisms that knit AML with supply-chain emissions monitoring create a new adjacency favouring firms able to integrate environmental intelligence. Competitive balance therefore tilts gradually toward AI-first specialists, maintaining healthy rivalry across the Middle East crime and combat market.

Middle East Crime And Combat Industry Leaders

SAS Institute Inc.

NICE Actimize (NICE Ltd)

Experian Information Solutions Inc. (Experian Ltd)

Symphony Innovation LLC

Fair Isaac Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: RegTech closed a USD 12 million Turkish bank deal for AI-based AML/KYC suites.

- April 2025: Morocco’s PayTic secured USD 4.4 million to scale compliance SaaS across MEA.

- March 2025: Oracle launched AI agents that cut manual investigations by 60% and elevated detection accuracy by 40% across several Gulf banks.

- February 2025: Tata Consultancy Services reported USD 7.54 billion Q3 FY25 revenue, with Middle East growth of 15% driven by AI and cybersecurity demand.

- January 2025: Experian’s 2024 Future of Fraud Forecast highlighted generative-AI fraud, noting USD 12 billion in client savings during 2024.

Middle East Crime And Combat Market Report Scope

The Middle East Crime and Combat Market Report is Segmented by Solution (Know-Your-Customer Systems, Transaction Monitoring, Compliance Reporting Suites, Auditing and Analytics, Fraud Detection and Case Management), Deployment Mode (Cloud, On-premises), End-user Vertical (BFSI, Government and Law-Enforcement Agencies, FinTechs and PSPs, DNFBPs), Application (AML, CTF, Fraud and Cyber-Crime Detection, Regulatory and Tax Compliance), and Geography (UAE, KSA, Qatar, Egypt, Kuwait, Bahrain, and Oman, Rest of Middle East). Market Forecasts are Provided in Terms of Value (USD).

| Know-Your-Customer (KYC) Systems |

| Transaction Monitoring |

| Compliance Reporting Suites |

| Auditing and Analytics |

| Fraud Detection / Case Management |

| Cloud |

| On-premises |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Law-Enforcement Agencies |

| FinTechs and Payment Service Providers |

| Designated Non-Financial Businesses and Professions |

| Anti-Money Laundering (AML) |

| Counter-Terrorist Financing (CTF) |

| Fraud and Cyber-Crime Detection |

| Regulatory and Tax Compliance (FATCA, CRS) |

| United Arab Emirates |

| Kingdom of Saudi Arabia |

| Qatar |

| Egypt |

| Kuwait |

| Bahrain and Oman |

| Rest of Middle East |

| By Solution | Know-Your-Customer (KYC) Systems |

| Transaction Monitoring | |

| Compliance Reporting Suites | |

| Auditing and Analytics | |

| Fraud Detection / Case Management | |

| By Deployment Mode | Cloud |

| On-premises | |

| By End-user Vertical | Banking, Financial Services and Insurance (BFSI) |

| Government and Law-Enforcement Agencies | |

| FinTechs and Payment Service Providers | |

| Designated Non-Financial Businesses and Professions | |

| By Application | Anti-Money Laundering (AML) |

| Counter-Terrorist Financing (CTF) | |

| Fraud and Cyber-Crime Detection | |

| Regulatory and Tax Compliance (FATCA, CRS) | |

| By Geography | United Arab Emirates |

| Kingdom of Saudi Arabia | |

| Qatar | |

| Egypt | |

| Kuwait | |

| Bahrain and Oman | |

| Rest of Middle East |

Key Questions Answered in the Report

How quickly is compliance spending expanding across GCC countries?

The Middle East crime and combat market is growing at a 13.3% CAGR between 2026 and 2031 as instant-payment traffic, e-KYC mandates and FATF reviews intensify automation demand.

Which technology category currently generates the most revenue?

Transaction monitoring holds 38.19% of 2025 billings, reflecting regulators reliance on automated sanctions and suspicious-activity detection.

Why are fintechs ramping up compliance budgets?

Fintechs and payment service providers must now meet the same AML and counter-terrorist-financing rules as banks, propelling their spend at a 13.58% CAGR through 2031.

What makes Qatar the region's fastest-growing market?

A 2025 Qatar Central Bank directive requires institutions to flag unusual patterns within 24 hours, accelerating technology adoption and fueling a 14.22% forecast CAGR.

How are vendors reducing false positives in Arabic narratives?

Explainable-AI modules translate model logic into Arabic and English, and pre-trained natural-language models tuned to Gulf dialects cut false positives and free analyst time.

Page last updated on: