Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

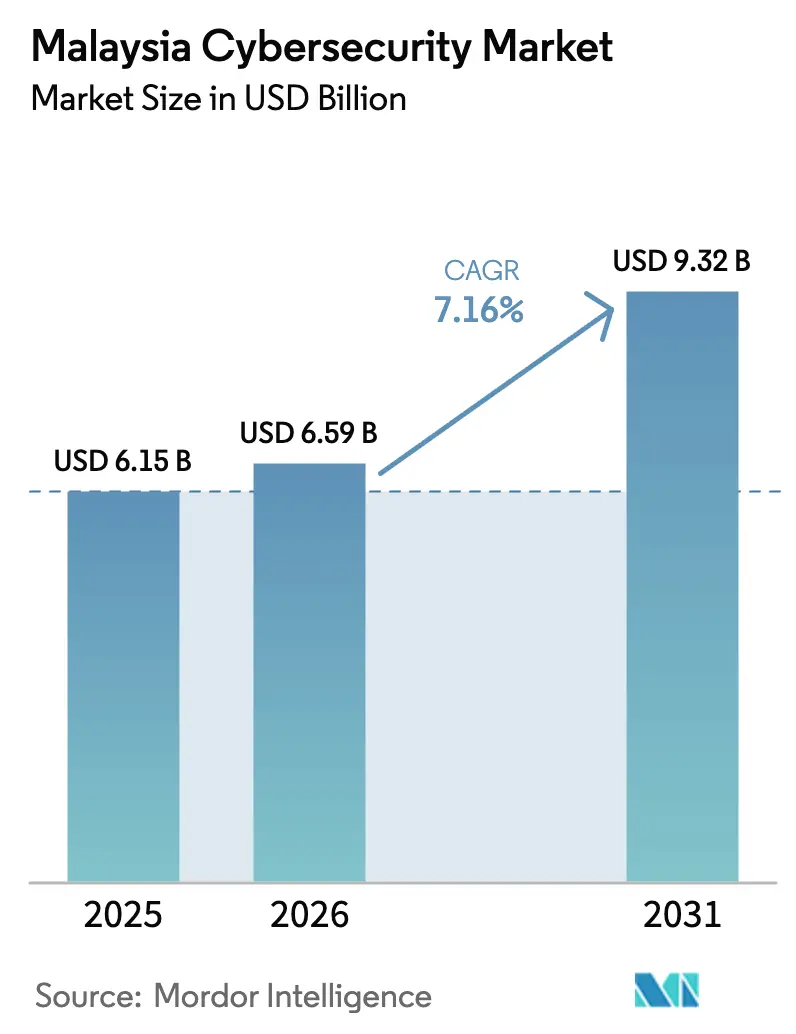

| Base Year Market Size (2025) | USD 6.15 Billion |

| Market Size (2026) | USD 6.59 Billion |

| Market Size (2031) | USD 9.32 Billion |

| Growth Rate (2026 - 2031) | 7.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Cybersecurity Market Analysis by Mordor Intelligence

The Malaysia cybersecurity market size is expected to grow from USD 6.15 billion in 2025 to USD 6.59 billion in 2026 and is forecast to reach USD 9.32 billion by 2031 at 7.16% CAGR over 2026-2031. This low-double-digit trajectory positions the Malaysia cybersecurity market among the faster-growing digital-infrastructure segments within the country’s wider ICT ecosystem. Cloud-first mandates, strict licensing under the Cyber Security Act 2024, and the monetized cost of data breaches are each propelling sustained demand. Large enterprises are broadening existing controls into zero-trust programs, while small and medium enterprises are starting first-time deployments through subscription services that lower upfront costs. Parallel investments in 5G edge networks, hyperscale data centers, and operational-technology modernization further anchor a long runway for the Malaysia cybersecurity market.

Key Report Takeaways

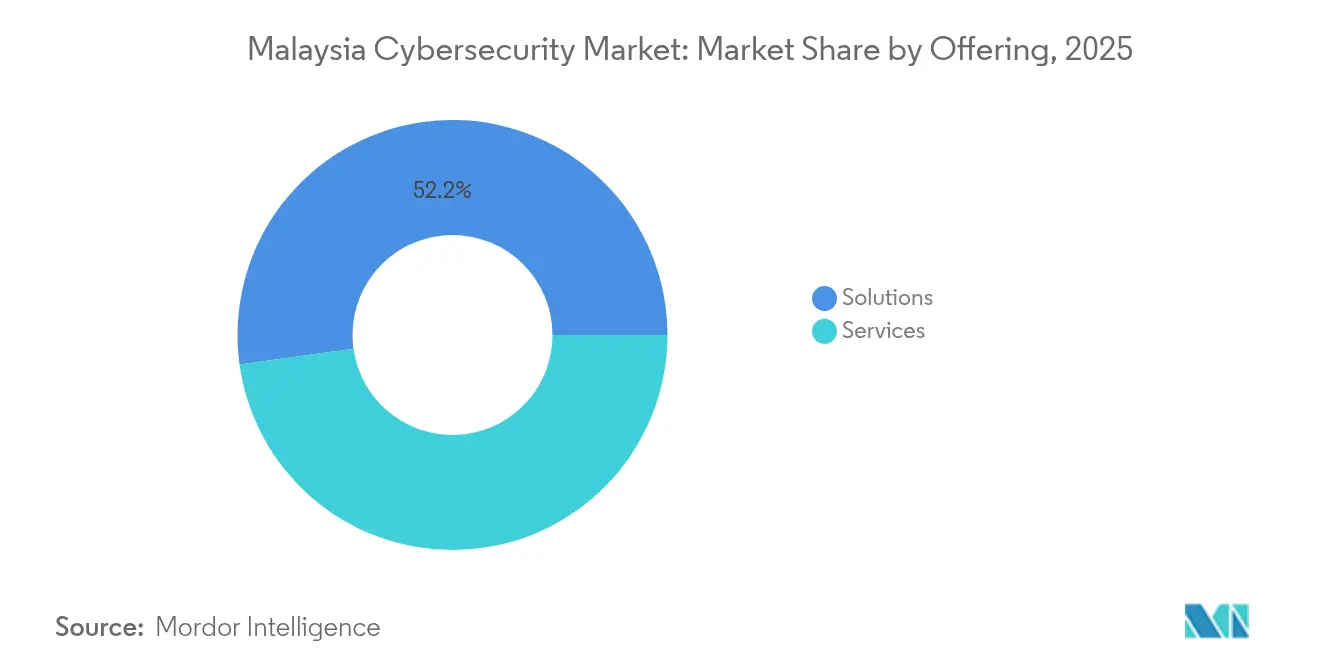

- By offering, solutions commanded 52.20% of the Malaysia cybersecurity market share in 2025, while services are projected to advance at a 7.42% CAGR through 2031.

- By deployment mode, on-premise held 52.85% share of the Malaysia cybersecurity market size in 2025 and cloud deployments are rising at an 8.05% CAGR to 2031.

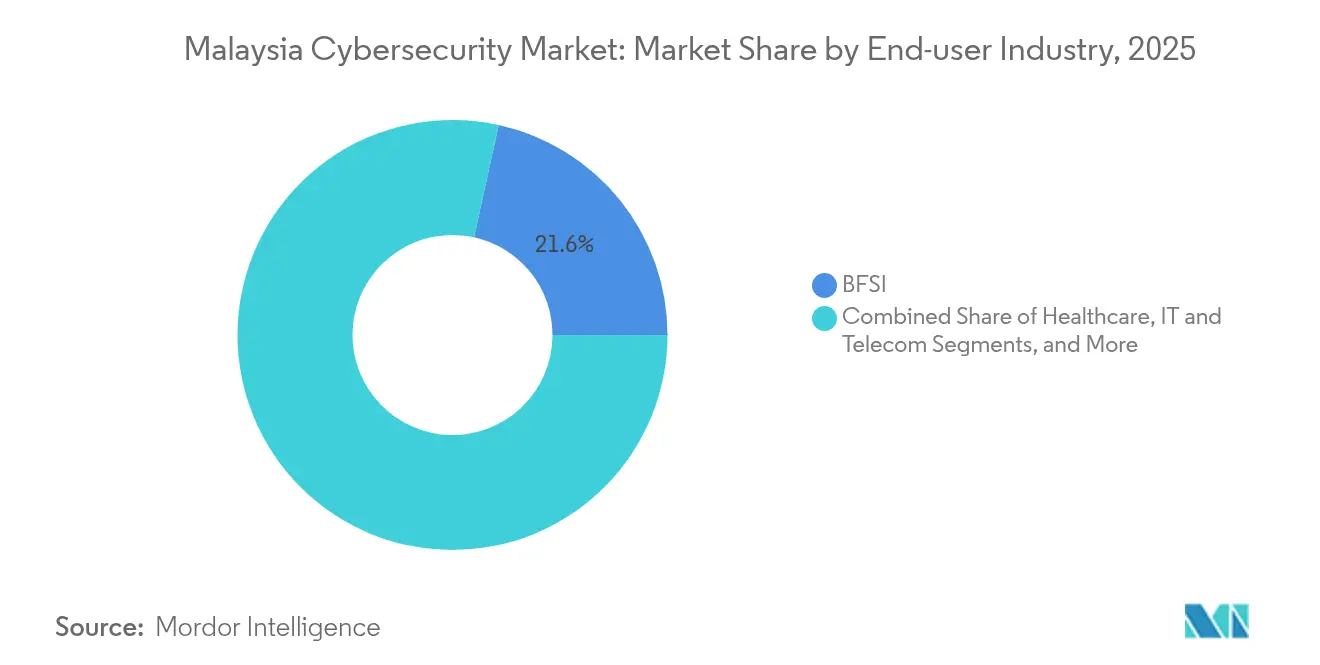

- By end-user industry, BFSI generated 21.55% revenue share in 2025; healthcare is forecast to grow at an 8.46% CAGR during 2026-2031.

- By end-user enterprise size, large enterprises controlled 70.80% of 2025 spending, whereas SMEs are set to expand at a 8.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Roll-out of Malaysia’s Cloud-First Strategy Propelling Public-Sector Cloud Security Spending | +2.10% | National; Kuala Lumpur, Cyberjaya | Short term (≤ 2 years) |

| Cyber Security Act 2024 Licensing and Mandatory NCII Compliance Fuelling Vendor Demand | +2.80% | National | Medium term (2-4 years) |

| Data-Centre Boom in Johor Bahru Elevating Perimeter and OT Security Investments | +1.70% | Johor Bahru; spill-over to Klang Valley | Medium term (2-4 years) |

| 5G Coverage ≥ 97 % Driving Mobile Core and Edge Security Upgrades | +1.50% | National | Short term (≤ 2 years) |

| USD 12.2 bn Economic Losses From Breaches Raising Boardroom Budgets | +2.30% | National; financial hubs | Short term (≤ 2 years) |

| National Goal of 25 000 Cyber Defenders Boosting Consulting and Training Spend | +1.40% | National; education centres | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Roll-out of Malaysia’s Cloud-First Strategy Propelling Public-Sector Cloud Security Spending

Malaysia’s accelerated cloud-first strategy is redirecting government spending toward cloud-native defenses such as cloud access security brokers and workload-protection platforms. Ministries now integrate classification, encryption, and continuous monitoring into every application-migration plan, lifting baseline demand for advisory and managed services. Public-sector visibility into early success stories is encouraging financial institutions and telecom carriers to adopt similar architectures, creating a multiplier effect across the Malaysia cybersecurity market. System integrators have redesigned portfolios around shared-responsibility models, bundling consulting, deployment, and managed detection under single contracts. Collectively, these changes translate to a structural uplift in addressable spending rather than a one-time spike.

Cyber Security Act 2024 Licensing and Mandatory NCII Compliance Fuelling Vendor Demand

The Cyber Security Act 2024 enforces mandatory licensing for penetration testing, security-operations, and other core services, while critical-infrastructure operators must observe sector-specific codes of practice. Organizations have responded by elevating compliance to board-level priority and retaining external auditors to align controls with the new legal baseline. Providers that secured early licences gained a measurable sales advantage because enterprises prefer pre-qualified partners to avoid regulatory missteps. The act also formalized incident-reporting timelines, spurring demand for real-time detection tools and threat-intelligence integrations. Together, these shifts embed recurring compliance obligations into IT budgets, sustaining momentum in the Malaysia cybersecurity market size.

Data-Centre Boom in Johor Bahru Elevating Perimeter and OT Security Investments

Johor Bahru is doubling data-center capacity from 1.3 GW to 2.7 GW by 2027, attracting investments from hyperscalers such as Google, Microsoft, and Amazon. The dense concentration of assets requires layered physical, network, and OT security, with anomaly-detection platforms and advanced biometrics leading procurement lists. Local authorities prioritize secure power and connectivity corridors, incentivizing operators to adopt integrated threat-monitoring consoles that correlate physical and cyber events in one dashboard. Growth in this corridor reverberates to service hubs in Kuala Lumpur, where MSSPs provide remote SOC coverage for regional facilities. The continuous construction cycle therefore offers multi-year revenue visibility for hardware vendors, integrators, and managed providers engaged in the Malaysia cybersecurity market.

5G Coverage ≥ 97 % Driving Mobile Core and Edge Security Upgrades

Digital Nasional Berhad’s 97% population coverage enables average mobile download speeds near 380 Mbps, but the distributed architecture stretches traditional perimeter controls. Telecommunications operators are rolling out zero-trust segmentation, micro-gateway firewalls, and API-security layers across network slices. Edge nodes process sensitive workloads, prompting real-time analytics and encryption at the point of data creation. Device suppliers must now comply with strict secure-coding guidelines to protect the expanded attack plane. Upstream, financial-services and gaming platforms integrate carrier–grade signaling-threat feeds into their own monitoring stacks, extending the opportunity set for the Malaysia cybersecurity market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Shortage of Senior Security Architects Inflating Project Timelines and Costs | -1.9% | National; highest in Kuala Lumpur | Medium term (2-4 years) |

| SME Budget Constraints Owing to Legacy CAPEX-heavy IT Footprints | -1.2% | National; stronger in secondary cities | Long term (≥ 4 years) |

| Fragmented Cross-border Data-Sovereignty Rules Slowing Cloud Migrations | −0.9% | National | Medium term (2-4 years) |

| Low Multi-factor-Auth Adoption Outside BFSI Heightening Residual Risk | −0.8% | Peninsular industrial belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Senior Security Architects Inflating Project Timelines and Costs

Complex cloud migrations stall because experienced architects remain scarce, extending project timelines by 37% and boosting labor costs by more than one-quarter [1]Nucamp, “Malaysia Cyber Talent Salary Survey 2024,” nucamp.co. The scarcity inflates bids for large transformation contracts, squeezing corporate budgets and delaying key milestones. Organizations counter by outsourcing architecture to MSSPs or importing expertise from regional hubs, but long visa lead times cap near-term relief. Vendor roadmaps now include low-code policy engines and reference architectures that cut design hours, yet hands-on oversight remains indispensable for regulated workloads. Talent constraints therefore act as a persistent drag on the Malaysia cybersecurity market CAGR.

SME Budget Constraints Owing to Legacy CAPEX-heavy IT Footprints

SMEs devote up to 85% of technology budgets to maintain on-premise hardware, leaving little capacity for preventive controls. Financing options specific to security remain limited, and cyber-insurance uptake is low, restricting alternatives for risk transfer. Breach statistics show SMEs suffer more incidents per endpoint than large peers, yet many owners underestimate downstream liability from supply-chain attacks. Government grants cover baseline assessments, but multi-year subscription costs still deter comprehensive adoption. Unless credit facilities improve, the SME cohort will continue to lag, trimming potential upside in the Malaysia cybersecurity market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Shifting Emphasis Toward Services

Solutions maintained 52.20% share of the Malaysia cybersecurity market in 2025, led by network and cloud-security suites that protect hybrid environments. However, services are forecast to outpace solutions at a 7.42% CAGR through 2031 as enterprises look for always-on expertise. Higher detection accuracy, round-the-clock monitoring, and built-in compliance dashboards position MSSPs as strategic partners rather than tactical suppliers. Pricing models based on monthly active assets lower entry barriers for mid-tier firms. Local providers leverage regulatory familiarity to capture contracts tied to the Cyber Security Act, while global vendors package orchestration platforms that unify alerts across point tools. Convergence of advisory, deployment, and MDR services brings value propositions beyond technology resale, solidifying service-led growth in the Malaysia cybersecurity market.

The solutions portfolio nevertheless remains critical for organizations with strict data-residency rules. Appliance refresh cycles in BFSI and utilities sustain revenue for firewall, intrusion-prevention, and secure-email gateways. New-generation SIEM platforms incorporate behavioral analytics and automation to offset talent scarcity, aligning product innovation with national skills-development goals. Vendors bundle perpetual licenses with cloud-delivered analytics to bridge on-premise controls and SaaS visibility. Co-delivery with local integrators accelerates time to value, reflecting the collaborative nature of the Malaysia cybersecurity market.

By Deployment Mode: Cloud Gains Pace While On-Premise Holds Majority

On-premise systems accounted for 52.85% of the Malaysia cybersecurity market size in 2025 because legacy workloads and data-sovereignty mandates still dominate in banking and public service. Hardware refreshes in these sectors provide a stable base for appliance vendors. Yet cloud deployments are expanding at an 8.05% CAGR through 2031, outstripping on-premise upgrades. Consumption-based pricing, continuous feature releases, and AI-driven analytics make cloud controls appealing for institutions pursuing digital-first strategies. Shared-responsibility frameworks encourage enterprises to off-load maintenance to specialized providers, supporting long-term adoption in the Malaysia cybersecurity market.

Vendor roadmaps include data-localization nodes within Malaysia to reassure regulated customers. Over time, improvements in sovereign-cloud platforms may erode the remaining resistance, but hardware refreshes tied to industrial-control networks ensure a continuing market for on-premise gear.

By End-User Industry: Healthcare Accelerates Under Data-Privacy Pressure

The BFSI sector retained 21.55% share of the Malaysia cybersecurity market in 2025 as regulators enforced stringent risk-management frameworks. Banks deploy behavioral-biometrics and secure-software-development pipelines to counter advanced fraud, ensuring continued wallet share. Interbank clearing modernization and open-banking APIs keep financial institutions reliant on multi-layer controls and third-party-risk platforms, buttressing stable demand.

Healthcare is projected to rise at an 8.46% CAGR through 2031, the fastest among verticals, as electronic medical-record expansion and connected devices increase exposure. The Personal Data Protection Amendment Bill 2024 introduces mandatory breach notifications with elevated fines, compelling hospitals to adopt encryption, micro-segmentation, and cyber-resilience testing . Telemedicine platforms integrate identity-verification and secure-video APIs, pulling additional spend. Cloud adoption within public-health agencies accelerates workload migration and follow-on security requirements. Collectively, these forces cement healthcare as a high-growth customer base for the Malaysia cybersecurity market.

By End-user Enterprise Size: SMEs Rising From a Low Base

Large enterprises controlled 70.80% of 2025 spending because financial, telecom, and energy leaders already run mature multi-layer programs. They continue to allocate budgets toward advanced analytics, penetration testing, and zero-trust segmentation that require skilled labor. Ongoing merger activity across banking and telco groups keeps demand for integration and red-team services high, reinforcing their dominance within the Malaysia cybersecurity market.

SMEs, however, are set to record a 8.78% CAGR, the fastest among size bands. Cloud-native security with pay-as-you-grow terms aligns with their cash-flow constraints. Government-backed assessments provide a starting blueprint, while local banks are piloting security-linked loan channels that reward certified controls with lower interest rates. MSSPs bundle endpoint detection, email security, and basic insurance into one monthly bill, simplifying the procurement journey. As SMEs integrate into regional supply chains, certifications become a prerequisite to win contracts, adding momentum to their cybersecurity investment.

Geography Analysis

Greater Kuala Lumpur remains the fulcrum of the Malaysia cybersecurity market, driven by the concentration of regional headquarters, regulatory bodies, and advanced managed-service facilities. Capital-city enterprises lead early adoption of zero-trust controls and red-team simulations, creating reference wins for vendors. A critical mass of talent, academia, and consulting firms fuels innovation cycles that spin off new niche providers. As a result, upstream demand for training services in the Klang Valley remains robust, sustaining capacity-building programs aligned with the twenty-five-thousand-defender national goal.

Johor Bahru follows as a fast-developing hub anchored by hyperscale data-center campuses. Global cloud providers select the region for abundant renewable power and submarine-cable proximity, catalyzing spending on physical, network, and OT protections. This cluster effect drives above-average growth in the Malaysia cybersecurity market across the southern corridor .

Penang and East-Malaysia contribute smaller absolute outlays but deliver above-average growth rates as manufacturing and e-government programs scale. Penang’s electronics exporters face strict customer audits that require demonstrated compliance with ISO 27001 and zero-downtime incident-response capabilities. Sabah and Sarawak digital-service agencies expand secure broadband and e-citizen platforms, adopting SaaS controls that bypass local-hardware shortages. Vendor ecosystems employ partner-led models to reach dispersed rural clients, showing that geography no longer limits participation in the Malaysia cybersecurity market.

Competitive Landscape

The Malaysia cybersecurity market presents moderate fragmentation, hosting global platforms, regional specialists, and rising local champions. Multinationals such as IBM, Cisco, and Microsoft supply integrated suites and win large framework contracts within banking and telecom sectors. They leverage long-standing enterprise relationships and wide product portfolios to anchor high-value transformation deals that span multiple security layers. Regional players like Ensign InfoSecurity provide deep consulting and managed detection expertise, often acting as prime contractors for complex, multi-country engagements.

Local specialists, including LGMS Berhad and Securemetric Bhd, exploit regulatory fluency and cultural alignment to secure compliance-driven projects. Their early certification under the Cyber Security Act licensing regime builds trust among critical-infrastructure operators that prioritize fast audit clearance. HeiTech Padu’s partnership with RSA demonstrates the value of co-branding advanced SIEM technologies with localized service wrap-arounds, enabling mid-tier organizations to access enterprise-grade analytics. Telecommunications operators such as CelcomDigi and Maxis extend security portfolios into managed firewalls and secure connectivity, monetizing network visibility built over decades.

Strategic alliances define go-to-market success: cloud providers work with telecom carriers to embed secure-access-service-edge nodes, while hardware vendors partner with local integrators for 24×7 field support. Talent scarcity accelerates merger activity as firms acquire niche consultancies to scale capacity. Market entry for pure-play software vendors remains accessible, yet service-heavy models face licensing and talent hurdles, encouraging white-label agreements with certified MSSPs. This dynamic supports a balanced competitive environment that limits price compression and sustains healthy margins across the Malaysia cybersecurity market.

Malaysia Cybersecurity Industry Leaders

LGMS Berhad

Wizlynx Group

IBM Corporation

Cisco Systems Inc.

Securemetric Bhd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Asia's leading cybersecurity provider, ABP Group, has strategically launched a new office in KL Eco City, right across from Mid Valley City, bolstering its presence in Malaysia.

- May 2025: BlackBerry Ltd has teamed up with Talent Corporation Malaysia Bhd (TalentCorp) to unveil the CyberNext Programme. This national initiative targets Malaysian students and educators, addressing the growing vulnerabilities in today's digital realm.

- October 2024: Ensign InfoSecurity ranked sixth in MSSP Alert’s global Top 250 list, underlining service leadership in Malaysia

- October 2024: BlackBerry Ltd, hailing from Canada, has set up its Asia Pacific regional headquarters for cybersecurity in Cyberjaya, Malaysia.

Malaysia Cybersecurity Market Report Scope

Cybersecurity solutions enable an organization to monitor, detect, report, and counter cyber threats that are internet-based attempts to damage or disrupt information systems and hack critical information using spyware, malware, and phishing to maintain data confidentiality.

The Malaysia cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By End-user Industry

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-user Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the current valuation of the Malaysia cybersecurity market?

The sector is valued at USD 6.59 billion in 2026 and is expected to reach USD 9.32 billion by 2031.

Which deployment model is growing fastest?

Cloud-based security is expanding at an 8.05% CAGR, outpacing the on-premise segment as enterprises favor consumption-based pricing.

Why is healthcare the fastest-growing vertical?

Digital medical records, telemedicine uptake, and stringent privacy amendments drive an 8.46% CAGR for healthcare cybersecurity spending.

How does the Cyber Security Act 2024 affect vendors?

It requires licensing for key services and continuous compliance reporting, giving certified providers a competitive edge.

Page last updated on: