Shortenings Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

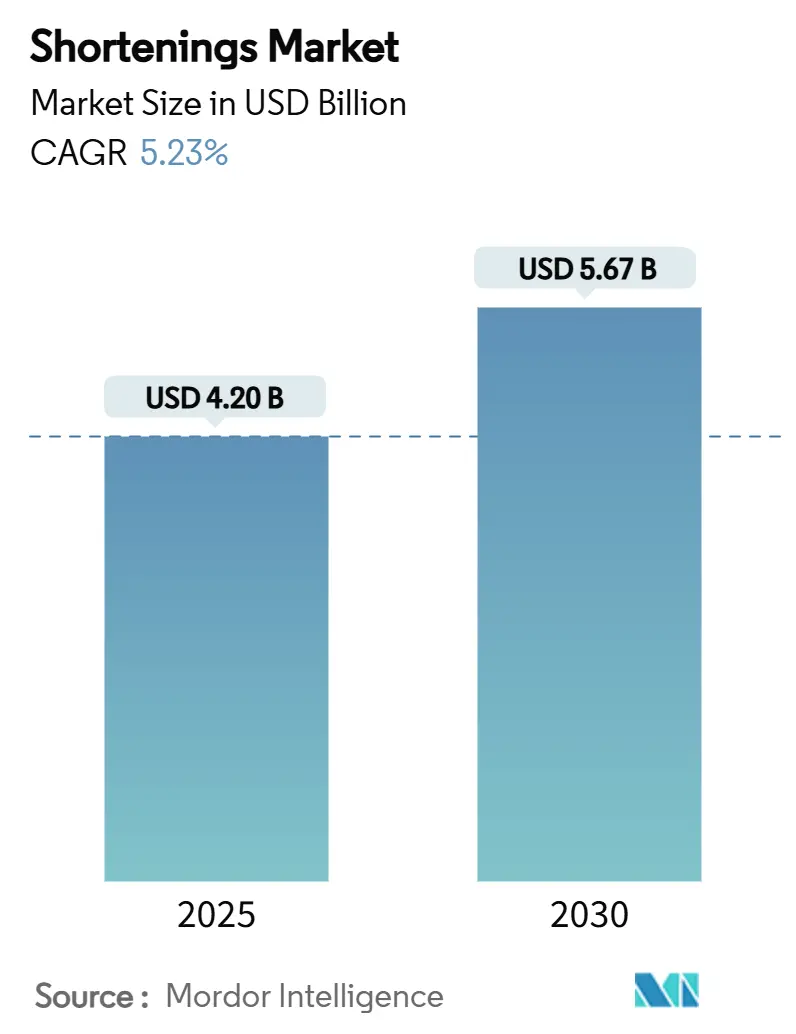

| Market Size (2025) | USD 4.20 Billion |

| Market Size (2030) | USD 5.67 Billion |

| Growth Rate (2025 - 2030) | 5.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Shortenings Market Analysis by Mordor Intelligence

The shortenings market size is valued at USD 4.2 billion in 2025 and is forecast to reach USD 5.67 billion in 2030, advancing at a 5.23% CAGR during 2025-2030. Growth is driven by global elimination of partially hydrogenated oils, rapid investment in enzymatic interesterification, and the pivot toward sustainable plant-based formulations that satisfy clean-label demands. Asia-Pacific dominates current revenues and leads expansion as Indonesia’s palm-oil output climbs and local industrial bakeries scale capacity, while North America shapes performance standards through frozen food innovation and trans-fat regulations. Competitive intensity remains moderate concentration score indicating room for new entrants, yet rewards incumbents that control technology portfolios and vertically integrated supply chains.

Key Report Takeaways

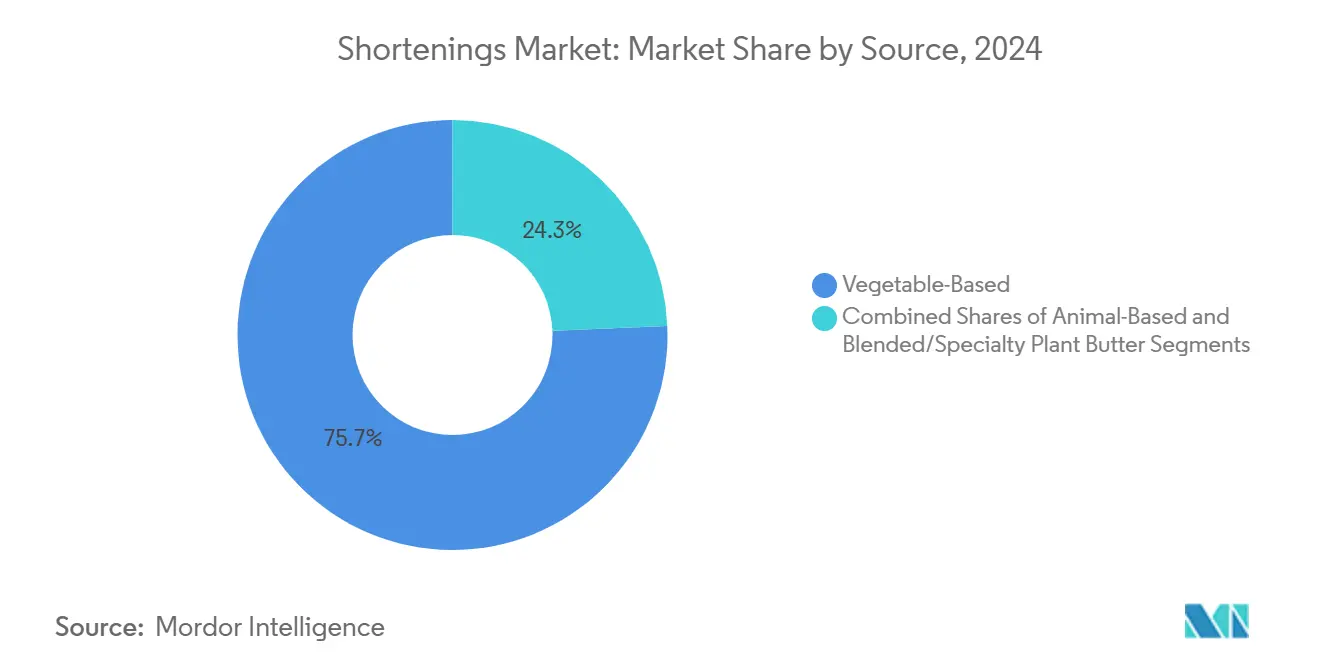

- By source, vegetable-based fats led with 75.67% share in 2024; specialty plant butters are projected to grow at a 7.12% CAGR from 2025 to 2030.

- By form, solid all-purpose fats held 42.50% of the 2024 bakery fats market share, while puff and lamination fats are set to rise at a 6.78% CAGR through 2030.

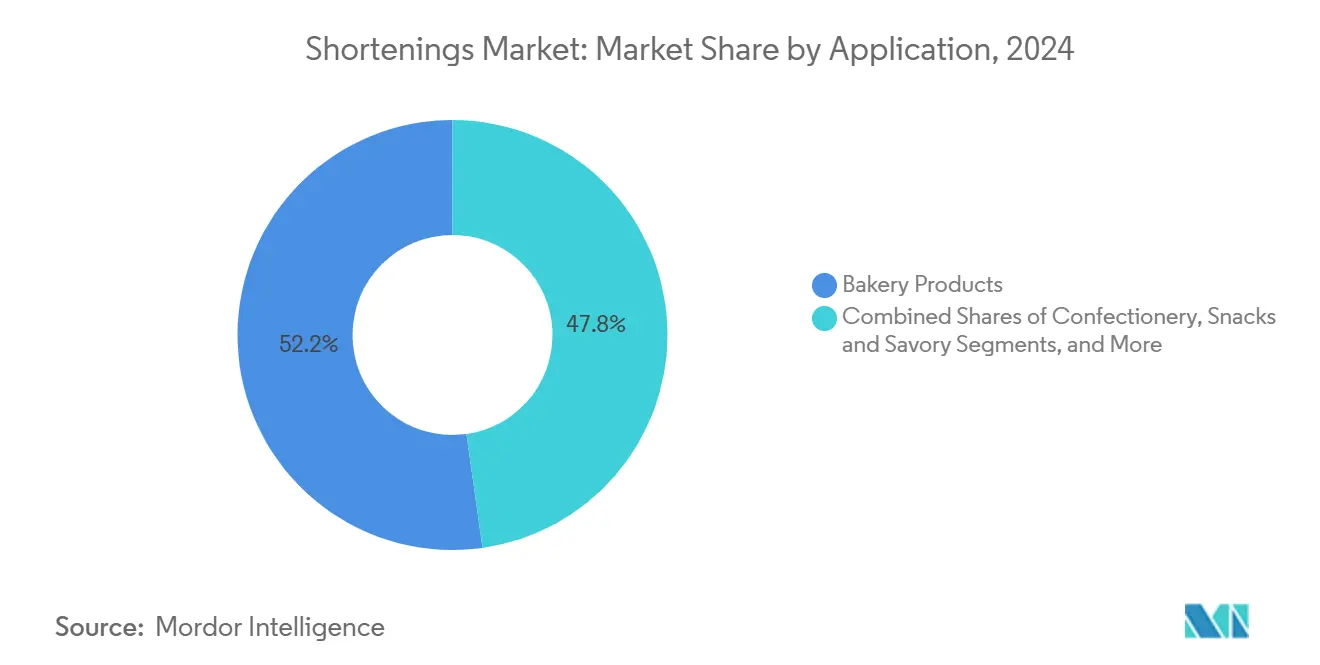

- By application, bakery products captured 52.23% of value in 2024, but frozen desserts and ice cream are on track for a 7.45% CAGR between 2025 and 2030.

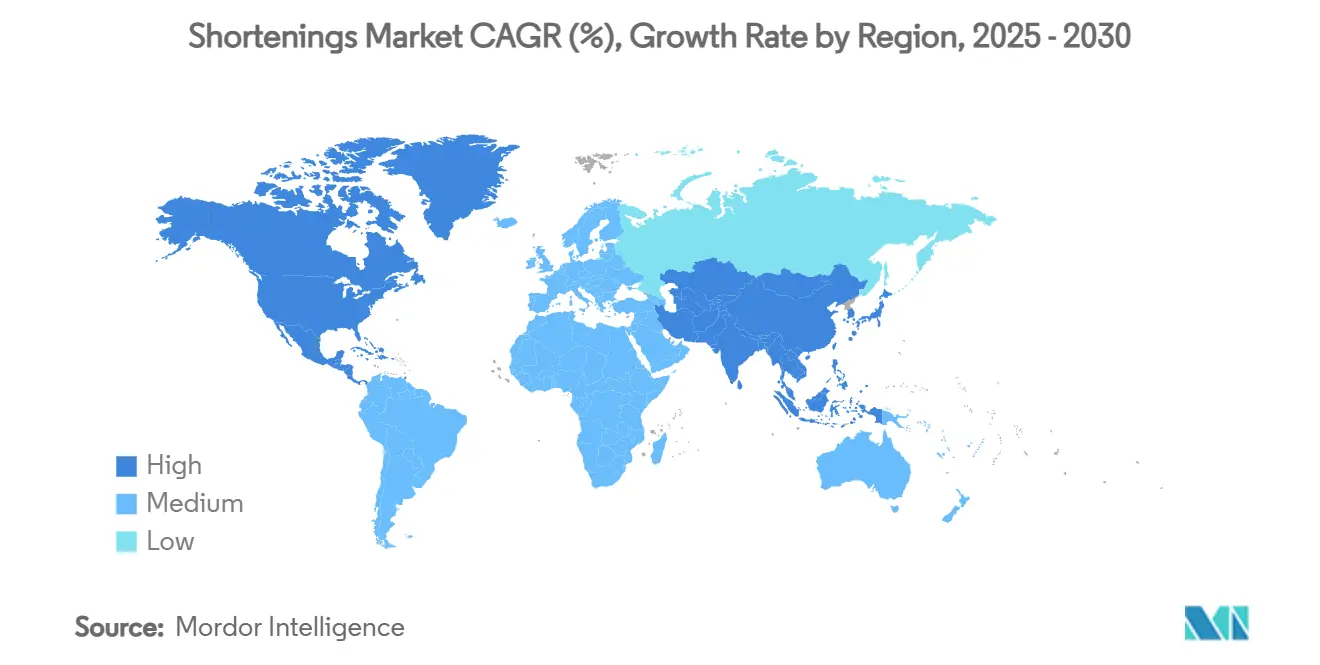

- By geography, the Asia-Pacific commanded 34.00% revenue in 2024 and is forecast to expand at a 6.50% CAGR to 2030.

Global Shortenings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label, trans-fat-free bakery fats | +1.2% | Global, with strongest impact in North America & EU | Medium term (2-4 years) |

| Industrial bakery capacity expansion in emerging markets | +0.9% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Growth of convenience & ready-to-eat food segments | +0.8% | Global, led by North America | Short term (≤ 2 years) |

| Surge in specialty plant-based shortenings for laminated pastries | +0.6% | Europe & North America, expanding to APAC | Medium term (2-4 years) |

| Adoption of interesterified structured fats for flash-freeze snack lines | +0.4% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Clean-Label, Trans-Fat-Free Bakery Fats

Regulatory pressures are reshaping fat formulation strategies. The FDA's[1]Food and Drug Administration, “FDA Finalizes Updated ‘Healthy’ Nutrient Content Claim,” fda.gov updated "healthy" nutrient content claim is opening doors for reformulated products. With the finalization set for December 2024, foods such as nuts, seeds, and select oils can now make health claims. However, there's a catch: stricter limits are being imposed on saturated fat, sodium, and added sugars. This regulatory shift comes hand-in-hand with the complete removal of partially hydrogenated oils from 52 outdated food standards. This move not only clears up regulatory uncertainties but also speeds up the industry's shift towards alternative technologies. Meanwhile, European markets are feeling the heat. The EU's trans-fat regulation has, somewhat unexpectedly, boosted palmitic acid content in savory baked goods. This is especially evident in cheese pies with puff pastry, leading to a surge in demand for advanced fat replacement strategies. As regulatory demands align with growing consumer health awareness, manufacturers are turning to solutions like enzymatic interesterification and saturated monoglyceride-based fat alternatives.

Industrial Bakery Capacity Expansion in Emerging Markets

Bakery operators are increasingly optimistic about capacity investments, driven by demographic pressures and changing consumption patterns in emerging markets. Industry surveys reveal that 84% of operators are prioritizing capacity growth, while 68% are turning their attention to automation. This shift is largely in response to a projected labor shortage, with an estimated 53,500 job openings anticipated in the bakery sector by 2030. A case in point is Indonesia, where Jakarta's flour milling facility, the largest in the world, ramped up its capacity from 800 to 1,200 tonnes daily. The facility aims for a total daily capacity of 11,650 tonnes, aligning with the country's annual flour market growth of 5%. Indonesia's market, characterized by 70% reliance on imported ingredients and a mandate for halal certification, presents unique opportunities. Specialized fat suppliers adept at navigating these regulatory intricacies while adhering to religious dietary standards stand to benefit. Furthermore, investments in automation are not limited to just capacity enhancements. They're also being channeled into quality control and traceability systems. This is especially pertinent given the EU's Deforestation Regulation, which mandates meticulous data collection on ingredient sourcing. The intricacies of these regulations amplify the demand for vertically integrated suppliers.

Growth of Convenience and Ready-to-Eat Food Segments

As the convenience food revolution unfolds, fat performance requirements are evolving. Frozen food applications now seek specialized formulations that remain stable, even in temperature extremes. Meanwhile, as consumers gravitate towards bite-sized snacks and products suited for air fryers, fat formulators face the challenge of balancing melting profiles with oxidative stability, especially over prolonged storage. The rising popularity of global cuisine flavors in frozen foods necessitates fats that not only enhance diverse seasoning profiles but also avoid off-flavors during reheating. The growth of the ready-to-eat segment mirrors shifts in workplace dynamics and urbanization, especially among younger individuals who favor convenience over traditional meal prep. This trend fuels a heightened demand for premium frozen bakery items, offering restaurant-quality experiences with easier preparation. Achieving this requires advanced fat systems that preserve texture and flavor integrity throughout the cold chain.

Surge in Specialty Plant-Based Shortenings for Laminated Pastries

Laminated pastries pose a technical challenge, as they require precise melting profiles and crystallization behaviors that traditional plant oils cannot achieve without modification. Enzymatic interesterification has emerged as the preferred technique for transforming rapeseed oil into zero-trans,dialkylketone-free fats. This method retains beneficial tocopherols while avoiding the harmful by-products associated with chemical interesterification. In Europe, the rising demand from artisanal bakeries for specialty shortenings is driving innovation. These shortenings are critical for achieving the complex lamination techniques needed for croissants and puff pastries. Furthermore, maintaining an optimal omega-3/omega-6 ratio of 2.2 through enzymatic processing creates opportunities for premium bakery applications. This aligns with consumer preferences for functional ingredients that provide both performance and nutritional benefits.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in palm-oil pricing | -0.7% | Global, strongest impact in APAC & Europe | Short term (≤ 2 years) |

| Stringent global limits on saturated & trans fats | -0.5% | North America & EU primarily | Medium term (2-4 years) |

| Limited interesterification tolling capacity | -0.3% | Global, concentrated in specialized facilities | Long term (≥ 4 years) |

| Consumer backlash against seed-oil ingredients | -0.2% | North America primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Palm-Oil Pricing

Indonesian production policies, pivotal in the global palm oil landscape, are causing ripples in the shortenings supply chain. With Indonesia's B40 biodiesel initiative set to boost domestic palm oil use by 1 million tonnes, exports are tightening, even as production is projected to grow by 6.9% to reach 20 million tonnes by 2025. President Prabowo Subianto's push for expansion in palm oil cultivation faces backlash, especially given the 74 million hectares of rainforest lost since 1950 to palm oil farming. This environmental concern introduces regulatory uncertainties, complicating long-term supply strategies. In 2024, exports plummeted by 13.75% year-over-year, underscoring how swiftly policy shifts can reshape global supply chains. As a result of this volatility, manufacturers of bakery fats are compelled to bolster their inventory buffers and explore alternative sourcing avenues. This not only escalates their working capital demands and operational intricacies but also casts a shadow on the stability of product pricing.

Stringent Global Limits on Saturated and Trans Fats

Regulatory tightening introduces technical formulation challenges, necessitating significant R&D investments and potential adjustments to product recipes across portfolios. The FDA's proposed front-of-package labeling for saturated fat disclosure is expected to influence consumer purchasing decisions, with the American Heart Association's 13-gram daily limit on a 2,000-calorie diet serving as a key benchmark. European markets reveal the unintended effects of regulatory actions: the elimination of trans fats led to increased palmitic acid levels in savory baked goods, potentially offsetting public health benefits and necessitating further reformulation efforts. The challenge of replacing coconut oil in confectionery applications highlights the technical difficulties manufacturers face, as its unique crystallization and melting properties are not easily replicated through simple substitutions. Advanced solutions, such as interesterified oil blends, can significantly reduce saturated fat content but require process modifications and may result in higher ingredient costs, impacting product economics. The evolving regulatory landscape imposes ongoing compliance costs and extends product development cycles to 18-24 months, delaying time-to-market for new formulations and potentially limiting resources for other strategic initiatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Vegetable-Based Sources Dominance Drives Innovation

In 2024, vegetable-based sources hold a dominant 75.67% market share, driven by regulatory pressures and increasing consumer preference for plant-derived ingredients over animal fats. Specialty plant butters are the fastest-growing segment, with a 7.12% CAGR projected through 2030. This growth is attributed to advancements that replicate the functionality of traditional animal fats without compromising performance. Conversely, animal-based sources are experiencing reduced adoption due to regulatory challenges and supply chain issues, particularly in regions like Indonesia, where strict halal certification is required, and 70% of bakery ingredients are imported. Blended and specialty plant butters are positioned as premium products, catering to artisanal bakeries and high-end applications where their performance justifies higher costs.

This shift in source segmentation highlights a broader industry transition toward sustainable and traceable supply chains. Companies such as Wilmar International are implementing policies like No Deforestation, No Peat, No Exploitation, which significantly impact raw materials sourcing strategies. Enzymatic interesterification technology now enables plant-based sources to achieve crystallization profiles previously exclusive to animal fats. Additionally, these zero-trans formulations preserve tocopherols while avoiding the formation of harmful dialkylketones. Innovations like algae-based cooking oils, featuring 93% monounsaturated fat content and a 535°F smoke point, further demonstrate the potential of novel plant sources in specialized applications.

By Form: Solid Foundations Meet Specialty Growth

In 2024, solid all-purpose shortenings command a dominant 42.50% market share, underpinning traditional bakery applications where consistency and cost-effectiveness reign supreme. Puff and lamination fats, riding the wave of a burgeoning premium pastry market and the rise of artisanal bakeries in emerging markets, are the fastest-growing segment, boasting a 6.78% CAGR projected through 2030. Cake and icing fats cater to specialized needs, demanding precise melting profiles and stability, while liquid and frying fats are tailored for high-efficiency demands in commercial operations. Meanwhile, flaked and dry forms find their niche in industrial applications, where their convenience in handling and storage stability justify a premium price tag.

The evolution of form segmentation underscores a leap in fat engineering sophistication. Techniques like crystallization control and melting profile optimization carve out distinct performance categories. CSM Ingredients' SlimBAKE emulsion technology showcases the industry's prowess, slashing fat content by 30% without compromising on taste or texture, applicable in both ambient and frozen settings. Lamination applications are reaping rewards from enzymatic interesterification breakthroughs, allowing meticulous control over solid fat content profiles. This precision is vital for achieving the desired dough layering and texture in the final product. Puff pastry applications, with their inherent technical intricacies, demand fats that maintain solidity during dough prep but melt entirely during baking, crafting steam pockets that yield the signature flaky texture.

By Application: Bakery Products Dominate the Market

In 2024, bakery products, including bread, cakes, pastries, and more, command a dominant 52.23% share of the market, owing to the rising consumption of these products. According to the Office for National Statistics data from 2023[2]Office for National Statistics, "Sales from the manufacture of bread, fresh pastry goods and cakes in the United Kingdom", www.ons.gov.uk, sales from the manufacturers of bread and pastry goods in the United Kingdom were USD 11,272.3 million. Meanwhile, frozen desserts and ice cream are making waves, growing at a brisk 7.45% CAGR, projected through 2030. The confectionery sector is navigating challenges, requiring specialized fat systems to harmonize chocolate compatibility with sugar crystallization. As the consumption of these products is increasing, the use of shortenings is also increasing. According to the Central Statistical Office of Poland[3]Central Statistical Office of Poland, "Average monthly per capita expenditure on confectionery in Poland", www.stat.gov.pl data from 2023, the Average monthly per capita expenditure on confectionery in Poland was USD 3.49. Snacks and savory items are riding the wave of air fryer trends, with bite-sized products demanding precise melting and stability. Ready-to-eat and prepared meals are carving out a niche, where the allure of convenience justifies premium pricing.

As consumer behaviors evolve, younger demographics are leading the charge, seeking global flavors and convenient meals. This shift necessitates specialized fat formulations. The frozen segment's upward trajectory is bolstered by health-centric product innovations, notably catering to GLP-1 medication users with tailored nutritional profiles. However, the frozen realm isn't without its hurdles: maintaining texture through freeze-thaw cycles and avoiding fat bloom, which can compromise both appearance and taste. In the confectionery world, there's a growing pivot towards cocoa butter alternatives, a response to surging cocoa prices, all while ensuring flavor harmony. To further enhance production efficiency, companies are turning to cutting-edge solutions like AI and fermentation technologies.

Geography Analysis

In 2024, Asia-Pacific emerges as both the largest regional market, holding a 34.00% share, and the fastest-growing region, with a projected 6.50% CAGR through 2030. This dual distinction is primarily driven by Indonesia's critical role in the global palm oil supply and its expanding industrial bakery sector. By 2025, Indonesia's palm oil production is expected to increase by 6.9%, reaching 20 million tonnes. However, regulatory challenges persist in the region. This situation benefits established suppliers with strong compliance capabilities. Additionally, industrial bakery expansions in China and India are driving demand for specialized fats, essential for automated production and extended shelf life, which are critical for large-scale distribution networks.

North America and Europe, recognized as mature markets, utilize regulatory leadership and premium positioning to drive advancements in clean-label and specialty applications. The US frozen food market, valued at USD 91.3 billion and representing 39% of the global market, has specific technical requirements for shortenings. These shortenings ensure stability across temperature extremes while accommodating diverse flavor profiles, as highlighted by Conagra Brands. In Europe, markets balance strict regulations with artisanal traditions. For example, the EU's trans-fat regulation, while promoting health benefits, inadvertently increased palmitic acid content in savory baked goods, leading to a demand for advanced replacement strategies. Moreover, the EU's Deforestation Regulation requires detailed supply chain documentation, particularly affecting palm oil sourcing. This regulation provides a competitive advantage to suppliers with strong traceability systems.

Emerging markets in South America, the Middle East, and Africa are experiencing distinct dynamics fueled by agricultural integration and increasing urban consumption. Brazil's importance in global supply chain integration is highlighted by ADM's acquisition of Algar Agro's oilseed processing facilities. However, these regions face challenges such as climate stability requirements, halal certification in Muslim-majority countries, and infrastructure limitations that impact cold chain integrity for specialized fat applications. Despite these obstacles, opportunities are emerging. The development of local processing capabilities and technical expertise is fostering technology transfers and partnerships. These collaborations are expected to accelerate market penetration and establish sustainable competitive advantages.

Competitive Landscape

With a rating of 6 out of 10, the bakery fats market showcases a moderate concentration. This level of concentration indicates a competitive intensity that fuels innovation. Yet, it also permits established players to leverage technological differentiation and integrate their supply chains for strategic advantages. Instead of merely competing on price or scale, market leaders are channeling their efforts into enzymatic interesterification capabilities, clean-label formulations, and expanding geographically through strategic acquisitions. Recent consolidation moves, such as the Bunge-Viterra merger forming a top-tier global agribusiness entity and Stratas Foods' USD 56.55 million takeover of AAK's foodservice division, bolstering its North American foothold, underscore the industry's push for operational synergies and broader market reach.

Furthermore, strategic collaborations, exemplified by ADM's partnership with Mitsubishi Corporation, highlight a collective industry acknowledgment: navigating the intricacies of the global supply chain demands teamwork, especially when tackling food security and sustainability issues. There's a burgeoning demand for specialized applications, especially those needing advanced technical skills. Notably, enzymatic interesterification is sought after for zero-trans formulations, and structured fats are in demand for flash-freeze applications. Patent filings related to shortening particle compositions hint at a vibrant innovation scene, especially in low trans fatty acid formulations. These innovations predominantly utilize non-tropical base oils, like soybean oil, and are fine-tuned for specific melting characteristics.

New entrants are making waves, particularly those crafting algae-based oils boasting enhanced monounsaturated fat profiles. Additionally, novel fermentation techniques are emerging, offering sustainable substitutes to conventional fat sources. Companies that adeptly meld AI and fermentation advancements with traditional processing stand to gain a competitive edge, both in cost savings and product uniqueness. Given the market's moderate concentration, there's ample room for further strategic acquisitions and partnerships, paving the way for accelerated geographic and technical growth.

Shortenings Industry Leaders

-

Cargill Inc.

-

AAK AB

-

Wilmar International

-

Stratas Foods LLC

-

Bunge Holdings S.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Bunge and Viterra completed their merger to create a premier global agribusiness solutions company, enhancing capabilities in oilseed processing and specialty plant-based oils and fats with projected annual operational synergies of USD 250 million within three years

- October 2024: Stratas Foods agreed to acquire AAK Foodservice in Hillside, New Jersey for approximately USD 56.55 million, expanding manufacturing facilities from eight to nine locations in the US

Global Shortenings Market Report Scope

| Vegetable-based |

| Animal-based |

| Blended and Specialty Plant Butters |

| Solid All-Purpose |

| Cake and Icing |

| Puff/Lamination |

| Liquid/Frying |

| Flaked and Dry |

| Bakery Products | Bread |

| Cakes & Pastries | |

| Cookies & Biscuits | |

| Donuts & Muffins | |

| Confectionery | |

| Snacks and Savory | |

| Frozen Desserts and Ice Cream | |

| Ready-to-Eat and Prepared Meals |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Netherlands | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South africa | |

| Rest of Middle East and Africa |

| By Source | Vegetable-based | |

| Animal-based | ||

| Blended and Specialty Plant Butters | ||

| By Form | Solid All-Purpose | |

| Cake and Icing | ||

| Puff/Lamination | ||

| Liquid/Frying | ||

| Flaked and Dry | ||

| By Application | Bakery Products | Bread |

| Cakes & Pastries | ||

| Cookies & Biscuits | ||

| Donuts & Muffins | ||

| Confectionery | ||

| Snacks and Savory | ||

| Frozen Desserts and Ice Cream | ||

| Ready-to-Eat and Prepared Meals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Netherlands | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of shortenings market by 2030?

The shortenings market is expected to reach USD 5.67 billion in 2030.

Which region is growing fastest in shortenings demand?

Asia-Pacific is forecast to post a 6.50% CAGR from 2025-2030, the highest among all regions.

Which shortenings form is expanding quickest?

Puff and lamination shortenings are projected to advance at a 6.78% CAGR through 2030.

How are regulations influencing shortenings formulations?

FDA and EU trans-fat bans are pushing manufacturers toward enzymatic interesterification and clean-label plant-based fats.

Page last updated on: