Cloud Identity and Access Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

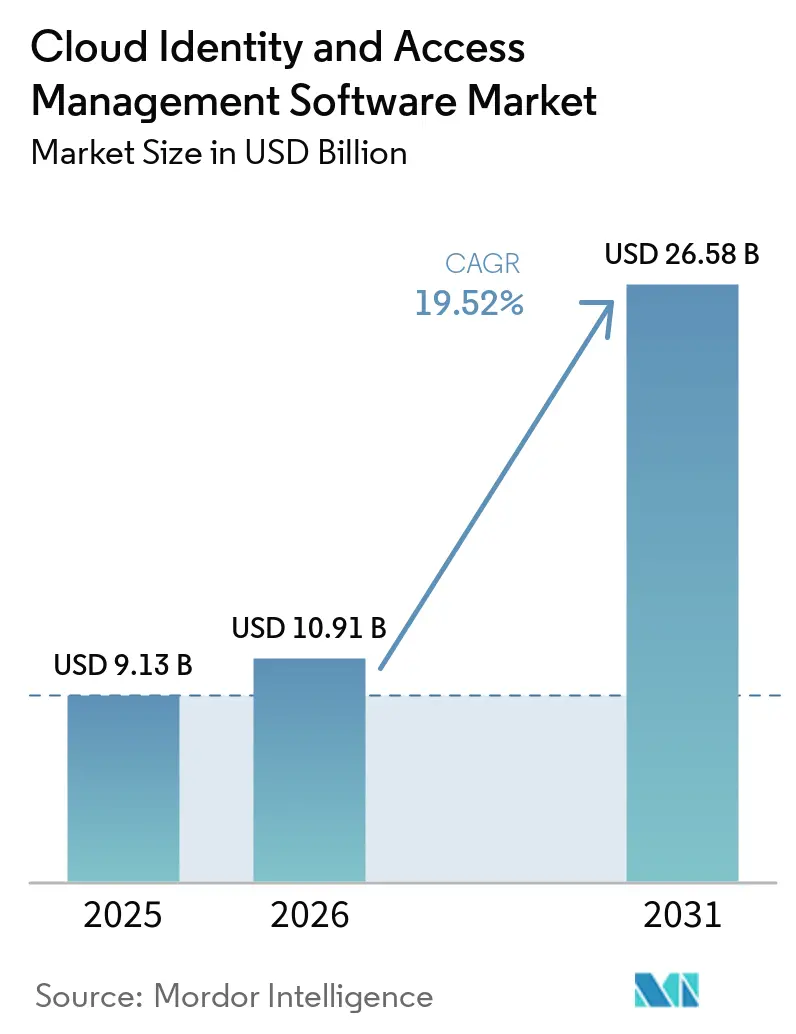

| Market Size (2026) | USD 10.91 Billion |

| Market Size (2031) | USD 26.58 Billion |

| Growth Rate (2026 - 2031) | 19.52% CAGR |

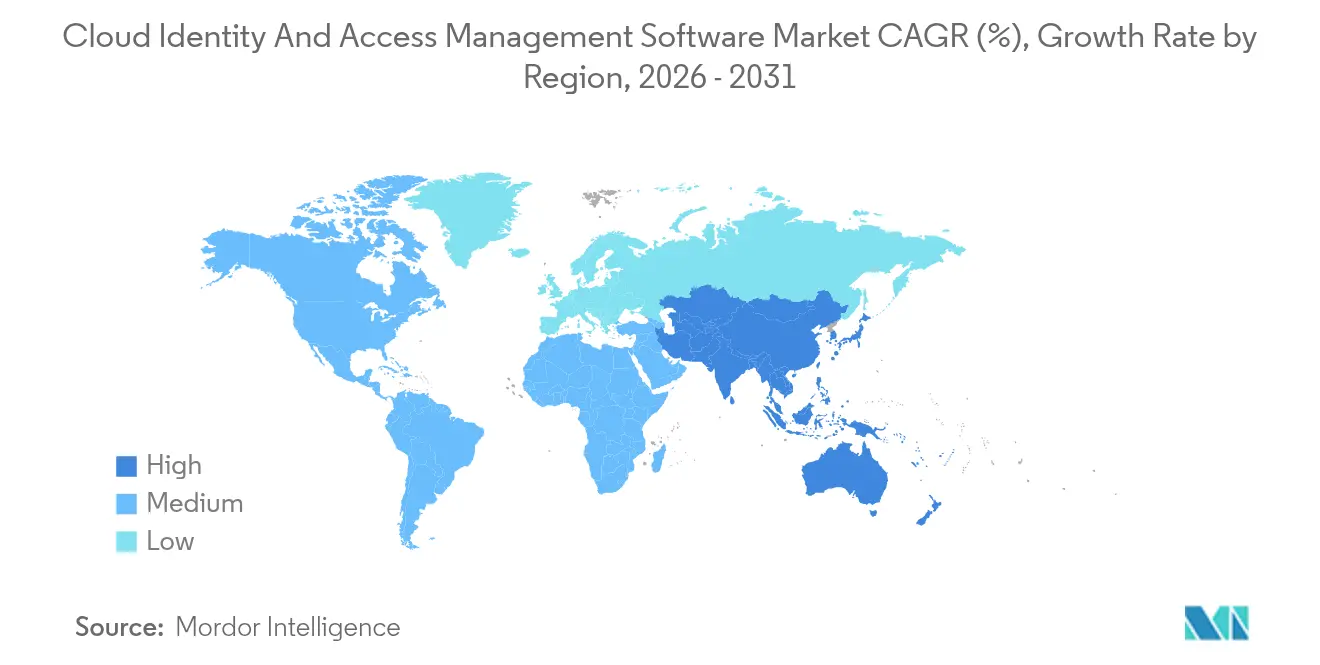

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

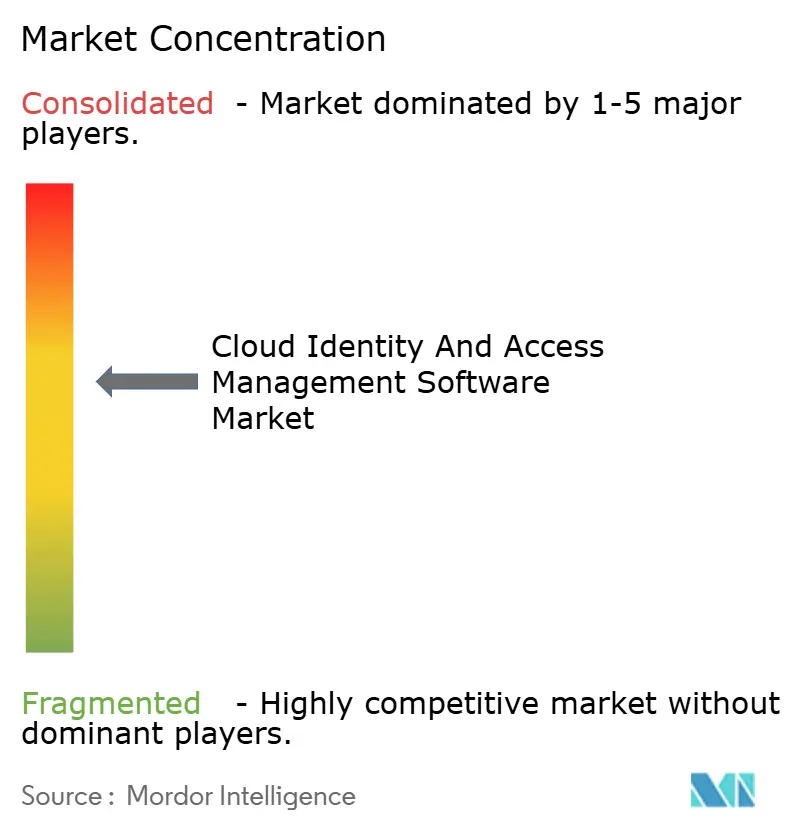

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Identity and Access Management Software Market Analysis by Mordor Intelligence

The cloud identity and access management software market size in 2026 is estimated at USD 10.91 billion, growing from 2025 value of USD 9.13 billion with 2031 projections showing USD 26.58 billion, growing at 19.52% CAGR over 2026-2031. The surge is directly attributed to enterprises re-architecting security around Zero Trust verification, the swelling adoption of multi-factor credentials, and stricter global data-protection statutes. Continuous authentication that re-checks user legitimacy mid-session has moved from niche pilots to mainstream practice, limiting the damage of credential-stuffing attacks that exposed 24 billion records in 2024. Regulatory fines that reach into the billions now make non-compliant identity governance an existential risk rather than a line-item penalty, pushing organizations toward cloud-native controls that offer immutable audit trails. Vendors are differentiating with AI-driven anomaly detection, passwordless user journeys, and managed services that offset the global IAM skills gap. At the same time, mounting private-equity buyouts signal confidence in the recurring-revenue model that underpins the cloud identity and access management software market.

Key Report Takeaways

- By component, services expanded at a 19.61% CAGR through 2031, while software retained 58.62% of the cloud identity and access management software market size in 2025.

- By deployment model, the public cloud held 46.95% of the cloud identity and access management software market size in 2025; the hybrid cloud is advancing at a 19.84% CAGR through 2031.

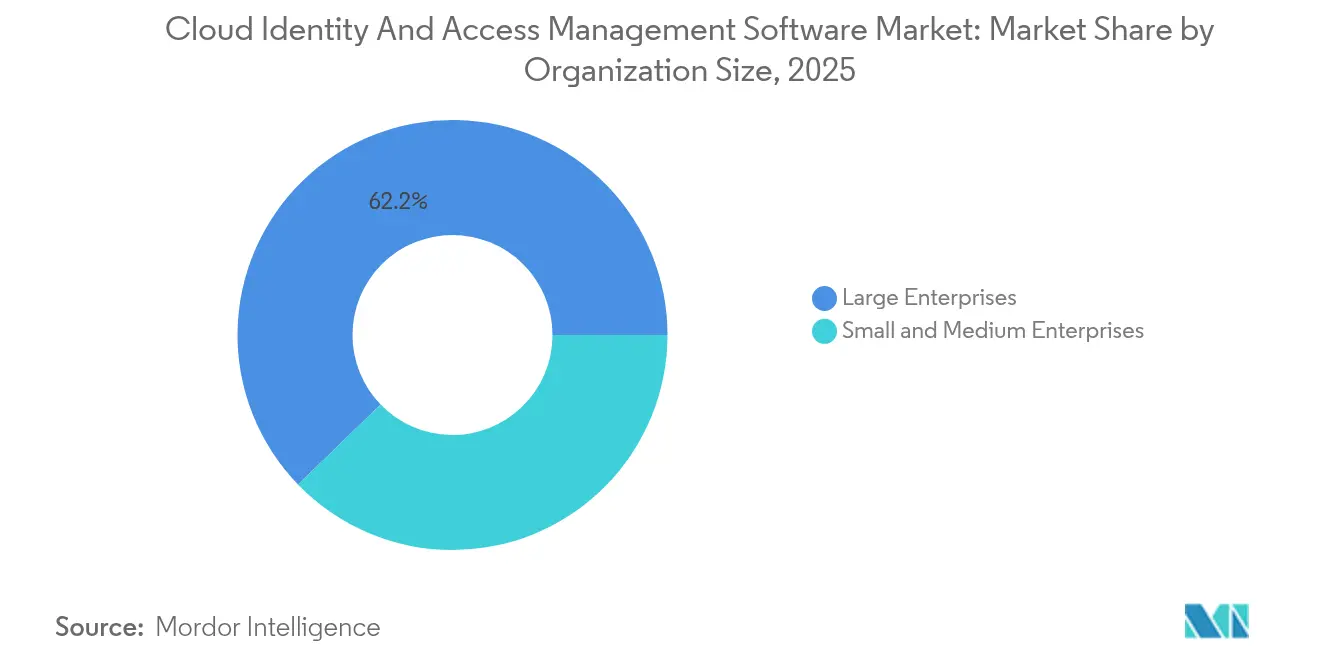

- By organization size, large enterprises captured 62.24% of the cloud identity and access management software market size in 2025, whereas SMEs are growing at a 19.7% CAGR.

- By industry vertical, IT and telecom led with a 25.38% of the cloud identity and access management software market size in 2025; healthcare is the fastest-growing vertical, with a 20.74% CAGR through 2031.

- By geography, North America accounted for 38.21% of the cloud identity and access management software market size in 2025, while the Asia Pacific recorded the strongest regional CAGR at 20.32% from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Identity and Access Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Zero Trust Security Frameworks | +4.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Proliferation of Cloud Services Across Enterprises | +3.8% | Global, accelerated in Asia Pacific | Short term (≤ 2 years) |

| Strict Regulatory Compliance Requirements Such as GDPR and CCPA | +3.5% | Europe, North America, expanding to Asia Pacific | Long term (≥ 4 years) |

| Surge in Remote Workforces Post-Pandemic | +2.9% | Global, with highest penetration in North America and Europe | Medium term (2-4 years) |

| Rising Integration of CIAM with Decentralized Identity (Blockchain) | +2.1% | Early adoption in Europe, North America, select Asia markets | Long term (≥ 4 years) |

| Emerging Demand for Passwordless Authentication to Enhance User Experience | +3.2% | Global, led by consumer-facing sectors in all regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Zero Trust Security Frameworks

Enterprises that once trusted perimeter firewalls now regard every request as potentially hostile. NIST codified Zero Trust in SP 800-207A during 2024, prompting 81% of global businesses to embed these principles into IAM roadmaps.[1]National Institute of Standards and Technology, “Zero Trust Architecture,” nist.gov Federal Executive Order 14028 compels U.S. agencies to verify each access attempt, driving commercial demand for Privileged Access Management and policy-based engines that enforce least-privilege rules across hybrid environments. Financial institutions illustrate the payoff, for instance, it is estimated to be reported a decline in unauthorized access was reported after shifting most of internal apps to Zero Trust controls. Service-mesh technologies, such as Istio, now embed mutual TLS between microservices, eliminating static passwords and reducing lateral-movement risk. ISO/IEC 27001:2022 links certification to demonstrable Zero Trust enforcement, turning the framework from optional best practice into a procurement prerequisite.

Proliferation of Cloud Services Across Enterprises

Organizations now average 3.4 distinct public-cloud platforms, each requiring federated identity to prevent credential sprawl.[2]Cloud Native Computing Foundation, “CNCF Annual Survey 2024,” cncf.io The emergence of Decentralized Identity solutions is enabling enterprises to enhance secure authentication, privacy control, and digital trust management across cloud ecosystems. AWS, Azure, and Google Cloud processed 1.2 trillion authenticated API calls daily in 2024, most gated by OAuth 2.0 tokens issued by centralized IAM hubs. Container workloads rotate certificates hourly, making automated SPIFFE frameworks indispensable for non-human identities. Telecom operators migrating 5G cores to hyperscale clouds exemplify machine-to-machine authentication at massive volume, as Verizon ran 60% of its 5G core on AWS in 2024. Europe’s NIS2 Directive, effective October 2024, now obligates supply-chain risk assessments for cloud dependencies, hard-wiring identity governance into compliance checklists.

Strict Regulatory Compliance Requirements Such as GDPR and CCPA

The European Data Protection Board levied EUR 3.9 billion in fines between 2021 and 2024, with 38% tied to weak identity controls.[3]European Union Agency for Cybersecurity, “NIS2 Directive,” enisa.europa.eu California’s Privacy Rights Act forces platforms to log every algorithmic data access, rewarding IAM tools that generate immutable audit trails. India’s Digital Personal Data Protection Act mandates that sensitive authentication logs remain in-country, accelerating adoption of hybrid IAM architectures. PCI DSS 4.0 now requires multi-factor authentication for any cardholder-data access, eliminating password-only logins that 60% of merchants used as late as 2023. Healthcare must now encrypt electronic records at rest and in transit under HIPAA amendments, driving granular IAM policies that separate clinician authority from patient consent.

Surge in Remote Workforces Post-Pandemic

Remote and hybrid work remained triple pre-2020 levels in 2024, dissolving the traditional perimeter. Cisco found that firms with mature IAM recorded 47% fewer breaches tied to compromised remote credentials. Hardware FIDO2 keys are gaining traction, Google distributed 10 million Titan devices, virtually eradicating phishing-based account takeovers. The FFIEC now mandates risk-based step-up authentication for online banking sessions, further cementing identity governance as critical infrastructure. Europe’s banking regulator echoes that stance, requiring continuous authentication from January 2025.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Implementation and Integration | -2.3% | Global, acute in SME segments and emerging markets | Short term (≤ 2 years) |

| Shortage of Skilled IAM Professionals | -1.8% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| Interoperability Challenges Among Heterogeneous Identity Protocols | -1.1% | Global, particularly in multi-cloud enterprises | Medium term (2-4 years) |

| Privacy Concerns Around Behavioral Biometrics | -0.7% | Europe and North America, emerging in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Implementation and Integration

Deloitte’s 2024 survey shows firms under 500 staff devote only 8% of IT budgets to identity controls, half the enterprise allocation. Legacy applications that lack modern protocols often need bespoke connectors that can swallow 40% of IAM project expenditure. Smaller U.S. businesses list cybersecurity costs, including IAM, as their third-largest digital-transformation barrier. Financial institutions report 18-24-month timelines when synchronizing IAM across ATMs, mobile apps, and core banking, leaving parallel systems in place and inflating operational risk during cutover. European lenders postponed upgrades in 42% of cases because of hidden training and help-desk expenses.

Shortage of Skilled IAM Professionals

ISC2 calculated a 4-million-person cybersecurity workforce gap in 2024, with IAM experts the rarest subset. U.S. salaries for IAM architects sit 22% above general security roles, and consultants bill up to USD 350 per hour. The NICE framework now tags IAM as a priority skill needing 40 additional training hours beyond general certifications. Only 15% of accredited U.S. computer-science programs offer IAM coursework, forcing companies to fund internal academies. India forecasts a shortage of 1 million security professionals by 2027, with acute IAM scarcity outside major tech hubs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Rise as Integrations Grow Harder

Software licenses and subscriptions captured 58.62% of 2025 revenue, yet professional and managed services are accelerating at 19.61% CAGR through 2031. The growth stems from enterprises discovering that off-the-shelf platforms still need custom connectors for legacy payroll systems, SCIM provisioning for SaaS apps, and role-engineering workshops that align entitlements with least-privilege mandates. Professional services now absorb up to 45% of total implementation spending, a trend that reinforces the cloud identity and access management software market message that expertise often outweighs code. Businesses also lock in multi-year support to keep pace with quarterly feature drops, such as the 14 significant updates Microsoft issued for Entra in 2024.

Recurring revenue from training, audits, and compliance assessments keeps the services pipeline full. GDPR Article 30 demands exhaustive records of every processing activity, pushing firms to enlist consultants who can configure audit logs that map each authentication decision to a policy line item. ISO/IEC 27001-driven penetration tests increasingly require evidence that privileges expire automatically, further embedding service fees into operating budgets. As a result, services play a pivotal role in scaling the cloud identity and access management software market.

By Deployment Model: Hybrid Cloud Balances Agility With Residency

Public cloud garnered 46.95% share in 2025 thanks to hyperscaler-native IAM features, but hybrid solutions are expanding at a 19.84% CAGR as regulators insist on local data residency. India’s data-protection act, for example, lets businesses process non-sensitive data abroad but forces sensitive identity logs to stay onshore, making dual-stack architectures unavoidable. A similar dynamic appears in China, where resident data must never leave national borders.

Latency and edge use cases reinforce the hybrid argument. Authentication for industrial sensors or point-of-sale terminals benefits from on-premise validation that executes in milliseconds. Standards bodies now recommend certificate-based device identities issued locally, while central policy engines in the cloud maintain governance consistency. The cloud identity and access management software market size for hybrid deployments is therefore on a double-digit trajectory.

By Organization Size: SMEs Adopt SaaS IAM to Close Risk Gaps

Large enterprises still account for 62.24% of spending, yet SMEs represent the fastest revenue growth at 19.7% CAGR, powered by subscription models that scale with headcount. JumpCloud, Okta Workforce Identity, and Microsoft Entra ID for Business deliver pre-configured policies, removing the need for a 24/7 security operations center.

Cyber-insurance carriers reinforce demand by requiring multi-factor authentication and privileged-access controls before underwriting coverage. U.S. CISA ranks IAM the second-most critical control for small firms after patching. Portable audit packs help SMEs satisfy California’s privacy thresholds and Europe’s Digital Operational Resilience Act without in-house governance teams, buoying the long-term outlook for the cloud identity and access management software market.

By Industry Vertical: Healthcare Leads in Telehealth Era

IT and telecom held the crown at 25.38% of 2025 revenue, leveraging their dual role as IAM providers and consumers. Yet healthcare posts the steepest climb, growing at 20.74% CAGR on the back of telehealth proliferation. The 21st Century Cures Act obliges providers to expose FHIR APIs, requiring IAM that distinguishes clinician orders from patient self-service. Epic Systems activated SMART-on-FHIR authentication during 2024, underscoring the sector’s pivot toward granular token scopes.

Financial services remain a heavyweight, driven by open-banking mandates that expire access tokens within 90 seconds and link them to transaction particulars. Retailers deepen customer-identity investments to honor GDPR Article 22 limits on algorithmic profiling. Government programs meanwhile scale national e-ID schemes, as seen with Estonia’s 100 000 e-Residency credentials secured via X.509 certificates. Manufacturing converges IT and OT networks, using certificates to authenticate programmable logic controllers in real time.

Geography Analysis

North America generated 38.21% of 2025 revenue, fueled by a concentration of IAM vendors, robust venture funding, and federal Zero Trust mandates. Canada’s breach-notification law and Mexico’s fintech licensing regime adds further regional momentum. Competitive grants and FedRAMP authorizations position the cloud identity and access management software market for continued scale across the continent.

Asia Pacific delivers the fastest CAGR at 20.32%. India’s biometric Aadhaar program integrates with private IAM for rapid e-KYC, while penalties of INR 2.5 billion (USD 30 million) for violations keep compliance top-of-mind. China restricts transfers of more than 1 million records without security clearance, prompting multinationals to deploy in-country identity vaults. Japan’s extraterritorial APPI amendments and South Korea’s mandatory audits sustain demand. Australia’s draft bill raising fines to AUD 50 million (USD 33 million) further underscores the stakes.

Europe remains a mature arena governed by GDPR, where 2 154 fines since 2021 underscore enforcement vigor. Germany’s BSI calls for hardware multi-factor for all privileged users, France’s CNIL restricts cloud-based biometrics, and the U.K.’s post-Brexit regime still imposes strict consent audits. The Middle East and South America emerge as growth corridors through Saudi Arabia’s and Brazil’s GDPR-like statutes, ensuring that the cloud identity and access management software market achieves global span.

Competitive Landscape

The five leading vendors, Microsoft, Okta, IBM, Ping Identity, and CyberArk, collectively hold roughly most of global revenue, leaving headroom for niche entrants. Private-equity roll-ups by Thoma Bravo, which blended SailPoint and ForgeRock into a unified stack, illustrate a consolidation wave that favors integrated governance-plus-access suites. Microsoft exploits its Azure Active Directory base of 400 million daily authentications to cross-sell Entra modules at bundle pricing that undercuts point solutions. Okta replies by open-sourcing 7 500 pre-built connectors, courting integrators and shielding customers from vendor lock-in.

Artificial intelligence shapes new battlegrounds. CyberArk embeds machine learning to spot out-of-hours privilege misuse and cut response times to minutes. IBM Security Verify parses access-request tickets with natural-language processing, trimming policy-writing workloads by 60%. Developer-centric entrants like Auth0 win greenfield SaaS customers with drop-in login widgets in 15 languages.

Managed services offset the IAM talent crunch. Deloitte Cyber and IBM Security Services operate outsourced identity operations centers, appealing to mid-market buyers lacking round-the-clock staff. Edge and operational-technology IAM remain fragmented, and decentralized-identity solutions for Web3 lack a clear leader, keeping competitive dynamics fluid in the cloud identity and access management software market.

Cloud Identity and Access Management Software Industry Leaders

Okta Inc.

Microsoft Corporation

IBM Corporation

Ping Identity Holding Corp.

CyberArk Software Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Amazon Web Services added adaptive, hardware-rooted passkey support to IAM Identity Center, extending phishing-resistant authentication to more than 200 million active enterprise users.

- August 2025: Okta agreed to acquire policy-as-code startup Styra for USD 650 million to embed fine-grained Open Policy Agent controls across its Workforce and Customer Identity Clouds.

- April 2025: IBM Security Verify introduced quantum-safe cryptography options for FIDO2 passkeys, allowing enterprises to future-proof authentication workflows against post-quantum threats.

- January 2025: Ping Identity obtained FedRAMP High authorization for PingOne Neo, enabling U.S. federal agencies to adopt its decentralized-identity platform for workforce and citizen services.

Global Cloud Identity and Access Management Software Market Report Scope

The Cloud Identity and Access Management Software Market Report is Segmented by Component (Software, and Services), Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (IT and Telecom, Banking Financial Services and Insurance, Healthcare, Government, Retail and Ecommerce, Manufacturing, Other Industry Vertical), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| IT and Telecom |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare |

| Government |

| Retail and Ecommerce |

| Manufacturing |

| Other Industry Vertical |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Software | ||

| Services | |||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Industry Vertical | IT and Telecom | ||

| Banking, Financial Services and Insurance (BFSI) | |||

| Healthcare | |||

| Government | |||

| Retail and Ecommerce | |||

| Manufacturing | |||

| Other Industry Vertical | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the growth outlook for the cloud identity and access management software market to 2031?

Revenue is projected to rise from USD 10.91 billion in 2026 to USD 26.58 billion by 2031, at a 19.52% CAGR.

Which region is expanding fastest in IAM adoption?

Asia Pacific records the strongest CAGR at 20.32% thanks to strict data-localization mandates in India, China, and Japan.

Why are services gaining traction compared with software licenses?

Enterprises need integration, audit, and managed-operations expertise, driving the services segment to a 19.61% CAGR, outpacing software growth.

How do Zero Trust frameworks influence buying behavior?

Zero Trust mandates continuous identity verification and least privilege, prompting 81% of enterprises to overhaul IAM stacks.

Which industry vertical will grow most quickly through 2031?

Healthcare leads with a 20.74% CAGR as telehealth requires federated patient identities and strict HIPAA compliance.

What challenges slow IAM deployments for smaller firms?

High upfront costs and a shortage of certified specialists remain primary hurdles, especially for SMEs working with limited IT budgets.

Page last updated on: