Cloud Billing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

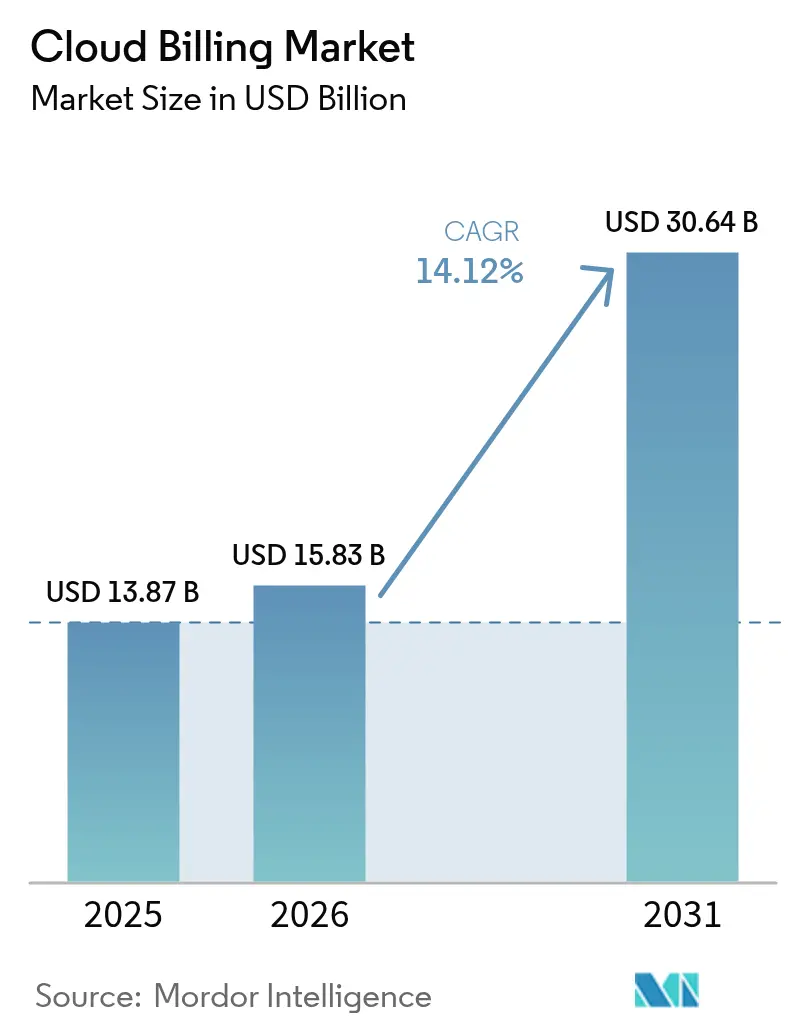

| Market Size (2026) | USD 15.83 Billion |

| Market Size (2031) | USD 30.64 Billion |

| Growth Rate (2026 - 2031) | 14.12% CAGR |

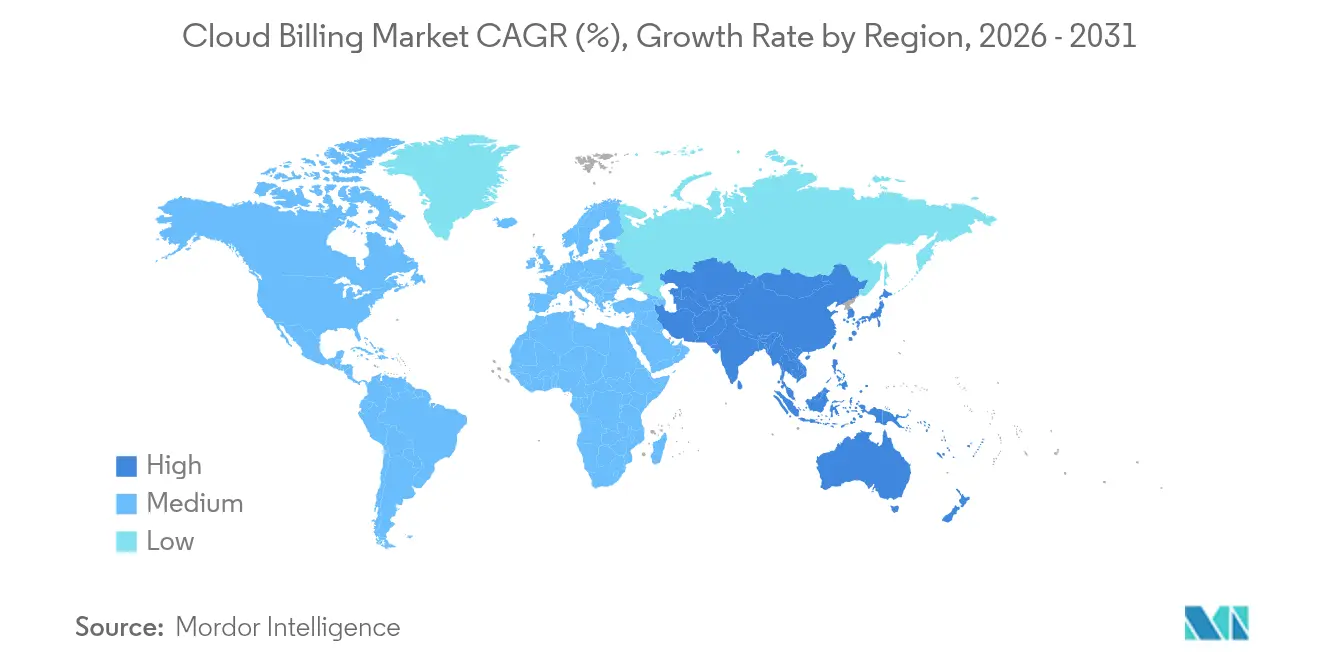

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

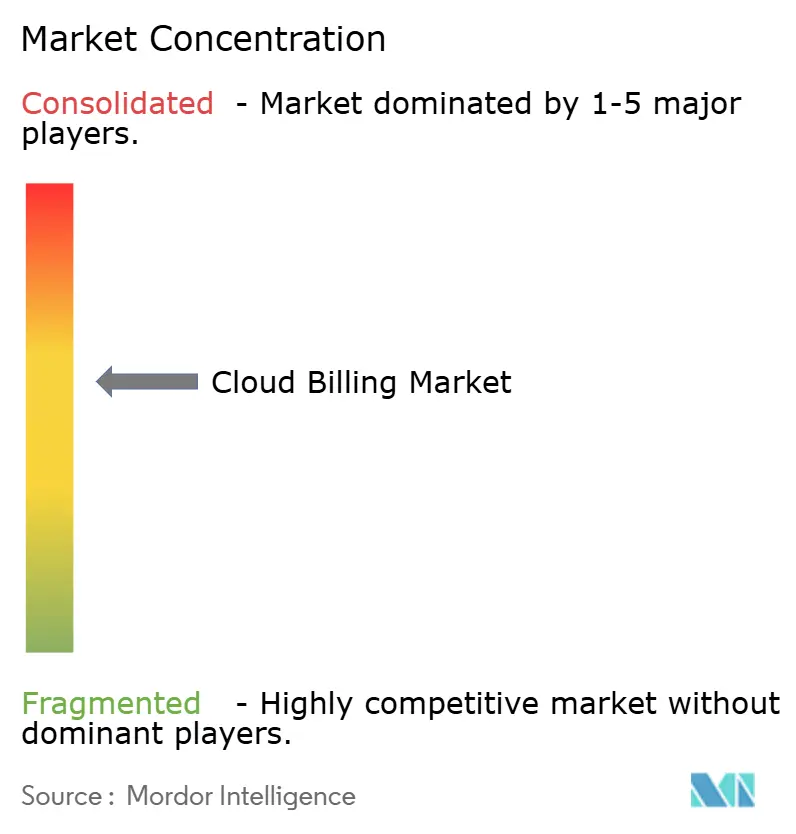

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Billing Market Analysis by Mordor Intelligence

Cloud Billing Market size in 2026 is estimated at USD 15.83 billion, growing from 2025 value of USD 13.87 billion with 2031 projections showing USD 30.64 billion, growing at 14.12% CAGR over 2026-2031. Enterprises are diverting spending toward usage-aligned commercial models that can translate millions of metering records into invoices without latency. Migration toward multi-cloud environments and the attendant demand for granular cost attribution are the pivotal forces behind this double-digit expansion. Heightened infrastructure outlays by hyperscalers, advances in real-time metering, and a pronounced shift from capacity-based to outcome-based purchasing have all amplified the relevance of the cloud billing market. In parallel, specialized vendors that embed machine-learning cost-optimization features are compressing implementation timelines and easing the skills burden on enterprise FinOps teams.

Key Report Takeaways

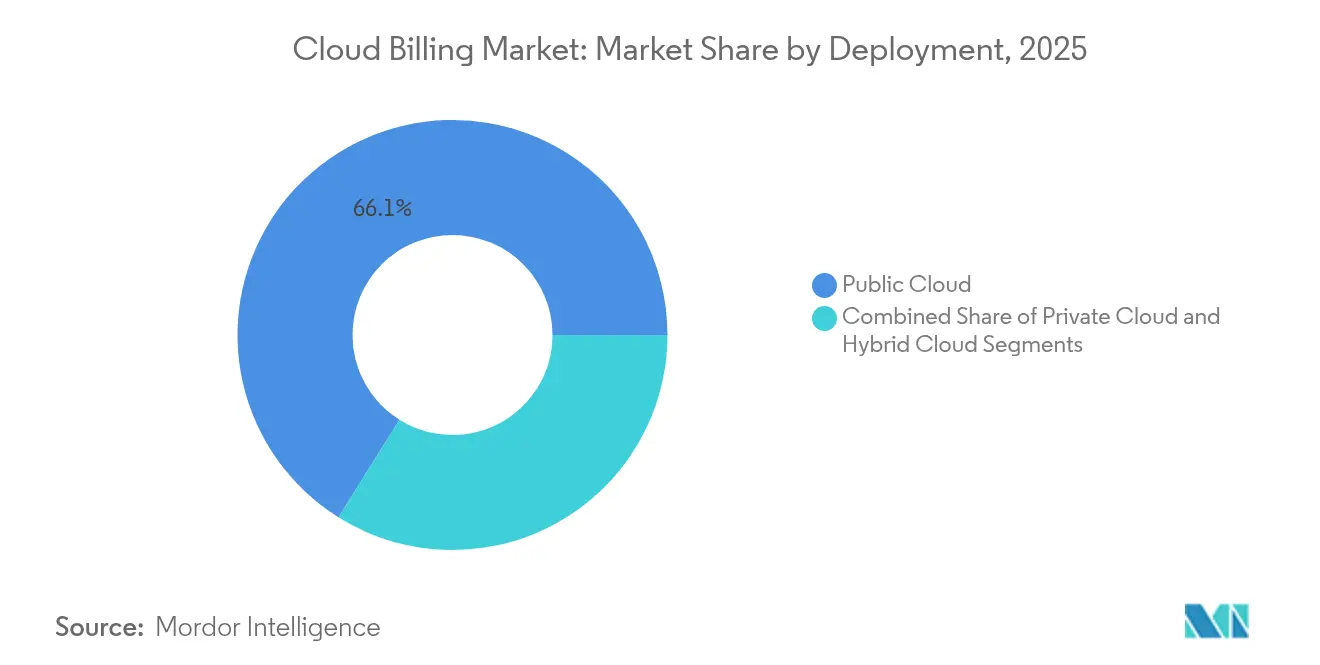

- By deployment, public cloud captured 66.10% of the cloud billing market share in 2025, while hybrid cloud is projected to compound at 15.81% CAGR through 2031.

- By component, platforms held 60.10% revenue in 2025; services are forecast to expand at 16.62% CAGR to 2031.

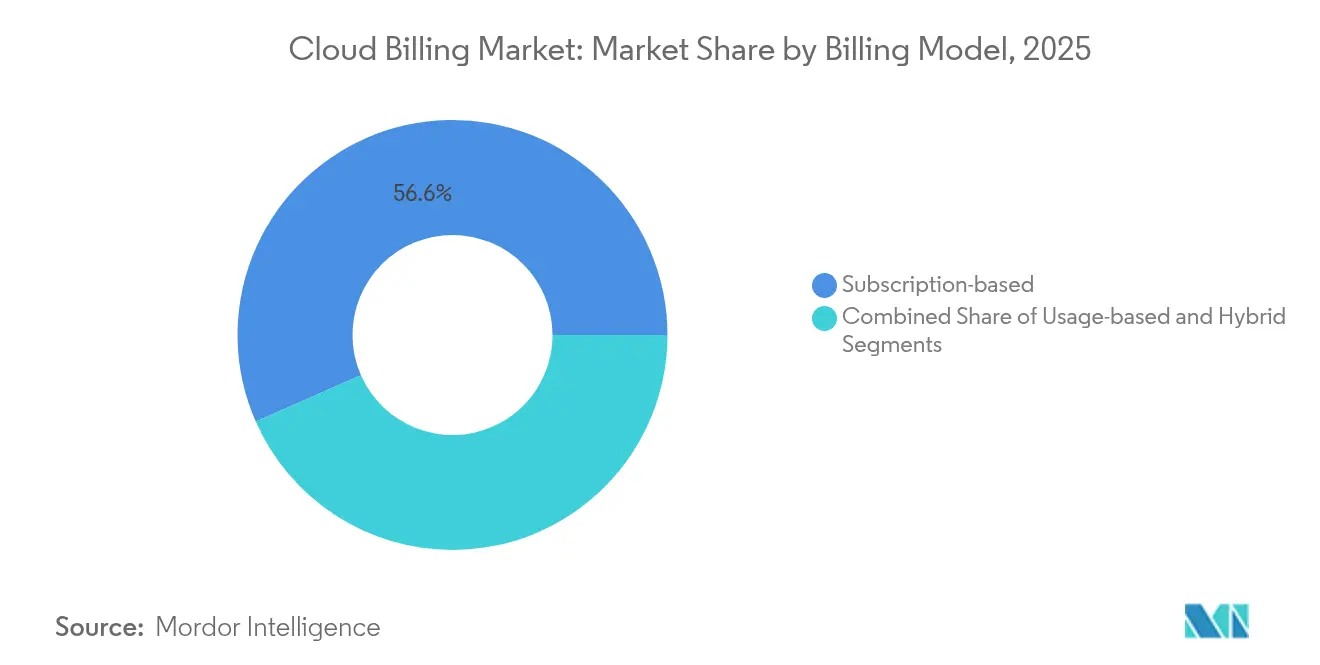

- By billing model, subscriptions commanded 56.60% of the cloud billing market size in 2025; usage-based models will rise at 15.34% CAGR through 2031.

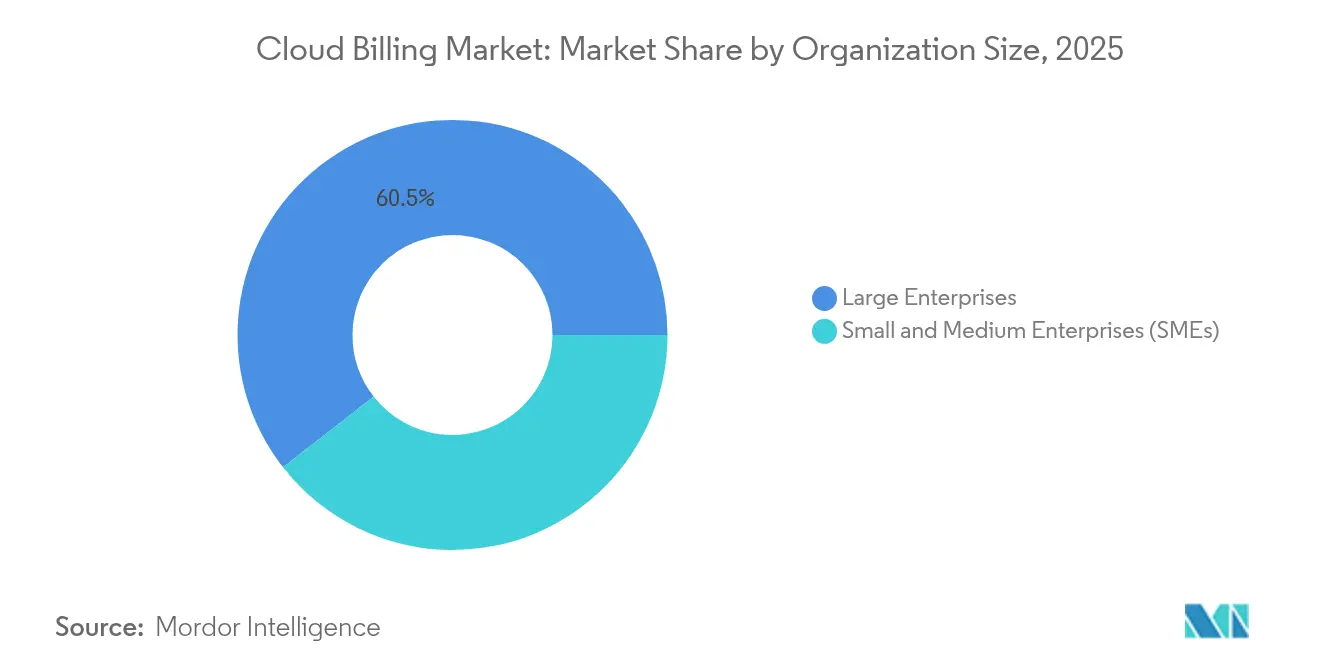

- By organization size, large enterprises controlled 60.55% of 2025 revenues, whereas SMEs are expected to post a 16.86% CAGR up to 2031.

- By service model, SaaS billing produced 46.80% of 2025 sales, and PaaS billing will advance at 16.04% CAGR.

- By end-user industry, retail and e-commerce led with 25.85% revenue in 2025; healthcare is set to grow at 15.78% CAGR.

- By geography, North America accounted for 36.80% of 2025 revenue; Asia-Pacific will accelerate at 16.28% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Billing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating multi-cloud adoption | +3.2% | Global with North America and Europe leading | Medium term (2-4 years) |

| Expansion of e-commerce subscription models | +2.8% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising demand for real-time usage-based pricing | +2.4% | Global, enterprise segments in developed markets | Medium term (2-4 years) |

| Token-based cloud consumption in Web3 | +1.1% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Carbon-aware workload scheduling incentives | +0.9% | Europe, North America expanding to Asia-Pacific | Long term (≥ 4 years) |

| Integration of AI-driven cost optimization engines | +2.6% | North America, Europe, Asia-Pacific enterprises | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Accelerating Multi-Cloud Adoption

Multi-cloud strategies are gaining popularity as organizations distribute workloads to balance resilience, pricing, and data-residency requirements. Policy-driven resource controls inside Kubernetes have demonstrated that finely tuned autoscaling curbs unpredictable spend while maintaining governance.[1]Microsoft, “Allocate Azure Costs,” microsoft.com Billing platforms now reconcile divergent price books, currencies, and taxonomies in real time and supply chargeback reports that promote unit-level accountability. The cloud billing market gains momentum as hyperscalers publish consumption APIs that shorten data ingestion cycles and as enterprises mitigate single-vendor risk by embracing provider diversity. Demand, therefore, concentrates on billing engines that normalise multi-cloud telemetry and present unified dashboards.

Expansion of E-Commerce Subscription Models

Subscription commerce no longer applies exclusively to SaaS. Retailers integrate physical goods, content bundles, and hybrid memberships that require intricate proration, tiered add-ons, and cyclical promotions. Platforms must orchestrate price adjustments triggered by customer behaviour and localise checkout in line with country-specific payment methods, PSD2 mandates, and GDPR obligations.[2]Stripe, “How to Accept Payments in Denmark,” stripe.com Growth in recurring commerce strengthens the cloud billing market by broadening the user base from software publishers to merchants that ship tangible products.

Rising Demand for Real-Time Usage-Based Pricing

Enterprises increasingly favour metered tariffs that mirror actual workload elasticity. Oracle’s elastic ECPU construct is emblematic of this pivot toward fine-grained metrics that supersede coarse commitments. Billing engines must ingest, aggregate, and rate sub-second logs without sacrificing accuracy. The cloud billing market capitalises on this need by embedding streaming-data ingestion and offering predictive insights that prevent bill shocks.

Token-Based Cloud Consumption Models in Web3 Startups

Web3 firms experiment with paying for resources using native tokens that settle instantly on-chain. Smart contracts automate rate adjustments tied to token economics, aligning infrastructure costs directly with application revenue. Although nascent, tokenised payment flows highlight how programmable money can converge with programmable infrastructure, thereby widening the addressable horizon for the cloud billing industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Migration complexities from legacy on-prem | −2.1% | Global, higher in established enterprises | Medium term (2–4 years) |

| Data-sovereignty and cross-border compliance | −1.8% | Europe, Asia-Pacific | Long term (≥ 4 years) |

| Rising FinOps tooling cannibalizing native margins | −1.3% | North America, Europe expanding globally | Short term (≤ 2 years) |

| Vendor lock-in and interoperability challenges | −1.6% | Global, notably in multi-cloud environments | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Migration Complexities from Legacy On-Premises Billing

Long-standing on-prem billing stacks often carry undocumented business logic, making data mapping and rule translation difficult. Enterprises in regulated verticals simultaneously uphold PCI-DSS, SOX, or HIPAA mandates during cut-over, obliging dual-run environments that inflate project budgets. The resource burden deters some organisations from full transition and tempers the near-term expansion pace of the cloud billing market.

Data-Sovereignty and Cross-Border Compliance Costs

Data-protection regimes differ across jurisdictions, and localisation clauses oblige providers to host ledgers in region-bound clusters. Draft guidance, such as NIST SP 800-228, sets stricter API security controls, intensifying development overhead. Continuous audits and redundant hosting can increase the total cost of ownership and slow down procurement in sensitive sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Hybrid Architectures Drive Complexity

Hybrid environments are recording a 15.81% CAGR as organisations pair on-prem assets with hyperscale elasticity. Enterprises value the ability to shift workloads without forfeiting data residency or latency-sensitive processing, yet they often encounter fragmented cost structures. Billing vendors respond by releasing adapters that harmonise private-cloud telemetry with public-cloud rate cards.

Public deployment maintains a 66.10% revenue lead due to its simplicity and broad tooling ecosystems. Nevertheless, compliance triggers, edge use cases, and geopolitics strengthen the case for hybrid spend governance. The cloud billing market, therefore, pivots toward unified orchestration engines that calculate blended effective rates and surface variance reports across locations.

By Component: Services Segment Transforms Market Dynamics

Services revenue is climbing at 16.62% CAGR as enterprises outsource roadmap planning, integration, and optimisation. Providers bundle advisory, implementation, and managed operations that target rapid payback. Platforms continue to dominate with a 60.10% share, yet service-led engagement secures footholds in regulated domains where bespoke controls are pivotal.

The cloud billing market benefits because service specialists translate domain nuances into configuration baselines that shrink deployment risk. Bundled offerings that pair platform licences with lifecycle services foster stickier contracts and unlock expansion into adjacent cost-governance modules such as carbon tracing and partner settlement.

By Billing Model: Usage-Based Pricing Gains Enterprise Traction

Usage-metered billing advances at a 15.34% CAGR, narrowing the gap with subscription, which holds 56.60%. The pattern reflects maturing FinOps practice and management appetite for aligning spend with unit economics. Hybrid constructs that mix a base fee with variable overage draw attention because they deliver predictable revenue without underutilised capacity.

Providers refine high-frequency intake pipelines that rate millions of events with near-zero latency, unlocking possibilities such as pay-per-function or pay-per-token. The cloud billing market size for usage models is forecast to reach USD 12.84 billion by 2031, underscoring sustained demand for flexible tariff engines that can be adjusted without requiring code refactoring.

By Cloud Service Model: PaaS Billing Drives Innovation

PaaS-oriented billing will log 16.04% CAGR, propelled by application modernisation, serverless adoption, and growing reliance on managed AI services. SaaS still leads with 46.80% revenue because of its entrenched subscription base. However, as enterprise developers lean on containers, serverless runtimes, and AI accelerators, PaaS usage grows and requires multidimensional metering such as per-invocation and per-token tracking.

Granular PaaS cost attribution shapes architectural decisions and fosters a culture of fiscal ownership among engineering squads. The cloud billing market thus integrates feature-flag-based routing, enabling teams to experiment on new services while limiting budget exposure. SaaS metering innovations such as seat-flexing and activity-based charges sustain segment vibrancy, creating cross-pollination between service-model categories.

By Organization Size: SMEs Embrace Cloud-Native Billing

SMEs are forecast to outpace large enterprises at 16.86% CAGR, propelled by plug-and-play billing software delivered in SaaS form. Lower cost of entry and templates aligned to common verticals enable these firms to deploy mature billing without hiring specialist staff. Large enterprises still generate 60.55% of 2025 spend because they operate multi-entity structures that demand consolidated invoicing and granular allocation.

The cloud billing market enjoys network effects as SME adoption opens indirect channels through resellers and marketplaces. Simplified APIs and low-code interfaces reduce onboarding friction and foster supplier diversification. Vendors cultivate scaled self-service support that keeps margins intact even on smaller contracts.

By End-user Industry: Healthcare Drives Compliance-Focused Growth

Healthcare is registering a 15.78% CAGR thanks to digital record mandates, telehealth expansion, and audit-ready traceability. The sector demands HIPAA-conformant encryption, immutable logs, and dual-run validations, raising complexity but also enlarging contract size. Retail and e-commerce still occupy 25.85% of revenue because high-volume checkouts, loyalty schemes, and international settlements call for sophisticated billing logic.

BFSI and telecoms consume advanced features such as multi-currency settlement, revenue-share accounting, and customer self-service portals. Energy utilities leverage real-time billing for smart-grid incentives, reflecting convergence between operational data and financial reconciliation. These vertical patterns collectively widen the addressable cloud billing market while rewarding providers that maintain industry-specific compliance expertise.

Geography Analysis

North America generated 36.80% of 2025 revenue and continues to benefit from a concentration of hyperscalers, venture funding, and FinOps talent. The region rewards vendors that comply with frameworks such as SOX and state-level privacy statutes. High usage of AI workloads also catalyzes the adoption of token-metered services, reinforcing demand for real-time rating.

The Asia-Pacific region posts the fastest growth rate of 16.28% CAGR, driven by public-sector digitization, mobile-first consumer bases, and sovereign AI computing initiatives. India’s national GPU programme exemplifies how government grants catalyse cloud capacity that must be monetised through scalable billing. Japan’s carbon-linked battery network highlights regional appetite for merging cost with environmental KPIs. Providers that bundle localisation and language support gain early footholds.

Europe balances GDPR leadership with emerging digital sovereignty plans. Enterprises require local data centres and transparent data-processing chains, so billing platforms that guarantee regional residency gain preference. Initiatives encouraging carbon-aware scheduling drive the cloud billing market toward environmental chargeback reports. Fragmented national rules prolong procurement cycles, yet they also amplify barriers for newcomers and solidify loyalty to vendors adept at navigating compliance nuances.

Regulatory Landscape

Regulation increasingly links cloud billing to mandated portability, security controls, and data-residency rules that shape metering, invoicing, and audit trails across jurisdictions. A key anchor is the EU Data Act (Regulation (EU) 2023/2854), applicable from September 12, 2025, which introduces cloud switching rights and interoperability-related obligations that flow into cloud service agreements, pricing constructs for migration, and supporting technical documentation; it also restricts how switching-related charges can be applied during the transition period leading up to January 12, 2027.

Data-sovereignty policies add operational constraints for billing ledgers and transaction data, particularly for public-sector and regulated workloads. South Africa released its National Data and Cloud Policy in 2024, mandating in-country storage for data tied to national security and sovereignty. In parallel, security and assurance frameworks (for example, NIST cybersecurity guidance and hyperscaler certification programs such as AWS ISO/IEC 27001/27017/27018 and CSA STAR CCM v4 attestations referenced in 2026 updates) remain common procurement gates, influencing which billing platforms and managed services are eligible for enterprise and government deployments.

Value Chain Analysis

The cloud billing value chain begins with usage data generation and collection across IaaS, PaaS, and SaaS environments (metering, tagging, and telemetry APIs), then moves through mediation and rating (normalization, policy enforcement, price-book and contract logic), invoice generation (tax, proration, multi-currency), and downstream settlement and reconciliation (payments, revenue-share, and reporting). Hyperscalers (AWS, Microsoft Azure, Google Cloud, Oracle Cloud Infrastructure) provide the infrastructure layer and native billing primitives, while specialized billing vendors and BSS providers (for example, Ericsson Billing, CSG Converged Mediation, Aria Systems) deliver configurable rating engines and order-to-cash workflows that enterprises and telecom operators extend with domain-specific rules.

System integrators and managed service providers are pivotal in implementation and migration, handling data mapping from legacy stacks and operating dual-run periods to reduce billing risk at scale. Recent ecosystem activity illustrates this handoff: Odido completed a migration of all mobile customers to cloud-native Ericsson Billing hosted on AWS with Wipro as integrator (October 2024), and TIM Brasil partnered with Ericsson to unify billing on a cloud-native Ericsson Billing platform hosted on Oracle Cloud Infrastructure (March 2025). Data and analytics platforms also sit midstream, as shown by Lumos integrating Gotransverse automated billing with Snowflake for centralized data (February 2025), while marketplace distribution and co-sell motions are reinforced by collaborations such as CSG expanding work with AWS to deliver Converged Mediation via AWS Marketplace (June 2025).

Competitive Landscape

The market positions hyperscalers such as AWS, Microsoft Azure, and Google Cloud as foundation vendors because they embed billing directly within their larger service ecosystems. These contenders exploit scale economies and release AI-powered optimisation recommendations that raise switching costs. Specialized pure-plays, including Zuora, Stripe, and Chargebee, differentiate themselves through rapid innovation, vertical templates, and extensive payment method libraries.

Competitive intensity sharpens around capabilities such as streaming ingestion, anomaly detection, and policy-based remediation. Providers now integrate machine learning into their billing engines to predict overspend and trigger automated actions. Strategic alliances also rise, Ericsson collaborates with AWS to modernise telecom billing, illustrating how domain expertise marries hyperscale infrastructure.[4]Ericsson, “How Ericsson and AWS Are Accelerating Digital Transformation and AI Innovation in OSS/BSS,” ericsson.com Vendors with broad API exposure and security certifications aligned to NIST SP 800-228 attract regulated customers seeking risk mitigation.

M&A activity tends to focus on niche analytics and compliance assets that can be integrated into broader suites. The cloud billing market is expected to witness further convergence between cost-management ISVs and payment service providers eager to expand into recurring revenue enablement.

Cloud Billing Industry Leaders

Amazon Web Services (AWS)

Microsoft Corporation (Azure)

Google Cloud Platform

Oracle Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major opportunity area is billing for AI-driven, high-frequency consumption patterns that require token-level and event-level metering, sub-second mediation, and contract flexibility across multi-cloud estates. Evidence of this shift is visible in telecom-focused launches and selections: Mavenir introduced billing-grade infrastructure to meter and monetize AI token consumption within existing BSS environments (June 2026), while Aria Systems and ServiceNow announced an agentic BSS concept combining ServiceNow AI orchestration with Aria real-time billing and monetization for CSPs (June 2026). These initiatives expand addressable use cases beyond traditional subscription proration into dynamic rating for AI, edge, and 5G services where product teams need rapid iteration on pricing without refactoring core systems.

Another whitespace lies in enterprise operating-model convergence between FinOps and billing, where chargeback/showback, allocation, and anomaly controls increasingly span public cloud, SaaS, licensing, and private infrastructure. The FinOps Foundation reported that 98% of practitioners manage AI-related spend and that FinOps scope now formally covers SaaS (90%) and software licensing (64%) as of early 2026, raising demand for billing platforms that can ingest heterogeneous cost and usage signals and support policy-based controls. In telecom and digital service provider modernization, Oracle Cloud Scale Charging and Billing on OCI was selected by KDDI to modernize legacy billing and support 5G and generative AI services (February 2026), and Ishan Technologies selected Oracle Communications for an overhaul integrating charging/billing with order orchestration and fulfillment (May 2026), reinforcing a market opening for cloud-native monetization stacks delivered as modular platforms plus integration services.

Recent Industry Developments

- June 2026: AWS added Cost Explorer historical data retention for accounts in billing groups, preserving access to historical billing data at the original billable rates. This strengthens chargeback accuracy for complex enterprise structures that reorganize payer relationships while maintaining continuity in unit economics and internal reporting.

- April 2026: AWS launched the Passthrough Pricing Plan in AWS Billing Conductor for Billing Transfer users, enabling billing group accounts to view billable data aligned to AWS invoice values. The update improves governance for multi-account operating models where internal pricing and allocation need to reconcile precisely with external invoices.

- October 2024: Odido completed the migration of all its mobile customers to the cloud-native Ericsson Billing platform hosted on AWS, with Wipro acting as the system integrator. The project highlights how large-scale customer migrations are being executed through hyperscaler infrastructure plus specialist billing software and integration partners, accelerating cloud-native monetization programs in telecom.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the cloud billing market covers software and related services that meter usage, rate charges, and generate invoices for cloud delivered products, including subscriptions and consumption based pricing, across end users and regions.

Scope exclusions: Traditional on-premise billing suites that never interface with external clouds are not counted in this market boundary.

Segmentation Overview

- By Deployment

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Component

- Platform

- Services

- By Billing Model

- Subscription-based

- Usage-based

- Hybrid (Subscription + Usage)

- By Cloud Service Model

- SaaS Billing

- PaaS Billing

- IaaS Billing

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-user Industry

- Retail and E-commerce

- BFSI

- Telecommunications

- Healthcare and Life Sciences

- Energy and Utilities

- Government and Public Sector

- Media and Entertainment

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Malaysia

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the demand context and to keep our assumptions realistic before we speak to industry participants. We review public materials such as SEC filings and investor presentations, plus product documentation and pricing pages that show how usage meters, tiers, and add ons are packaged.

To anchor the model to visible signals, we also refer to non-paywalled sources such as US SEC EDGAR filings, US Bureau of Economic Analysis and US Census datasets for IT and software spending context, OECD and World Bank digital economy indicators, ITU connectivity statistics, and relevant standards and cloud governance publications (for example, from NIST). Where needed, paid subscriptions for company financials and news, patent lookups, and an import export shipment level database help with cross checks. These sources are illustrative, and many other public references were also used during data collection, clarification, and validation.

Primary Interviews and Surveys

Primary work is used to confirm what the market really includes, how billing modules are priced, and how adoption differs by enterprise size and regulated industries. We speak with a mix of billing platform providers, cloud service ecosystem participants, system integrators, and enterprise buyers across major regions so assumptions on attach rates, discounting, and usage mix can be checked and then adjusted.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | APAC: 46% |

| Mid tier: 46% | Functional/Unit leaders: 40% | EMEA: 32% |

| Smaller Players: 18% | Managers: 48% | Americas: 22% |

Market-Sizing & Forecasting

Market sizing starts from a top-down build where cloud software spend and digital transformation budgets are reconstructed by region and then filtered through billing and revenue management adoption in cloud-first delivery. To avoid overstating value, the model is then corroborated with selective bottom-up approximations, including sampled price book checks, typical module bundles, and volume proxies based on enterprise counts and cloud workload growth.

Key inputs used in the model include the mix of subscription versus usage based charging, average contract duration and renewal patterns, the share of enterprises running multi cloud environments, integration intensity with ERP and CPQ tools, and typical discount ranges by deal size. Where product pricing is tiered, we normalize to an implied ASP curve so very large customers do not get counted at list price. For forecasting, scenario analysis is applied, followed by a simple multivariate regression check using cloud spend growth, enterprise SaaS penetration, and connectivity indicators, with the final trajectory aligned to what primary respondents view as achievable under base case conditions. When bottom-up signals are missing for smaller geographies, we bridge gaps using peer country adoption ratios and then recheck outcomes against regional IT spending totals.

Data Validation & Update Cycle

Validation is handled through several passes, starting with triangulation across the demand build, pricing logic, and independent growth indicators so outliers are caught early. Analysts run variance checks by region and by customer cohort, and any abnormal jumps are traced back to a specific assumption such as attach rate, discounting, or currency conversion timing.

Before sign-off, a second analyst reviews the model trail and the narrative so calculations match the stated market boundary. Reports are refreshed annually, and interim updates are triggered when material events shift pricing, packaging, or adoption, followed by quick re-contacts with select respondents to confirm impact. Right before delivery, we do a final sweep of recent public updates so clients receive the most current view available.

Mordor Intelligence's Cloud Billing Market Sizing Compared With Other Published Estimates

Published market sizes for cloud billing can look far apart even when the topic name is the same, because the counted revenue streams and pricing treatment are not always aligned. Differences usually come from what is included as cloud billing, the year used for currency conversion, and whether the pricing curve reflects real world discounting.

When refresh timing is slower, older price points and exchange rates can stay in the model longer, which changes totals even if growth rates look similar, and this is one reason the 2026 value in Mordor Intelligence is higher than some other published figures. Another driver is ASP logic, where some estimates lean on list pricing or broader revenue management suites, while our approach keeps billing value tied to metering, rating, and invoicing functions that are actively used for cloud delivered services.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.83 B (2026) | |

| Global Consultancy A | USD 9.00 B (2026) | Uses a narrower pricing and revenue capture view, and may apply list pricing or earlier-year currency conversion, which can reduce the implied ASP and total market value for the same year. |

| Industry Publisher B | USD 20.59 B (2029) | Different base year and forecast horizon, with a higher growth assumption and possible inclusion of adjacent revenue management functions, which inflates the later-year figure versus a billing-only scope. |

Overall, the spread is mainly explained by timing and scope, not by a single right or wrong number. By keeping pricing normalization, currency timing, and validation checks traceable to specific adoption and usage signals, the resulting estimate stays easier to reproduce and to update when market conditions change.

Key Questions Answered in the Report

What is the current size of the cloud billing market?

The cloud billing market reached USD 15.83 billion in 2026 and is forecast to achieve USD 30.64 billion by 2031, advancing at 14.12% CAGR.

Which deployment model is growing fastest within the cloud billing market?

Hybrid cloud billing solutions are expanding at 15.81% CAGR as enterprises orchestrate costs across on-prem and public-cloud resources.

Why are usage-based pricing models gaining traction?

Enterprises want charges that mirror real consumption, reducing idle capacity costs and aligning spend with output, which propels usage-metered growth at 15.34% CAGR.

Which region shows the highest growth potential?

Asia-Pacific is projected to post a 16.28% CAGR through 2031, driven by government infrastructure programmes and rapid digital adoption.

How are SMEs influencing the cloud billing market?

SMEs, empowered by low-code SaaS billing platforms, will grow at 16.86% CAGR and democratise access to advanced cost-management capabilities.

What technologies differentiate leading cloud billing providers?

Leaders integrate AI-based anomaly detection, real-time data streaming, and carbon-aware cost reporting to improve accuracy and transparency.

Page last updated on: