Goat Milk Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

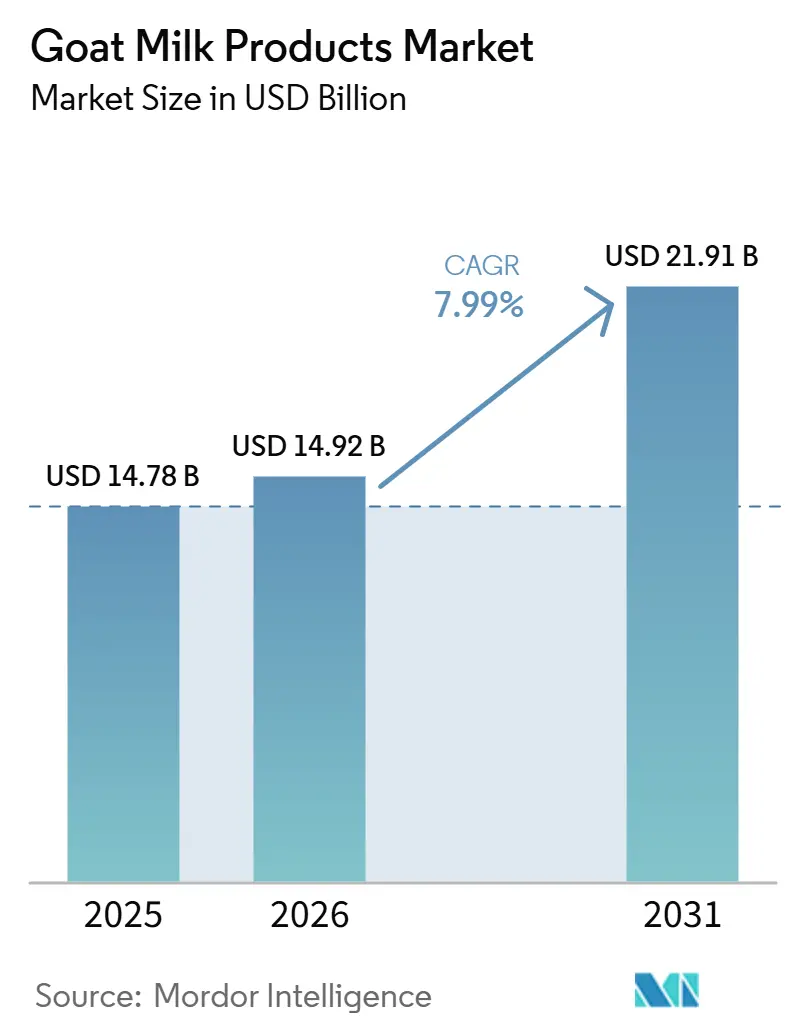

| Market Size (2026) | USD 14.92 Billion |

| Market Size (2031) | USD 21.91 Billion |

| Growth Rate (2026 - 2031) | 7.99% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Goat Milk Products Market Analysis by Mordor Intelligence

The goat milk market size is projected to grow from USD 14.78 billion in 2025 to USD 14.92 billion in 2026, reaching USD 21.91 billion by 2031, with a CAGR of 7.99% during 2026-2031. Regulatory approvals for goat milk ingredients in infant nutrition, investments in spray-drying technology to enhance powder production, and smart-farming incentives across the Asia-Pacific region are driving both demand and supply growth. In the United States and Canada, lighter regulatory requirements have facilitated access to mainstream retail channels, while the rapid adoption of e-commerce has expanded the availability of premium-priced niche products, even in cost-sensitive markets. Processors with vertical integration are better positioned to manage challenges such as seasonality, kid mortality risks, and fragmented farm structures. Packaging has evolved into a key differentiator, with recyclable mono-material stand-up pouches and low-carbon foil lids enhancing brand sustainability, reflecting trends already seen in premium artisanal cheese products. Competitive pressure is most pronounced in milk powder exports, while artisanal cheeses and functional yogurts continue to provide viable opportunities for smaller brands with strong provenance narratives.

Key Report Takeaways

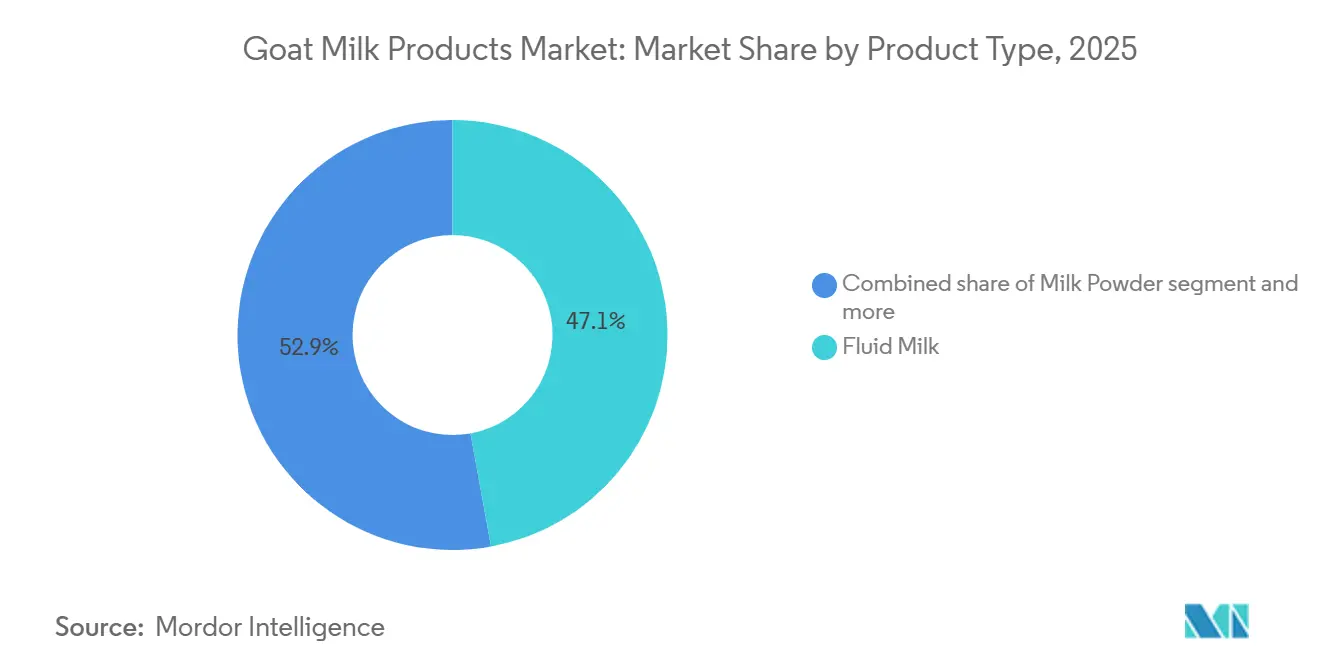

- By product type, fluid milk led with 47.13% of the goat milk market share in 2025; milk powder is projected to expand at an 8.18% CAGR through 2031 in Asia-Pacific and Europe.

- By packaging, tetra pack captured 36.19% revenue share in 2025, while stand-up pouches are forecast to grow at an 8.58% CAGR on sustainability uptake in Europe and Latin America.

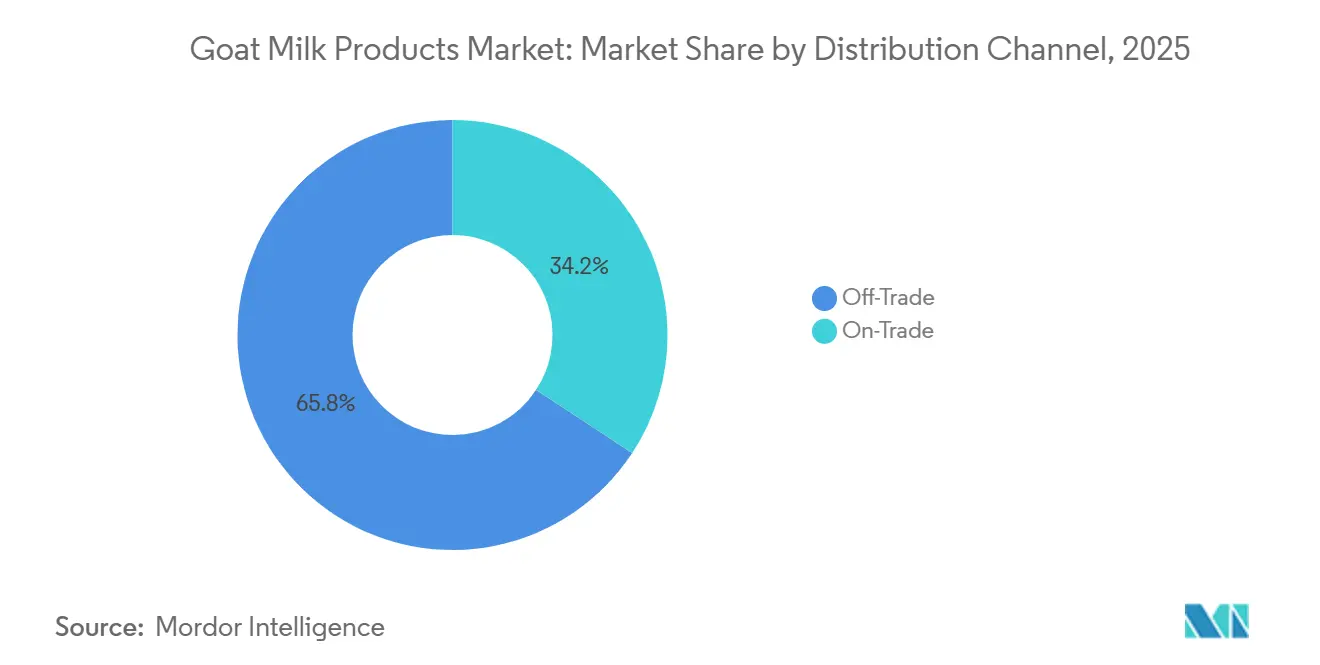

- By distribution, off-trade channels accounted for 65.76% of turnover in 2025, and are advancing at a 9.07% CAGR as e-commerce deepens penetration in China, India, and the Gulf.

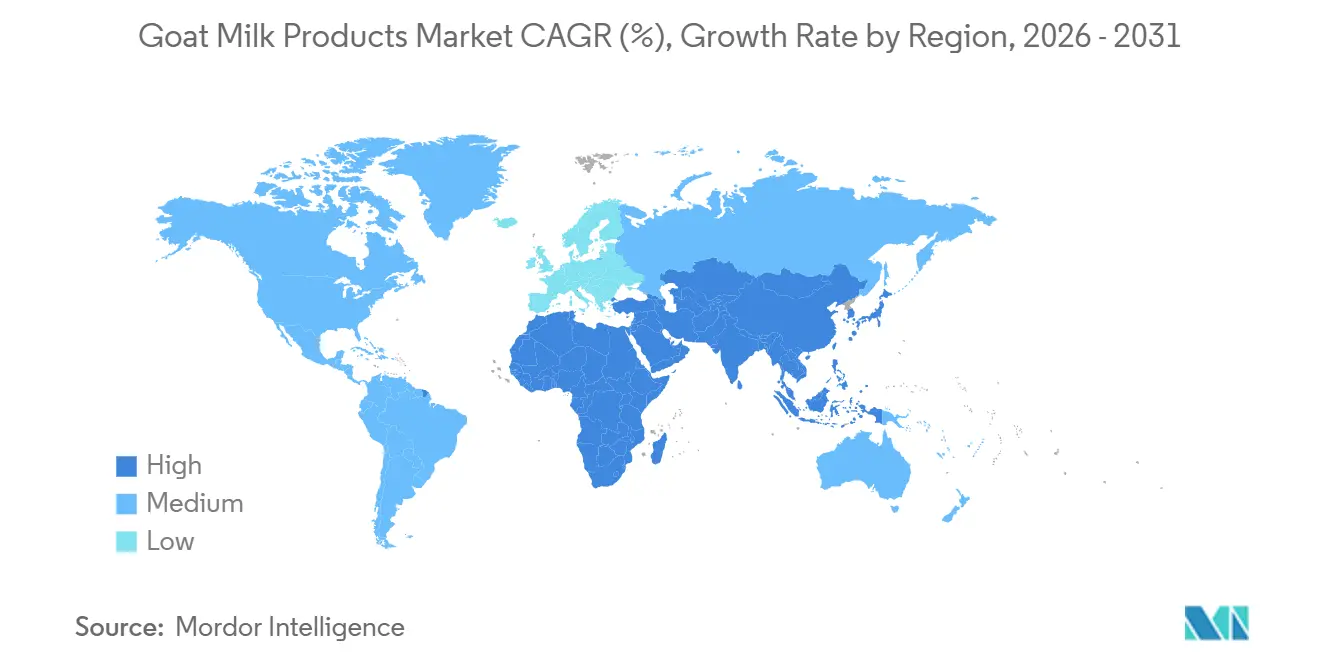

- By geography, Asia-Pacific commanded 39.40% of global sales in 2025, whereas the Middle East and Africa region is expected to post the fastest 8.41% CAGR between 2026 2031, led by Saudi Vision 2030 dairy investments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Goat Milk Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing lactose intolerance and cow milk allergy cases | +1.8% | Global, higher in North America and Europe | Long term (≥ 4 years) |

| Rising awareness of functional health benefits | +1.2% | North America, Europe, affluent Asia-Pacific | Medium term (2-4 years) |

| Expansion of infant nutrition applications | +0.9% | Global | Long term (≥ 4 years) |

| Health and digestibility advantages vs. cow milk | +0.8% | Asia-Pacific, Middle East and Africa, parts of North America | Medium term (2-4 years) |

| Government incentives for small-ruminant dairying | +0.7% | North America, Europe, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Premiumization of specialty goat milk products | +0.6% | Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing lactose intolerance and cow milk allergy cases

Globally, the increasing prevalence of lactose intolerance and cow milk allergies is driving the growth of the goat milk products market. Approximately 65–68% of the global population experiences some degree of lactose malabsorption, with rates exceeding 70% in many Asian, African, and Middle Eastern countries [1]Source: World Population Review, "Lactose Intolerance by Country", worldpopulationreview.com. For individuals with lactose intolerance, traditional cow's milk can cause symptoms such as bloating, cramps, and diarrhea, while others may experience allergic reactions. As a result, many consumers are opting for alternative dairy products. Goat milk, which naturally contains lower levels of lactose and has distinct protein structures, presents a reduced risk of allergic reactions, making it a preferred alternative. This trend is further supported by increased health awareness, the introduction of more lactose-free products by major food companies, and a global shift towards personalized nutrition. Consequently, the demand for goat milk and its derivatives is rising, particularly in regions with high rates of lactose intolerance, reinforcing its position as a digestible and nutritionally beneficial dairy option.

Premiumization of specialty goat milk products

Affluent consumers are increasingly prioritizing artisanal texture, traceability, and clean-label attributes, enabling brands to charge premiums of up to 30% over mass-market dairy products. As demand grows for unique, high-quality alternatives to traditional dairy, brands are expanding their offerings to include artisan cheeses, probiotic yogurts, high-protein beverages, and products that are organic or feature clean labels. These offerings often differentiate themselves through fortification, distinctive regional flavors, and eco-friendly packaging. By enhancing the appeal of goat milk products, brands cater to health-conscious and younger consumers while positioning themselves to command premium pricing and build stronger brand loyalty. This trend is gaining traction globally, supported by the growth of e-commerce and specialty retail channels. Marketing efforts emphasizing goat milk's digestibility, hypoallergenic properties, and sustainability further drive this premiumization trend, appealing to both everyday consumers and those seeking health-focused options. Continued investments in herd genetics, on-farm cold storage, and microfiltration technology ensure flavor consistency and support premium product tiers, contributing to margin stability in the goat milk products market.

Health and digestibility advantages vs. cow milk

Goat milk is gaining recognition in the global market for its health benefits and superior digestibility, often positioning itself as an alternative to cow milk. Its smaller fat globules and higher concentration of short- and medium-chain fatty acids contribute to the formation of a softer curd, which facilitates easier digestion. This makes goat milk particularly suitable for individuals with sensitive stomachs or digestive issues. Nutritionally, goat milk offers higher levels of essential minerals and vitamins, such as calcium, vitamin A, potassium, and vitamin B6, often exceeding those found in cow milk. It also provides higher protein content per serving and nutrients that are more easily absorbed by the body. Studies suggest that goat milk is less likely to cause allergic reactions compared to cow milk. Furthermore, its prebiotic oligosaccharides support the growth of beneficial intestinal bacteria, promoting improved gut health. These attributes are driving the growing global demand for goat milk products, as consumers increasingly seek nutrient-dense and digestion-friendly options. Research highlights that goat milk contains higher levels of calcium, medium-chain fatty acids, and antimicrobial peptides compared to cow milk. Additionally, FDA guidance on goat milk ice cream allows companies to highlight specific micronutrient claims, further distinguishing these products from cow dairy [2]Source: Code of Federal Regulations, ecfr.gov. These scientific findings reinforce brand messaging that appeals to health-conscious consumer segments.

Government incentives for small-ruminant dairying

In rapidly growing economies such as India and parts of Africa, government incentives are driving the growth of the global goat milk products market. Initiatives like India's National Livestock Mission (NLM), the Goat Development Scheme, and the National Programme for Dairy Development (NPDD) are key contributors. These programs provide various forms of support, including direct financial assistance, subsidies of up to 50% (with higher rates for marginalized groups), low-interest loans, infrastructure grants, and capacity-building initiatives for both new and experienced goat farmers[3]Source: Alpine Goats Farms, "Government Schemes & Subsidies for Goat Farming in India: A Complete Guide for 2025", alpinegoatsfarms.in. Such measures reduce the financial strain on smallholders and entrepreneurs aiming to establish or upgrade their herds while improving access to quality breeding stock, veterinary services, and feed resources. This support enhances productivity and facilitates greater participation in the market. Additionally, government-backed animal health and irrigation programs mitigate risks related to diseases and climate, further stabilizing and professionalizing the small-ruminant dairy sector. As a result, these incentives not only boost rural employment and encourage sustainable farming practices but also integrate small-scale producers into formal goat milk supply chains. This integration significantly contributes to the growth and modernization of the global goat milk products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited large-scale supply chain and seasonality | -1.1% | Global, stronger in developing regions | Medium term (2-4 years) |

| Price premium over cow dairy | -0.8% | Price-sensitive Asia-Pacific and South America | Long term (≥ 4 years) |

| Lack of harmonised export standards | -0.7% | EU-Asia trade corridors | Short term (≤ 2 years) |

| High kid-mortality rates constraining supply | -0.6% | Developing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited large-scale supply chain and seasonality

The global goat milk products market faces restraints due to a limited large-scale supply chain infrastructure and the seasonality of production. Unlike cow milk, goat milk production is less industrialized and primarily sourced from smallholder farms rather than large-scale integrated operations. This fragmented structure results in higher production costs, logistical inefficiencies, and irregular availability of raw milk for processors and buyers. Disruptions such as pandemics or transportation issues can further impact the supply chain, leading to delays, shortages, and price fluctuations. Additionally, goat milk production is affected by breeding cycles, causing inconsistent raw milk supply, which complicates processing schedules and inventory management for retailers. The predominance of smallholder farms contributes to batch variability, higher collection costs, and the need for larger safety-stock inventories in downstream channels. Moreover, modern cold-chain facilities are concentrated in urban areas, leaving rural regions susceptible to spoilage and quality degradation, which can harm brand reputation. To address these challenges, integrators are adopting cooperative pooling hubs and UHT technology. However, the high capital requirements for these solutions hinder their widespread implementation in less-developed markets.

Price premium over cow dairy

Goat milk products, despite increasing awareness of their health benefits, face challenges due to their premium pricing compared to cow dairy products. Several structural factors contribute to these higher prices, including significantly lower global production volumes, underdeveloped economies of scale, higher feed and animal care costs, and a more fragmented supply chain. Unlike the cow dairy industry, which benefits from industrialization and efficiency, goat farming is predominantly small-scale and regionally concentrated. This results in higher per-unit costs throughout the supply chain, from production to retail. Additionally, the seasonal nature of goat milk supply and transportation or import costs, particularly in countries with insufficient domestic production- further widens the price gap. As a result, goat milk products are often perceived as niche items, categorized as specialty or premium products. This perception limits their affordability for price-sensitive consumers and restricts their availability in mainstream retail channels. In emerging markets, where price sensitivity is especially high, the premium pricing of goat milk products poses a significant barrier, impeding broader market penetration and slowing growth compared to the more affordable cow dairy alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fluid Milk Dominance Meets Powder Innovation

Fluid milk accounted for 47.13% of the goat milk products market size in 2025, driven by strong consumer demand for fresh, minimally processed nutrition. Households in North America and Europe are willing to pay premiums for bottled goat milk available in health-food aisles, prompting dairy cooperatives to expand pasteurization capacity and enhance direct-to-consumer delivery channels. Goat milk is perceived as a highly nutritious beverage due to its essential vitamins and minerals, including potassium, calcium, and iron. Additionally, its health benefits, such as improved digestion, lower allergenicity, and higher digestibility compared to cow’s milk, contribute to its dominant position in the market.

Milk powder, while representing a smaller segment, is projected to grow at a CAGR of 8.18% through 2031. This growth is supported by its application in infant formula and clinical-nutrition sachets, which facilitate global shipping and emergency-relief stockpiling. The variety of product formats strengthens the goat milk products market's resilience against isolated demand fluctuations. Advancements in spray-drying technology, enzymatic standardization, and lipid microencapsulation enhance the functional benefits of powdered goat milk, particularly for neonatal and geriatric applications. Global brands emphasize oligosaccharide content on product labels to attract consumers focused on digestive health, a feature less practical for fluid milk due to storage constraints. As a result, processors adopt hybrid strategies, balancing high-margin fluid milk sales with stable export revenues from milk powder. These strategies help manage seasonal raw milk supply fluctuations, ensuring revenue diversification and supporting the long-term growth of milk powder within the goat milk products market.

By Packaging: Tetra Pack Leadership Challenged by Flexible Innovation

Tetra Pak cartons accounted for 36.19% of the goat milk products market share in 2025, driven by their aseptic filling and tamper-evident seals that extend shelf life without refrigeration. This segment leads the goat milk products packaging market due to its ability to provide extended shelf life, making it suitable for regions with limited cold chain infrastructure and for export purposes. Additionally, Tetra Pak cartons are lightweight, cost-effective, and less prone to breakage compared to glass bottles and tins, which helps reduce shipping and handling costs. The convenience they offer, being easy to open, reseal, and store, further enhances their appeal to consumers. Moreover, Tetra Pak is widely regarded as a more sustainable option due to its recyclability.

Stand-up pouches are expected to achieve a CAGR of 8.58% through 2031, supported by their lighter weight compared to cartons, reduced freight emissions, and single-serve convenience, which is particularly favored by younger consumers. Manufacturers are collaborating with film suppliers to incorporate mono-material laminates, improving recyclability and aligning with emerging Extended Producer Responsibility (EPR) mandates in the European Union. These advancements are enhancing the functionality of stand-up pouches, making them a promising packaging option. Diversification in packaging formats strengthens shelf presence and enables brands to address various consumer needs, thereby enhancing competitive positioning in the goat milk products market.

By Distribution Channel: Off-Trade Dominance Accelerates

In 2025, off-trade channels account for a significant 65.76% market share, highlighting their effectiveness in reaching a broad consumer base. This success is rooted in a robust retail infrastructure that ensures product availability and fosters consumer trust. Goat milk products benefit from this established distribution network, avoiding the need for substantial infrastructure investments. Supermarkets and hypermarkets, key players in this channel, not only drive sales but also serve as platforms for consumer education. Through strategic product placements and promotions, they introduce mainstream consumers to goat milk alternatives. This dominant position provides logistical and inventory management advantages, surpassing smaller specialty channels.

Off-trade channels are projected to be the fastest-growing segment, with an expected CAGR of 9.07% from 2026 to 2031. This growth is driven by the expansion of e-commerce and government initiatives aimed at strengthening rural retail infrastructure. These efforts enhance product accessibility, particularly in underserved markets. For instance, India's National Livestock Mission facilitates connections between rural producers and urban consumers, enabling smoother transactions through organized retail channels. Similarly, USDA programs, such as the Dairy Forward Pricing Program, provide dairy processors with risk management tools, reinforcing their market position. The online retail segment within off-trade channels is experiencing rapid growth, supported by government investments in digital infrastructure. Improved internet connectivity in rural areas, often the hub of goat farming, enables direct-to-consumer sales, reducing reliance on traditional intermediaries. This development further strengthens the market's growth trajectory.

Geography Analysis

Asia-Pacific accounted for 39.40% of the goat milk products market in 2025, supported by India’s 6 million-ton production and strong household consumption in China and Pakistan. India’s 50% capital subsidy for breeding farms under the National Livestock Mission has facilitated the development of cold-chain infrastructure and improved sanitary milking practices, enhancing both production volume and quality. In China, the implementation of the National Food Safety Standards in 2026, which limits reconstituted imports, is expected to increase demand for premium domestically sourced goat milk powders. Meanwhile, Pakistan’s rural micro-financing initiatives are transitioning subsistence goat farming into semi-commercial dairying, improving household incomes and ensuring a more reliable local supply.

The Middle East and Africa region is projected to achieve a compound annual growth rate (CAGR) of 8.41% from 2026 to 2031, driven by urbanisation, rising disposable incomes, and halal-certified goat dairy exports to Gulf Cooperation Council (GCC) countries. Sudan and Nigeria are experiencing double-digit herd growth, supported by agri-development bank credit for breeding stock and fodder. Additionally, pan-Arab e-commerce platforms are introducing value-added goat yogurt products to expatriate communities. The harmonisation of product codes under the African Continental Free Trade Area is expected to streamline intra-regional trade, reduce seasonal supply deficits, and enhance intra-African trade in goat milk products.

North America is experiencing steady mid-single-digit growth, supported by sophisticated retail networks, broad insurance coverage for allergy-specific formulas, and USDA export support programmes. The United States’ USD 8.2 billion dairy export tally in 2024 positions goat milk powders to penetrate Mexico and Canada under USMCA tariff preferences. Europe continues to nurture artisanal cheese culture; subsidies for Natura 2000 grazing land indirectly bolster free-range goat herds, reinforcing environmental credentials sought by eco-conscious shoppers. South America’s regulatory simplification in Argentina and Brazil unlocks containerised exports to Asia, positioning the region as a seasonal counter-supply node that moderates global spot-price volatility in the goat milk products market.

Competitive Landscape

The goat milk products market is highly fragmented, with companies like Emmi Group focusing on vertical integration by owning farms, processing facilities, and distribution networks. This approach ensures raw milk security and supports product innovation. Market players are also enhancing their processing capabilities to strengthen their competitive position. For instance, Canadian cooperative Gay Lea Foods expanded its goat cheese production capacity through a partnership with the Ontario Dairy Goat Co-operative, ensuring a steady supply of milk and improving its bargaining power with retailers.

Strategic collaborations in packaging are also notable. Australian dairy-tech company Pact Group provides mono-material pouches to New Zealand's Oete Goat Dairy, reducing plastic usage by 25% and supporting shared environmental sustainability goals. Additionally, Saputo leverages research and development synergies across its specialty cow- and goat-dairy portfolios. The company is piloting UV-treated whey in cross-functional product lines following the FDA's acceptance of its additive petition.

Digital traceability platforms, such as OriginTrail, utilize blockchain technology to authenticate farm-level data. This enables exporting processors to access premium markets where origin verification is a requirement. Overall, agility, quality assurance, and regulatory compliance are key success factors influencing competition within the goat milk products market.

Goat Milk Products Industry Leaders

-

Ausnutria Dairy Corporation Ltd.

-

Emmi AG

-

Saputo Inc.

-

Lactalis Group

-

Granarolo S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kabrita, a prominent goat milk formula brand, has introduced a new product globally: Kabrita High-Calcium Adult Goat Milk Powder. This product, manufactured in Australia, is made using milk powder sourced exclusively from Kabrita's goat farm in the Netherlands. Australia has been selected as the initial launch market for this product.

- November 2024: Montchevre, a goat cheese brand owned by Saputo, has launched two new cheeses in the U.S. market. Among these, the Cold Brew & Donuts goat cheese is notable as the only cold brew-flavored goat cheese available. This cheese combines rich coffee flavors with a subtle doughnut-like sweetness, making it suitable for desserts, snacks, and breakfast.

- September 2024: LittleOak Company, based in New Zealand, has introduced its Natural Goat Milk Toddler Drink in a sachet format to the U.S. market, marking a first in this category. Produced in New Zealand, LittleOak’s From Fresh sachets utilize a Fresh processing method, derived from fresh whole goat milk. Certified by POFCAP as the world’s first toddler milk to be 100% Palm Oil Free, LittleOak leverages the natural benefits and lower lactose content of goat milk.

Global Goat Milk Products Market Report Scope

| Fluid Milk |

| Cheese |

| Milk Powder |

| Yogurt |

| Butter and Ghee |

| Ice Cream and Desserts |

| Glass Bottle |

| Tetra Pack |

| Stand up Pouches |

| Tins |

| On-trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Specialty/Gourmet Stores | |

| Online Retail/E-commerce | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Russia | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Iran | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Fluid Milk | |

| Cheese | ||

| Milk Powder | ||

| Yogurt | ||

| Butter and Ghee | ||

| Ice Cream and Desserts | ||

| By Packaging | Glass Bottle | |

| Tetra Pack | ||

| Stand up Pouches | ||

| Tins | ||

| By Distribution Channel | On-trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Specialty/Gourmet Stores | ||

| Online Retail/E-commerce | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Iran | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the goat milk products market?

The goat milk products market size is USD 14.92 billion in 2026 and is projected to reach USD 21.91 billion by 2031.

Which region leads global demand?

Asia-Pacific leads with 39.40% share in 2025, anchored by India, China, and Pakistan.

Why are goat milk products priced higher than cow dairy?

Lower per-animal yields, higher feed conversion costs, and limited economies of scale contribute to its' price premium

How are governments supporting industry expansion?

Incentives such as India’s 50% capital subsidy for goat breeding farms and U.S. risk-management programs reduce producer costs and stabilize revenues.

Page last updated on: