Buttermilk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

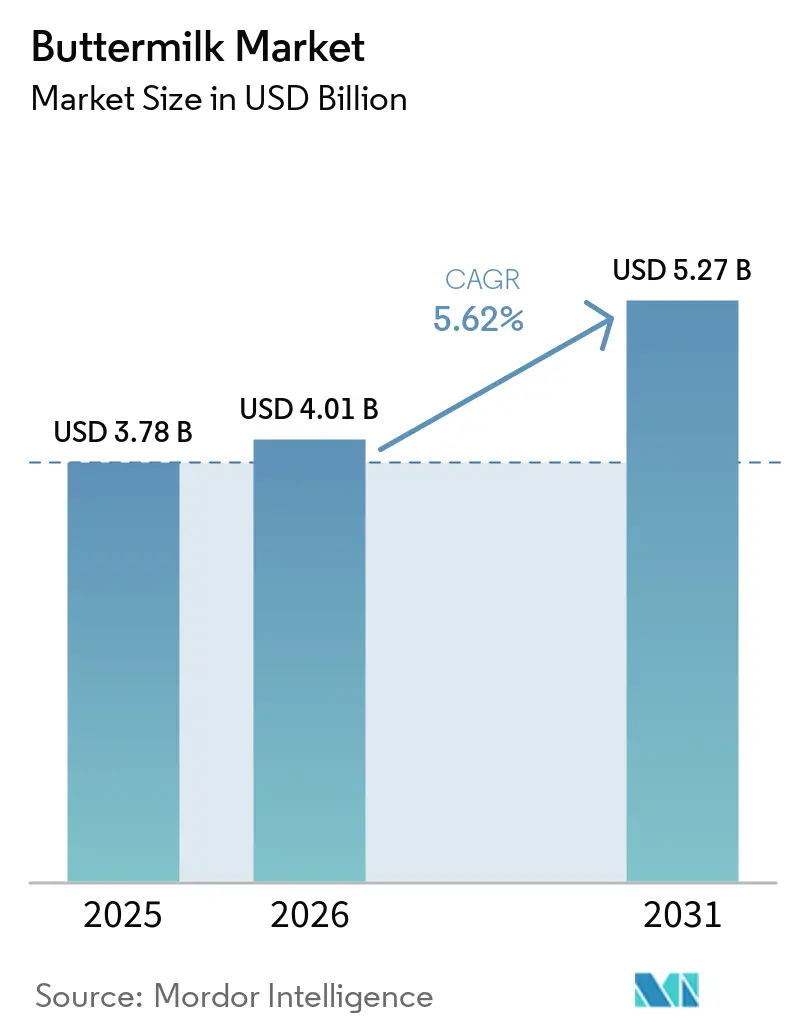

| Market Size (2026) | USD 4.01 Billion |

| Market Size (2031) | USD 5.27 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

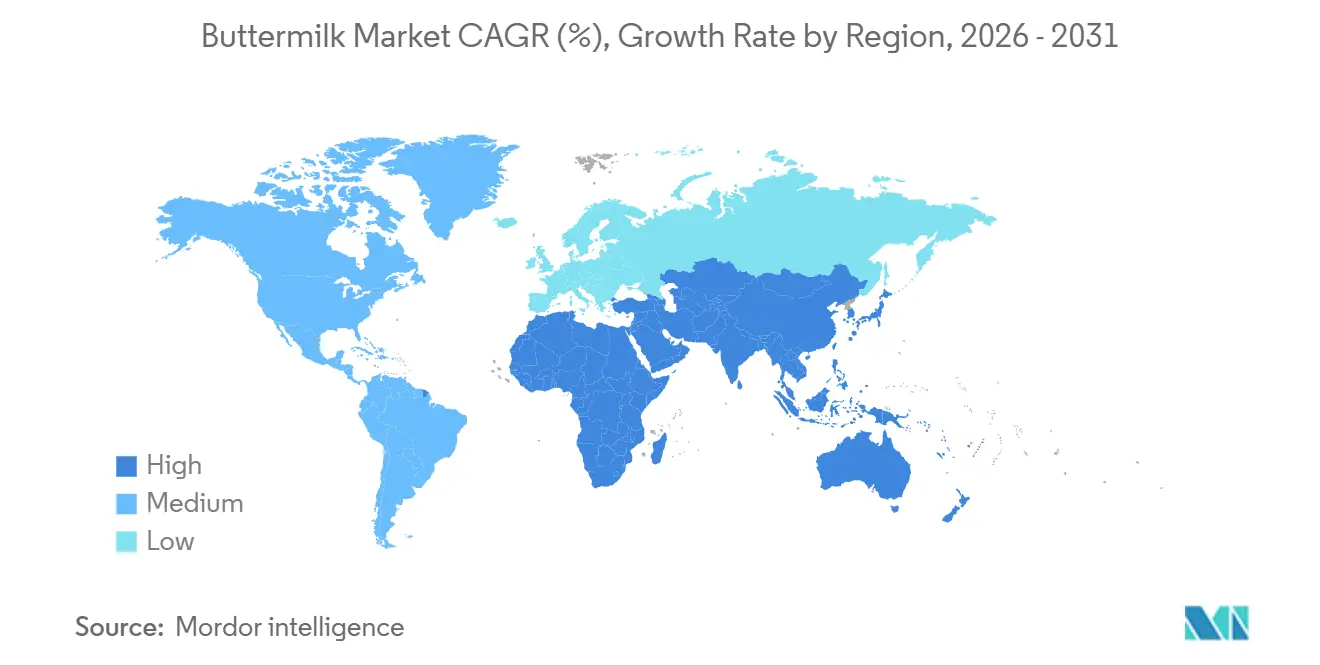

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Buttermilk Market Analysis by Mordor Intelligence

The Buttermilk market size is expected to increase from USD 3.78 billion in 2025 to USD 4.01 billion in 2026 and reach USD 5.27 billion by 2031, growing at a CAGR of 5.62% over 2026-2031. Amid shifting consumer preferences and regulatory pressures, the market showcases resilience, with buttermilk's unique position as both a traditional dairy staple and a sought-after functional ingredient fueling its diverse demand. While Asia-Pacific stands as the dominant revenue center, Europe is witnessing the quickest growth, spurred by accelerating product innovations in response to sustainability mandates. The EU's Green Deal, emphasizing dairy by-product utilization, is bolstering buttermilk's reputation as a sustainable ingredient. This is especially true as processors aim to derive maximum value from milk streams by repurposing by-products like buttermilk into high-value applications, including food, beverages, and personal care products. Competitive dynamics remain moderate, with regional cooperatives and global multinationals chasing scale efficiencies through mergers, joint ventures, and strategic capacity expansions. These strategies enable companies to optimize production processes, reduce costs, and meet the growing demand for sustainable and functional dairy ingredients.

Key Report Takeaways

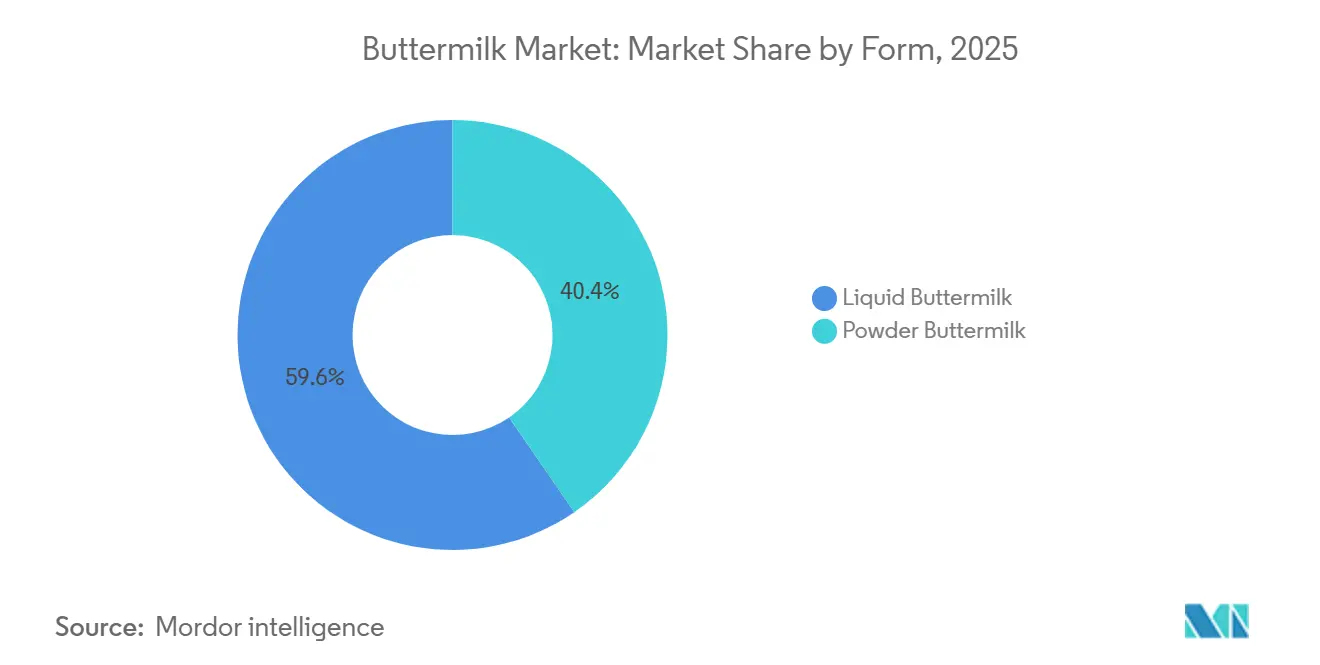

- By form, Liquid buttermilk led with 59.59% of the buttermilk market share in 2025, while powdered buttermilk is forecasted to expand at a 6.48% CAGR through 2031.

- By category, Conventional products held an 85.69% share of the buttermilk market size in 2025, while organic variants are expected to grow at a 6.97% CAGR through 2031.

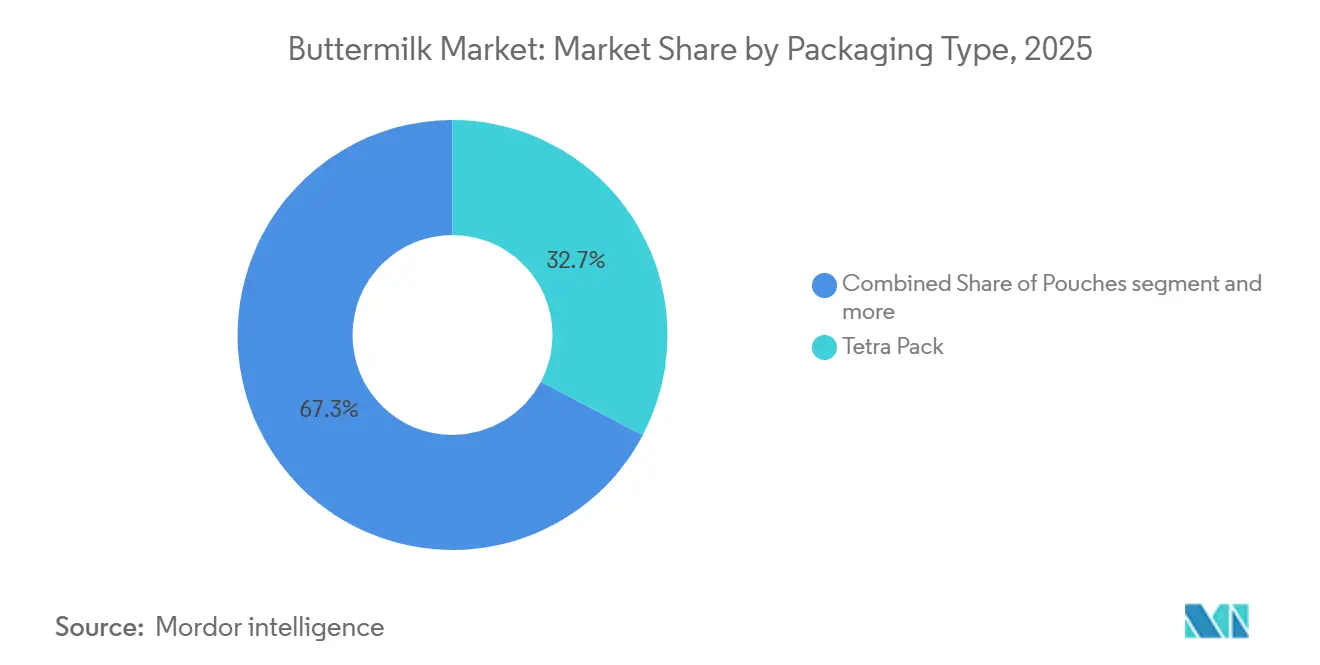

- By packaging, Tetra Pak captured a 32.72% share in 2025, whereas pouches are projected to advance at a 6.70% CAGR through 2031.

- By end user, Retail channels accounted for 77.12% of 2025 revenue, while foodservice is anticipated to rise at a 7.20% CAGR between 2026 and 2031.

- By geography, Asia-Pacific commanded 38.40% of 2025 sales, whereas the Middle East and Africa region is predicted to advance at a 6.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Buttermilk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in advanced bakery applications (clean-label, high-protein recipes) | +1.2% | Global, with a concentration in North America and the EU | Medium term (2-4 years) |

| Growing demand for long-shelf-life buttermilk powder in emerging markets | +0.9% | Asia-Pacific core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Premiumization of cultured dairy beverages in Asia-Pacific convenience stores | +0.8% | Asia-Pacific, particularly Japan, South Korea, and urban China | Short term (≤ 2 years) |

| Expansion of HoReCa waffles and fried-chicken chains in North America | +0.7% | North America, with expansion to EU markets | Medium term (2-4 years) |

| Valorization of milk-fat-globule-membrane (MFGM) for infant-nutrition blends | +1.1% | Global, led by developed markets with premium infant formula demand | Long term (≥ 4 years) |

| Upcycling mandates incentivizing dairy by-product utilization (EU Green Deal) | +0.6% | EU primary, with regulatory spillover to other developed regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advanced bakery applications drive clean-label innovation

Buttermilk powder is evolving from its traditional role to meet modern demands, marking a significant shift in advanced bakery applications. As highlighted by the American Dairy Products Institute, commercial bakeries are now turning to buttermilk powder, not just for its tangy flavor reminiscent of artisanal goods, but also as a natural acidulant and flavor enhancer[1]American Dairy Products Institute, " Dry Buttermilk Standard", adpi.org. This shift sees them moving away from synthetic additives to cater to the growing consumer preference for clean-label products. Additionally, the protein content of buttermilk powder, which typically ranges from 32-35%, positions it as a versatile and budget-friendly substitute for isolated proteins in high-protein bread formulations. This versatility is particularly significant as trends in sports nutrition and wellness continue to drive the demand for protein-rich everyday foods, making buttermilk powder an essential ingredient in addressing these evolving consumer needs.

Emerging markets embrace shelf-stable formats

Emerging markets are increasingly adopting long-shelf-life buttermilk powder due to infrastructure challenges and shifting consumption preferences that prioritize ambient-stable dairy products over refrigerated ones. As per the USDA, by 2025, Indonesia's dairy demand is expected to reach 5.3 million metric tons, driven by the Free Nutritious Meals Program, which benefits over 82 million individuals daily[2]United States Department of Agriculture, "Indonesia: Dairy and Products Annual 2024", www.fas.usda.gov. This trend presents significant growth opportunities for buttermilk powder, particularly in institutional feeding applications. Similarly, India's milk consumption is projected to rise to 91 million metric tons in 2025, with factory-use consumption climbing to 125.5 million metric tons, highlighting a strong demand for processed dairy ingredients like buttermilk powder[3]United States Department of Agriculture, " India: Dairy and Products Annual", www.fas.usda.gov. In areas with limited cold chain infrastructure, powdered formats offer a cost-effective solution, as transporting and storing liquid buttermilk can be expensive. To leverage local value-added opportunities and reduce dependency on imported dairy ingredients, processors in emerging markets are increasingly investing in spray-drying capabilities. This approach addresses the growing domestic demand for convenience foods and bakery applications while marking a strategic evolution in the region's dairy industry.

Asia-Pacific convenience store premiumization transforms cultured dairy

In Asia-Pacific convenience stores, cultured dairy beverages are undergoing a premiumization trend. Buttermilk-based products, in particular, are being sold at premium prices, thanks to their functional positioning and artisanal branding. Starting February 2025, Japan is tightening its dairy governance. The new rules require detailed applications for adding probiotics to dairy, creating hurdles that benefit established players. These regulations, set by Japan's Ministry of Health, Labour, and Welfare, not only uphold product quality but also inadvertently bolster premiumization. This is achieved by raising compliance costs and giving an edge to brands with robust quality systems. Convenience store chains are capitalizing on buttermilk's inherent probiotic benefits. They're promoting their private-label products with claims of enhancing digestive health and boosting immunity, appealing directly to health-conscious urbanites. This trend isn't limited to traditional cultured buttermilk. It's expanding to fusion products, blending buttermilk with regional flavors and added functional ingredients, paving the way for justifying premium pricing.

MFGM valorization elevates functional nutrition

As dairy processors, biotech firms, and research institutions collaborate more closely, the pace of product development and clinical validation is accelerating significantly. This convergence is enabling the integration of advanced biotechnological innovations into traditional dairy processing, fostering the creation of novel buttermilk-based products with enhanced nutritional profiles. Consequently, buttermilk is being rebranded from a mere traditional ingredient to a potent source of targeted health benefits, particularly in areas such as cognitive function enhancement and immune system support. These developments are not only expanding the functional applications of buttermilk but are also driving its adoption in various segments of the global nutrition market, including functional foods, dietary supplements, and specialized nutrition products. Over time, these advancements are poised to transform how consumers perceive buttermilk, elevating it from a commodity by-product to a highly valued, multifunctional ingredient that plays a critical role in addressing evolving consumer demands for health and wellness solutions in the global nutrition landscape.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile skim-milk prices squeezing processor margins | -1.4% | Global, with acute impact in commodity-sensitive regions | Short term (≤ 2 years) |

| Rising popularity of plant-based "buttermilk" substitutes | -0.8% | North America and the EU are primary, spreading to urban Asia-Pacific | Medium term (2-4 years) |

| Cold-chain gaps in last-mile distribution across Africa and South Asia | -0.6% | Africa and South Asia, with rural areas most affected | Long term (≥ 4 years) |

| Regulatory sodium-reduction targets impacting salted cultured buttermilk | -0.4% | North America and EU, with potential global expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Margin pressure from skim-milk price swings

Volatile skim-milk prices are squeezing margins in the global buttermilk market. Fluctuating input costs can unpredictably erode profitability. Processors grapple with forecasting challenges due to uncertainties in Class III and IV milk prices, complicating their pricing strategies and heightening financial loss risks. To counter these challenges, larger processors often adopt hedging strategies or pursue vertical integration, granting them greater control over supply chains and margin stabilization. Yet, these financial maneuvers and structural shifts demand significant capital and adept risk management resources that many small and mid-sized firms lack. Consequently, these smaller entities struggle to absorb price shocks or invest in protective measures, curtailing their production expansion and market entry efforts. This scenario not only hampers growth for these firms but also fuels market consolidation, diminishing competition and potentially hindering innovation in the buttermilk sector.

Plant-based alternatives vie for consumer attention

As environmentally conscious consumers increasingly favor products with lower carbon footprints, the traditional buttermilk market faces mounting pressure from the rise of plant-based alternatives. Both start-ups and established brands are touting sustainability and innovative formulations, marketing their plant-based "buttermilk" and butter analogues as appealing substitutes, especially to younger urban consumers. This shift in preference not only jeopardizes the volume growth of conventional dairy buttermilk but also undermines its premium status in select niches. In retaliation, dairy suppliers are ramping up marketing, highlighting buttermilk's natural health benefits, such as probiotics and the unique milk fat globule membrane (MFGM) compounds, to differentiate themselves from plant-based rivals. Yet, as plant-based options grow more sophisticated and achieve taste parity, traditional dairy finds it harder to hold onto market share, particularly in areas with pronounced vegan or flexitarian trends. This competitive dynamic not only fragments demand, stunting the buttermilk market's expansion, but also forces dairy processors to pour more into innovation and consumer education just to keep their current clientele.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Shelf-Stable Powder Widens Access

In 2025, liquid buttermilk commands a dominant position, securing over 59.59% of the global buttermilk market share. Its leadership stems from its prevalent use in bakery and confectionery items, alongside its popularity in traditional dairy drinks, prized for their probiotic and nutritional benefits. Established dairy markets show a clear preference for liquid buttermilk, drawn by its fresh sensory qualities and versatile functionality in recipes. This preference is bolstered by strong distribution networks and the entrenched role of liquid buttermilk in both commercial and home cooking. In regions boasting advanced dairy processing, liquid buttermilk finds its way into functional foods and beverages, solidifying its dominant stance. Consequently, while other formats are emerging in new applications, liquid buttermilk is poised to maintain its market leadership.

On the other hand, buttermilk powder is on a rapid ascent, with projections indicating a CAGR of 6.48% over the next decade. Its surge is attributed to advantages like cost-effective transport, extended shelf life, and its utility in areas with unreliable refrigeration. Innovations, especially in spray-drying, have enhanced the preservation of bioactive compounds, making the powder a sought-after ingredient in sports nutrition, baking mixes, and infant formulas. Moreover, industrial users appreciate the powder's consistent moisture and protein levels, vital for large-scale food production. The extraction of MFGM-enriched fractions from buttermilk powder is unveiling new revenue avenues in supplements and functional foods, further driving the segment's premiumization and widespread adoption. With food and beverage manufacturers on the lookout for stable, versatile, and value-added dairy ingredients, buttermilk powder's significance in the global arena is set to surge, outpacing its liquid counterpart.

By Category: Organic Lines Benefit From Sustainability Branding

In 2025, conventional buttermilk variants dominate the global market, capturing 85.69% of total revenues. Their widespread availability, bolstered by established supply chains and cost-effective production, makes them the preferred choice for both industrial users and everyday consumers. Competitive pricing solidifies their leadership, particularly in price-sensitive regions and high-usage applications like baking and foodservice. The reliability of conventional supplies guarantees consistent product quality and extensive market penetration, reinforcing their staple status in the dairy sector. Major brands and processors depend on these variants to sustain steady sales and cater to the bulk of consumer demand. Consequently, while premium alternatives are carving out niches, conventional buttermilk is set to remain the market's cornerstone.

On the other hand, organic buttermilk is rapidly gaining traction, with projections indicating a CAGR of 6.97%. This surge is driven by consumers' growing emphasis on sustainability and animal welfare. Brand owners amplify the allure of organic products by touting grass-fed and regenerative agriculture claims, harmonizing with broader corporate sustainability goals, such as Nestlé’s net-zero emissions roadmap. While organic production may yield lower volumes, the associated higher margins compensate for the reduced output. Moreover, enhanced transparency through on-farm data systems fosters consumer trust and secures premium shelf placements in both retail and specialty outlets. The rising popularity of organic buttermilk not only diversifies revenue streams for producers but also fortifies the global market by appealing to environmentally conscious shoppers. As this segment expands, it is set to significantly influence the future trajectory of the buttermilk industry.

By Packaging Type: Flexible Formats Disrupt Rigid Incumbents

Tetra Pack held 32.72% of 2025 revenues, leading the aseptic carton market with 6-12 months of ambient shelf life, ideal for markets without refrigerated infrastructure. Pouches, however, are projected to grow fastest at a 6.70% CAGR through 2031, driven by 15-25% lower per-unit costs, 40-50% lighter shipping weight, and demand for portion-controlled formats in emerging markets. In 2025, Tetra Pak invested EUR 60 million (USD 65 million) in paper-based barrier technology, achieving 80% paper content and 92% renewable materials, cutting carbon footprint by 43% compared to conventional cartons. Bottles held a mid-tier share in 2025, with premium brands like Organic Valley and Straus Family Creamery using glass or HDPE bottles to signal quality and support deposit-return schemes.

Pouches are gaining traction in India, Southeast Asia, and sub-Saharan Africa, where single-serve 200-250 milliliter formats align with purchasing power and reduce waste in households without refrigeration. Amul pioneered milk pouches in India during the 1970s White Revolution, a format now accounting for 40-50% of liquid-dairy sales and expanding to buttermilk and lassi. Sustainability drives packaging trends: Tetra Pak's paper-based barriers, pouch manufacturers' mono-material films for recycling, and bottle producers' shift to post-consumer recycled (PCR) content address retailer and regulatory demands to reduce plastic waste. Processors investing in flexible-packaging lines and partnering with pouch manufacturers like Amcor and Sealed Air gain cost and sustainability advantages, challenging rigid-format players facing stranded-asset risks.

By End User: Foodservice Taps Culinary Authenticity

In 2025, retail channels solidified their lead in the global buttermilk market, capturing a commanding 77.12% of total revenue. This robust showing is primarily due to the enduring allure of home baking and the ubiquitous presence of buttermilk in supermarkets and grocery outlets. Consumers frequently turn to these retail venues, incorporating buttermilk into a myriad of dishes, from pancakes and biscuits to marinades and dressings. The combination of familiarity and accessibility cements retail channels as the go-to source for households, bolstering their market dominance. Supermarkets, leveraging established distribution networks and savvy merchandising tactics, ensure buttermilk remains prominent and easily accessible to shoppers. Consequently, retail channels not only anchor buttermilk sales but also guarantee consistent revenue and expansive market reach.

Meanwhile, the foodservice sector emerges as the fastest-growing channel, with projections indicating a CAGR of 7.20%. This surge is driven by the rising incorporation of buttermilk in favored menu items, including waffles, fried chicken, and other fast-casual delights. The worldwide spread of American-style dining, especially via franchising, has amplified buttermilk's presence in dining establishments. Furthermore, institutional catering, spanning schools to hospitals, is witnessing a surge in buttermilk demand, as these entities adopt it to enhance nutritional standards and diversify their meal offerings. Strengthening this trend, dairy processors are forging strategic alliances with restaurant operators, bolstering supply chains, and ensuring a steady buttermilk influx to foodservice venues. As these partnerships deepen, they not only fortify buttermilk's standing in the foodservice realm but also herald a promising growth trajectory for this vibrant channel.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 38.40% of the global buttermilk market revenues. Factors such as a rising middle class with increased purchasing power, a cultural inclination towards fermented beverages, and the expansion of convenience-store networks are driving sales. In India, a surge in dairy processing, coupled with a policy emphasis on child nutrition, bolsters domestic demand for buttermilk powder. The government's initiatives to enhance dairy production and promote nutritional programs further support this growth. Meanwhile, Japan's stringent probiotic regulations are fueling premiumization and brand differentiation in the market, as companies focus on meeting these standards to cater to health-conscious consumers.

The buttermilk market in the Middle East and Africa is on a rapid ascent, with projections indicating a CAGR of 6.58% through 2031. This surge is largely attributed to an escalating demand for shelf-stable dairy imports, coinciding with the evolution of local manufacturing. Both government entities and private investors are channeling funds into cold-chain infrastructure, a vital component for upholding product quality and curbing wastage in the region's warmer climates. Furthermore, these areas are actively forging partnerships and attracting foreign direct investments, aiming to modernize dairy processing facilities and bolster local production. With a burgeoning urban populace and increasing disposable incomes, there's a marked consumer shift towards convenient, value-added dairy products, notably buttermilk. Consequently, the Middle East and Africa are not just narrowing the gap with their more established counterparts but are also laying the groundwork for ongoing growth and innovation in the buttermilk domain.

Europe stands as the vanguard of the buttermilk market, underscored by its commitment to sustainability, cutting-edge processing technologies, and optimal by-product utilization. The region's stringent regulatory stance on environmental conservation is nudging manufacturers towards eco-friendly production techniques and enhanced returns from dairy streams. Cooperatives like Arla–DMK, boasting revenues of EUR 19 billion, highlight the scale and Research and development investments pivotal for market penetration and product evolution. European processors are harnessing methods such as high-pressure processing and membrane separation, not only to prolong shelf life but also to extract premium MFGM fractions and craft superior functional dairy offerings. This focus on innovation allows European producers to align with the preferences of health-conscious consumers, securing a competitive stance in both local and international arenas. With sustainability and product functionality taking center stage, Europe is set to cement its reputation as the epicenter for premium and value-added buttermilk, even as its growth rates temper in comparison to emerging markets.

Competitive Landscape

Farmer-owned cooperatives like Amul, FrieslandCampina, Arla, and Fonterra dominate the buttermilk market, controlling a significant portion of global processing capacity. These cooperatives leverage their upstream milk procurement to gain cost advantages, a feat that multinational brands such as Danone, Lactalis, and Saputo find challenging without vertical integration. Unlike their multinational counterparts, cooperatives emphasize volume and stability in farmer milk prices over margin optimization. This approach, while compressing overall industry profitability, ensures a reliable supply even during commodity downturns.

Technology is carving out a competitive edge in the industry. Membrane-filtration innovations are allowing processors to harness high-value MFGM and phospholipid fractions from buttermilk, a resource previously relegated to animal feed or waste. In 2024, GEA Group introduced its Smart Filtration systems at Molkerei Ammerland in Germany, reducing water usage by 48% and energy consumption by 77% during membrane-cleaning cycles. Their success highlights that MFGM extraction can be both eco-friendly and economically viable, with payback periods of under two years.

The competitive arena is splitting: Major players like FrieslandCampina, Lactalis, and Fonterra are channeling investments into ingredient-extraction technologies and mergers to tap into lucrative niches. Meanwhile, regional cooperatives such as Amul, Prairie Farms, and Goulburn Valley are fortifying their market presence through local sourcing, direct-to-consumer strategies, and collaborations with government entities for subsidies and tariff safeguards. These strategies enable regional players to defend market share while maintaining supply reliability and farmer loyalty.

Buttermilk Industry Leaders

-

Arla Foods amba

-

Lactalis Group

-

Fonterra Co-operative Group

-

Gujarat Cooperative Milk Marketing Federation (Amul)

-

Dairy Farmers of America (Mayfield Dairy Farms)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Arla Foods announced a EUR 300 million (USD 324 million) investment to build a new cheese dairy at its Götene, Sweden production site, expected to double incoming milk to approximately 1 billion kilograms per year and raise Sweden's cheese self-sufficiency by 10 percentage points when operational in 2030.

- March 2025: Karnataka Milk Federation (KMF) introduced its Nandini brand products, including milk, curd, and buttermilk, in Hathras district, Uttar Pradesh. The debut of Nandini buttermilk in Uttar Pradesh aligns with a broader trend: a rising demand for ready-to-drink beverages and a surge in the popularity of flavored buttermilk.

- June 2024: AMul has rolled out its Kathiyawadi buttermilk in a 400 ml pouch, debuting the product across Gujarat. This launch has contributed to a significant increase in the company's sales, highlighting the growing consumer demand for regionally inspired dairy products.

- April 2024: Heritage Foods Ltd has rolled out its A-one branded spiced buttermilk, complementing its lineup of refreshing drinks. These offerings are now available in Andhra Pradesh, Telangana, and other regions where the company operates.

Global Buttermilk Market Report Scope

Buttermilk is a versatile dairy product that exists in two primary forms: a traditional byproduct of butter production and a modern cultured beverage. The buttermilk market is segmented by form, category, packaging type, end user, distribution channel, and geography. By form, the market is segmented into powder and liquid. By category, the market is segmented into conventional and organic. By packaging type, the market is segmented into pouches, tetra packs, bottles, and others. By end user, the market is segmented into foodservice and retail. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Powder Buttermilk |

| Liquid Buttermilk |

| Conventional |

| Organic |

| Pouches |

| Tetra Packs |

| Bottles |

| Others |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Powder Buttermilk | |

| Liquid Buttermilk | ||

| By Category | Conventional | |

| Organic | ||

| By Packaging Type | Pouches | |

| Tetra Packs | ||

| Bottles | ||

| Others | ||

| By End User | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global buttermilk market?

The global buttermilk market size is USD 4.01 billion in 2026.

Which region holds the largest share of buttermilk sales?

Asia-Pacific leads with 38.40% of 2025 revenue.

Which form of buttermilk is growing fastest?

Powder variants are projected to expand at a 6.48% CAGR between 2026 and 2031 due to shelf-life and logistics advantages.

What is driving premium pricing in convenience-store dairy drinks?

Stricter probiotic fortification standards and consumer interest in functional ingredients lift the profile and price of cultured buttermilk beverages.

Page last updated on: