Hazelnut Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

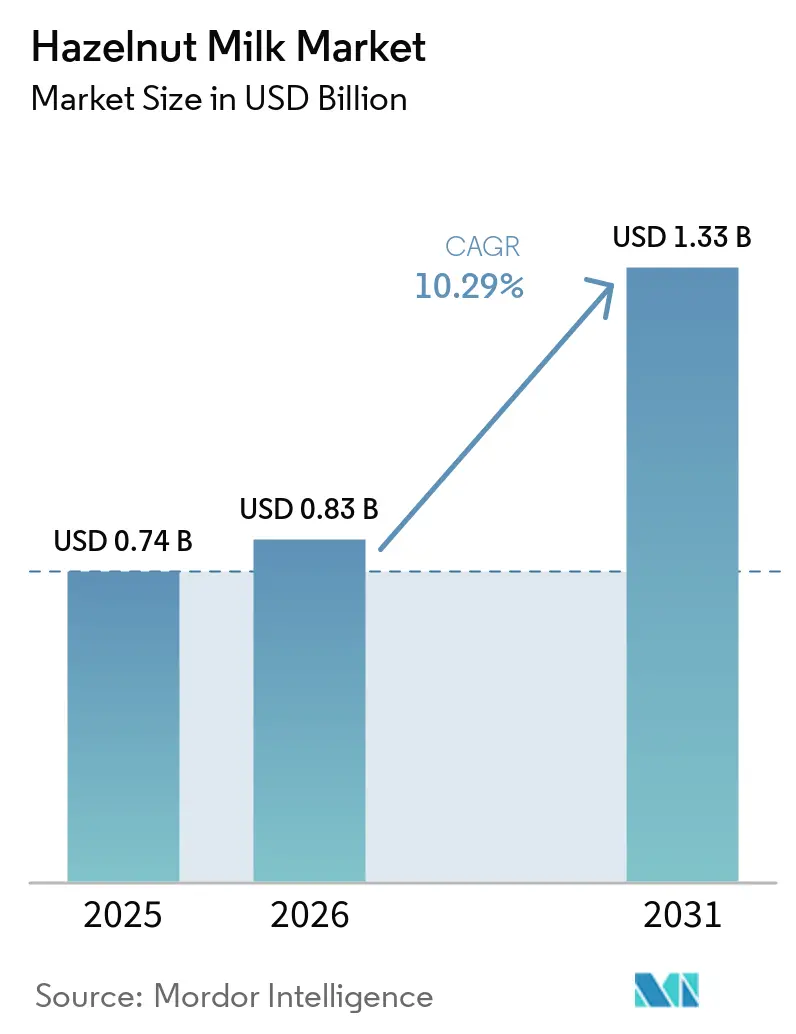

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.33 Billion |

| Growth Rate (2026 - 2031) | 10.29% CAGR |

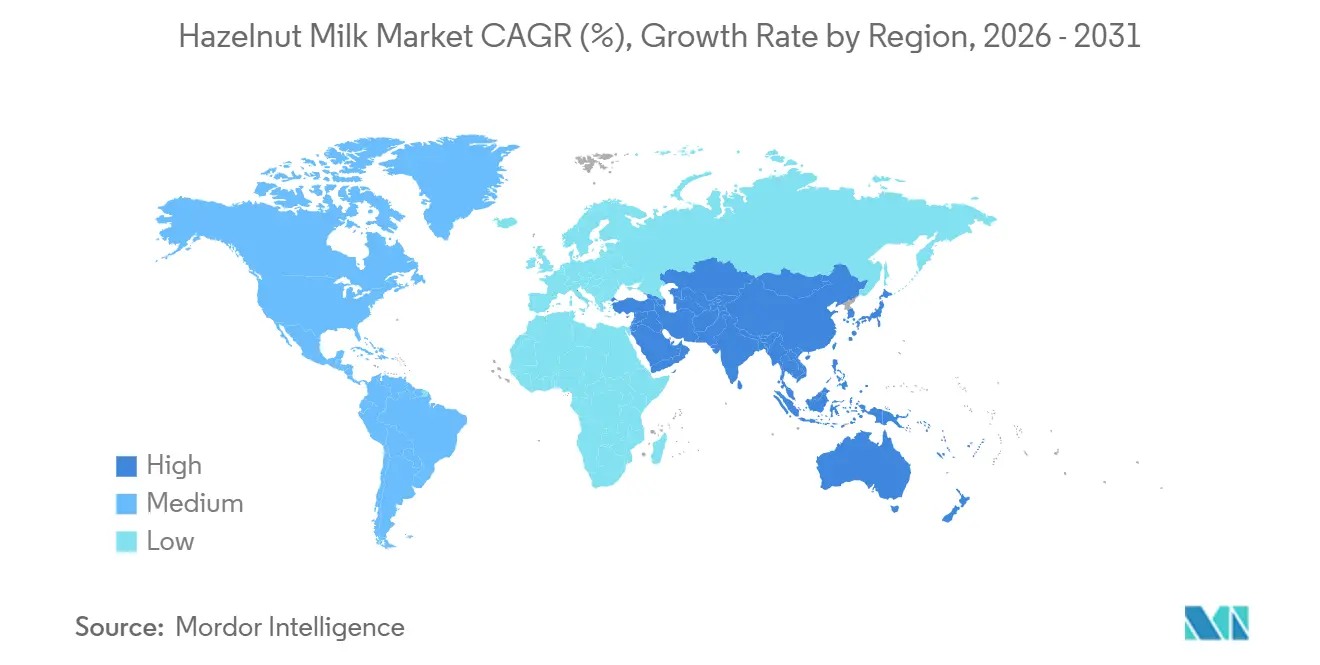

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hazelnut Milk Market Analysis by Mordor Intelligence

The hazelnut milk market size was USD 0.74 billion in 2025 and is expected to reach USD 0.83 billion in 2026 and USD 1.33 billion by 2031, growing at a CAGR of 10.29% over 2026-2031. This growth reflects structural shifts in consumer behavior rather than temporary trends, as the prevalence of lactose intolerance globally continues to drive a sustained shift away from dairy products. The increasing adoption of flexitarian diets, particularly in Europe, highlights the mainstream appeal of hazelnut milk. The U.S. Food and Drug Administration’s January 2025 draft guidance on plant-based milk labeling aims to clarify product positioning and nutritional content, further encouraging broader consumer adoption [1]Source: United States Food and Drug Administration, "Plant-Based Milk and Animal Food Alternatives," fda.gov. Plant-based procurement mandates, rising online grocery penetration, and flavor-driven innovations collectively support the market's sustained value expansion. Although a tightening Turkish hazelnut crop in 2025 led to higher raw-nut costs, advancements in ingredient diversification and processing technologies, such as ultra-high-temperature (UHT) treatment, have ensured consistent product availability.

Key Report Takeaways

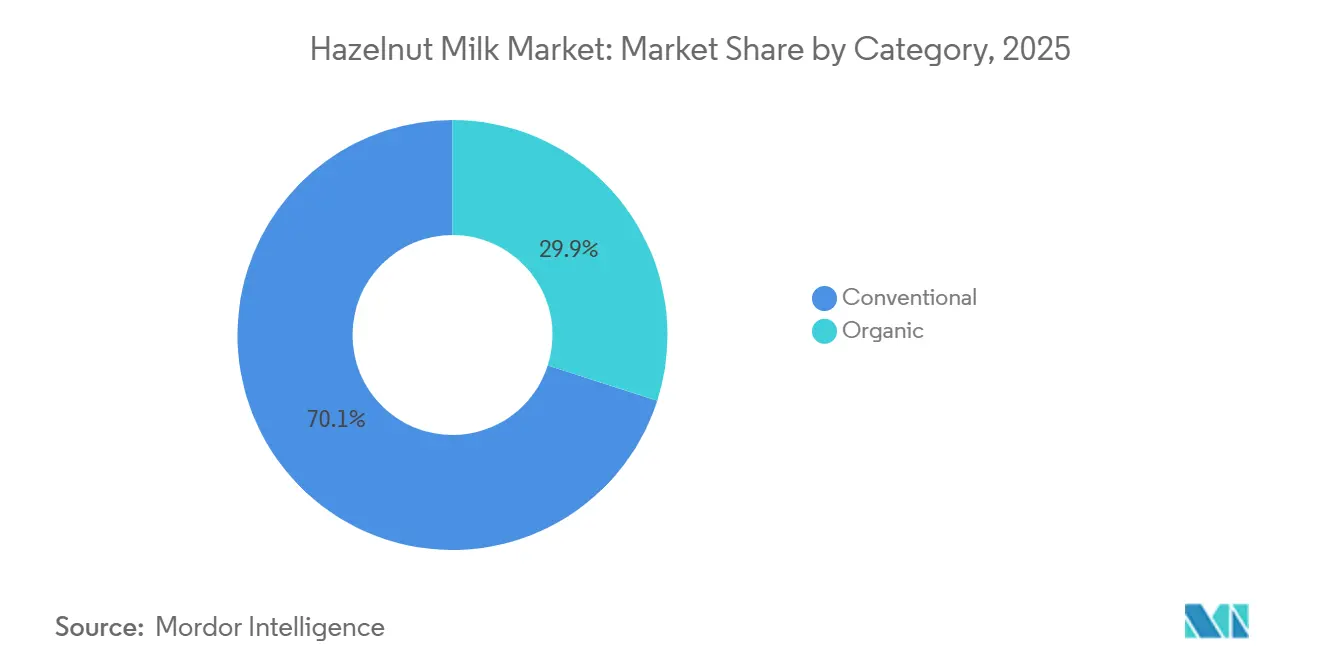

- By category, conventional products led the hazelnut milk market with 70.03% share in 2025, while organic variants are projected to advance at a 10.03% CAGR through 2031.

- By flavor, unflavored SKUs captured 60.14% of 2025 revenue; flavored formats are forecast to grow at a 10.18% CAGR over 2026-2031.

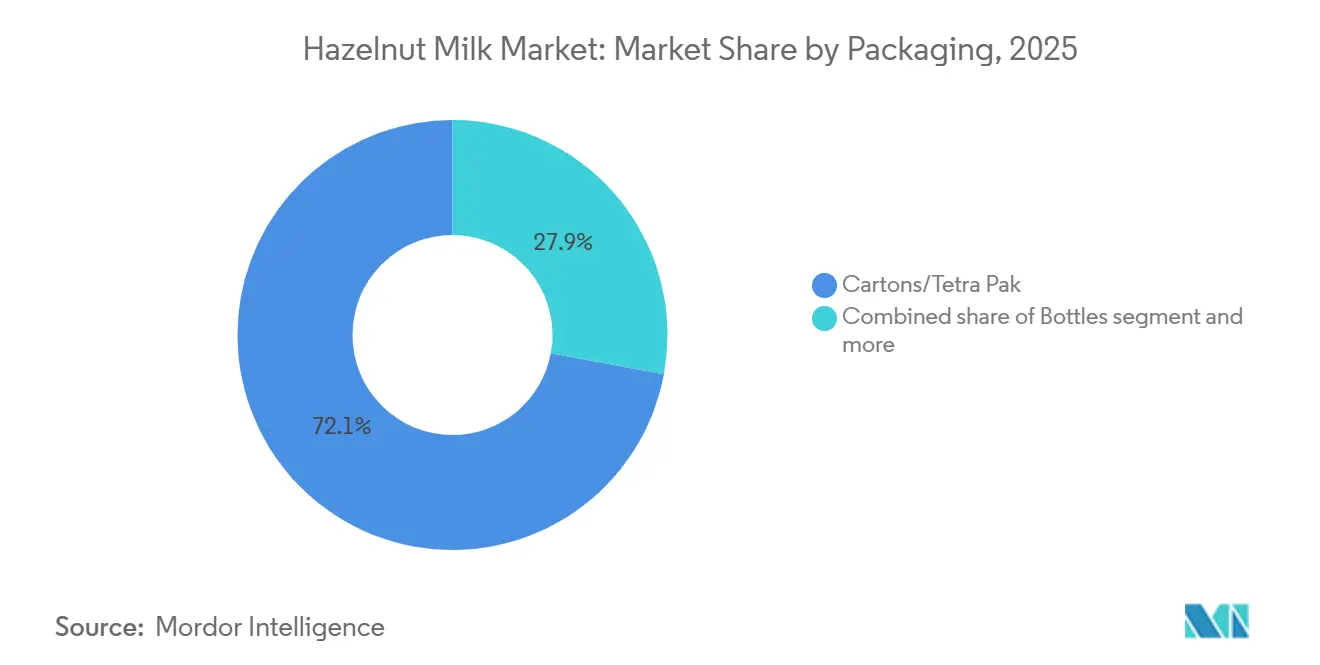

- By packaging, cartons held 72.08% of the 2025 market share, yet bottles are set to record the highest CAGR of 9.82% during 2026-2031.

- By distribution channel, supermarkets and hypermarkets accounted for 55.56% of 2025 sales, whereas online retail stores will post a 10.55% CAGR to 2031.

- By geography, Europe commanded 37.65% of the 2025 market share; Asia-Pacific is expected to grow at 10.67% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hazelnut Milk Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of vegan and flexitarian diets | + 2.1% | Global, with concentration in Western Europe and North America | Medium term (2-4 years) |

| Increasing lactose-intolerance awareness | +1.8% | Global, highest in East Asia, Africa, Hispanic populations | Long term (≥ 4 years) |

| Expansion of plant-based milks in retail and e-commerce | +1.5% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Advancements in product formats and flavor innovations | +1.3% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Government support for nut-based beverage production | +0.9% | Europe (Denmark, Netherlands), select U.S. states | Long term (≥ 4 years) |

| Enhanced shelf life through UHT and aseptic packaging technologies | +1.2% | Global, critical for Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing adoption of vegan and flexitarian diets

The growing shift toward plant-based diets has significantly increased the demand for hazelnut milk, appealing to a wider audience beyond traditional lactose-intolerant consumers. This trend is driven by the rising popularity of flexitarian lifestyles in the Netherlands and the United Kingdom, confirming that the hazelnut milk market can transcend niche vegan demand. Additionally, the increasing awareness of environmental sustainability and the health benefits of plant-based alternatives has further fueled this growth. Denmark's national action plan mandates plant-based foods in public procurement across 77 municipalities serving 1.03 million meals daily. It has introduced 133 new plant-based products in schools, resulting in increased plant-based food consumption and demonstrating that institutional demand can de-risk the scale-up of production. Furthermore, advancements in processing technologies and innovative product formulations are enabling manufacturers to enhance the taste, texture, and nutritional profile of hazelnut milk, making it more appealing to a broader consumer base.

Increasing lactose-intolerance awareness

Lactose intolerance affects a large portion of the global population, driving demand for plant-based milk alternatives such as hazelnut milk. According to the U.S. National Institute of Diabetes and Digestive and Kidney Diseases, about 36% of people in the United States have lactose intolerance. Recent clinical evidence indicates that consumers of alternative milk may produce fewer beneficial gut metabolites, prompting producers to fortify hazelnut milk with essential nutrients such as calcium and vitamin D to comply with the U.S. Food and Drug Administration's draft labeling guidance. Additionally, the growing consumer preference for functional foods has encouraged manufacturers to incorporate ingredients such as omega-3 fatty acids and probiotics into hazelnut milk formulations, thereby enhancing the product's nutritional profile. This trend highlights the need for producers to strike a balance between clean-label positioning and strategic fortification to meet regulatory standards, address nutritional gaps, and cater to health-conscious consumers. By aligning with these evolving consumer demands, hazelnut milk producers can strengthen their market position while mitigating potential regulatory or reputational risks.

Government support for nut-based beverage production

Governments are increasingly supporting the processing of nut-based beverages due to their potential to diversify agriculture and drive economic growth. Denmark, for instance, has allocated DKK 1 billion through 2030 via the Plant-Based Food Grant, with a 2025 funding pool of DKK 212.5 million [2]Source: Plantefonden, "The Plant-Based Food Grant," plantefonden.dk. This initiative targets projects across the value chain, from primary production to retail, with a mandate that at least 50% of resources are directed toward organic initiatives. Such funding not only promotes innovation in plant-based beverages, including hazelnut milk, but also encourages sustainable practices, aligning with growing consumer demand for eco-friendly, health-conscious products. Similar government-backed programs in other regions are expected to further bolster the market, creating opportunities for producers to expand their portfolios and enhance their competitive positioning.

Enhanced shelf life through UHT and aseptic packaging technologies

Ultra-high-temperature (UHT) processing at 135-150°C for 1-10 seconds achieves commercial sterility and extends shelf life under ambient conditions when paired with aseptic packaging. This significantly reduces reliance on cold-chain logistics, enabling broader retail distribution in regions with limited refrigeration infrastructure. UHT processing, particularly through direct heating methods such as steam injection or infusion, is highly suitable for plant-based beverages. Tetra Pak's paper-based barrier technology replaces aluminum foil with a paper-based layer. This advancement achieves 87% renewable content and reduces the carbon footprint by 26%, as verified by the Carbon Trust, while maintaining equivalent protection against oxygen, light, moisture, and bacterial contamination. For hazelnut milk and other plant-based beverages, direct steam-injection methods help preserve the natural aroma and flavor profiles that consumers associate with premium quality. Additionally, shelf-stable options are driving market penetration in emerging regions such as Africa and Latin America, where high refrigeration costs and infrastructure limitations have historically constrained the adoption of dairy alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from alternative plant-based milks | -1.6% | Global, most intense in North America and Western Europe | Short term (≤ 2 years) |

| Concerns regarding limited shelf life and quality preservation | -0.8% | Emerging markets in Asia-Pacific, Middle East, Africa | Medium term (2-4 years) |

| Susceptibility to supply chain disruptions | -1.4% | Global | Short term (≤ 2 years) |

| Regulatory complexities and challenges related to food safety | -0.7% | Global, varying by jurisdiction (European Union, United States, Asia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from alternative plant-based milks

Almond milk continues to dominate the U.S. plant-based milk category, with oat milk experiencing significant growth, leaving hazelnut milk to compete in a crowded market alongside cashew, coconut, macadamia, and emerging bases like pistachio. This is further intensified by established players like Blue Diamond Growers, which recently revamped its almond milk with a simplified three-ingredient recipe to strengthen its market position. Hazelnut milk faces challenges in carving out a distinct niche, as it must position itself as a premium, flavor-forward alternative. To succeed, it needs to emphasize unique taste profiles, creamy texture, and sustainability credentials that justify its higher price points. However, competing on cost with well-established almond and oat milk options remains a significant restraint, particularly as consumers increasingly seek affordable plant-based alternatives. Additionally, limited consumer awareness and availability in mainstream retail channels further hinder hazelnut milk's market penetration, requiring targeted marketing efforts and strategic partnerships to drive growth.

Susceptibility to supply chain disruptions

Turkey supplies the majority of global hazelnuts, making it a critical player in the global supply chain. The 2025-26 Turkish hazelnut season faces significant challenges with production projected to drop 36% to 500,000 metric tons due to adverse weather, including frost and drought [3]Source: International Nut and Dried Fruit Council (INC), "Hazelnut Crop Update & Outlook," inc.nutfruit.org. This supply shortage, combined with quality concerns, has led to record-high export prices and stagnant demand. This supply disruption led to a 51.5% increase in farmgate prices, reaching TRY 200 per kilogram for Giresun-grade hazelnuts, while international prices surged to USD 15,090 per metric ton by November 2025. The reliance on Turkey as a dominant supplier underscores the hazelnut market's vulnerability to climatic events. Alternative origins are attempting to scale production to meet global demand. Azerbaijan exported approximately 18,700-19,000 metric tons valued at USD 170 million in 2025, while Georgia produced 43,600 metric tons in 2024. Despite these efforts, the combined output from these regions remains insufficient to fully offset the shortfall caused by Turkey's reduced production. For hazelnut milk producers, this supply constraint underscores the need to diversify strategic sourcing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Organic Variants Capture Premium Positioning

Conventional hazelnut milk accounted for 70.03% of the market share in 2025, driven by its affordability and established supply chains. Its competitive pricing appeals to mainstream consumers and foodservice operators, making it a preferred choice in the market. Mainstream grocers strategically price conventional hazelnut milk at an affordable premium, attracting flexitarians who prioritize value. However, the cost gap between conventional and organic hazelnuts is narrowing as more Turkish and Georgian orchards pursue organic certification to meet EU demand. Forward contracts increasingly include sustainability scorecards, indicating a shift toward reduced pesticide use and regenerative practices, even within the conventional segment.

Organic hazelnut milk is projected to grow at a CAGR of 10.03% during 2026-2031, supported by the European Union's organic market recovery, which increased in 2024 following inflation stabilization. Western and Northern European countries are driving higher per-capita organic spending, reflecting a growing consumer preference for products perceived as healthier, environmentally friendly, and ethically sourced. However, organic certification costs and lower agricultural yields limit supply elasticity, creating opportunities for brands that can secure long-term organic hazelnut contracts from Turkish, Azerbaijani, or Georgian growers. Additionally, the EU's target of 25% farmland under organic cultivation by 2030 remains ambitious, with Austria being the only country currently exceeding this threshold, signaling strong policy support for organic ingredient supply.

By Flavor: Innovation Drives Premiumization

Unflavored hazelnut milk captured 60.14% of the market share in 2025, serving as a versatile base for coffee, cereal, smoothies, and cooking applications. Its dominance reflects its functional adaptability and appeal to consumers seeking neutral bases for customization. However, its growth rate lags behind flavored variants due to direct competition with established almond and oat milk offerings, which are often priced more competitively and have broader availability. To sustain growth, unflavored hazelnut milk producers are focusing on improving supply chain efficiencies and promoting their nutritional benefits, such as their high vitamin E content and lower calorie count compared to other plant-based milk options.

Flavored variants are expanding at a robust 10.18% CAGR for 2026-2031, driven by rising consumer demand for indulgent, café-style experiences at home and Gen Z's preference for personalization. Flavored hazelnut milk differentiates itself through unique profiles such as chocolate-hazelnut (leveraging the classic Nutella association), vanilla-hazelnut, or coffee-hazelnut blends that emphasize the nut's inherent richness while complementing its natural flavor. The segment is also benefiting from innovations in natural flavoring and sweetening, which cater to health-conscious consumers seeking indulgence without added sugars. Furthermore, as chocolate confectioners increasingly adopt dairy-free couvertures, co-branding opportunities are emerging for flavored hazelnut bases in bakery and dessert kits. This expansion into adjacent categories, such as ready-to-drink beverages and plant-based dessert toppings, is expected to further drive the growth of flavored hazelnut milk.

By Packaging: Sustainability Accelerates Bottle Adoption

Cartons and Tetra Pak formats commanded 72.08% of market share in 2025, benefiting from established aseptic technology, ambient shelf life, and consumer familiarity. These formats are particularly favored for their lightweight, cost-effectiveness, and recyclability, aligning with growing consumer demand for sustainable packaging solutions. Cartons and Tetra Pak packaging also support large-scale distribution, making them a preferred choice for manufacturers targeting mass-market penetration. Elmhurst 1925's barista-edition products are packaged in 100% recyclable, FSC-certified paperboard cartons, with direct-to-consumer shipping materials now primarily post-consumer recycled molded fiberboard trays and scrap corrugate, demonstrating that sustainability extends beyond primary packaging to fulfillment logistics.

Bottles are the fastest-growing packaging format, with a 9.82% CAGR for 2026-2031, propelled by paper-based barrier innovation and consumer preference for resealable, premium-positioned containers. Bottles offer tactile premiumization, improved shelf visibility, and resealability that extends post-opening freshness, making them ideal for refrigerated hazelnut milk positioned as a premium, artisanal product. Furthermore, the versatility of bottles allows manufacturers to cater to diverse consumer needs, including single-serve options and family-sized packaging. Pouch and can formats remain niche, serving specific use cases such as single-serve on-the-go consumption or foodservice bulk packaging, but face limited consumer adoption due to perceived lower quality and lack of resealability.

By Distribution Channel: Digital Platforms Reshape Retail

Supermarkets and hypermarkets held 55.56% of market share in 2025, leveraging broad geographic reach, high foot traffic, and established dairy-aisle placement that increases impulse purchases. These channels remain pivotal for mass-market penetration, offering consumers the convenience of one-stop shopping and the ability to compare multiple brands and price points. Additionally, supermarkets and hypermarkets often run promotional campaigns, such as discounts and in-store sampling, which drive trial and repeat purchases. Brands should prioritize strategic shelf placement in high-traffic areas, such as the refrigerated dairy aisle, to maximize visibility and attract mainstream consumers.

Online retail stores are expanding at a 10.55% CAGR for 2026-2031, driven by the growing adoption of e-commerce platforms and the convenience of doorstep delivery. Platforms like Instacart and Amazon Fresh address the logistical challenges of refrigerated products by offering efficient fulfillment solutions. Online retail enables hazelnut milk brands to reach geographically dispersed, health-conscious consumers who prioritize clean-label, organic, or specialty formulations. Moreover, digital platforms provide advanced analytics and targeted marketing opportunities, allowing brands to personalize their campaigns and optimize customer engagement. Subscription models and bundling options further enhance customer loyalty and drive consistent sales through online channels. Convenience stores, specialty stores, and other distribution channels collectively serve niche segments but face margin pressure from limited assortment depth and higher per-unit logistics costs.

Geography Analysis

In 2025, Europe accounted for 37.65% of the market share, driven by increasing consumer preference for plant-based beverages, rising awareness of lactose intolerance, and the growing trend of veganism. Key markets in Europe include Germany, the United Kingdom, Italy, France, the Netherlands, Poland, Belgium, and Sweden. Germany and the United Kingdom lead the region due to their well-established retail infrastructure and high consumer spending on premium plant-based products. Southern European markets, such as Spain, are witnessing growing demand for barista-grade hazelnut milk, particularly within café culture. Additionally, the European Union's stringent sustainability regulations and consumer demand for eco-friendly packaging have further propelled the adoption of hazelnut milk.

The Asia-Pacific region is the fastest-growing, with a projected CAGR of 10.67% for 2026-2031, driven by young urban demographics, rising e-commerce penetration, and a strong coffee-shop culture in countries such as South Korea and Australia. In China, demand is rebounding post-lockdown, although regulatory uncertainties surrounding the use of dairy-related terms remain a challenge. Localization efforts, such as Singapore-based production for regional supply, along with grants and brand tariffs, provide competitive advantages in the region.

North America, while facing category maturity, continues to maintain momentum through clean-label reformulations and private-label diversification. Latin America and the Middle East present growth opportunities, particularly where UHT functionality addresses refrigeration constraints. However, brands must adapt packaging sizes to align with lower per capita incomes in these regions. Turkey, serving as both a major raw-nut exporter and an emerging domestic beverage market, holds a unique position as a critical hub for both supply and demand in the hazelnut milk market.

Competitive Landscape

The Hazelnut milk market is moderately concentrated, with established players commanding significant share while leaving room for niche entrants to capture premium segments through differentiation in ingredient quality, sourcing transparency, and functional positioning. Major players such as Danone S.A (Alpro), Rude Health Foods Ltd, Pacific Foods (The Campbell's Company), and Elmhurst Milked, LLC leverage scale economies, multi-category portfolios, and extensive distribution networks to maintain market share. However, they face margin pressure from premium challengers such as Hazelicious, Inc., Al Naturale, and Unigra S.p.A. (OraSì), which emphasize clean-label formulations, higher nut content, and patented processing methods.

Emerging opportunities cluster around three vectors: functional fortification targeting specific health outcomes (bone health, cognitive function, digestive wellness), localized sourcing to reduce supply-chain risk and the carbon footprint, and format innovation for adjacent consumption occasions such as meal replacement, sports recovery, and children's nutrition. Smaller entrants such as Hazelicious, Inc., Al Naturale, and Unigra S.p.A. (OraSì) are exploiting these niches by avoiding head-to-head competition with major players in mainstream grocery and instead pursuing specialty retail, e-commerce, and foodservice channels where brand storytelling and product differentiation command premium pricing.

Technology adoption is advancing through patented processing methods such as Elmhurst's HydroRelease, which uses only water to separate and recombine nutritional components, preserving source nutrition and upcycling waste into energy. High-pressure homogenization at 172 megapascals is also being utilized to reduce particle size and improve emulsion stability in hazelnut milk. Additionally, licensing paper-based barrier packaging from Tetra Pak allows brands across all tiers to enhance sustainability claims affordably, fostering innovation throughout the hazelnut milk market. Regulatory developments, such as the FDA's January 2025 draft guidance on labeling plant-based milk alternatives, provide clarity that reduces litigation risks and enables consistent branding across jurisdictions.

Hazelnut Milk Industry Leaders

-

Danone S.A. (Alpro)

-

Borges International Group

-

Rude Health

-

The Hain Celestial Group

-

Elmhurst Milked, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Danone's Alpro brand launched Meal To Go, a ready-to-drink plant-based beverage blending hazelnut milk with oats and fruit, positioned as a breakfast replacement competing with meal-replacement shakes.

- April 2025: Saba, a plant-based beverages company, has expanded its product line with the launch of its own Hazelnut Milk. According to the brand, the new milk is creamy, full of flavor, and 100% plant-based, appealing to those seeking a dairy alternative with a rich and smooth texture.

- May 2024: Lactalis Canada has launched a new plant-based milk brand called Enjoy, entering the rapidly growing dairy-alternative market. Among its offerings, the brand features a hazelnut milk variety, catering to consumers seeking diverse and sustainable beverage options, according to the brand.

Global Hazelnut Milk Market Report Scope

Hazelnut milk is a plant-based, dairy-free alternative made by blending soaked hazelnuts with water and straining the mixture, yielding a rich, creamy beverage. The hazelnut milk market is segmented by category, flavor, packaging, distribution channel, and geography. By category, the market is segmented into conventional and organic. By flavor, the market is segmented into unflavored and flavored. By packaging, the market is segmented into cartons/tetra pak, bottles, cans, and pouches. By distribution channels, the market has been segmented into foodservice and retail. By geography, the market has been segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (USD) and Volume (Liters).

| Conventional |

| Organic |

| Unflavored |

| Flavored |

| Cartons/Tetra Pak |

| Bottles |

| Cans |

| Pouch |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Specialty Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Category | Conventional | |

| Organic | ||

| By Flavor | Unflavored | |

| Flavored | ||

| By Packaging | Cartons/Tetra Pak | |

| Bottles | ||

| Cans | ||

| Pouch | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Specialty Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big will the Hazelnut milk market be by 2031?

The hazelnut milk market is forecast to reach USD 1.33 billion, up from USD 0.83 billion in 2026, reflecting a 10.29% CAGR.

Which region is projected to grow fastest in Hazelnut milk sales?

Asia-Pacific, expected to post a 10.67% CAGR through 2031 on expanding café culture and local manufacturing.

Why are flavored hazelnut milks gaining traction?

Café-style SKUs such as chocolate-hazelnut deliver indulgence at home, driving a 10.18% CAGR in flavored lines.

Which sales channel offers the highest growth outlook?

Online retail, expanding at a 10.55% CAGR as click-and-collect and algorithmic substitutions boost category penetration.

Page last updated on: