Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 24.37 Billion |

| Market Size (2026) | USD 25.36 Billion |

| Market Size (2031) | USD 30.94 Billion |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Flavored Milk Market Analysis by Mordor Intelligence

The Asia-Pacific flavored milk market size is projected to expand from USD 24.37 billion in 2025 and USD 25.36 billion in 2026 to USD 30.94 billion by 2031, registering a 4.07% CAGR between 2026 and 2031. Middle-class consumers in China, India, and fast-growing Southeast Asian economies are trading up from loose dairy to packaged, fortified products, while lactose-intolerant segments across East Asia are embracing soy-, almond-, and oat-based alternatives that mirror traditional flavors yet add functional nutrition. Chocolate remains the dominant flavor, but strawberry and a widening array of local variants such as gula melaka, kesar badam, matcha, and taro are accelerating, fueled by social media buzz and café cross-overs. Premium claims around A2 protein, probiotics, and calcium fortification support margin expansion even as regulatory scrutiny on sugar labeling and raw-milk sourcing raises compliance costs. Off-trade retail still moves most volume, yet on-trade partners—coffee shops, bubble-tea chains, and vending networks—are reshaping how the Asia-Pacific flavored milk market reaches urban consumers.

Key Report Takeaways

- By product type, dairy-based variants commanded 88.32% of the Asia-Pacific flavored milk market share in 2025, while plant-based alternatives are advancing at a 5.54% CAGR through 2031.

- By flavor profile, chocolate led with 44.59% revenue share in 2025; strawberry is forecast to expand at a 6.67% CAGR to 2031.

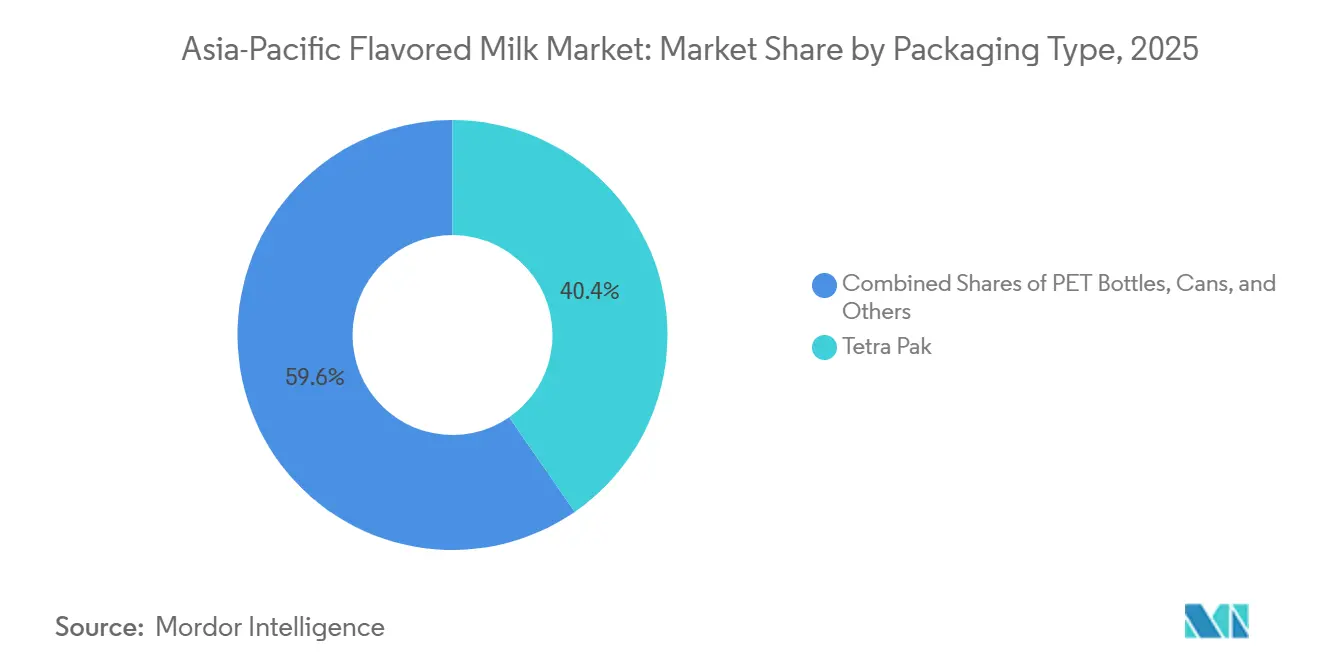

- By packaging type, Tetra Pak accounted for 40.38% of the Asia-Pacific flavored milk market size in 2025, whereas PET and glass formats are set to grow at a 4.89% CAGR during 2026-2031.

- By distribution channel, off-trade outlets held 41.72% revenue share in 2025, but on-trade venues are projected to post a 6.02% CAGR through 2031.

- By geography, China generated 65.24% of revenues in 2025; Australia is the fastest-growing market at a 5.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Flavored Milk Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Health-Centric Dairy Products | +0.9% | Global, with peak adoption in Japan, South Korea, Australia | Medium term (2-4 years) |

| Rising Disposable Incomes in Emerging Countries | +1.2% | China, India, Indonesia, Vietnam, with spillover to Philippines | Long term (≥ 4 years) |

| Product Innovation, Including Plant-Based Variants and Local Flavors | +0.8% | Global, early gains in Singapore, Malaysia, urban China | Medium term (2-4 years) |

| Rising Consumption of Fortified and Functional Milk Products | +0.7% | India, China, Southeast Asia core markets | Medium term (2-4 years) |

| Increasing Modern Retail Expansion in the Region | +0.6% | Indonesia, Vietnam, rural China and India | Long term (≥ 4 years) |

| Rising Inclination Towards Protein-Rich and Nutrient Dense Beverages | +0.5% | Global, with early traction in Australia, urban China, South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Health-Centric Dairy Products

Consumers across Asia-Pacific increasingly view flavored milk as a functional beverage rather than an indulgent treat, driving demand for low-sugar, high-protein, and probiotic-enriched variants. Tetra Pak's 2025 consumer research found that 62% of respondents prioritize physical health when selecting dairy products, and 59% express interest in ready-to-drink liquid formats that deliver convenience without compromising nutrition. This shift is most pronounced in Japan and South Korea, where aging populations seek calcium and vitamin D fortification to mitigate osteoporosis risk, and in Australia, where lactose-free and A2 protein milk cater to digestive sensitivities. Manufacturers respond by reformulating existing SKUs: Vinamilk upgraded its chocolate milk in December 2025 to contain 2.5 times more chocolate while reducing fat by 21%, and introduced Vinamilk Flex with 70% more calcium than its no-sugar nutritional milk baseline, fortified with vitamin D3 for absorption. The trend extends to plant-based offerings, where soy and oat variants are fortified with B12, calcium, and omega-3 to match dairy's nutritional profile, blurring the line between indulgence and wellness.

Rising Disposable Incomes in Emerging Countries

Rising per capita incomes in China, India, Indonesia, and Vietnam are driving a shift among millions of households from unbranded dairy products to packaged, branded flavored milk. According to China's National Bureau of Statistics, per capita disposable income reached USD 6,025 in 2025, reflecting a 5.0% increase in real terms. Urban incomes averaged USD 7,848, while rural incomes stood at USD 3,397[1]Source: National Bureau of Statistics of China, “Per Capita Disposable Income 2025,” stats.gov.cn. This income growth corresponds with a 9.3% year-on-year rise in retail sales of grains, oils, and food products, alongside a 26.1% share for online retail, emphasizing a shift toward modern, traceable supply chains. In India, Amul reported a FY25 turnover of INR 90,000 crore (USD 1,078 billion) and aims to achieve INR 100,000 crore (USD 1,198 billion) within two years. This goal is supported by an INR 10,000 crore (USD 120 billion) expansion plan, which includes a new processing plant in Assam with a daily capacity of 100,000 liters, costing USD 12 million. In Indonesia, the "Free Nutritious Meals" program, launched in January 2025 and targeting 83 million children, is generating institutional demand for fortified flavored milk. However, economic slowdowns during the first half of 2025 have impacted middle-class purchasing power, highlighting the sector's sensitivity to macroeconomic conditions, as reported by the Government of Indonesia.

Product Innovation, Including Plant-Based Variants and Local Flavors

Manufacturers are increasingly leveraging plant-based formulations and region-specific flavors to align with cultural preferences. In March 2026, Oatside introduced Nobo Soy, a soy-based flavored milk, in Singapore and Malaysia. This launch targets the 48% of Malaysian consumers who have increased their plant-based intake and the 30% of Singaporeans reducing dairy consumption. In the same month, Farm Fresh expanded its UHT flavored milk range with two new variants: gula melaka, a traditional Malaysian palm sugar, and Ichiba Melon, inspired by Japanese flavors. The rapid sell-out of Ichiba Melon highlights the market's demand for hybrid local-global flavors. In India, Parle Agro launched Smoodh Kesar Badam in February 2026. This product, featuring a blend of saffron and almond, is available in 80 ml (priced at INR 10) and 150 ml (priced at INR 20) packs, targeting both urban and rural consumers. In May 2025, Nestlé unveiled Bear Brand Milk N' Soy in the Philippines. This product, aimed at school-age children, combines dairy and soy protein. By utilizing enzyme-based technology, Nestlé has effectively removed the beany flavor and gritty texture, addressing concerns in a market where nearly 1 in 3 children under five experience stunting. These product innovations reflect a strategic industry shift: companies are moving beyond importing Western flavors. Instead, they are collaborating with local consumers to incorporate flavors like taro, matcha, red bean, and tropical fruits into their product pipelines.

Rising Consumption of Fortified and Functional Milk Products

As consumers increasingly demand tangible health benefits, functional claims such as probiotics, HMO, A2 beta-casein, and high protein have become critical in the market. In the first half of 2025, Mengniu introduced over 100 new products, including 72 ready-to-drink items. These products included flavored milk with intellectual property tie-ins, probiotic variants like You Yi C lemon tea and Guan Yi Ru yogurt, as well as HMO children's milk and A2 beta-casein formulations. Mengniu also developed proprietary probiotic strains, Lc19 and Hi188, emphasizing its position as a science-driven innovator rather than a commodity supplier. In India, Country Delight launched Provilac, a protein-fortified flavored milk. Amul benefited from GST reductions in September 2025, which made UHT milk tax-free and applied a 5% GST on butter, ghee, and cheese, encouraging trials across more than 700 SKUs. Danone's ultra-premium Aptamil Essensis range, fortified with Bifidobacteria breve M-16V and a 9:1 ratio of prebiotics scGOS to lcFOS, achieved a 14% market share in China's infant formula segment by December 2024, showcasing how fortification drives premiumization and margin growth.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns about High Sugar Content in Flavored Milk | -0.6% | Global, with regulatory pressure in India, Australia, Japan | Short term (≤ 2 years) |

| Prevalence of Lactose Intolerance | -0.4% | East Asia (China, Japan, South Korea), Southeast Asia | Long term (≥ 4 years) |

| Supply Chain Inefficiencies in the Region | -0.5% | India, Indonesia, Vietnam, rural China | Medium term (2-4 years) |

| Stringent Food Safety and Labeling Regulations | -0.3% | China, India, Australia, with spillover to ASEAN | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Concerns about High Sugar Content in Flavored Milk

Public health campaigns and regulatory mandates targeting added sugar are pressuring manufacturers to reformulate or risk losing shelf space and consumer trust. India's Food Safety and Standards Authority issued draft amendments in February 2025 requiring bold, larger fonts for added sugar, saturated fat, and sodium declarations, along with the percentage of the recommended daily allowance, directly impacting flavored milk SKUs that often exceed 10 grams of sugar per 100 ml. Australia's FSANZ and Japan's Ministry of Health, Labour and Welfare have signaled similar front-of-pack labeling initiatives, creating compliance costs and potential SKU rationalization. Manufacturers respond by launching reduced-sugar variants, Vinamilk's upgraded chocolate milk cuts fat by 21% while increasing chocolate intensity, and Vinamilk Flex contains no added sugar, but these reformulations risk alienating consumers accustomed to sweeter profiles. The tension between health positioning and taste preference is most acute in children's segments, where parents demand nutrition but children drive purchase decisions based on flavor.

Prevalence of Lactose Intolerance

Lactose intolerance affects 70-100% of adults in East Asia (China, Japan, South Korea), 50-80% in Southeast Asia, and 30-60% in South Asia (India), constraining dairy-based flavored milk penetration and accelerating plant-based adoption. This genetic predisposition explains why plant-based segments will grow at 5.54% CAGR through 2031, outpacing dairy-based variants, and why manufacturers invest in lactose-free formulations. Meiji launched lactose-free chocolate milk in Thailand, while Vinamilk Flex is explicitly lactose-free, targeting the 50-80% of Southeast Asian adults who experience digestive discomfort from conventional dairy. However, lactose-free and plant-based products command 10-20% price premiums, limiting adoption among price-sensitive rural consumers and creating a bifurcated market where urban, affluent households access functional alternatives while rural populations remain underserved. This dynamic favors multinational and premium local brands with R&D budgets to develop enzyme-treated or plant-protein blends, widening the gap between market leaders and smaller players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Plant-Based Variants Gain Share Despite Dairy Dominance

In 2025, dairy-based flavored milk accounted for 88.32% of the market revenue, driven by strong consumer preferences, a robust cold-chain infrastructure, and competitive pricing. However, plant-based alternatives are set to grow at a 5.54% CAGR through 2031, as manufacturers address the needs of lactose-intolerant consumers and respond to increasing sustainability demands. Within the dairy segment, cow milk remains the primary choice, supporting the majority of chocolate, strawberry, and vanilla products. In contrast, goat milk occupies a niche market, focusing on premium, digestibility-oriented products targeted at infants and elderly consumers. Buffalo and camel milk cater to hyper-local markets in India and the Middle East but lack the scale to influence broader regional trends. The plant-based sector is diversifying into soy, almond, oat, and hybrid blends, each appealing to specific consumer groups. Soy attracts cost-conscious households seeking protein, almond appeals to health-focused urban consumers willing to pay a premium, and oat resonates with environmentally conscious millennials and Gen Z. Nestlé's Bear Brand Milk N' Soy, launched in the Philippines in May 2025, exemplifies this hybrid innovation. By combining dairy and soy with enzyme technology to eliminate the beany flavor and gritty texture, Nestlé expands its market reach without cannibalizing its core dairy sales.

Oatside's Nobo Soy, introduced in March 2026 in Singapore and Malaysia, taps into the 48% of Malaysian consumers who have increased their plant-based consumption. Meanwhile, Farm Fresh's gula melaka and Ichiba Melon UHT variants demonstrate how local flavors can drive consumer trials, even in emerging plant-based categories. Regulatory frameworks are increasingly distinguishing between dairy and plant-based products. For example, India's FSSAI requires flavored milk to meet specific fat and solids-not-fat standards and mandates clear heat treatment declarations. Conversely, plant-based beverages are prohibited from using the term "milk" unless it is prefixed with the plant source. While these regulations reduce consumer confusion, they also limit plant-based brands' ability to leverage dairy's established health reputation. As a result, plant-based brands are focusing on building independent identities centered on sustainability, allergen-free claims, and functional fortification.

By Flavor Profile: Strawberry Accelerates as Chocolate Holds Majority

Chocolate flavor held 44.59% of 2025 revenue, benefiting from universal appeal, established supply chains for cocoa powder and chocolate compounds, and IP-driven product launches such as Mengniu's Tom & Jerry co-branded milk and Oak's Rolo collaboration with Nestlé in Australia, yet strawberry will grow at 6.67% CAGR through 2031 as manufacturers target younger demographics with fruit-forward, lower-sugar formulations. Vanilla occupies a stable third position, serving as a base for customization in foodservice channels where baristas add syrups and toppings, while "others", including local flavors like kesar badam, gula melaka, matcha, taro, and tropical fruits, are the fastest-innovating segment, with launches in 2025-2026 demonstrating appetite for novelty. Parle Agro's Smoodh Kesar Badam, introduced in February 2026, combines saffron and almond in 80 ml and 150 ml packs priced at INR 10 and INR 20, leveraging cultural resonance and affordability to penetrate both urban and rural markets.

Flavor preferences vary sharply by geography: chocolate dominates in China, India, and Southeast Asia, where Western confectionery associations drive trial; strawberry performs strongly in Japan and South Korea, where fruit-flavored dairy has deep cultural roots; and local flavors such as taro and matcha resonate in East Asia, with Binggrae's Taro Flavoured Milk achieving cult status in South Korea and export markets like New Zealand. Manufacturers face a strategic trade-off: chocolate and strawberry deliver volume and margin predictability, but local flavors generate buzz, social-media engagement, and premiumization opportunities. The rise of bubble tea, projected to grow from USD 2.83 billion to USD 4.78 billion by 2032, creates crossover demand for flavored milk as a base ingredient, with cafés and QSRs incorporating taro, matcha, and fruit-flavored milk into boba lattes and smoothies, blurring the line between retail and foodservice segments

By Packaging Type: PET Bottles Gain Ground on Sustainability Push

Tetra Pak packaging captured 40.38% of 2025 revenue, supported by ambient-stable distribution, low spoilage rates, and cost-effectiveness in rural markets where cold-chain infrastructure remains underdeveloped, yet PET and glass bottles will expand at 4.89% CAGR through 2031 as urban consumers prioritize recyclability, resealability, and on-the-go convenience. Tetra Pak's February 2026 launch of a paper-based barrier package with Maeil Dairies in South Korea, featuring 87% renewable content and 26% carbon footprint reduction, addresses sustainability concerns while maintaining the format's core advantages of high-speed filling (24,000 packs per hour on A3/Speed lines) and extended shelf life. Cans occupy a niche in vending-machine and convenience-store channels, particularly in Japan, where Starbucks launched its first vending-machine-exclusive RTD beverage, My Retreat Caramel Macchiato, in October 2025, priced at JPY 240 and leveraging Japan's 2.1 million vending machines for impulse purchases. Other packaging formats, pouches, cups, and bulk containers, serve institutional and foodservice segments but lack the retail visibility to drive consumer brand equity.

PET bottles' growth trajectory reflects urbanization and premiumization: single-serve 200-300 ml bottles cater to commuters and gym-goers, while 600 ml formats like Oak's Rolo x Oak collaboration in Australia (RRP AUD 3.90) target at-home consumption and sharing occasions Inside FMCG. Glass bottles remain marginal due to weight, breakage risk, and reverse-logistics complexity, but premium brands deploy them for differentiation in specialty retail and export markets. Regulatory pressure on single-use plastics is intensifying: China's National Development and Reform Commission and Ministry of Ecology and Environment have phased out non-degradable plastic bags and straws in major cities, prompting manufacturers to explore compostable PET alternatives and deposit-return schemes. This regulatory environment favors large players with capital to invest in sustainable packaging R&D, while smaller brands face margin compression or risk losing shelf space in environmentally conscious retail chains.

By Distribution Channels: On-Trade Gains Momentum via Foodservice Partnerships

In 2025, off-trade channels, comprising supermarkets, hypermarkets, convenience stores, specialist retailers, and online platforms, represented 41.72% of total revenue. This highlights the prominence of household consumption and the extensive modern retail infrastructure. Meanwhile, on-trade outlets, including cafés, quick-service restaurants, vending machines, and institutional food services, are expected to grow at a 6.02% CAGR through 2031. This growth is driven by manufacturers establishing B2B partnerships and leveraging impulse purchases. Within the off-trade segment, supermarkets and hypermarkets dominate due to their broad assortments and promotional visibility. However, convenience stores are rapidly increasing their market share, benefiting from 24/7 availability, strategic high-footfall locations, and chilled-beverage coolers designed for grab-and-go purchases. The 2025 expansion of FamilyMart and Lawson across China and Southeast Asia, featuring exclusive SKUs like Morinaga's Milk Pudding Ice Bar, demonstrates how convenience chains use limited-edition products to attract foot traffic and increase basket size.

On-trade channels are shifting from a secondary role to a strategic focus. Coffee-shop chains, bubble-tea outlets, and quick-service restaurants (QSRs) are increasingly incorporating flavored milk into their core offerings. China's coffee consumption, which reached 3.3 billion cups in 2023, is projected to grow to 5 billion cups by 2025. This surge is fueled by the rising demand for dairy-based lattes and milk teas, which frequently use flavored milk as a key ingredient. This trend could contribute an additional CNY 26.5 billion (USD 3.68 billion) to the sector. Yili and Mengniu have both launched professional dairy brands targeting catering, coffee, tea, and bakery operators. These brands provide bulk formats, customized fat and protein ratios, and co-branding opportunities, embedding their products into high-margin foodservice offerings. In October 2025, Starbucks Japan introduced the My Retreat Caramel Macchiato, a ready-to-drink beverage exclusive to vending machines and priced at JPY 240. This initiative highlights how global chains are leveraging Japan's 2.1 million vending machines to expand their brand presence beyond traditional retail locations.

Geography Analysis

In 2025, China's 65.24% revenue share highlights its competitive advantages: a massive consumer base of 1.4 billion, well-developed cold-chain networks in tier-1 and tier-2 cities, and leading local companies like Mengniu and Yili. These firms capitalize on vertical integration and B2B partnerships to drive volume growth. Mengniu reported H1 2025 revenue of CNY 41.57 billion (USD 5.77 billion) and an operating profit of CNY 3.54 billion (USD 492 million), reflecting a 13.4% increase. This growth was supported by over 100 new product launches, including flavored milk with IP tie-ins, probiotic variants, and A2 beta-casein formulations. Similarly, Yili achieved a 16% revenue increase and a 12% rise in pre-tax profits during H1 2025, driven by capacity expansions at Westland Hokitika (10,000 tonnes of butter), Glenavy (skim milk powder), and Rolleston (20% UHT cream growth). Yili's focus on deep-processed dairy and its ice cream expansion in Southeast Asia, where it leads the market in Indonesia, further contributed to its success. In 2025, China's per capita disposable income reached CNY 43,377 (USD 6,025), a 5.0% real-term increase. Urban incomes averaged CNY 56,502 (USD 7,848), while rural incomes stood at CNY 24,456 (USD 3,397). This income growth enabled middle-class households to upgrade to fortified, branded flavored milk. However, regulatory changes present challenges: In September 2025, China's State Administration for Market Regulation revised UHT milk standards, requiring manufacturers to use raw milk instead of reconstituted powder. While this improves perceived quality, it also raises input costs.

India, Japan, and South Korea represent a secondary tier, each driven by distinct growth factors. In India, Amul's cooperative model, which includes 3.6 million farmers, recorded a turnover of INR 90,000 crore (USD 1.08 billion) in FY25. The company aims to reach INR 100,000 crore (USD 1.20 billion) within two years, supported by a INR 10,000 crore (USD 120 million) expansion plan that includes a new USD 12 million processing plant in Assam. A GST revision in September 2025 made UHT milk tax-free, while butter, ghee, and cheese now carry a 5% GST. This change reduced prices on over 700 SKUs, encouraging consumer trials. Additionally, FSSAI's February 2025 draft amendments, which require bolder sugar declarations, are pushing manufacturers to reformulate products[2]Source: Food Safety and Standards Authority of India, “Draft Labelling Amendment Feb 2025,” fssai.gov.in. Meanwhile, Japan and South Korea are experiencing premiumization trends. Companies like Meiji, Morinaga, and Lotte are introducing lactose-free products, probiotic-enriched options, and limited-edition flavors. Notable launches include Morinaga's Milk Pudding Ice Bar, exclusive to Lawson in December 2024, and MOW PRIME's Strawberry Chocola Milk in April 2025. Morinaga's Global Business, which accounted for 12.5% of consolidated sales, reached JPY 69.9 billion (USD 490 million) in FYE March 2025. The company is expanding into markets such as Pakistan, Vietnam, Malaysia, Indonesia, and China, leveraging its proprietary bifidobacteria and lactoferrin ingredients.

Australia is projected to achieve the fastest CAGR at 5.32% through 2031, driven by A2 Milk's focus on A2 protein and export-oriented strategies. A2 Milk's share in Australia's liquid milk market rose to 11.2% in FY25, an increase of 0.8 percentage points. The company is also among the top-4 brands in China's infant formula market, benefiting from a strategic partnership with Fonterra in March 2024. This collaboration established combined A2 milk pools in New Zealand and Australia, granted exclusive fresh milk licenses in New Zealand, and enabled the production of nutritional products for Southeast Asia and the Middle East. However, markets like Indonesia, Vietnam, and the broader Asia-Pacific face challenges due to cold-chain limitations. In India, 10-15% of milk is lost to spoilage, despite a cold-chain infrastructure valued at USD 9.75 billion in 2023, which is expected to grow to USD 12.85 billion by 2028, according to the Government of India[3]Source: Government of India, “Cold Chain Infrastructure Report 2025,” india.gov.in. Vietnam's cold-chain market, valued at USD 169 million, meets only 20% of demand, limiting the distribution of chilled flavored milk beyond tier-1 cities. Indonesia's Free Nutritious Meals program, launched in January 2025 and targeting 83 million children, has increased institutional demand. However, economic slowdowns in the first half of 2025 have weakened middle-class purchasing power, highlighting the sector's sensitivity to macroeconomic conditions.

Competitive Landscape

The Asia-Pacific flavored milk market is moderately concentrated, with the top four players holding notable but not dominant shares. This leaves opportunities for regional specialists, plant-based innovators, and foodservice-focused players to target niche segments. Leading companies like Mengniu, Yili, and Amul utilize vertical integration to manage raw milk procurement, processing, and distribution. This approach enables them to achieve cost efficiency and extensive market penetration. On the other hand, multinational companies such as Nestlé, Danone, and FrieslandCampina differentiate themselves through proprietary technologies, including enzyme-based dairy-soy blends and synbiotic formulations, focusing on functionality and premiumization. Mengniu's development of proprietary probiotic strains Lc19 and Hi188, along with Danone's ultra-premium Aptamil Essensis range fortified with a specific 9:1 ratio of Bifidobacteria breve M-16V and prebiotics scGOS:lcFOS, highlights the role of R&D investments in creating intellectual property that smaller competitors find difficult to replicate.

Growth opportunities are concentrated in plant-based hybrids and local flavor innovations. For example, Nestlé's Bear Brand Milk N' Soy in the Philippines and Oatside's Nobo Soy in Singapore/Malaysia demonstrate how affordable dairy-plant blends can expand market reach without eroding core dairy sales. Similarly, local flavors like Farm Fresh's gula melaka and Ichiba Melon variants are driving social media engagement and consumer trials, showcasing the potential of localized offerings. Emerging players, including plant-based brands like Oatside and Vitasoy and premium local names such as Farm Fresh and Binggrae, are leveraging the incumbents' focus on volume and cost efficiency. These disruptors appeal to urban consumers and early adopters who are willing to pay 10-20% premiums for innovative flavors and functional benefits. The market is also experiencing a technological divide.

Large players are investing in high-speed aseptic filling lines, AI-driven demand forecasting, and blockchain for supply chain optimization, while smaller brands are utilizing quick-commerce platforms and direct-to-consumer models to bypass traditional retail channels and gather real-time consumer feedback. Yili and Mengniu are redefining flavored milk's role by launching professional dairy brands for catering, coffee, tea, and bakery operators. This strategy transforms flavored milk from a retail product into a foodservice ingredient, diversifying revenue streams and mitigating the impact of retail price wars. As food safety standards evolve, larger vertically integrated players are better equipped to upgrade their processing infrastructure, giving them a competitive edge. In contrast, smaller brands face tighter margins and the risk of losing shelf space in quality-conscious retail chains.

Asia-Pacific Flavored Milk Industry Leaders

China Mengniu Dairy Co. Ltd.

Gujarat Co-operative Milk Marketing Federation Ltd. (Amul)

Nestlé S.A.

Danone S.A.

Saputo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Maola Local Dairies introduced Strawberry Whole Milk, a new flavored dairy product targeting consumer preferences for indulgent, clean-label options with rich texture and balanced strawberry taste. Available in quart sizes, it provides 8 grams of protein and 13 essential nutrients per serving, and is free from artificial dyes.

- December 2025: Milku launched a novel flavored milk variant inspired by the iconic Marie biscuit, marking a strategic fusion of traditional snacking heritage with contemporary dairy innovation.

- April 2025: Unilever Australia and dairy brand Breaka launched a limited‑edition Breaka Weis Mango and Cream flavored milk in Queensland. The product, a low‑fat mango‑and‑cream‑flavored milk with no artificial colors or flavors, was rolled out in 500 mL packs across grocery and convenience stores.

- March 2025: Hamdard Foods India entered the flavored milk segment with the launch of Hamdard Asli Milkshakes, a ready‑to‑drink milkshake range in Chocolate, Strawberry, Mango, and Vanilla flavors targeted at children and young consumers.

Asia-Pacific Flavored Milk Market Report Scope

The Asia-Pacific flavored milk market is segmented by type into dairy-based and plant-based. By distribution channel, the market is segmented into Off-Trade and On-Trade. Off-trade is further segmented into supermarkets/hypermarkets, convenience stores, specialist stores, online retail stores, and other distribution channels. The report also involves the geographical segmentation of the market.

Product Type

| Dairy Based | Cow |

| Goat | |

| Others | |

| Plant Based | Soy |

| Almond | |

| Oats | |

| Others |

Flavor Profile

| Chocolate |

| Strawberry |

| Vanilla |

| Others |

Packaging Type

| PET/Glass Bottles |

| Cans |

| Tetra Pak |

| Others |

Distribution Channels

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Specialist Retailers | |

| Convenience Stores | |

| Online Retail | |

| Other Distribution Channels |

Geography

| China |

| India |

| Japan |

| Australia |

| South Korea |

| Vietnam |

| Indonesia |

| Rest of Asia-Pacific |

| Product Type | Dairy Based | Cow |

| Goat | ||

| Others | ||

| Plant Based | Soy | |

| Almond | ||

| Oats | ||

| Others | ||

| Flavor Profile | Chocolate | |

| Strawberry | ||

| Vanilla | ||

| Others | ||

| Packaging Type | PET/Glass Bottles | |

| Cans | ||

| Tetra Pak | ||

| Others | ||

| Distribution Channels | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Specialist Retailers | ||

| Convenience Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| Geography | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large will the Asia-Pacific flavored milk market be by 2031?

It is forecast to reach USD 30.94 billion, advancing at a 4.07% CAGR from 2026 to 2031.

Which flavor is growing fastest in Asia-Pacific flavored milk?

Strawberry is projected to register a 6.67% CAGR through 2031 as brands roll out fruit-forward, lower-sugar recipes appealing to younger consumers.

Why is Australia the fastest-growing country market?

Australia benefits from the a2 protein proposition, export-oriented processing capacity, and a forecast 5.32% CAGR, the quickest in the region.

How are sugar-labeling rules affecting flavored milk makers?

India’s draft front-of-pack regulation and similar moves in Australia and Japan are forcing reformulations that trim added sugar to maintain shelf presence.

Page last updated on: