Soy Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

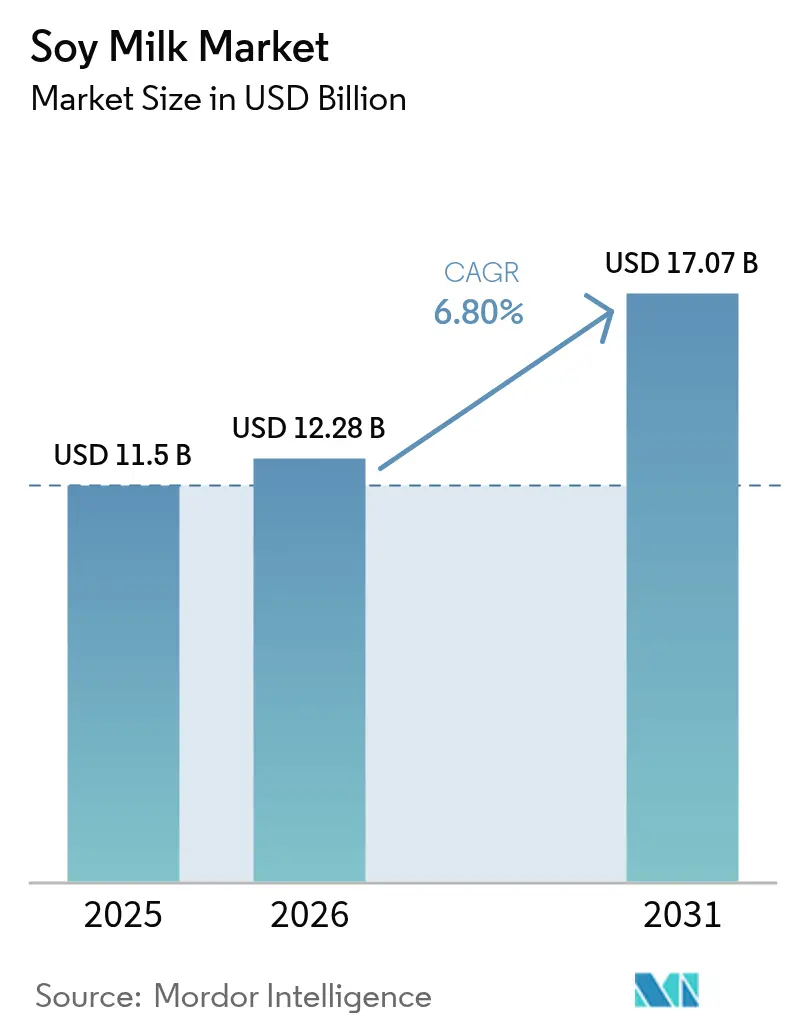

| Market Size (2026) | USD 12.28 Billion |

| Market Size (2031) | USD 17.07 Billion |

| Growth Rate (2026 - 2031) | 6.80% CAGR |

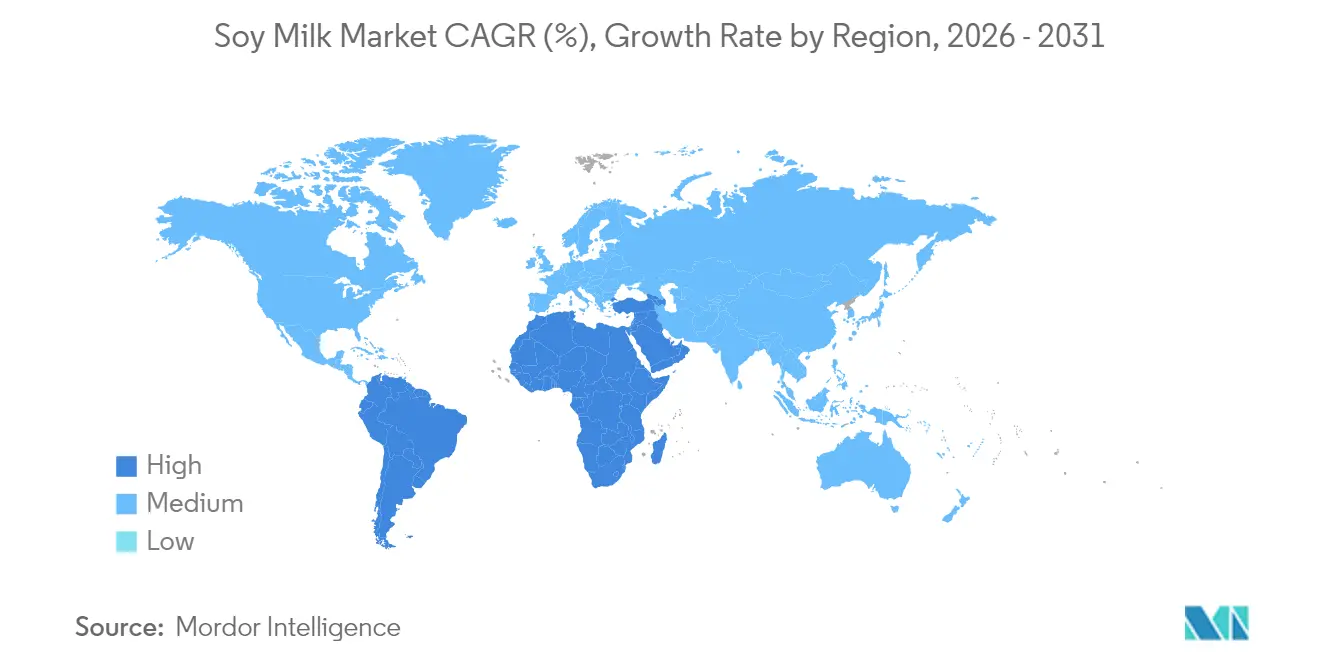

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Soy Milk Market Analysis by Mordor Intelligence

The soymilk market size in 2026 is estimated at USD 12.28 billion, growing from 2025 value of USD 11.50 billion with 2031 projections showing USD 17.07 billion, growing at 6.8% CAGR over 2026-2031. Several factors contribute to this growth, including increased health awareness and growing concerns about sustainability among consumers. The rising cases of lactose intolerance and milk allergies worldwide have driven consumers toward soymilk, a naturally lactose-free and hypoallergenic alternative. The adoption of vegan and flexitarian diets, particularly among younger and urban populations, has accelerated the transition from traditional dairy products. Soymilk's nutritional composition, which includes high-quality protein, essential amino acids, vitamins, and minerals, appeals to health-conscious consumers seeking nutritious beverages. Improvements in food processing technology have enhanced soymilk's taste, texture, and shelf life, addressing previous consumer concerns. The increased availability of soymilk through supermarkets, convenience stores, and online platforms, supported by marketing campaigns and celebrity endorsements, has improved product accessibility. Additionally, government policies and regulations supporting plant-based diets for environmental and health benefits have contributed to market growth.

Key Report Takeaways

- By product type, unflavored soy milk lines captured 77.68% of the soy milk market share in 2025, while flavored variants are forecast to expand at a 7.01% CAGR to 2031.

- By form, ready-to-drink (RTD) formats controlled 73.75% share of the soy milk market size in 2025; powder formats are projected to grow at a 12.57% CAGR through 2031.

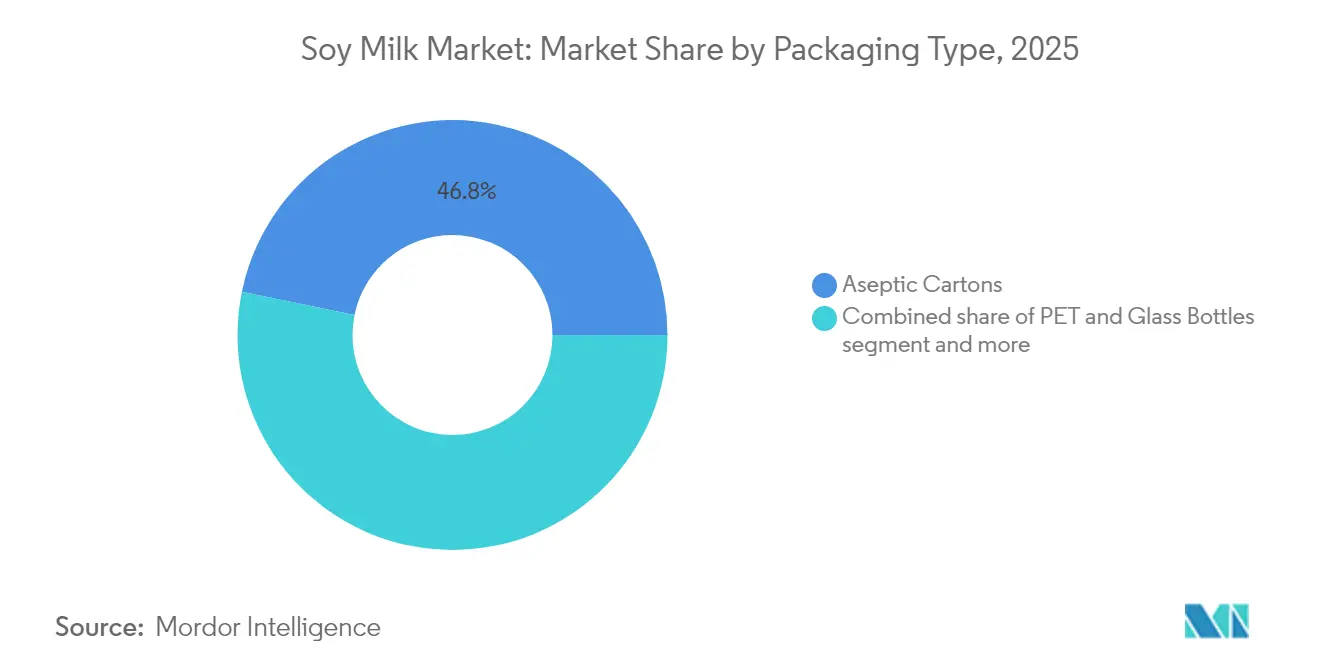

- By packaging type, aseptic cartons led with 46.78% revenue share in 2025, whereas flexible pouches are set to post a 12.18% CAGR to 2031.

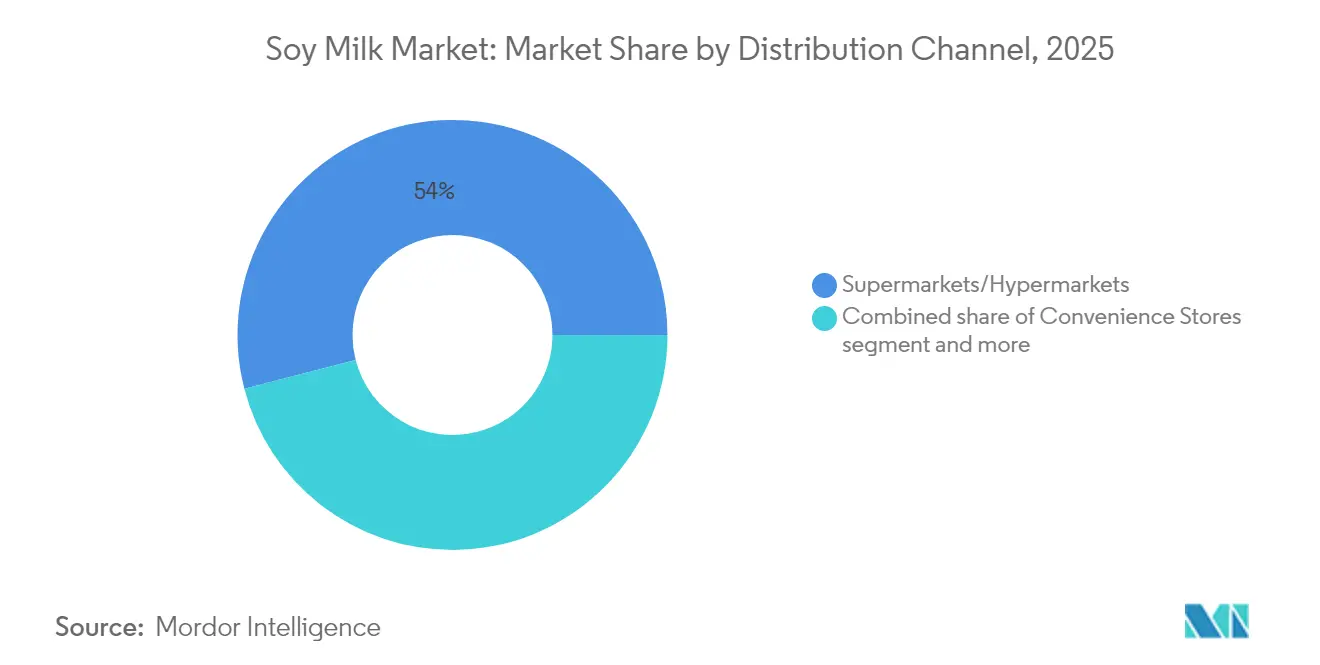

- By distribution channel, supermarkets/hypermarkets held 54.02% of 2025 sales, while online channels recorded the fastest growth at 13.34% CAGR.

- By geography, Asia-Pacific captured 66.88% of 2025 revenue; the Middle East and Africa are expected to register the highest regional CAGR of 11.34% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Soy Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of soy milk in foodservice channels | +1.2% | Global, with strongest gains in North America and Europe | Medium term (2-4 years) |

| Increasing adoption of vegan and vegetarian diets | +1.8% | Global, led by Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Product innovations and diverse flavors expand market reach | +0.9% | Global, with premium positioning in developed markets | Short term (≤ 2 years) |

| Nutritional benefits propel market growth | +1.4% | Global, particularly strong in health-conscious demographics | Long term (≥ 4 years) |

| EU carbon-footprint labelling favouring soy beverages | +0.7% | Europe, with spillover effects to other regulated markets | Medium term (2-4 years) |

| E-commerce milk-subscription boom | +0.8% | Global, led by urban markets in developed economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adoption of Soy Milk in Foodservice Channels

The foodservice industry's adoption of soy milk is driving market growth, as institutional buyers select plant-based alternatives to meet dietary requirements and manage costs. Foodservice operators choose soy milk for its high protein content and operational efficiency in large-scale food preparation. Among plant-based alternatives, soy milk's protein composition is most similar to dairy milk, making it suitable for institutional nutrition programs. The demand for specialized barista formulations is increasing, particularly from coffee chains and restaurants that require products that maintain foam stability and prevent curdling in hot beverages. The removal of additional charges for non-dairy milk options by Starbucks in October 2024 demonstrates the growing institutional acceptance and demand for plant-based alternatives, including soy milk. The foodservice sector values soy milk's consistent supply and standardized nutritional content over alternatives like almond or oat milk, which face greater raw material price and availability fluctuations. This widespread adoption in foodservice establishments supports sustained market growth beyond retail consumer trends, establishing soy milk as an essential component of the food industry.

Increasing Adoption of Vegan and Vegetarian Diets

The global soy milk market is experiencing substantial growth due to the increasing adoption of vegan and vegetarian diets, primarily driven by health consciousness, environmental sustainability concerns, ethical considerations, and economic factors. Consumer preferences are shifting towards plant-based alternatives due to rising awareness of lactose intolerance, concerns about cholesterol levels, and the environmental impact of traditional dairy farming. The market growth is further propelled by technological advancements in processing methods, enhanced product formulations, and significant investments in research and development. According to World Population Review, India and Mexico's vegan population reached 9% in 2025, particularly supported by the rapid expansion of modern retail formats, increasing urbanization, rising disposable incomes, and growing awareness of plant-based nutrition benefits [1]Source: World Population Review, "Veganism by Country 2025", worldpopulationreview.com . This shift is further accelerated by the expansion of retail distribution networks, product innovations in taste and nutritional content, and increasing investments in plant-based protein technologies across the food and beverage industry.

Product Innovations and Diverse Flavors Expand Market Reach

Product innovation and flavor diversification are driving the expansion of the global soy milk market through strategic responses to consumer demands for health benefits and taste preferences. The market growth is primarily influenced by increasing health consciousness, rising lactose intolerance cases, and the growing adoption of plant-based diets. Manufacturers are responding to these trends by developing enhanced soy milk products beyond traditional plain varieties, utilizing advanced processing technologies and ingredient formulations. Companies have systematically expanded their product portfolios to include vanilla, chocolate, and functional variants fortified with calcium, vitamin D, and omega-3s, addressing specific nutritional requirements. This trend is exemplified by Lactasoy's March 2023 launch of a chocolate-flavored soy milk with 26% reduced sugar content, directly addressing the growing consumer demand for healthier alternatives in the flavored beverage segment. The product contains nine amino acids and omega-3, 6, and 9, strategically targeting the expanding demographic of consumers seeking chocolate flavor with additional protein benefits. These systematic innovations particularly resonate with younger consumers and flexitarians who demonstrate a consistent preference for products that balance taste and nutritional value in their beverage choices.

Nutritional Benefits Propels Market Growth

The global soy milk market growth is driven by its nutritional benefits, as consumers seek healthier beverage alternatives. Soy milk contains all nine essential amino acids and offers protein quality and digestibility comparable to cow's milk. Its cholesterol-free composition and low saturated fat content appeal to consumers focused on heart health management. Commercial soy milk products are typically fortified with calcium, vitamin D, and vitamin A at levels equivalent to dairy milk, addressing nutritional requirements for consumers who reduce dairy intake. The beverage also contains potassium and unsaturated fatty acids, with studies indicating potential anti-inflammatory effects and reduced risks of cardiovascular disease, certain cancers, and menopausal symptoms. These health benefits influence product development in the market. For instance, in December 2024, Tofusan launched a sugar-free soy milk in Thailand, combining soybeans and black sesame seeds to provide 29 grams of protein. The product features sesamin, an antioxidant with anti-aging properties, and is lactose-free.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Allergen-labelling tightening for soy milk | -0.4% | Global, with strictest enforcement in North America and Europe | Short term (≤ 2 years) |

| Soybean price volatility hinders market growth | -0.8% | Global, with highest impact in price-sensitive markets | Medium term (2-4 years) |

| Shelf-life limitations in rural or underdeveloped areas | -0.3% | Emerging markets, particularly rural areas in Asia-Pacific and Africa | Long term (≥ 4 years) |

| Competition from other plant-based milks | -1.1% | Global, with intense competition in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Allergen-Labelling Tightening for Soy Milk

The implementation of increasingly stringent allergen-labeling regulations for soy milk represents a substantial market restraint, as regulatory authorities worldwide strengthen their oversight measures to protect consumers with food allergies. The Food and Drug Administration (FDA) categorizes soybeans as one of the nine major food allergens, along with milk, eggs, fish, crustacean shellfish, tree nuts, peanuts, wheat, and sesame, necessitating a comprehensive declaration on all packaged food labels. In January 2025, the Food and Drug Administration (FDA) issued revised guidance emphasizing explicit allergen labeling, mandating manufacturers to specify soy and other major allergens in both the ingredient list and a contains statement. These regulatory requirements, while fundamental for consumer safety and transparency, impose substantial compliance burdens on soy milk producers, particularly in critical areas of ingredient sourcing documentation, manufacturing process validation, and cross-contamination prevention protocols.

Soybean Price Volatility Hinders Market Growth

Soybean price volatility significantly constrains the global soy milk market by affecting production costs and supply chain operations. Since soybeans are the key ingredient in soy milk production, price fluctuations caused by weather conditions, geopolitical issues, and agricultural output variations affect manufacturers' pricing decisions, margins, and production volumes. The increase in global soybean prices has raised manufacturing costs, making it difficult for producers to maintain competitive retail prices while preserving profitability. In Japan, this impact is evident through data from the Japan Soy Milk Association, which reported that soy milk product shipping volume decreased to 394.62 thousand kiloliters in 2023, continuing the decline from previous years [2]Source: Japan Soy Milk Association, " Soy Milk Production Volume Survey, January-march 2025", tounyu.jp . This reduction correlates with increased input costs and market inflation from higher raw material prices. As a result, the persistent volatility in soybean prices poses a substantial challenge to market growth, affecting both manufacturers' operational strategies and market expansion potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Sustainable Innovation Drives Flexible Packaging Growth

Aseptic cartons maintain market leadership in the soy milk packaging segment, commanding a 46.78% share in 2025. This market position is attributed to their demonstrated capabilities in product preservation, ambient temperature shelf life extension, and stringent safety standards maintenance. The format has established substantial market penetration and consumer acceptance across international markets, positioning it as the primary packaging solution for residential consumption and portable applications. Aseptic cartons demonstrate full compliance with the European Union's Packaging and Packaging Waste Regulation, which mandates comprehensive packaging recyclability and establishes a 5% reduction target in packaging waste. This regulatory adherence enhances their environmental sustainability credentials and compels industry stakeholders to implement this packaging format to address regulatory requirements and evolving consumer environmental preferences.

Flexible pouches demonstrate significant market momentum as the fastest-expanding packaging segment, exhibiting a compound annual growth rate of 12.18% through 2031. This growth trajectory is attributed to their material efficiency, optimized logistics costs, and reduced storage requirements, complemented by a compact structural design that resonates with environmentally conscious consumer segments. The format delivers operational advantages through integrated resealable mechanisms and enhanced portability characteristics, particularly resonating with younger demographic segments and household consumers. Moreover, PET and glass bottles maintain a consistent market presence in premium product categories, where packaging aesthetics and perceived quality metrics significantly influence consumer purchasing behavior. Other packaging formats, including bag-in-box and bulk containers, serve specialized applications in foodservice and industrial markets.

By Product Type: Unflavored Dominance Faces Flavor Innovation Challenge

Unflavored soy milk maintains a substantial 77.68% market share in 2025, primarily attributed to its extensive utilization in traditional consumption patterns and institutional applications requiring neutral taste profiles. The segment's market dominance is reinforced by its fundamental role in food preparation processes and significant acceptance across multiple cultural demographics, particularly in Asian markets where consumer preferences align with neutral plant-based beverages. The production methodology of unflavored variants demonstrates operational efficiency through streamlined manufacturing processes and reduced ingredient requirements, facilitating competitive price points that drive market expansion in price-sensitive regions.

The flavored soy milk segment demonstrates robust growth prospects with a projected 7.01% CAGR through 2031, attributed to increasing consumer demand for enhanced taste profiles and strategic market expansion initiatives by manufacturers. Within this category, vanilla and chocolate variants maintain prominent positions, with vanilla products serving dual purposes in direct consumption and culinary applications, while chocolate variants specifically target youth demographics and dessert substitute markets. The segment encompasses additional flavor variations, including seasonal and regional formulations, which present opportunities for premium market positioning, although these subcategories currently maintain limited distribution networks and market penetration.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Supermarkets/hypermarkets maintain a dominant 54.02% distribution share in the soy milk market as of 2025. These large-format retail establishments facilitate comprehensive product visibility through strategically positioned plant-based sections and optimal shelf placement. Their extensive product portfolio encompasses fortified formulations, flavor variants, and multiple packaging configurations. The substantial consumer traffic and established shopping patterns enable systematic product comparison and access to structured promotional programs. These retail establishments maintain consistent product availability and market-competitive pricing through sophisticated supply chain networks and established manufacturer partnerships.

Online retail distribution demonstrates significant market momentum, achieving a 13.34% CAGR through 2031. This growth trajectory is attributed to structured subscription models, strategic direct-to-consumer implementations, and evolving consumer purchasing patterns. The online distribution channel has established specialized infrastructure for perishable and semi-perishable product management. Subscription-based distribution systems generate consistent revenue streams and enhance customer retention metrics, while direct-to-consumer frameworks enable manufacturers to optimize margins and establish direct customer relationships. Convenience retail establishments serve as strategic secondary distribution points, particularly for individual unit sales. On-trade channels, encompassing restaurants, cafes, and institutional foodservice, represent growing opportunities for volume expansion and brand building.

By Form: Ready-to-Drink Leadership Challenged by Powder Segment Growth

Ready-to-drink formats maintain a commanding 73.75% market share in 2025, attributed to their strategic positioning in convenience and well-established distribution infrastructure across retail and foodservice channels. The segment's market leadership is fundamentally driven by increasing consumer requirements for immediate consumption solutions and advanced packaging innovations that deliver superior portability and shelf stability characteristics. The implementation of aseptic processing technologies enables Ready-to-Drink (RTD) products to achieve extended shelf stability without refrigeration requirements, thereby optimizing distribution efficiency and minimizing supply chain operational costs.

The powder segment projects a 12.57% CAGR through 2031, supported by cost efficiency, longer shelf life, and increasing adoption in emerging markets with limited cold chain infrastructure. This format appeals to institutional buyers and price-sensitive consumers, creating a distinct market segment with specific competitive dynamics. Growth is significant in markets where consumers accept reconstitution processes and prioritize cost savings. The segment's expansion also comes from foodservice applications that value bulk preparation and storage efficiency. Improvements in powder processing technology enhance solubility and taste, reducing traditional barriers to adoption and expanding the consumer base.

Geography Analysis

Asia-Pacific holds 66.88% market share in 2025, driven by the deep cultural integration of soy-based beverages and robust manufacturing infrastructure in China, Japan, and South Korea. The region's growth is supported by expanding middle-class populations, rising health consciousness, and government policies promoting plant-based protein for food security. China's regulatory changes requiring sterilized milk production from raw milk create market opportunities for plant-based alternatives. The region's manufacturing capabilities and supply chain networks serve both domestic consumption and global export markets.

The Middle East and Africa region projects 11.34% CAGR through 2031, supported by increasing disposable incomes, health awareness, and government food security initiatives. The United Arab Emirates (UAE) position as a regional food distribution hub facilitates market entry for international brands. In 2023, the United States' exports of agricultural and related products to the United Arab Emirates reached USD 1.33 billion, with consumer-oriented goods accounting for over 75% of the increase . Moreover, the Food Innovation Laboratory at the University of the Free State (UFS) in South Africa launched affordable, protein-rich soy-based dairy alternatives in June 2024, addressing regional nutritional needs and food security concerns.

North America and Europe maintain steady market growth through health awareness, environmental concerns, and supportive regulations for sustainable food systems. European markets benefit from carbon footprint labeling requirements and sustainability directives that advantage soy milk over dairy alternatives. North American manufacturers focus on processing capacity expansion and product development to meet consumer demand. South America leverages its soybean production advantage for cost-effective manufacturing, though market growth faces distribution and consumer awareness challenges.

Competitive Landscape

The soy milk market exhibits moderate fragmentation, with established companies maintaining significant market shares through their vertical integration strategies, brand recognition, and distribution capabilities. Major players, including Danone S.A., Vitasoy International Holdings Ltd, The Hain Celestial Group Inc., and Kikkoman Corporation, employ distinct competitive strategies. Danone prioritizes brand portfolio optimization and sustainability positioning, while Vitasoy focuses on regional market leadership and product innovation.

The competitive landscape continues to transform as traditional dairy companies enter the plant-based segments, while specialized plant-based manufacturers expand their portfolios and geographic presence. Companies with strong supply chain integration hold an advantage, as soybean price fluctuations and processing efficiency directly influence profitability. Smaller companies are also gaining market presence, as demonstrated by Zambian manufacturer 260 Brands, which launched the country's first plant-based milk factory in Lusaka in October 2023. The company markets its plant-based milk under the Nutramilk brand.

Moreover, technology adoption creates competitive advantages, with leading manufacturers investing in advanced processing equipment, packaging innovations, and quality control systems to achieve premium positioning and operational efficiency. Patent activities in processing technologies, flavor systems, and nutritional enhancement highlight ongoing innovation competition. Companies aim to establish proprietary advantages in taste, nutrition, and manufacturing efficiency. The competitive landscape reflects shifting consumer preferences, with successful companies adapting their product portfolios and marketing strategies while maintaining operational efficiency and profitability in increasingly competitive markets.

Soy Milk Industry Leaders

-

Danone S.A.

-

Vitasoy International Holdings Ltd

-

The Hain Celestial Group Inc.

-

Campbell Soup Company

-

Kikkoman Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: MALK Organics expanded its product portfolio by introducing Unsweetened Organic Coconut and Unsweetened Organic Soy milk alternatives in response to consumer demand for plant-based beverages with low sugar content. The product development aligned with the company's strategy of manufacturing minimal-ingredient, clean-label beverages for health-conscious consumers.

- February 2025: Kikkoman Corporation had established a global website to showcase its soymilk business operations outside Japan, expanding its international presence. The website provided comprehensive information about the Kikkoman Soymilk brand's overseas expansion to international consumers.

- July 2024: Sanitarium Health Food Company launched a PLANTWELL range of plant-based milk products containing clinically tested ingredients. The product line included high-protein soy milk formulated with seaweed-derived calcium to support bone density and prebiotic fibers to promote gut health.

- April 2024: Yeo Hiap Seng introduced Yeo's Immuno Soy Milk, which contained vitamin B6 and zinc for immune system support. The beverage was naturally high in protein and calcium, available in original and chocolate variants.

Global Soy Milk Market Report Scope

The soymilk market comprises plant-based milk alternatives manufactured from soybeans. These products address the requirements of consumers seeking dairy-free, lactose-free, or vegan beverages. The market consists of both plain and flavored variants utilized for direct consumption, cooking, and as ingredients in food and beverage manufacturing.

The Soy Milk market is segmented by product type, form, packaging, distribution channel, and geography. By product type, the market is segmented into unflavored soy milk and flavored soy milk. Flavored soy milk is further sub-segmented into vanilla, chocolate, and others. By form, the market is segmented into ready-to-drink (RTD) and powder. By packaging type, the market is segmented into aseptic cartons, PET & glass bottles, flexible pouches, and others. By distribution channel, the market is segmented into on-trade and off-trade. Off-trade is further segmented into supermarkets/hypermarkets, convenience stores, online retailers, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Unflavored Soy Milk | |

| Flavored Soy Milk | Vanilla |

| Chocolate | |

| Others |

| Ready-to-Drink (RTD) |

| Powder |

| Aseptic Cartons |

| PET and Glass Bottles |

| Flexible Pouches |

| Others |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retailers | |

| Other Off-Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Unflavored Soy Milk | |

| Flavored Soy Milk | Vanilla | |

| Chocolate | ||

| Others | ||

| By Form | Ready-to-Drink (RTD) | |

| Powder | ||

| By Packaging Type | Aseptic Cartons | |

| PET and Glass Bottles | ||

| Flexible Pouches | ||

| Others | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retailers | ||

| Other Off-Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the soy milk market?

The soy milk market is valued at USD 12.28 billion in 2026 and is forecast to climb to USD 17.07 billion by 2031.

Which region leads global consumption?

Asia-Pacific accounts for 66.88% of worldwide sales, supported by cultural familiarity and strong manufacturing infrastructure.

What segment is growing the fastest?

Powder formats are advancing at a 12.57% CAGR to 2031 as they offer cost and shelf-life advantages in emerging markets.

How are online channels influencing the market?

E-commerce subscription models are expanding at 13.34% annually, providing predictable revenue and direct consumer engagement.

Page last updated on: