Market Overview

| Study Period | 2021 - 2031 |

|---|---|

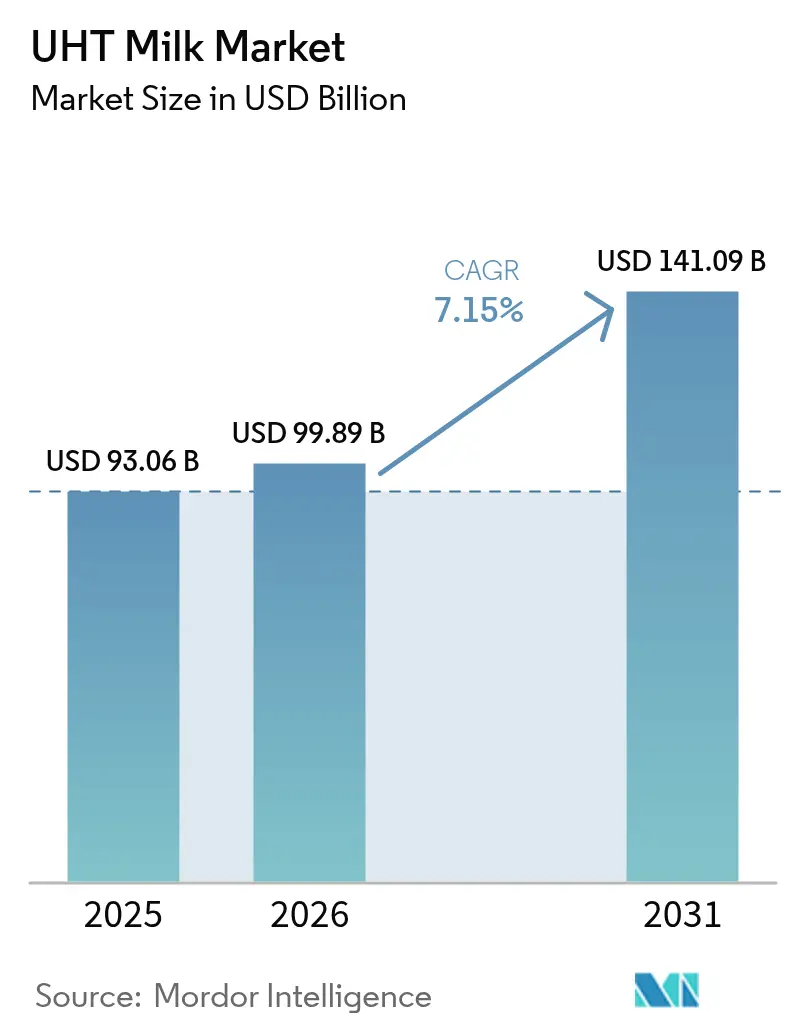

| Market Size (2026) | USD 99.89 Billion |

| Market Size (2031) | USD 141.09 Billion |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

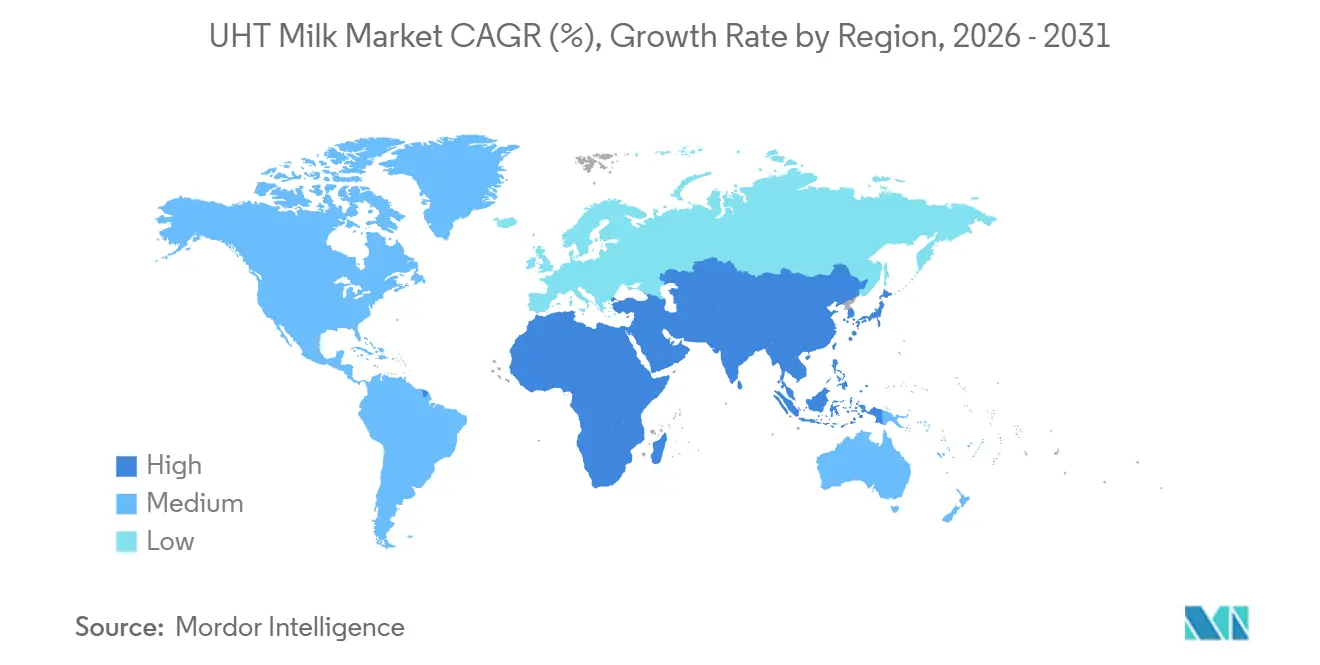

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UHT Milk Market Analysis by Mordor Intelligence

The UHT Milk Market size is expected to increase from USD 93.06 billion in 2025 to USD 99.89 billion in 2026 and reach USD 141.09 billion by 2031, growing at a CAGR of 7.15% over 2026-2031. The growth trajectory underscores the widening gaps in cold-chain infrastructure within emerging economies, the increasing prevalence of households with dual incomes, and the growing penetration of organized retail networks. These factors collectively are encouraging consumers to shift toward shelf-stable dairy products, which offer convenience and longer shelf life. Whole or full-cream variants have traditionally dominated sales; however, there is a noticeable shift as consumers increasingly prefer protein-rich and low-fat options, driving the demand for skimmed formulations. Flexible pouches, known for their cost-effectiveness, are gaining traction in tier-2 and tier-3 cities, making these products more accessible to a broader audience. Additionally, direct-to-consumer platforms are playing a transformative role in reshaping the economics of market distribution by streamlining supply chains and enhancing customer reach. The competitive landscape is intensifying as global companies expand their portfolios to include plant-based blends, while regional cooperatives leverage their local sourcing capabilities to offer products at prices that are up to 20% lower than premium alternatives, thereby appealing to cost-conscious consumers.

Key Report Takeaways

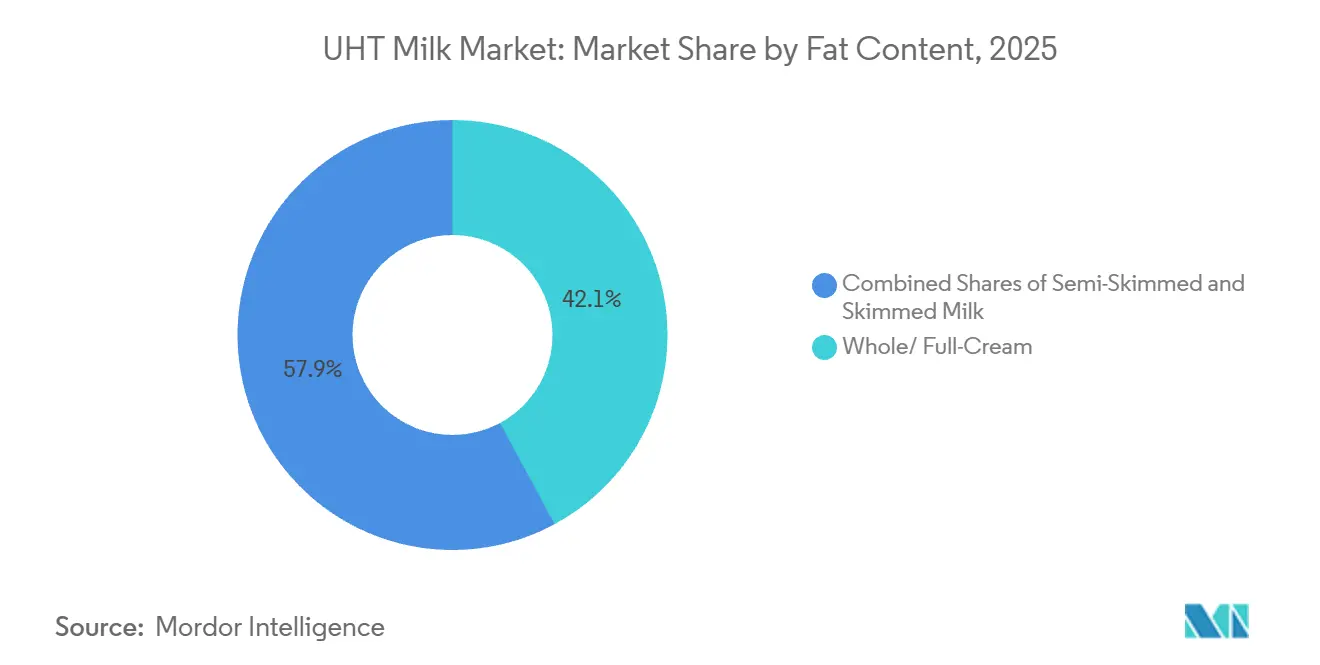

- By fat content, whole or full-cream variants led with 42.12% of the Ultra-high Temperature Milk market share in 2025, while skimmed formulations are projected to expand at a 9.54% CAGR through 2031.

- By flavor, unflavored products accounted for 59.43% of revenue in 2025; flavored variants are forecast to grow at a 9.32% CAGR to 2031.

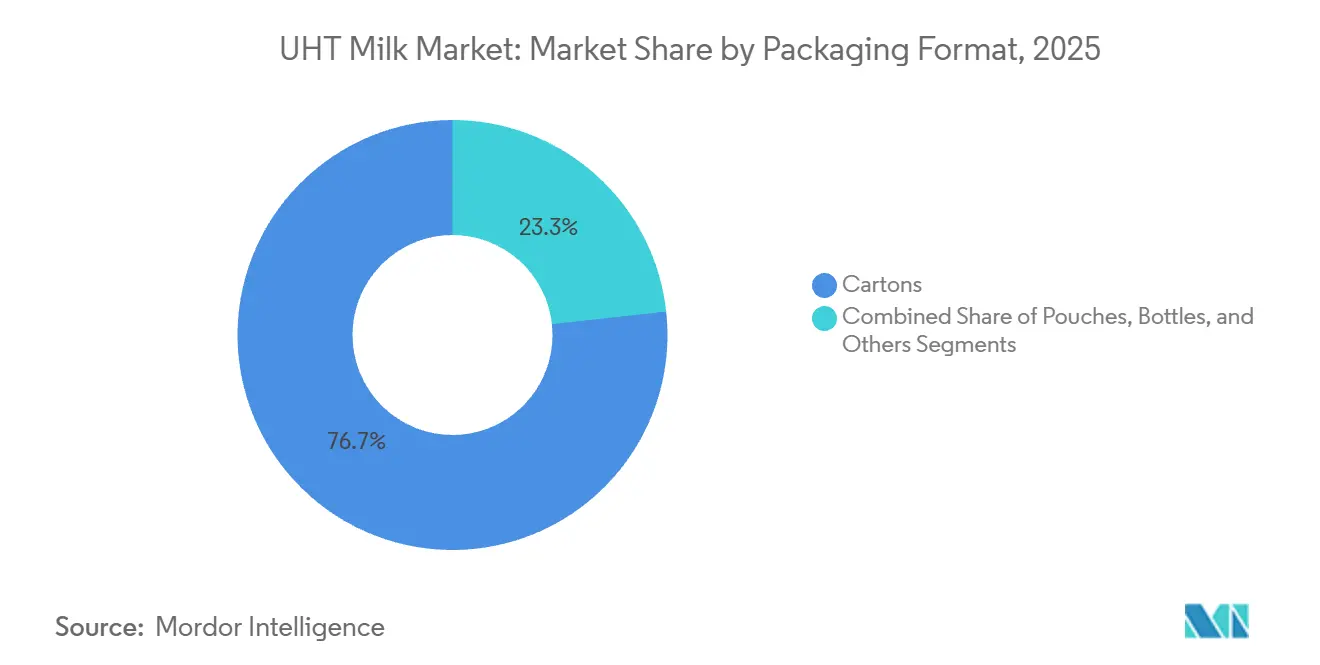

- By packaging format, aseptic cartons captured 76.74% of 2025 volume, yet pouches are poised to rise at a 10.34% CAGR through 2031.

- By distribution channel, retail represented 77.66% of sales in 2025, whereas food-service and HoReCa are rebounding at a 9.74% CAGR on post-pandemic institutional demand.

- By geography, Asia-Pacific is projected to lead regional growth at a 9.82% CAGR, closing the gap with North America, which commanded 37.32% revenue in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global UHT Milk Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Improvements in aseptic packaging extending shelf life | +1.8% | Global, with pronounced gains in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Shift to organized retail boosting ultra-high temperature availability | +1.5% | Asia-Pacific core, spillover to South America and Middle East and Africa | Medium term (2-4 years) |

| E-commerce and online retail expansions aiding distribution | +1.2% | North America and Europe lead, rapid adoption in Asia-Pacific urban centers | Short term (≤ 2 years) |

| Demand from working parents for ready-to-use nutritious products | +1.4% | Global, strongest in North America, Europe, and Asia-Pacific metropolitan areas | Long term (≥ 4 years) |

| Nutritional retention during high-temperature processing | +0.9% | Global, particularly relevant in Europe and North America where health claims drive premium positioning | Medium term (2-4 years) |

| Investments in dairy innovation for flavored ultra-high temperature variants | +1.1% | Asia-Pacific and North America, with emerging traction in South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Improvements in aseptic packaging extending shelf life

Aseptic carton technology offers extended ambient shelf stability without requiring refrigeration, enabling dairy processors to expand into regions with limited or cost-prohibitive cold-chain infrastructure. Tetra Pak has introduced fiber-based barrier coatings that reduce the thickness of aluminum foil while maintaining oxygen impermeability. This innovation lowers material costs and improves the recyclability of packaging. Dairy Farmers of America has invested significantly in upgrading several facilities with aseptic filling lines capable of processing large volumes of dairy products annually. This initiative targets export markets in regions such as Southeast Asia and West Africa, where high ambient temperatures challenge traditional dairy distribution methods. In India, this packaging advancement is particularly significant as the Food Safety and Standards Authority of India (FSSAI) requires ultra-high temperature milk to display production and best-before dates in regional languages. This regulation necessitates localized labeling by both multinational and cooperative dairy brands while maintaining product sterility. The combination of reduced packaging costs and improved distribution capabilities is enabling dairy companies to expand into tier-2 cities. These areas, where per-capita dairy consumption is lower than in metropolitan regions, are witnessing faster growth in consumption compared to the national average.

Shift to organized retail boosting ultra-high temperature availability

Modern trade channels, such as supermarkets and hypermarkets, have increased the shelf space dedicated to ultra-high temperature (UHT) milk across Asia-Pacific markets. This shift highlights retailers' recognition that ambient products, which do not require refrigeration, achieve higher inventory turnover compared to chilled alternatives. In 2024, Walmart added ultra-high temperature private-label milk to its Great Value portfolio, utilizing vertical integration with dairy cooperatives to offer lower prices than branded competitors while maintaining strong gross margins. In Brazil, the penetration of organized retail has grown significantly, benefiting ultra-high temperature milk as chains like Carrefour and Pão de Açúcar focus on shelf-stable assortments to reduce spoilage losses. A similar trend is observed in Middle Eastern markets, where Almarai leads Saudi Arabian supermarket dairy aisles with ultra-high temperature formats that cater to consumer preferences for bulk purchasing and extended storage. The focus of organized retail on traceability and quality assurance is raising standards for unbranded and loose milk vendors. This development is driving the shift toward packaged ultra-high temperature products, which include batch codes and nutritional labeling, addressing consumer demand for quality and safety.

E-commerce and online retail expansions aiding distribution

Direct-to-consumer dairy platforms are transforming the distribution of dairy products by removing intermediary markups and ensuring the prompt delivery of ultra-high temperature (UHT) milk shortly after order placement. This model appeals particularly to urban professionals who prioritize convenience and high-quality products. In India, companies such as Country Delight and Mother Dairy have built a substantial subscription customer base by offering ultra-high temperature and pasteurized milk through mobile applications that enable real-time tracking from farm to doorstep. Similarly, Amazon Fresh has expanded its ultra-high temperature milk offerings in North American and European markets by collaborating with regional dairies to meet same-day delivery demands in urban areas. In China, this direct-to-consumer approach has had a significant impact, with e-commerce platforms like Alibaba's Tmall and JD.com playing a key role in the packaged dairy market. These platforms allow major dairy brands such as Mengniu and Yili to bypass traditional wholesale networks, resulting in higher profit margins. Additionally, the rapid expansion of e-commerce is increasing the availability of premium and fortified ultra-high temperature milk variants. Previously limited to specialty retail outlets, these higher-priced formulations are now reaching a broader audience more effectively through online channels.

Demand from working parents for ready-to-use nutritious products

Dual-income households, which make up a significant percentage of families with children under 12 years old in North America and Europe, are increasingly choosing shelf-stable dairy products that do not require refrigeration. These products provide convenience, especially during school commutes or outdoor activities. Ultra-high temperature (UHT) milk, available in single-serve 200-milliliter cartons and pouches, is gaining popularity in the lunchbox segment. Parents value the portion control and ambient stability these products offer, considering them more practical than bulk packaging. Nestlé has introduced a fortified UHT milk line tailored for children aged 3 to 10. This product is enriched with vitamin D3, calcium, and docosahexaenoic acid (DHA) and is positioned as a beverage supporting cognitive development rather than a standard commodity drink. In the Asia-Pacific region, where nuclear families are increasingly replacing multigenerational households, working mothers are driving the majority of UHT milk purchases, according to a survey by the International Dairy Federation. This trend is further supported by the rising participation of women in the labor force, particularly in countries like India and China. The growing demand for products that simplify meal preparation while ensuring nutritional adequacy highlights the changing needs and priorities of these households.

Restraint Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer preference for fresh, pasteurized milk's flavor | -1.3% | North America and Western Europe, moderate impact in Asia-Pacific | Long term (≥ 4 years) |

| Lactose intolerance driving shifts away from dairy ultra-high temperature | -0.8% | Global, with pronounced effects in Asia-Pacific and parts of Europe | Medium term (2-4 years) |

| High initial costs for sterilization equipment and aseptic technology | -0.7% | Emerging markets in South America, Middle East, and Africa | Short term (≤ 2 years) |

| Perceptions of nutrient degradation from ultra-high heat | -0.6% | North America and Europe, diminishing as scientific evidence accumulates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer preference for fresh, pasteurized milk's flavor

Taste perception remains a notable challenge in North America and Western Europe, where blind taste tests consistently reveal that consumers detect subtle caramelized notes in ultra-high temperature (UHT) milk. These notes are a result of Maillard reactions occurring during thermal processing. A sensory study by Cornell University found that most participants in the United States preferred the flavor profile of pasteurized milk over UHT milk, citing a "cooked" aftertaste as the primary drawback. This preference is particularly pronounced in regions with advanced cold-chain infrastructure, where fresh milk is delivered promptly after processing and often sold at premium prices, signaling higher quality to consumers. In contrast, markets such as Germany and Spain show higher acceptance of UHT milk, with penetration rates exceeding 80%. This indicates that taste aversion to UHT milk is influenced by cultural factors rather than being universal. Dairy processors are working to address this issue by optimizing thermal processing methods to minimize flavor deviations. For example, FrieslandCampina has implemented direct steam injection systems, which reduce heating time to just a few seconds. This method helps preserve the organoleptic properties of fresh milk while ensuring sterility. The challenge is further intensified by premium fresh milk brands that promote cold-pressed or minimally processed variants, often priced significantly higher. These products reinforce the perception that ultra-high temperature processing compromises milk quality.

Lactose intolerance driving shifts away from dairy ultra-high temperature

Lactose malabsorption affects a significant portion of the global population, with particularly high prevalence in East Asian, South Asian, and African populations. This widespread condition poses considerable challenges for the dairy industry, including the ultra-high temperature (UHT) milk category. In response to this, plant-based milk alternatives such as oat, almond, and soy milk have been gaining popularity, especially in regions like North America and Europe. These alternatives are increasingly preferred by consumers who might otherwise opt for UHT dairy products, offering a viable solution for those seeking lactose-free options. Companies like Oatly and Califia Farms have introduced ultra-high temperature plant-based milk in aseptic cartons, providing similar shelf stability and convenience as traditional UHT dairy products. These offerings cater specifically to the needs of lactose-intolerant and vegan consumers. To address this shift, the dairy industry has also developed lactose-free ultra-high temperature milk, with companies such as Lactalis and Danone investing in lactase enzyme treatments to expand this segment. However, the higher cost of lactose-free variants compared to standard UHT milk remains a barrier to adoption, particularly among price-sensitive consumers in emerging markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fat Content: Health Trends Accelerate Skimmed Adoption

Skimmed ultra-high temperature (UHT) milk is projected to grow at a compound annual growth rate (CAGR) of 9.54% between 2026 and 2031, surpassing the growth of whole or full-cream variants, which accounted for a 42.12% market share in 2025. This trend is driven by consumers increasingly prioritizing protein intake while reducing saturated fat consumption. Semi-skimmed formulations, offering moderate fat content without compromising creaminess, appeal to households seeking a balanced option. These formulations are particularly popular in European markets, where regulatory definitions classify milk as skimmed (less than 0.5% fat), semi-skimmed (1.5% to 1.8% fat), or whole milk (minimum 3.5% fat).

Whole or full-cream ultra-high temperature milk continues to dominate in South Asia and Middle Eastern markets, where cultural preferences favor richer dairy products, and higher fat content is often associated with quality and nutritional value. The growing preference for skimmed variants is influenced by rising obesity rates and the prevalence of cardiovascular diseases. According to the World Health Organization, 39% of adults globally were overweight in 2025, prompting dietary shifts toward lower-calorie options [1]Source: World Health Organization, “Adult Obesity Statistics,” who.int. Additionally, fitness and wellness influencers are driving demand for high-protein, low-fat dairy products. Skimmed ultra-high temperature milk is increasingly positioned as a post-workout recovery beverage, offering 8 grams of protein per 250-milliliter serving with minimal fat content.

By Flavor: Functional Fortification Propels Flavored Growth

Flavored ultra-high temperature milk is projected to grow at a compound annual growth rate (CAGR) of 9.32% between 2026 and 2031. In contrast, unflavored variants accounted for 59.43% of revenue in 2025, highlighting a division between commodity dairy products and value-added functional beverages. Chocolate and strawberry remain the most popular flavors, while coffee-infused and matcha-blended ultra-high temperature milk are emerging as premium subcategories. These products are particularly gaining traction in Asia-Pacific and North America, where ready-to-drink coffee culture is well-established. For instance, Nestlé launched a cold-brew coffee ultra-high temperature milk in 2025, containing 120 milligrams of caffeine per 330-milliliter serving, positioning it as a breakfast alternative to traditional coffee beverages.

Flavored ultra-high temperature milk is also being utilized as a medium for functional fortification, with brands incorporating probiotics, omega-3 fatty acids, and plant sterols to address health concerns such as digestive health, cardiovascular wellness, and immune support. Meanwhile, unflavored ultra-high temperature milk continues to dominate household consumption due to its versatility in cooking, baking, and beverage preparation. It is also widely used in institutional channels, including food service and hotel, restaurant, and catering (HoReCa) segments, where neutral flavor profiles are essential for culinary applications.

By Packaging Format: Pouches Gain Ground on Sustainability and Cost

Flexible pouches are projected to grow at a compound annual growth rate (CAGR) of 10.34% between 2026 and 2031, making them the fastest-growing packaging format. In comparison, cartons accounted for 76.74% of the market share in 2025, reflecting a steady shift toward lightweight, cost-effective, and environmentally sustainable alternatives. Pouches use 60% less packaging material compared to rigid cartons, which helps reduce transportation costs and carbon emissions. This makes them an attractive option for sustainability-focused consumers and corporate procurement teams working to lower Scope 3 emissions.

In 2025, Amul launched a 500-milliliter ultra-high temperature (UHT) milk pouch priced 10% lower than comparable carton formats, encouraging adoption in cost-sensitive rural and semi-urban markets across India. Pouches also provide flexibility in portion sizes, with single-serve 200-milliliter and family-size 1-liter formats catering to the diverse needs of households. Cartons continue to be the preferred choice for premium and export-oriented UHT milk due to their superior barrier properties, stacking strength, and ability to enhance brand differentiation through high-quality printing. Tetra Pak's aseptic cartons with fiber-based barriers are gaining traction among brands aiming to improve recyclability, with 85% of carton material now derived from renewable sources.

By Distribution Channel: Food Service Rebounds as Institutional Demand Recovers

The food service and hotel, restaurant, and catering (HoReCa) channels are expected to grow at a compound annual growth rate (CAGR) of 9.74% between 2026 and 2031, recovering from disruptions caused by the pandemic. In 2025, retail accounted for 77.66% of sales, showcasing the market's resilience and diversification across supermarkets, hypermarkets, convenience stores, and online platforms. Institutional buyers, including schools, hospitals, and corporate cafeterias, are resuming bulk procurement of ultra-high temperature (UHT) milk as operations normalize, with average order sizes exceeding 500 liters per transaction.

Coffee chains such as Starbucks and Costa Coffee are piloting ultra-high temperature (UHT) milk in markets where cold-chain infrastructure is unreliable. This strategy helps reduce spoilage losses and supports menu standardization across various regions. The food service channel is also benefiting from the rise of cloud kitchens and delivery-only restaurants, which prioritize shelf-stable ingredients to minimize inventory risks and refrigeration costs.

Geography Analysis

In 2025, North America accounted for 37.32% of the global ultra-high temperature (UHT) milk revenue, making it the leading segment. This dominance was driven by consumer preferences for shelf-stable products in the United States and Canada. Despite the widespread availability of refrigeration infrastructure in these countries, ambient products are valued for emergency preparedness and extended pantry storage. The Food and Drug Administration regulates UHT milk under the same nutritional labeling and safety standards as pasteurized milk, simplifying market entry for both domestic and imported brands [2]Source: United States Food & Drug Administration, “Milk Guidance Documents & Regulatory Information,” fda.gov. Mexico is emerging as a growth area within the region, supported by increasing organized retail penetration and rising per-capita dairy consumption, which aligns with the expansion of the middle class.

The Asia-Pacific region is projected to grow at a compound annual growth rate (CAGR) of 9.82% between 2026 and 2031, making it the fastest-growing segment globally. This growth is primarily driven by gaps in cold-chain infrastructure in countries such as India, Indonesia, and rural China, making UHT milk a practical alternative to chilled dairy products. In India, the Food Safety and Standards Authority enforces stringent quality controls for UHT milk, including microbial testing and shelf-life validation, which has bolstered consumer trust in packaged dairy [3]Source: Food Safety and Standards Authority of India, “UHT Quality Controls,” fssai.gov.in. In China, dairy modernization efforts are leading to capacity expansions by companies like Mengniu and Yili, which collectively invested USD 2.3 billion in 2024 and 2025 to establish aseptic processing facilities aimed at meeting domestic demand without relying on imported milk powder. Meanwhile, Japan and Australia represent mature markets in the region, where UHT milk is positioned as a premium convenience product rather than a necessity, resulting in stable rather than growing consumption levels.

Europe leads in per-capita UHT milk consumption globally, with Germany, France, Spain, Belgium, and the Netherlands collectively accounting for the majority of the region's volume in 2025. This reflects decades of consumer familiarity with ambient dairy products. The European Food Safety Authority's harmonized standards for UHT processing and labeling facilitate cross-border trade, enabling companies like Arla and Lactalis to operate pan-European supply chains. Sustainability is a key focus in the region, with European consumers prioritizing recyclable packaging and carbon-neutral production. This has prompted dairy processors to invest in renewable energy and circular economy initiatives.

Competitive Landscape

The ultra-high temperature (UHT) milk market shows moderate concentration, with a score of 5 out of 10, indicating a competitive environment. The market includes multinational corporations such as Nestlé, Lactalis, and Danone, alongside regional cooperatives like Amul and Fonterra, as well as private-label brands catering to cost-sensitive consumers. Key strategic trends highlight a focus on efficiency-driven scale operations and differentiation through functional fortification, sustainability initiatives, and direct-to-consumer channels.

Multinational companies are increasingly investing in plant-based ultra-high temperature milk blends to meet the growing demand from lactose-intolerant and vegan consumers. Similarly, Asian market leaders such as Mengniu and Yili are concentrating on expanding domestic production capacity to serve China's population, thereby reducing reliance on imported milk powder. Opportunities are also expanding in the flavored and fortified ultra-high temperature milk segment, where brands can achieve 20% to 30% price premiums over standard variants by appealing to health-conscious millennials and Generation Z consumers.

Smaller players, including Country Delight and Mother Dairy in India, are disrupting the market by adopting direct-to-consumer subscription models. This strategy bypasses traditional wholesale networks, compressing margins for established brands. Furthermore, technological advancements are playing a significant role, with processors utilizing methods such as direct steam injection and indirect heating systems to minimize thermal degradation and preserve the sensory qualities of fresh milk. These innovations aim to address taste-related challenges in regions such as North America and Western Europe.

UHT Milk Industry Leaders

Nestlé S.A.

Groupe Lactalis SA

Royal FrieslandCampina N.V.

Danone SA

Fonterra Co-operative Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Malo Dairy, a subsidiary of Sill Enterprises, introduced UHT milk in a sustainable Pure-Pak carton developed by Elopak. This product launch aligns with the company's sustainability strategy.

- March 2025: Arla Foods has inaugurated a new UHT milk production facility in the United Kingdom, with an investment of USD 124.72 million. Located in Scotland, the facility produces both lactose-free and regular UHT milk.

- January 2025: PT Ultrajaya Milk Industry & Trading (Ultra Milk) launched Indonesia's organic UHT milk, certified Organik Indonesia. Sourced from 100% organic cow's milk at certified farms, this innovation elevates the company up the value chain in the dairy sector.

Global UHT Milk Market Report Scope

UHT milk is produced by heating milk at ultra-high temperatures for a specific or extended duration. The global UHT milk market is categorized based on fat content, flavor, packaging format, distribution channel, and geography. By fat content, the market is divided into Whole/Full-Cream, Semi-Skimmed, and Skimmed Milk. By flavor, it is segmented into Unflavored and Flavored. Based on packaging format, the categories include Cartons, Bottles, Pouches, and Others. Regarding distribution channels, the market is classified into Food Service/HoReCa and Retail, with the Retail segment further subdivided into Supermarkets/Hypermarkets, Convenience Stores, Online Retail, and Others. Geographically, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD and volume in liters for all the abovementioned segments.

By Fat Content

| Whole/Full-cream |

| Semi-skimmed |

| Skimmed |

By Flavor

| Unflavoured |

| Flavoured |

By Packaging Format

| Cartons |

| Bottles |

| Pouches |

| Others |

By Distribution Channel

| Food Service/HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Fat Content | Whole/Full-cream | |

| Semi-skimmed | ||

| Skimmed | ||

| By Flavor | Unflavoured | |

| Flavoured | ||

| By Packaging Format | Cartons | |

| Bottles | ||

| Pouches | ||

| Others | ||

| By Distribution Channel | Food Service/HoReCa | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of global ultra-high temperature milk sales by 2031?

The Ultra-high Temperature Milk market is forecast to reach USD 141.09 billion by 2031.

Which region is expected to post the fastest growth through 2031?

Asia-Pacific is projected to advance at a 9.82% CAGR, the quickest among all regions.

Which fat-content segment is expanding the most rapidly?

Skimmed ultra-high temperature milk is forecast to rise at a 9.54% CAGR between 2026-2031 as consumers seek low-fat, high-protein options.

What packaging format is gaining share on sustainability grounds?

Flexible pouches are set to grow at 10.34% CAGR, driven by 60% material savings and reduced transport emissions.

How are retailers influencing category growth?

Organized retail and online grocery platforms are enlarging shelf space and leveraging private-label strategies that widen consumer access and price competitiveness.

Page last updated on: