India Plant Based Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

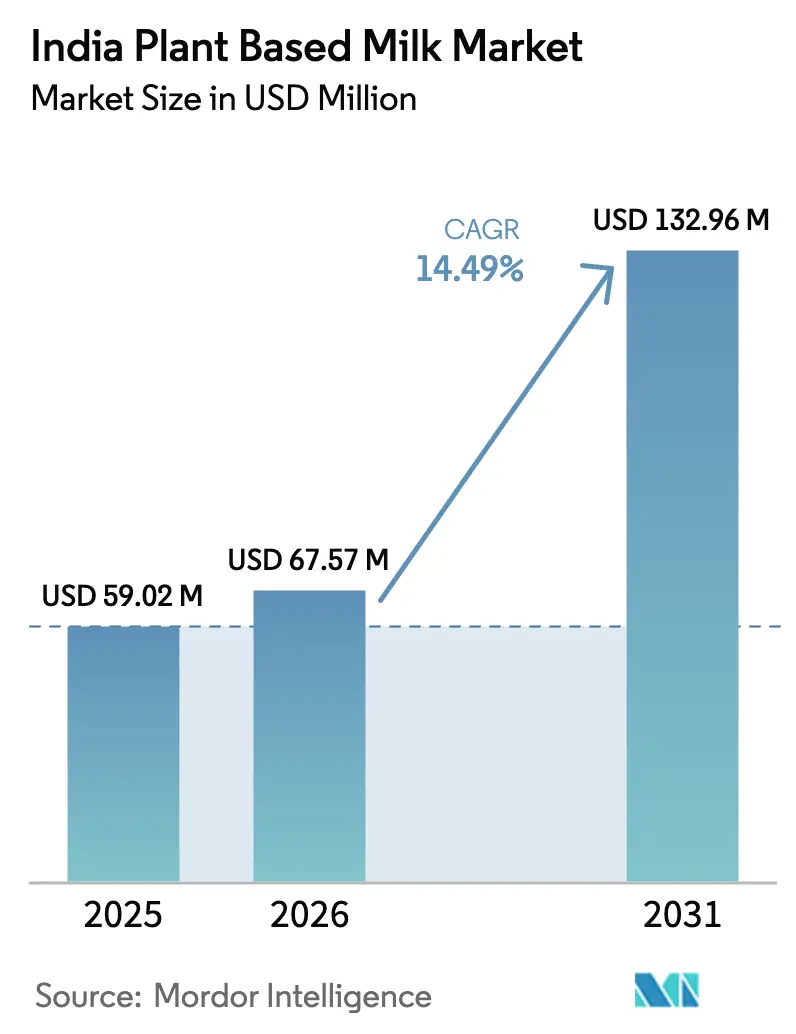

| Base Year Market Size (2025) | USD 59.02 Million |

| Market Size (2026) | USD 67.57 Million |

| Market Size (2031) | USD 132.96 Million |

| Growth Rate (2026 - 2031) | 14.49% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Plant Based Milk Market Analysis by Mordor Intelligence

The Indian plant-based milk market size is expected to grow from USD 59.02 million in 2025 to USD 67.57 million in 2026 and is forecast to reach USD 132.96 million by 2031 at 14.49% CAGR over 2026-2031. This growth is primarily attributed to several key factors. The increasing prevalence of lactose intolerance among the population has significantly boosted the demand for plant-based milk as a viable alternative to traditional dairy products. Additionally, the implementation of national vegan food regulations has created a favorable environment for the growth of the plant-based milk market, encouraging both manufacturers and consumers to explore plant-based options. Urban consumers are also playing a pivotal role in driving market expansion, as they increasingly adopt low-carbon diets to align with sustainable and environmentally conscious lifestyles. Besides, the rising awareness of the environmental impact of dairy production, coupled with the health benefits associated with plant-based milk, has further fueled its adoption.

Key Report Takeaways

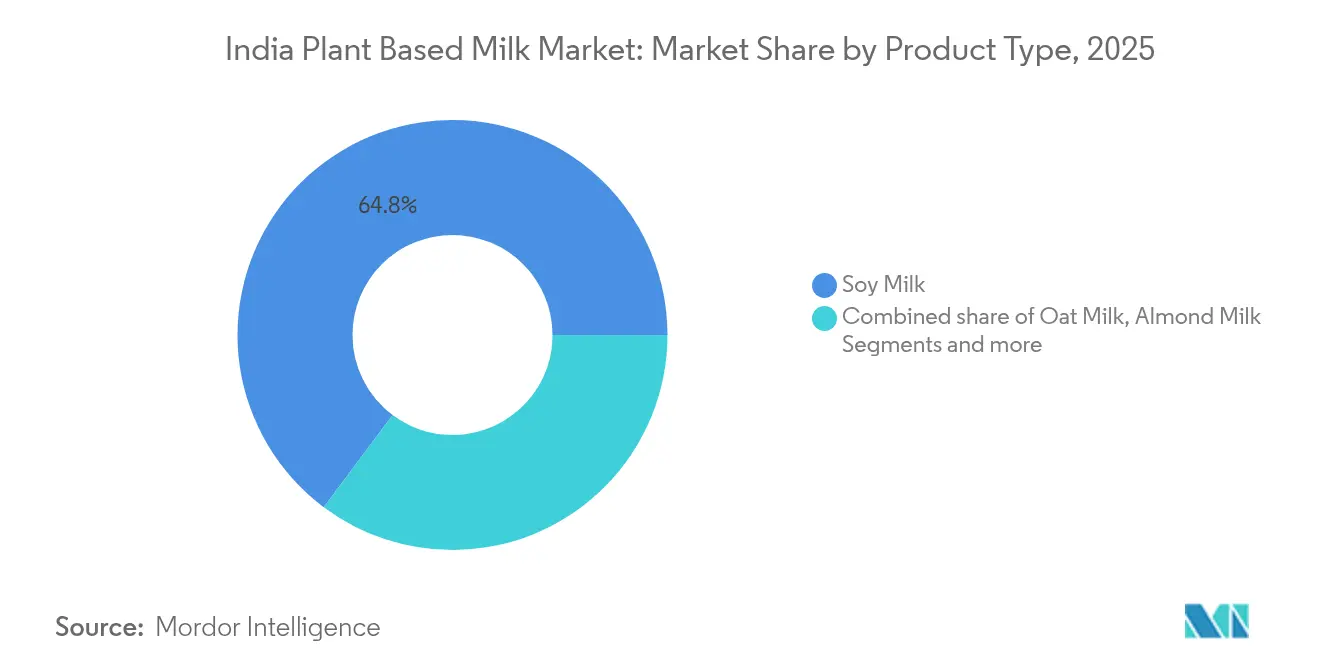

- By product type, soy milk led with 64.78% of India's plant-based milk market share in 2025, while hazelnut milk is projected to expand at a 19.05% CAGR to 2031.

- By distribution channel, off-trade outlets commanded 67.65% of the Indian plant-based milk market in 2025; on-trade is the fastest-growing route at 15.2% CAGR through 2031.

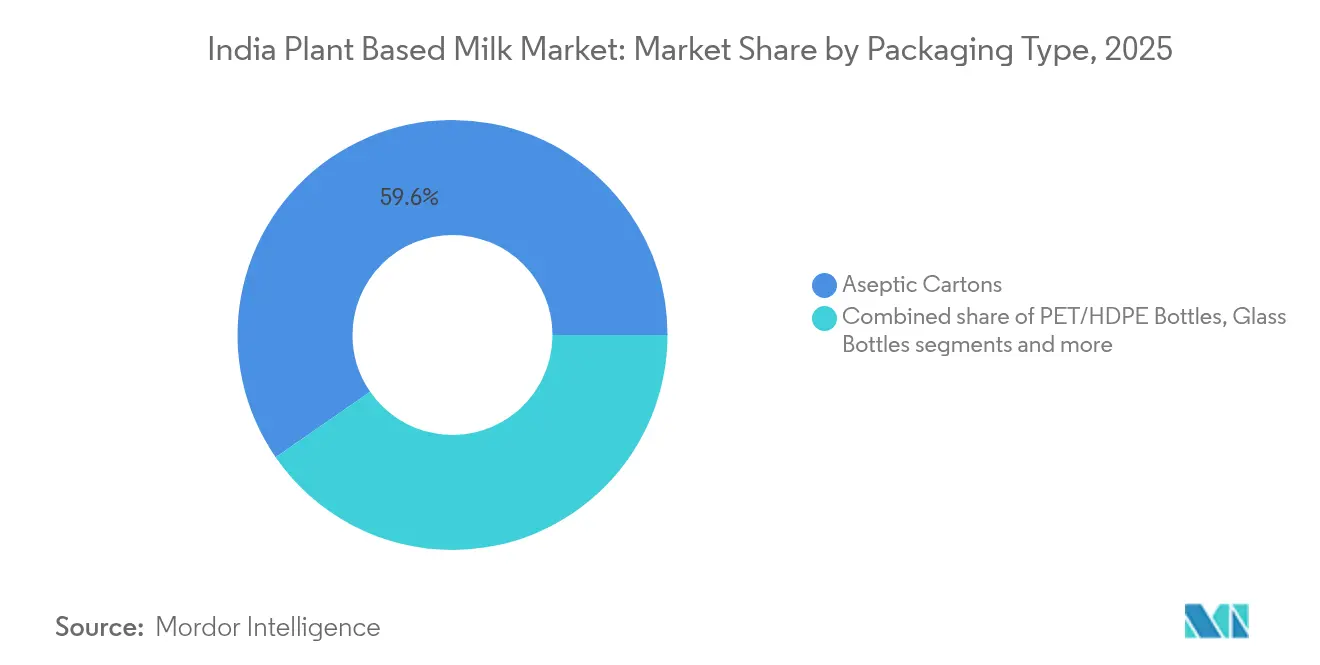

- By packaging, aseptic cartons captured 59.62% revenue share in 2025, whereas PET/HDPE bottles are advancing at 20.05% CAGR to 2031.

- By region, West India held 33.85% of the India plant-based milk market size in 2025, while South India records the highest 17.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on plant-based milk market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India Plant Based Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in lactose-intolerance diagnosis among urban consumers | +2.8% | South India core, spill-over to West and North India | Medium term (2-4 years) |

| Rapid scale-up of D2C and Q-commerce plant-based brands | +2.1% | Metro cities with expansion to Tier-2 urban centers | Short term (≤ 2 years) |

| Domestic almond cultivation expansion | +1.4% | North India production, National consumption benefits | Long term (≥ 4 years) |

| Government initiatives boost plant-based milk | +1.9% | National, with early gains in Maharashtra, Gujarat, Karnataka | Medium term (2-4 years) |

| Vegan options in corporate cafeterias of IT and BPO majors | +1.2% | Bangalore, Hyderabad, Pune, Chennai IT corridors | Short term (≤ 2 years) |

| Celebrity endorsements boosting category awareness | +0.8% | National, with stronger impact in urban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise in Lactose-Intolerance Diagnosis Among Urban Consumers

The increasing prevalence of lactose intolerance among urban consumers is a significant driver of the Indian plant-based milk market. According to the National Institutes of Health Report 2023, over 60% of the Indian population exhibits some degree of lactose intolerance [1]Source: National Institutes of Health, "Self‐reported food intolerances in an Indian population: Need for individualization rather than a universal low‐FODMAP diet", pmc.ncbi.nlm.nih.gov. This condition is more commonly diagnosed in urban areas due to better access to healthcare facilities and increased health awareness. Additionally, the National Family Health Survey (NFHS) highlights a growing trend of urban consumers seeking dairy alternatives to address dietary restrictions and health concerns. This shift is fueling the demand for plant-based milk products, which are perceived as healthier and more suitable for lactose-intolerant individuals. The rising awareness of lactose intolerance, coupled with government initiatives promoting nutritional alternatives, is expected to further drive the growth of the plant-based milk market in India during the forecast period.

Rapid Scale-up of D2C and Q-commerce Plant-based Brands

The rapid scale-up of direct-to-consumer (D2C) and quick-commerce (Q-commerce) channels is significantly driving the growth of the plant-based milk market in India. With increasing consumer demand for convenience and health-conscious alternatives, plant-based milk brands are leveraging these platforms to reach a broader audience efficiently. D2C channels allow brands to establish direct relationships with consumers, offering personalized experiences and fostering brand loyalty. For instance, brands like Goodmylk and Urban Platter have successfully utilized D2C platforms to promote their plant-based milk products, providing subscription models and exclusive offers to retain customers. Meanwhile, Q-commerce platforms such as Swiggy Instamart and Blinkit enable faster delivery, catering to the growing preference for instant access to products. This dual-channel approach is helping plant-based milk brands expand their market presence and meet the evolving needs of Indian consumers. Additionally, the integration of digital marketing strategies, such as targeted advertisements and influencer collaborations, further enhances the visibility and accessibility of plant-based milk products in India.

Domestic Almond Cultivation Expansion

The expansion of domestic almond cultivation is emerging as a significant driver in the Indian plant-based milk market. With the increasing demand for almond-based milk products, farmers are shifting focus toward almond farming to meet the growing needs of the industry. According to the Ministry of Agriculture and Farmers Welfare, the government has been promoting horticulture crops, including almonds, through various schemes such as the Mission for Integrated Development of Horticulture (MIDH). These initiatives aim to enhance almond production by providing financial assistance, technical support, and infrastructure development. Moreover, according to the United States Department of Agriculture, the production of almonds in India was 4,150 metric tons in 2024 [2]Source: United States Department of Agriculture, "Tree Nuts Annual - September 2024", apps.fas.usda.gov . The production generates higher demand for plant-based milk, accelerating market growth. The expansion of domestic almond cultivation decreases import dependency, stabilizes raw material costs, and facilitates the growth of the plant-based milk market in India.

Government Initiatives Boost Plant-Based Milk

The Indian plant-based milk market is witnessing significant growth, driven by various government initiatives aimed at promoting sustainable and healthier food alternatives. The government has been actively encouraging the adoption of plant-based diets as part of its broader efforts to address environmental concerns and improve public health. Policies such as subsidies for plant-based food production, awareness campaigns highlighting the benefits of plant-based diets, and support for research and development in the alternative protein sector are contributing to the expansion of the plant-based milk market. For instance, the Food Safety and Standards Authority of India (FSSAI) has been working on guidelines to regulate and promote plant-based food products, ensuring quality and safety standards [3]Source: Food Safety and Standards Authority of India, "Vegan Food", fssai.gov.in. The government’s focus on reducing greenhouse gas emissions and promoting sustainable agriculture aligns with the growth of plant-based milk, as it is considered an eco-friendly alternative to traditional dairy products. These initiatives are expected to further boost the market during the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Allergen-driven recalls of soy/nut-based milks | -1.6% | National, with higher impact in urban markets | Short term (≤ 2 years) |

| Limited cold-chain beyond metro cities | -2.3% | Rural and Tier-3 cities, affecting national expansion | Medium term (2-4 years) |

| FSSAI labeling rules on "milk" terminology for non-dairy | -1.1% | National regulatory compliance requirement | Long term (≥ 4 years) |

| Consumer perception and taste preferences | -1.8% | Traditional dairy-consuming regions, rural markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Allergen-Driven Recalls of Soy/Nut-based Milks

In the Indian plant-based milk market, allergen-driven recalls of soy and nut-based milks act as a significant market restraint. These recalls often occur due to the presence of undeclared allergens, such as soy proteins or nut traces, which pose serious health risks to consumers with allergies. For instance, in recent years, several soy milk brands in India faced recalls after failing to disclose allergen information on their packaging. Similarly, nut-based milk products, such as almond milk, have been withdrawn from the market due to cross-contamination during production processes. Such incidents not only lead to financial losses for manufacturers but also erode consumer trust, thereby hindering market growth. The lack of comprehensive allergen labeling regulations in India further compounds the problem. Unlike some developed markets, where allergen disclosure is mandatory and closely monitored, the Indian regulatory framework is still evolving. This regulatory gap creates inconsistencies in labeling practices, increasing the risk of allergen-related recalls.

Limited Cold-Chain Beyond Metro Cities

The limited availability of cold-chain infrastructure beyond metro cities poses a significant restraint in the Indian plant-based milk market. Cold-chain systems, which are essential for maintaining the quality and shelf life of plant-based milk products, are predominantly concentrated in urban areas. This lack of infrastructure in tier-2 and tier-3 cities, as well as rural regions, hampers the distribution and accessibility of these products. For instance, plant-based milk brands often struggle to expand their reach to smaller towns due to inadequate refrigerated storage and transportation facilities. This results in higher spoilage rates and increased operational costs, making it challenging for companies to maintain competitive pricing in these areas. Furthermore, the absence of a robust cold-chain network limits the ability of manufacturers to introduce a diverse range of plant-based milk products in non-metro markets, thereby restricting market growth. Addressing these cold-chain limitations is crucial for ensuring the widespread availability and affordability of plant-based milk across India.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Soy Milk Dominates While Hazelnut Milk Accelerate

In 2025, soy milk dominated the Indian plant-based milk market, capturing a significant 64.78% market share. This dominance is attributed to the well-established domestic crushing capacity, which ensures a steady supply of soy-based products. Additionally, soy milk's retail prices remain competitive with conventional dairy, making it an attractive option for cost-conscious consumers seeking plant-based alternatives. Its affordability and widespread availability have solidified its position as the leading segment in the market. Furthermore, soy milk is recognized for its high protein content and versatility, making it a preferred choice for consumers incorporating plant-based options into their diets. The segment benefits from its use in various applications, including beverages, cooking, and baking, further driving its widespread adoption.

Hazelnut milk, on the other hand, is projected to experience the fastest growth in the Indian plant-based milk market, with a remarkable 19.05% CAGR forecasted through 2031. This growth is fueled by increasing consumer preference for nut-based beverages, which are perceived as indulgent yet rich in protein. The premium positioning of hazelnut milk, combined with its nutritional benefits, appeals to health-conscious and affluent consumers. As awareness of plant-based diets continues to rise, hazelnut milk is expected to gain further traction in the market. Additionally, its unique flavor profile and association with premium and indulgent products make it a popular choice for consumers seeking variety in plant-based milk options.

By Distribution Channel: Off-Trade Channel Leads, On-Trade Channel Accelerates

In 2025, the off-trade channel accounted for a significant 67.65% share of India's plant-based milk market. This dominance can be attributed to the convenience and accessibility offered by supermarkets, hypermarkets, and online retail platforms, which are the primary distribution points in this channel. Consumers increasingly prefer purchasing plant-based milk through these outlets due to the availability of diverse product options, competitive pricing, and ease of comparison. The off-trade channel's established infrastructure and widespread reach have further solidified its position as the leading distribution channel in the market.

On the other hand, the on-trade channel is projected to grow at a faster CAGR of 15.2% during the forecast period from 2026 to 2031. This growth is driven by the rising adoption of plant-based milk in cafes, restaurants, and other food service establishments, where consumers are seeking healthier and sustainable alternatives. The increasing trend of plant-based diets and the growing awareness of lactose intolerance are encouraging food service providers to incorporate plant-based milk into their offerings. As a result, the on-trade channel is expected to witness robust growth, contributing significantly to the overall expansion of the market.

By Packaging Type: Innovation Addresses Preservation Challenges

In 2025, aseptic cartons dominated the Indian plant-based milk market, holding a significant 59.62% market share. These cartons are highly favored due to their ability to extend the shelf life of products without requiring refrigeration, a critical advantage in a country where cold-chain infrastructure remains unevenly distributed. The convenience and durability of aseptic cartons make them an ideal packaging solution for plant-based milk, ensuring product safety and quality over extended periods. This packaging format also aligns with the growing consumer preference for sustainable and efficient storage solutions, further solidifying its dominance in the market.

PET/HDPE bottles are projected to grow at a strong CAGR of 20.05% through 2031, driven by increasing demand for resealable packaging and the expansion of curbside recycling programs in major urban areas. These bottles offer enhanced convenience for consumers, particularly in terms of portability and ease of use. Additionally, the rising focus on sustainability and the growing adoption of recycling initiatives in large cities are contributing to the popularity of PET/HDPE bottles. Their ability to balance functionality with environmental considerations positions them as a key growth segment in the Indian plant-based milk market.

Geography Analysis

West India accounted for 33.85% of India's plant-based milk market share, driven by a concentration of affluent consumers, global culinary influences, and a robust refrigerated logistics network. Retailers in Mumbai and Pune have dedicated entire aisles to dairy alternatives, offering shoppers a range from family-sized one-litre cartons to barista blends. The cosmopolitan nature of these cities, bolstered by a significant expatriate presence, has lowered acceptance barriers, making them prime testing grounds for new product launches. Consequently, the product variety seen in West India often sets the tone for national trends, granting regional distributors an edge in negotiations for space in new shopping complexes.

South India is on track to lead the nation with a projected 17.65% CAGR from 2026 to 2031. This growth is fueled by a combination of prevalent lactose intolerance, deep-rooted vegetarian traditions, and a prominent tech-savvy workforce. In Bengaluru, the start-up scene drives word-of-mouth trends, with employees from major IT parks exchanging health tips and opting for weekly almond milk deliveries. This trend is mirrored in Hyderabad and Chennai, where celebrity endorsements further amplify the category's allure.

North India, with its diverse demographics and evolving consumer preferences, is witnessing a significant surge in the plant-based milk market. The region, traditionally known for its dairy consumption, is now embracing alternatives like almond, soy, and oat milk. This shift can be attributed to rising health consciousness, environmental concerns, and a growing vegan population. Urban centers like Delhi and Chandigarh are leading the charge, with numerous brands setting up shop and local players expanding their offerings. Moreover, the region's robust distribution network, coupled with increasing shelf space in retail outlets, is further propelling the market's growth.

Competitive Landscape

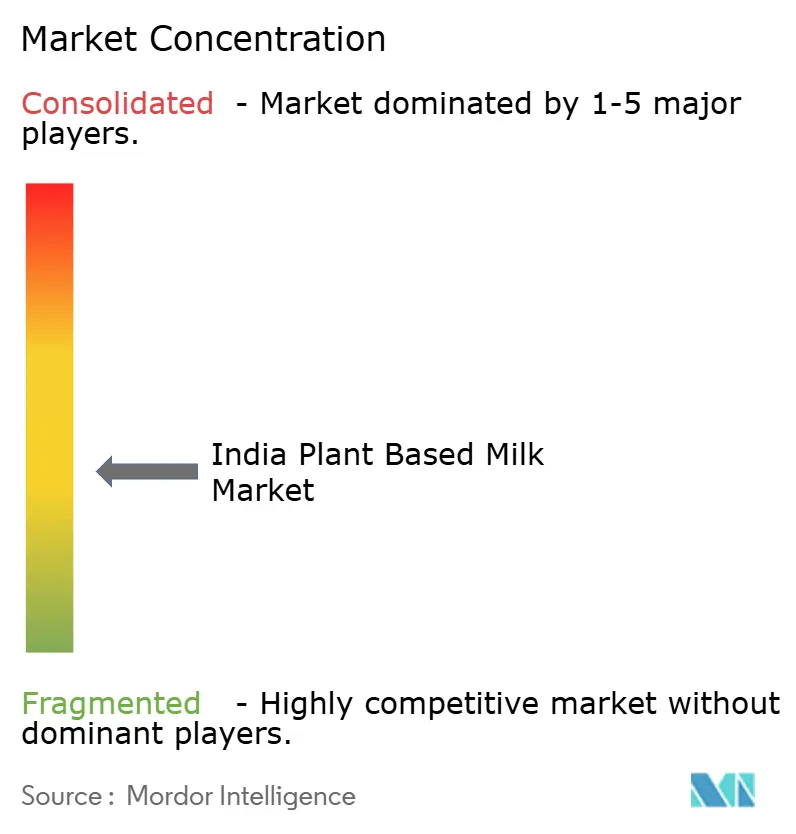

The Indian plant-based milk market is characterized by moderate fragmented competition. This competitive environment creates ample opportunities for both global giants and local innovators to establish and expand their market presence. Global players like Danone are actively re-entering the Indian market, showcasing their commitment through significant investments. For instance, in 2024, Danone allocated EUR 20 million to develop facilities in Punjab, signaling its intent to strengthen its foothold in the region.

Strategic initiatives are shaping the competitive dynamics of the market. Companies are increasingly adopting vertical integration strategies to gain better control over their supply chains, ensuring efficiency and cost-effectiveness. The development of direct-to-consumer (D2C) channels is another prominent trend, as it allows companies to optimize margins and build stronger relationships with their customer base. Additionally, partnerships with celebrities for endorsements are being utilized to enhance brand visibility and appeal to a broader audience. These strategies are enabling both global and domestic players to differentiate themselves in a competitive market and capture consumer attention effectively.

Technology adoption is playing a pivotal role in driving innovation within the Indian plant-based milk market. Companies are focusing on precision fermentation capabilities to develop high-quality, animal-free dairy alternatives. For example, Blue Diamond Growers is investing heavily in research and development initiatives to create innovative plant-based products that align with evolving consumer preferences. Such advancements not only enhance product offerings but also position companies as leaders in sustainability and innovation. As the market continues to grow, the integration of advanced technologies and strategic initiatives is expected to further intensify competition, fostering a dynamic and evolving landscape.

India Plant Based Milk Industry Leaders

-

Danone S.A.

-

Blue Diamond Growers

-

Dabur India Ltd.

-

The Hershey Company (Sofit)

-

Life Health Foods (So Good)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Indian dairy and grocery brand Country Delight entered the plant-based beverage market with a new milk alternative. The product, named Oat Beverage, utilized Australian oats and contained no chemical additives, preservatives, or added sugars. The beverage was free from soy and nuts, and was manufactured in an allergen-controlled facility to minimize cross-contamination risks.

- September 2024: Oxbow Brands launched Vegan Drink Company (VDC) to address the increasing demand for dairy-free alternatives among lactose-intolerant consumers and vegan lifestyle adopters. VDC manufactures plant-based milk beverages made from millets, nuts, fruits, and grains, providing consumers multiple alternatives to traditional dairy products for their daily consumption.

- December 2023: Life Health Foods (India) Pvt. Ltd., a leader in the plant-based beverage market, introduced its latest offering: the So Good Oat Caramel beverage. This dairy-free, plant-based milk embodies the brand's commitment to delivering a healthy and versatile drink.

India Plant Based Milk Market Report Scope

Plant-based milk, derived from sources like nuts, grains, and legumes, is crafted by blending these ingredients with water. To closely resemble the texture and nutritional profile of cow's milk, manufacturers often incorporate additional elements such as vitamins, minerals, and stabilizers.

The Indian plant-based milk market is segmented by product type, distribution channel, packaging, and region. By product type, the market is segmented into almond milk, soy milk, oat milk, coconut milk, rice milk, cashew milk, hazelnut milk, pea-protein milk, and multi-nut blends. By distribution channel, the market is segmented into off-trade and on-trade. The off-trade segment is further classified into supermarkets/hypermarkets, convenience stores, specialist retailers, online retail stores, and other off-trade channels. By packaging, the market is segmented into aseptic cartons, PET/HDPE bottles, glass bottles, Tetra Pak bricks, and others. By region, the market is segmented into North India, West India, South India, East India, Central India, and North-East India. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Almond Milk |

| Soy Milk |

| Oat Milk |

| Coconut Milk |

| Rice Milk |

| Cashew Milk |

| Hazelnut Milk |

| Pea-protein Milk |

| Multi-nut Blends |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialist Retailers | |

| Online Retail Stores | |

| Other Off-Trade Channels | |

| On-Trade (HoReCa) |

| Aseptic Cartons |

| PET/HDPE Bottles |

| Glass Bottles |

| Tetra Pak Bricks |

| Others (Pouch, Bag-in-Box) |

| North India |

| West India |

| South India |

| East India |

| Central India |

| North-East India |

| By Product Type | Almond Milk | |

| Soy Milk | ||

| Oat Milk | ||

| Coconut Milk | ||

| Rice Milk | ||

| Cashew Milk | ||

| Hazelnut Milk | ||

| Pea-protein Milk | ||

| Multi-nut Blends | ||

| By Distribution Channel | Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Specialist Retailers | ||

| Online Retail Stores | ||

| Other Off-Trade Channels | ||

| On-Trade (HoReCa) | ||

| By Packaging Type | Aseptic Cartons | |

| PET/HDPE Bottles | ||

| Glass Bottles | ||

| Tetra Pak Bricks | ||

| Others (Pouch, Bag-in-Box) | ||

| By Region (India) | North India | |

| West India | ||

| South India | ||

| East India | ||

| Central India | ||

| North-East India | ||

Key Questions Answered in the Report

How large is the India plant-based milk market in 2026?

It is valued at USD 67.57 million, with projections indicating a move to USD 132.96 million by 2031.

What packaging format is gaining traction?

PET/HDPE bottles are the fastest climber, registering 20.05% CAGR as single-serve convenience gains favor.

Which product type leads sales?

Soy milk remains dominant, accounting for 64.78% of India plant-based milk market share in 2025.

Which region is expanding the fastest?

South India is growing at 17.65% CAGR, driven by higher lactose intolerance and a strong technology-sector workforce.

Page last updated on: