Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 49.02 Billion |

| Market Size (2031) | USD 61.77 Billion |

| Growth Rate (2026 - 2031) | 4.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carpets and Rugs Market Analysis by Mordor Intelligence

The Carpets and Rugs Market size was valued at USD 46.81 billion in 2025 and estimated to grow from USD 49.02 billion in 2026 to reach USD 61.77 billion by 2031, at a CAGR of 4.73% during the forecast period (2026-2031).

Expansion continues despite rising competition from hard-surface flooring, driven by resilient residential spending, accelerating e-commerce adoption, and sustained commercial refurbishment activity. Rapid urbanization in Asia-Pacific, a pronounced shift toward sustainable materials, and premiumization in mature economies are steering product innovation and new-capacity investments. Vertically integrated players are leveraging in-house yarn production and omnichannel distribution to shield margins from volatile petroleum costs, while smaller brands focus on niche aesthetics and direct-to-consumer models. Government regulations that reward circular design and extend producer responsibility are simultaneously raising compliance costs and spurring innovation, nudging the carpets and rugs market toward low-carbon manufacturing and closed-loop recycling strategies.

Key Report Takeaways

- By type, tufted products led with 67.62% of carpets and rugs market share in 2025; knotted carpets post the fastest 5.28% CAGR to 2031.

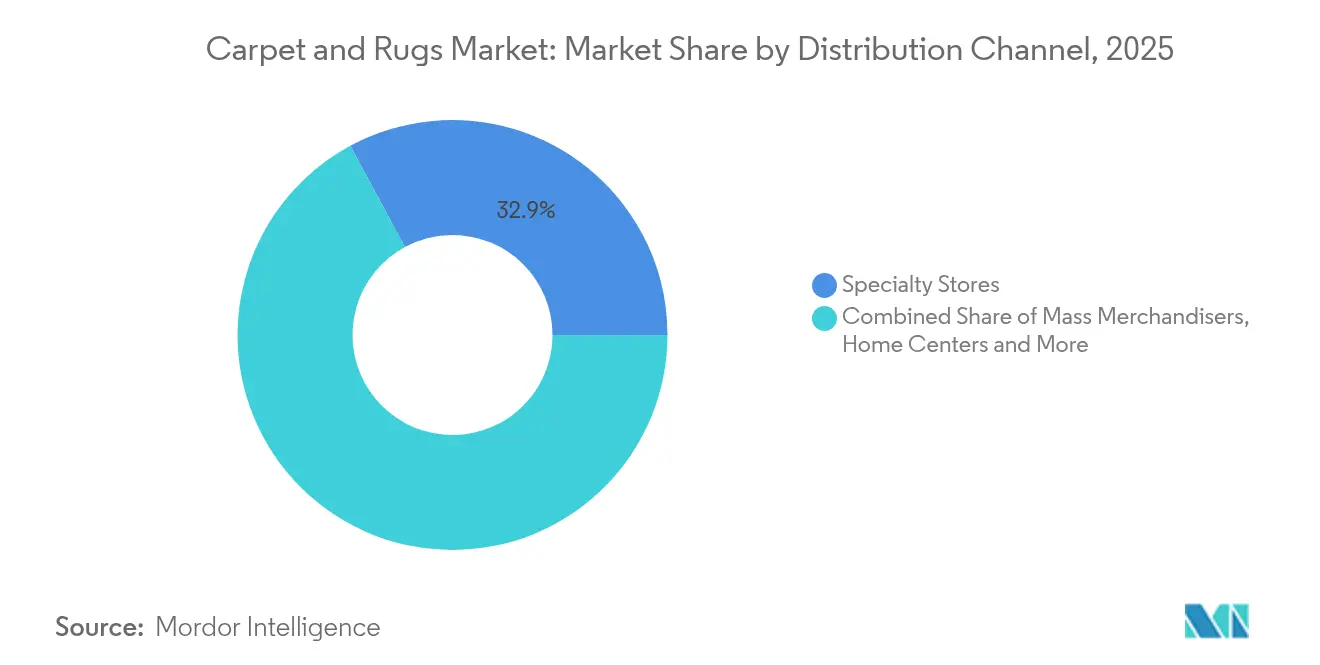

- By distribution channel, specialty stores held 32.88% revenue share in 2025, while online retailers expanded at a 7.48% CAGR through 2031 in the Carpets and Rugs Market.

- By end-use industry, the residential segment captured 66.92% of the carpets and rugs market size in 2025 and continues to grow at 5.73% CAGR.

- By geography, North America commanded a 31.55% share in 2025, whereas Asia-Pacific is projected to advance at an 7.06% CAGR to 2031 in the Carpets and Rugs Market.

- Mohawk Industries, Shaw Industries Group, Oriental Weavers Carpet Co., Interface, and Beaulieu International Group are among the leading company that collectively holds a significant market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Carpets and Rugs Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Rising Demand for Home Decor and Interior Design | +1.2% | Global, with emphasis on North America and Europe | Medium term |

| Growing Demand for Sustainability and Eco-Friendly Products in Home Decor | +0.9% | North America, Europe, Urban APAC | Long term |

| Expansion of Online Retail Channels | +0.7% | Global, with higher impact in developed markets | Short term |

| Presence of Government Initiatives and Trade Policies | +0.4% | India, Middle East, Europe | Medium term |

| Growth in Hospitality and Commercial Sectors | +0.6% | Global, with emphasis on APAC and Middle East | Medium term |

| Source: Mordor Intelligence | |||

Rising Demand for Home Decor and Interior Design

Home spaces have become lifestyle showpieces. Consumers increasingly treat carpets as focal décor elements, catalyzing demand for bold colors, digital prints, and bespoke motifs. The residential segment’s 5.87% CAGR underscores the shift, while suppliers ramp up on-demand manufacturing to deliver short-run premium styles without ballooning inventory.

Growing Demand for Sustainability and Eco-Friendly Products in Home Decor

Environmental scrutiny now extends from fiber source to end-of-life disposition. Brands deploying recycled PET or bio-based yarns, lower-emission dyeing, and transparent supply-chain disclosures enjoy pricing power among younger buyers. Interface, through its Carbon Neutral Floors program, supplies cradle-to-gate carbon-neutral carpet tiles, turning compliance into brand equity.

Expansion of Online Retail Channels

Digital migration remains relentless as visualization apps let buyers project rug patterns onto real rooms. E-commerce outpaces legacy showrooms due to seamless sampling, free returns, and direct shipping. Pure-play platforms and omnichannel majors are reshaping margins and customer acquisition, forcing specialty retailers to reinvent store formats around experiential design consultations.

Presence of Government Initiatives and Trade Policies

Export incentives in India and tariff relaxations in parts of the Middle East facilitate market entry for regionally produced hand-knotted brands, whereas shifting trade levies between major economies compel supply-chain recalibration. Forward-looking manufacturers diversify sourcing and near-shore finishing to hedge against regulatory volatility.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR | Geographic Relevance | Peak Impact |

|---|---|---|---|

| LVT and SPC Cannibalization in Retail and Education Fit-outs | -1.1% | North America, Europe | Short term |

| Crude-Oil Price Spikes Inflating PP and Nylon Feedstock Costs | -0.7% | Global | Medium term |

| EU Extended-Producer-Responsibility Fees Elevate End-of-Life Cost | -0.5% | European Union | Long term |

| Skilled-Artisan Attrition Threatening Hand-Knotted Supply Chains (India, Iran) | -0.3% | South Asia, Middle East | Long term |

| Source: Mordor Intelligence | |||

LVT and SPC Cannibalization in Retail and Education Fit-outs

Luxury vinyl tile and stone plastic composite floors combine aesthetics with low lifetime cost, eroding carpet’s position in high-traffic commercial corridors. As photo-realistic embossing mimics timber and marble, facility managers opt for resilient hard surfaces, limiting carpet specifications to acoustic zones and lounge spaces.

Crude-Oil Price Spikes Inflating PP and Nylon Feedstock Costs

Upstream volatility squeezes margins because 85% of carpet fiber tonnage remains petroleum-derived. Integrated giants such as Mohawk Industries counterbalance input shocks via captive yarn capacity, but smaller converters face working-capital strain, prompting alliances for recycled polymer sourcing and biobased R&D partnerships.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tufted Scale, Knotted Prestige

Tufted offerings accounted for 67.62% of carpets and rugs market share in 2025, underscoring their cost-efficiency and rapid production cycles. Continuous upgrades in multi-needle machinery now permit intricate loop-pile graphics, sustaining relevance in commercial refurbishment programs. Woven constructions occupy the durability mid-tier, appealing to hospitality lobbies that require dimensional stability. Although small in volume, the hand-knotted niche is climbing at 5.28% CAGR as affluent buyers seek heirloom craftsmanship. Knotted rugs’ limited supply raises average selling prices, yet artisan attrition in India and Iran threatens pipeline continuity. Producers are adopting vocational upskilling incentives and hybrid wool-silk blends to broaden design palettes while safeguarding heritage techniques. Tufted segment commanded 67.62% share of the carpet market size in 2025, whereas knotted carpets delivered the sharpest value expansion pace.

Across all varieties, manufacturers embed recycled PET and solution-dyed nylon to cut dye-house emissions. Digital printing now bridges the aesthetic gap between tufted and woven, thereby democratizing high-definition imagery for mid-price SKUs. These converging innovations sustain the carpets and rugs market’s product ladder from value to ultra-luxury.

By Distribution Channel: Physical Expertise vs Digital Scale

Specialty stores retained 32.88% revenue share in 2025 through consultative selling and installation services that simplify complex fiber, pad, and seaming choices for homeowners. However, online retailers are scaling at a 7.48% CAGR, leveraging algorithmic merchandising and rapid sampling to win convenience seekers. The result is a blended journey where shoppers research designs online and finalize selections in store or vice versa.

Mass merchandisers use national reach to push value bundles, whereas home-center chains bundle carpet with renovation materials to capture project spend. Direct-to-consumer upstarts ship vacuum-packed rugs and promote machine-washable covers, disrupting install norms. Traditional dealers respond with showroom VR stations and white-glove take-back programs that embed sustainability into service contracts. The channel equation now pivots on last-mile agility and post-purchase maintenance assurance.

By End-Use Industry: Residential Momentum

Residential applications captured 66.92% of the carpets and rugs market share in 2025 and expanded fastest at 5.73% CAGR. Post-pandemic living spaces double as offices, gyms, and classrooms, reviving interest in soft flooring that dampens sound and offers thermal comfort. Solution-dyed polyester resists stains, supporting family rooms and pet zones, while waterproof backings unlock kitchen and basement usage. Meanwhile, modular carpet tiles populate flexible home workstations, mirroring commercial trends.

Commercial demand remains diverse. Offices favor tackless squares for selective replacement as occupancy patterns evolve. Hotels specify custom motifs that echo brand narratives, with underlays engineered for footfall and trolley durability. Healthcare facilities deploy low-VOC, antimicrobial carpets to temper noise in patient corridors. Industrial sites adopt needle-punched mats with electrostatic dissipation or chemical resistance, a small but margin-accretive slice. Across settings, facility managers increasingly demand Environmental Product Declarations to document cradle-to-grave impacts, embedding sustainability KPIs into procurement scoring.

Geography Analysis

North America held 31.55% of the carpets and rugs market share in 2025, supported by high per-capita consumption and a robust residential replacement cycle. Cooler climates favor carpet for insulation, and remodeling incentives sustain sales amid mature housing stock. Premiumization prevails as consumers trade up to patterned loop-cut-loop styles and recycled-content nylon. Canada tracks similar trends, especially in new condo builds, while Mexico’s housing stimulus and expanding middle class fuel incremental volume growth.

Asia-Pacific represents the fastest trajectory, expanding at 7.06% CAGR through 2031. Urban migration and rising disposable incomes in China, India, Indonesia, and Vietnam elevate demand for mid-range carpets in apartments and mixed-use complexes. China remains the consumption giant, whereas India stands out for export-oriented hand-knotted and tufted plants in Rajasthan and Uttar Pradesh. Developers in Australia and South Korea integrate eco-labels into specification tendering, further amplifying sustainable product demand. Asia-Pacific’s share of the carpets and rugs market size is expected to surpass one-quarter by 2031, underscoring its role as the growth engine.

Europe commands significant value through stringent eco-design regulations that push the industry toward circularity. The EU’s Extended Producer Responsibility framework assigns disposal fees to manufacturers, accelerating R&D in recyclable backing systems. Nordic markets reward cradle-to-cradle certification with price premiums, while Germany and the United Kingdom dominate regional volume behind robust refurbishment programs. South America shows emerging momentum, mainly in Brazil and Chile, where hospitality construction is scaling. The Middle East and Africa cater to luxury hospitality and palatial residential projects; the United Arab Emirates and Saudi Arabia import custom wool-silk blends for high-profile developments, sustaining the premium tier of the carpets and rugs market.

Competitive Landscape

Innovation and Sustainability Drive Future Success

Success in the carpet industry increasingly depends on companies' ability to align with evolving consumer preferences and sustainability requirements. Market leaders are investing heavily in sustainable manufacturing processes, recycled materials, and eco-friendly product lines to maintain their competitive edge. Companies are also focusing on developing smart carpet technologies, enhanced durability features, and innovative design capabilities to differentiate their offerings. The ability to provide customized solutions, efficient installation services, and comprehensive after-sales support has become crucial for maintaining market share in both residential and commercial segments.

Future market success will require companies to effectively address the growing threat from alternative flooring solutions while adapting to changing regulatory landscapes regarding environmental impact and product safety. Emerging players can gain ground by focusing on niche market segments, developing innovative product features, and establishing strong regional distribution networks. The increasing importance of online sales channels and digital marketing strategies presents both opportunities and challenges for market participants. Companies must also consider the concentration of buying power among large commercial customers and the growing influence of interior designers and architects in product specification decisions.

Carpets and Rugs Industry Leaders

Mohawk Industries Inc.

Shaw Industries Group, Inc.

Oriental Weavers Carpet Co.

Interface, Inc.

Beaulieu International Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Oriental Weavers launched a polyester yarn dyeing unit in 10th of Ramadan City to reinforce internal yarn capacity.

- March 2025: Interface earmarked USD 45 million to boost modular carpet tile output at its Georgia plant, adding equipment designed for 100% recycled nylon.

- February 2024: Shaw Floors unveiled six Pet Perfect+ styles featuring LifeGuard Spill-Proof technology for pet-oriented households.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the carpet and rugs market as sales revenue generated from newly manufactured tufted, woven, knotted, needle-punched, and other textile floor coverings that are installed in residential, commercial, institutional, and industrial interiors. It follows the value chain from yarn conversion through finished, factory-bound products reaching first buyers.

Scope exclusion: After-sales services such as installation fees, cleaning contracts, and used-product resale lie outside the boundary.

Segmentation Overview

- By Product Type

- Tufted

- Woven

- Needle-Punched

- Knotted

- Others (Loop, Shag, Braided, etc.)

- By Distribution Channel

- Mass Merchandisers

- Home Centers

- Specialty Stores

- Other Channels (Manufacturer Retailers, Warehouse Clubs, Discount, Omnichannel)

- By End-Use

- Residential

- Commercial Offices

- Hospitality and Leisure

- Retail and Shopping Centres

- Healthcare Facilities

- Institutional (Education & Government)

- Industrial Manufacturing Plants

- Warehouses and Logistics Hubs

- Cleanrooms and Controlled Environments

- Other Industrial Facilities

- Industrial

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with plant managers in the U.S., distributors in Germany, home-center buyers in India, and design consultants across the Gulf. Their feedback validated utilization rates, retailer mark-ups, and upcoming sustainability-driven product launches that were only hinted at in documents.

Desk Research

We began with publicly available datasets such as the U.S. Census Bureau's monthly new-housing starts, Eurostat building-permit statistics, UN Comtrade HS-570249 trade flows, and the World Bank's urban population indicators. Industry bodies, including the Carpet and Rug Institute and the European Carpet & Rug Association, offered production ratios and fiber mix insights that sharpened material split assumptions. Company 10-Ks, investor decks, and reputable press articles then helped us trace average selling price (ASP) movements and channel shifts. D&B Hoovers supported revenue breakouts for leading manufacturers. This list is illustrative; many other sources were consulted for cross-checks and context.

Market-Sizing & Forecasting

A top-down model converts floor-area completions, average room carpeting ratios, and import-export balances into unit demand, which is then priced using weighted ASPs. Target totals are corroborated through selective bottom-up supplier roll-ups and channel checks before adjustments. Key variables like nylon and polypropylene fiber prices, per-capita renovation spend, and residential mortgage rate trends drive both the historical fit and the five-year outlook. Multivariate regression projects each driver, while scenario analysis captures potential policy shifts on recycled content. Gaps in bottom-up estimates are bridged by proportional allocation to under-reported regions using trade proxy data.

Data Validation & Update Cycle

Outputs pass anomaly flags, peer review, and senior sign-off. We refresh the model annually, and we reopen it sooner if raw-material shocks or construction slowdowns exceed preset thresholds. Before any client delivery, an analyst reruns the latest data sweep so users receive the freshest view.

Why Our Carpet And Rugs Baseline Commands Reliability

Published values often diverge because publishers apply different product mixes, inflation conversions, and refresh cadences.

Key gap drivers include whether rugs sold through décor boutiques are counted, how aggressively ASP escalators compound, and the frequency with which forecasts are realigned to housing starts. Mordor's disciplined scope, annual refresh, and dual-track validation keep our figure grounded, while some peers lean on broad assumptions or infrequent updates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 52.46 B (2025) | Mordor Intelligence | |

| USD 60.06 B (2025) | Global Consultancy A | Includes installation revenue and uses five-year static ASP ladder |

| USD 64.19 B (2025) | Regional Consultancy B | Counts luxury custom rugs, applies aggressive construction boom scenario |

| USD 53.80 B (2025) | Industry Research C | Excludes low-end tufted imports, updates every three years |

In sum, Mordor's approach blends transparent sourcing with repeatable calculations, giving decision-makers a balanced starting point that they can confidently trace and stress-test.

Key Questions Answered in the Report

What is the current market value of the carpets and rugs market?

The carpets and rugs market size is valued at USD 49.02 billion in 2026 and is forecast to reach USD 61.77 billion by 2031.

Which region is growing fastest in the carpets and rugs market?

Asia-Pacific is the growth engine, projected to expand at an 7.06% CAGR to 2031 as urbanization and rising incomes lift demand.

Who are the leading companies in the carpets and rugs market?

Mohawk Industries, Shaw Industries Group, Oriental Weavers Carpet Co., Interface, and Beaulieu International Group collectively hold the largest revenue share.

Which carpet type shows the highest growth rate?

Hand-knotted carpets advance fastest at 5.28% CAGR, driven by luxury consumer demand for artisanal craftsmanship.

How is sustainability influencing carpet purchasing decisions?

Buyers increasingly favor products made with recycled or bio-based fibers and seek verification of low carbon footprints, lifting demand for offerings such as Interface’s Carbon Neutral Floors.

Page last updated on: