Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

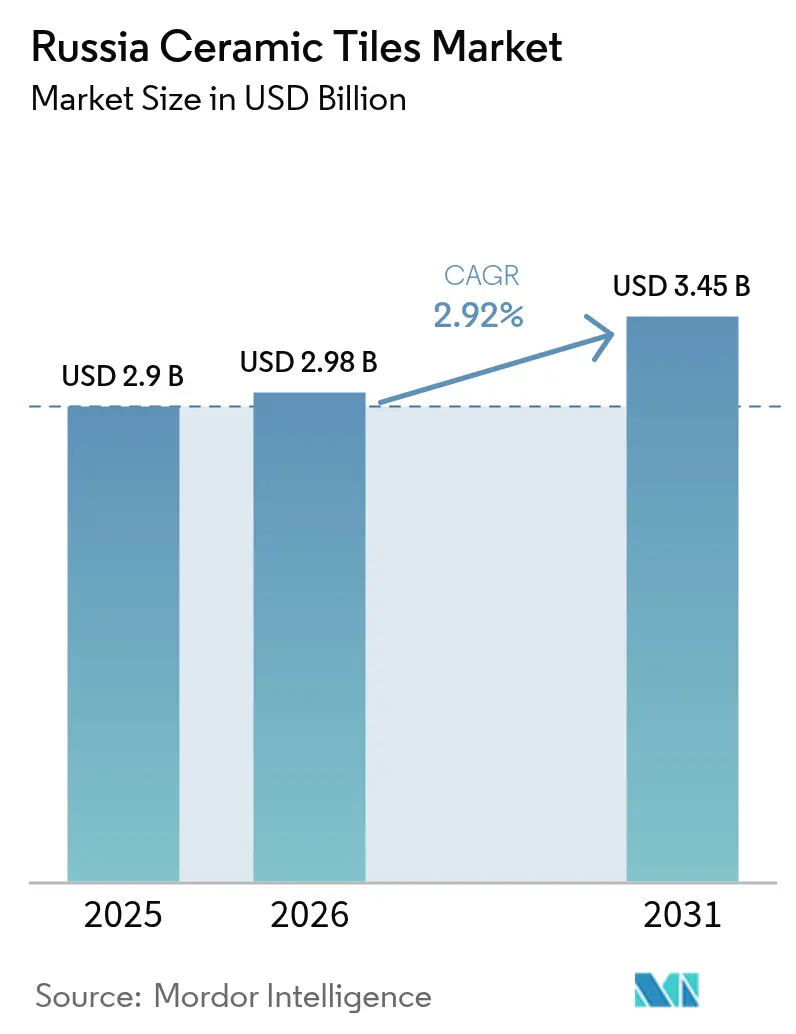

| Base Year Market Size (2025) | USD 2.90 Billion |

| Market Size (2026) | USD 2.98 Billion |

| Market Size (2031) | USD 3.45 Billion |

| Growth Rate (2026 - 2031) | 2.92% CAGR |

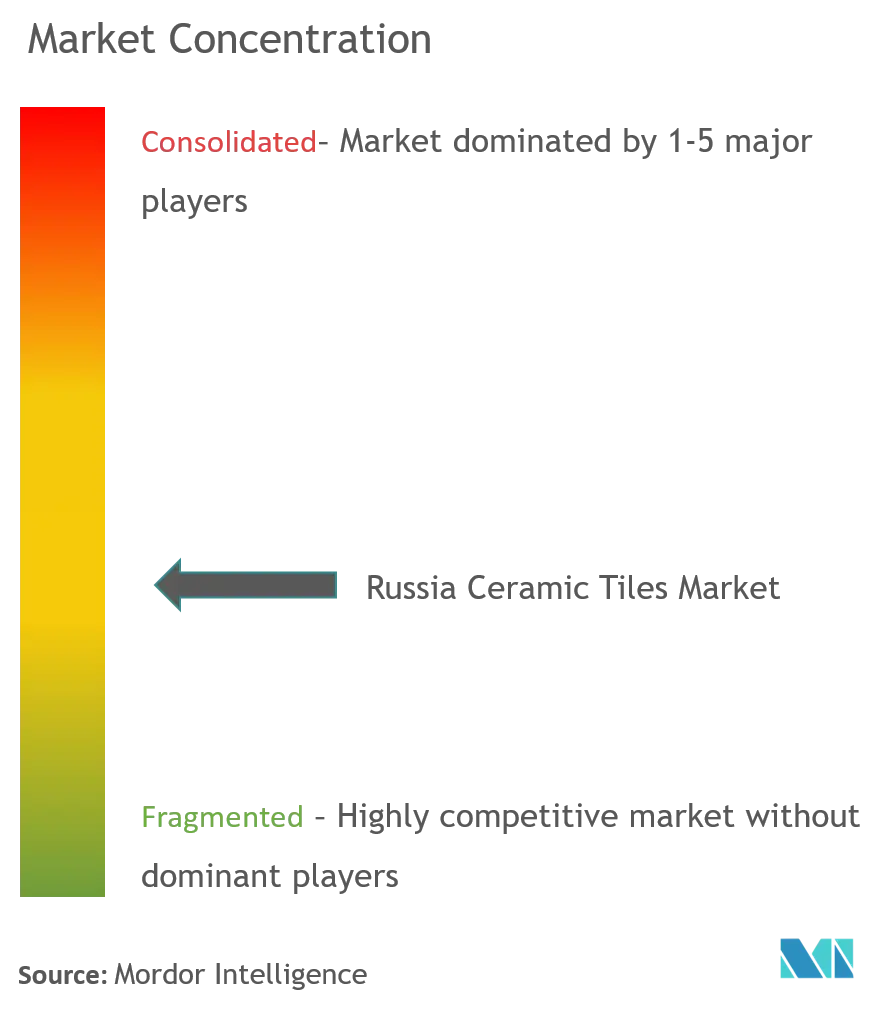

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Ceramic Tiles Market Analysis by Mordor Intelligence

The Russia ceramic tiles market size in 2026 is estimated at USD 2.98 billion, growing from 2025 value of USD 2.90 billion with 2031 projections showing USD 3.45 billion, growing at 2.92% CAGR over 2026-2031. The market’s resilience rests on government‐led import substitution, energy-efficient housing incentives, and mortgage subsidies that keep renovation spending high despite currency swings. Builders prefer porcelain for its durability, and digital printing now lets domestic firms deliver premium designs that rival imports. Price inflation, driven by a weaker ruble and rising energy tariffs, is partially absorbed because government housing programs sustain demand. Integrated producers with local raw-material sources hold a cost edge, while online retail and premium DIY formats are widening consumer access to advanced tile options.

Key Report Takeaways

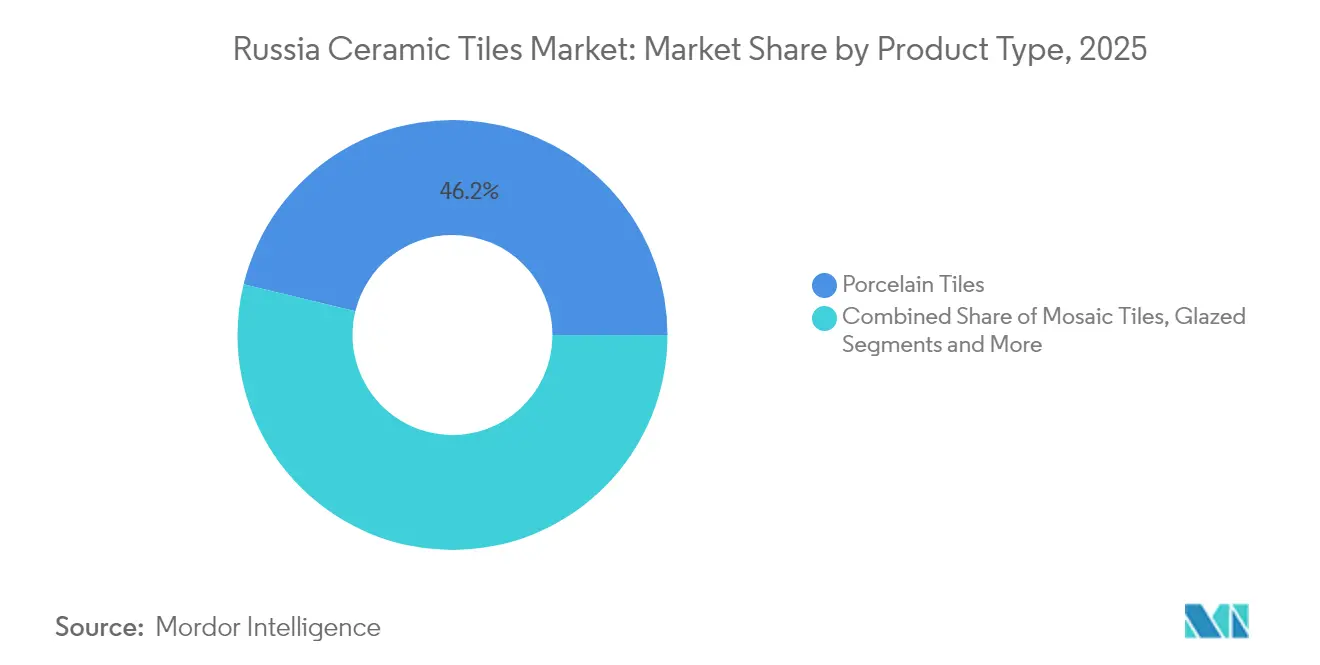

- By product type, porcelain tiles led with 46.20% of the Russia ceramic tiles market share in 2025, while mosaic tiles are projected to grow at a 3.65% CAGR through 2031.

- By application, floor installations captured 71.10% of the Russia ceramic tiles market size in 2025, and wall applications are advancing at a 3.95% CAGR to 2031.

- By end-user, residential demand accounted for 55.70% of the Russia ceramic tiles market size in 2025, yet commercial demand shows the fastest growth at 5.18% CAGR.

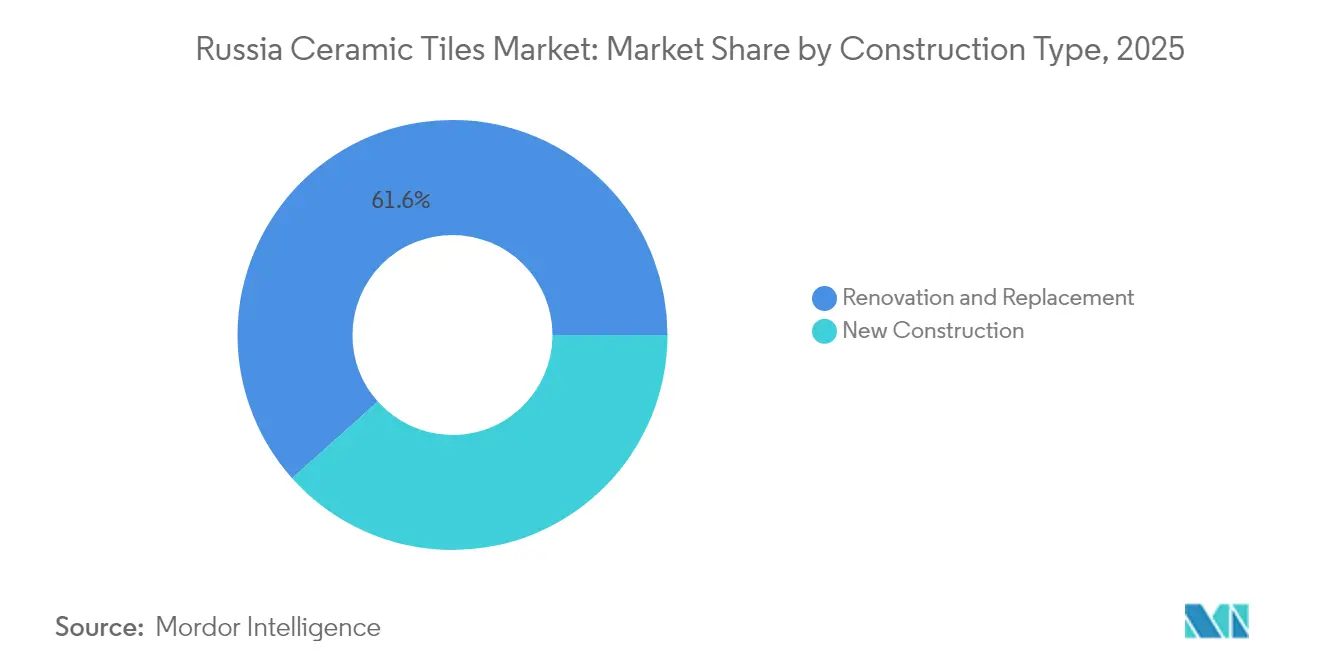

- By construction type, renovation held 61.60% share of the Russia ceramic tiles market size in 2025; new construction is set to expand at a 4.30% CAGR.

- By distribution channel, specialty tile stores commanded 37.60% revenue in 2025, whereas online retail is forecast to post a 5.55% CAGR.

- By geography, the Central Federal District dominated at 31.10% share in 2025; the Southern Federal District exhibits the highest 4.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficient multifamily housing stimulus (2025–2028) | +0.8% | Central Federal District, Northwestern Federal District | Medium term (2-4 years) |

| National mortgage-subsidy extension boosts renovation demand | +0.6% | National, with concentration in Central and Southern Federal Districts | Short term (≤ 2 years) |

| Import-substitution policy for porcelain tile raw materials | +0.5% | Volga Federal District, Ural regions | Long term (≥ 4 years) |

| Growth of premium DIY retail chains into Tier-2 cities | +0.4% | Southern Federal District, Northwestern Federal District | Medium term (2-4 years) |

| Construction of >30 new transport hubs through 2030 | +0.3% | National, with focus on Central and Southern Federal Districts | Long term (≥ 4 years) |

| Industrial park expansion in Volga & Ural districts | +0.2% | Volga Federal District, Ural regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficient Multifamily Housing Stimulus Drives Ceramic Demand

The federal program running from 2025 to 2028 offers incentives to developers who achieve higher energy-efficiency benchmarks in new multifamily buildings. To meet these standards, architects select dense porcelain tiles that enhance thermal regulation and extend façade durability. Demand is strongest in the colder Central and Northwestern districts, where lower heating loads translate into tangible operating savings. The multi-year pipeline gives domestic tile factories confidence to invest in capacity upgrades and R&D focused on high-efficiency products. Because certification scoring now includes tile performance, suppliers that deliver compliant materials gain a clear advantage in public tenders

National Mortgage Subsidy Extension Fuels Renovation Market

The subsidy prolongation cuts interest costs for homeowners, lifting spending on kitchen and bathroom upgrades. Banks report a surge in home-improvement loans earmarked for tile purchases, especially across Central and Southern districts where homeownership rates are high. Renovation budgets increasingly favor porcelain for its lifecycle savings despite a 19% price uptick in 2025. Mortgage‐supported demand cushions producers from currency volatility and underpins the Russia ceramic tiles market even as new-build activity softens[1]Source: “Russian Housing Reform and Renovation Statistics,” RBC Realty, rbc.ru. Mortgage subsidy programs are particularly effective in Central and Southern Federal Districts, where homeownership rates are highest and renovation activities generate substantial ceramic tile demand. Financial institutions are developing specialized lending products for home improvement projects, creating accessible financing options that support the ceramic tile market growth.

Import Substitution Policy Strengthens Domestic Raw-Material Supply

Incentives for kaolin and feldspar mining have cut foreign dependency, stabilizing cost structures for Volga and Ural factories. Integrated supply chains allow price quotes in rubles, shielding margins from exchange-rate swings. Joint ventures between miners and tile makers accelerate quality upgrades that now match European benchmarks, positioning local brands for premium segments[2]Source: “Energy Efficient Residential Construction Programs,” E3S Web of Conferences, e3s-conferences.org. Ceramic manufacturers are partnering with domestic raw material suppliers to build integrated supply chains that improve efficiency and simplify logistics. Government-backed upgrades to mining infrastructure are improving raw material quality and availability, enabling domestic ceramic producers to meet product specifications comparable to international standards.

Premium DIY Retail Expansion Transforms Distribution Landscape

New big-box DIY chains entering Tier-2 cities such as Rostov-on-Don and Kaliningrad showcase wide ceramic assortments alongside augmented-reality design kiosks, educating consumers on advanced options. Their floor displays demonstrate large-format slabs and mosaic sheets, helping shoppers visualize complete room concepts without relying on specialist showrooms. Omnichannel models let buyers order online and collect in store, overcoming delivery hurdles for heavy, fragile goods while broadening geographic reach. The scale of these outlets pressures traditional tile boutiques to upgrade service levels and curate more distinctive collections to stay competitive. Manufacturers benefit from the chains’ nationwide logistics networks, which enable higher throughputs and more predictable inventory turns, reinforcing demand for domestically made premium tiles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ruble volatility inflates raw-material costs | -0.4% | National, with higher impact in regions dependent on imported materials | Short term (≤ 2 years) |

| Energy-tariff hikes raise kiln-operating expenses | -0.3% | National, with concentration in energy-intensive manufacturing regions | Medium term (2-4 years) |

| Shrinking skilled-labor pool for tile-laying trade | -0.2% | National, with acute shortages in major metropolitan areas | Long term (≥ 4 years) |

| Tightened silica-dust regulations for factories | -0.1% | National, affecting all manufacturing facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ruble Volatility Creates Raw-Material Cost Pressures

A weaker ruble lifts prices for imported glazes and additives still not produced locally. Tile manufacturers hedge currency risk yet must adjust price lists quarterly to protect margins. The 19% average tile price rise in 2025 strains consumer budgets, although subsidies soften the impact[3]Source: “Currency Fluctuation Impact on Building Materials,” RBC Realty, rbc.ru. This forces manufacturers to balance price increases with competitiveness in a price-sensitive market. Import substitution efforts are reducing exposure to currency fluctuations, but the transition timeline extends beyond immediate market needs, maintaining vulnerability to exchange rate movements. Regional manufacturers with higher import dependence face greater cost pressures than integrated producers with domestic supply chains, creating competitive disparities across the market. Currency volatility forces manufacturers to factor exchange-rate risk into pricing, capital expenditures, and working capital.

Energy Tariff Increases Challenge Manufacturing Economics

Gas and electricity tariffs climbed 12% in 2025, raising kiln firing costs. Plants with older tunnel kilns suffer most and now plan retrofits to high-efficiency models. Some producers test methanol firing to cut energy intensity, but payback periods stretch beyond three years. Government energy policies affecting industrial users create uncertainty in long-term cost planning, complicating investment decisions for capacity expansion and equipment upgrades. Ceramic manufacturers are investing in energy management systems and production optimization technologies to reduce consumption per unit of output, but implementation timelines extend beyond immediate cost pressures. The energy challenge is driving consolidation pressures as smaller manufacturers struggle to absorb cost increases while maintaining competitive pricing in the ceramic tiles market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Dominance Faces Mosaic Innovation

Porcelain tiles held 46.20% of the Russia ceramic tiles market share in 2025 and remain the benchmark for durability. Mosaic tiles post the fastest 3.65% CAGR as architects seek accent walls and custom patterns. Porcelain’s leadership stems from scratch resistance and low water absorption, vital for Russia’s freeze-thaw cycles. Domestic giants invested in presses exceeding 15,000 tons to manufacture slabs up to 120 cm, narrowing the technology gap with imports. Glazed ceramics keep mid-market loyalty where buyers trade a slight performance loss for cost savings. Unglazed lines cater to factories and transport hubs requiring slip control. Decorative and handmade tiles appeal to niche consumers willing to pay for artisanal flair, although volumes stay small.

The product type segmentation reflects broader market maturation, with porcelain tiles increasingly becoming the standard for new construction projects requiring long-term performance guarantees. Manufacturing investments in large-format capabilities are enabling domestic producers to compete with international suppliers in premium segments, reducing import dependence while maintaining quality standards. Mosaic tile growth is supported by architectural trends emphasizing feature walls and accent applications that showcase design creativity. Glazed ceramic tiles face pressure from porcelain alternatives but maintain relevance in cost-sensitive applications where performance requirements are less demanding. Unglazed options continue serving specialized industrial applications where surface treatments would compromise functional performance.

By Application: Floor Dominance Challenged by Wall Growth

Floor installations accounted for 71.10% of the Russia ceramic tiles market size in 2025, reflecting the material’s strength under heavy loads. Wall applications grow 3.95% annually as large-format panels create seamless vertical surfaces in living rooms and lobbies. In bathrooms, channel drains and wall-mounted fixtures drive continuous floor-to-wall layouts that boost tile volumes per unit. Roofing remains a specialty niche in heritage projects needing frost-resistant ceramics. Architects specify thin 6 mm porcelain on facades for weight reduction, blending wall and exterior demand and nudging the application mix toward higher value.

The shift pushes manufacturers to perfect rectified edges and lighter substrates for easier vertical handling. Wall-focused collections now include coordinating trims, speeding installation, and raising average selling prices. Builders appreciate the hygienic benefits of grout-free 1.2 m panels, enhancing appeal in hospitals and food halls. The application mix is shifting toward higher-value segments where ceramic tiles command premium pricing through superior performance or aesthetic qualities. Commercial applications are driving demand for specialized products that meet specific performance standards for safety, durability, and maintenance efficiency. Consumer education about ceramic tile advantages in various applications is expanding market penetration beyond traditional use cases.

By Construction Type: Renovation Resilience Supports Market Stability

Renovation projects dominated with 61.60% share in 2025 since Russia’s housing stock averages 32 years of age. Homeowners prioritize bathroom refreshes where leak prevention and aesthetics overlap. Mortgage subsidies let them finance higher-priced porcelain, sustaining volumes despite price inflation. New construction, though smaller, climbs 4.30% annually as energy-efficient multifamily starts gain momentum in satellite cities. Builders specify porcelain as the default finish, embedding long-run demand into every new unit. The construction type mix reflects broader housing market dynamics, with renovation activities providing market stability while new construction drives growth momentum. Renovation projects typically involve higher-value ceramic tile specifications as consumers upgrade from basic finishes to premium options that enhance property value.

Renovation trends focus on waterproof systems and underfloor heating compatibility. Tile suppliers bundle leveling compounds and membranes, capturing more wallet share. In new builds, standardized 60x60 cm formats speed installation and reduce waste, controlling project budgets. New construction enables standardized product specifications that support efficient manufacturing and installation processes. Government policies affecting construction financing and building standards influence both segments, with energy efficiency requirements driving demand for high-performance ceramic tile products. The balance between renovation and new construction activities provides market stability while creating opportunities for product differentiation across different application requirements.

By End-User: Commercial Momentum Accelerates

Residential use maintained a 55.70% share in 2025 owing to steady mortgage-backed renovation volumes. Commercial projects, however, expand 5.18% annually through 2031 as airports, malls, and logistics centers proliferate. Hospitality chains demand patterned mosaics and wood-look porcelains that endure rolling luggage. Healthcare facilities specify antimicrobial glazes to meet hygiene codes. Industrial parks install thick unglazed tiles that tolerate forklift pressure. Transport hubs order anti-slip finishes for passenger safety, reinforcing commercial pull on the Russia ceramic tiles market.

Developers value porcelain’s lower life-cycle cost compared with vinyl in high-traffic venues. Domestic producers answer with ranges meeting EN 14411 Group BIa water-absorption specs, enabling local sourcing without quality trade-off. The commercial swing encourages suppliers to add project management teams that coordinate delivery with critical construction milestones. Healthcare facilities require ceramic tiles that meet stringent hygiene standards while providing slip resistance and chemical compatibility. Educational applications balance cost considerations with durability requirements, creating demand for mid-market ceramic solutions that provide long-term value.

By Distribution Channel: Online Retail Disrupts Traditional Patterns

Specialty showrooms captured 37.60% of sales in 2025, leveraging design consultations and sample libraries. Online retail, however, rises 5.55% annually as freight networks refine last-mile delivery of bulky goods. Web stores offer AR visualization and AI-based calculators that estimate tile counts, attracting digital-native buyers to the Russia ceramic tiles market. DIY chains gain from weekend renovation culture, while contractor-direct sales keep traction in commercial segments where project logistics dictate purchasing. The distribution channel mix reflects changing consumer behavior and retail innovation that expands ceramic tile market accessibility. Online platforms are developing specialized tools for ceramic tile selection, including augmented reality applications that help consumers visualize products in their spaces.

Showrooms respond by adding click-and-collect and virtual appointments. Online platforms partner with installers to bundle service, tackling the skill shortage hurdle. Logistics providers invest in break-resistant packaging and route optimization to cut damage rates and costs. Contractor sales channels remain important for commercial applications, where professional relationships and project support services influence purchasing decisions. The distribution landscape is becoming more complex as manufacturers must support multiple channel strategies while maintaining consistent pricing and brand positioning. Consumer education about ceramic tile selection and installation is becoming a key competitive factor across all distribution channels.

Geography Analysis

The Central Federal District continues to generate the bulk of premium sales due to Moscow’s higher incomes and design-savvy homeowners. Developers refurbish Soviet-era stock into upscale apartments, specifying large-format porcelain that meets stringent fire and acoustic codes. Retailers in the capital curate imported-style collections made domestically, avoiding import duties while matching fashion trends. Northwestern Federal District maintains a steady market presence through St. Petersburg's urban development and regional construction activities. Volga Federal District benefits from industrial park expansion and import substitution policies that support domestic ceramic tile manufacturing.

Southern Federal District enjoys the fastest expansion pace as state investments overhaul airports in Rostov and mineral-rich Stavropol opens logistics zones. Hotels built for year-round tourism demand slip-resistant pool surrounds and salt-resistant exterior cladding, giving local producers volume and technical challenges that push product innovation. Other regions collectively represent emerging markets where economic development and infrastructure investments are creating new ceramic tile demand centers. The geographic distribution reflects broader economic development patterns and government investment priorities that influence regional construction activity levels.

Northwestern and Volga districts collectively account for more than one-third of national consumption. St. Petersburg’s heritage restorations use mosaics that replicate historic motifs, sustaining artisan workshops. Volga’s industrial boom amplifies B2B orders for technical ceramics that resist chemicals and abrasion. These dynamics highlight the regional mosaic that defines the Russia ceramic tiles market. Regional market dynamics are creating opportunities for manufacturers to develop location-specific distribution strategies and product offerings that address local preferences and requirements. The geographic segmentation influences logistics strategies, with manufacturers optimizing supply chain configurations to serve regional markets efficiently while maintaining competitive cost structures.

Competitive Landscape

The market shows moderate concentration. Kerama Marazzi, Unitile, and Italon together control more than half of organized sales, while Mohawk’s local unit broadens capacity through joint ventures. Integrated supply chains and domestic raw-material contracts protect margins from currency shocks. Firms pour capital into inkjet lines and automated sorting to match European quality at lower cost. In 2025 Kerama Marazzi launched its Morocco range with 60x119.5 cm slabs that target high-end wall applications, signaling a tech-driven arms race. Market competition intensifies around product innovation, with manufacturers investing in digital printing technologies and large-format capabilities to differentiate their offerings while maintaining cost competitiveness against imported alternatives.

Scale matters because tightened dust rules and energy hikes raise compliance cost. Smaller players lacking captive quarries face thinning margins, hinting at future consolidation. Distribution innovation is another battlefield. Italon opened hybrid studios where architects can book VR sessions, and Mohawk’s digital storefront lists real-time stock visibility, cutting lead times for B2B buyers[4]Source: Mohawk Industries Annual Report 2025, mohawkindustries.com. White-space opportunities exist in specialized segments such as large-format tiles, technical ceramics for industrial applications, and premium decorative products where consumer sophistication is driving demand for advanced features and aesthetic appeal.

Firms that excel at premium positioning and omnichannel engagement are poised to outgrow the Russia ceramic tiles market average. Large players also invest in training installers, easing labor bottlenecks while locking in brand loyalty among contractors. Emerging competitive dynamics reflect technology adoption patterns, with manufacturers investing in automated production systems and quality control technologies to address skilled labor shortages while improving product consistency and cost efficiency. Market disruption potential exists in distribution channels, where online retail growth and DIY market expansion are creating new pathways to consumers that bypass traditional specialty retail relationships. Companies are developing omnichannel strategies that combine digital marketing with physical showroom experiences to capture evolving consumer preferences for ceramic tile selection and purchasing.

Russia Ceramic Tiles Industry Leaders

Kerama Marazzi

Unitile

Cersanit

Italon

Lasselsberger

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Italon expanded its portfolio with high-performance porcelain stoneware collections aimed at architects and designers working on commercial interiors.

- January 2025: Kerama Marazzi launched its Morocco collection featuring 20 wall-tile series and 16 porcelain stoneware series with large-format options up to 60x119.5 cm for residential and commercial projects.

- July 2024: Ural-based Piastrella announced plans to invest ₽1 billion (approx. USD 11 million) to expand and modernize its ceramic tile and porcelain production facility near Polevskoy.

Russia Ceramic Tiles Market Report Scope

Ceramic tiles are made up of sand, natural products, and clay, and once they are molded into a shape, they are fired in a kiln. Ceramic tiles are durable, resistant to water, moisture, and fire, and are cheap as compared to other flooring products. Russia's ceramic tile market is segmented by product (glazed, porcelain, scratch-free, and other products), application (floor tiles, wall tiles, and other applications), construction type (new construction and replacement renovation), and end-user (residential and commercial).

The report offers market size and forecasts for Russia's ceramic tile market in value (USD) for all the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Volga Federal District |

| Central Federal District |

| Southern Federal District |

| Northwestern Federal District |

| Other Regions |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Volga Federal District | |

| Central Federal District | ||

| Southern Federal District | ||

| Northwestern Federal District | ||

| Other Regions | ||

Key Questions Answered in the Report

What is the forecast value of the Russia ceramic tiles market by 2031?

The Russia ceramic tiles market is projected to reach USD 3.45 billion by 2031.

Which product type currently leads demand in Russia?

Porcelain tiles lead with 46.20% market share owing to superior durability and design versatility.

Why are wall applications growing faster than floor uses?

Architectural trends favor large vertical panels and feature walls, driving a 3.95% CAGR for wall installations.

How do import substitution policies affect tile producers?

Local sourcing of kaolin and feldspar stabilizes costs and reduces exposure to currency volatility, boosting domestic competitiveness.

Which region shows the fastest market growth in Russia?

The Southern Federal District posts the highest 4.60% CAGR through 2031, fueled by transport hubs and industrial expansion.

Page last updated on: