Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.51 Billion |

| Market Size (2031) | USD 5.87 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

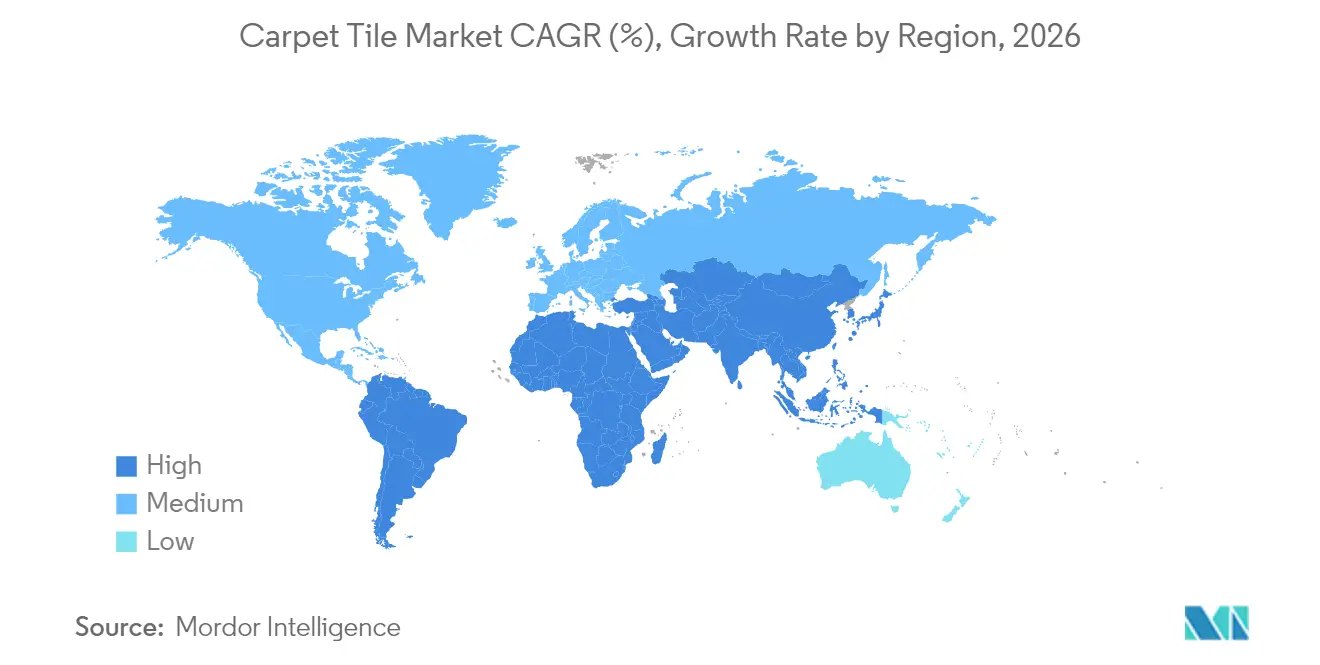

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

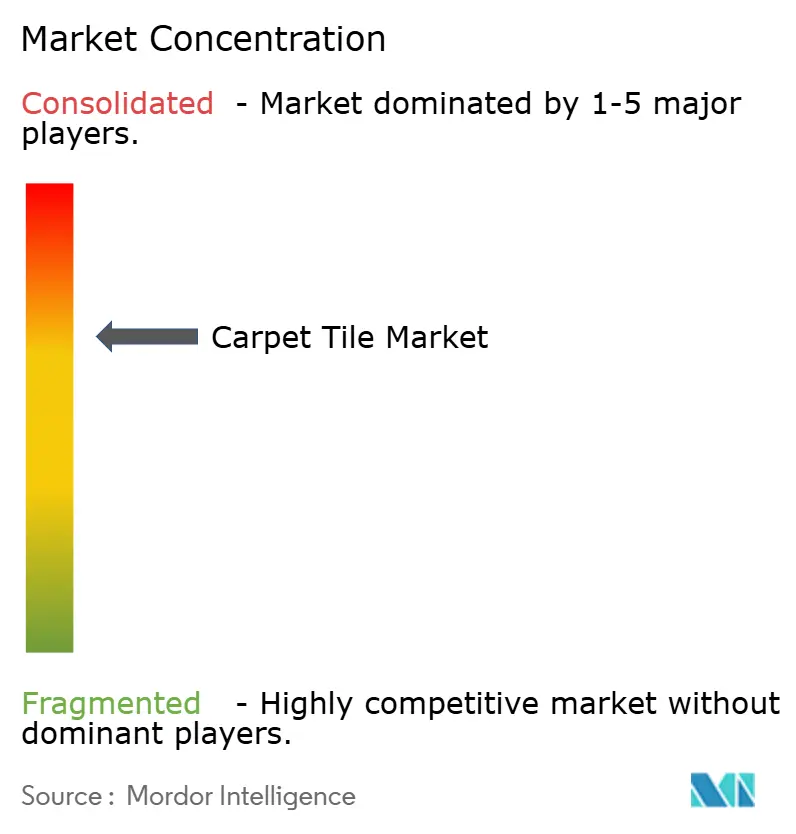

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carpet Tile Market Analysis by Mordor Intelligence

The carpet tile market size is expected to grow from USD 4.28 billion in 2025 to USD 4.51 billion in 2026 and is forecast to reach USD 5.87 billion by 2031 at 5.42% CAGR over 2026-2031. Growth arises from consistent corporate renovation spending, sustainability-driven specification shifts, and rising digital procurement, even as hard-surface flooring intensifies price competition. Carpet tiles now capture roughly 80% of commercial soft-surface specifications, underscoring their total-cost and reconfiguration advantages. [1] Source: Floor Covering Weekly, “Future Forecast,” floorcoveringweekly.com. North America retains the largest regional share, yet Asia-Pacific’s faster build-out of technology hubs and offices propels global demand. Nylon continues as the dominant fiber, though bio-based alternatives expand fastest as ESG mandates become embedded in real-estate procurement. Commercial applications anchor revenues, while peel-and-stick formats open new residential and small-business opportunities.

Key Report Takeaways

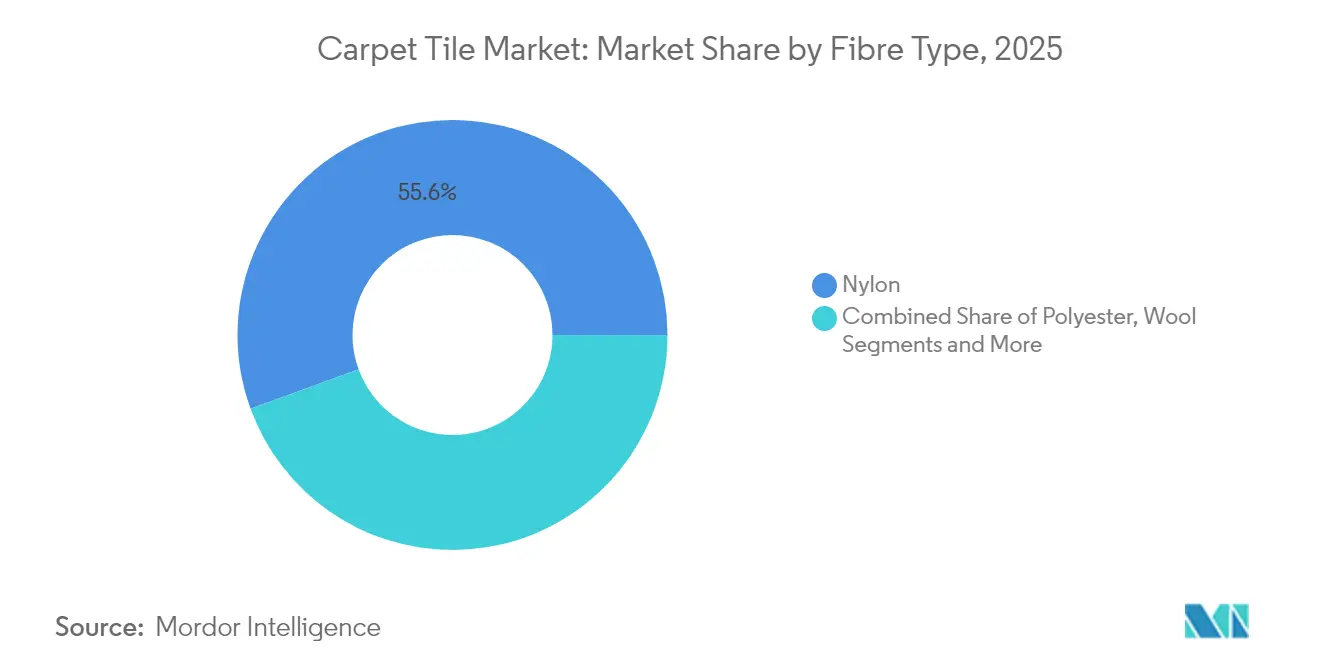

- By material, nylon led with 55.58% of carpet tile market share in 2025; bio-based fibers are projected to advance at a 6.78% CAGR through 2031.

- By end user, commercial installations accounted for 71.62% of the carpet tile market size in 2025, whereas residential demand is expected to increase at a 6.52% CAGR to 2031.

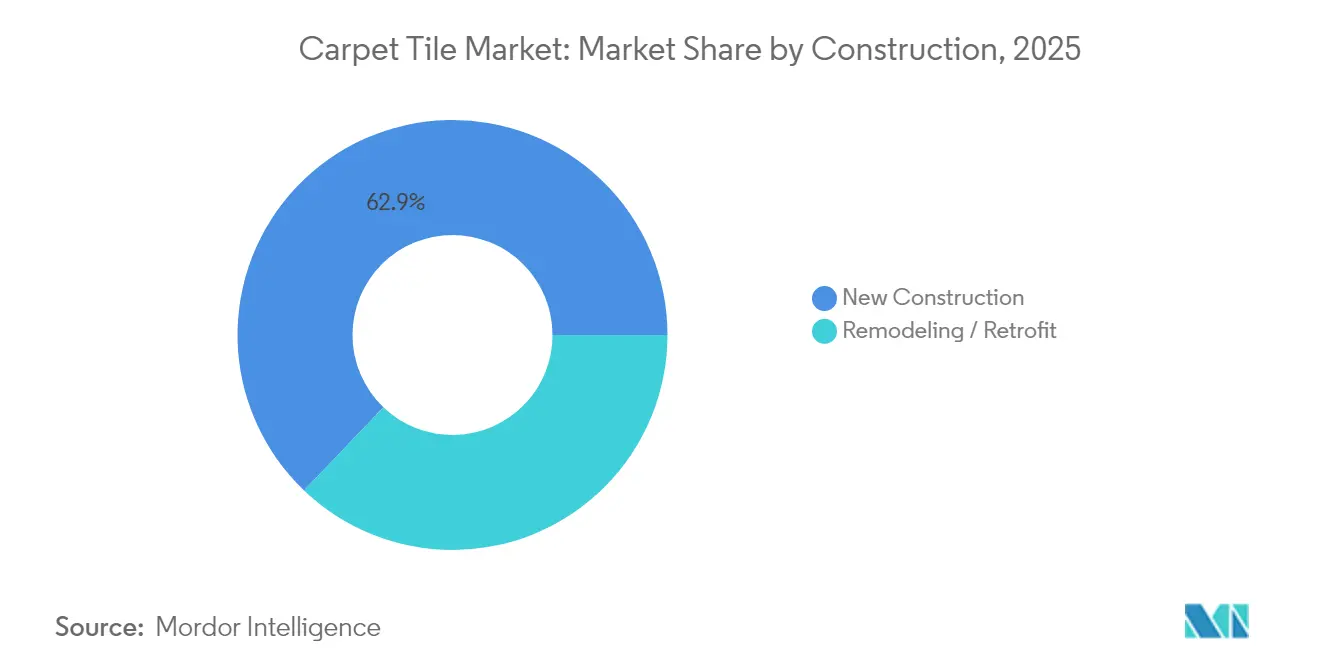

- By construction type, new construction accounted for 62.87% of the carpet tile market size in 2025, whereas remodeling/retrofit demand is expected to increase at a 6.15% CAGR to 2031.

- By distribution channel, direct B2B sales contributed 57.28% share of the carpet tile market size in 2025; online sales represent the fastest-growing channel at a 7.46% CAGR through 2031.

- By geography, North America held 33.62% revenue share in 2025; Asia-Pacific is set to expand at a 7.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Carpet Tile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability-driven specification boom | +1.2% | Global, strongest in North America & EU | Medium term (2-4 years) |

| Commercial renovation cycle rebound | +0.9% | North America & Asia-Pacific | Short term (≤ 2 years) |

| Rapid-install peel-&-stick systems | +0.7% | Global | Short term (≤ 2 years) |

| Cost advantage over broadloom (life-cycle) | +0.8% | Global | Long term (≥ 4 years) |

| Modular office re-configuration demand | +0.6% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Static-control adoption in data centers | +0.4% | Global, concentrated in tech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainability-driven Specification Boom

Corporate ESG targets have moved environmental metrics from nice-to-have to mandatory purchase criteria. Interface’s goal of carbon negativity by 2040 and Shaw’s carbon-neutral commercial production achieved in 2018 illustrate how climate commitments reposition product portfolios. Partnerships such as Tarkett–Mycocycle, which uses mycelia to detoxify construction waste, showcase the push toward regenerative cycles[2]Source: Commercial Tarkett, “Tarkett-Mycocycle Partnership,” commercial.tarkett.com.. Aquafil’s expansion of ECONYL recycled nylon derived from discarded carpet feeds closed-loop manufacturing and reduces dependency on virgin petrochemicals. Architect specifications increasingly reference cradle-to-cradle and embodied-carbon metrics, making recycled or bio-based content a procurement prerequisite. Peel-and-stick systems support waste minimization by eliminating wet adhesives and simplifying end-of-life reclamation.

Commercial Renovation Cycle Rebound

Deferred pandemic projects are resurfacing as occupiers reimagine workplaces for hybrid models. McKinsey notes offices are morphing into tech-enabled collaboration hubs, triggering flooring upgrades to support flexible layouts. CBRE’s 12% revenue increase in Q1-2025 aligns with rising fit-out demand, particularly in healthcare and technology verticals. Interface booked 17% order growth in the Americas and 18% education billings, confirming that renovation dollars translate directly into carpet tile orders[3]Source: Interface, “Q3-2024 Results,” interface.com.. JLL design reports spotlight adaptive reuse, while education facilities deploy stimulus funds to refresh floor coverings. These dynamics reinforce a steady replacement cadence that underpins the carpet tile market.

Rapid-install Peel-&-stick Systems

Installation efficiency has emerged as a critical competitive differentiator, with peel-and-stick systems addressing labor shortages while reducing project timelines. Interface's TacTiles innovation exemplifies this trend, enabling easier installation without traditional adhesives while maintaining performance standards. The labor shortage crisis affecting flooring installation creates urgency around self-adhesive solutions, particularly as contractors struggle to find skilled workers for complex projects. These systems also align with sustainability objectives by eliminating volatile organic compound emissions from wet adhesives and enabling easier end-of-life reclamation. The technology's maturation has overcome early performance concerns, with improved adhesive formulations providing comparable durability to traditional installation methods. Commercial tenants increasingly value the flexibility to reconfigure spaces without professional installation, making peel-and-stick systems attractive for dynamic work environments.

Cost Advantage Over Broadloom in Life-cycle Terms

Total cost of ownership calculations increasingly favor carpet tiles despite higher initial acquisition costs, driven by replacement flexibility and maintenance efficiencies. The ability to replace individual damaged tiles rather than entire installations creates compelling economic arguments, particularly in high-traffic commercial environments where wear patterns vary significantly across floor areas. Maintenance advantages extend beyond replacement to include easier cleaning access and the ability to rotate tiles to distribute wear patterns evenly. The modular approach also reduces waste during renovations, as undamaged tiles can be relocated or repurposed rather than discarded entirely. Insurance considerations further support the life-cycle cost advantage, as localized damage from floods or stains requires minimal replacement compared to broadloom installations. Corporate real estate managers increasingly recognize these operational benefits, with total cost models demonstrating 15-20% savings over typical commercial lease terms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hard-surface (LVT) cannibalisation | -1.4% | Global, strongest in North America | Medium term (2-4 years) |

| Volatile nylon & bitumen prices | -0.8% | Global, manufacturing-intensive areas | Short term (≤ 2 years) |

| Recycling of mixed-fibre backings | -0.3% | EU & California regulatory focus | Long term (≥ 4 years) |

| Acoustic performance limitations in open offices | -0.2% | North America & Europe commercial | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hard-surface (LVT) Cannibalisation

Luxury vinyl tile (LVT) imports surged to an 81% penetration rate, outpacing all other flooring categories in the U.S. and drawing market share away from carpet tiles. In the wake of the pandemic, there's been a heightened emphasis on hygiene, leading to a preference for washable surfaces. Additionally, the rigid-core SPC formats of LVT have addressed previous denting concerns while remaining competitively priced. Designers in retail and hospitality highlight design versatility and a perceived ease of cleaning as key factors in their choices. Carpet tiles, however, emphasize their superior sound absorption, supported by data from the Carpet and Rug Institute, which demonstrates better sound coefficients compared to hard surfaces. Despite this advantage, carpet tiles face increasing challenges from price wars and the localization of LVT supply chains. These factors are putting pressure on the margin resilience of carpet tiles, further intensifying competition in the flooring market.

Volatile Nylon & Bitumen Prices

Nylon accounts for over half of carpet tile fiber volume, making the sector sensitive to petrochemical swings. Ascend Performance Materials’ 2024 bankruptcy amidst nylon 6,6 overcapacity and Chinese imports evidenced systemic vulnerability [4]Source: Chemical & Engineering News, “Ascend Bankruptcy,” cen.acs.org. Bitumen, used for backings, mirrors the undulations of oil prices, posing a significant procurement risk for projects with fixed bids. While manufacturers turn to multi-fiber platforms and recycled materials as a hedge, the associated R&D investments, coupled with the need for customer validation, extend the adoption cycles, making it a long-term endeavor. Additionally, short-term budgeting uncertainty can delay large-capex flooring decisions, further softening near-term order flows and impacting overall market stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Type: Bio-based Innovation Challenges Nylon Dominance

Bio-based fibers emerge as the fastest-growing segment at 6.78% CAGR through 2031, despite nylon maintaining 55.58% market share in 2025. This growth acceleration reflects corporate sustainability mandates and green building certification requirements that prioritize renewable material content. Polyester (PET) segments benefit from recycling infrastructure development, with Mohawk's EcoFlex ONE incorporating 76% recycled content and achieving 64% embodied carbon reduction compared to traditional options. Polypropylene applications expand in moisture-sensitive environments, while wool segments maintain premium positioning in hospitality applications despite higher costs.

Research into wool/PA56 blended yarns demonstrates enhanced moisture absorption and biodegradability characteristics, suggesting bio-based alternatives can match traditional fiber performance while reducing environmental impact. Nylon's market leadership faces pressure from volatile petroleum-based raw material costs and sustainability requirements, though superior durability and stain resistance maintain specification preference in high-traffic commercial applications. The fiber type segmentation increasingly reflects end-user sustainability priorities rather than pure performance considerations, with bio-based options gaining traction despite premium pricing.

By End User: Residential Acceleration Contradicts Industry Trends

Commercial applications command 71.62% market share in 2025, yet residential segments drive growth momentum at 6.52% CAGR through 2031, contradicting broader soft surface flooring decline patterns. This residential acceleration stems from multifamily development adoption and DIY installation capabilities that differentiate carpet tiles from traditional broadloom products. Healthcare facilities represent a key commercial growth driver, with lifecycle cost analysis demonstrating modular carpet tiles provide superior financial value over 50-year service periods compared to hard surface alternatives. Education segments show particular strength, with Interface reporting 13% global billing growth in 2024 as deferred renovation projects materialize.

Hospitality applications benefit from Milliken's Modular Landscapes system, which delivers 25% cost savings compared to broadloom through simplified installation and selective replacement capabilities. Corporate offices increasingly specify carpet tiles for acoustic performance and employee wellness considerations, with Tarkett's DESSO SoundMaster achieving +8 dB impact sound insulation improvement.

By Construction Type: Retrofit Market Gains Momentum

New construction projects capture 62.87% of installation volume in 2025, while remodeling applications grow faster at 6.15% CAGR through 2031, reflecting deferred renovation cycles and workspace adaptation requirements. This retrofit acceleration benefits carpet tile manufacturers as modular systems reduce installation disruption compared to broadloom alternatives that require complete floor replacement. Commercial renovation projects increasingly prioritize rapid installation systems that minimize business interruption, with peel-and-stick technologies enabling overnight installation in occupied buildings.

The construction type segmentation reflects broader economic patterns, with new construction moderating from 20% growth in 2023 to 4% in 2024 according to American Institute of Architects forecasts. Retrofit applications benefit from carpet tiles' selective replacement capabilities, enabling facility managers to refresh high-traffic areas without disrupting entire floor systems. This advantage becomes particularly valuable in healthcare and education environments where operational continuity requirements limit renovation windows.

By Distribution Channel: Retail Expansion Signals Market Evolution

Direct B2B sales maintain 57.28% market share in 2025, reflecting commercial market dominance, yet retail consumer channels expand rapidly at 7.46% CAGR through 2031, indicating residential market penetration acceleration. This channel evolution suggests carpet tiles are transitioning from purely commercial products to consumer-accessible solutions, driven by DIY installation capabilities and home center availability. Online distribution gains particular momentum as consumers research modular flooring options and compare lifecycle costs against traditional alternatives.

The B2C expansion reflects broader trends toward modular home improvement solutions that enable incremental renovation and design flexibility. This distribution channel diversification reduces manufacturer dependency on commercial construction cycles while creating new growth opportunities in residential renovation markets.

Geography Analysis

North America maintains leads the market with dominating share in 2025, driven by commercial renovation recovery and sustainability specification requirements, though growth moderates to 4.82% CAGR through 2031 as market maturity constrains expansion. The region benefits from domestic manufacturing capabilities that provide competitive advantages against tariff-affected imports, with companies like Shaw Industries expanding production capacity in Georgia to serve growing demand. U.S. General Services Administration P100 standards mandate performance-based requirements for federal buildings, creating specification stability for carpet tile manufacturers serving government segments. Canada and Mexico contribute to regional growth through construction activity recovery, though housing market softness constrains residential applications.

Asia-Pacific emerges as the fastest-growing region through 2031, led by commercial construction expansion in India and China's urbanization trends. India accounts for over half of regional office space demand, with technology hubs like Bengaluru and Hyderabad driving specification activity. China's market development benefits from domestic manufacturing capabilities and growing corporate sustainability awareness, though regulatory complexity creates specification challenges for international manufacturers. Southeast Asian markets including Vietnam and Thailand contribute to regional growth through foreign direct investment and manufacturing facility expansion. Japan and Australia maintain steady demand patterns, with emphasis on acoustic performance and design flexibility in commercial applications.

Europe demonstrates moderate growth patterns constrained by economic uncertainty and regulatory compliance requirements, with the EU's Ecodesign for Sustainable Products Regulation creating both opportunities and challenges for carpet tile manufacturers. Tarkett achieved EcoVadis Platinum rating, ranking in the top 1% of assessed companies, demonstrating how sustainability leadership creates competitive advantages in European markets. The region's focus on circular economy principles drives demand for recyclable carpet tile systems, with DESSO SoundMaster products featuring 80% recycled content and Cradle to Cradle certification. South America and Middle East/Africa regions contribute modest growth, with Brazil and UAE leading through commercial development projects and hospitality sector expansion.

Competitive Landscape

The carpet tile market is shaped by a handful of dominant players, reflecting a high level of consolidation. While major vendors hold significant influence, the landscape still offers room for emerging brands to innovate and capture specialized segments. Interface leads the pack, setting itself apart with a strong focus on sustainability, particularly through its carbon-negative product offerings, which appeal to environmentally driven clients and green building initiatives. The company’s commitment to reducing its environmental footprint has positioned it as a leader in the market, attracting customers who prioritize eco-friendly solutions.

Shaw follows as a close competitor, leveraging its scale and vertically integrated operations to ensure cost control, product consistency, and market breadth. By maintaining a robust supply chain and focusing on operational efficiency, Shaw has been able to strengthen its market presence and compete effectively. Mohawk advances eco-backing platforms such as EcoFlex ONE, which achieves a 64% reduction in embodied carbon, further solidifying its commitment to sustainability. This innovation underscores Mohawk’s dedication to addressing environmental concerns while meeting customer demands for sustainable products. Tarkett and Milliken round out leading positions through their design depth and expertise in ESD (electrostatic discharge) solutions, which cater to specific industry needs and enhance their competitive edge.

Strategic themes center on end-of-life take-back programs, the use of recycled content, and digitized customer engagement strategies. These initiatives reflect the industry’s focus on sustainability and customer-centric innovation. Capital investment focuses on expanding domestic manufacturing capabilities to mitigate tariff risks and enhance service responsiveness. By prioritizing local production, companies aim to reduce lead times and improve their ability to meet market demands efficiently. Emerging opportunities for market expansion include data-center ESD solutions, healthcare antimicrobial coatings, and bio-polymer fibers. These areas represent significant growth potential as they align with evolving customer needs and industry trends. Consolidation is likely to increase as medium-tier manufacturers pursue scale economies, mirroring moves like Lowe’s entry into professional installation networks. The carpet tile market, therefore, balances entrenched incumbency with innovation-led disruption, creating a dynamic environment for growth and competition. This balance between established players and new entrants fosters a competitive landscape that encourages continuous improvement and adaptation.

Carpet Tile Industry Leaders

Interface Inc.

Shaw Industries Group Inc.

Tarkett S.A.

Mohawk Industries Inc.

Milliken & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Lowe's Companies acquired Artisan Design Group for USD 1.325 billion, adding 3,200 installers across 18 states to strengthen Pro flooring services.

- April 2025: Lowe's Companies acquired Artisan Design Group for USD 1.325 billion, adding 3,200 installers across 18 states to strengthen Pro flooring services.

- November 2024: Interface launched segment-specific carpet tile collections for offices, healthcare, and education.

- June 2024: Tarkett teams up with Mycocycle to use mushroom mycelia in recycling old flooring via its ReStart program, aiming to detoxify construction waste and create biobased raw materials pioneering circular economy innovation.

Global Carpet Tile Market Report Scope

Carpet tiles, also known as modular carpets or square carpets, are squares cut from wall-to-wall rolls that can be fitted together to make up a carpet. Carpet tiles are justly popular as a flooring option for commercial environments, such as bars and restaurants, and other relatively uncomplicated projects. A complete background analysis of the global carpet tile market, which includes an assessment of the emerging trends by segments and regional markets, significant changes in market dynamics, and a market overview, is covered in the report. The market is segmented by product type into square and rectangle, by end-user into residential and commercial, by distribution channel into offline stores and online stores, and by geography into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report offers market size and forecasts by value (USD) for all the above segments.

By Fiber Type

| Nylon |

| Polyester (PET) |

| Polypropylene |

| Wool |

| Bio-based Fibres |

| Other Fiber Types |

By End User

| Residential | |

| Commercial | Hospitality & Leisure |

| Retail & Shopping Centers | |

| Healthcare Facilities | |

| Education | |

| Corporate Offices | |

| Public & Government Buildings | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Remodeling / Retrofit |

By Distribution Channel

| B2C/Retail Consumers | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Other Distribution Channels | |

| B2B/Contractors/Builders |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Fiber Type | Nylon | |

| Polyester (PET) | ||

| Polypropylene | ||

| Wool | ||

| Bio-based Fibres | ||

| Other Fiber Types | ||

| By End User | Residential | |

| Commercial | Hospitality & Leisure | |

| Retail & Shopping Centers | ||

| Healthcare Facilities | ||

| Education | ||

| Corporate Offices | ||

| Public & Government Buildings | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Remodeling / Retrofit | ||

| By Distribution Channel | B2C/Retail Consumers | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Contractors/Builders | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the carpet tile market?

The carpet tile market size is valued at USD 4.51 billion in 2026.

Which region is expanding fastest for carpet tiles?

Asia-Pacific leads growth with an 7.08% CAGR through 2031 driven by new office construction.

Which is the fastest growing region in Global Carpet Tile Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which fiber type dominates carpet tile production?

Nylon remains dominant, accounting for 55.58% of 2025 volume.

How quickly are B2C/Retail Consumers channel growing in carpet tile sales?

B2C/Retail Consumers distribution is rising at a 7.46% CAGR driven by design trends and increased home renovations.

What share do commercial applications hold in carpet tiles?

Commercial installations contribute 71.62% of 2025 revenue owing to office, healthcare, and education demand.

Page last updated on: